49

WHEN GENIUS FAILED THE RISE AND FALL OF LONG-TERM CAPITAL MANAGEMENT

| Date post: | 03-Apr-2018 |

| Category: |

Documents |

| Upload: | liu-shuang |

| View: | 216 times |

| Download: | 0 times |

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 1/49

WHEN GENIUSFAILEDTHE RISE AND FALL OF LONG-TERM CAPITAL MANAGEMENT

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 2/49

Agenda

INTRODUCTION: Rise and fall of LTCM-Background- LIU SHUANG

-Example of trade- ZHANG ZHENGZHOU

-Size & liquidity- DAVID CHLEBECEK

-The unfavorable events- ZHANG XI & ELINA KOZMENKO

-Rescue of LTCM- WANG YAO

ANALYSIS: What went wrong?-Risk factors- TANG LEI & MIAO LIQIANG

-VAR- YANG JIE

DISCUSSION: How should LTCM avoid failure?-How should LTCM avoid failure- WU XIN

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 3/49

Background of LTCM

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 4/49

Background of LTCM

The Constellation of Elite

John Meriwether -MBA in Chicago University.-The founder of arbitrage group in Salomon 1980’s -Brought the nerds to the trading floor

Eric Rosenfeld -MIT Ph.D., HBS professor

Victor Haghani -Master in LSE, joined Salomon in his twenties.

Larry Hilibrand -Ph.D., MIT

Gregory Hawkins -MIT Ph.D., Pupil of Merton.

William Krasker -MIT Ph.D.

Robert C. Merton Myron Scholes

-The BSM model and Nobel LaureatesDavid W. Mullins -The vice chairman of the US Federal Reserve

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 5/49

Fund Development

$6.7BLN

$3BLN

$1.23BLN

- 1994: LTCM launching

campaign raised $1.23 billion- 1994: LTCM raised additional

$2 billion- 1997: LTCM’s net capital

reached $6.7 billion

- Monthly return volatility: -3% to 8%- Return creation slows down in 1997- The accumulation of net

performance index slows down in1997

Source: LTCM

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 6/49

Hallmark Strategy

- Relative valueLong convertible bond, short equity

- Convergence tradeLong off-the-run Treasury bond, short on-the-run Treasury bond

Other Strategy

- Directional tradeUnhedged long position in French Government bonds

Long-term Financing

- Stringent 3-year lockup period- $230 million unsecured loan and $700 million unsecured revolving line of credit- 6 to 12 month maturity repo

Trading Strategy & Financing

Source: LTCM, L.P. (A)

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 7/49

LTCM Structure & Role

Year Return

Feb to Dec, 1994 19.9% (unannualized)

1995 42.8%

1996 40.8%

Jan to Aug, 1997 11.1% (unannualized)

LTCM Performance

Management fee Performance fee

2% p.a. 25% p.a.

LTCM Fee Structure

Management fee Performance fee

1% p.a. 20% p.a.

Hedge Fund Fee Structure

Source: LTCM, L.P. (A)

Protection Seller

- Counterparty tohedger and workdirectly with end

clients

- Provide liquidity to themarket

- Major competitor are

bulge bracket tradingfloor instead of other hedge funds

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 8/49

Risk Management & Leverage

Method Return

VaR

Economicstress test

Scenario Analysis

Correlation

test

The correlation of profits

across positionsRisk overhorizon

Different considerationover horizon

Risk Management

Source: LTCMNote: *average ratio for LTCM from Jun 94 to Aug 97. Banks’ ratio is for 1996.

Correlation test

Leverage

Company D/A*

LTCM 22.5

Salmon Inc. 42.5

Morgan Stanley 26.5

Lehman Brothers 33.2

Banker Trust 21.9

Chase Manhattan 15.6

- LTCM’s leverage is lower than what figure indicates.

