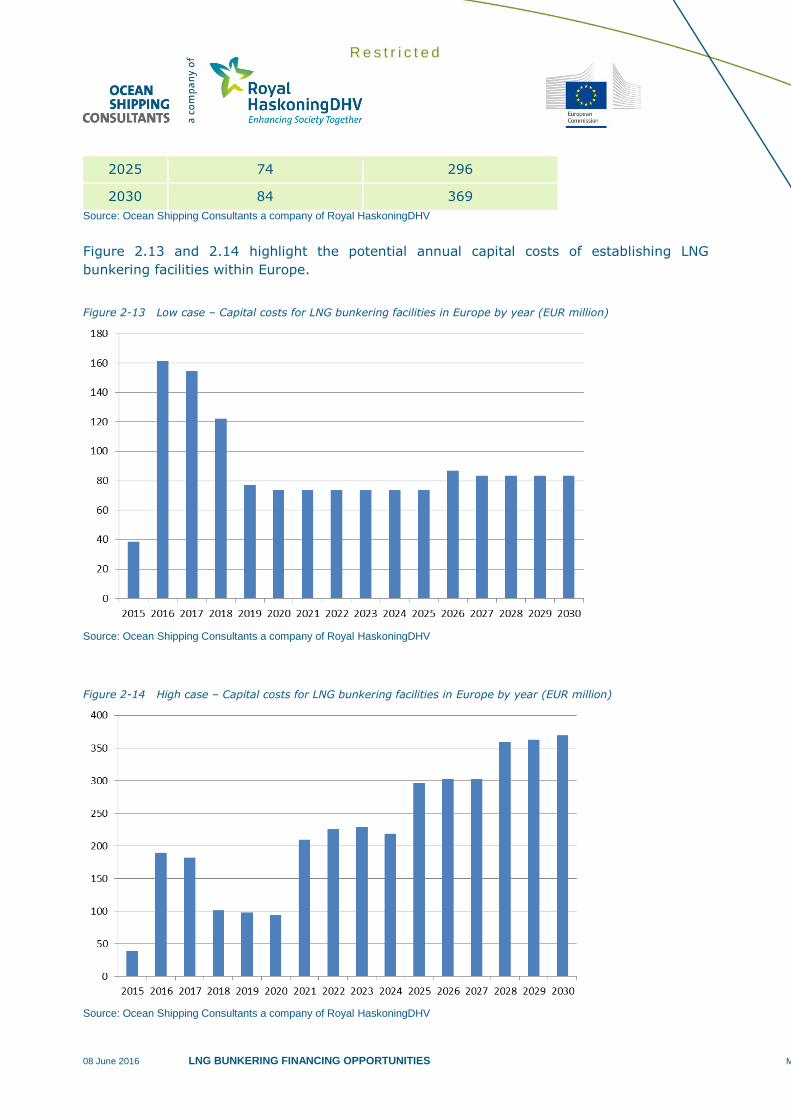

Report LNG bunkering financing opportunities Explore financing opportunities, assess and develop financial mechanisms beyond the EU financial framework aiming at supporting the deployment of marine LNG technology Client: European Commission Reference: M&WPB3039-103-100R001D11 Revision: 11/Final Date: 08 June 2016

Transcript

Report

LNG bunkering financing

opportunities

Explore financing opportunities, assess and develop

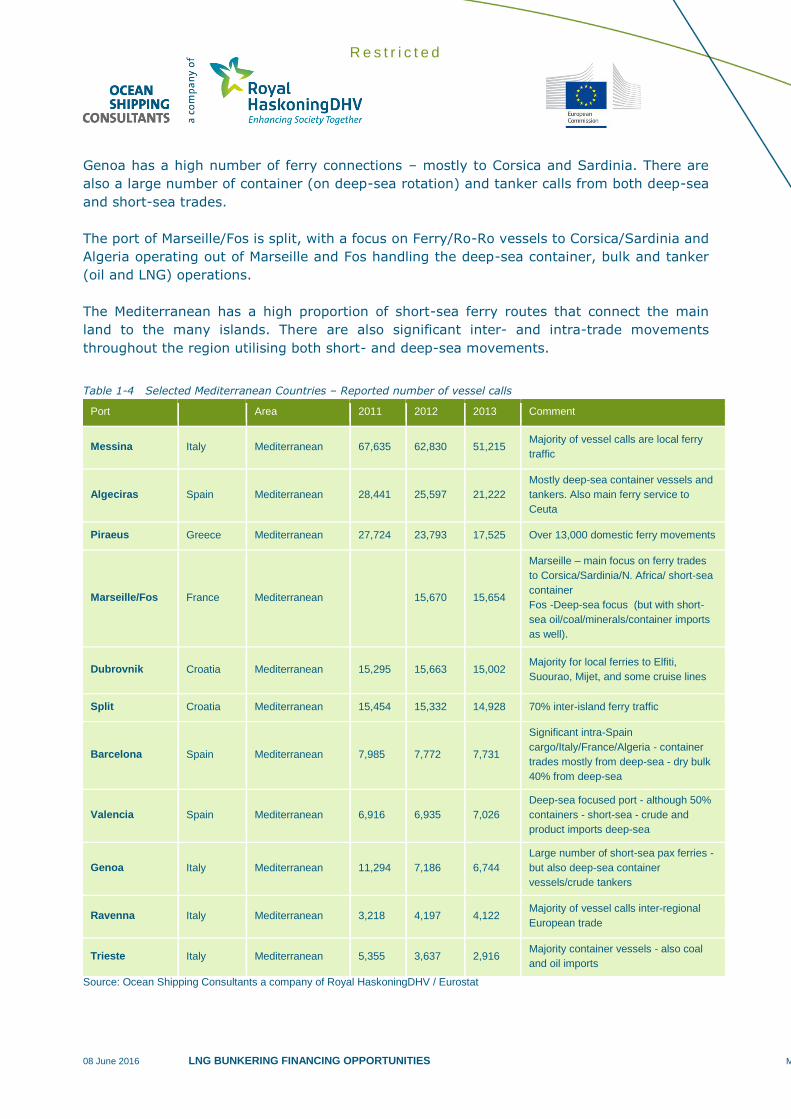

Source: Ocean Shipping Consultants a company of Royal HaskoningDHV / Eurostat

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

26

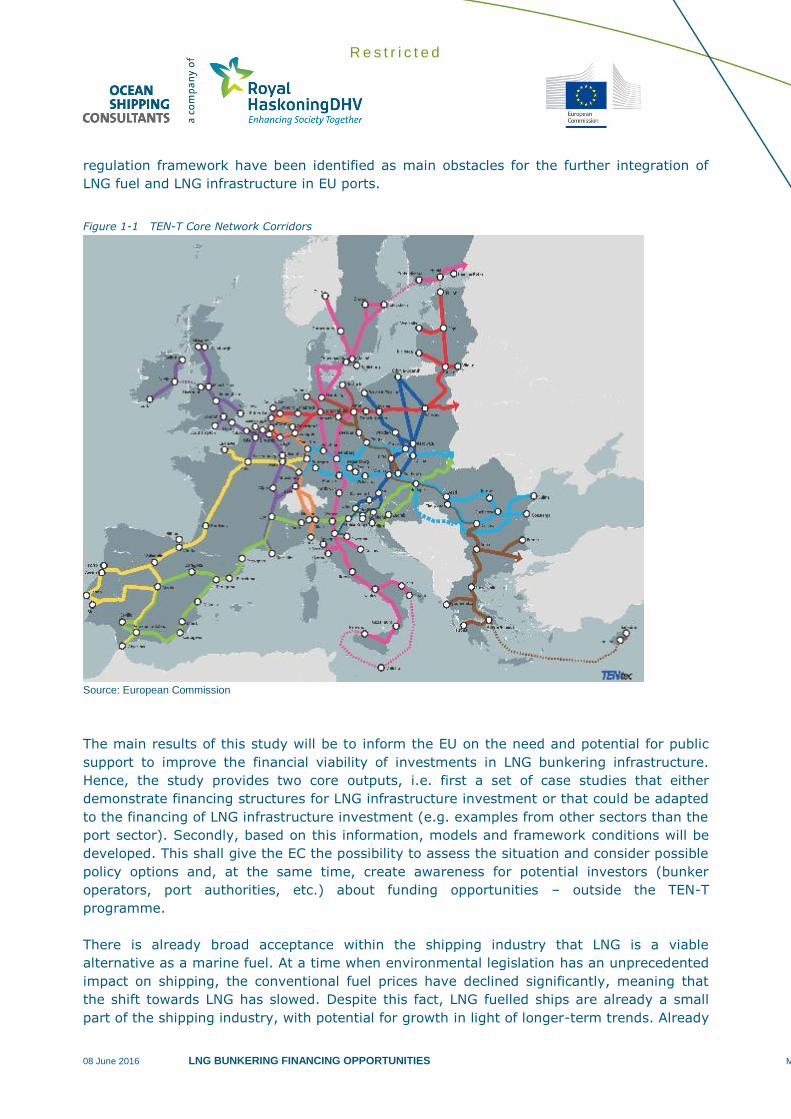

To highlight the scale and the numbers of vessels operating in European waters, Appendix A

uses a vessel tracking platform that highlights the number of vessels recorded on a single

days (February 13th 2015) for the North Sea, Baltic and Mediterranean. The sectors

highlighted are:

Container vessels

Dry bulk carriers

Crude/product tankers

Passenger Ferries/Cruise vessels

Chemical carriers

LNG/LPG carriers

General cargo vessels

RO-RO

Car carriers

Offshore

It should be noted that the vessel information provides an overview of vessels operating in

the region on a particular day. This is a representative snap shot of the number of vessels

operating in European waters. This investigation into the number of vessels operating in

European waters showed that there were approximately 8,000 vessels.

Appendix A highlights the number of vessels in each area by sector. Within each sector

vessels that are moving, at anchor, moored or not moving are represented. This also

includes in-land vessels.

