19

LNG AS A KEY DRIVER FOR MALAYSIA AND REGIONAL MARKETS – CHALLENGES AND PROSPECTS By Datuk Ir. Ahmad Fauzi Hasan Energy Commission

LNG AS A KEY DRIVER FOR MALAYSIA AND REGIONAL MARKETS

– CHALLENGES AND PROSPECTS

By

Datuk Ir. Ahmad Fauzi Hasan

Energy Commission

Source: Draft - National Energy Balance 2011

2

Final Use of Commercial Energy

Source: Draft - National Energy Balance 2011

3

Commercial Energy Supply

Indigenous Gas

1600mmscfd

(71%)

PM3 CAA

50mmscfd

(2%)

West Natuna ‘B’

250mmscfd

(11%)

Joint Development

Area (JDA)

350mmscfd

(16%)

Gas

Processing

Plant (GPP)

PGU System

Power Sector

1100mmscfd

(49%)

Non-Power

Sector

Export

200mmscfd

(9%)

PETRONAS

Customers

590mmscfd

(26%)

Gas Malaysia Bhd

360mmscfd

(16%)

Peninsular Malaysia Gas Value Chain

Peninsula Natural Gas Pricing Situation

May 1997 – June 2008:

October 2002:

June 2008:

March 2009:

June 2011:

Electricity Generation Fuel Mix:

From Oil to Gas and Coal Dependency

46%

45%

4%

5%

0

50

100

150

200

250

300

350

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

60.2 63.9 62.4 68.4

77.6

126.2

186.9

252.39

277.55 291.26

280.01

306.87

325.19 332.37

Nat

ura

l Gas

Co

nsu

mp

tio

n ,

mm

scfd

Year

Gas Consumption Via the Natural Gas Distribution System

200

400

600

800

1,000

1,200

1,400

1,600

1-Jan 1-Feb 1-Mar 1-Apr 1-May 1-Jun 1-Jul 1-Aug 1-Sep 1-Oct 1-Nov 1-Dec

2009 2010 2011 2012

Date

GAS NOMINATION FOR 2009, 2010, 2011 & 2012

Gas volume supplied in 2012 decreased by 10.12% compared to 2009 but electricity

generation increased by 12.65% from 94,748 GWh to 108,473 GWh.

Year 2009 2010 2011 2012 Unit

Average (daily) 1,224 1,139 1,050 1,100 mmscfd

Maximum (daily) 1,398 1,270 1,288 1,261 mmscfd

Minimum (daily) 700 750 833 822 mmscfd

Total 446,639 415,682 383,356 401,404 mmscf

8

The Gas Supply Challenge

Global Natural Gas Pricing Situation

10

Peak Demand *(MW)

15,072 17,671 20,847 24,770

Energy Generated (GWh)

100,991 118,420 140,613 169,250

*Peninsula Malaysia

0%

20%

40%

60%

80%

100%

2010 2015 2020 2030

5% 4% 4% 4%

58% 53%

35% 28%

37%

39%

53%

43%

9%

5%

5% 8% 10%

Hydro Gas Coal Nuclear Interconnection RE

Towards A More Diversified And Affordable Fuel Mix

0

500

1000

1500

2000

2500

3000

2013 2016 2019 2022 2025

mm

scfd

Domestic Gas Supply*

Forecasted Gas Demand**

Gas shortfall to be addressed by importing LNG

* Includes JDA, Natuna and PM3

** Demand growth projected for power and non-power sectors

Domestic gas supply is not

able to support additional

gas demand

Peninsula Gas Supply and Demand Projection

The Gas Supply Challenges

• Depleting domestic productions due to high decline rates

• Technically and commercially challenging new fields

• Rapid demand growth has led to over-stretching of the supply

system

• Reduced reliability of ageing upstream facilities has led to frequent

supply interruptions and shortfalls

• Increasingly dependent on gas supplies from other pipeline gas

sources such as Joint Development Area (JDA) (Thailand),

West Natuna (Indonesia) and PM3 (Vietnam)

• LNG imports are required to address supply shortfall and increasing

demand

Melaka

Kuantan

Segamat

Jerneh

(1992)

