18

March 2016 LOS ANGELES INTERNATIONAL AIRPORT

March

2016

LOS ANGELES

INTERNATIONAL

AIRPORT

2

GENERAL

This presentation you are about to view is provided as of March 16, 2016. If you are viewing this presentation after March 16, 2016, there may have been events that occurred subsequent to

such date that would have a material adverse effect on the information that is presented in this presentation, and the Department of Airports of the City of Los Angeles (the “Department”) does

not undertake any obligation to update this presentation. The information provided in this presentation is not warranted as to completeness or accuracy and is subject to change without notice. All

numbers contained in this presentation are approximate.

ADDITIONAL INFORMATION

For further information and a more complete description of the Department and the Department’s securities, investors are referred to (i) the Official Statements of the Department related to the

Department’s securities and (ii) the Department’s reports of annual financial information available on the Department’s investor relations website at

http://lawa.aero/InvestorRelations/investors.aspx or http://emma.msrb.org/, all of which speak only as of their respective dates. This presentation is provided for your information and

convenience only. Any investment decisions regarding the Department’s securities should only be made after a careful review of an Official Statement of the Department related to such

securities. Department financings are subject to, among other things, review and approval by the Department’s governing board. The issuance of any securities, and the size and timing of any

transaction are subject to market conditions and the approvals referenced above. The Department is under no obligation to pursue any transaction, any particular structure and reserves the right

to change or modify its plans as it deems appropriate.

NO OFFER OF SECURITIES

This presentation does not constitute a recommendation or an offer or solicitation for the purchase or sale of any security or other financial instrument, including the Department’s securities, or to

adopt any investment strategy. Any offer or solicitation with respect to the Department’s securities will be made solely by means of an Official Statement of the Department related to such

securities, which describes the actual terms of the Department’s securities. In no event shall the Department be liable for any use by any party of, for any decision made or action taken by any

party in reliance upon, or for any inaccuracies or errors in, or omissions from, the information contained in this presentation and such information may not be relied upon by any party in

evaluating the merits of participating in any transaction mentioned in this presentation. Nothing in these materials constitutes a commitment by the Department to enter into any transaction. No

assurance can be given that any transaction mentioned in this presentation could in fact be executed. Past performance is not indicative of future returns, which will vary. Transactions involving the

Department’s securities may not be suitable for all investors. Each investor should consult with his, her or its own advisors as to the suitability of securities or other financial instruments for the

investor’s particular circumstances.

FORWARD-LOOKING STATEMENTS

Certain statements included in this presentation constitute “forward‐looking statements.” Such statements are generally identifiable by the terminology used, such as “plan,” “expect,” “estimate,”

“budget,” or other similar words. The achievement of certain results or other expectations contained in such forward‐looking statements involves known and unknown risks, uncertainties and other

factors which may cause actual results, performance or achievements described to be materially different from any future results, performance or achievements expressed or implied by such

forward‐looking statements. No assurance can be given that any future results discussed in this presentation will be achieved, and actual results may differ materially from the expectations and

forecasts described in this presentation. All projections, forecasts, assumptions, expressions of opinion, estimates and other forward-looking statements are expressly qualified in their entirety by

the cautionary statements set forth in this presentation. The Department does not plan to issue any updates or revisions to those forward‐looking statements if or when the expectations, or events,

conditions or circumstances on which such statements are based, occur. Statements contained in this presentation which involve estimates, forecasts or other matters of opinion, whether or not

expressly so described in this presentation, are intended solely as such and are not to be construed as representations of fact. Further, expressions of opinion contained in this presentation are

subject to change without notice and the delivery of this presentation will not, under any circumstances, create any implication that there has been no change in the affairs of the Department. By

providing the information in this presentation, the Department does not imply or represent (a) that all information provided in this presentation is material to investors’ decisions regarding

investment in the Department’s securities, (b) the completeness or accuracy of any financial, operational or other information not included in this presentation, (c) regarding any other financial,

operating or other information about the Department or its outstanding securities, (d) that no changes, circumstances or events have occurred since the dated date of the information provided this

presentation or (e) that no other circumstances or events have occurred or that no other information exists concerning the Department, its outstanding securities or the contemplated transactions

which may have a bearing on Department financial condition, the security for the Department outstanding securities, or an investor’s decision to buy, sell, or hold Department’s securities.