1.3 LNG as a bunker fuel

LNG as a bunker fuel has significant potential to alter the configuration of the existing vessel

fuel market. LNG is seen as a more environmentally friendly fuel than heavy and distillate

fuels. As such it can be used as one of the possible solutions to enable shipowners to

become environmentally compliant in Emission Control Areas (ECAs). However, it is

understood that the financial viability of LNG as a fuel needs to be considered and

investigated to ensure that its uptake is economical for both the vessel and its owner.

Developments in the past decade on the production of unconventional gas, particularly in the

United States, have created a boost in supply of natural gas. At the same time, gas demand

in other sectors (most notably power generation and industry) has been relatively low in

many parts of the world due to the economic recession. These developments have had a

major impact on regional price levels, trade movements and the supply/demand balance.

The past decade has also seen a continuing growth of the share of LNG in the supply of

natural gas. New liquefaction plants and regasification plants continue to come online,

adding to the overall strong development of the global LNG market.

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

27

In addition to the abundant supply of gas, increased environmental awareness of ship-based

emissions has encouraged discussion and implementation of Emission Control Areas (ECAs),

where a specific stepwise approach to SOx emission reductions has been adopted. In this

context LNG as an alternative fuel for shipping has lower emissions of sulphur, NOX and PM

as well as other advantages when compared to vessels fitted with other abatement

technologies. The business cases for retrofits and newbuilds are very different however, with

a shipowner often led to choose between abatement methods as a function not only of

technical/operational factors but also remarkably on the basis of payback time calculations.

With the above into account, demand for LNG as a bunker fuel is forecast to increase

throughout the next decade and beyond. The following section highlights some of the main

vessel sectors that will benefit from LNG as a bunker fuel and examines the potential

number of LNG-fuelled vessels through to 2030.

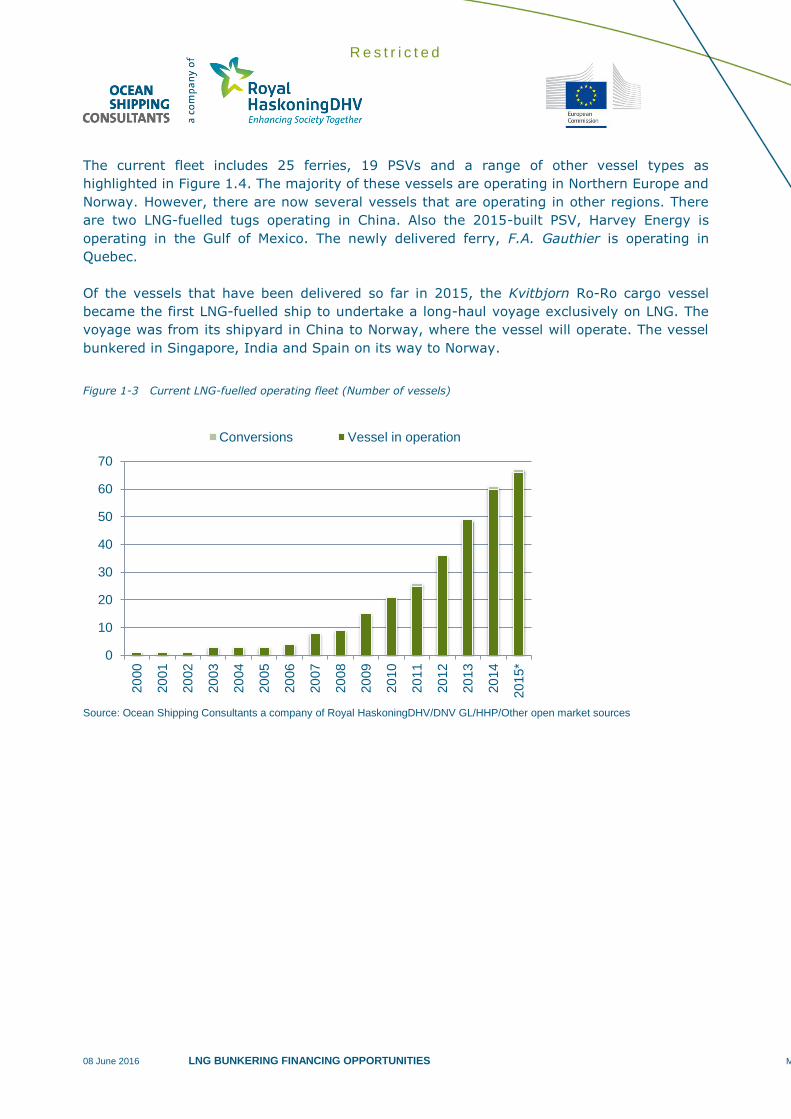

Current Operating LNG-Fuelled Fleet

The current global fleet operating on LNG-bunkers amounts to 102 vessels (as of end-2015),

as shown in Figure 1.3. The fleet consists of the first vessel to utilise LNG as a fuel, the

2000-built ferry Glutra, to the recently delivered PSV, Stril Barents. The fleet also includes

seven inland barges that are operating in Northern Europe and three vessels that have been

converted to operate on LNG.

Figure 1.1 Glutra – 2000-built LNG-fuelled ferry

Figure 1.2 Stril Barents – 2015-built PSV

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

28

The current fleet includes 25 ferries, 19 PSVs and a range of other vessel types as

highlighted in Figure 1.4. The majority of these vessels are operating in Northern Europe and

Norway. However, there are now several vessels that are operating in other regions. There

are two LNG-fuelled tugs operating in China. Also the 2015-built PSV, Harvey Energy is

operating in the Gulf of Mexico. The newly delivered ferry, F.A. Gauthier is operating in

Quebec.

Of the vessels that have been delivered so far in 2015, the Kvitbjorn Ro-Ro cargo vessel

became the first LNG-fuelled ship to undertake a long-haul voyage exclusively on LNG. The

voyage was from its shipyard in China to Norway, where the vessel will operate. The vessel

bunkered in Singapore, India and Spain on its way to Norway.

Figure 1-3 Current LNG-fuelled operating fleet (Number of vessels)

Source: Ocean Shipping Consultants a company of Royal HaskoningDHV/DNV GL/HHP/Other open market sources

0

10

20

30

40

50

60

70

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15*

Conversions Vessel in operation

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

29

Figure 1-4 Current LNG-fuelled operating fleet – vessel type (Number of vessels)

Source: Ocean Shipping Consultants a company of Royal HaskoningDHV/DNV GL/HHP/Other open market sources

The current LNG-Fuelled Orderbook

The current orderbook for LNG-fuelled vessels contains approximately 160 units. There are

over 86 vessels scheduled to be delivered during the remainder 2016, with a further 33

vessels during 2017, as shown in Figure 1.5.

Of the current orderbook, over 30 vessels are container ships, as highlighted in Figure 1.6.

The largest order is for six container ships from UASC, of which five will by 15,000 TEU and

one will be 18,000 TEU. These vessels will be ‘LNG Ready’, meaning that they will need an

up-grade in the future to utilise LNG. These vessels have been ordered to eventually operate

on LNG, when there is sufficient LNG-bunkering infrastructure in place. MOL have also

ordered six 20,000 TEU container vessels, these vessels will also be ‘LNG ready’.

There are 20 product tankers on order. Of these Crowley Maritime have ordered six. These

tankers will be ‘LNG ready’ – and will have the fuel tanks mounted on deck.

There are 21 ferries on order. These newbuilds have a diverse range of propulsion systems –

ranging from pure LNG operations to dual-fuel, through to hybrid systems that utilise LNG

and battery propulsion.

There are 11 bunker vessels currently on order. These vessels have been ordered by Shell,

Mitsubishi/GDF Suez/NYK, Veka Deen LNG and Anthony Veder. The bunker vessels range

from 2,250-6,500m3

0

5

10

15

20

25

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

30

Figure 1-5 Current LNG-fuelled orderbook – by year of delivery (Number of vessels)

Source: Ocean Shipping Consultants a company of Royal HaskoningDHV/DNV GL/HHP/Other open market sources

Figure 1-6 Current LNG-fuelled orderbook – by vessel type (Number of vessels)

Source: Ocean Shipping Consultants a company of Royal HaskoningDHV/DNV GL/HHP/Other open market sources

0

10

20

30

40

50

60

70

80

90

100

2016 2017 2018 2019 2020 2021

0

5

10

15

20

25

30

Conta

iner

Ferr

y

Pro

duct

Tanker

Inla

nd b

arg

e

LN

G B

unker

vessel

Gas C

arr

ier

Pro

d t

anker

PSV

Cru

ise

Pro

d/c

hem

Dre

dger

LEG

carr

ier

RO

PAX

RO

-RO

Tug

Bitum

en t

anker

ConR

o

Gen.

Carg

o

PCTC

Cable

layer

Coasta

l gas c

arr

ier

Energ

y B

arg

e

Ice B

reaker

LN

G c

arr

ier

Sem

i-subm

esib

le…

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

31

Vessel Conversions

There are only a few vessels that are either undergoing conversion or are scheduled to be

converted to operate on LNG. Tote, an American vessel owner, was the first to announce

that they would convert two ferries, the Midnight Sun and the North Star.

1.4 Future LNG-fuelled fleet

The current fleet of LNG-fuelled vessels is concentrated in niche or high-specification sectors,

such as offshore support vessels, ferries and Ro-Ro vessels. As mentioned previously, the

current newbuilds orderbook highlights that, in the longer-term, a wider range of vessel

types will be constructed, or converted, for the use of LNG as bunker fuel.

Short-sea vessels that spend the majority of their operating time in ECAs (and future ECAs)

are ideally placed to take advantage of LNG as a bunker fuel. In addition, the developing

bunkering market is forecast to enable larger long-haul vessels to utilise LNG as a fuel.

