Page 1

LONDON INTERBANK OFFERED RATE Financial Markets & Instruments

2012

Jaime Arimany (FIN3560-01), Maxwell Rispoli (FIN3560-02)

Joshua Street (FIN3560-02), Matthew Vacaro (FIN3560-01)

Babson College

12/3/2012

Page 2

1

Executive Summary

The London Interbank Offered Rate (Libor) is considered the worldwide benchmark for

interest rates. Not only does this key bank interest rate impact major US indices, derivative

markets, and adjustable rate mortgages, but it also accounts for trillions of dollars in loans under

its influence. The Libor was officially recognized as a benchmark rate in 1989 because of the

increased activity in swap derivative and overnight trading. The Libor rate was becoming

progressively more popular with trading centers around the world that involved many different

currencies and markets. This ultimately inspired global markets to follow it as a guideline for

interest setting worldwide due to its collaborative and joint nature with banks in different

countries. Unfortunately, the Libor is considered fundamentally flawed by many- including

current US Federal Reserve Chairman Ben Bernanke- due to its manipulative nature and lack of

regulation1.

In running statistical analysis, we initially believed that the 6-month Treasury bill and the

6-month Libor would be highly correlated between 1990 to present day. Analysis showed that

both rates were highly correlated as a whole (R2 of 96.84%) throughout the years of 1989-2012.

In separating the data for the Libor rate into five year periods, correlation was not as strong

between the years 1995-1999 (R2 of 68.39%). This was most likely attributed to uncertainty in

the interest rate market and the introduction of the euro. For years 2005-2009, there was high

fluctuation in the correlation due to the Libor scandal in the midst of the financial crisis. The

initial hypothesis was correct in relation to the overall correlation, but the results for recent years

have not been as correlated as what they were before the financial crisis and Libor scandal.

1 Staff, and Agencies. "Ben Bernanke and Mervyn King Describe Libor Fixing as 'fraud'" The Guardian. Guardian

News and Media, 17 July 2012.

Page 3

2

Table of Contents

Executive Summary ........................................................................................................................ 1

History of Libor .............................................................................................................................. 3

The Scandal Begins......................................................................................................................... 6

The Aftermath ................................................................................................................................. 7

Statistical Analysis .......................................................................................................................... 9

Six Month Rates ........................................................................................................................ 10

Significant Observations ............................................................................................................... 10

1989-2012.................................................................................................................................. 10

1989-2008.................................................................................................................................. 11

1990-1994.................................................................................................................................. 11

1995-1999.................................................................................................................................. 12

2000-2004.................................................................................................................................. 14

2005-2009.................................................................................................................................. 14

Conclusion .................................................................................................................................... 16

References ..................................................................................................................................... 18

Appendix ....................................................................................................................................... 21

“I pledge my honor that I have neither received nor provided any unauthorized assistance

during the completion of this work.”

“The authors of this paper hereby give permission to Professor Michael Goldstein to distribute

this paper by hard copy, to put it on reserve at Horn Library at Babson College, or to post a

PDF version of this paper on the internet”.

Page 4

3

History of Libor

Known by many as “the Greek banker” who carried out syndicate financing from a new

merchant bank in London during the 1970s, Minos Zombanakis was a financial visionary whose

legacy will long outlive him.2 In 1969, Zombanakis established a branch of Manufacturers

Hannover in London, one of the first banks to operate in the Eurodollar syndicated loan market

that was beginning to gain momentum. He is credited with being one of the first to write a

Eurodollar syndicated loan because of his early deals, specifically the $80 million loan to the

Shaw of Iran.3 The loan to Iran’s central bank was followed by another loan to Italy for $200

million, whose terms became the standard for the industry. The loan to Italy was structured for

five years, with interest rates recalculating semi-annually at a 0.75% premium over a floating

rate that represents market conditions; this floating rate is what Zombanakis called the London

interbank offered rate. 4

The birth of the London interbank offered rate5 came as a necessary product of

combining two types of loans: Eurodollar loans and syndicated loans. The Eurodollar market

emerged in the 1960s as a way for corporate and sovereign borrowers to raise funds while

avoiding taxation and regulation. However, there was a demand for large loans in the Eurodollar

market, some much larger than any one bank would be willing to hold as a portion of their

portfolio. 6

In order to make a loan of this magnitude, a group of lenders had to form a syndicate

2 Eade, Philip. "Minos Zombanakis." Euromoney.358 (1999).

3 Zombanakis is often credited with being the inventor of Eurodollar syndicated loans because of how much he used

and advocated these instruments, even though they were used more than a year earlier by other bankers in Austria. 4 Ridley, Kirstin, and Huw Jones. "A Greek Banker Spills On The Early Days Of The LIBOR And His First Deal

With The Shah Of Iran." www.businessinsider.com. Business Insider, 8 Aug. 2012. 5 The London interbank offered rate can be referred to by a variety of names and abbreviations including Libor,

LIBOR, BBA Libor, BBALIBOR, and bbalibor. This paper will refer to it as Libor. 6 Taaffe, Ouida. "The Life and Good times of LIBOR." - Minos Zombanakis. IFS School of Finance, n.d.

Page 5

4

in which they all contribute funds to one sole borrower.7 Merging the Eurodollar loans and

syndicated loans created new issues that had not been necessary to consider before. To adjust for

changes in market conditions for these loans to be paid off over longer periods to multiple banks,

the interest rate on each loan had to be a floating rate with a premium over a generally accepted

rate that represents the cost of lending.8

Fourteen years after Zombanakis created Libor, global banking trends in 1984 were

characterized by increased trading of new products, such as interest rate swaps, foreign currency

options, and forward rate agreements. Further growth in this London interbank market would

have been inhibited without an element of standardization for these trades; the BBAIRS9 was

established in October of 1984, as a result. 10

Part of the BBAIRS included BBA Interest

Settlement rates, which were the immediate predecessor of the London Interbank Offered Rate.11

Libor has viewed as an industry standard since it was first calculated in 1986.

Libor rate data is available from various private data vendors, even though Thompson

Reuters calculates the rates. To calculate all the rates on London business days for ten different

currencies12

and fifteen borrowing periods13

, contributing banks send their interbank borrowing

rates to Thompson Reuters every day at 11:00AM. In the time before Thompson Reuters

distributes the data at noon, it receives all the data for each borrowing period from different

contributing banks, sorts the data from smallest to largest, removes the upper and lower quartile

7 "Syndicated Loan." Investopedia.com. Investopedia, n.d.

8 Eade, Philip. "Minos Zombanakis." Euromoney.358 (1999).

9 BBAIRS stands for the British Bankers Association Interest Rate Swaps, which acted as the predecessor of

LIBOR. 10

"BBA LIBOR - Frequently Asked Questions (FAQs)." BBA LIBOR. British Bankers Association. 11

"Interest Rate Swaps - Interest Rate, LIBOR Rates, Base Rates, Euribor Rates, Gilt Rates, Historic Rates and

Trends." Www.Swap-Rates.com. CLP Structured Finance, n.d. 12

The ten currencies that LIBOR rates are calculated for include: Pound Sterling (GBP), US Dollar (USD), Japanese

Yen (JPY), Swiss Frank (CHF), Canadian Dollar (CAD), Australian Dollar (AUD), Euro (EUR), Danish Kroner

(DKK), Swedish Krona (SEK), and New Zealand Dollar (NZD). 13

The fifteen borrowing periods range from overnight to one year.

Page 6

5

in an attempt to remove outliers, and finally calculates the mean on the remaining data. This

process, referred to as calculating a ‘shaved’ or ‘trimmed’ mean, is performed 150 times each

day (for the fifteen periods in each of the ten currencies). 14

After calculating, Thompson Reuters

distributes the Libor rates and the rates submitted by the contributing banks to data vendors who

make the information available worldwide.

The current Libor is quite different from when Zombanakis first calculated it over forty

years ago. Aside from the computational differences that come along with currently using a

trimmed mean for rates, Libor today is also notably different based on who uses the rates and for

what purpose. Libor rates are widely used as a benchmark for short-term interest rates and the

settlement of interest rate contracts.15

In addition to the syndicated loans that it was originally

designed for, Libor is used to gauge the cost of unsecured borrowing, as a basis for derivatives

trading, and as a basis for many different types of lending, such as commercial loans and

residential mortgages.16

When Libor was first created, contributing banks had little reason to manipulate the rates

that they were reporting; the potentially destroyed relationship within a syndicate was enough to

prevent the borrower from artificially adjusting the reported rates.17

Until recent years, few have

thought critically about how the Libor rates are being calculated and, more importantly, the

potential of contributing banks to manipulate the reported rates.

