72

LowCVP ‘Low Carbon Road Transport Challenge’ Proposals to reduce road transport CO2 emissions in the UK to help mitigate climate change June 2006

| Date post: | 28-May-2019 |

| Category: |

Documents |

| Upload: | truongtram |

| View: | 223 times |

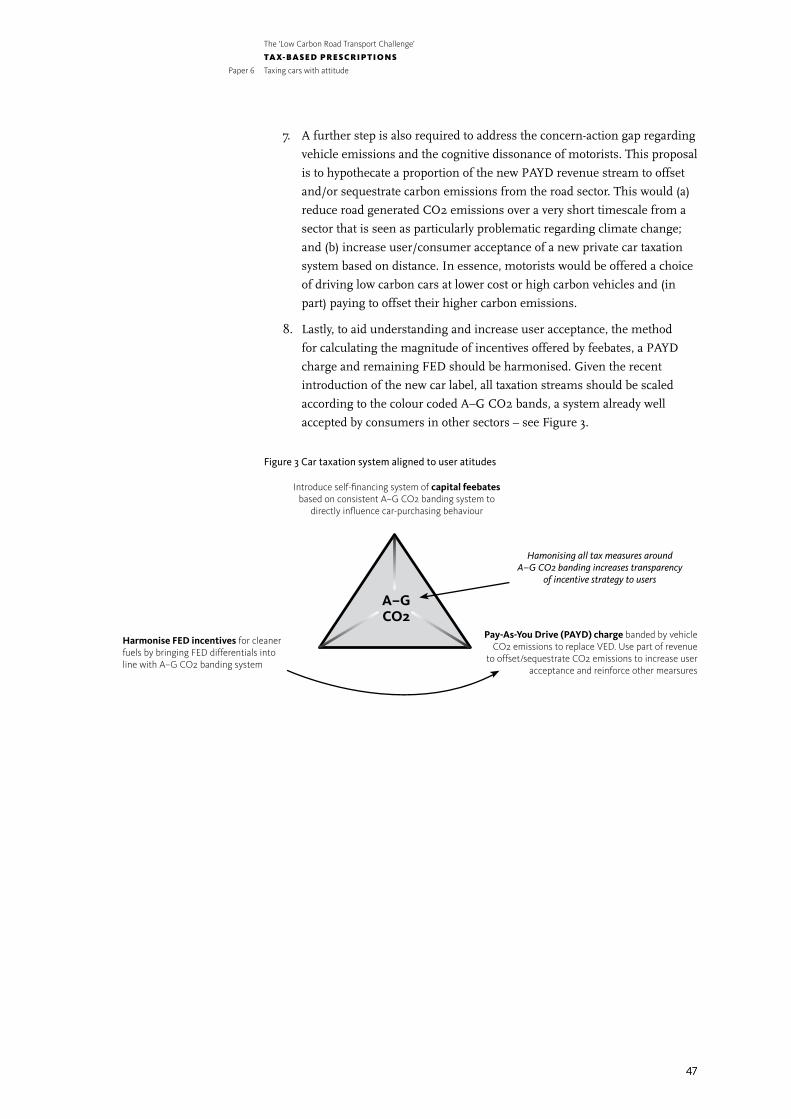

| Download: | 0 times |

LowCVP ‘Low Carbon Road Transport Challenge’Proposals to reduce road transport CO2 emissions in the UK to help mitigate climate change

June 2006

The LowCVP was established in January 2003 as one of the main initiatives announced in the Government’s ‘Powering Future Vehicles Strategy’. The Partnership now has over 200 member organisations including automotive and energy industry companies, transport operators, road user groups, transport operators, academic organisations, central and local government representatives and environment groups.

The LowCVP aims to accelerate the shift to low carbon vehicles and fuels through activities including: developing initiatives to promote the sale and supply of low carbon vehicles and fuels; providing input and advice on Government policy; providing a forum for stakeholders to share knowledge and information. It also seeks to ensure that UK motor, fuel and related businesses are best placed to capitalise on the opportunities in the low carbon markets of the future; contributing to the achievement of UK Government targets for road transport carbon reductions.

The LowCVP is jointly funded by the Department for Transport and the Department of Trade and Industry.

June 2006

Note:

The LowCVP acted to facilitate the Challenge process leading to the publication of the papers presented in

this booklet. However, neither the LowCVP as a whole nor individual members necessarily endorse the specific

proposals that appear here.

�

The ‘Low Carbon Road Transport Challenge’

Contents

Foreword by Professor M�ke Hulme ��� D�rector, Tyndall Centre for Cl�mate Change Research

Introduct�on by Graham Sm�th v Cha�rman, The Low Carbon Veh�cle Partnersh�p

M A R K E T- B A S E D S O LU T I O N S Paper 1 Ta�lp�pe trad�ng: how to �nclude road transport �n the EU Em�ss�ons Trad�ng Scheme (EU ETS) 1 Tony Grayl�ng, T�m G�bbs and Ben Castle, Inst�tute for Publ�c Pol�cy Research

Paper 2 Us�ng carbon markets to encourage the uptake of low carbon veh�cles* 7 Robert Rab�now�tz, ECX Assoc�ate Membersh�p Ltd

R E g U L AT O Ry A p p ROAc h E S Paper 3 Opt�ons for carbon regulat�on of the European car �ndustry* 15 Alex Ve�tch, Energy Sav�ng Trust

Paper 4 Gett�ng the gen�e back �n the bottle: l�m�t�ng speed to reduce carbon 22 em�ss�ons and accelerate the sh�ft to low carbon veh�cles* J�ll�an Anable, UKERC and the Centre for Transport Pol�cy, Robert Gordon Un�vers�ty

Pa�ge M�tchell, The Slower Speeds In�t�at�ve

Russell Layberry, UKERC and the Env�ronmental Change Inst�tute, Un�vers�ty of Oxford

Paper 5 Green badge park�ng perm�t (GBPP) project 33 Ke�th Boxer, Le�la O’Sull�van, Manchester: Knowledge Cap�tal

TA x- B A S E D p R E S c R I p T I O N S Paper 6 Tax�ng cars w�th att�tude* 41 Ben Lane, D�rector, Ecolane Transport Consultancy/Open Un�vers�ty

Stephen Potter, Professor of Transport Strategy, Technology Faculty, The Open Un�vers�ty

James Warren, Technology Faculty, The Open Un�vers�ty

Paper 7 A feebate scheme for the UK 48 Malcolm Fergusson, Ian Sk�nner, Eleanor Mackay, Inst�tute for European Env�ronmental Pol�cy

cO N S UM E R I N f O R M AT I O N A p p ROAc h Paper 8 New dashboard �nstruments �nform CO2 pol�c�es for new veh�cles 55 Steven Cous�ns, School of Industr�al and Manufactur�ng Sc�ence, Cranfield Un�vers�ty

* Presented at the LowCVP Conference, June 2006

��

���

The ‘Low Carbon Road Transport Challenge’

Foreword

A key part of the Tyndall Centre’s m�ss�on �s to promote �nformed and effect�ve d�alogue across soc�ety about �ts ab�l�ty and w�ll�ngness to choose our future cl�mate.

We are work�ng to seek, evaluate and fac�l�tate susta�nable solut�ons that w�ll m�n�m�se the adverse effects of cl�mate change and st�mulate pol�cy for the trans�t�on to a more ben�gn energy and mob�l�ty reg�me. We were, consequently, very pleased to be able to support the Low Carbon Veh�cle Partnersh�p’s ‘Road Transport Challenge’ wh�ch set out to br�ng forward t�mely and �nnovat�ve proposals w�th the potent�al to ease the trans�t�on to a lower carbon future.

Road transport contr�butes about a quarter of the UK’s man-made em�ss�ons of carbon d�ox�de and the sector’s share has been grow�ng. Cuts �n em�ss�ons from th�s and other key sectors are needed �n the UK, and elsewhere, to help meet the challenge of cl�mate change. There �s a clear sc�ent�fic consensus that the world �s warm�ng as a d�rect result of the r�s�ng concentrat�on of greenhouse gases �n the atmosphere. Carbon d�ox�de �s the most s�gn�ficant of these gases; �ts concentrat�on has �ncreased by a th�rd follow�ng the rap�d r�se �n the combust�on of foss�l fuels for transport and other energy uses �n the last century.

I hope that the proposals set out �n th�s booklet help to broaden the d�scuss�on on cl�mate-fr�endl�er transport and serve to st�mulate the pol�cy and other developments that are the necessary precursors of truly susta�nable mob�l�ty �n the 21st Century.

Professor Mike Hulme, Director Tyndall Centre for Cl�mate Change Research

v

The ‘Low Carbon Road Transport Challenge’

Introduct�on

In July 2005 the Low Carbon Veh�cle Partnersh�p challenged the UK’s pol�cy and academ�c commun�t�es to contr�bute �nnovat�ve proposals to accelerate the sh�ft to low carbon veh�cles and fuels.