The North Sea and Baltic Sea already have a number of vessels that use LNG as a fuel. The

majority of these vessels operate on short-sea voyages. These include:

Glutra -2000-built ferry

Stril Pioneer – 2003-built PSV

Bergensfjord – 2006-built ferry

Korsfjord – 2011-built ferry

Viking Princess – 2012-built PSV

Viking Grace – 2013-built cruise ferry

Bergenfjord – 2014-built cruise ferry

Stril Barents – 2015-built PSV

Each of the main shipping sectors is considered in terms of their potential for future LNG-

fuelled vessels. Each of the vessel sectors has different operational profiles – which will

determine their applicability as an LNG-fuelled vessel. In addition, other factors are also

important, such as environmental compliance and fuel prices. It should be noted that the

life-cycle economics of a given ship design will never be replaced by only looking at the

operational profile aspects. Construction and maintenance costs also play an important role

when making the decision for an LNG-fuelled design. Nonetheless, only by looking at the

operational profile it is possible to understand how likely it is for LNG to work out as a fuel

for a given design. The main factors to take into consideration in this analysis are:

1. Type of voyages: It is important to distinguish whether the vessel will be engaged in

round-trip regular voyages or if a more irregular voyage pattern is followed as in the

case of “tramp shipping”.

2. Duration of voyages: The duration of the voyage might dictate, if long, that a large

storage capacity may be required with direct influence on the ships general arrangement,

in particular regarding the volume required for LNG storage tanks.

3. Type of Cargo: The type of cargo will influence the location of LNG fuel storage location.

It will also influence the net present value for a given project and the time for investment

pay-back, mostly influenced by the effect of different applied freight rates.

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

32

4. Type of operations: Vessels operations may influence the risk & safety case for a given

design. Tug-boats and other special service vessels are work intensive platforms above

deck. Their main dimensions are also mostly influenced by operational requirements. For

both these reasons the location and design arrangement for LNG fuel systems may not

be always easy to draft. Simultaneous operations (SIMOP’s), during LNG bunkering can

be considered a subject where some uncertainty still subsists, thus affecting the

operational analysis study for a given design and, therefore, also its business case.

5. Bunkering: LNG fuel bunkering procedures are still being harmonised. Different LNG

bunkering guidelines have been issued from Classification Societies, SGMF amongst

others. More importantly ISO issued in January 2015 the Technical Specification ISO/TS

18683:2015 providing requirements and recommendations for operator and crew

competency training, for the roles and responsibilities of the ship crew and bunkering

personnel during LNG bunkering operations. Bunkering requirements, if influenced by

typical ship operations at berth, may therefore affect the decision to opt for LNG as fuel.

Highlighted below are the different vessel types and their operational profile/characteristics

and their potential for adoption of LNG as a bunker fuel.

Ferries/RO-PAX – there are significant numbers of short-sea ferries that operate in EU

waters. These vessels are ideally placed to utilise LNG as a bunker fuel. The majority of

the vessels trade on fixed routes which enables bunkering schedules to be tailored to suit

LNG bunkering. Furthermore, aspects such as sizing of the LNG fuel storage tank can be

optimized in order to avoid ageing of LNG. A RO-PAX optimized for a given route can

easily program the tanks to be filled at a minimum threshold close to minimum levels.

This has the potential to optimize the filling times during bunkering and also reduce the

likelihood of the roll-over of the LNG during bunkering, especially for larger tanks. From

an economic perspective, predictability of bunkering is likely to favour commercially

advantageous agreements with LNG bunker suppliers.

A possible problem that can be faced by RO-PAX operators is the simultaneous operations

of LNG bunkering and Embarkation/Disembarkation of passengers.

For ferries operating in Northern European waters, such as the North Sea and the Baltic,

LNG enables vessels to meet the strict ECA requirements. There is increased interest in

LNG for these vessels in the region, with many ship-owners investigating this option,

against other abatement methods such as scrubbers. Short-sea ferries are already

amongst some of the early adopters of LNG bunkers, as already highlighted with the

Viking Grace that trades between Stockholm (Sweden) and Turku (Finland). A more

recent order has been placed by Tallink in late-2014, who has ordered a new LNG-fuelled

ferry for its Tallin-Helsinki route (the vessel is named Megastar). There are several other

examples of LNG-fuelled Ro-Ro vessels that are operating in the Baltic and North Sea

region, such the Fjord Line vessels. This has stimulated interest from other owners to

investigate LNG-powered vessels.

Cross Channel and Mediterranean ferry operations, such as those that support Corsica,

Sardinia and Sicily, as well as the Greek Island trades, could also benefit from LNG fuelled

conversion/newbuilds, especially if LNG is cheaper than conventional fuels.

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

33

Offshore (OSV/PSV/AHTS) – as with other vessel types, a major influence on the use of

LNG as a fuel will be where a vessel operates. Already there are a number of PSV vessels

utilising LNG as a bunker fuel in the North Sea.

The varying OSV operational modes represent a design challenge in order to achieve high

fuel efficiency. Full integration of the propulsion systems is needed to optimise the

performance of the thrusters and prime movers. Without having a regular operational

profile, OSVs have to rely on optimisation of fuel consumption by adoption of energy

efficiency strategies. The typical amount of time spent at sea will represent a major

design driver for LNG fuelled OSVs.

The offshore sector has had a major influence on the introduction of gas-fuelled vessels.

The cost benefits of utilising the fuel and the reduced emissions are strong positive

factors in this regard. In addition, LNG-fuelled offshore vessels have been shown to

operate satisfactorily in some of the most demanding North Sea weather conditions.

There is currently a high proportion of offshore vessels in the LNG-fuelled vessel

orderbook (approximately eight vessels), with future orders forecast to increase

significantly. This sector is currently at the fore-front of adopting gas-fuelled vessels.

Tugs – a major influence on the design of vessels will be the location of operation and

the type of work to be undertaken. The work intensive profile of the above deck typical

tug configuration will dictate the LNG fuel location. This will very likely need to be placed

below deck in order to favour structural protection. The size and autonomy of the tug will

be mostly influenced by the fact that LNG-fuelled tugs are able to operate in ports that

are within an ECA. Tugs now account for around three vessels within the LNG-fuelled

orderbook. This sector is one that is expected to significantly expand in the future within

the EU.

Cruise ships– as with ferries and Ro-Ro vessels, some cruise ships follow a regular

voyage pattern, with a number of vessels operating within the Baltic region. However,

depending on the operational profiles of the vessel, there can be extended periods

between ports. Whilst RO-PAX vessels tend to be more regular with regards to their

journey durations, cruise vessels will require the adoption of energy efficient technologies

in addition to a carefully studied LNG fuel consumption estimate in order to size LNG fuel

storage.

There is increasing awareness of environmental protection through more sustainable

forms of travel and holidaying. Increased numbers of passengers are participating in and

encouraging environmental tourism. The cruise industry is also an expanding market.

As owners and operators seek new initiatives to differentiate themselves from the

competition and reduce fuel costs, it is envisaged that gas-fuelled vessels (in this case

either newbuilds or retro-fitting of existing vessels) will enable new opportunities to both

owners and passengers. Vessels trading in and between ECAs could be a major growth

sector for the up-take of LNG as these can cover both Short- and Deep-sea routes.

Some operational aspects regarding LNG as fuel for cruise vessels remain under

development, especially those relating to bunkering operations, Embarkation

/disembarkation of passengers to/from the LNG fuelled cruise ship whilst bunkering, is an

aspect that needs to be addressed.

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

34

Containerships – container vessels could benefit from LNG as a bunker fuel, especially if

the majority of their voyages are concentrated in ECAs, such as Northern Europe/Baltic.

However, a major concern for container vessels is the reduction of cargo space due to the

size of the required fuel tanks. This is also a concern for the larger deep-sea vessels. This

would be particularly relevant for short-sea shipping feeder container vessels, but also for

larger deep-sea trade.

However, the economics of potentially cheaper LNG fuel could be a defining motivation for

owners to reduce costs, thus markedly increasing demand for LNG as a bunker fuel in the

future.

Having “LNG-ready” ships can be one option to build now and decide on LNG fuel later.

The architecture of a containership favor’s modularity and it is possible to have the

adoption of LNG later during service life, provided the ship design and relevant fuel

system safety aspects are taken into consideration at early design stages.

The particular case of LNG fuelled containerships can be favoured by the predictability of

the operational profiles. Especially for larger containerships the ports visited and the

speeds kept throughout the journeys tend to be a constant. This can have a very positive

influence on the design of the potential LNG fuel storage system, but also on the

arrangement/tailoring of service framework contracts for LNG bunkering services.

Tankers (crude/product/chemical) – Tankers are ideally placed to benefit from the

use of LNG as a bunker fuel. The Bit Viking product tanker was converted to run on LNG

during 2011, with LNG fuel tanks placed on deck, having minimal impact on the internal

general arrangement and global cargo capacity of the vessel. Even in this very specific

application, it is possible to say that in general the above deck areas for tankers offer

potentially favourable locations for LNG fuel storage. This is however a design driver that

there are no significant practical limitations to this solution, meaning larger crude tankers

could also utilise this concept. Depending on the owners/operators requirements,

potentially this option could result in either the converting of current vessels or ordering

newbuilds for both Short- and Deep-sea vessels. From a naval architecture perspective,

the addition of above deck LNG-fuel tanks has potential to reduce conversion costs as

impact on general arrangement is minimum and, provided the right weight-volume

distribution/balance is achieved it is possible to optimize cargo capacity.

Bulk carriers – as with tankers, bulkers could benefit from LNG as a bunker fuel. There

is significant deck space where fuel tanks could be located, depending on the size and

design of the hatch coverings. As such, deck-based tanks could allow limited impact on

the cargo capacity of the vessel. Unlike Tankers however, bulk carriers tend to be rather

work intensive above deck areas, especially during crane loading/unloading (LO-LO)

operations. This would require external tanks to be provided with dedicated physical

protection measures.

This sector could benefit from future converted or newbuilding vessels.

Also as with tankers, given the fact that the majority of the fleet is not deployed on fixed

itineraries (unlike cruise ships, ferries etc.), the main restriction to LNG adoption might

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

35

come from a limited infrastructure (i.e. insufficient number / spread of bunkering

locations).