14

"BBA LIBOR - Frequently Asked Questions (FAQs)." BBA LIBOR. British Bankers Association, n.d. 15

"Interest Rate Swaps - Interest Rate, LIBOR Rates, Base Rates, Euribor Rates, Gilt Rates, Historic Rates and

Trends." Www.Swap-Rates.com. CLP Structured Finance, n.d. 16

"BBA LIBOR - Frequently Asked Questions (FAQs)." BBA LIBOR. British Bankers Association, n.d. 17

Ridley, Kirstin, and Huw Jones. "A Greek Banker Spills On The Early Days Of The LIBOR And His First Deal

With The Shah Of Iran." Business Insider, 8 Aug. 2012.

Page 7

6

The Scandal Begins

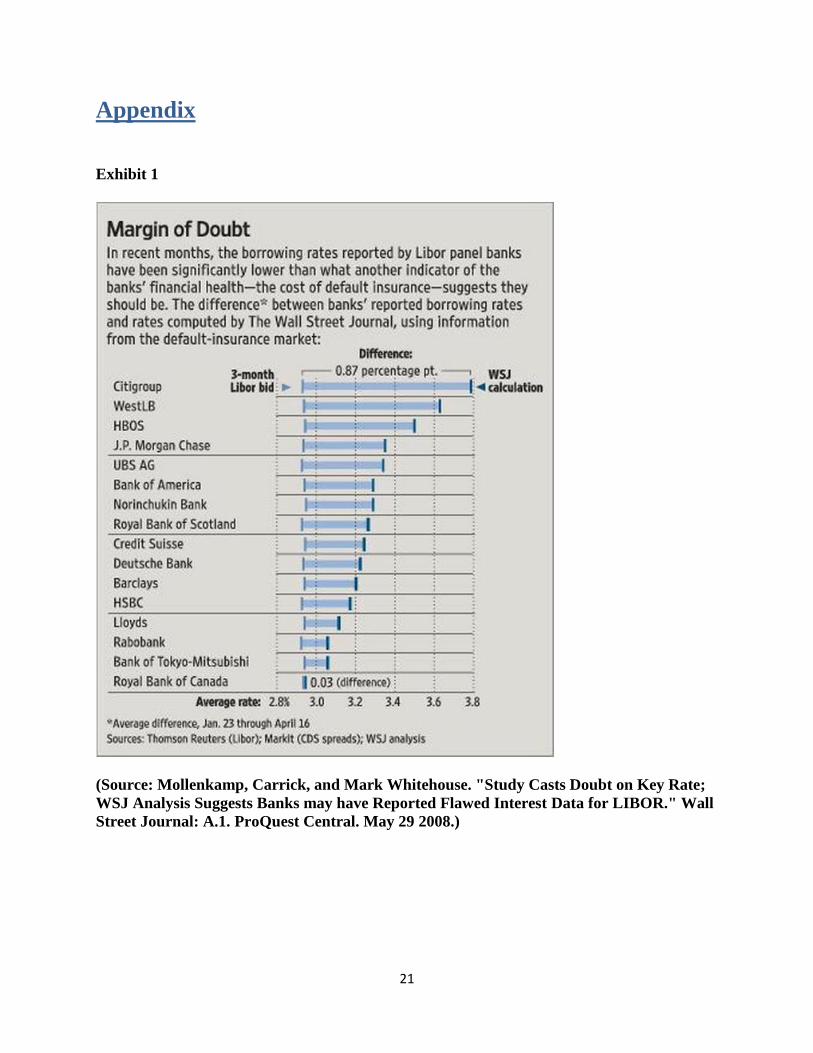

On May 29, 2008, the Wall Street Journal published a controversial article about a

handful of banks who “[had] been reporting significantly lower borrowing costs for the London

interbank offered rate, or Libor, than what another market measure suggests they should be.” The

Wall Street Journal article mentioned that the reported rates seemed unusually low, especially

since the cost of borrowing should have gone up during the financial crisis. One explanation for

this discrepancy is that banks were reporting lower rates to seem healthier and avoid appearing

desperate for cash. To further examine the suspicions about banks manipulating rates, the Wall

Street Journal performed its own analysis by comparing borrowing rates to the default-insurance

rates for any given contributing bank. As expected, these two variables moved together for the

most part, until January 2008. The cost of default-insurance increased as the possibility of bank

failures increased; however, the reported borrowing rates did not increase to reflect the stress

being experienced by various financial institutions.18

Seen in Exhibit 1, the difference in the cost

of default-insurance from borrowing costs is much larger for some of the banks that contribute to

Libor. Although the data analyzed by the Wall Street Journal suggests that some banks are

reporting lower borrowing costs than what other indicators say they should be, further

investigation from the BBA arrived at no such conclusions.

As discussed in the previous section, “The History of Libor,” daily bank submissions are

based on estimates and not actual trades. This calculation method can potentially entice banks to

collaborate amongst themselves to adjust the benchmark to a more favorable rate. On June 27,

2012, Barclays Bank was fined a total of $453 million for influencing the manipulation of the

Libor rate starting in 2005 when one Barclays’ trader told another member bank’s trader to raise

18

Mollenkamp, Carrick, and Mark Whitehouse. "Study Casts Doubt on Key Rate; WSJ Analysis Suggests Banks

may have Reported Flawed Interest Data for LIBOR." Wall Street Journal: A.1. ProQuest Central. May 29 2008.

Page 8

7

the three-month dollar Libor rate19

. According to a report by the Financial Service Authority

(FSA), a total of 257 requests were made by Barclay’s derivative traders to manipulate Libor and

Euribor rates20

. Further discussion on the specifics of legal actions taken against Barclay’s, and

on the scandal’s aftermath, can be found later in the next section.

In the eve of the financial crisis, Banks became increasingly speculative of other banks’

credit worthiness following the downfall of Northern Rock in September of 2007. In order to

alleviate inter-bank lending tension fueled by a spike in Libor rates, Barclay’s officials requested

member banks to submit low Libor estimates21

. The mentality behind these fraudulent decisions

revolve around the concept that a low Libor rate suggests that banks are confident on the ability

of others to pay back loans. The problem during this time was that increasingly high Libor rates

were attracting scrutiny from the media on the potential weakness of the financial system.

The Aftermath

It is easy to underestimate the colossal influence that the Libor rate has around the world.

To give some perspective on the matter, the total value of securities and loans affected by Libor

sum up to $800 trillion22

while the world’s gross domestic product circles around the $70

trillion23

mark. Libor has an effect on everything from financial institutions’ earnings to the

small loans and payments individual citizens make.

Andrew Lo, professor of finance at the Massachusetts Institute of Technology, said that

the Libor scandal “dwarfs by orders of magnitude any financial scams in the history of

19

The Barclays’ trader said “What’s up with ur guys 34.5 3m fix… tell him to get it up!” 20

"Timeline: Libor-fixing Scandal." BBC News. BBC, 26 Sept. 2012. 21

In December of 2007, a Barclay’s employee reached out to the New York Federal Reserve Bank to express his

concern that his bank was involved in Libor rate-fixing. 22

Fernandez, Tommy. "Libor Pains: What's the Impact?" Money Management Executive 20.32 (2012):

1,n/a. ProQuest Central.Web. 2 Dec. 2012. 23

"Focus: World GDP." The Economist. The Economist Newspaper, n.d. Web. 25 Nov. 2012.

Page 9

8

markets”24

. These manipulations had a universal influence and directly affected pensions, mutual

funds, derivative markets, currencies, adjustable rate mortgages and other financial institutions,

government agencies, and individuals who are influenced by fluctuations of the cost of debt.