Disclaimer

3

RESTRICTIONS ON USE

This presentation may not be reproduced, disseminated, quoted or referred to, in whole or in part. By accessing or otherwise accepting this presentation, you agree not to duplicate, copy, screen

capture, electronically store or record this presentation, nor to produce, publish or distribute this presentation in any form whatsoever.

NO RELIANCE ON THE DEPARTMENT

The Department makes no representations as to the legal, tax, credit or accounting treatment of any transactions mentioned in this presentation, or any other effects such transactions may have on

you and your affiliates or any other parties to such transactions and their respective affiliates. You should consult with your own advisors as to such matters and the consequences of the purchase

and ownership of securities or other financial instruments. The Department does not provide tax advice. Any statements contained in this presentation as to tax matters were neither written nor

intended to be used and cannot be used by any taxpayer for the purpose of avoiding tax penalties that may be imposed on such taxpayer.

SUMMARIES NOT COMPREHENSIVE OR DEFINITIVE

This presentation may include brief descriptions of the Department, LAWA, The Department’s Bonds, t and summaries of the Department’s indentures and certain other documents. Such summaries

do not purport to be comprehensive or definitive. All references in this presentation to such documents and to any other documents, statutes, reports or other instruments described in this

presentation are qualified in their entirety by reference to each such document, statute, report or other instrument. Copies of such documents are available from the Department upon written

request.

Disclaimer Continued

4

LAX Core Credit Factors

LAX Core Credit

Factors

LAX has strong financial metrics, stable and experienced management, diverse air

service and dynamic passenger growth

Experienced management team is

successfully implementing the Capital

Program that is expanding and

modernizing LAX for the benefit of

its stakeholders.

Consistent growth of predominantly

O&D traffic that is supported by a

diverse base of carriers.

Large airport serving a region with

favorable demographics and a robust

economic environment.

Conservative financial management and

strong financial metrics that are expected

to persist through the capital program.

Healthy liquidity and robust debt service

coverage that help mitigate investor risk

and preserve financial strength.

International gateway airport serving

numerous markets around the world.

Core Credit Factors

5

Prudent Management Vision

The

Groundwork

The Current Program

Future

Management’s strategic vision has set the foundation for LAX’s ability to meet traffic demand

Terminal leasehold

acquisitions

Critical rehabilitation

and renewal projects

Controlled measures to

efficiently improve

facilities

Landside improvements

to facilitate passenger

access and alleviate

congestion

Adopted new rate-

setting methodology and

10 year (through 2022)

airline agreements to

enable terminal

redevelopment

Reconstruction and

expansion of Tom

Bradley International

Terminal

Airline & concessionaire

supported and managed

terminal improvement

projects

Ongoing program of

facility repair and

maintenance

New concessionaire

agreements in all

terminals

Support facilities –

Central Utility Plant,

utilities connections,

airfield improvements

Balance gate capacity

with passenger demand

(Midfield Terminal)

Maintain efficient

utilization of landside,

terminal and airside

facilities to meet demand

Accomplishments

6

Air Service

Market

In CY2015, LAX added service to 14 new destinations (6 domestic; 8 international)

Additional service added in CY2016

Operational

Results

Over 36.1 million enplanements in FY2015 (76.5% O&D), 5.2% more than FY2014

Trend has continued into FY2016

Financial

For FY2015:

Senior Lien Debt Service Coverage = 3.82x; Total Debt Service Coverage = 2.54x

Operating Income (before depreciation and amortization) was up 13.9% from FY2014 to over

$400 million

Capital

Development

2nd Level Roadway work completed as scheduled

Terminal 5 Improvements and Bradley West Interior Enhancements are substantially completed