Table 1-4 Vessel sectors and their potential for adoption of LNG as a bunker fuel

Vessel type Likely factors favouring LNG as fuel Challenges to the Adoption of LNG as fuel

RO-PAX

Predictable routes typically in short-sea shipping routes

Routes inside ECA

LNG availability/planning

Possibility of LNG fuel service framework contract

Risk & Safety aspects

Simultaneous operational restrictions during bunkering

Additional construction (and life-cycle) cost of LNG-fuelled newbuilding

Offshore

(OSV/PSV/

AHTS)

LNG availability

Typically based at a specific port, close to offshore operation areas. Possibility of LNG fuel service framework contract

Operational profile not constant, with multi-purpose mission profiles

Risk & Safety aspects if OSV has work intensive operational profile, with close contact operations

Tugs

Air emissions reduction

Operation inside port areas, under increasingly stricter environmental requirements

LNG availability (if port of operations has LNG bunkering facility)

Operational profile not constant, with multi-purpose mission profiles

Risk & Safety aspects – Tugs have typically work intensive above-deck areas

Space available for LNG fuel tanks is reduced, especially if protective design arrangement needs to be taken into consideration

Cruise Ships

Predictable routes, even if typically longer than RO-PAX

Time spent inside ECA’s

Public image for cruise ships with potential gains with environmental friendly image (“sustainable tourism”)

LNG availability if operational routes favoured with LNG prepared ports

Risk & Safety aspects

Simultaneous Operations possible restrictions during bunkering

Additional construction (and life-cycle) cost of LNG-fuelled newbuilding

Containerships

Predictable operational profiles (for both deep-sea and short-sea feeder vessels)

Modular general arrangement favouring LNG-ready solutions for later adoption of LNG fuel systems

Time spent inside ECA (especially for short-sea feeder container vessels)

Space taken by LNG fuel storage systems, which reduce marginally cargo capacity, for similar displacement ships

Required freight rate calculations highly sensitive to fuel price fluctuations

LNG fuel availability, for feeder containerships, if ports have no LNG bunkering facility

Tankers

Time spent inside ECA (especially for short-sea tankers)

Typical above-deck arrangement favouring installation of LNG storage tanks with minimum impact in cargo capacity

Environmental compliance, especially if operation inside ECA’s is envisaged

Operational profile can be less predictable than other types of ships, especially for short-sea tankers

Availability of LNG fuel can be reduced in ports dealing with other dangerous cargo (such as flammable liquid cargo)

Risk & Safety management for tankers

Bulk Carriers

Time spent inside ECA (especially for short-sea bulk carriers)

Typical above-deck arrangement likely to favour installation of LNG storage tanks with minimum impact in cargo capacity, depending on hatch arrangement.

Operational profile can be less predictable than other types of ships, especially for short-sea bulk carriers

Availability of LNG fuel can be reduced in ports dealing with other dangerous cargo

If cranes are installed, general arrangement

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

36

Vessel type Likely factors favouring LNG as fuel Challenges to the Adoption of LNG as fuel

Environmental compliance, especially if operation inside ECA’s is envisaged

Particular interest for bulk carriers with self-unloading capability, since these are usually heavy polluters at berth during unloading operations

above deck can be made more complicated

Small domestic

ferries

Typically used for short distance canal or riverine crossings, spending all time within port areas in ECA’s. Reduction of air emissions is therefore a key benefit and driver

Public image of “greener” ferries, highly visible to populations

Predictable operational profile, as an advantage for possible LNG fuel service framework contract

Small riverine ferries are highly space-sensitive. LNG fuel systems take a considerable internal volume and affect therefore transport capacity

Risk & Safety aspects, depending on specific risk acceptance criteria

Inland shipping

Positive environmental benefits inland, contributing to improve the air emissions footprint along the inland waterways

Increased availability of LNG refueling points via important inland multi-modal nodes

Small inland vessels are highly space-sensitive. LNG fuel systems take a considerable internal volume and affect therefore transport capacity

Risk & Safety aspects, depending on specific risk acceptance criteria

Source: Ocean Shipping Consultants a company of Royal HaskoningDHV / EMSA

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

37

1.4.1 LNG-fuelled vessels in 2030

There have been a number of studies that have forecast the growth in the LNG-fuelled fleet.

During 2011, the Danish Maritime Authority published a report highlighting that 1,000

vessels would be operating in the Northern European SECA region through to 2020.3 In

addition, DNV forecast that 1,000 LNG-fuelled newbuilds would be delivered through to

2020.4 This would account for approximately 35% of all newbuilds to be gas fuelled. Ocean

Shipping Consultants (a company of Royal HaskoningDHV) published a study highlighting the

growth in the LNG-fuelled vessel market.5 The Report forecast 1,250 LNG-fuelled vessels by

2025.

However, the newbuilding sector has not witnessed the significant increase in new-orders for

vessels in the last year as compared to the previous couple of years. Therefore it is

anticipated that the sector will still develop, albeit not at the rate and scale as recent

forecasts have suggested.

This study will highlight the future gas fuelled vessel market through to 2030.

To provide background into the forecast for the development of the LNG-fuelled fleet a

number of assumptions for the High and Low case are highlighted below.

High Case

Global Sulphur limits are introduced in 2020 – meaning that some vessel owners

will seek, amongst the possible abatement methods, alternative fuels to enable full

compliance. This will potentially benefit the up-take of LNG as a fuel.

Additional countries implement air emission standards – as air emissions

continue to rise, a switch to LNG fuel can dramatically reduce vessel emissions.

Additional Emission Control Areas (ECAs) – Additional ECAs, such as in the

Mediterranean and around Japan, would add the obligation for SOx limits lower than

the future global cap of 0.5%. The ‘High Case’ scenario reflects the effect of this

possibility, with an optimistic anticipation of additional stricter emissions at new

specified areas.

Development of alternative fuels/propulsion – under the high case, alternative

fuels to HFO and MGO will be developed to be utilised for marine propulsion. Of

these, LNG will be a significant alternative. Developments in the regulatory

framework of these alternative fuels, together with improved risk perception of their

utilisation as marine fuels, are expected to encourage their uptake.

Rising economic growth and Increase in Shipping Trade – brings increased

demand for shipping activity as national economies expand.

Rising oil/distillate fuel prices – oil/distillate fuel prices can be affected in many

ways, but mostly if demand rises, prices will traditionally follow, or if supply is

restrained, prices can also increase. Either of these scenarios could be positive for

LNG as a fuel.

3 North European LNG Infrastructure Project, 2011

4 Shipping 2020, 2012

5 LNG as a Bunker Fuel: Future Demand Prospects & Port Design Options

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

38

Rising freight rates – this occurs as demand for vessels increases. This will occur

when today’s underutilised vessels are fully active. This usually implies that there is

growing economic activity in line with ‘High Case’ assumption of rising economic

growth.

Increase in newbuilding orders – increased vessel activity is usually a stimulus for

owners to order new or additional vessels. As such, these vessels could be ordered

with alternative fuels systems, such as LNG.

Additional research into LNG-fuelled vessels – as vessel demand rises, vessels

that can offer operating savings – such as those that can be operated on alternative

cleaner fuels (LNG) may have an advantage in the charter market. Key research

areas in LNG ship design, such as tank optimised integration, efficient engines, boil-

off gas consumption and cryogenic liquefaction are developed at a higher pace under

the ‘High Case’.

Harmonised LNG bunkering standards – this will encourage new entrants to

utilise LNG and complying with industry standards for bunkering. Harmonised LNG

bunkering guidance would help the uptake of LNG by addressing specifically the

safety/risk perception regarding LNG as fuel.

Enforcement Levels – The enforcement levels of environmental legislation, with the

application of dissuasive and effective penalties to those non-complying to air

emission regulations, are assumed under the High Case.

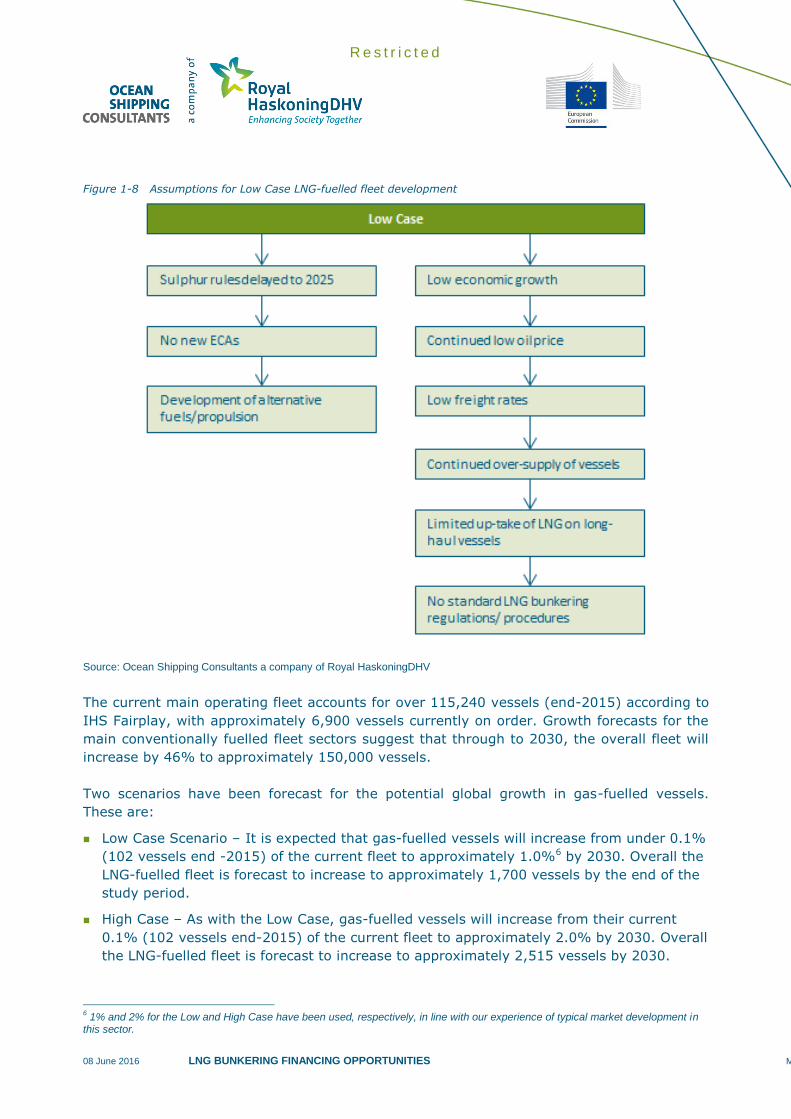

Low Case

Global Sulphur cap/limits delayed to 2025 – the review in 2018 allows the

deferring of stricter SOx global cap to 2025. This would have the potential impact of

delaying the investment in LNG-fuelled ships by several years.