The ‘Low Carbon Road Transport Challenge’ was �ntended to br�ng forward succ�nct pol�cy proposals and other �n�t�at�ves to be val�dated by representat�ve stakeholders of the 200-member Low Carbon Veh�cle Partnersh�p (LowCVP). The Partnersh�p was very pleased that the Challenge process has been supported by the Tyndall Centre for Cl�mate Change Research, a lead�ng academ�c network work�ng on var�ous fronts to m�t�gate the progress and �mpacts of cl�mate change. The Challenge was spec�fically targeted at those �nvolved �n transport and env�ronment pol�cy stud�es, located �n ‘th�nk-tanks’, academ�a or w�th�n other non-governmental organ�sat�ons. Proposals were welcomed �n the areas of fiscal and regulatory measures; consumer �nformat�on; motor/fuels �ndustry protocols or voluntary measures and the promot�on of �ndustry cooperat�on across the low carbon supply cha�n.

The LowCVP Secretar�at rece�ved over 30 �n�t�al responses from spec�al�sts work�ng predom�nantly for organ�sat�ons w�th�n the pol�cy-form�ng commun�ty by the �n�t�al deadl�ne of 16 October 2005. The subm�ss�ons were rev�ewed by a panel of LowCVP stakeholders �nclud�ng �nd�v�duals from: a lead�ng motor company; a fuel suppl�er; a low carbon technology company; a government env�ronment pol�cy spec�al�st; a road user group; a fleet operator; an academ�c organ�sat�on; a government-funded energy agency and an env�ronmental NGO.

Those who subm�tted what were cons�dered the best of the or�g�nal entr�es were �nv�ted to develop extended proposals by a December 2005 deadl�ne. Follow�ng a panel rev�ew meet�ng, held early �n 2006, e�ght entr�es were chosen to appear �n th�s booklet and four to be presented at the LowCVP’s annual conference. Var�ous suggest�ons were made to authors by the panel, �ntended to strengthen aspects of each proposal. The Challenge panel were asked to assess the subm�ss�ons accord�ng to a number of cr�ter�a �nclud�ng or�g�nal�ty, academ�c mer�t and potent�al for pract�cal adopt�on as pol�cy, or �n other terms. The LowCVP has acted to fac�l�tate the Challenge process but ne�ther the panel nor the LowCVP as a whole spec�fically endorse any of the proposals that appear �n th�s publ�cat�on.

Graham Smith, Chairman The Low Carbon Veh�cle Partnersh�p

v�

M A R K E T- B A S E D S O LU T I O N S

1

The ‘Low Carbon Road Transport Challenge’

Summary

We propose that the European Un�on Em�ss�ons Trad�ng Scheme (EU ETS) should be extended to �nclude ta�lp�pe em�ss�ons

of carbon d�ox�de (CO2) from road transport, �nd�rectly through fuel suppl�ers. Th�s would be relat�vely s�mple and cheap to

adm�n�ster because of the small number of compan�es �nvolved: 20 compan�es �n the UK account for more than 99 per cent

of road fuels suppl�ed.

Em�ss�ons allowances could be allocated at EU or country level, free of charge or through auct�on�ng or a comb�nat�on of the

two. Revenue from auct�on�ng could be used to reduce fuel duty or for cl�mate change m�t�gat�on measures or a comb�nat�on

of these. B�ofuels would not requ�re em�ss�ons allowances, s�nce they are renewable, hence the�r supply would be promoted.

Includ�ng road transport �n the EU ETS �n th�s way would prov�de the framework for assured em�ss�ons reduct�ons but would

not negate the need for complementary measures to promote low carbon veh�cles, fuels and journeys.

If road transport makes a proport�onate contr�but�on to reduc�ng greenhouse gas em�ss�ons by 15–30 per cent from the 1990

level by 2020 – the goal suggested by the European Counc�l �n March 2005 – then �nclud�ng road transport �n the EU ETS

could potent�ally save about 75–235 m�ll�on tonnes of CO2 per year by phase IV (2018–22) compared to phase II (2008–12).

The European Comm�ss�on should �n�t�ate a feas�b�l�ty study followed by consultat�on and leg�slat�on to �nclude road

transport �n the EU ETS through fuel suppl�ers from phase III (2013–17) onwards. Fa�l�ng that, the UK Government should

cons�der act�ng un�laterally.

Tailpipe trading: how to include road transport in the EU Emissions Trading Scheme (EU ETS)Tony Grayling, Tim Gibbs and Ben CastleInstitute for Public Policy Research

.

Introduction

Potentially the most efficient and effective way to reduce human-induced climate change caused by carbon dioxide emissions would be through a comprehensive, global, mandatory emissions cap and trading scheme covering all greenhouse gas emissions from all sectors of the economy in every country. This would put a quantified limit on global greenhouse gas emissions reducing over time and enable emissions reductions to be achieved in the most cost-effective way, through emissions trading.

The establishment of the EU Emissions Trading Scheme (ETS) is an important step towards this goal. The EU ETS already covers nearly half of all carbon dioxide emissions in the EU. We propose that the EU ETS should be expanded to cover carbon dioxide emissions from road transport, indirectly through fuel suppliers.

Paper 1

22

The ‘Low Carbon Road Transport Challenge’

M A R K E T- B A S E D S O LU T I O N S

Ta�lp�pe trad�ng: how to �nclude road transport �n the EU Em�ss�ons Trad�ng Scheme (EU ETS)

Paper 1

EU Emissions Trading Scheme

The EU ETS currently covers CO2 emissions from power stations and energy-intensive industries such as steel, cement, paper and oil refining, throughout the EU. The first phase of the scheme runs from 2005–7 (phase I) and the second from 2008–12 (phase II), coinciding with the first commitment period of the Kyoto Protocol. Subsequent phases will also have five year periods.

Under the scheme, each member state devises a National Allocation Plan (NAP) for each phase. The NAPs specify the total permitted emissions for the phase and how allowances are to be allocated to the installations included in the scheme. In phase I, governments have the discretion to auction up to five per cent of their allowances but the other 95 per cent must be allocated free of charge. Up to ten per cent can be auctioned in phase II.

Installations, such as factories or power stations, are allocated a quota of allowances. Each allowance permits the installation to emit one tonne of carbon dioxide (tCO2). Allowances can be traded between installations (and intermediaries) across the EU. If an installation produces more emissions than its quota it must purchase additional allowances. Installations emitting less than their quota can sell their surplus allowances. The penalty for producing more emissions than allowances is €40 per allowance in the first phase and €100 per allowance in the second phase. The excess emissions must also be covered by allowances surrendered by the installation in the following year so that the environmental integrity of the scheme is not compromised.

In phase II, allowances must be backed by equivalent greenhouse gas emission allowances under the Kyoto Protocol (Assigned Amount Units). It will also be possible for emissions credits to be acquired through Kyoto’s Clean Development Mechanism (CDM) and Joint Implementation (JI) whereby investments in emissions saving projects abroad, in developing countries and industrialised countries respectively, earn ‘emission reduction units’ equivalent to allowances.

The EU ETS is, potentially, a sure way of capping and reducing total emissions from the installations covered by the scheme across the EU, or achieving equivalent emissions savings through the flexible mechanisms (CDM and JI). It is currently the single most important policy instrument in the EU and UK climate change programmes, covering around half the CO2 emissions from the EU and UK (excluding international aviation and shipping). Trading of allowances should ensure that emissions savings are made in the most cost-effective way between the sectors covered. Installations will either limit their emissions and sell surplus allowances or buy extra allowances, whichever is the most profitable or costs least.

33

The ‘Low Carbon Road Transport Challenge’

M A R K E T- B A S E D S O LU T I O N S

Ta�lp�pe trad�ng: how to �nclude road transport �n the EU Em�ss�ons Trad�ng Scheme (EU ETS)

Paper 1

Potential for expanding the EU ETS

The EU ETS Directive1 provides expressly for extending the scope of the scheme in future phases through:

• Amendment to Annex I to include other activities and greenhouse gas emissions; and

• Article 24, unilateral inclusion of additional activities, installations and gases.

It is unlikely that there will be major alterations for phase II. Member states are unlikely to make very substantial changes unilaterally, though some new sectors of industry may be included.2 The Commission is not intending to change the Directive in time for phase II. However, under article 30 the Commission will come forward with proposals for later phases to the European Parliament and Council by 30 June 2006.

This includes, “how and whether Annex I should be amended to include other relevant sectors, inter alia the chemicals, aluminium and transport sectors, activities and emissions of other greenhouse gases listed in Annex II, with a view to further improving the economic efficiency of the scheme.” It also encompasses the method of allocating allowances including auctioning for the time after 2012 and the criteria for NAPs, among other things.

The Commission already intends to come forward with legislative proposals for including air transport in the scheme3, which is also a priority for the UK Government. The Commission’s preference is to include emissions from all flights departing from EU airports, whether their destination is within or outside the EU. Aircraft operators would be the designated trading entities.