Design-Build contract for Midfield Satellite Concourse has been secured

Operating, Financial, and Capital

LAX has continued its strong operational and financial performance:

7

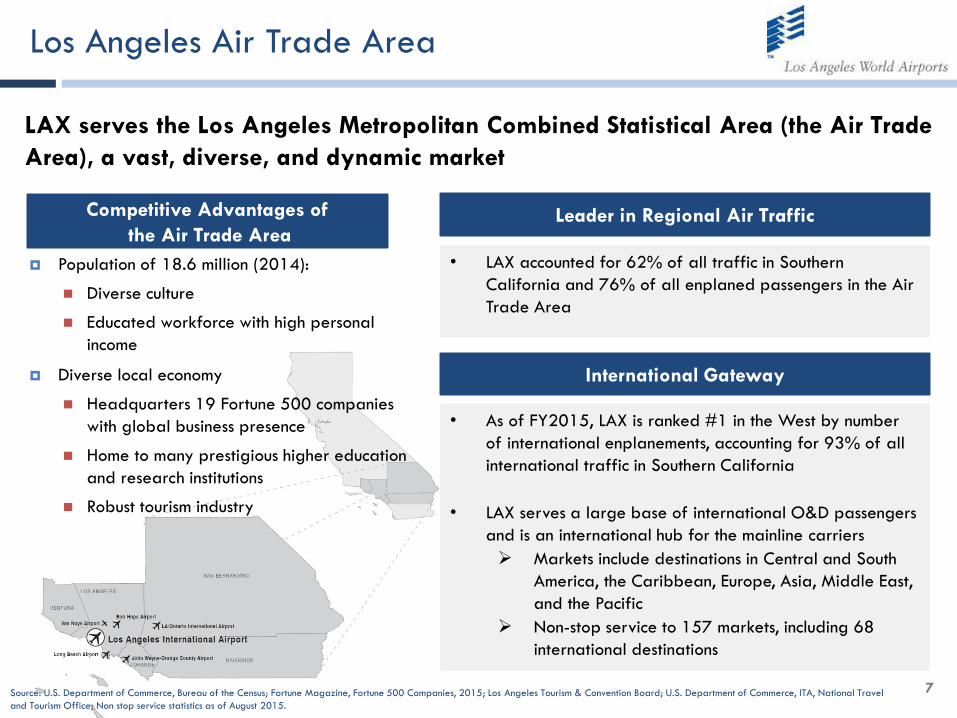

Los Angeles Air Trade Area

LAX serves the Los Angeles Metropolitan Combined Statistical Area (the Air Trade

Area), a vast, diverse, and dynamic market

Competitive Advantages of

the Air Trade Area

Population of 18.6 million (2014):

Diverse culture

Educated workforce with high personal

income

Diverse local economy

Headquarters 19 Fortune 500 companies

with global business presence

Home to many prestigious higher education

and research institutions

Robust tourism industry

Source: U.S. Department of Commerce, Bureau of the Census; Fortune Magazine, Fortune 500 Companies, 2015; Los Angeles Tourism & Convention Board; U.S. Department of Commerce, ITA, National Travel

and Tourism Office; Non stop service statistics as of August 2015.

• LAX accounted for 62% of all traffic in Southern

California and 76% of all enplaned passengers in the Air

Trade Area

Leader in Regional Air Traffic

• International

enplanements grew

6.1% in FY2015 and

have grown 17.6% from

FY2005 to FY2015

International Gateway

• As of FY2015, LAX is ranked #1 in the West by number

of international enplanements, accounting for 93% of all

international traffic in Southern California

• LAX serves a large base of international O&D passengers

and is an international hub for the mainline carriers

Markets include destinations in Central and South

America, the Caribbean, Europe, Asia, Middle East,

and the Pacific

Non-stop service to 157 markets, including 68

international destinations

8

Diverse Carrier Mix and Distribution

LAX has a diverse air carrier mix with 21 domestic and 45 foreign flag carriers*

*As of August 1, 2015

(1) Passengers reported by regional code-sharing affiliates have been grouped with their respective code-sharing

partners. American Airline includes US Airways

Source: Los Angeles International Airport records; LeighFisher

Enplanement Carrier Mix as of FY2015(1)