No new ECAs – reduced economic or political determination to implement new

emission control areas. As such, this may limit the number of future LNG-fuelled

vessels to specific areas/regions that already have ECAs, leading the deep-sea trade

to opt for other compliancy strategies/technologies.

Development of alternative fuels/propulsion – alternative fuels that are either

cheaper or/and easier to handle compared to LNG may be developed and utilised.

Even though methanol has a limited regional availability this could be subject to

research and preferred against LNG for some cases. Additionally the development of

low-sulphur distillates, blends, and their increased availability, could lead to reduced

LSFO prices, with an impact on the adoption of LNG as an alternative fuel. These

developments are assumed in the ‘Low Case’.

Low economic growth – national and regional economies continue to remain at

either low or stagnant levels of activity.

Continued low fuel prices – low cost traditional fuels mean that vessel

owner/operators can utilise their vessels without investing in additional new fuel

systems. This is especially relevant if low-sulphur distillates prices are also made

available at lower prices.

Low freight rates – continued low vessel activity, with some vessels being laid-up.

Currently, the offshore and dry-bulk sectors are experiencing low freight rates. If the

tendency persists, with the low freight rates, the business case for LNG is very

difficult with expected pay back times for investment unsatisfactorily increased.

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

39

Continued over-supply of vessels – as above, the offshore and dry-bulk sectors

have significant over-supply of vessels. This is forecast to continue in to the near-

term.

Limited up-take of LNG on long-haul vessels – with significant over-supply of

vessels, particularly in the long-haul sectors, vessel renewal will be limited. Thus

reducing the impact of new LNG-fuelled vessels in the medium-term.

No standard LNG bunkering regulations/procedures – The ‘Low Case’ reflects

uncertainty and lack of harmonization in LNG-bunkering. The adoption of LNG as an

alternative fuel, on the basis of this assumption, could be excluded in favour of other

compliance technologies/abatement methods.

Environmental Concerns – The GHG emission factor of LNG/methane (when

leaked) is much higher than CO2. In the ‘Low Case’ scenario this is a fact that could

affect the uptake of LNG as an alternative fuel for shipping.

It should be noted, that these assumptions are used to help forecast the future LNG-

fuelled fleet. Any changes to the assumptions could impact on the fleet’s development.

Figure 1-7 Assumptions for High Case LNG-fuelled fleet development

Source: Ocean Shipping Consultants a company of Royal HaskoningDHV

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

40

Figure 1-8 Assumptions for Low Case LNG-fuelled fleet development

Source: Ocean Shipping Consultants a company of Royal HaskoningDHV

The current main operating fleet accounts for over 115,240 vessels (end-2015) according to

IHS Fairplay, with approximately 6,900 vessels currently on order. Growth forecasts for the

main conventionally fuelled fleet sectors suggest that through to 2030, the overall fleet will

increase by 46% to approximately 150,000 vessels.

Two scenarios have been forecast for the potential global growth in gas-fuelled vessels.

These are:

Low Case Scenario – It is expected that gas-fuelled vessels will increase from under 0.1%

(102 vessels end -2015) of the current fleet to approximately 1.0%6 by 2030. Overall the

LNG-fuelled fleet is forecast to increase to approximately 1,700 vessels by the end of the

study period.

High Case – As with the Low Case, gas-fuelled vessels will increase from their current

0.1% (102 vessels end-2015) of the current fleet to approximately 2.0% by 2030. Overall

the LNG-fuelled fleet is forecast to increase to approximately 2,515 vessels by 2030.

6 1% and 2% for the Low and High Case have been used, respectively, in line with our experience of typical market development in

this sector.

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

41

Figure 1-9 Low and High Case Scenarios for LNG-Fuelled Fleet Development to 2030

(Number of vessels)

Source: Ocean Shipping Consultants a company of Royal HaskoningDHV

Figure 1.10 highlights the forecast through to 2020, to provide a more detailed outline

of the near-term development of the fleet.

Figure 1-10 Low and High Case Scenarios for LNG-Fuelled Fleet Development to 2020

(Number of vessels)

Source: Ocean Shipping Consultants a company of Royal HaskoningDHV

The price of LNG is a major factor for shipowners in determining whether to invest.

Especially the relative price difference between marine fuel oil and LNG and the

expectations regarding the long-term price differential are of great importance.

The ship owner will choose from proven technology, as this is readily available in the

market at the moment.

In terms of political risk, the ship owner has to rely on the continuation of the ECAs,

and even expanding, as well as that no policy implications against LNG as marine fuel

are undertaken in the future.

If the points as outlined here can be solved sufficiently well, LNG as fuel for shipping can

materialize in economically viable business cases. Summarising, we see the following major

risks that the shipowners are facing, which may prevent them from making a positive

investment decision:

1. Guarantee of supply of LNG bunkering facilities (sufficient facilities in a grid of

locations).

2. Energy price differential between LNG and marine oil fuels.

5.1.3 Bunkering facility operators

The operators of LNG bunkering facilities face a different investment decision. In this study,

we look at four different bunkering facilities (for which the investment decision is similar due

to similarities in the business model, albeit that the capital expenditure involved differs

hugely between the different facilities)11:

Truck to ship facility

Ship to ship facility

Small shore storage tank facility

Large shore storage tank facility

The investment decision of operators is based on an assessment of several factors. These

include:

11

These options are further explained in Task 3.Although minor differences may exist between different types of bunkering facilities in terms of type and degree of risks, these differences are much less relevant than the risks they have in common, as discussed in this paragraph for bunkering facilities in general.

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

97

Availability of LNG is not likely to impede investments in LNG bunkering facilities. The

UK and Spain are Europe’s main importing countries of LNG, and many other

countries (such as The Netherlands, Belgium and France) have facilities to import

LNG as well12. In the absence of (nearby) LNG regasification terminals, natural gas

can be sourced on a trading hub or through bilateral contracts and liquefied at the

bunkering facility.

The main risk is the offtake risk: the operator would not make a positive investment

decision if the offtake is uncertain. In other words, the operator’s business model

depends on sufficient LNG fuelled vessels being available in the market, and beyond

that, his capacity to enter into longer term offtake contracts with shipowners.

The price level of LNG is less relevant to the bunkering facility operator than for the

ship owner, as the operator earns a premium on the commodity price, transferring all

price risk to the ship owner.

The technology risk for the operator is small, as the technology is readily available in

the market and is deemed proven.

Necessary landside infrastructure is usually provided by the port, in return for a fee

(included in the land lease / rent agreement). This is therefore no great risk to the

project.

If the points as outlined here can be resolved sufficiently well, then this is an economically

viable business case. Summarising, we see the following major risk the operators of LNG

bunkering facilities are facing, which may prevent them from making a positive investment

decision:

1. Uncertainty about offtake agreements with sufficiently large client base.

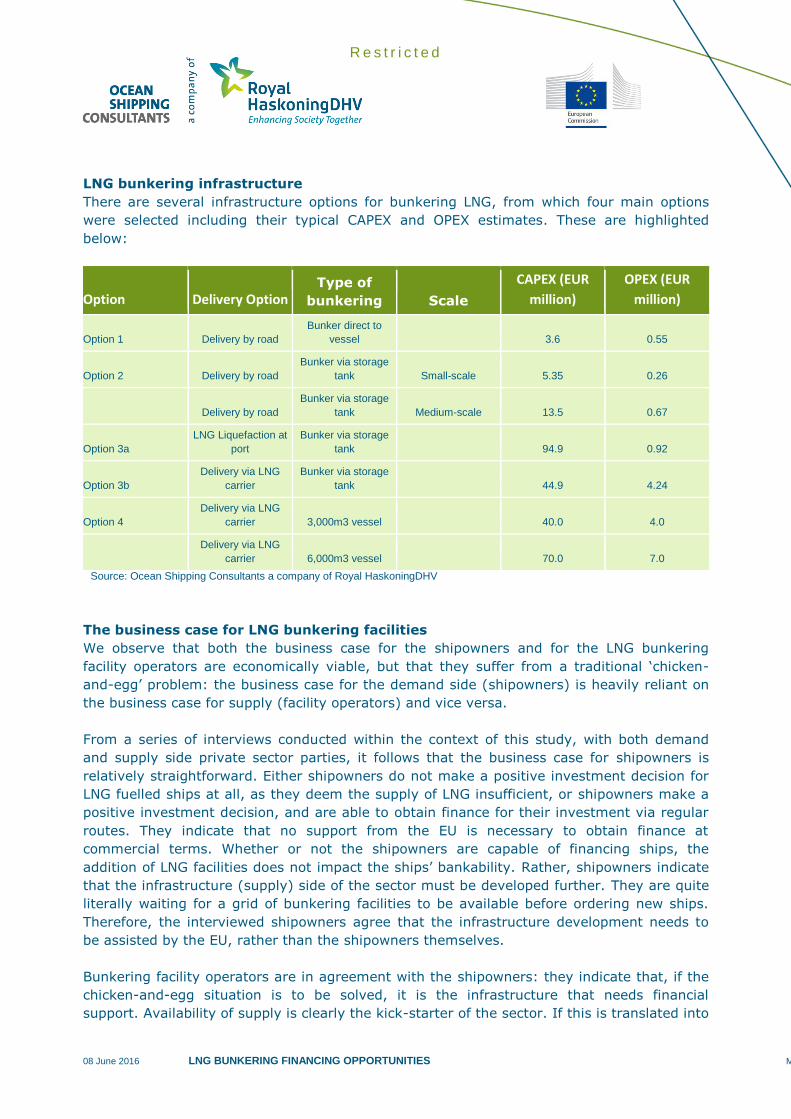

5.2 Needs analysis: combining demand and supply

We observe that both the business case for the shipowners and for the LNG bunkering

facility operators are economically viable, but that they suffer from a traditional ‘chicken-

and-egg’ problem: the business case for the demand side (shipowners) is heavily reliant on

the business case for supply (facility operators) and vice versa.