Including road transport

The review of the UK Climate Change Programme included a commitment to consider the scope for including surface transport in the EU ETS.4 Aviation sets a precedent for moving beyond including only stationary installations. But road transport is different. Whereas the study by consultants CE for the European Commission on including aviation in the EU ETS shows that there are only 774 aircraft operators in the EU5, most road vehicles are not owned by fleet operators but are in the hands of tens of millions of private households. There are more than 200 million cars in the 25 countries of the EU.6

The political barriers and the administrative costs and complexity of including individual car owners in the trading scheme would be great. It would require people getting to grips with emissions as a new currency (sometimes called Domestic Tradable Quotas or Personal Carbon Allowances). Under any system of allocation, huge numbers of people would have to pay for extra emissions allowances to carry on driving as usual, or change their behaviour, which may

1 Directive 2003/87EC http://europa.eu.int/eur-lex/pri/en/oj/dat/2003/l_275/l_27520031025en00320046.pdf

2 The UK is considering gypsum, rock wool, glass, integrated steelworks, foundries and other ferrous metals, offshore flaring and petrochemicals http://www.defra.gov.uk/corporate/consult/euets-phasetwo/consultdoc.pdf

3 http://www.europa.eu.int/comm/environment/climat/aviation_en.htm

4 HM Government (2005) Review of the UK Climate Change Programme – Consultation Paper, December 2004 http://www.defra.gov.uk/corporate/consult/ukccp-review/index.htm

5 http://europa.eu.int/comm/environment/climat/pdf/aviation_et_study.pdf

6 http://europa.eu.int/comm/dgs/energy_transport/figures/pocketbook/2004_en.htm

44

The ‘Low Carbon Road Transport Challenge’

M A R K E T- B A S E D S O LU T I O N S

Ta�lp�pe trad�ng: how to �nclude road transport �n the EU Em�ss�ons Trad�ng Scheme (EU ETS)

Paper 1

be a good thing but is unlikely to meet with universal acclaim. In principle, information technology (IT) is up to the task of enabling administration of a scheme but the risks and costs of implementing major IT projects are large. None of these barriers may be insurmountable in the longer term but including households as entities in the EU ETS is unlikely to be a politically viable option for phase III (2013–17).

Instead, we propose the option of including road transport CO2 emissions through fuel suppliers should be adopted. This would be relatively simple and cheap to administer and is much more politically feasible. The feasibility study for the Renewable Transport Fuel Obligation (RTFO), which the UK Government proposes to introduce, shows that just 20 companies (eight oil refiners and a dozen other major companies) dominate the supply of road fuels in the UK, paying over 99 per cent of all road fuel duties7. Every litre of fuel supplied in the UK is already accounted for the purpose of fuel duty by HM Revenue & Customs (HMRC). We propose that road transport fuels should be included in the EU ETS at the duty point. The administrative costs of incorporating road transport in the EU ETS in this way is likely to be similar in scale to the costs of administering the RTFO, which is a tradable obligation on fuel suppliers to supply biofuels. The costs of administering the RTFO are estimated to be in the order of £1 million per year for the Government and around £2 million per year for the industry8; peanuts in comparison to the industry’s turnover. In the case of the EU ETS, the Environment Agency is the administrative authority in the UK and could administer the inclusion of road transport fuel suppliers in the scheme.

Extrapolating to the European level, there are currently about 102 oil refineries in the 25 EU countries plus two in Norway and two in Switzerland. These are owned by 31 companies, including 23 who are members of the European petroleum industry association, EUROPIA. In addition, there will be a number of other companies importing road fuels into the EU. Every country has its own system of fuel duty that would provide the administrative foundation for including road transport fuels in the EU ETS. Hence the administration of the scheme would be likely to be relatively straightforward and cost effective.

Allocating emissions allowances

There is more than one option for allocating emissions allowances to fuel suppliers. It could be done at EU or national level. The inclusion of international aviation already raises the issue of whether it would be more logical to allocate allowances at EU rather than country level for this industry. The oil industry also operates trans-nationally. Allocations could be made free of charge based on market share or through auctioning, or some combination of the two. One option would be 100 per cent auctioning with recycling of the revenue to reduce fuel duty, hence ensuring it is an instrument used to reduce emissions rather than raise money. Another option would be to earmark some of the revenue for climate change mitigation measures.

7 http://www.dft.gov.uk/stellent/groups/dft_roads/documents/page/dft_roads_610329.hcsp

8 ibid.

55

The ‘Low Carbon Road Transport Challenge’

M A R K E T- B A S E D S O LU T I O N S

Ta�lp�pe trad�ng: how to �nclude road transport �n the EU Em�ss�ons Trad�ng Scheme (EU ETS)

Paper 1

Fuel suppliers would, of course, also be able to buy and sell allowances on the market. They would be required to surrender allowances to cover the CO2 emissions of the fossil fuels they supplied each year. Biofuels should be exempted, since their carbon content is renewable. Although production of biofuels involves CO2 emissions, this varies hugely between different biofuels and it would be very difficult and complex to account for this at the point of supply. In the longer term future, these emissions should be accounted for at the point of production if and when there is a fully comprehensive global trading scheme.

Standard values for the amount of CO2 emissions from each litre of each road fuel type are already used to calculate emissions produced through employee transport for company reporting purposes. These are shown in the table below. There would, therefore, be no difficulty in calculating the number of allowances required for the volume of fuel supplied.

Table1Source:DEFRA(2005)GuidelinesforCompanyReportingonGreenhouseGasEmissions 9

Potential emissions savings

The amount of emissions saved by including road transport in the EU ETS depends on the amount of allowances issued. Savings would either be direct, through less fuel consumption, or indirect, through fuel suppliers buying additional allowances and thus reducing the amount available to other sectors. Under the Kyoto Protocol, the EU is committed to reducing its greenhouse gas emissions (excluding international shipping and aviation) by 8 per cent from the 1990 level in the first commitment period (2008–12). In March 2005, the European Council agreed to explore with other parties “reduction pathways for the group of developed countries in the order of 15–30 per cent by 2020, compared to the baseline envisaged in the Kyoto Protocol”.10

CO2 emissions from road transport account for about one fifth of the EU’s greenhouse gas emissions11. For illustration, let us assume that the EU meets its Kyoto obligation and adopts a commitment to cut greenhouse gas emissions by 15 to 30 per cent from the 1990 level by 2018–22 (corresponding to the third Kyoto commitment period and phase IV of the EU ETS). Let us also assume that road transport makes a proportionate contribution to meeting this commitment i.e. about one fifth of the additional 7 to 22 per cent reduction. That corresponds to potential emissions savings of about 75–235 MtCO2 (20–64 MtC) per year.

Fuel kgCO2perlitre

Petrol 2.31

D�esel (�ncl. low sulphur) 2.68

Compressed Natural Gas (CNG) 2.67

L�qu�d Petroleum Gas (LPG) 1.51

9 http://www.defra.gov.uk/environment/business/envrp/gas/

10 http://ue.eu.int/ueDocs/cms_Data/docs/pressData/en/ec/84335.pdf

11 http://reports.eea.eu.int/eea_report_2005_8/en

66

The ‘Low Carbon Road Transport Challenge’

M A R K E T- B A S E D S O LU T I O N S

Ta�lp�pe trad�ng: how to �nclude road transport �n the EU Em�ss�ons Trad�ng Scheme (EU ETS)

Paper 1

Complementary measures

Mandatory emissions ‘cap and trade’ schemes like the EU ETS provide the framework for assured reductions in greenhouse gas emissions but not the whole solution. One criticism of including road transport in the EU ETS indirectly through fuel suppliers is that it does not provide any direct incentive on consumers to reduce fuel use. This is similar to the current situation in the electricity market, since power stations are included in the scheme while homes, commercial buildings and train operators are not. An indirect incentive does occur as the price of electricity would include the value of emission allowances. In addition, there are complementary measures including the home Energy Efficiency Commitment, the Climate Change Levy on business combined with Climate Change Agreements, and the Renewables Obligation. In the case of road transport, measures would continue to be needed to promote low carbon vehicles, low carbon fuels and low carbon journeys, such as tax incentives, the RTFO and policies to encourage smarter travel choices. In the longer term, it may be possible to introduce Domestic Tradable Quotas or Personal Carbon Allowances to provide direct incentives to consumers. Realistically, we think this could happen no earlier than phase IV of the EU ETS (2018–22). Meanwhile, the perfect should not be the enemy of the good.

Next steps

The European Commission should commission a feasibility study on including road transport in the EU ETS through fuel suppliers. This should be followed by a consultation with the aim of introducing legislation to include CO2 emissions from road transport from phase III (2013–17). Failing that, the UK Government should consider unilateral inclusion of road transport to set a lead and ensure that road transport plays its full role in emissions reductions under the UK’s climate change programme.

7

The ‘Low Carbon Road Transport Challenge’

Using carbon markets to encourage the introduction of low carbon vehiclesRobert Rabinowitz, PhDECX Associate Membership Ltd1

1. Introduction

Market-based policies have three significant advantages for reducing emissions:a) they allow emitters flexibility and cost-effectiveness in meeting targets

b) they provide financial incentives for emitters to exceed the required standards

c) they offer certainty on the level of emissions for each compliance period

There are few technical barriers to market-based policies for reducing emissions from new vehicles. Methods for calculating emissions are standardized and can be subject to verification. There are also precedents from existing emissions markets.

2. Precedents

There are various successful emissions markets in the world today. The market in sulphur emissions in the US has reduced emissions by 38% since 1990, with over 99% compliance. Estimated health benefits exceed programme costs by 40:1.

The most important market in the evolving global carbon market is the EU ETS. It began on January 1, 2005 and has built up considerable liquidity. Over 600 million tonnes have traded to date. It is supported by a significant infrastructure including electronic emissions exchanges and registries, verification protocols and practitioners, and a range of financial intermediaries offering trading and risk management tools.

The project-based UN-sponsored Clean Development Mechanism (CDM) which issues credits to projects in the developing world is hampered by a slow-moving regulatory system, but a wide range of emission reduction protocols have been developed. A similar system, Joint Implementation (JI), is getting up and running for former communist countries. Up to a billion tonnes of emission reductions are already under contract.

