16

PT Pertamina ( Persero ) LNG Demand Outlook in Asia; Indonesia Outlook JCCP-15 24 July 2018- 1 August 2018

PT Pertamina (Persero)

LNG Demand Out look in Asia;Indonesia Out look

JCCP-1524 July 2018- 1 August 2018

2

South Asia, ASEAN and China will drive the LNG demand growth out to 2030

mtpa

2%

1%

13%

15%

-2%

10%

-8%

CAGR%

~95% LNG Demand Growth coming from China, India and ASEAN

5

6

93

65

(25)

72

(4)

Growth, mtpa

4.5% p.a.

1 Includes US, Canada and Mexico 2 Include Bangladesh, India and Pakistan

SOURCE: McKinsey Energy Insights, McKinsey Global Gas Model

102127

3744

2799

76

114

2211

455

2016

244

2030

North America1

China

Middle EastEurope

Japan Korea Taiwan

S. Asia2

ASEAN

2

15

619

LNG Outlook 2016-2030 , Million tonnes per annum (MTPA)

3

Contractual preferences have moved to shorter durations and smaller volumes; oil indexation remains prevalent outside the EU

Portfolio composition% of total LNG buyers

Key insights

• Buyers’ future preferences for long-term contracts are shifting to shorter duration andsmaller volumes, while DES contracting remains prevalent

• A straight preference for Henry Hub indexing has subsided vs. 1-2 years ago, in favor of hybrid formulas to better balance exposure

• Marked regional differences exist in a few dimensions:

‒ A preference for gas hub indexing is pervasive in Europe, in SE Asia oil linkage dominates

‒ Open tenders may prevail in M. East and S. America

SOURCE: McKinsey’s Energy Insights LNG buyer survey 2016

1 Includes NBP/TTF and Henry Hub

4

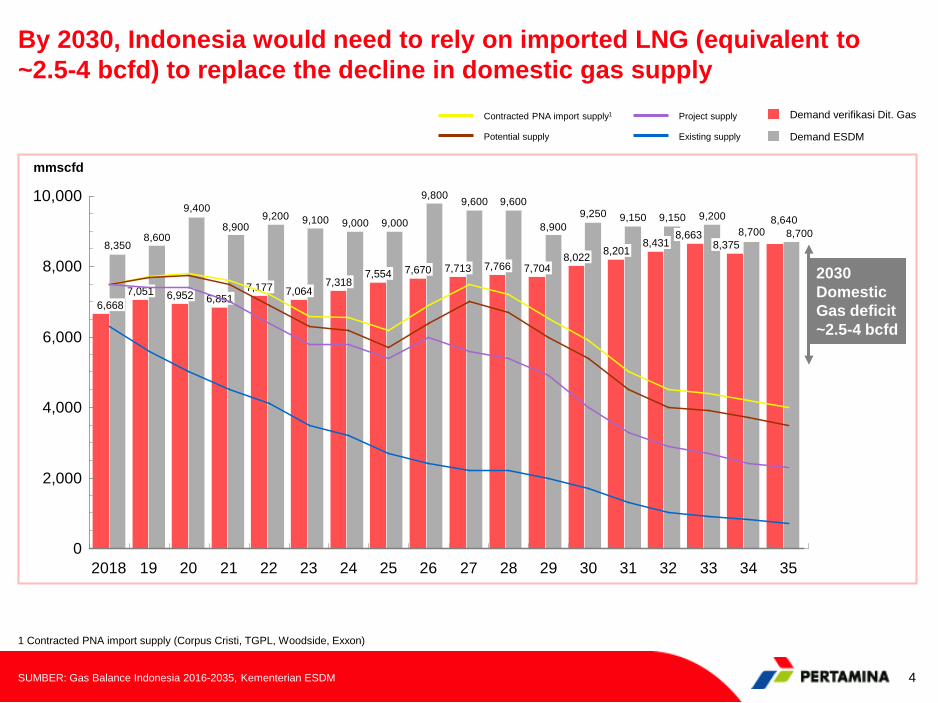

By 2030, Indonesia would need to rely on imported LNG (equivalent to ~2.5-4 bcfd) to replace the decline in domestic gas supply