From our interviews with both demand and supply side private sector parties, it follows that

the business case for shipowners is relatively straightforward. Either shipowners do not

make a positive investment decision for LNG fuelled ships at all, as they deem the supply of

LNG insufficient, or shipowners make a positive investment decision, and are able to obtain

finance for their investment via regular routes. They indicate that no support from the EU is

necessary to obtain finance at commercial terms. Whether or not the shipowners are capable

of financing ships, the addition of LNG facilities does not impact the ships’ bankability.

Rather, shipowners indicate that the infrastructure (supply) side of the sector must be

developed further. They are quite literally waiting for a grid of bunkering facilities to be

available first before considering to ordering new LNG fuelled ships (notwithstanding other

considerations in their investment decision). Therefore, shipowners agree that the

infrastructure development needs to be assisted by the EU, rather than the shipowners

themselves. Table 5-9 highlights the relevant findings from 5 interviews carried out as part

of the validation task (Task 9). All 5 interviewees represent large, professional organisations

12

The website of Gas Infrastructure Europe provides an overview of existing and under construction infrastructure for LNG: http://www.gie.eu/index.php/maps-data/lng-map

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

98

with a deep experience in their line of business. All interviewees support the conclusions

drawn here.

Table 5-2: Relevant findings from interviews on financing support

Type of organisation View on the need for financing support

Port operator

Support from EU should be aimed at facilities; there is an egg

and hen problem. To kick-start the market, facilities should be

widely available. If supply is created, demand will follow. Any

potential EU investment / financial assistance should go to

supply infrastructure instead of ship owners, since most added

value can be reached in improving the infrastructure network.

Ferry operator

Agrees with the statements made by the Port. “In financing the

ships, no specific issues were stumbled upon. The project had already

been commercially financed, after which the existence of EIB funding

was discovered by the project. The project has since been refinanced

by the EIB at more favourable terms.”

Financial institution

This bank is involved in the financing of vessels, not so much in LNG

infrastructure. Key to unlocking the LNG as marine fuel sector lies in

infrastructure, this is the element that needs to come first. Ships won’t

be ordered speculatively. The bank has looked at this type of projects

in the past. Some parties will take demand risk that will be reduced

over time. Demand will follow supply.

Cruise operator

When the company compared the total costs of ownership of a LNG

vessel with a HFO vessel, the company ultimately decided not to

invest. The main reason for that decision is the unavailability of a well-

developed supply chain of marine LNG around the world. Asked

whether there are any obstacles/ gaps in the availability of private

financing for LNG vessels, the company representative replied that this

is not likely; its competitor recently bought new LNG vessels and they

work with the same lenders. Using LNG means losing some cabins

(since tanks are bigger). However, with a good explanation for

investors/ financiers, all in all, investors and financiers do not deny

investments in vessels based on the fact that they use LNG as a fuel.

In the company representative’s view, the availability (supply) of marine

LNG would have to improve for the market to develop. Focus of

support by the EU on the demand side (in the form of loans at attractive

conditions) would help, but is far from necessary. Availability (supply) of

marine LNG is the showstopper. LNG is quite an attractive option for an

owner of vessels, also taking into account the (capital and operational)

costs of exhaust gas treatment. If the EC wants to move the market of

marine LNG forward, investments should focus on the infrastructure

side.

Ship owner (transporting RoRo

goods short-sea)

While LNG was certainly a topic in the discussions with financiers, this

did not render the investment in LNG fuelled vessels difficult to finance.

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

99

The company’s representative is not aware of any gaps in the private

financing of infrastructure either. He stresses that implementing marine

LNG is a matter of jointly developing a collaborative project with

partners on the demand and on the supply side, so both develop

simultaneously. In that way, uncertainty in the business case is

minimised. In his view, stimulation of the supply side of the market will

cause demand to follow.

Source: Ocean Shipping Consultants a company of Royal HaskoningDHV

This view is supported by the minutes from a meeting13 of the ESSF sub-group on funding

for LNG-fuelled vessels, stating that “Shipowners can encounter some difficulties in

accessing banking resources [red: in general, not aggravated by the decision to implement

LNG facilities].” “Moreover, those [financial] instruments can promote the deployment of

LNG infrastructure in ports.”

Bunkering facility operators are in agreement with the shipowners: they indicate that, if the

chicken-and-egg situation is to be solved, it is the infrastructure that needs financial

support. Availability of supply is clearly the kick-starter of the sector. If this is translated into

a business case perspective, it means that LNG bunkering facilities will be built that will have

a very limited customer base for the first years of operations (unless there is a ‘home

customer’ for the facility, such as a ferry operator). For only if it is certain that the facilities

will become available, shipowners will make a positive investment decision to buy LNG

vessels. These first years of operations, having low revenue levels, have to be bridged. This

is essential to retain a viable business case for the bunkering facility operator. The figure

below illustrates this time gap during which the facility operator has a very low level of

revenues.

One way to bypass this problem is to use an integrated project approach towards the

development of the sector. This means that demand and supply are developed

simultaneously; the bunker facility operator and the vessel operator discuss the timeline,

volumes, capacities, terms and conditions etc. and reach a mutual commitment that enables

both sides to take a positive investment decision. Lead times of the LNG powered vessels

and bunkering facilities would then ideally be aligned to avoid or at least minimise the

aforementioned time gap. The vessel owner may even decide to participate financially in the

facility, thus gaining more control over his supply chain of fuel and strengthening the

business case for the facility (although potential conflicts of interest may arise as well).

Several parties have indicated that if the EU wishes to accelerate the development of marine

LNG, it could consider contributing to a network of bunkering facilities and thereby improve

the availability and removing the most important barrier to investing in LNG powered ships.

This approach can be taken even further by adding demand sectors for LNG other than

marine use, such as heavy-duty trucks or buses and inland water vessels. If for instance a

long-term offtake contract with the owner of a fleet of long-haul trucks can be closed then

the offtake risk for the terminal is significantly reduced. As the onshore LNG refueling

infrastructure develops further, the truck fleet owners will become less dependent on the

LNG port-facility they helped to launch and vice versa.

13

On 29 October 2014

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

100

Table 5-3 Schematic overview of the resulting time gap between the two business cases

Source: Ocean Shipping Consultants a company of Royal HaskoningDHV

For this approach to be feasible, a necessary precondition is that one or more shipowners

can commit themselves to bunkering their ship(s) at one (or a limited number of) specific

facility or facilities. This will only apply to those shipowners that operate regionally.

However, some portion of the capacity not being contracted at the completion of the facility

means that this capacity is available to the market, which contributes to a grid of LNG

bunkering facilities and enhances the availability of marine LNG. This is an approach that is

similar to the ‘anchor fleet’ approach that has been successfully applied for CNG as fuel for

road transport14.

Notwithstanding this bypass to the problem, it is recognised that this solution will not be

applicable in all situations, meaning that the time gap will remain. Potential financing

mechanisms looking to promote LNG as a marine fuel should focus on this issue.

5.3 Financing gap analysis

5.3.1 Investment considerations

In general, investors and financiers use the following set of assessment criteria when making

investment considerations. In the next paragraph, we will describe the criteria that financiers

indicate will impact their decision to invest in LNG bunkering facilities (and to a lesser

extent, vessels).

Asset type: Assets are often specialised and should have an economic life well beyond the

term of the debt.

14

As described in e.g. “Natural Gas as a Transportation Fuel: Models for Developing Fueling Infrastructure”, American Gas Foundation, September 2012.

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

101

Term: The term of financing facilities should be commensurate with the economic life of the

asset, and the project structure should encourage subsequent refinancing either in the bank

or capital markets.

Performance risk: An investor is exposed to the performance risks involved in the design,

construction and operation of the project. Suitable contractual protections, qualified and

competent counterparties and independent technical advice should be sought to ensure

adequate comfort.

Issuer financial covenants: Financial covenants, in which the issuer undertakes to comply

with certain ratios, act as a proxy measure of the issuer’s ability to service and repay its

debt and, if measured in a consistent way, can be an effective 'early warning system' which

allows investors to assess deteriorations in the risk attached to the credit quality of the

issuer and to the debt. Well-designed and appropriate financial covenants can also provide

timely performance indicators for investors.

It is however difficult to design a finite list of appropriate financial covenants as the terms

may vary considerably depending on the circumstances, including the nature of the issuer’s

business, its credit quality and the scope of financial covenants in existing bank loan and

other debt documentation (although the starting point for financial covenants will usually be

the scope of any financial covenants in the issuer’s existing bank loan and other debt

documentation, if any). Key ratios in project finance include the Debt Service Coverage Ratio

(DSCR), Loan Life Coverage Ratio (LLCR), Project Life Coverage Ratio (PLCR) and Debt to

Equity ratio.

Third Parties: Where third parties have significant obligations to the project company, their

credit standing is an important part of the credit application for the project. Third parties

may include corporate entities, banks and insurance companies.

Environmental Risk: Environmental issues may materialise due to the intrinsic nature of

project finance transactions and sector environmental risk profiles. Most investors have

adopted the ‘Equator Principles’ which seek to provide a framework for assessing and

managing social and environmental risks, in line with international best practice.

Documentation: Rights and obligations of the various parties must be clearly set out to

avoid the risk of lengthy litigation at a later stage. In respect of PFI/PPP projects the powers

of the public sector body to enter into contracts with the project company needs to be

investigated. Other issues include the transaction structure, security, step-in rights, events

of default and compensation on termination.

Interest Rates and Currency Risk: Changes in interest and currency exchange rates may

materially affect the project company cashflow. A hedging strategy should be established

and described in the credit application.

Insurance: Insurance is required by the SPV to allow for, inter alia, reinstatement of

assets, loss of earnings and third party liabilities.

Tax: With the exception of corporation tax, the project company should not be exposed to

changes in tax.