In the US, the Chicago Climate Exchange operates a voluntary, but legally binding market. Members include public and private entities such as Ford, DuPont, IBM, American Electric Power, Rolls Royce, the State of New Mexico, the City of Chicago, the World Resources Institute and the CBI’s US office. Regulated by NASD, over 9 million tonnes have traded to date. Other carbon emissions markets are the UK ETS and the New South Wales Greenhouse Gas Abatement Scheme.

Paper 2

1 This discussion paper represents a consideration of possible design options and does not constitute a recommendation for future government policy by ECX Associate Membership Ltd or any of its affiliates.

88

The ‘Low Carbon Road Transport Challenge’

M A R K E T- B A S E D S O LU T I O N S

Us�ng carbon markets to encourage the �ntroduct�on of low carbon veh�cles

Paper 2

There are also precedents for market-based policies to reduce auto emissions.

Phasing lead out of gasoline in the USATo reduce the lead content in gasoline, in 1982 the US EPA introduced trading of the right to add lead to gasoline. Refineries with excess allowances could sell to refiners in deficit. The number of participants trading peaked at 416 in 1985. The percentage of lead rights traded relative to those used reached 60% in Q2 1987. By the time the programme ended, all refiners had complied with the required standard and no refiner requested additional time to meet it. Early achievement of the target generated around 10 billion allowances which were banked to offset costs later in the programme, saving an estimated $250 million compared to a “command-and-control” regulatory approach.

Corporate Average Fuel Economy (CAFE)CAFE is the sales weighted annual average fuel economy of a manufacturer’s automobile fleet sold in the United States. Manufacturers earn “credits” when a fleet exceeds the target. Credits can be used for three years before or after the year they were earned. Credits are also granted for alternative and dual-fuel vehicles. Credits cannot be traded. The current penalty for failing to meet CAFE standards is $5.50 per tenth of a mpg over the target value per vehicle. Since 1983, manufacturers have paid more than $618 million in penalties. A recent National Academy of Science study concluded that CAFE had increased fuel efficiency beyond the business as usual level. It also recommended that trading of CAFE credits be introduced.

Averaging, Banking and Trading Programmes (ABT)US emission regulations allow engine manufacturers to “average” emissions, “bank” credits to offset emissions from future years and to “trade” credits. The regulations use standard factors such as estimated average annual use and the expected useful life of each engine. While averaging and banking has taken place, there have been very few trades. Reasons include the small number of potential trading partners, high transaction costs and sensitivity about releasing sensitive information to competitors.2

3. Integrating car emissions into the EU ETS

There have been several papers on market-based policies for the creation of low-carbon vehicles.3 Mostly, they suggest creating a specific credit to be traded within the auto industry and/or restricting trading to large groups such as ACEA, JAMA and KAMA.4

Such proposals are likely to be ineffective at creating a vibrant market for the same reasons that ABT programmes have seen low levels of trading. Simply, they are likely to lack liquidity. The liquidity of a market is measured by the ease with which a participant can find a counter-party willing to trade sufficient volumes at a price close to the market price. In a liquid and effective emissions market such

2 Emissions Trading in the U.S. (Pew Center on Global Climate Change, 2003).

3 Act Locally, Trade Globally: Emissions Trading for Climate Policy (OECD/IEA 2005), Reducing CO2 Emissions from Cars (German Advisory Council on the Environment, 2005), Service Contract to Carry Out Economic Analysis and Business Impact Assessment of CO2 Emissions Reduction Measures in the Automotive Sector (IEEP/ TNO/CAIR, 2005)

4 Agenda for Climate Action (Pew Center on Global Climate Change, 2006) advocates replacing CAFE with a market-based scheme but does not insist that it be integrated with a broader emissions market.

99

The ‘Low Carbon Road Transport Challenge’

M A R K E T- B A S E D S O LU T I O N S

Us�ng carbon markets to encourage the �ntroduct�on of low carbon veh�cles

Paper 2

as the carbon market or the US sulphur market, participants not only use the market to buy or sell once a year for compliance. They buy and sell often as part of their risk management programmes and employ derivatives such as futures and options.

A trading system limited to the auto industry is very unlikely to have sufficient liquidity. A paucity of market participants, and competitive sensitivities, would reduce companies’ willingness to use the market, reducing the capital that it can generate for investment in emission reduction technologies and activities. Financial intermediaries and speculators are also unlikely to devote adequate resources to enhance the liquidity of such a market.

There already is a vibrant carbon market in Europe which has liquidity, many active traders, low transaction costs and price transparency. This paper assumes that any market-based policy would be integrated with the EU ETS. Any market not connected to the EU ETS, however sophisticated in its construction, is likely to lack liquidity.

4. Designing a market-based policy for reducing emissions from new vehicles

There are a variety of design options for a market-based policy to reduce emissions from new vehicles. All of the options considered below are based on the current voluntary European standards for average fleet emissions. The basic approach to calculating the performance of a particular manufacturer would be:

Manufacturer A sells 1,300,000 vehicles per year across Europe. It has a fleet emissions average of 152.8 g/km, thus exceeding its target of 140g/km by 12.8g/km. Average annual mileage per vehicle is 16,000 km and bio-fuels constitute 10% of the fuel supply.

Manufacturer A’s liability is: 12.8g x 1,300,000 x 16,000 x .9 = 239,616 tonnes of CO2, or approximately 0.18 tonnes per vehicle At the current EU ETS price of CO2 of around €20 per tonne5, offsetting this liability would cost approximately €4.79 million or €3.60 per vehicle. At the current price for CDM carbon credits of €7 to €12 per tonne, offsetting this liability would cost approximately €1.7 to €2.9 million or €1.26 to €2.16 per vehicle.

Data calculations:• Figures for fleet average emissions and number of vehicles sold would be

calculated on the same basis as currently.

5 Approximate prices at 24th May, 2006.

1 2 3 4

Differencebetweenfleet

averageandtarget

Numberofvehiclessold

Averageannualmileage

pervehicle

Percentagefossilfuelsupply x x x

1010

The ‘Low Carbon Road Transport Challenge’

M A R K E T- B A S E D S O LU T I O N S

Us�ng carbon markets to encourage the �ntroduct�on of low carbon veh�cles

Paper 2

• A standard figure would have to be used for the average annual mileage per vehicle based on an agreed research methodology.

• Percentage of fossil fuel in fuel supply can be counted in the method used for the Renewable Transport Fuels Obligation.

Supporting the integrated approachThis gives the auto industry flexibility to meet its obligations through various methods. If it is unable to achieve the targets directly, it can work to increase the percentage of biofuels in the fuel supply, purchase carbon credits or, more speculatively, support driver education to reduce overall mileage and improve the fuel efficiency of driving.

This policy addresses emissions from new cars only. Over time, however, the policy on new cars will reach an ever greater percentage of the vehicle fleet.

5. Design options

There are many adjustments that can be made in the basic design of a trading system. To ensure liquidity it is crucial that, however complex the system design, the compliance value of the credit must be absolutely clear at the time of trade.

TargetsThere are a range of options for setting emissions targets, including using existing voluntary targets or setting simple percentage improvements from historical baselines. The key issue is whether to use a “relative” or an “absolute” target. An absolute target caps the total number of emissions from new vehicles per manufacturer. For example, if manufacturer A is projected to have sales of 1,300,000 vehicles in 2009 with an emissions target of 140g/km then its overall cap would be 1,300,000 x 140 x 16,000 = 2,912,000 tonnes of CO2

An absolute target is directly consistent with the approach of Kyoto and the EU ETS, which focus on total emissions levels. A relative target, by contrast, focuses solely on emissions per km per vehicle, but does not set a hard cap on total emissions.

On the other hand, an absolute target allows manufacturers with declining sales to avoid meeting the emissions target. For example, if emissions from manufacturer A’s vehicles averaged 150g/km, it would meet its target, so long as sales did not exceed 1,213,333 vehicles since 1,213,333 x 150 x 16,000 = 2,912,000 tonnes of CO2

Targets could follow a fixed schedule of reductions or they could be dynamic, whereby improvements in one compliance period are used to establish the target for future periods.

1111

The ‘Low Carbon Road Transport Challenge’

M A R K E T- B A S E D S O LU T I O N S

Us�ng carbon markets to encourage the �ntroduct�on of low carbon veh�cles

Paper 2

CreditingThe discussion above focuses solely on liabilities for failing to meet a target. The EU ETS also allows emitters that reduce beyond their targets to sell excess allowances, creating incentives to reduce emissions as much as possible. Carbon credits can be sold forward and the revenue used to fund the investment in activities and technologies that reduce emissions and hence generate credits.

Credits could also be issued as a reward for early action and for programmes to reduce overall vehicle emissions, such as a programme for scrapping older vehicles with high emission rates.

Relation to EU ETSIf manufacturers are issued with carbon credits for selling vehicles that emit at levels below a relative emissions target, a scenario is possible in which rising sales could offset increased efficiency. Thus the auto sector would be issued with credits even as total emissions from new vehicles were increasing. A similar concern was addressed in the design of the voluntary UK ETS which preceded the EU ETS by about three years. It included a “gateway” which ensured that no more credits flowed from emitters with “relative” targets to emitters with “absolute” targets than vice versa. Although this gateway never actually closed, this is a relatively complex and untested design feature. Access for car manufacturers to the broader carbon market (ie the EU ETS should be integrated if at all possible). There are various other ways this concern could be met, such as tightening the target to account for growth in the vehicle fleet.