Due to the massive discrepancies caused by the Libor scandal, the CFTC “[required]

Barclays to pay a $200 million civil monetary penalty, cease and desist from further violations as

charged, and take specified steps, such as making the determinations of benchmark submissions

transaction-focused (as set forth in the Order), to ensure the integrity and reliability of its Libor

and Euribor submissions and improve related internal controls”25

. These manipulations caused a

complex web of legal actions that are still far from being settled. Vast arrays of companies and

government agencies, such as the California Public Employees’ Retirement System (CalPERS),

have started investigating whether or not they lost money from causes related to Libor rate

manipulation. Other entities, such as the New York Nassau Country have already come forward

saying that a total of $13 million in losses were attributed to these manipulations26

.

The scandal has critically damaged both investor and public confidence in the financial

system. On September 11, 2012, The Times of London reported that “central banks around the

world are establishing a group to monitor the reform of Libor”27

in the scandals aftermath,

although no further details on the specifics have been revealed. In order to restore confidence in

the system, new regulations have to be set in place that specifically addresses the system’s

24

Farrel, Maureen. "Explaining the Libor Interest Rate Mess." CNNMoney. Cable News Network, 03 July 2012 25

"RELEASE: Pr6289-12." CFTC Orders Barclays to Pay $200 Million Penalty for Attempted Manipulation of and

False Reporting concerning Libor and Euribor Benchmark Interest Rates. U.S. Commodity Futures Trading

Commission, 27 June 2012. 26

Grovum, Jake. "More States Dig into Libor Scandal." McClatchy - Tribune News ServiceProQuest Central. Nov

29 2012. Web. 2 Dec. 2012 . 27

Roberts, William. "Report: Central Bankers Form Committee to Monitor Interbank Reform." SNL European

Financials Daily(2012)ProQuest Central. Web. 2 Dec. 2012.

Page 10

9

fundamental flaws. In the future, the estimated rates that banks submit as contributions to the

calculation of Libor will have to be backed up by actual transaction data28

.

Statistical Analysis

In conducting analysis on Libor and Treasury rates, all of the elements used to determine

an interest rate need to be considered. An interest rate can be determined using the following

equation:

iJ*= f( IP , RIR , DRPj , LRPj , SCPj , MPj )

Where

iJ* = Fair Interest Rate on an individual (jth) security

IP = Inflation Premium

RIR = Real Interest Rate

DRPj = Default risk premium on the jth security

LRPj = Liquidity risk premium on the jth security

SCPj = Special feature premium on the jth security

MPj = Maturity premium on the jth security

This equation is used by many banks, governments, and corporations when determining

what interest rate to charge, including the premium above the assumed inflation and real interest

rates, to a potential borrower. However, there are situations where some of these variables may

not need to be taken into consideration when determining an interest rate. This can be

particularly noticed in the determination of Treasury bills. Treasury bills are noted as being

default risk free, meaning that there is a very little chance that they will default due to the US

Treasury’s ability to print more money or increase taxes 29

. The ability for the US Treasury to be

able to have this control and power allows the rates of their interest rates to be determined

without taking into consideration a default risk premium. A bank, on the other hand, does not

28

Reece, Rhodri. "Getting Libor Back on the Path to Righteousness." Financial Adviser (2012): n/a. ProQuest

Central. Web. 2 Dec. 2012. 29

Saunders, Anthony, and Marcia M. Cornett. Financial Markets and Institutions: A Modern Perspective. 5th ed.

N.p.: Irwin/McGraw-Hill, 2012. Print.

Page 11

10

have the ability to print money or tax its customers, which gives banks a reason to charge a

default risk premium based on an idea that there is a possibility that they will not be able to be

completely compensated for their investments. The Treasury bill rate seemed like a good

benchmark towards the Libor because it was the minimum rate that people would get back for

investing their money.

Six Month Rates

For this analysis, the use of the 6 month Treasury and 6 month Libor rate will be used.

These two rates have been selected for several reasons. One of the most significant is that there

was no data on the 1 month Treasury bill rate during the 1990s.30

The shortest duration and

maturity in the US Treasury market was instead a 3 month rate. Since this was the shortest, it

was also the most susceptible to short term volatility. Therefore, when selecting data for all of

the points, it was imperative that the credit risk premium was not the highest, lending to the

rationale that the 6 month rate was the best. Given the data from both the Treasury and the BBA,

the 6 month rate was the most readily available and reasonable to use considering the risks to

interest rates discussed previously.

Significant Observations

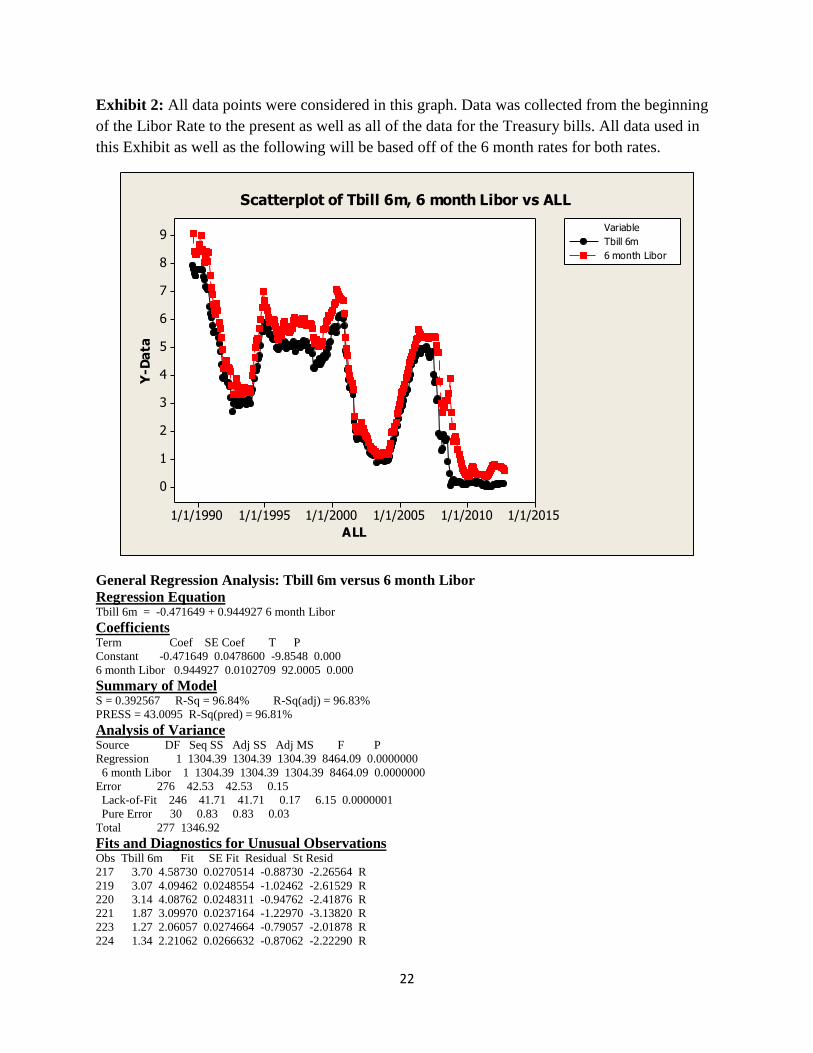

1989-2012

Since the inception of the Libor rate, the correlation to the US Treasury bill has been very

highly correlated. While viewing the data as a whole, over the last twenty-two years the two rates

have remained highly correlated as was observed in the regression model created in Exhibit 2 .

Over the entire life time of the Libor rate, the regression model calculated that the R2 value was

30

http://www.Treasury.gov/resource-center/data-chart-center/interest-

rates/Pages/TextView.aspx?data=yieldYear&year=2001

Page 12

11

extremely high with a value of 96.84% (Exhibit 2). As a generally accepted principle, R2 values

above 0.9 represent a very strong correlation31

. This correlation is also based off of 275 data

points for each rate, giving the analysis a statistically significant amount of points to consider.

However, it is not perfect and when examining the output, fifteen points in close proximity to

each other have been noted by the program as being outliers. These outliers are stated as

‘unusual observations,’ which means that they have standard deviations above 2.0 (Exhibit 2).

These outliers begin to occur in late 2007, perhaps right at the peak of the market bubble before

the collapse of the financial markets in the following year (Exhibit 2). The ‘unusual

observations’ continue all the way through the crisis to 2009, which could indicate that there was

something outside of the normal trend that impacted one of the two rates. The cause of this is

very likely to be that of the Libor Scandal.