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

102

5.3.2 Criteria impacting the investment decision for LNG facilities

In interviews with financiers (and operators) we have established that the most important

factors that influence the decision whether or not to finance LNG facilities (and to a lesser

extent, vessels) are the following:

Project performance risk due to lack of demand

Financiers confirm that to kick-start the sector, investment in LNG bunkering

facilities, rather than vessels, is necessary. Without the infrastructure in place,

vessels will not be ordered speculatively. Thus, the infrastructure must be realised

first. Financiers want the offtake to be contracted up-front before they will enter into

the project. In terms of a threshold (i.e. an offtake level above which financiers are

willing to lend to the project), the following information was provided to us:

o a minimum offtake level of 50% to 60% of the total offtake; and / or

o offtake that guarantees a debt service cover ratio (DSCR) of 1.0 (i.e. 100%).

With respect to the latter, banks normally demand the project to be able to have

substantially higher cover ratios to service debt (for example 1.15), but considering

the limited age of the sector for LNG as marine fuel, a cover of 1.0 would be

acceptable. Commercial banks would potentially be willing to ‘take a market view’ on

the remainder of the offtake (i.e. that would not have to be contracted up-front).

Legislation

As mentioned in Section 1, new EU rules have been adopted during September 2014

to ensure the build-up of alternative refueling points across the EU. However, there is

still some ambiguity as to the rules/legislations/guidelines for this sector. There are

concerns that the bunkering methods utilised may differ between countries. This is a

worry for both operators and financiers. It does not create a financing gap, but it

does add to the severity of it. Transparent legislation that is common between the

member states is important for LNG bunkering projects to be financed, especially

related to realising a network of such facilities throughout Europe. It is understood

that this is a new industry and processes and procedures need time to be worked out

and ratified by the various stakeholders involved.

Technology

The parties we have interviewed differ in their statements about the technology:

some say that the technology is not new anymore, which enables commercial

financiers to lend to projects. However, others suggest the technology is still a factor

that must be considered in the investment decision, albeit that the impact on the

financing gap of this criterion is smaller than the previously stated criteria.

5.3.3 The financing gap

There clearly exists a financing gap for LNG bunkering facilities in Europe. Without a ‘home

customer’ (such as a ferry operator) or substantial guarantees regarding the offtake of LNG,

such facilities cannot be financed commercially at the moment. This is mainly due to the

uncertainty about offtake (demand), as indicated above. The uncertainty is made worse by

limited knowledge about LNG as a marine fuel at commercial banks and the limited amount

of due diligence that has been executed in this sector. This prevents commercial banks from

taking a view on the development of future market demand.

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

103

Whereas certain individual facilities could potentially be financed commercially (i.e. the ones

for which offtake has (largely) been guaranteed), the majority of facilities are less likely to

achieve this. The financing gap calls therefore for public sector participation in this sector,

especially if it wants to ensure development of a grid (network) of LNG bunkering facilities.

It is clear that potential public involvement should focus on the (temporary) lack of demand

as explained in the previous points (time gap).

5.4 Identification and assessment of financial mechanisms

5.4.1 The EU structure of financial mechanisms

For the definition of financial mechanisms as used by the European Union, we draw upon

REGULATION (EU, EURATOM) No 966/2012 OF THE EUROPEAN PARLIAMENT AND OF THE

COUNCIL of 25 October 2012 on the financial rules applicable to the general budget of the

Union and repealing Council Regulation (EC, Euratom) No 1605/200, which reads:

(39) For reasons of legal certainty, the scope of grants and financial instruments should be

clarified. A more detailed definition of the specific conditions applicable to grants, on the one

hand, and to financial instruments, on the other, should also contribute to maximising the

impact of those two types of financial support.

(40) The grant rules applicable to entities specifically established for the purpose of an

action should be adjusted so as to facilitate access to Union funding and management of

grants by applicants and beneficiaries having decided to work together within a partnership

or grouping constituted in accordance with relevant national law, in particular where the

legal form chosen offers a solid and reliable cooperation environment. In addition, in the

light of the limited financial risks for the Union and the need to avoid adding a layer of

contractual requirements to existing structural arrangements, entities affiliated to a

beneficiary through permanent capital or legal links should be entitled to declare eligible

costs without having to comply with all the obligations of a beneficiary.

Moreover, we understand that a three-level structure applies to EU financial mechanisms as

outlined in the figure below. The first level contains a set of financial mechanisms, namely

financial instruments (such as equity, debt and guarantees), investment grants and

economic incentives (such as tax exemption).

The second level of the structure considers the deployment of the mechanisms: this can

either be done by the Member States, or, in case of the financial instruments, by a financial

institution. We understand that the EIB deploys most financial instruments, alongside certain

other selected financial institutions. The EIB can either invest directly in projects, or does so

via intermediary financial institutions.

The third level of the structure is formed by financial programmes and products that are

developed and marketed (as well as administered) by the financial institutions as explained

under level 2. Financial programmes usually hold a range of financial products. Financial

products must be understood as ‘financial facilities’ that are additional sources of investment

or guarantees.

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

104

Table 5-4 EU structure of financial mechanisms

Source: EIB interview July 2015, and “The Connecting Europe Facility & its Financial instruments, catalysts for infrastructure

financing”, presentation by Matthieu Bertrand, Unit Connecting Europe – Infrastructure Investment strategies, DG Mobility and

Transport, European Commission, at CEF Workshop in NL, Ede, 29th October 2014.

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

105

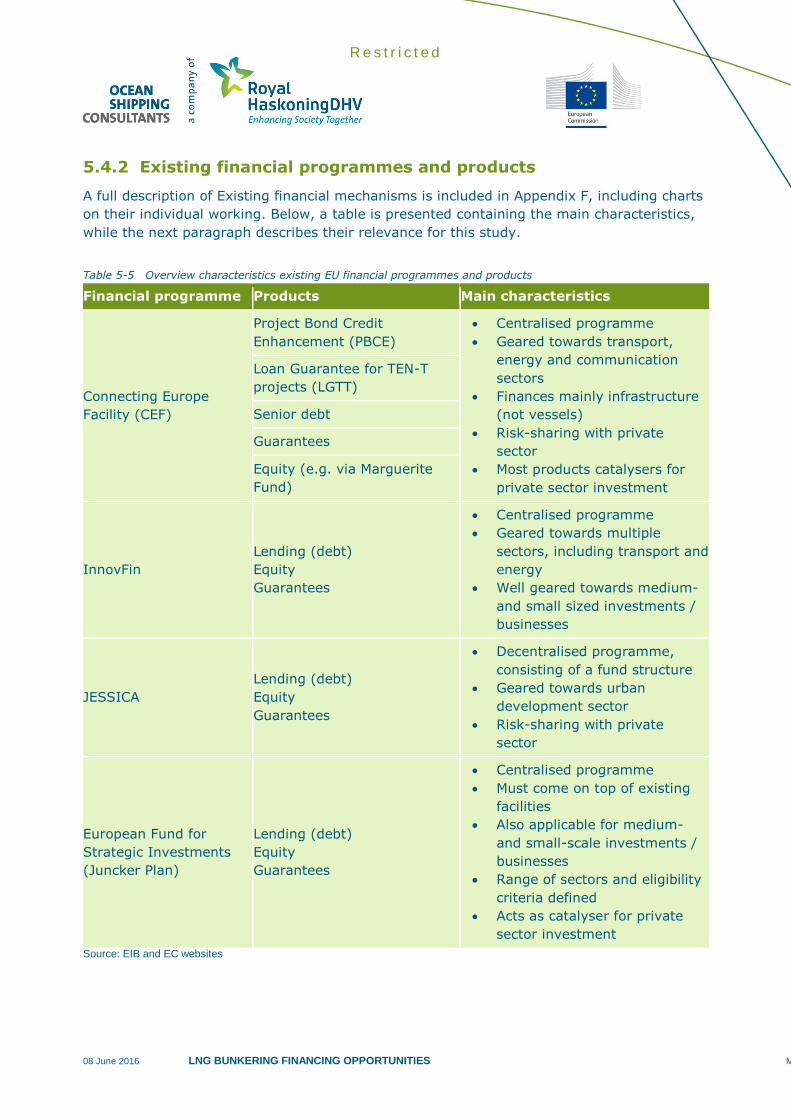

5.4.2 Existing financial programmes and products

A full description of Existing financial mechanisms is included in Appendix F, including charts

on their individual working. Below, a table is presented containing the main characteristics,

while the next paragraph describes their relevance for this study.

Table 5-5 Overview characteristics existing EU financial programmes and products

Financial programme Products Main characteristics

Connecting Europe

Facility (CEF)

Project Bond Credit

Enhancement (PBCE)

Centralised programme

Geared towards transport,

energy and communication

sectors

Finances mainly infrastructure

(not vessels)

Risk-sharing with private

sector

Most products catalysers for

private sector investment

Loan Guarantee for TEN-T

projects (LGTT)

Senior debt

Guarantees

Equity (e.g. via Marguerite

Fund)

InnovFin

Lending (debt)

Equity

Guarantees

Centralised programme

Geared towards multiple

sectors, including transport and

energy

Well geared towards medium-

and small sized investments /

businesses

JESSICA

Lending (debt)

Equity

Guarantees

Decentralised programme,

consisting of a fund structure

Geared towards urban

development sector

Risk-sharing with private

sector

European Fund for

Strategic Investments

(Juncker Plan)

Lending (debt)

Equity

Guarantees

Centralised programme

Must come on top of existing

facilities

Also applicable for medium-

and small-scale investments /

businesses

Range of sectors and eligibility

criteria defined

Acts as catalyser for private

sector investment

Source: EIB and EC websites

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

106

5.5 Relevance of the mechanisms for the sector for LNG as

marine fuel

Here, we elaborate on the relevance of the mechanisms described above for projects relating

to LNG as marine fuel. Whereas not all programmes and products described may seem

directly applicable to this sector, we believe there are relevant comparisons to be made.