Existing supply

Contracted PNA import supply1

Potential supply

Project supply

8,6408,7008,700

9,2009,1509,1509,2508,900

9,6009,6009,800

9,0009,0009,1009,2008,900

9,400

8,6008,350

7,713

8,3758,2018,431

8,663

8,0227,7047,7667,6707,554

6,8517,177

6,952 7,0647,0516,668

7,318

Demand ESDM

Demand verifikasi Dit. Gas

8,000

0

2,000

6,000

4,000

10,000

34 352421 30252220

mmscfd

31292018 32272619 2823 33

1 Contracted PNA import supply (Corpus Cristi, TGPL, Woodside, Exxon)

SUMBER: Gas Balance Indonesia 2016-2035, Kementerian ESDM

2030 Domestic Gas deficit ~2.5-4 bcfd

5

ASEAN countries are investing in new infrastructure development to anticipate this increase of LNG Demand

SOURCE: IEA, Enerdata

Myanmar

Thailand

Lao PDR

Cambodia

Malaysia

Vietnam

Philippines

Sumatra

Arun

FSRU Lampung

JawaTengah

FSRU Jawa Barat

Kalimantan

Lahad DatuBrunei

BatangasFSRU

Map Ta Phut*

Sulawesi

Timor Timur

LNG Regasification TerminalEksisting

Development

Planning

JurongIsland

AB

C

D

E F

H

I

J Bin Thuan

Thi VaiKL

VIV

II

ISingapura

PengerangGLekas

III

Trans pipelines

Regas Infrastructure

CapacityName

ABC

D

EFGH

I

KL

FSRU Jawa BaratFSRU Lampung

Arun (Aceh)

FSRU Jawa Tengah

Lekas (Malaca)

Lahad Datu (Sabah)Pengerang (Johor)

Batangas FSRU

Jurong Island

Ma Ta Phut

Thi Vai

Bin Thuan

3.03.0

3.0

3.0

3.8

0.83.8

4.0

9.0

10.0

1.0

10.0

mtpa bcm/y

4.14.1

4.1

4.1

5.2

1.15.2

5.5

12.2

13.8

1.4

13.8

Operated Year

20122015

2014

2020+

2013

On hold2018+

2020+

2013+

2011+

2020+

2020+

Pipeline Infrastructure

Connected Countries

IIIIIIVV

I Indonesia-Malaysia-SingapuraIndonesia (Sumatra)-SingapuraPerbatasan Myanmar-ThaiThailand-MalaysiaMalaysia-Vietnam

Capacity mmscfd

150/250350410/565750270/300

J

Owner

PertaminaPGN

Pertamina

Pertamina

Petronas

TBCPetronas

PNOC

SLNG

PTT

PV Gas

PV Gas

6

Pertamina is building a global LNG portfolio leveraging its capabilities (LNG infrastructure, commercial) and strong market position

Pertamina’s business model in LNG value chain

Business model

Core LNG operational and

commercial capabilities

Pure LNG Supply

LNG supply and Regas

infra

Integrated LNG to Power

Retail LNG

▪ Trusted LNG and Regas developer and operator

▪ Reputed LNG marketer

▪ Respected partner in LNG and Power value chain

▪ Building gas and power and Retail LNG business model

7

Pertamina has a comprehensive presence across the gas value chain

Sourcing and trading

Transmission and distri-bution

Pro-cessing

LNG Infra-structure Marketing

Pertamina Gas

Transportation of natural gas through pipeline network ~2,130 km of gas

pipelines Subsidiary in gas

trading business: Pertagas Niaga

PT PertaminaPower IndonesiaGas and NREpower plants

Gas, New & Renewable Energy

PT Badak (Bontang)LNG provider Kalimantan

Donggi Senoro (DS) LNG LNG provider Sulawesi

PT Nusantara RegasJV Co with PGN, operating floating storage facilities and regas terminals