1989-2008

Additionally, it can be observed that the correlation rises after removing the data points

where the unusual observations begin. The increase is only incremental, but the rise by 173 basis

points (bps) indicates that this new range, which removed the most recent four years, in fact did

alter the outcome of the regression model (Exhibit 3). By removing data from the tail of this

collection range, the steep drop off is not shown32

which occurred when the financial markets

collapsed.

1990-1994

In this section, the correlation between these two rates for the years of 1990 to 1994 was

very high. According to the analysis, which is noted in Exhibit 4, there was R² of 98.69%, and a

31

"Biz/ed - Correlation Explained [TimeWeb] | Biz/ed." Biz/ed - Correlation Explained [TimeWeb] | Biz/ed. N.p., 2

Nov. 2002. 32

Data sans 07 on

Page 13

12

P-value of 0.000 for this regression model. These strong results show that there is a very large

correlation between these two rates for these years. This is imperative to note because the

Treasury bill, being default risk free, and the Libor, being an arithmetic mean of the interest rates

that banks would pay to borrow money, show that the interest rates are determined in relation to

each other and the high correlation would show that the countries involved in the Libor were not

seeing too much additional risk in their investments during the majority of these years. The mean

of the spread was comparatively low at 0.7011%, which shows that the average difference

between the Libor and Treasury Bill 6 month rates were about 70bps, within a standard deviation

of about 26bps (Exhibit 5).

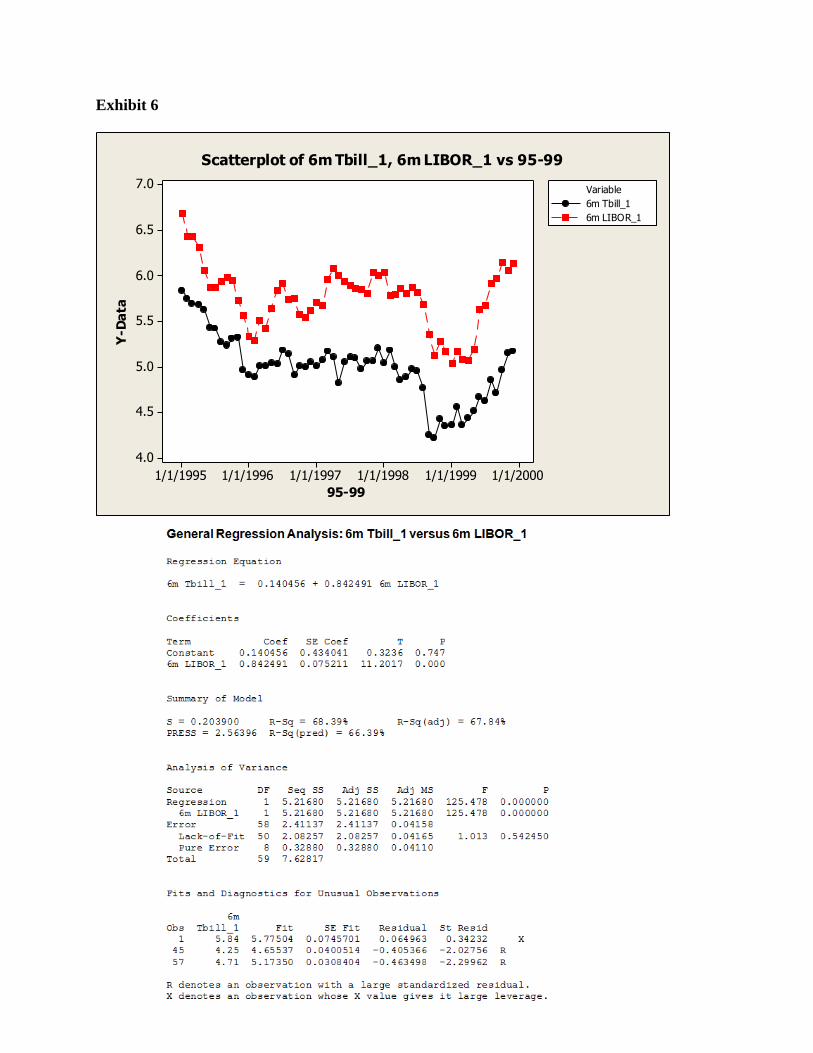

1995-1999

In comparing these two rates for the years of 1995 to 1999, we noticed that there was a

notable weaker correlation. As seen in Exhibit 6, there was an R² of 68.39%, which statistically

speaking is only moderately correlated. The regression model for these years yielded outcomes

where the spread was further apart than in the previous years, as noted in Exhibit 7 where the

spread had a mean of 0.7669 and standard deviation of 0.2097; however, the P-value remained

strong at 0.000. It is also important to note that even though the regression for this model was not

as strong than from 1990-1994, the graphs of both the Treasury bill and Libor Rates still make

the same basic curves and follow the same overall trends (Exhibit 4). In examining the results

further, we noticed that the spread between these rates at this time were larger, which was most

likely because of a number of events that were happening in the market at this time. In 1995,

there was uncertainty about the interest rate market earlier that year due to the unrest in the

Page 14

13

future and direction of the economy33

. In 1998, the Yen was losing value due to the Russian

Financial Crisis and Pakistan’s nuclear tests, which ultimately inspired people to takeout their

currency investments in the Yen and reallocate them to other, more secure currencies. During

this time the Yen dropped to 138.55 Yen per 1 USD, and ultimately caused investors to switch

back into investing in US dollar, which was the more secure currency34

. The effect of many

people withdrawing their currency investments could cause problems, especially in relation to

the Libor rate, which is primarily used for swap and future rates. The rapid depreciation of a

currency and the influx of withdrawn investments in the banks could have created additional risk

for any futures or derivatives for the banks in Japan, which also relay interest rate quotes to the

BBA. Also, another big event that was happening at this time was the introduction of the Euro at

the end of the decade. With uncertainty as to how the Euro would pan out in the future, both the

short and long-term the interest rates were higher than what they thought they should have been.

This uncertainty could have been a major cause in the added risk premiums on the European

interest rates.35

The lack of correlation between the Treasury bill and the Libor rates could have

been caused by this transition because the added uncertainty increased risk premiums and banks

were less willing to lend out or swap money due to the potential rise or fall of the currency’s

transition. Because of this dramatic change of the times the correlation between Libor and the

Treasuries fell. Had none of these dramatic currency revolutions occurred it is very likely that the

two rates would have remained highly correlated.

33

Pesek, William,Jr, and Xander Mellish. "Treasurys Finish Narrowly Mixed as the Dollar Remains the Focus in

Lieu of Other Indicators." Wall Street Journal: 0. 34

SHEEL KOHLI, in L. "US Trade Relations Tested as Japan Warns of Strict Measures to Stem Currency's Fall

Nuclear Fallout Hurts Yen." South China Morning Post: 1. 35

Hamour, Elwaleed A. "Initial Implications of the Introduction of the European Common Currency "The Euro" for

the Economies of the OIC Countries. www.sesric.org. Journal of Economic Cooperation, 21 Jan. 2000.

Page 15

14

2000-2004

Here it can again be observed that there is a significantly high correlation at an almost

perfect R2 value. During this time period the USA and the UK

36 were experiencing the

developments of globalization as well as the collapse of the Dot com bubble37

. During these

years both the Libor rate and the US Treasuries followed a similar pattern downward followed

by an upward trend towards the later time frame of this data (Exhibit 8). The following result of

the two rates being so close to each other created an R2 of 99.07%. With 60 data points, this

analysis still provides a strong enough pool of data to find statistically significant results (Exhibit

8). This recessionary time helps to highlight how the two rates behave. As can be seen through

the statistical analysis the two perform hand in hand when economic times are bad and as seen

previously they also preform closely when times are good.