The instruments and products under the Connecting Europe Facility (CEF) can directly be

applied to the projects for LNG bunkering facilities (supply side). The successful project bond

(PBCE) and loan guarantee (LGTT), but also senior debt and other forms of guarantees,

could be used to support projects for new LNG bunkering facilities. Based on our discussions

with market parties, equity seems less likely an option, as the parties indicate there is no

obvious need for more equity, and in addition, the EIB’s preferred options are debt and/or

guarantees, as providing equity could give rise to a conflict of interest.

We acknowledge that the InnovFin is not directly applicable to the LNG as marine fuel

sector (the sector is no longer deemed to be innovative / new technology), we do use it to

show that the way this programme is structured means there is a solution for programmes

of projects that involve both low CAPEX and high CAPEX projects. This is the case for the

LNG as marine fuel sector too: e.g. truck-to-ship solutions typically have a low CAPEX

requirement, whereas large LNG storage facilities require a big investment. The InnovFin

structure is flexible in providing corporate finance or project finance solutions fitting the

scope of the project at hand, which is a useful characteristic.

The purpose of introducing the JESSICA programme here (albeit that this was designed for

a different sector) lies in the fact that the programme is de-centrally managed (through

holding funds). In the LNG sector, we see that many countries have national schemes to

assist projects financially. If the EU’s assistance to projects is at least well aligned with the

national incentives, this will help the sector select the most appropriate financing options.

The newly created European Fund for Strategic Investments (EFSI) is directly relevant

for the LNG as marine fuel sector. Not only does EFSI financing come on top of other forms

of European (financial) support, also the LNG bunkering sector fits both the EC’s

requirements as well as the targeted areas. Therefore, the EFSI programme is well suited to

provide additional support for this sector. This is beneficial as the risks that cannot be

covered by commercial banks in this sector are significant. EFSI indeed allows the EIB to

offer products that absorb more risk than current products and enable investment in projects

with a higher risk and high added value.

5.6 An alternative solution: deferred equity

As we have established, one of the most pressing issues in financing bunkering facilities for

LNG is bridging the time gap between making the capital investment for the facility and the

sufficient availability of demand (and revenues). A similar gap also had to be bridged in

another project, in a different sector. We believe an interesting lesson can be learnt from

this experience. The box below elaborates on the solution for this project.

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

107

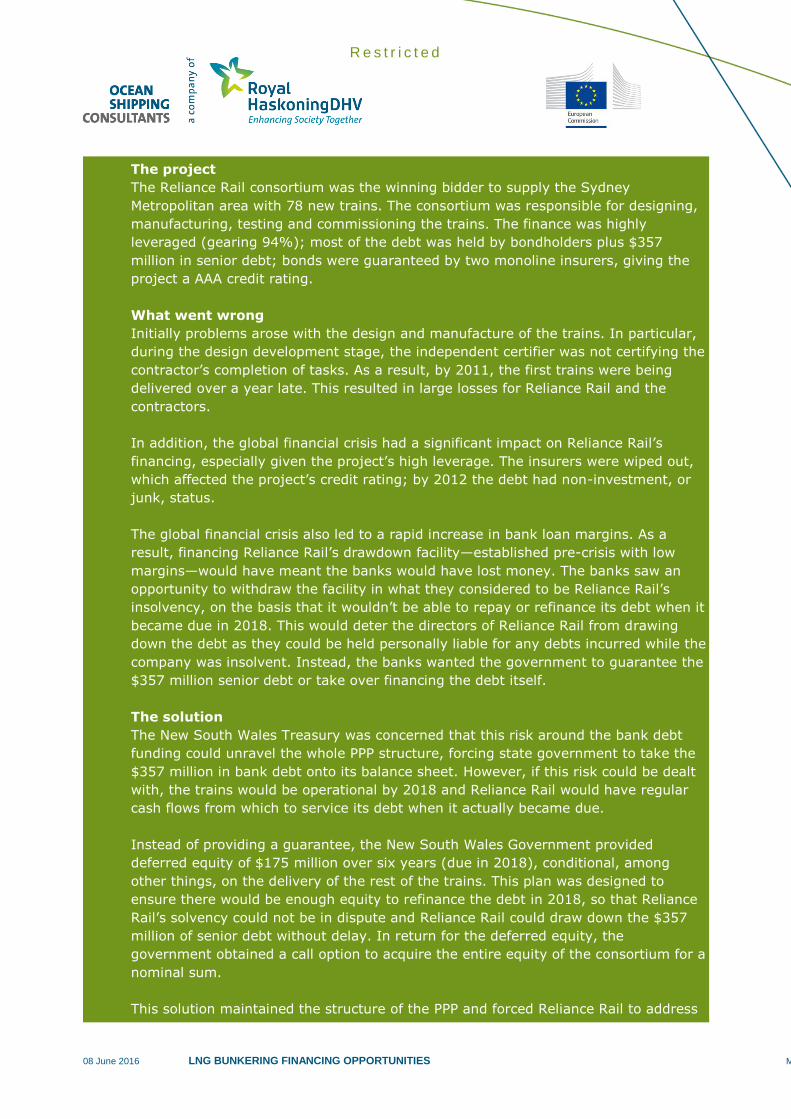

The project

The Reliance Rail consortium was the winning bidder to supply the Sydney

Metropolitan area with 78 new trains. The consortium was responsible for designing,

manufacturing, testing and commissioning the trains. The finance was highly

leveraged (gearing 94%); most of the debt was held by bondholders plus $357

million in senior debt; bonds were guaranteed by two monoline insurers, giving the

project a AAA credit rating.

What went wrong

Initially problems arose with the design and manufacture of the trains. In particular,

during the design development stage, the independent certifier was not certifying the

contractor’s completion of tasks. As a result, by 2011, the first trains were being

delivered over a year late. This resulted in large losses for Reliance Rail and the

contractors.

In addition, the global financial crisis had a significant impact on Reliance Rail’s

financing, especially given the project’s high leverage. The insurers were wiped out,

which affected the project’s credit rating; by 2012 the debt had non-investment, or

junk, status.

The global financial crisis also led to a rapid increase in bank loan margins. As a

result, financing Reliance Rail’s drawdown facility—established pre-crisis with low

margins—would have meant the banks would have lost money. The banks saw an

opportunity to withdraw the facility in what they considered to be Reliance Rail’s

insolvency, on the basis that it wouldn’t be able to repay or refinance its debt when it

became due in 2018. This would deter the directors of Reliance Rail from drawing

down the debt as they could be held personally liable for any debts incurred while the

company was insolvent. Instead, the banks wanted the government to guarantee the

$357 million senior debt or take over financing the debt itself.

The solution

The New South Wales Treasury was concerned that this risk around the bank debt

funding could unravel the whole PPP structure, forcing state government to take the

$357 million in bank debt onto its balance sheet. However, if this risk could be dealt

with, the trains would be operational by 2018 and Reliance Rail would have regular

cash flows from which to service its debt when it actually became due.

Instead of providing a guarantee, the New South Wales Government provided

deferred equity of $175 million over six years (due in 2018), conditional, among

other things, on the delivery of the rest of the trains. This plan was designed to

ensure there would be enough equity to refinance the debt in 2018, so that Reliance

Rail’s solvency could not be in dispute and Reliance Rail could draw down the $357

million of senior debt without delay. In return for the deferred equity, the

government obtained a call option to acquire the entire equity of the consortium for a

nominal sum.

This solution maintained the structure of the PPP and forced Reliance Rail to address

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

108

its management and manufacturing issues. Following the deferred equity

arrangement, many of the practical problems with manufacturing the trains were

resolved, and delivery rates began to improve. The final trains were delivered in

2014. As a result, the project will be able to generate a reliable payment stream

going forward, from which it can service its debt and deliver double-digit returns. This

means the government should have no difficulty in selling its deferred equity in

Reliance Rail in 2018, potentially at a profit, without ever having to provide the $175

million.

Obviously, the case of Reliance Rail is a different one from the case for LNG as a marine fuel,

one difference being the guaranteed off-take of the trains (once delivered). However, there

is also a striking similarity: a time gap between investment and revenue generation has to

be bridged, and the risk associated with this time gap is not acceptable for commercial

banks. In the case of LNG bunkering facilities, it is demand risk due to the uncertainty about

LNG demand taking off, in the case illustrated above it is the operational / technical risk of a

satisfactory delivery of the trains. In both cases, the government provides a safety net for

what the market perceives as the key risk in the project.

Providing a direct guarantee would have cost the NSW government $357 (on-balance sheet),

whereas the deferred equity option provided the consortium with sufficient guarantees to

draw down the necessary senior debt. Moreover, the public sector party gained a stake in

the company, providing it with a return when the project started to become profitable.

We understand that the EIB is hesitant to provide equity to projects in which they also

participate as a lender. However, in certain circumstances, in which a project can almost be

financed commercially, but needs additional reassurances to bridge the initial period of low

revenues, the provision of deferred equity (as shown in this example) can be an option.

5.7 Recommendation for characteristics for a financial

instrument for the sector for LNG as marine fuel

Summarising, we list our recommendations for the key characteristics for a financial

instrument for the sector for LNG as marine fuel.

From extensive discussions with private sector parties operating in this market, we

derive that the instrument should focus on the supply side infrastructure rather than

ship financing. These discussions included shipowners who highlighted that whether a

vessel had LNG capabilities or not, it did not impact on the ships’ bankability.

A suitable instrument should have the flexibility to offer a mix of (senior) debt,

guarantees and possibly project bonds, as well as potentially (deferred) equity.

The instrument must be flexible to finance both low and high CAPEX investments

(and provide solutions for both corporate finance and project finance).

The instrument must be able to be aligned with existing support measures by

national governments in the different member states.

The instrument must allow EFSI additional support for projects as the characteristics

of the sector are in line with EFSI’s targets.

R e s t r i c t e d

08 June 2016 LNG BUNKERING FINANCING OPPORTUNITIES M&WPB3039-103-100R001D11

109

The instrument should be able to bridge a time gap between the initial investment in

new infrastructure and the start of revenues for the project (when offtake starts).

This time gap is caused by the demand side waiting for the suppliers to move first15.

The instrument should be available cross-member states so that it benefits a grid

(network) of LNG bunkering facilities.

15