36

LUX ACTUARIES & CONSULTANTS BAHRAIN | CYPRUS | INDIA | UAE Portfolio Transfer IA Report American Life Insurance Company (CY) LTD 12 June 2015

L U X A C T U A R I E S & C O N S U L T A N T S

B A H R A I N | C Y P R U S | I N D I A | U A E

Portfolio Transfer IA Report

American Life Insurance Company (CY) LTD

12 June 2015

1 Introduction 1

2 Executive Summary 3

3 Overview of MetLife Europe Limited 7

4 Overview of American Life Insurance Company (CY) Ltd 11

5 Outline of the Transfer 16

6 Financial Impact 18

7 Risk Profile Changes 21

8 Impact Assessment on Policyholders 23

9 Policyholder Communication 27

Appendices

Appendix A: Marios Schizas CV i

Appendix B: Sources of Data ii

Appendix C: Corporate Structure iv

Table of Contents

MetLife Portfolio Transfer IA | Page 1

1 Introduction

1.1 Purpose of the Report

I have prepared this report as an Independent Actuary (“IA”) on the Transfer of American Life

Insurance Company (CY) Ltd (“MetLife CY”) portfolio to MetLife Europe Limited (“MEL”) for the

purpose agreed under our engagement letter dated 08 January 2015. The transfer covers both life

and non-life portfolios of MetLife CY. This report has been prepared in accordance with the Cyprus

Law on Insurance Services and other related issues, 2002-2013 (“Insurance Law”), and the provision

of Article 115, Articles 102-106 for life business, and 107-111 for non-life business and we understand

the reliance that may be placed on it by policyholders and other related parties such as the Cyprus

Superintendent of Insurance in understanding the impact of the proposed transfer on the affected

policyholders.

In compiling this report Lux Actuaries & Consultants Cyprus Ltd (“Lux”, “we”) have held regular

meetings/calls with the management of both MetLife CY and MEL to obtain detailed information

around the transfer and understand the impact on policyholder protection and security, along with

reasonable expectations both before and after the transfer.

1.2 Reliance & Limitations

This report has been prepared particularly for the use of the bodies or persons listed below:

The Courts of the Republic of Cyprus

The Cyprus Superintendent of Insurance (“Regulator” or “SoI”)

The Central Bank of Ireland (“CBI”)

The directors and senior management of MetLife Cy and MEL

The policyholders and insured lives of MetLife CY

The report must be considered in its entirety, as reading individual sections in isolation could be

misleading.

In compiling this report several sources of information have been considered which have been

received exclusively from the management of MetLife CY and MEL, which are listed in Appendix B. I

have placed reliance on the accuracy of all information received and should not be held liable for any

conclusions drawn as a result of considering inaccurate data or information. Any tax implications have

been taken directly from the tax experts of MEL.

No liability will be accepted by Lux, or me, for any application of this Report for the purpose for which

it was not intended, nor for the results of any misunderstandings by any user of any aspect of the

report. If other persons choose to rely in any way on the contents of this Report then they do so

entirely at their own risk.

1.3 Independent Actuary

With regards to the definition for Independent Actuary included in the insurance Law I hereby confirm

that I am a Fellow of the institute of Actuaries, having qualified in 2004, and an Executive Director of

Lux. I am also a Fellow of the Cyprus Association of Actuaries and acting as Appointed Actuary for a

number of Life Insurance and Reinsurance companies. I am aware of the fact that my duty to the

Court overrides any obligations to those that appointed me in this position and accept this

responsibility. The Regulator has approved my appointment as an Independent Actuary for this

transfer.

MetLife Portfolio Transfer IA | Page 2

1.4 Independence

Lux has performed actuarial review work for MetLife CY between 2010 and 2012. This work stream

ended in 2012 and since then Lux has not performed any audit or advisory work for either MetLife CY

or MEL.

I have no insurance policies with either MetLife CY or MEL and neither I nor my immediate family

have any financial interest in either of them.

1.5 Peer Review Process

Dimitris Dimitriou, an executive director of the Lux team of similar seniority and experience has acted

as peer reviewer on this engagement and is responsible for quality assurance.

1.6 Disclosures

This report may not be published or made available without my written consent, apart for the parties

mentioned in the Reliance & Limitation section and making the report available for inspection by or

circulation to policyholders as required by legislation or in order to meet any other specified legal

requirements. A summary of this report may not be made and distributed to any party without my

written consent.