PT Perta Daya GasLNG provider East

IndonesiaMini LNG storage and

regas

PT Perta Arun GasLNG receiving terminal and regasification

PT Perta Samtan GasLPG, NGL and CNG plant

Gas business

8

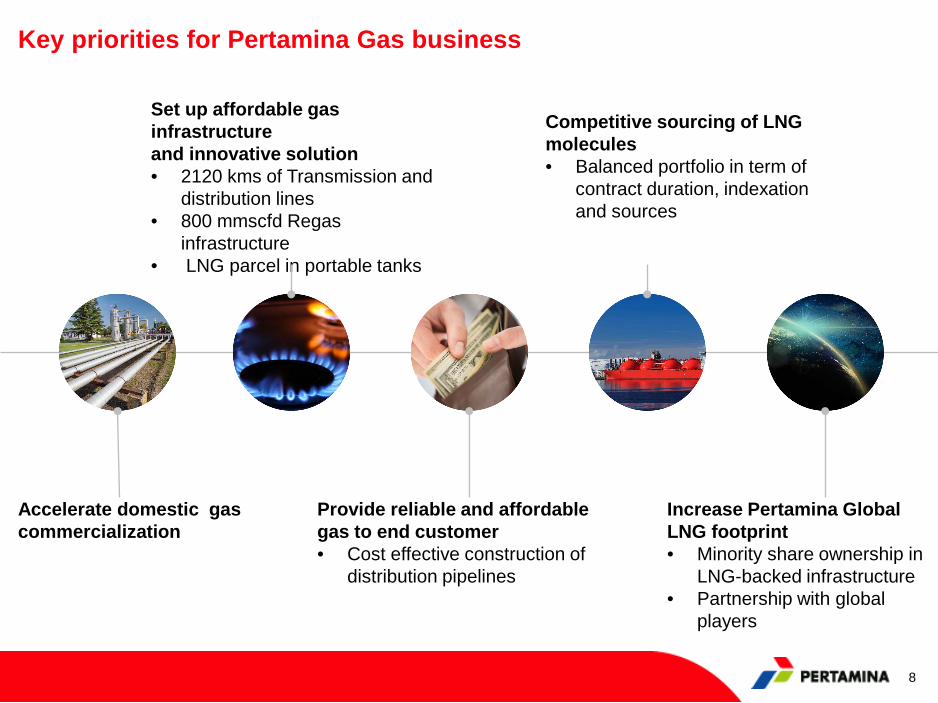

Key priorities for Pertamina Gas business

Set up affordable gas infrastructure and innovative solution• 2120 kms of Transmission and

distribution lines• 800 mmscfd Regas

infrastructure• LNG parcel in portable tanks

Competitive sourcing of LNG molecules• Balanced portfolio in term of

contract duration, indexation and sources

Provide reliable and affordable gas to end customer• Cost effective construction of

distribution pipelines

Accelerate domestic gas commercialization

Increase Pertamina Global LNG footprint• Minority share ownership in

LNG-backed infrastructure • Partnership with global

players

9

LNG dispenser

LNG for industry

LNG for mall/ hotel/apartment

LNG vertical gas liquid for promotion

LNG for workshop

LNG microbulk for hotel/restaurant/cafe

Shipping & other transportation

Source Transportation MarketBig - Medium Medium - Small

Rail transportation

Road transportation(trucking)

LNG for co-gen

Customer

Eastern Indonesia

Electricity

Pertamina is bringing LNG parcel in portable tank to the customer gate (virtual pipeline)

10

Pertamina has established itself as global LNG portfolio player

Source: Pertamina

LNG &Gas supply

LNG & Gas Offtakers

Pertamina as Global portfolio LNG player:• Secure long term LNG and Gas supply• LNG Spot trading, short term and long term• Taking calculated risks to deliver profit

Captive Refinery Demand

Electricity Demand

Domestic Industry

Existing International Buyers

Emerging LNG markets

International LNG Supply Domestic LNG Supply Domestic Pipelines Gas

Main challenges in the gas industry in Indonesia

2

4

5

Pipeline Gas• Limited long-term gas supply• Mismatch between supply-demand

locations• Field development timeline is not in line

with market needs• Field economics not compatible with

price regimes in domestic gas marketLNG• Long-term supply commitments must be

decided and finalized 4-5 years before delivery to ensure alignment with development of LNG infrastructure