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 9/49

Agenda

INTRODUCTION: Rise and fall of LTCM-Background

-Example of trade

-Size & liquidity

-The unfavorable events

-Rescue of LTCM

ANALYSIS: What went wrong?-Risk factors

-VAR

DISCUSSION: How should LTCM avoid failure?-How should LTCM avoid failure

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 10/49

Treasury Bond-Swap spread trade

Buy the bond through repo market

LTCM Bank

B0

B0 bonds

CollateralB0 bonds

LoanB0-haircut

LTCM needs to fund the haircut with its working capital

- Long the spread

The swap rate (measure of macro economy)>TB yield (risk free)

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 11/49

Enter the swap as the fixed rate payer

- When spread is very small, LTCM can get positive cost of carry—pure arbitrage.- LTCM can hold to maturity. Not an optimal situation for LTCM.

- As long as swap spread is considered to be small compared to historical rangeLTCM would take this trade.

Scenarios:- Swap spread remains constant: no effect.- Swap spread decrease: value of bond decreases relative to the value of

swap LTCM loses money.- Swap spread increase: value of bond increases relative to the value of

swap LTCM makes money.

So LTCM looks forward to a widening spread, hoping bond yield decreasesrelative to the fixed swap rate.

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 12/49

Closing position

- Sell the bond in the repo market

LTCMBank

B1SellB1 bonds

ReturnCollateralB0 bonds

LoanB0-haircut

+ repo cost

Terminate the swapposition by offsetting.

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 13/49

- Short the bond through reverse repo

LTCM Bank

B0SellB0 bonds

BorrowB0 bonds

LoanB0-haircut

Enter the swap as fixed rate receiver, short the swap spread.

Short the spread

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 14/49

Enter the swap as fixed rate receiver

Scenarios:- Swap spread remains constant: no effect- Swap spread decrease: value of bond decreases relative to the value of

swap LTCM makes money.- Swap spread increase: value of bond increases relative to the value of

swap LTCM loses money.

So LTCM looks forward to shortening spread, hoping bond yield increaserelative to the fixed swap rate.

- When the spread is very large, LTCM can get positive cost of carry.

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 15/49

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 16/49

Agenda

INTRODUCTION: Rise and fall of LTCM-Background

-Example of trade

-Size & liquidity

-The unfavorable events

-Rescue of LTCM

ANALYSIS: What went wrong?-Risk factors

-VAR

DISCUSSION: How should LTCM avoid failure?-How should LTCM avoid failure

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 17/49

Size

- 1997: 6.7 billion USD, borrowed up to 125 billion

- 100 different strategies, 7600 positions,

- Became too big

- Wanted to redeem at least part of the investors to lower the size

- Danger-people knew what the fund was doing-couldn’t hide-takingopposite positions

- Leverage ratio 19:1 (up to 31:1)

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 18/49

Liquidity-financing

- Two way mark to market

- Secured financing might become difficult to obtain or

too expensive

- Institution wanted to lend them money-favorable terms

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 19/49

Liquidity-market

- Underestimated liquidity as a risk factor

- During crises, flight to liquidity=buy US, sellemerging, shift in liquidity (LTCM too big, whenthey sell the price drops even more, they looseeven more)

- Problems with liquidating their big positions, sharpdrops in prices, liquidation slow

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 20/49

Agenda

INTRODUCTION: Rise and fall of LTCM-Background

-Example of trade

-Size & liquidity

-The unfavorable events

-Rescue of LTCM

ANALYSIS: What went wrong?-Risk factors

-VAR

DISCUSSION: How should LTCM avoid failure?-How should LTCM avoid failure

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 21/49

Russia Default

Blocked

foreigntransactionby Russia

banks.

Increasingspread btw

Eur mktand

emergingmkt bond

3.5weekslater of bondissue

Default

onrouble

Ratherthan

simpleprintingmoney

LTCM bet on

narrowspread

[18 Aug 1998]

Russia Default its gov. debt

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 22/49

Tellabs canceled acquisition

• Tellabs abruptlycanceled the

acquisition of Ciena Corp

NoAcquisition

• Spread betweenthe two firms’ stock priceswideneddramatically.