BankingOne question to be examined is whether and how manufacturers can “bank” credits earned in one period to use for compliance in the next. The EU ETS currently allows banking within compliance phases only (i.e. 2005–2007 and 2008–2012). By contrast, the US SO2 market allows unlimited banking, the US NOx market employs “flow control” which discounts banked allowances once the total number exceeds a certain threshold and the CAFE programme allows credits to be banked for a maximum of three years. Uniquely, the CAFE programme allows “borrowing” credits from the future to meet current compliance needs. Worries about indefinite postponement of emission reductions or “busting the market” have generally prevented widespread adoption of borrowing.

Crediting/debiting periodThere are at least three options for the basis on which credits and liabilities accrue. If manufacturer A incurs a liability of 0.18 tonnes per vehicle, that liability might be incurred for one year only or it might incur a liability for the vehicle’s lifetime emissions, e.g. if the average vehicle has a useful life of 10 years, the manufacturer might incur a liability of 1.8 tonnes per vehicle in the year in which the vehicle is sold.

1212

The ‘Low Carbon Road Transport Challenge’

M A R K E T- B A S E D S O LU T I O N S

Us�ng carbon markets to encourage the �ntroduct�on of low carbon veh�cles

Paper 2

Alternatively, manufacturer A might be liable for 0.18 tonnes per year for 10 years. This would reduce the upfront liability and enable more effective risk management by allowing such liabilities to be offset against credits earned in future years.

Taking into account the lifetime emissions of vehicle fleets would ensure gradual coverage of total vehicle emissions. It would, however, mean that liabilities can accumulate that might endanger the economic viability of particular manufacturers. It also means that, eventually, car manufacturers would effectively become responsible for the greenhouse gas emissions of the nation’s drivers.

Conclusion

The use of market-based mechanisms would greatly ease the implementation of policies to reduce the emissions from new vehicles. It could significantly reduce the costs for vehicle manufacturers, increase their flexibility in meeting such targets and allow them to undertake effective risk-management by giving them access to global carbon markets. It would also reward the most efficient manufacturers and offer incentives for all manufacturers to maximize their revenues by exceeding the targets. There are few technical barriers to implementation of such policies. What remains to be determined is the potential role of such policies among the wide range of actions to be taken to combat climate change.

14

The ‘Low Carbon Road Transport Challenge’

R E g U L AT O Ry A p p ROAc h E S

15

The ‘Low Carbon Road Transport Challenge’

Options for carbon regulation of the European car industry

Alex VeitchEnergy Saving Trust1

1. Will the 2008/2009 target be met?

Background to the agreementsThe European Commission (EC) has established voluntary agreements on new-car carbon dioxide (CO2) emissions with the European (European Automobile Manufacturers’ Association – ACEA), the Japanese (Japan Automobile Manufacturers’ Association – JAMA) and Korean (Korean Automobile Manufacturers’ Association – KAMA) automobile industries. The agreements call for the average of new passenger cars sold in the European Union to be 140g/CO2 per km. This is to be achieved by 2009 by JAMA and KAMA, and by 2008 by ACEA (EC 2006).

Are the associations on track to meet the targets?The annual reduction rate required – if the targets are to be met by the agreed year – is around 3% for ACEA and JAMA, and nearer 4% for KAMA. In their Monitoring Report for the year 2003 (published in 2005) the EC asserted that ACEA and JAMA are on track to meet the 140g target, but acknowledge that the pace of CO2 reduction must increase (EC 2005). The picture for KAMA is less positive with the EC admitting: “There is a real risk that KAMA will not meet its 2004 intermediate target range of 165 to 170g/km, seeing that only one year is left to close the gap of 9g/km” (EC 2005).

It can be argued that the EC are taking a rather optimistic view, to say the least. In the UK, average new-car CO2 emissions stood at 169.4 in 2005, down by 1.2% from 2004 to 2005 – an improvement on the decrease of just 0.4% from 2003 to 2004 (SMMT 2005, 2006). If this pace of change is replicated across the EU, then it is unlikely that the voluntary agreement targets will be met. While official EU figures for 2004 and 2005 are not available, analysis by the environmental group T&E using commercially-available European car sales data concludes that the ACEA average for 2005 was 160g CO2/km – a reduction of only 1 per cent from the previous year.

If these figures are correct, ACEA members would need an unprecedented improvement rate of 4.3 per cent per year for the next three years to meet their commitment. To date, the best performance was 2.9 per cent, recorded in 2000 (T&E 2006). The key official statistics on current progress toward the target are summarised in the table below. It is worth noting that reporting on the voluntary agreements is frustratingly slow, with monitoring reports typically two years out of date, despite the fact that EU car sales data are readily available from

Paper 3

1 The views expressed in this paper are the author’s and do not represent those of the Energy Saving Trust or its members.

16

The ‘Low Carbon Road Transport Challenge’

R E g U L AT O Ry A p p ROAc h E S

Opt�ons for carbon regulat�on of the European car �ndustry

Paper 3

commercial providers2. There are also discrepancies between reporting from the auto industry, and member states3.

Table1 AutomanufactureraverageCO2,andannualraterequiredtomeetthevoluntarytargetSource:EC2005

What will replace the current agreements?As the agreement period comes to an end, the question of “what comes next” is looming large. On the basis of the current evidence, it is possible to voice strong doubts that the current voluntary agreement targets will be met, which in turn casts doubt on the whole voluntary approach. As the EC point out, KAMA are not currently on track, and if they fail to meet their target then “this could affect the whole approach on CO2” (EC 2005). In the original agreement, the EC reserved the right to regulate if the voluntary commitments are not met4, and regulation would presumably apply to the entire industry, not just one association. The remainder of this paper discusses possible options for this regulation.

2. Structural problems with the current agreement

Industry association approach is flawedThe vehicle manufacturers associations (ACEA, JAMA and KAMA) have no control over individual car companies’ production decisions. This allows car manufacturers in each association to “free-ride” on the achievements of others. An ACEA member, for instance, may simply be able to rely on other members reducing average CO2 emissions instead of cutting their own. Indeed, research commissioned by the EC into possible carbon regulation in the auto sector concluded that manufacturer associations are not appropriate legal entities for regulation since they do not control production and that CO2 targets should be set by regulation at the manufacturer level (IEEP/TNO 2005).

Risk of companies leaving the associationThere is a further risk that individual manufacturers may simply leave their relevant association and, therefore, avoid their CO2 obligations. This is, admittedly, a low risk and has happened only once: when Rover left ACEA on 30 April 2002, at a time when that company had only a one per cent share of the passenger car market in the EU (German Advisory Council, 2005). Nevertheless, this does set a dubious precedent.

2003Average Improvement Annualimprovement Association FleetEmissions from2002 tomeet140gtarget

ACEA 163 g/km 1.2% 2.8%

JAMA 172 g/km 1% 3.1%

KAMA 179 g/km 2.2% 3.6%

2 See for example the data used in IEEP/TNO 2005 and T&E 2006

3 The 2003 monitoring report notes that, if data collected by ACEA were taken, its average specific CO2 emissions would be 161 g/km as opposed to the 162 g/km reported by Member States

4 The introduction to the Agreement between ACEA and the EC states “the Commission intends to present a legislative proposal on CO2 emissions from passenger cars, should ACEA fail to achieve the CO2 emission objective for 2008 in its Commitment or not make sufficient progress towards this objective…and…should the Commission not be satisfied that such failure is due to factors for which ACEA cannot be held accountable;” Agreement with ACEA, 1999, ref (1999/125/EC)

17

The ‘Low Carbon Road Transport Challenge’

R E g U L AT O Ry A p p ROAc h E S

Opt�ons for carbon regulat�on of the European car �ndustry

Paper 3

Lack of transparencyNeither the industry associations nor the EC publish individual manufacturers’ progress on new car CO2. This limits transparency, causing problems for sustainable investment groups and stakeholders alike (SAM/WRI 2005). Interestingly, the EC originally said that its intention was to use its monitoring scheme to demonstrate the contributions of each manufacturer to their common commitment (T&E 2005). This intention has not translated into action.

Sales-based average approach reduces manufacturers’ control The voluntary agreement targets are based on the sales-weighted average across each association, rather than an average of models produced. This reduces the control that the car industry has over the success or failure of their agreement. Motor manufacturers strongly influence purchase decisions through their vast advertising budgets – indeed, the motor sector as a whole spent more on advertising in the UK than any other sector in 2003; a total of £934.6 million (WARC 2005). However, they cannot actually control the cars customers buy!

3. A new approach to regulation

Why regulate?There is a clear public good in requiring cars to achieve higher fuel economy, not only in terms of carbon emissions but also in reducing oil imports and cutting fuel costs for consumers. There is strong public support for regulation; in a 2005 poll of 970 consumers, 70% agreed with the statement: “Car makers should be legally required to make cars that get high MPG (miles-per-gallon)” (Energy Saving Trust 2005). Setting clear carbon reduction goals through regulation could therefore be a politically popular step, providing required industry stability. Regulations already exist in the major automotive markets of Europe, the U.S. and Japan, and have recently entered into force in China.