United 17.2%

American 18.8%

Delta 16.7%

Southwest 11.7%

Alaska 4.6%

Virgin America 4.2%

Other 26.7%

Air Carriers Serving LAX*

Update with Table 6 from OS

Scheduled U.S. Carriers (21)

Alaska Airlines Aeroflot Eva Airw ays

Allegiant Air AeroMexico Iberia

American Airlines Avianca/TACA Japan Airlines

Compass Air Berlin KLM Royal Dutch

Delta Air Lines Air Canada Korean Airlines

Dynamic Airw ays Air China LATAM

Express Jet Air France Lan Peru

Frontier Airlines Air New Zealand LACSA

Great Lakes Aviation Air Pacif ic (Fiji Airw ays) Lufthansa German

Haw aiian Airlines Air Tahiti Nui Norw egian Air Shuttle

JetBlue Airw ays Alitalia OJSC Transaero Airlines

Mesa Airlines All Nippon Philippine Airlines

MN Airlines (Sun Country) Asiana Qantas

Republic British Airw ays Saudi Arabian Airlines

SkyWest Airlines Cathay Pacif ic Singapore Airlines

Southw est Airlines China Airlines SWISS

Spirit Airlines China Eastern Thai Airw ays

Ultimate Jetcharters China Southern Turkish Airlines

United Airlines Copa Virgin Atlantic Airw ays

US Airw ays El Al Israel Virgin Australia

Virgin America Emirates Volaris

Etihad Airw ays Westjet

Ethiopian Airlines

Foreign Flag Carriers (45)

9

Airline Alliance Network

Prevalence and diversity of airline alliances support LAX’s role as a competitive

international gateway

FY2015 Airline Alliance Mix*

Other/

Non-Affiliated

*Percentages are of enplanements.

Source: OAG Aviation Worldwide Ltd, OAG Analyser database, accessed October 2015.

24%

23%

21%

32%

10

Traffic Growth

There were 36.1 million enplaned passengers (EPAX) in FY2015, an increase of 5.2% over FY2014

In FY2015, LAX continued to experience strong traffic growth and a healthy

passenger mix (76.5% O&D)

Historical Enplanements (FY2000-2015)

CAGR: Compound Annual Growth Rate

Source: Los Angeles International Airport records.

0

5

10

15

20

25

30

35

40

45

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1

Millions

Domestic International Total

Enplaned

Passengers FY2014 FY2015 % Change

Domestic 25,016,409 26,237,839 4.88%

International 9,316,116 9,883,929 6.09%

Total 34,332,525 36,121,768 5.21%

Enplanements for FY2014 & FY2015

Total EPAX 5-Year CAGR

(2010-2015): 4.5%

11

Midfield Satellite Concourse – North

Current Plans:

12 new gates – 2 for ADG-VI aircraft and 10 for ADG-V aircraft

All gates capable of both domestic and international operations

Connection via underground tunnel to TBIT/Bradley West

Approximately 760,000 ft2

MSC - North will improve terminal operations, add concessions facilities, and enhance

overall passenger experience at LAX

Site Plan Proposed Facility

ADG: Aircraft Design Group

ADG – V Boeing 777/787; Airbus 330

ADG – V1 Boeing 747-8; Airbus 380

# of New

Gates

Aircraft

Categorization Aircraft Type

10 ADG – V Boeing 777/787;

Airbus 330

2 ADG – V1 Boeing 747-8; Airbus

380

12

Tenant Managed Projects

The terminal improvement projects will be managed and financed by the airlines

Tenants control design and construction and are focused on improving efficiencies and enhancing the passenger experience

The Department will purchase the improvements at an agreed upon price in phases when they are complete