2005-2009

Leading up to the financial collapse the data begins to stray from the previously high and

significantly high correlations. While the correlation remains strong it is visibly apparent that the

two rates begin to find different trend lines and as the fall in rates begins in late 2007 for both

Libor and the Treasury38

(Exhibit 10). However, by mid-2007 the spread between the two rates

widened dramatically. With spreads for the past 6 years standing around 41bps on average, after

mid-2007, spreads increased to highs of 343bps (Exhibit 9). The decoupling of these two rates

can be explained by several factors. As it is now known, several banks that reported to the BBA

were not stating the true costs of borrowing but at the time there was a great variety of

explanations that also made sense. Some of these often consisted of stating that the risk of

36

"Dot.Com to Dot.Bomb." BBC News. BBC, 15 Dec. 2000.

Madslien, Jorn. "Dotcom Bubble Burst: 10 Years on." BBC News. BBC, 03 Sept. 2010. 37

"The Dot-Com Bubble Bursts." The New York Times. The New York Times, 24 Dec. 2000. 38

Finch, Gavin, and Anna Rascouet. "- Bloomberg." - Bloomberg. N.p., 14 Apr. 2009.

Page 16

15

default increased the Libor rates39

, or for liquidity risk premiums needed be added, but compared

to the previous years of Libor, this did not fall in line with other recessionary trends. There was

also speculation that Libor was being altered by quantitative easing efforts from the central

banks40

. By 2008 several news wires and investigative journalists began to dive into why the

Libor rate was so far from its historic correlations with the treasuries as well as its previous

trends. Despite extensive research, it was still quite apparent that there was no clear answer and

that journalists were still guessing; this statement comparing Libor and a newer similarly

structured New York equivalent shows that it was not clear, “The BBA’s Libor rate has some

advantages over this newer rate. For one, it is more transparent, whereas the New York rate is

anonymous”41

. On the other hand, as some did indicate in 2008, there were signs that the Libor

was being toyed with and evidence of several trading desks looking for other rates to calculate

interest rates with became apparent in the Wall Street Journal article by Mark Whitehouse. In

this now famous but at the time controversial article, Whitehouse claimed that BBA reporting

banks were lowballing their rates to appear less desperate for cash than they actually were. In

this report, the comparisons between Libor and default insurance rates were analyzed showing

that the two had historically diverged when economic crises were occurring however Libor had

not behaved the same way as its historic trends42

. It can be noted that in the years prior to 2007

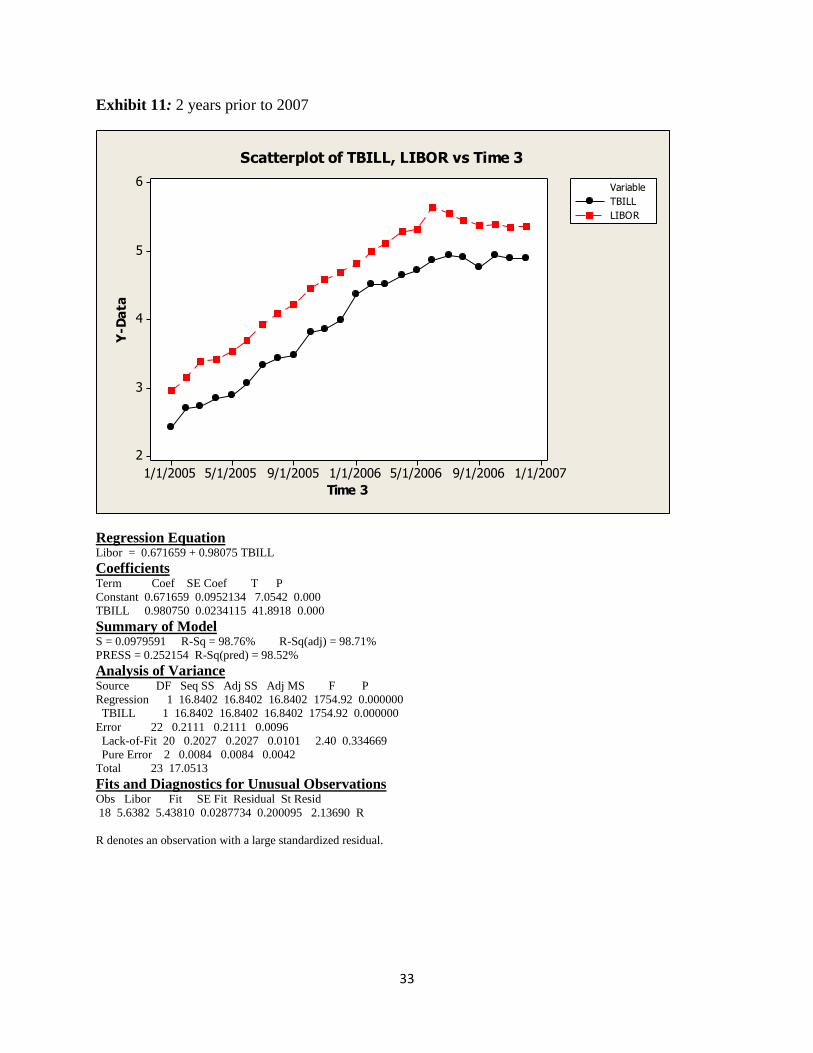

the correlation was very similar to what it had been previously, i.e. 2005-2007 holds an R2 value

of 98.76% (Exhibit 11). Additionally, the 5 years leading up to 2008 represent an R2 value of

96.70%, which is also statistically speaking very high and significant considering the number of

39

Michaud, François-Louis, and Christian Upper. "What Drives Interbank Rates? Evidence from the Libor

Panel." What Drives Interbank Rates? Evidence from the Libor Panel. N.p., 3 Mar. 2008. 40

Smith, Yves. "Are Central Banks Making Libor WORSE?" Naked Capitalism RSS. N.p., 11 Oct. 2008. 41

Gaffen, David. "Libor, Damned Libor, and Statistics." MarketBeat RSS. N.p., 18 Sept. 2008. 42

Mollenkamp, Carrick, and Mark Whitehouse. "Study Casts Doubt on Key Rate; WSJ Analysis Suggests Banks

may have Reported Flawed Interest Data for Libor." Wall Street Journal: A.1.

Page 17

16

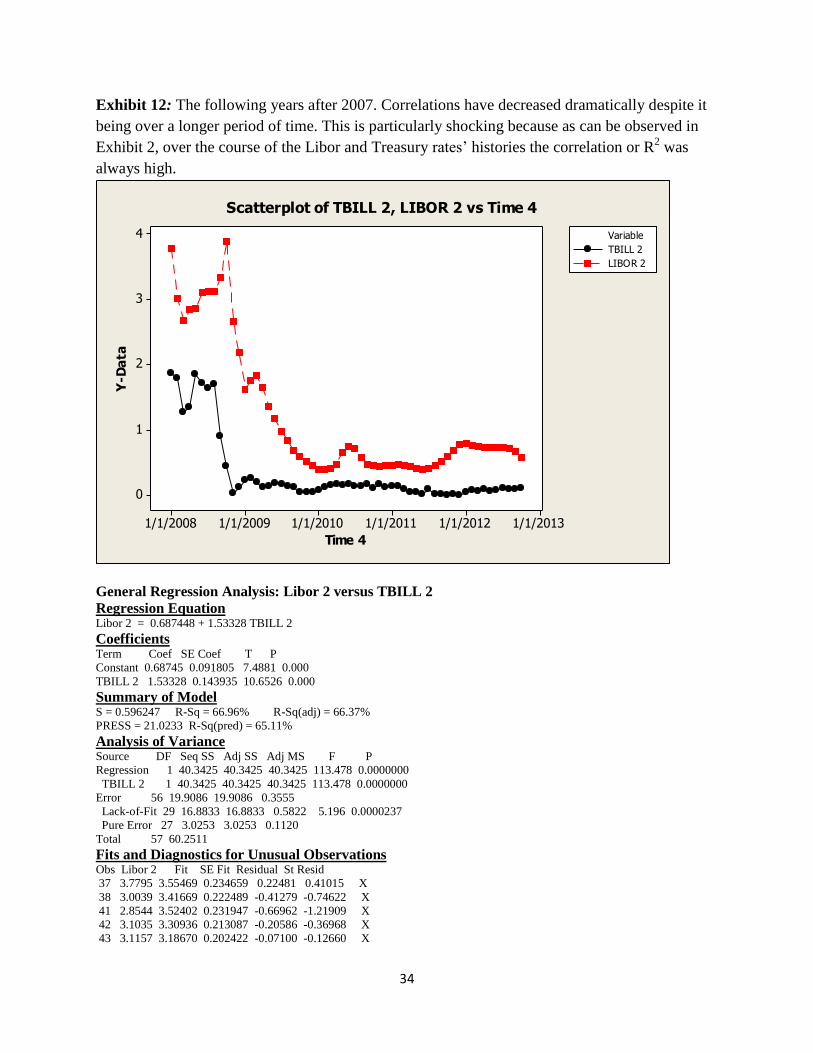

points observed (Exhibit 13). However, past 2007 and into 2008 through the present, the Libor

and the Treasuries diverged significantly; the ensuing R2 valued dropped to 66.96% from the

year 2008 to the present. Again, as compared to the previous years, this trend is dramatically

different from the one that was once observed by traders and the financial markets (Exhibit 12).