1.7 Technical Actuarial Standards

This report has been prepared in accordance with the relevant UK Technical Standards (TASs)

including the Technical Actuarial Standards on Reporting Actuarial Information (TAS R), Modelling

(TAS M), Data (TAS D) and the Insurance TAS. Additionally, a specific TAS on Transformations (TAS

T) has been adhered to in the production of the report.

This report constitutes an aggregate report as defined by the Financial Reporting Council of the UK in

its Technical Actuarial Standard on reporting actuarial information, ‘TAS R’. A number of data sources

have been used, exclusively provided by MetLife CY and MEL, to support the efforts of the

Independent Actuary assessment. A full list of the material used in this assessment is provided in

Appendix B.

To the extent possible, all material matters have been considered in the preparation of this report.

Where material uncertainty exists, I have tried to indicate the extent that the existence of such

uncertainty may influence the final results.

MetLife Portfolio Transfer IA | Page 3

2 Executive Summary

2.1 Overview

This report sets out my findings, considerations and conclusions of my review in relation to the

proposed transfer of MetLife CY portfolio to MEL. The main area of my consideration relates to the

impact of the proposed transfer on the policyholder and beneficiaries expectations and security of the

existing policyholders and beneficiaries of MetLife CY and MEL. Throughout this report any reference

to policyholders applies equally to the corresponding beneficiaries and insureds. My review does not

take into account any future potential transfers to MEL or any new business written following the date

of the proposed transfer. The transfer is expected to be completed on 01 January 2016 when the

statutory basis for reporting liabilities will be Solvency II and hence, in my review and findings for

forming my opinion, I have concentrated on figures provided under that basis.

The table below provides Solvency II figures for MetLife CY and MEL pre and post transfer as at 31

December 2014:

Table 2.1 Solvency II Comparisons

ALL FIGURES ARE IN €M

31-DEC-14

MEL EXCL CY

METLIFE CYPRUS

METLIFE CYPRUS TO

MEL

MEL INCL. CY

Total Assets 9369.3 387.6 266.7 9636.0

Technical Provisions 7577.3 261.6 261.6 7838.8

Other Liabilities 597.2 5.1 5.13 602.3

Total Liabilities 8174.5 266.7 266.7 8441.2

Available Assets 1194.9 120.9 0 1194.9

Solvency Capital Requirement

Regulatory Minimum 493.6 43.6 522.9

Risk Appetite Target 617.0 54.4 653.7

Solvency Ratio 242% 278% 228%

2.2 Key Findings

In my review of the information received and from the discussions I had with the management of MEL

and MetLife CY, I have noted the following key findings:

Only a portion of MetLife CY assets equal to the Total Liabilities as at 31 December

2015 are being transferred to MEL. Total Liabilities refer to the MetLife CY liabilities

calculated under Solvency II basis and include the Best-Estimate Liability (BEL), the

Risk Margin (RM) and other Solvency II liabilities. As per the Business Transfer

Agreement the remaining of the assets which will include the joint venture with

Hellenic Bank, will remain at MetLife CY. At the time of writing this report no further

information on the particular assets to be transferred has been available - A work

stream for defining these is currently in progress and is expected to complete prior to

the transfer date. Note that the terms of the Business Transfer Agreement would

allow for the transferred assets to further include an amount equivalent to the

Transfer Consideration, of a de minimis amount, which I have ignored for the

purposes of this report.

A large proportion of the in-force portfolio carries reversionary and/or terminal bonus

additions – this business represents around 70% in terms of MetLife’s Solvency I

MetLife Portfolio Transfer IA | Page 4

liabilities. This does not include products that carry only Excess Interest Benefit

additions. I refer to this as participating business in the rest of this report to

distinguish it from those other products historically reported by MetLife CY as with-

profits business as described in section 4.2. These products do not have the usual

features of UK ‘with-profit’ products however there is a significant element of

discretion in the determination of bonus rates and hence pay-outs for these policies.