Certain public area improvements will be funded and managed by Westfield Concessions Management, LLC and purchased by the Department when they are complete. The total cost of these projects is estimated at $145 million

Many of the Terminal Improvement Projects are being managed by the Airlines and Concessionaires

Terminal Manager Total Amount

1 Southwest $526 million

2 LAWA $216 million

TBIT/1/2/3/6 Westfield $145 million

4 American $220 million

5 Delta $201 million

6/7/8 United $538 million

Terminal Improvements in the Capital Plan

Terminal 1

Terminal 7

13

CONRAC, APM and Associated Facilities

The Landside Access Modernization Program (LAMP) seeks to address LAX’s challenge of being the

busiest O&D airport in the world by relieving traffic congestion and improving passenger experience

LAMP is part of the Department’s long-term strategic plan and

will be managed through the same meticulous, conservative

process

Initial estimates of total costs are in the range of $4.5 billion to

$5.5 billion, which includes approximately $1 billion for the

Consolidated Rent-A-Car project (CONRAC).*

The CONRAC project and portions of the Automated People

Mover may be funded through CFC Revenues and CFC Revenue

Bonds.

Status:

In February, 2016, LAWA held

an Industry Forum for various

stakeholder groups including

potential investors and

contractors

Timing:

Projects expected to be

completed after Fiscal Year

2021**

*Scopes, costs, and timing of implementation are subject to substantial revision as project planning and preliminary design proceed.

**Subject to environmental and other approvals . Construction

of some components could begin prior to June 30, 2021

14

Financial Performance

In FY2015:

Total operating revenues increased by 8.7%; concession revenues increased by 6.9%

Operating expenses increased by 5.8%

Net operating income increased by 13.9%

Notes:

Revenue include interest income , anticipated BABs subsidy on Series 2009C and 2010C, and Non-Operating TSA Revenue, which are part of Pledged Revenue

Source: Department of Airports of the City of Los Angeles

Actual and Budgeted Financial Results

$-

$200

$400

$600

$800

$1,000

$1,200

FY2014 FY2015 FY2016 Budget

$M

illion

Other Operating Revenue

Concession revenue

Aviation revenue

Operating Expenses

15

Debt Service Coverage

The Airline Agreements, Terminal Tariff and Airfield Operating Permits, along with robust non-

aeronautical revenue ensure that debt service coverage will remain strong

Debt service coverage has remained strong

Source: City of Los Angeles, Department of Airports

Notes:

(1) As defined in Senior Indenture. Equals Pledged Revenues less LAX Maintenance and Operating Expenses

(2) Net of approximately $19 million, approximately $25.2 million, approximately $34.4 million, approximately $96.5 million and approximately $91.0 million passenger facility charge reimbursements for Fiscal Years

2011, 2012, 2013, 2014 and 2015 debt service payments, respectively, pursuant to the Senior Indenture. Presentations of PFC reimbursements in this table differ from those in the audited financial statements of the

Department due to differences in accounting practices.

(3) Includes actual debt service on Subordinate Commercial Paper Notes

Historical Debt Service Coverage ($000’s)

Amounts in thousands Actual

(except for coverage ratios) FY2011 FY2012 FY2013 FY2014 FY2015

Net Pledged Revenues (1) $256,273 $277,237 $288,143 $375,936 $421,023

Senior Lien Aggregate Annual Debt Service (2) $ 60,095 $ 60,577 $ 45,486 $ 62,560 $110,237

Senior Lien Coverage 4.26x 4.58x 6.33x 6.01x 3.82x

Subordinate Lien Debt Service (3) $ 40,649 $ 45,508 $ 49,904 $ 52,067 $ 55,439

Subordinate Lien Coverage 4.83x 4.76x 4.86x 6.02x 5.61x

Total Debt Service Coverage 2.54x 2.61x 3.02x 3.28x 2.54x

16

Liquidity, Cash on Hand, and DSRF

Liquidity is strong, even during a major capital program

LAX had approximately $729.0 million in available funds on hand to pay operating

expenses at the end of FY2015, representing 412 days cash on hand

LAX’s $500 million Commercial Paper Program has a remaining capacity of $449.8

million with $50.2 million currently outstanding1

LAX had approximately $507.7 million in PFC funds on hand at the end of FY2015

Debt Service Reserve Funds are fully cash funded

The Operating Permits and Terminal Tariff/Airline Rate Agreements are designed to

provide the Department with future funding and discretionary cash

1. As of December 1, 2015

Source: Department of Airports of the City of Los Angeles. Figures are preliminary, unaudited.