Over the course of any other 5 year period the Libor and the Treasury rates rose and fell at the

same pace, keeping high correlations to each other.

Conclusion

Over the past 22 years, the Libor and the Treasury rates have performed in tandem with

each other. The high statistical correlations during the boom and bust cycles have traditionally

remained very high giving credence to the argument that the two would perform similarly well

into the future. However, as it was seen through the analysis, the Libor rate had diverged

significantly from its previous correlations. The hypothesis that the two rates were highly

correlated remains true but only when the rates to the BBA are reported truthfully and honestly

and when there is a reasonable level certainty unlike during the late 1990s currency upheaval.

The divergence of the Libor rate during the scandal during the most recent financial crisis

therefore clearly showed that the rates were being tampered with. With both hindsight and

statistical analysis it is clear that the banks had acted in a collusive way that would prevent the

world from truly understanding how bad they were doing in during the financial crisis of 2008.

From the analysis, it is clear that the US Treasury was a good benchmark to use when examining

the Libor rate. However, in light of recent events, the comparison may no longer hold the same

significance or weight as previous understood. Until further regulation and policies are adopted

the BBA’s Libor rate cannot be fully trusted. We would adamantly state that until all of the

BBA’s reporting banks are closely examined, investors should be cautious of using this rate. But

Page 18

17

just as in many things, when there is a will to find shortcuts there will be both a way and

someone looking to exploit it.

Page 19

18

References _________________________________

"Banking Overview;British Bankers' Association." The Times: 1. Jan 23 1995. ProQuest

Central. Web. 27 Nov. 2012 .

"BBA Libor - The Basics." BbaLibor.com. BBA Libor, n.d. Web. 29 Nov. 2012.

<http://www.bbaLibor.com/bbaLibor-explained/the-basics>.

"Biz/ed - Correlation Explained [TimeWeb] | Biz/ed." Biz/ed - Correlation Explained

[TimeWeb] | Biz/ed. N.p., 2 Nov. 2002. Web. 02 Dec. 2012.

<http://www.bized.co.uk/timeweb/crunching/crunch_relate_expl.htm>.

"Dot.Com to Dot.Bomb." BBC News. BBC, 15 Dec. 2000. Web. 01 Dec. 2012.

<http://news.bbc.co.uk/2/hi/in_depth/business/2000/review/1069169.stm>.

Eade, Philip. "Minos Zombanakis." Euromoney.358 (1999): 24-. ProQuest Central. Web. 27

Nov. 2012. <http://search.proquest.com.ezproxy.babson.edu/docview/198853343>

Farrel, Maureen. "Explaining the Libor Interest Rate Mess." CNNMoney. Cable News Network,

03 July 2012. Web. 30 Nov. 2012. <http://money.cnn.com/2012/07/03/investing/Libor-

interest-rate-faq/index.htm>.

Finch, Gavin, and Anna Rascouet. "- Bloomberg." - Bloomberg. N.p., 14 Apr. 2009. Web. 01

Dec. 2012. http://www.bloomberg.com/apps/news?pid=newsarchive

Gaffen, David. "Libor, Damned Libor, and Statistics." MarketBeat RSS. N.p., 18 Sept. 2008.

Web. 01 Dec. 2012. <http://blogs.wsj.com/marketbeat/2008/09/18/Libor-damned-Libor-

and-statistics/>.

Hamour, Elwaleed A. "Initial Implications of the Introduction of the European Common

Currency "The Euro" for the Economies of the OIC Countries."Http://www.sesric.org/.

Journal of Economic Cooperation, 21 Jan. 2000. Web. 29 Nov. 2012.

<http://www.sesric.org/files/article/182.pdf >.

John Authers, Investment Editor. "Libor Rates." FT.com (2008): 1. ProQuest Central. Web. 27

Nov. 2012. <http://search.proquest.com.ezproxy.babson.edu/docview/229118837>

Madslien, Jorn. "Dotcom Bubble Burst: 10 Years on." BBC News. BBC, 03 Sept. 2010. Web. 01

Dec. 2012. <http://news.bbc.co.uk/2/hi/business/8558257.stm>.

Michaud, François-Louis, and Christian Upper. "What Drives Interbank Rates? Evidence from

the Libor Panel." What Drives Interbank Rates? Evidence from the Libor Panel. N.p., 3

Mar. 2008. Web. 01 Dec. 2012. <http://www.bis.org/publ/qtrpdf/r_qt0803f.htm>.

Page 20

19

Mollenkamp, Carrick, and Mark Whitehouse. "Study Casts Doubt on Key Rate; WSJ Analysis

Suggests Banks may have Reported Flawed Interest Data for Libor." Wall Street Journal:

A.1. ProQuest Central. May 29 2008. Web. 1 Dec. 2012 .

Pesek, William,Jr, and Xander Mellish. "Treasurys Finish Narrowly Mixed as the Dollar

Remains the Focus in Lieu of Other Indicators." Wall Street Journal: 0. ProQuest

Central. Mar 24 1995. Web. 1 Dec. 2012 .

http://search.proquest.com.ezproxy.babson.edu/docview/398451963/13AB01D89DA23D

7CACF/2?accountid=36796

"RELEASE: Pr6289-12." CFTC Orders Barclays to Pay $200 Million Penalty for Attempted

Manipulation of and False Reporting concerning LIBOR and Euribor Benchmark Interest

Rates. U.S. Commodity Futures Trading Commission, 27 June 2012. Web. 30 Nov. 2012.

<http://www.cftc.gov/PressRoom/PressReleases/pr6289-12>.

Ridley, Kirstin, and Huw Jones. "A Greek Banker Spills On The Early Days Of The Libor And

His First Deal With The Shah Of Iran." Www.BusinessInsider.com. Business Insider, 8

Aug. 2012. Web. 27 Nov. 2012. <http://www.businessinsider.com/history-of-the-Libor-

rate-2012-8>.

Saunders, Anthony, and Marcia M. Cornett. Financial Markets and Institutions: A Modern

Perspective. 5th ed. N.p.: Irwin/McGraw-Hill, 2012. Print.

SHEEL KOHLI, in L. "US Trade Relations Tested as Japan Warns of Strict Measures to Stem

Currency's Fall Nuclear Fallout Hurts Yen." South China Morning Post: 1. ProQuest

Central. May 30 1998. Web. 1 Dec. 2012 .

http://search.proquest.com.ezproxy.babson.edu/docview/265436666/13AB26E55FD7DD

CDE8B/3?accountid=36796

Smith, Yves. "Are Central Banks Making Libor WORSE?" Naked Capitalism RSS. N.p., 11 Oct.

2008. Web. 01 Dec. 2012. <http://www.nakedcapitalism.com/2008/10/are-central-banks-

making-Libor-worse.html>.

Staff, and Agencies. "Ben Bernanke and Mervyn King Describe Libor Fixing as 'fraud'" The

Guardian. Guardian News and Media, 17 July 2012. Web. 02 Dec. 2012.

<http://www.guardian.co.uk/business/2012/jul/17/federal-reserve-ben-bernanke>.

"Syndicated Loan." Investopedia.com. Investopedia, n.d. Web. 29 Nov. 2012.

<http://www.investopedia.com/terms/s/syndicatedloan.asp>.

Taaffe, Ouida. "The Life and Good times of Libor." - Minos Zombanakis. IFS School of Finance,

n.d. Web. 29 Nov. 2012.