WideningSpread • LTCM suffered a

significant loss

in a riskarbitrageposition

Loss

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 23/49

Widespread efforts to liquidate similar positions inAugust 1998

- Many of the world leading banks had put on the sameconvergence trades.

- In adverse market movements taking positions up toor beyond the risk limits, the traders have to try to cuttheir losses and sell.

- In August 1998, widespread efforts to liquidate broadlysimilar positions in roughly the same markets hadintensified the adverse movements.

- Correlations between historically only loosely relatedmarkets were enhanced.

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 24/49

LTCM’s difficulties became public

- On 2 September Meriwether sent a letter to thecompany’s investors, describing it’s financial situationand seeking to raise further capital.

- Letter was read as evidence of desperation.

- No one could be persuaded to buy an asset that LTCMwas known or believed to hold.

- Some counterparties saw an opportunity to trade againstLTCM’s known positions.

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 25/49

Agenda

INTRODUCTION: Rise and fall of LTCM-Background

-Example of trade

-Size & liquidity

-The unfavorable events

-Rescue of LTCM

ANALYSIS: What went wrong?-Risk factors

-VAR

DISCUSSION: How should LTCM avoid failure?-How should LTCM avoid failure

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 26/49

Rescue LTCM

- September 1998, LTCM avoided bankruptcy.

- “Not to protect LTCM’s investors, creditors, ormanager from loss, but to avoid the distortionto market processes caused by a fire-saleliquidation and the consequent spending of those distortions through contagion.”

----Alan Greenspan

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 27/49

- The participating banks got 90% share in the fundand a promise the a supervisory board would beestablished.

- $300 million: Bankers Trust, Barclays, Chase, Credit Suisse FirstBoston, Deutsche Bank, Goldman Sachs, Merrill Lynch,J.P.Morgan, Morgan Stanley, Salomon Smith Barney, UBS

- $125 million: Société Générale

- $100 million: Lehman Brothers, Paribas

- Bear Stearns declined to participate.

- LTCM’s partners received a 10% stake, still worthabout $400million, but this money was completeconsumed by their debts.

Rescue LTCM

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 28/49

- The Buffet offer

- Berkshire Hathaway, AIG, and Goldman Sachs would bewilling to buy the fund for $250 million.

- LTCM partners with no stake in the firm

- “The management of LTCM rejected the offer, and one canonly presume that they did so because they were confidentof getting a better deal from the Fed.”

- The bid was formally structured to purchase the assets of LTCM which did not include the portfolio.

Alternatives to the Restructuring

Source: Dowd, Kevin. 1999. “Hedge Funds and the collapse of Long-Term CapitalManagement”, Journal of Economic Perspectives.

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 29/49

Agenda

INTRODUCTION: Rise and fall of LTCM-Background

-Example of trade

-Size & liquidity

-The unfavorable events

-Rescue of LTCM

ANALYSIS: What went wrong?-Risk factors

-VAR

DISCUSSION: How should LTCM avoid failure?-How should LTCM avoid failure

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 30/49

What went wrong?