Targets: model range or sales-weighted?As noted above, the current regime is based on sales-weighted average CO2, which to some extent puts success or failure in the hands of consumers rather than manufacturers. Interestingly, however, in 2005 the sales-weighted average was lower than the non-sales-weighted average: in other words almost every car company sold more low carbon models than high carbon models5 (see Figure 1 for details from 20 large car companies). Arguably, while it would be simpler to use a model range average to set CO2 targets – in the UK at least – the major manufacturers benefit from the sales-based approach, selling more low-carbon than the high-carbon cars in their range.

5 The non-sales-weighted average is found by counting the number of models with certain CO2 emissions (e.g. the number of models with emissions of 160g/km), then by calculating the production of CO2 and the number of models, and dividing the sum of the products by the total number of models. The sales-weighted average is calculated the same way, except that sales of cars of certain CO2 emissions are added up, rather than the number of models.

18

The ‘Low Carbon Road Transport Challenge’

R E g U L AT O Ry A p p ROAc h E S

Opt�ons for carbon regulat�on of the European car �ndustry

Paper 3

Figure1 AverageCO2emissions:top20sellingcarcompaniesintheUK2005Source: EST analys�s of data from SMMT and VCA

4. Framing the regulation

Option 1: maximum CO2 limitIn other sectors (e.g. domestic boilers), market transformation in energy efficiency is driven by setting minimum efficiency standards, supplemented by other fiscal and information measures (such as the Energy Efficiency Commitment on household energy suppliers). Similar minimum standards could be introduced for passenger cars. Indeed, cars already meet minimum standards for noise and regulated pollutants.

One clear drawback of this approach is that the impact on average emissions of reducing the high-emitting ‘tail’ of the vehicle parc would initially be small (see Figure 2 showing the distribution of car sales in the UK by CO2 emissions). However, if the threshold were progressively reduced over time, it would provide a clear incentive to introduce low carbon technologies.

A more fundamental problem is that it would probably put a number of car companies out of business. Small niche producers such as Porsche, Ferrari and, possibly, even companies like Mercedes and BMW may find it hard to adapt to a world of maximum CO2 regulations. These brands are built on fast, powerful, high-CO2, high-value automobiles. A maximum CO2 limit, while simple and potentially effective in carbon terms, may be too politically sensitive to progress.

Figure2UKCarSales–DistributionbyCO2emissions(g/km)Source:SMMT

20

15

10

5

0under 100

120 140 160 180 200 220 240 260 280 300

Market Share (percentage) 25

2005

2000

1997

F�at

Skoda A

uto U

K Ltd

C�troen

Peuge

otFo

rd

Renau

lt Cars

Vauxh

all

Volkswag

en C

ars

Toyo

ta

Honda CarsK�a

N�ssan

Moto

rs

Hyunda�

M�n�

Aud�

Maz

da

Volvo C

arsBM

W

Merc

edes

Cars

Land Rove

r

Average CO2 (g/km) 350

300

250

200

150

100

50

Sales We�ghted

Model Range

0

320

CO2 em�ss�ons

19

The ‘Low Carbon Road Transport Challenge’

R E g U L AT O Ry A p p ROAc h E S

Opt�ons for carbon regulat�on of the European car �ndustry

Paper 3

Option 2: Company averageThe Company Average approach would essentially replicate the Corporate Average Fuel Economy (CAFE) regulations, which have been in place in the United States since the mid-1970s. CAFE requires automakers to produce vehicles to an overall average MPG standard, with no trading allowed, and separate standards for heavy SUVs and passenger cars – a loophole that has actually reduced the overall average fuel economy of new vehicles (Sierra Club 2005). A CAFE–style system would have the benefit of simplicity. However, introducing it in Europe would penalise higher-CO2 manufacturers who would have to change their entire model range to meet the standard.

An alternative to imposing the same company average CO2 target for every company could be to require each company to instead achieve a percentage improvement in average CO2 from an agreed baseline year. Alternatively, an average CO2 reduction target could be based on the size of vehicle produced. Both these options are suggested and discussed in detail in the IEEP/TNO report for the EC. The report concludes that both these options would offer high-CO2 manufacturers some much-needed flexibility, allowing them to gradually improve CO2 performance without changing utterly their model range (IEEP/TNO 2005).

Option 3: Industry average with internal tradingCarbon trading between companies would allow niche manufacturers to reduce new-car CO2 without radically changing their offer. However, there are problems with this approach. The IEEP/TNO report is not explicit in favouring internal trading over company-average targets. On the one hand, flexibility and trading should reduce compliance costs. On the other, trading between manufacturers may not be easy to establish. For example, there is the risk that companies earning credits may contrive to reduce liquidity in the system, pushing up the price of credits beyond their real market value (so-called “hamstering”) (IEEP/TNO 2005).

Option 4: External tradingIf car manufacturers were to enter existing carbon trading markets such as the EU Emissions Trading Scheme then there would need to be an agreed methodology for calculating lifetime carbon emissions from each company’s products. Taking full lifetime CO2 emissions into account offers a different perspective on companies’ relative environmental impacts. Smaller, “niche” producers with high average CO2 sell a comparatively low number of cars, while “mainstream” manufacturers with moderate average CO2 emissions sell so many cars that their overall carbon footprint is much higher. Figure 3 illustrates this point by comparing the sales-weighted average CO2 of the top 20 car sellers in the UK in 2005 with an estimated lifetime CO2 emissions of vehicle sold in that year.

20

The ‘Low Carbon Road Transport Challenge’

R E g U L AT O Ry A p p ROAc h E S

Opt�ons for carbon regulat�on of the European car �ndustry

Paper 3

Figure3 Comparison:AverageCO2andestimatedlifetimeemissions,2005Source:SMMTdata200,000kmvehiclelifetime.

Bringing car makers into existing carbon markets would offer additional flexibility. As well as – or instead of – making lower-CO2 cars, companies could sell fewer cars, produce measurable reductions in lifetime car usage, or buy carbon credits on the open market. Of these, the most contentious would be reducing car usage – mainly because of the difficulty of proving the impact that any one company could have on individuals’ behaviour.

Conclusions

The current voluntary agreement is structurally flawed and is in serious danger of failure. Carbon regulation for new passenger cars would be a popular measure and is necessary to provide industry with genuine certainty. In framing a regulation the key questions are whether to opt for a model-range – rather than sales-based average – and whether or not to use carbon trading, either internal or external.

The key problem with internal trading is the lack of liquidity and danger of “hamstering”. External trading would require a full carbon “footprint” to be developed and allowing auto manufactures credit for reducing car use is fraught with difficulties. The simplest option would be to avoid carbon trading altogether. A company-specific CO2 target would be clear and relatively easy to frame, while flexibility for higher-CO2 producers could be provided by a “utility” target or percentage improvement approach. This currently appears to be the most attractive option.

350

300

250

200

150

100

50

0

14

12

10

8

6

4

2

0

F�at

Skoda A

uto U

K Ltd

C�troen

Peuge

otFo

rd

Renau

lt Cars

Vauxh

all

Volkswag

en C

ars

Toyo

ta

Honda carsK�a

N�ssan

Moto

r

Hyunda�

M�n�

Aud�

Maz

da

Volvo C

arsBM

W

Merc

edes

Cars

Land Rove

r

Average CO2

Est�mated l�fet�me CO2 Em�ss�ons

Sales-we�ghted CO2 average M�ll�on tonnes CO2

21

The ‘Low Carbon Road Transport Challenge’

R E g U L AT O Ry A p p ROAc h E S

Opt�ons for carbon regulat�on of the European car �ndustry

Paper 3

Bibliography

ENDS Environment Daily 2005, Issue 1998

Energy Saving Trust 2005, Omnibus Survey by Ipsos Mori for EST, Base 1,001

EUCAR, 2002, “LIRECAR” Project

European Commission (EC) 2005, Implementing the Community Strategy to Reduce CO2 Emissions from Cars: Fifth annual Communication on the effectiveness of the strategy

EC 2006, Objectives of the agreements concluded with the automobile industry, EC Website, updated January 16, 2006 http://europa.eu.int/comm/environment/co2/co2_agreements.htm

Friends of the Earth, 10 November 2005, Press Release

German Advisory Council 2005, Reducing CO2 Emissions from Cars

Sustainable Asset Management (SAM)/World Resources Institute (WRI), 2005, Transparency Issues with the ACEA agreement: Are investors driving blindly?

Society of Motor Manufacturers and Traders (SMMT), 2005, UK New Car Registrations by CO2 Performance: Report on the 2004 market

SMMT 2006, UK New Car Registrations by CO2 Performance: Report on the 2005 market

Sierra Club 2005, The Biggest Single Step (Factsheet)

T&E 2005, Reducing CO2 Emissions from New Cars

T&E 2006, “Car industry failing on climate pledge” (Press release issued April 19, 2006)

Transport Research Ltd, 2004, Sustainable resource use in the motor industry: a mass balance approach

Toyota, 2004, Environmental and Social Report

World Advertising Resource Centre (WARC) 2005, The European Marketing Pocket Book

14

22

The ‘Low Carbon Road Transport Challenge’

Getting the genie back in the bottle:limiting speed to reduce carbon emissions and accelerate the shift to low carbon vehicles

Paper 4

Reduce CO2

Reduce Casualt�es

Dr Jillian Anable UKERC and the Centre for Transport Policy, Robert Gordon University

Paige MitchellThe Slower Speeds Initiative

Dr Russell LayberryUKERC, and the Environmental Change Institute, University of Oxford

IntroductionIn the discussion relating to the myriad of carbon abatement solutions from the transport sector, surprisingly little attention is paid to speed enforcement and reduction. Speed limits are rarely regarded as an innovative instrument to achieve carbon reductions or to alter the context for the supply and demand of low carbon vehicles. Where the carbon reducing potential is acknowledged, limiting speed is generally dismissed as not politically viable.