<http://fw.ifslearning.ac.uk/Archive/2012/June/Features/ThelifeandgoodtimesofLibormin

oszombanakis.aspx>.

Page 21

20

"Timeline: Libor-fixing Scandal." BBC News. BBC, 26 Sept. 2012. Web. 30 Nov. 2012.

<http://www.bbc.co.uk/news/business-18671255>.

"The Dot-Com Bubble Bursts." The New York Times. The New York Times, 24 Dec. 2000. Web.

01 Dec. 2012. <http://www.nytimes.com/2000/12/24/opinion/the-dot-com-bubble-

bursts.html>.

Page 22

21

Appendix

Exhibit 1

(Source: Mollenkamp, Carrick, and Mark Whitehouse. "Study Casts Doubt on Key Rate;

WSJ Analysis Suggests Banks may have Reported Flawed Interest Data for LIBOR." Wall

Street Journal: A.1. ProQuest Central. May 29 2008.)

Page 23

22

Exhibit 2: All data points were considered in this graph. Data was collected from the beginning

of the Libor Rate to the present as well as all of the data for the Treasury bills. All data used in

this Exhibit as well as the following will be based off of the 6 month rates for both rates.

1/1/20151/1/20101/1/20051/1/20001/1/19951/1/1990

9

8

7

6

5

4

3

2

1

0

ALL

Y-D

ata

Tbill 6m

6 month Libor

Variable

Scatterplot of Tbill 6m, 6 month Libor vs ALL

General Regression Analysis: Tbill 6m versus 6 month Libor

Regression Equation Tbill 6m = -0.471649 + 0.944927 6 month Libor

Coefficients Term Coef SE Coef T P

Constant -0.471649 0.0478600 -9.8548 0.000

6 month Libor 0.944927 0.0102709 92.0005 0.000

Summary of Model S = 0.392567 R-Sq = 96.84% R-Sq(adj) = 96.83%

PRESS = 43.0095 R-Sq(pred) = 96.81%

Analysis of Variance Source DF Seq SS Adj SS Adj MS F P

Regression 1 1304.39 1304.39 1304.39 8464.09 0.0000000

6 month Libor 1 1304.39 1304.39 1304.39 8464.09 0.0000000

Error 276 42.53 42.53 0.15

Lack-of-Fit 246 41.71 41.71 0.17 6.15 0.0000001

Pure Error 30 0.83 0.83 0.03

Total 277 1346.92

Fits and Diagnostics for Unusual Observations Obs Tbill 6m Fit SE Fit Residual St Resid

217 3.70 4.58730 0.0270514 -0.88730 -2.26564 R

219 3.07 4.09462 0.0248554 -1.02462 -2.61529 R

220 3.14 4.08762 0.0248311 -0.94762 -2.41876 R

221 1.87 3.09970 0.0237164 -1.22970 -3.13820 R

223 1.27 2.06057 0.0274664 -0.79057 -2.01878 R

224 1.34 2.21062 0.0266632 -0.87062 -2.22290 R

Page 24

23

227 1.63 2.47246 0.0254519 -0.84246 -2.15055 R

229 0.90 2.68148 0.0246787 -1.78148 -4.54702 R

230 0.44 3.19315 0.0236159 -2.75315 -7.02594 R

231 0.02 2.03978 0.0275835 -2.01978 -5.15780 R

232 0.12 1.58621 0.0304441 -1.46621 -3.74622 R

233 0.22 1.06017 0.0343547 -0.84017 -2.14844 R

234 0.25 1.18849 0.0333527 -0.93849 -2.39933 R

235 0.20 1.25502 0.0328445 -1.05502 -2.69694 R

236 0.12 1.08928 0.0341250 -0.96928 -2.47845 R

R denotes an observation with a large standardized residual.

Page 25

24

Exhibit 3: In this data set we observed the Libor vs the Treasury using only data that occurred

before the 217th

data point, or in terms of dates, August 2007. We conducted this analysis to

show that the R2 value was higher before this time frame and that the unusual observations were

in fact unusual.

1/1/20101/1/20051/1/20001/1/19951/1/1990

9

8

7

6

5

4

3

2

1

0

Time

Y-D

ata

6 m Tbill

6 month Libor

Variable

Scatterplot of 6 m Tbill, 6 month Libor vs Time

General Regression Analysis: 6 month Libor versus 6 m Tbill

Regression Equation 6 month Libor = 0.218341 + 1.09934 6 m Tbill

Coefficients Term Coef SE Coef T P

Constant 0.21834 0.0379692 5.750 0.000

6 m Tbill 1.09934 0.0083958 130.940 0.000

Summary of Model S = 0.214849 R-Sq = 98.77% R-Sq(adj) = 98.76%

PRESS = 10.0490 R-Sq(pred) = 98.75%

Analysis of Variance Source DF Seq SS Adj SS Adj MS F P

Regression 1 791.429 791.429 791.429 17145.3 0.000000

6 m Tbill 1 791.429 791.429 791.429 17145.3 0.000000

Error 214 9.878 9.878 0.046

Lack-of-Fit 162 7.830 7.830 0.048 1.2 0.197857

Pure Error 52 2.049 2.049 0.039

Total 215 801.307

Fits and Diagnostics for Unusual Observations 6 month

Obs Libor Fit SE Fit Residual St Resid

15 8.3750 7.93573 0.0280130 0.439268 2.06215 R

58 5.2500 4.76962 0.0146214 0.480377 2.24108 R

64 7.0000 6.29771 0.0185298 0.702290 3.28099 R

93 6.0080 5.51718 0.0155929 0.490824 2.29055 R

Page 26

25

109 5.3590 4.89055 0.0146326 0.468450 2.18544 R

121 5.9740 5.39625 0.0152961 0.577752 2.69595 R

122 6.1440 5.67108 0.0160398 0.472916 2.20732 R

129 7.0640 6.25374 0.0183253 0.810264 3.78511 R

130 7.0140 6.48460 0.0194395 0.529402 2.47421 R

138 4.9550 5.40724 0.0153210 -0.452242 -2.11030 R

216 5.3773 4.60472 0.0146998 0.772579 3.60436 R

Page 27

26

Exhibit 4

1/1/19951/1/19941/1/19931/1/19921/1/19911/1/1990

9

8

7

6

5

4

3

2

90-94

Y-D

ata

6m Tbill

6m LIBOR

Variable

Scatterplot of 6m Tbill, 6m LIBOR vs 90-94

Page 28

27

Exhibit 5

1.41.21.00.80.60.40.2

12

10

8

6

4

2

0

1990-1994 Spread

Fre

qu

en

cy

Mean 0.7011

StDev 0.2640

N 60

Histogram of 1990-1994 SpreadNormal

Page 29

28

Exhibit 6

1/1/20001/1/19991/1/19981/1/19971/1/19961/1/1995

7.0

6.5

6.0

5.5

5.0

4.5

4.0

95-99

Y-D

ata

6m Tbill_1

6m LIBOR_1

Variable

Scatterplot of 6m Tbill_1, 6m LIBOR_1 vs 95-99

Page 30

29

Exhibit 7

1.21.00.80.60.4

12

10

8

6

4

2

0

1995-1999 Spread

Fre

qu

en

cy

Mean 0.7669

StDev 0.2097

N 60

Histogram of 1995-1999 SpreadNormal

Page 31

30

Exhibit 8: From the beginning of 2000 through 2004, the markets had just experienced a major

collapse of the technology and dot come bubble. The following result shows both of the rates

decreasing. But towards the end of this time frame, the global economy was on the rise and the

United States in particular was gaining traction for the housing bubble.