Kuala Lumpur

Lawit (1997)

Bekok

THAILAND

JDA

(2005)

PM-3

(2003)

Angsi (2002)

SONGKHLA

Bintang

(2003)

Resak (2000)

KERTIH

Duyong (1984)

Kangar

West Natuna ‘B’

(Indonesia - 2002)

SOURCE: PETRONAS

13

Boosting Gas Supply to the Peninsula for Local

Consumption

14

Bintulu

Kimanis

Sabah Sarawak gas pipeline (under construction)

Sepangar Bay Kota Kinabalu

ERB WEST

SEMARANG

Patricia

Mahkota

E11, E13, F13

Helang

Congkak

Golok

Labuan

Betty Miri Crude Oil Terminal

Miri

SOURCE: PGB

RGT Lahad Datu

(2016)

SOGT

SAMUR

Boosting Gas Supply to Sabah and Sarawak for Local

Consumption and Export

APEC’s Technically Recoverable Conventional and Unconventional Gas Resource Base, in MToe

Economy Conventional

Gas

Unconventional Gas

Conventional &

Unconventional Gas

2009

Production

Years of

Production Shale Gas

Coal Bed

Methane Tight Gas Total

China 5 225 22 150 9 625 na 31 775 37 000 76.7 482

US 30 750 14 475 3 500 13 000 30 975 61 725 532.7 116

Australia 5 700 9 950 10 975 500 21 425 27 125 38.1 712

Canada 8 650 2 250 1 125 4 250 7 625 16 275 147.6 110

Mexico 2 375 7 425 100 na 7 525 9 900 49.1 202

Russia 86 125 1 825 50 na 1 875 88 000 474.9 185

Source: APERC

Abundant Future Natural Gas Resources In APEC

100%

80%

60%

40%

20%

0%

20%

40%

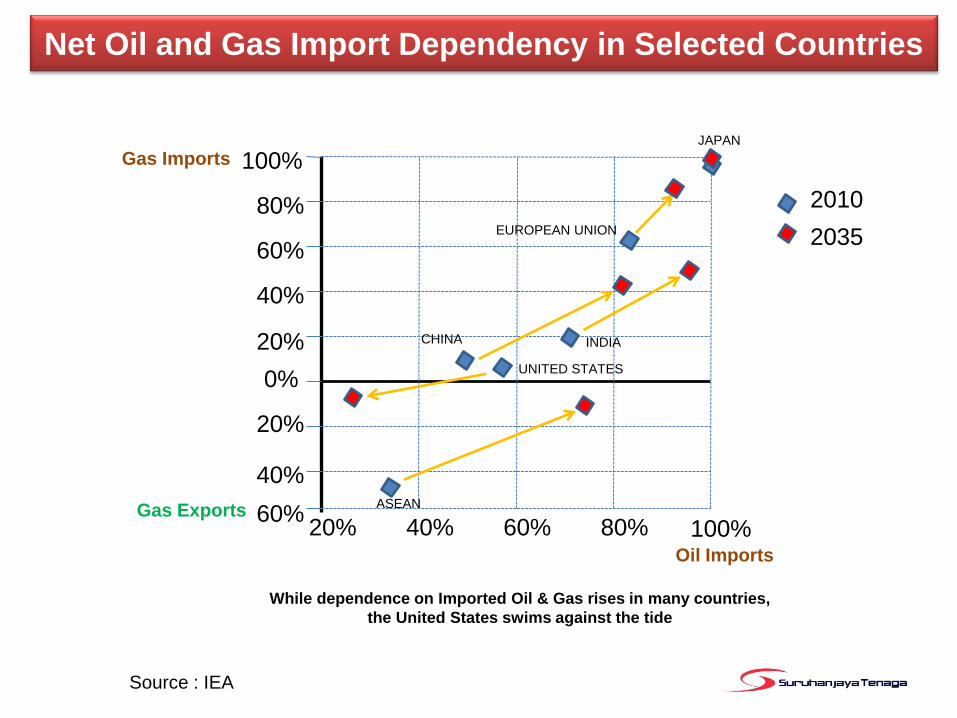

60% 20% 40% 60% 80% 100%

ASEAN

CHINA

UNITED STATES

INDIA

EUROPEAN UNION

JAPAN

Gas Exports

Oil Imports

While dependence on Imported Oil & Gas rises in many countries,

the United States swims against the tide

Gas Imports

2010

2035