This paper will demonstrate that a lower, or even merely better enforced, top speed limit should not be ignored as it is one of the most certain, equitable, cost effective and potentially popular routes to a lower carbon economy.

The best available official data on the vehicle fleet, fuel consumption, emissions factors, traffic flows and speeds on motorways and dual carriageways have been used to develop a model to assess potential carbon savings between now and 2010 from (i) enforcing the current top 70mph speed limit and (ii) reducing this limit to 60mph. In addition, the wider effects of a lower top speed limit on traffic demand, vehicle design, traffic flow and road safety are explored. Together these provide an overview of the direct and indirect effects of speed on carbon emissions in the road transport sector. Figure 1 outlines the relationships explored in this paper:

Figure1 TherelationshipbetweenspeedenforcementandCO2reduction

REDUCE SPEED

Rat�onal�se Car Market

Improve Traffic Flow

Reduce Traffic Demand

2323

The ‘Low Carbon Road Transport Challenge’

R E g U L AT O Ry A p p ROAc h E S

L�m�t�ng speed to reduce carbon em�ss�ons and accelerate the sh�ft to low carbon veh�cles

Paper 4

The vital statistics: speed, motorway traffic and CO2 emissionsFuel consumption and carbon dioxide emissions are a function of speed, mileage, vehicle weight, engine and fuel type, driving style, traffic flow conditions and, to an increasing extent, optional features such as air conditioning. Figure 2 shows the relevant carbon dioxide emission curves for two engine size groups of Euro II cars1. Petrol Euro II cars with engines between 1.4 litres and 2 litres emit 10% less CO2 at 60mph than they do at 70mph. Diesel Euro II cars with engines under 2 litres emit about 16% less. At 80mph, Euro II petrol cars with engines between 1.4 litres and 2 litres emit 14% more CO2 per kilometre and cars with engines over 2 litres will emit 19% more CO2 than at 70mph.

Figure2 ChangesinCO2emissionswithspeed(Source:NETCENNationalAtmosphericEmissionsInventory)

Summaryfindings

• A properly enforced 70mph speed l�m�t would cut carbon em�ss�ons from road transport by nearly 1milliontonnesofcarbon(MtC)perannum, or nearly 5 MtC over 5 years.

• Anew60mphlimitwouldnearlydoublethisreduction, reduc�ng em�ss�ons by an average 1.88MtCayear,

or approx�mately 9.4MtCover5years.

• These sav�ngs, wh�ch are based on low project�ons of traffic growth, representbetween15%and29%ofthetotalsavingsexpectedfromthetransportsectorby2010,asstatedinthe2006ClimateChangeProgrammeReview(CCPR).

• These sav�ngs compare favourably to other pol�c�es �n the CCPR such as the 1.6 MtC expected from the Road Traffic Fuels

Obl�gat�on (RTFO), yet to be �ntroduced �n the UK.

• These figures assume that speed enforcement and reduct�on w�ll not affect travel demand. However, ifrestraintwereincludedinthecalculation,thereductioninemissionswouldbeevengreater.

• A better enforced 70mph l�m�t on motorways would preventover300deathsandseriousinjuriesperannum on

motorways alone. A 60mph l�m�t would preventover600deathsandseriousinjuries.

• Lower top speeds and the safety benefits would incentivisethemarketforlighterandlesspowerfulcars, thus �ncreas�ng

the carbon sav�ngs further.

• In�t�al �nd�cat�ons of cost are that th�s would be oneofthecheapestcarbonabatementpolices, across all sectors,

espec�ally when anc�llary benefits such as casualty and congest�on reduct�ons are cons�dered.

• Of all measures to manage the demand for travel by car, speedlimitsaresimultaneouslythemildest,moststraightforward,theleastintrusiveandmostegalitarianintheirimpacts.

g/CO2 per km 350

300

250

200

Petrol Euro II 1.4–2.0 l�tres

Petrol Euro II > 2.0 l�tres

45 50 55 60 65 70 75 80 85 90 95

D�esel Euro II < 2.0 l�tres

D�esel Euro II > 2.0 l�tres

150

100

40

mph

1 The way emissions vary with average speed for most vehicle types making up the national fleet has been calculated for the National Atmospheric Emissions Inventory (NAEI): NETCEN (2003) Vehicle Emissions Factor Database v02.8.xls

2424

The ‘Low Carbon Road Transport Challenge’

R E g U L AT O Ry A p p ROAc h E S

L�m�t�ng speed to reduce carbon em�ss�ons and accelerate the sh�ft to low carbon veh�cles

Paper 4

Motorways account for less than 1% of Britain’s total road length, yet account for 19% of total annual road mileage2, of which 75% is accounted for by ‘cars and taxis’. Driven speeds on motorways and dual carriageways are well above the optimum for fuel efficiency. Traffic is distributed across various speed bands, ranging from 50mph and below to 90mph and above3. These figures take current levels of congestion on the motorway network into account. During the morning and evening weekday peak, 51% and 48% of cars respectively exceed the motorway speed limit4. The average motorway speed during congested periods is 55mph5.

In 2003, road transport accounted for just under 33 MtC – 21% of the UK’s total CO2 emissions of 156.1 MtC6. Using the most recent figures7 on the distribution of distance travelled by each vehicle type in each speed band, 13.2 MtC was emitted by all categories of four-wheeled vehicles driving on roads with 70mph limits on motorways and in 2005. This is about 40% of the annual emissions by source from the road transport sector. This figure forms the basis of the calculations on potential carbon savings to follow.

How much CO2 could be saved by enforcing or reducing the current top speed limits on motorways and dual carriageways?

A model was developed to calculate the emissions savings from speed reduction and enforcement under a number of scenarios8. These included different speed limit scenarios (Business as usual (BAU), 70mph enforced and 60mph enforced) and different assumptions relating to the extent to which speed reductions will curb traffic growth.

Table 1 shows the annual and cumulative carbon savings from (i) enforcement of the current 70mph speed limit and (ii) enforcement of a 60 mph limit on motorways and dual carriageways, assuming that no change in mileage takes place as a result of the policy.

Table1 Carbonsavingsfromspeedenforcementonmotorwaysanddualcarriagewaysto2010

Taking 2006 as a baseline, our calculations show that carbon emissions would be reduced by between an average of 0.97 and 1.88 MtC in each year to 2010. These estimates are conservative because of our moderate estimates of traffic growth and the assumption that there would be no restraining effect on traffic growth. We take the potential impact on distances travelled into account below.

PerAnnumcarbonsavings(MtC) Totalcumulative savingsin 2006 2007 2008 2009 2010 2010

70mph enforced 0.94 0.96 0.98 1.00 1.00 4.87

60mph enforced 1.81 1.84 1.88 1.91 1.94 9.38

2 Department for Transport (2005) Road Traffic Statistics 2004

3 Department for Transport (2005) Vehicle Speeds in Great Britain: 2004, Table 1

4 Ibid, Table 2

5 Department for Transport (2004) A Measure of Road Traffic Congestion in England: Method and 2000 Baseline figures

6 http://www.defra.gov.uk/news/2005/050321a.htm

7 On 22nd December 2005, the DfT released a Freedom of Information (FOI) request for an analysis of the impact on carbon of changes to vehicle speeds. The figures provided in their spreadsheet formed the basis for many of the figures used in the model developed for this paper. See: http://www.dft.gov.uk/stellent/groups/dft_foi/documents/divisionhomepage/610911.hcsp

8 The following assumptions were used in the modelling:

– An average emissions coefficient reflecting fleet technology mix for each year and the relevant speed distribution based on 2004 data for motorways and dual carriageways. (Netcen (2003) Vehicle Emissions Factor Database; DfT (2005) Vehicle Speeds Great Britain 2004; and the FOI spreadsheet cited in note 7.

– For speed reduction scenarios, all of the distance previously driven above either 70mph or 60mph is redistributed to the highest remaining band.

– Figures for traffic growth are based on the National Traffic Model midpoint projections for interurban roads between 2000 and 2010 (29–35%). Given the actual growth rates witnessed since these projections were made, this appears to be a conservative estimate of growth, and therefore the emissions savings in the model may be an underestimate.

– Figures apply to all vehicles travelling in 70mph speed limits except motorcycles.

– Levels of non compliance with the speed limits are not accounted for in this model.

2525

The ‘Low Carbon Road Transport Challenge’

R E g U L AT O Ry A p p ROAc h E S

L�m�t�ng speed to reduce carbon em�ss�ons and accelerate the sh�ft to low carbon veh�cles

Paper 4

Given that the BAU projections for emissions from 4 wheeled vehicles on roads with 70 mph limits are projected in this model to be just under 14.6 MtC in 2010, this equates to a reduction of between 6.6% and 12.9% in 2010. As total road traffic (all roads and all vehicle types) is projected to be 34.5Mtc in 2010, this policy could be responsible for a reduction of between 2.8% and 5.4% of carbon emissions from this sector.