17

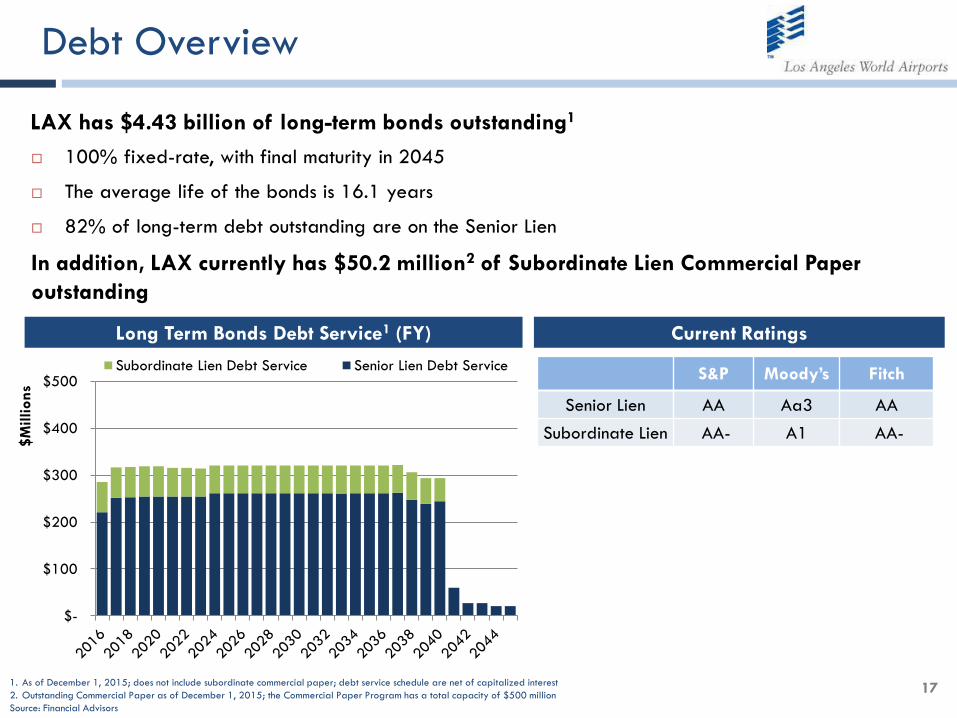

Debt Overview

100% fixed-rate, with final maturity in 2045

The average life of the bonds is 16.1 years

82% of long-term debt outstanding are on the Senior Lien

In addition, LAX currently has $50.2 million2 of Subordinate Lien Commercial Paper

outstanding

LAX has $4.43 billion of long-term bonds outstanding1

1. As of December 1, 2015; does not include subordinate commercial paper; debt service schedule are net of capitalized interest

2. Outstanding Commercial Paper as of December 1, 2015; the Commercial Paper Program has a total capacity of $500 million

Source: Financial Advisors

S&P Moody’s Fitch

Senior Lien AA Aa3 AA

Subordinate Lien AA- A1 AA-

Current Ratings

$-

$100

$200

$300

$400

$500

$M

illions

Subordinate Lien Debt Service Senior Lien Debt Service

Long Term Bonds Debt Service1 (FY)

18

Calendar 2016 Planned Bond Issuances

The Department is planning to issue Revenue Bonds in Spring and Fall of 2016 to fund capital projects*

*Preliminary, subject to change

Source: Department of Airports of the City of Los Angeles