• Inadequate infrastructure• Overlap in infrastructure

development: planning and utilization of infrastructure not optimized yet

• Complex land acquisition process

• Gas infrastructure master plan is not aligned with supply-demand profile

• Difficult to make long-term demand projections

• Anchor customers are more likely to be traditional consumers

• Demand is strongly influenced by:– Electricity supply plan by

PLN– Global prices (not

Indonesia-specific) for fertilizer

1

• Fixed price with annual escalation• Price indexation with the crude oil

price• Indexation of the product price

• Unavailability of gas/ LNG import policy in Indonesia• Currency exchange risks• Absence of fiscal incentives• Absence of regulations that will govern reasonable

margins

3

l 11

HUMAN CAPITAL DEVELOPMENT as A FUNDAMENTAL to SUPPORT GAS GROWTH IN PERTAMINA

MAN POWER STRENGTH (GAS DIVISION)

66.18%

33.82%

Staffing Status

OccupiedVacant

0

10

20

30

40

50

60

Commercial Engineering

51

39

2620

Occupied

Vacant

0

5

10

15

20

25

30

35

26-30 31-35 36-40 41-45 46-50 51 above

系列1

By Age

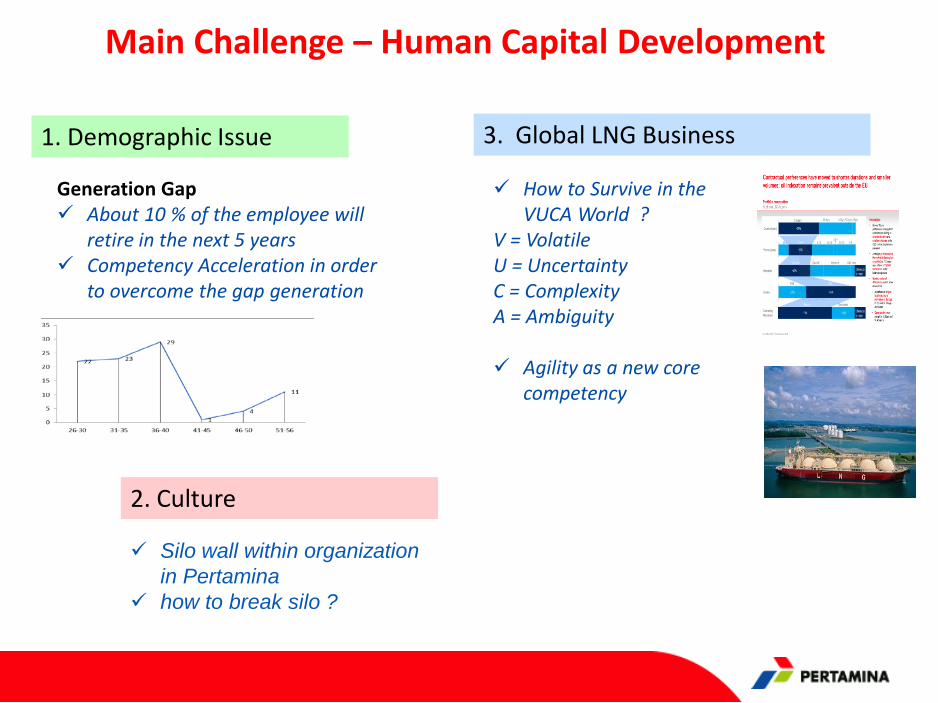

Main Challenge – Human Capital Development

1. Demographic Issue

2. Culture

3. Global LNG Business

Generation Gap About 10 % of the employee will

retire in the next 5 years Competency Acceleration in order

to overcome the gap generation

How to Survive in theVUCA World ?

V = Volatile U = Uncertainty C = ComplexityA = Ambiguity

Agility as a new corecompetency

Silo wall within organizationin Pertamina

how to break silo ?

ENTRY LEVEL

MID LEVEL

HIGH LEVEL

Talent Development Acceleration in Pertamina

General Skill

Technical Skill

Leadership Skill

Global Leadership

Technical Skill

Development Program

EPDP (Early Professional Developmet

Program)

LNG Global Venture Academy

People Leader Development Program

PGEDP (Pertamina Global Executive

Development Program)

2018年7月25日プレゼンの様子@JCCP