Net Oil and Gas Import Dependency in Selected Countries

Source : IEA

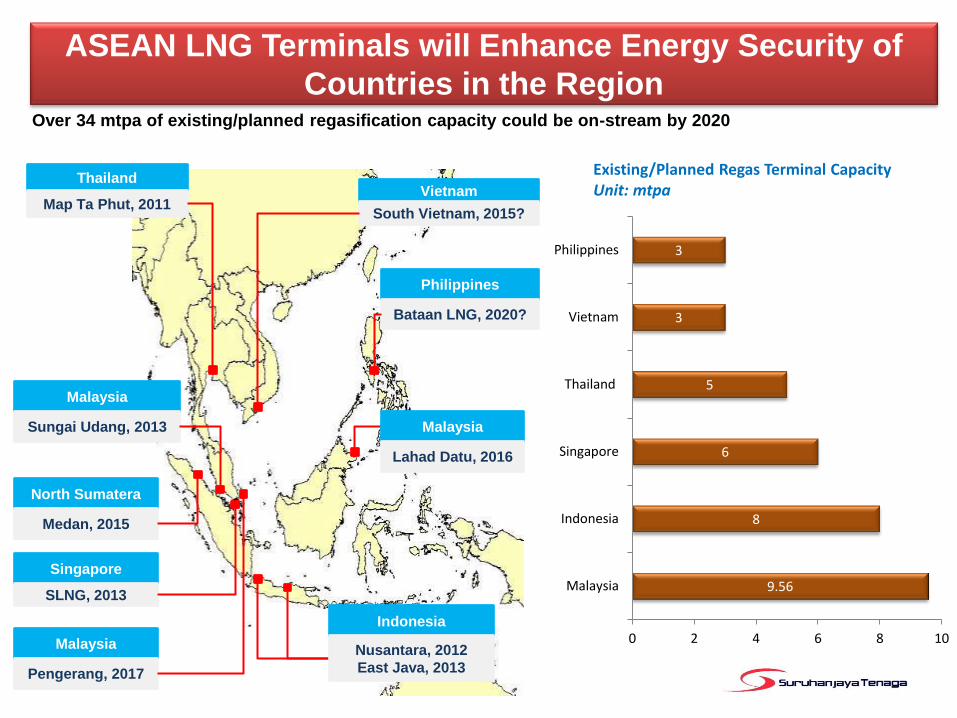

Over 34 mtpa of existing/planned regasification capacity could be on-stream by 2020

Thailand

Map Ta Phut, 2011 Vietnam

South Vietnam, 2015?

Malaysia

Sungai Udang, 2013

Philippines

Bataan LNG, 2020?

Indonesia

Nusantara, 2012

East Java, 2013

North Sumatera

Medan, 2015

Singapore

SLNG, 2013

Malaysia

Lahad Datu, 2016

Malaysia

Pengerang, 2017

Existing/Planned Regas Terminal Capacity Unit: mtpa

9.56

8

6

5

3

3

0 2 4 6 8 10

Malaysia

Indonesia

Singapore

Thailand

Vietnam

Philippines

ASEAN LNG Terminals will Enhance Energy Security of

Countries in the Region

• PETRONAS is intensifying exploration, recovery enhancement from depleted

fields and marginal fields development

• PETRONAS is developing LNG Regasification Terminals (RGTs) at :

• Sungai Udang, Melaka (2013)

• Lahad Datu, Sabah (2016)

• Pengerang, Johor (2016)

• RGT facilities plus transmission and distribution system will be made accessible to

third party gas and utility companies to import and deliver gas to consumers.

• Government is moving towards market-based gas pricing with discounts for local

consumptions

• Power sector is moving towards a more diversified and balanced fuel mix

• Government is planning the national strategic gas reserve

• Unconventional gas developments in APEC and increasing LNG regasification

capacity in ASEAN will enhance overall future supply security in the region

Positive Developments In Meeting Gas Supply Challenges

Thank You