1/1/20051/1/20041/1/20031/1/20021/1/20011/1/2000

7

6

5

4

3

2

1

0

00-04

Y-D

ata

6m Tbill_2

6m LIBOR_2

Variable

Scatterplot of 6m Tbill_2, 6m LIBOR_2 vs 00-04

General Regression Analysis: 6m Tbill_2 versus 6m Libor_2

Regression Equation 6m Tbill_2 = -0.123156 + 0.899559 6m Libor_2

Coefficients Term Coef SE Coef T P

Constant -0.123156 0.0420073 -2.9318 0.005

6m Libor_2 0.899559 0.0114493 78.5688 0.000

Summary of Model S = 0.182084 R-Sq = 99.07% R-Sq(adj) = 99.05%

PRESS = 2.13872 R-Sq(pred) = 98.96%

Analysis of Variance Source DF Seq SS Adj SS Adj MS F P

Regression 1 204.664 204.664 204.664 6173.06 0

6m Libor_2 1 204.664 204.664 204.664 6173.06 0

Error 58 1.923 1.923 0.033

Total 59 206.587

Fits and Diagnostics for Unusual Observations 6m

Obs Tbill_2 Fit SE Fit Residual St Resid

5 5.49 6.23133 0.0517149 -0.741331 -4.24624 R

6 5.70 6.18635 0.0512057 -0.486353 -2.78337 R

14 4.72 4.33416 0.0321392 0.385840 2.15283 R

R denotes an observation with a large standardized residual.

Page 32

31

Exhibit 9: In this chart it can be observed that the spread between the two rates became

dramatically larger after mid-2007.

0

0.5

1

1.5

2

2.5

3

3.5

4

8/1/20042/17/20059/5/20053/24/200610/10/20064/28/200711/14/20076/1/200812/18/20087/6/20091/22/20108/10/2010

Rat

e

6 Month Libor and Treasury Rate Spread

Page 33

32

Exhibit 10: 2005 through 2009 shows the bottom of the market as well as the peak. This data

represents 2 very different environments of the global economy as well as the domestic UK and

USA.

1/1/20101/1/20091/1/20081/1/20071/1/20061/1/2005

6

5

4

3

2

1

0

05-09

Y-D

ata

6m Tbill_3

6m LIBOR_3

Variable

Scatterplot of 6m Tbill_3, 6m LIBOR_3 vs 05-09

General Regression Analysis: 6m Tbill_3 versus 6m Libor_3

Regression Equation 6m Tbill_3 = -1.28095 + 1.07721 6m Libor_3

Coefficients Term Coef SE Coef T P

Constant -1.28095 0.201783 -6.3482 0.000

6m Libor_3 1.07721 0.049880 21.5959 0.000

Summary of Model S = 0.621018 R-Sq = 88.94% R-Sq(adj) = 88.75%

PRESS = 23.7717 R-Sq(pred) = 88.25%

Analysis of Variance Source DF Seq SS Adj SS Adj MS F P

Regression 1 179.867 179.867 179.867 466.383 0

6m Libor_3 1 179.867 179.867 179.867 466.383 0

Error 58 22.369 22.369 0.386

Total 59 202.236

Fits and Diagnostics for Unusual Observations 6m

Obs Tbill_3 Fit SE Fit Residual St Resid

45 0.90 2.31360 0.0823309 -1.41360 -2.29653 R

46 0.44 2.89691 0.0806000 -2.45691 -3.99001 R

47 0.02 1.58207 0.0958876 -1.56207 -2.54586 R

R denotes an observation with a large standardized residual.

Page 34

33

Exhibit 11: 2 years prior to 2007

1/1/20079/1/20065/1/20061/1/20069/1/20055/1/20051/1/2005

6

5

4

3

2

Time 3

Y-D

ata

TBILL

LIBOR

Variable

Scatterplot of TBILL, LIBOR vs Time 3

Regression Equation Libor = 0.671659 + 0.98075 TBILL

Coefficients Term Coef SE Coef T P

Constant 0.671659 0.0952134 7.0542 0.000

TBILL 0.980750 0.0234115 41.8918 0.000

Summary of Model S = 0.0979591 R-Sq = 98.76% R-Sq(adj) = 98.71%

PRESS = 0.252154 R-Sq(pred) = 98.52%

Analysis of Variance Source DF Seq SS Adj SS Adj MS F P

Regression 1 16.8402 16.8402 16.8402 1754.92 0.000000

TBILL 1 16.8402 16.8402 16.8402 1754.92 0.000000

Error 22 0.2111 0.2111 0.0096

Lack-of-Fit 20 0.2027 0.2027 0.0101 2.40 0.334669

Pure Error 2 0.0084 0.0084 0.0042

Total 23 17.0513

Fits and Diagnostics for Unusual Observations Obs Libor Fit SE Fit Residual St Resid

18 5.6382 5.43810 0.0287734 0.200095 2.13690 R

R denotes an observation with a large standardized residual.

Page 35

34

Exhibit 12: The following years after 2007. Correlations have decreased dramatically despite it

being over a longer period of time. This is particularly shocking because as can be observed in

Exhibit 2, over the course of the Libor and Treasury rates’ histories the correlation or R2 was

always high.

1/1/20131/1/20121/1/20111/1/20101/1/20091/1/2008

4

3

2

1

0

Time 4

Y-D

ata

TBILL 2

LIBOR 2

Variable

Scatterplot of TBILL 2, LIBOR 2 vs Time 4

General Regression Analysis: Libor 2 versus TBILL 2

Regression Equation Libor 2 = 0.687448 + 1.53328 TBILL 2

Coefficients Term Coef SE Coef T P

Constant 0.68745 0.091805 7.4881 0.000

TBILL 2 1.53328 0.143935 10.6526 0.000

Summary of Model S = 0.596247 R-Sq = 66.96% R-Sq(adj) = 66.37%

PRESS = 21.0233 R-Sq(pred) = 65.11%

Analysis of Variance Source DF Seq SS Adj SS Adj MS F P

Regression 1 40.3425 40.3425 40.3425 113.478 0.0000000

TBILL 2 1 40.3425 40.3425 40.3425 113.478 0.0000000

Error 56 19.9086 19.9086 0.3555

Lack-of-Fit 29 16.8833 16.8833 0.5822 5.196 0.0000237

Pure Error 27 3.0253 3.0253 0.1120

Total 57 60.2511

Fits and Diagnostics for Unusual Observations Obs Libor 2 Fit SE Fit Residual St Resid

37 3.7795 3.55469 0.234659 0.22481 0.41015 X

38 3.0039 3.41669 0.222489 -0.41279 -0.74622 X

41 2.8544 3.52402 0.231947 -0.66962 -1.21909 X

42 3.1035 3.30936 0.213087 -0.20586 -0.36968 X

43 3.1157 3.18670 0.202422 -0.07100 -0.12660 X

Page 36

35

44 3.1116 3.27870 0.210413 -0.16710 -0.29952 X

45 3.3369 2.06740 0.113082 1.26950 2.16851 R

46 3.8784 1.36209 0.079789 2.51631 4.25855 R

47 2.6578 0.71811 0.090335 1.93969 3.29115 R

48 2.1778 0.87144 0.084085 1.30636 2.21309 R

R denotes an observation with a large standardized residual.

X denotes an observation whose X value gives it large leverage.

Page 37

36

Exhibit 13:

1/1/20081/1/20071/1/20061/1/20051/1/20041/1/2003

6

5

4

3

2

1

Time 3

Y-D

ata

TBILL

LIBOR

Variable

Scatterplot of TBILL, LIBOR vs Time 3

General Regression Analysis: Libor versus TBILL

Regression Equation Libor = 0.306616 + 1.08948 TBILL

Coefficients Term Coef SE Coef T P

Constant 0.30662 0.0877202 3.4954 0.001

TBILL 1.08948 0.0264312 41.2194 0.000

Summary of Model S = 0.319572 R-Sq = 96.70% R-Sq(adj) = 96.64%

PRESS = 6.22133 R-Sq(pred) = 96.53%

Analysis of Variance Source DF Seq SS Adj SS Adj MS F P

Regression 1 173.516 173.516 173.516 1699.04 0.0000000

TBILL 1 173.516 173.516 173.516 1699.04 0.0000000

Error 58 5.923 5.923 0.102

Lack-of-Fit 48 5.898 5.898 0.123 49.25 0.0000001

Pure Error 10 0.025 0.025 0.002

Total 59 179.439

Fits and Diagnostics for Unusual Observations Obs Libor Fit SE Fit Residual St Resid

56 5.3773 4.65364 0.0498878 0.72366 2.29258 R

57 5.3538 4.33769 0.0460170 1.01611 3.21308 R

59 4.8324 3.65132 0.0414249 1.18108 3.72727 R

60 4.8250 3.72758 0.0416324 1.09742 3.46354 R

R denotes an observation with a large standardized residual.