- Cocktail risks

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 31/49

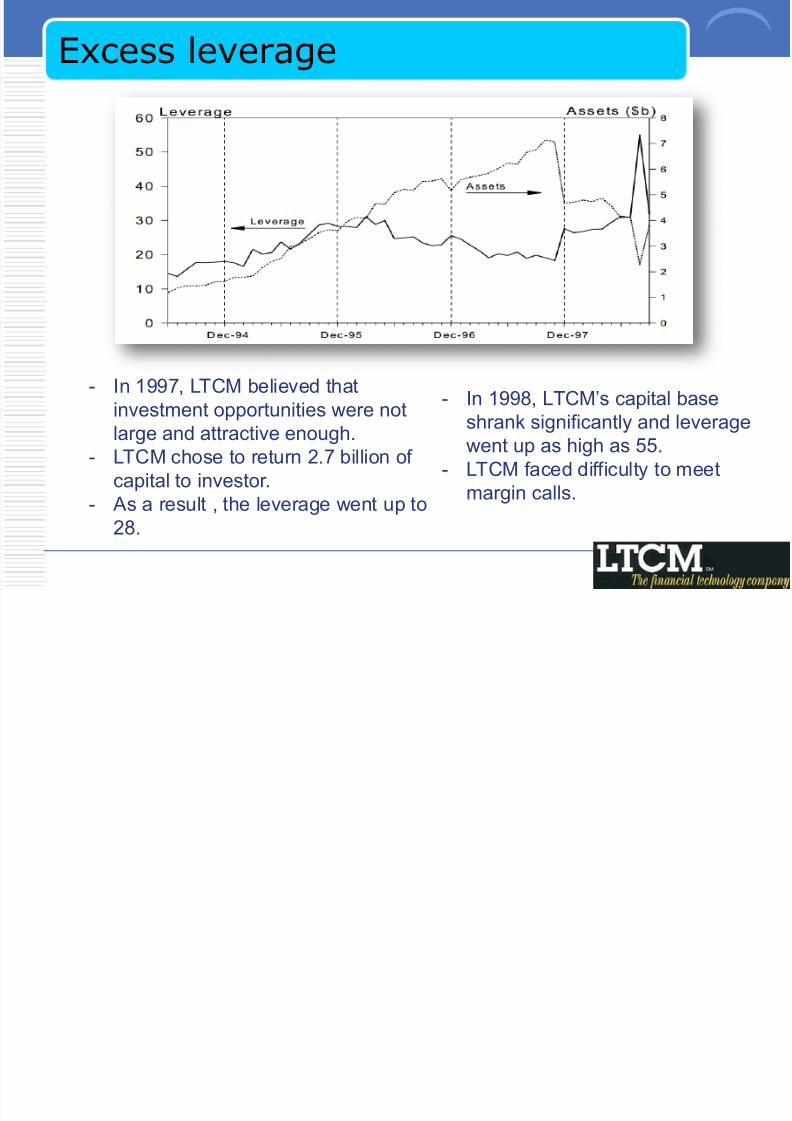

Excess leverage

- In 1997, LTCM believed that

investment opportunities were notlarge and attractive enough.- LTCM chose to return 2.7 billion of

capital to investor.- As a result , the leverage went up to

28.

- In 1998, LTCM’s capital base

shrank significantly and leveragewent up as high as 55.

- LTCM faced difficulty to meetmargin calls.

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 32/49

Excess leverage

- The ability of withstanding unfavorable marketmovements is compromised when usingdramatic leverage.

- The failure of LTCM does not mean use of leverage is bad, but it is very dangerous if excessive leverage is present.

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 33/49

Liquidity Issue

- LTCM underestimated the probability of a marketcrisis and potential for a flight to liquidity.

- Globalization and time compression: High sigma

events are more likely to occur.

- Poor liquidity management in 1998.

- LTCM was a big player and liquidity of its positionsdried up in a liquidity crisis.

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 34/49

Too concentrated

- LTCM’s positions were too concentrated on relatedrisk factors, and were singularly undiversified .

- Large positions that were exposed to liquidity, credit

and volatility spreads.

- Swap spread trade- Equity volatility trade

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 35/49

Complex Adaptive System

- The spread convergence trades were fundamentallysound in the long term.

- The real world is a complex adaptive system.

- Whether the spread would widen or narrowdepended on actions of other players.

- LTCM was very large, but no player is larger than

the market.

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 36/49

Agenda

INTRODUCTION: Rise and fall of LTCM

-Background

-Example of trade

-Size & liquidity

-The unfavorable events

-Rescue of LTCM

ANALYSIS: What went wrong?-Risk factors

-VAR

DISCUSSION: How should LTCM avoid failure?-How should LTCM avoid failure

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 37/49

VAR

Basic understanding

- VAR should be viewed as a measure of “risk capital” necessary tosupport a financial activity.