The scale of this reduction, given that it essentially limited to motorways and dual carriageways, is of a similar order to that projected by the Royal Commission on Environmental Pollution in 1994 in its influential report: Transport and the Environment.9:

‘Effective enforcement of the 70mph limit on dual carriageway roads and the 60mph limit on single carriageway roads would reduce casualties and would also lower carbon dioxide emissions from road vehicles by about 3%.’

The Commission found that a reduction of the speed limit on inter-urban roads to 55mph would achieve a further reduction of 3%. Our figure is also consistent with a recent assessment of the potential of a 55mph motorway speed limit to reduce oil demand in the case of a sudden disruption in supply. It is estimated that this measure would achieve a 3.3% reduction in transport fuel use in European countries10.

Additional carbon savings from speed enforcement and reduction

Recent carbon savings from improvements in vehicle efficiency have been eroded by offsetting changes in vehicle weight, performance and distance travelled. Countervailing demand management measures are needed if the benefits of greater fuel efficiency are to be realised. The argument for a lower speed limit is also primarily based on increasing fuel efficiency by ensuring that average speeds are closer to the optimum. However, a lower motorway speed limit has the advantage of being simultaneously a demand management measure by having an effect on traffic flow, journey time and the utility of high performance vehicles. Hence, speed enforcement could amplify the benefits of many of the changes that are being proposed to curb emissions from road transport in the following ways:

Reduction in traffic growthTraffic growth is at least partly driven by the ability to travel further, faster. Indeed, an important parameter determining the attractiveness of roads and other traffic infrastructure is the speed they permit. In 1994, the Standing Advisory Committee on Trunk Road Assessment concluded that ‘travel speed affects the amount of traffic’11 and this ‘speed elasticity’ can determine the traffic induced by the improvement of infrastructure12. SACTRA concluded that in the short term, half the time savings created by road improvements would be used for additional travel. In the longer term, nearly all the time savings would be used up in additional travel.

9 Royal Commission on Environmental Pollution (1995) Eighteenth Report: Transport and the Environment, Oxford: Oxford University Press (paras 12.23–12.26)

10 International Energy Agency (2005) Saving Oil in a Hurry, Paris: International Energy Agency

11 SACTRA (The Standing Advisory Committee on Trunk Road Assessment) (1994) Trunk Roads and the Generation of Traffic, London: HMSO

12 Pfleiderer, R. and Dieterich, M. (2003) Speed elasticity and mileage demand World Transport Policy and Practice Vol.9 (4), pp.21–27

2626

The ‘Low Carbon Road Transport Challenge’

R E g U L AT O Ry A p p ROAc h E S

L�m�t�ng speed to reduce carbon em�ss�ons and accelerate the sh�ft to low carbon veh�cles

Paper 4

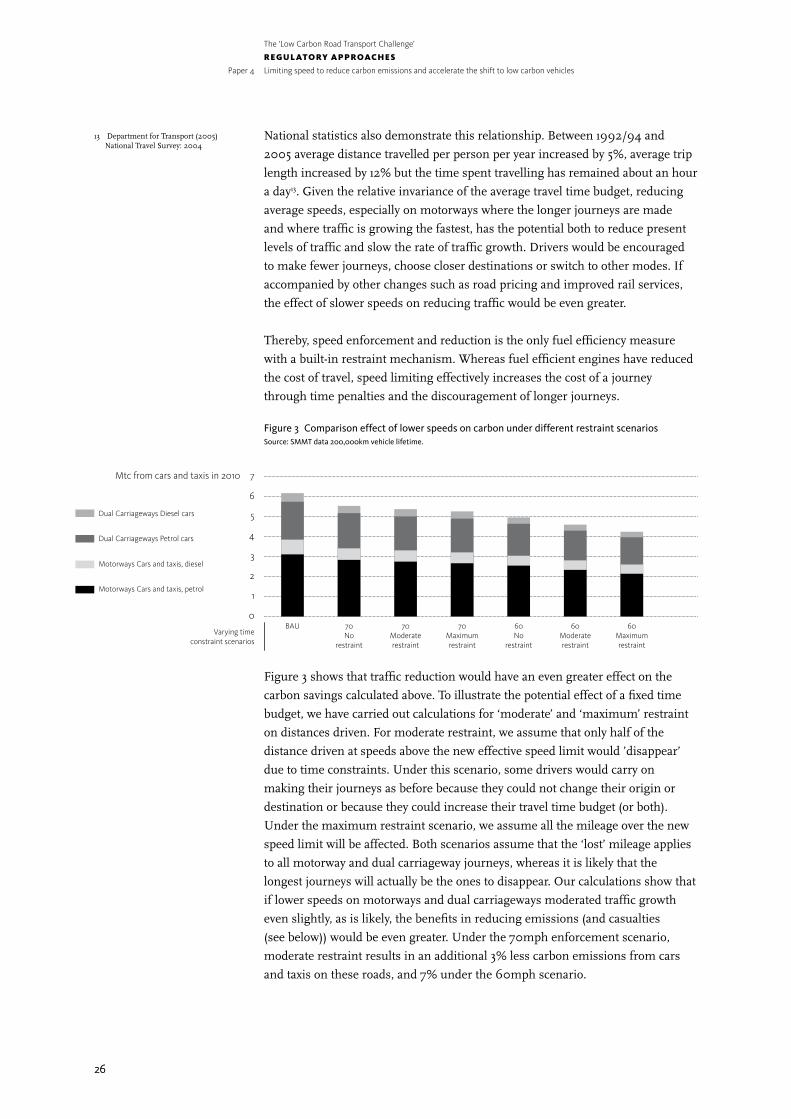

National statistics also demonstrate this relationship. Between 1992/94 and 2005 average distance travelled per person per year increased by 5%, average trip length increased by 12% but the time spent travelling has remained about an hour a day13. Given the relative invariance of the average travel time budget, reducing average speeds, especially on motorways where the longer journeys are made and where traffic is growing the fastest, has the potential both to reduce present levels of traffic and slow the rate of traffic growth. Drivers would be encouraged to make fewer journeys, choose closer destinations or switch to other modes. If accompanied by other changes such as road pricing and improved rail services, the effect of slower speeds on reducing traffic would be even greater.

Thereby, speed enforcement and reduction is the only fuel efficiency measure with a built-in restraint mechanism. Whereas fuel efficient engines have reduced the cost of travel, speed limiting effectively increases the cost of a journey through time penalties and the discouragement of longer journeys.

Figure3 ComparisoneffectoflowerspeedsoncarbonunderdifferentrestraintscenariosSource:SMMTdata200,000kmvehiclelifetime.

Figure 3 shows that traffic reduction would have an even greater effect on the carbon savings calculated above. To illustrate the potential effect of a fixed time budget, we have carried out calculations for ‘moderate’ and ‘maximum’ restraint on distances driven. For moderate restraint, we assume that only half of the distance driven at speeds above the new effective speed limit would ’disappear’ due to time constraints. Under this scenario, some drivers would carry on making their journeys as before because they could not change their origin or destination or because they could increase their travel time budget (or both). Under the maximum restraint scenario, we assume all the mileage over the new speed limit will be affected. Both scenarios assume that the ‘lost’ mileage applies to all motorway and dual carriageway journeys, whereas it is likely that the longest journeys will actually be the ones to disappear. Our calculations show that if lower speeds on motorways and dual carriageways moderated traffic growth even slightly, as is likely, the benefits in reducing emissions (and casualties (see below)) would be even greater. Under the 70mph enforcement scenario, moderate restraint results in an additional 3% less carbon emissions from cars and taxis on these roads, and 7% under the 60mph scenario.

Mtc from cars and tax�s �n 2010 7

6

5

4

3

2

1

0

BAU 70No

restra�nt

70Moderate restra�nt

70 Max�mum restra�nt

60 No

restra�nt

60 Moderate restra�nt

60 Max�mum restra�nt

Vary�ng t�me constra�nt scenar�os

Dual Carr�ageways D�esel cars

Dual Carr�ageways Petrol cars

Motorways Cars and tax�s, d�esel

Motorways Cars and tax�s, petrol

13 Department for Transport (2005) National Travel Survey: 2004

2727

The ‘Low Carbon Road Transport Challenge’

R E g U L AT O Ry A p p ROAc h E S

L�m�t�ng speed to reduce carbon em�ss�ons and accelerate the sh�ft to low carbon veh�cles

Paper 4

Maximising existing capacity by improving traffic flowHighway capacity is also a function of speed. The highest speed at which maximum capacity is safely and reliably achieved is 60mph. The traffic smoothing effects of a 60mph limit would help to reduce harsh driving styles and overtaking which can cause flow breakdown, crashes and disruption, further reducing CO2 emissions and optimising existing capacity. Making better use of existing capacity would render motorway widening schemes unnecessary. Creating additional capacity by widening would ultimately generate traffic, increase CO2 emissions and make their reduction even more intractable. A speed limit of 60mph or less would increase capacity while simultaneously discouraging traffic growth due to the restraining effect of lower speeds.

Rationalising car designSetting a limit to the top speeds acceptable on the public highway could trigger far-reaching changes to vehicle design, reducing impacts across the network and effectively acting as a ‘system boundary’ to the ever increasing cycle of counter-efficient vehicle design and longer distance travel.