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 38/49

How to calculate capital needs

AssumptionsDaily Std

(market risk)Time Horizon

Trading Days

(within 1 yr)

Default

Probability

$100 million 1 year 252 days 0.022%

Calculation

Annual StdNormal

Distribution

$1.6 billion $5.6 billion

- LTCM stated that its target daily volatility was $45 million aroundMay 1998 (based on 4.7 billion capital).

- However, the actual daily volatility was closer to $100 million.

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 39/49

Weak Assumptions in VAR

1. In reality, hedge fund’s return distribution is asymmetric:

skewness and kurtosis should be taken into account.

- Merton: long positions in credit-sensitive instruments can be interpreted asshort positions in options, which have limited upside potential and largedownside risks.

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 40/49

- LTCM’s capital (after distributing 2.7 billion to its investors): $4.7 billion

Assumptions

Daily Std (market

risk)Time Horizon

Trading Days

(within 1 yr)

Default

Probability

$100 million 1 year 252 days 0.022%

Calculation

Annual StdNormal

Distribution

Student t-

Distribution

(6 degree)

Student t-

Distribution

(4 degree)

$1.6 billion $5.6 billion $12.6 billion $20.4 billion

How to calculate capital needs

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 41/49

Weak Assumptions in VAR

2. Volatility is changing over time.

- The assumption of constant volatility is mistaken, which in fact can easilydouble in turbulent times.

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 42/49

Weak Assumptions in VAR

3. Actual correlation may change over time.

- The correlation between highly-correlated assets may drop especially whenthe assets are credit-sensitive. E.g. corporate bonds V.S. Treasury.

4. Time compression—Danger of measuring event risksbased on the very recent data.- Estimating risk based on the recent history, LTCM assigned a low predicted

exposure to events such as sovereign defaults and market disruptions.

5. Price-taker assumption is inappropriate.

- The size of the fund is large enough to affect the price.- The very size made it impossible to maneuverer once it had loss $2.3

billion.

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 43/49

Agenda

INTRODUCTION: Rise and fall of LTCM

-Background-Example of trade

-Size & liquidity

-The unfavorable events

-Rescue of LTCM

ANALYSIS: What went wrong?-Risk factors

-VAR

DISCUSSION: How should LTCM avoid failure?-How should LTCM avoid failure

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 44/49

How should LTCM avoid failure

Shall LTCM take this risky strategy

- Mainly bet on the convergence

- Totally independent of the trend of market

- Highly possible to huge loss in volatilitymarket.

High leverage to accumulate the tiny profit

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 45/49

Fall of LTCM

May 1998 -6.7%

June 1998 -10.1%

The principal found the loss could be quite surprising

End of June 1998 Decrease some relative value position

Trimmed directional reads

Increase the most profitable position

7 July 1998 Disband the bond team

22 July 1998 Market move adversely

August Cut 5% position where possible

17 August Small loss from Russian default , 10%

21 August U.S \U.K T swap spread widened

Event driven position loss

23 august Other market participants shrink their position

Market trade volume declined

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 46/49

How should LTCM avoid failure

Know yourself and beat yourself

- Know your strength and why you success.

- Never fight the market.

- Never be a price maker.

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 47/49

How should LTCM avoid failure

Know the market

- A significant volatility is always followed byaftershocks.

- Full dynamic hedging must be proceeded when black

swan event happens.

- Monitor the assumptions of your model.

- Market participants’ reaction.

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 48/49

How should LTCM avoid failure

Know your position

- Base all risk management on the payoff of certainposition.

- Do not take the positions you do not know wherethe loss comes from.

7/28/2019 Long Term Capital Management Rise and Fall

http://slidepdf.com/reader/full/long-term-capital-management-rise-and-fall 49/49