The current bonus methodology for participating contracts is complex and is linked to

a prospective surplus calculation under a number of scenarios. Additionally, there is

an element of discretion within the bonus determination. MetLife CY and MEL have

commissioned consultants to propose clarifications in the bonus declaration

methodology. The proposed methodology which has been endorsed by both MEL

and MetLife CY is a formulaic approach for setting bonus rates based structured in

such a way as to be similar to, although not the same as, the Excess Interest Benefit

described in Section 4.1. I have been informed by MetLife CY that under the

proposed methodology there will be no changes in the terms and conditions of the

policies. The parameterisation of this approach has not been finalised at the time of

writing this report however I have been informed by MetLife CY that the parameters

will be set in a way to:

- Preserve the Policyholder Reasonable Expectations (PRE)

- Reduce discretion where applicable and hence enhance transparency and

ease of communication to policyholders

In relation to the participating business reference assets, the management of MetLife

CY has provided evidence that there is no requirement for ring-fencing those assets

under Solvency II. Allowance however will have to be made for the investment mix of

the assets to be used for the determination of the asset earned rate in the

determination of reversionary and terminal bonuses to preserve PRE for participating

business. At the time of writing this report, the actual assets on which the earned rate

will be made under the proposed bonus methodology has not been finalised. The

management commissioned a project to define those assets and make sure that they

will not materially affect PRE.

At the proposed transfer date 01 January 2016 Solvency II will have been

implemented by both jurisdictions, by MetLife CY in Cyprus and MEL in Ireland.

Based on the transaction design only market value of assets equal to the Total

Liabilities of MetLife CY will be transferred to MEL based on the Business Transfer

Agreement. It is therefore of significant importance that the transfer does not happen

prior to that date. Completion of the transfer prior to that date will potentially create a

gap of an estimated €186.6million due to Irish Solvency I being more onerous than

Solvency II. This funding gap will have to be considered in case the transfer moves

forward, however management confirmed that the transfer will not take place prior to

Solvency II implementation.

I have reviewed the Solvency II valuation basis used to generate the MetLife CY best-

estimate liability and can confirm that assumptions are in line with the latest

experience investigations. Some assumptions have been based on out-of-date

experience investigations and management confirmed that these will be updated in

the last quarter of 2015 prior to the generated final best-estimate liability figures.

Updated assumption parameters and relevant backing evidence will be provided

closer to the transfer date when up-to-date figures will become available. I am

however comfortable that the methodology followed for the derivation of the Solvency

II best-estimate liabilities as described in the various documentation received is

compliant with the latest EIOPA guidelines issued in respect to that.

MetLife Portfolio Transfer IA | Page 5

2.3 Conditions Prior to Transfer

In forming my opinion, I have relied on a number of conditions that should be fulfilled prior to the

implementation of the proposed transfer. These are:

The Solvency II balance sheet for both MEL and MetLife CY should be updated and

based on data and assumptions as at 30 September 2015 and submitted to the

Independent Actuary in the fourth quarter of 2015. All assumptions used should be

backed by experience investigation where applicable or relevant market experience

where company experience is not statistically significant.

The formulaic approach for defining the bonus determination of all participating

policies should be fully defined and parameterised and submitted to the Independent

Actuary in the fourth quarter of 2015. Testing should be carried-out and presented to

demonstrate that the proposed approach meets PRE and is equitable between

policyholders. This work stream is currently in progress and is expected to be

completed and approved by the MEL Appointed Actuary prior to the transfer date and

go through any additional governance required by MEL and MetLife CY.

The work stream in relation to the assets transferred to MEL should be completed

and the proposal of which should be approved by the relevant bodies prior to the

transfer date.

Regulatory approval is granted from both the Cypriot and Irish regulators.

The Boards of MetLife CY and MEL approve the proposed transfer as outlined in this

report.

2.4 Opinion

Based on my review of all documentation provided by the management of both MEL and MetLife CY

and regular discussions held with key team members of both Companies to understand the impact on

policyholders of the proposed transfer, I note the following:

Only assets sufficient to cover Total Liabilities of MetLife CY will be transferred to

MEL. The expected incremental SCR for MEL to cover risks of the transferred

portfolio is €23.7million and this will be covered by excess assets within MEL. Based

on an implied target capital requirement of 125% of SCR there is €662million of

projected surplus assets within MEL as at 31 December 2016 hence I do not expect

that this will have any material impact on MEL’s Solvency Position and coverage

ratio.

MEL is anticipating significant business volumes through its various branches in the

future. Any comments and conclusions expressed in this report do not take into

account this business plan. This however will enhance the strategic importance of

MEL to the overall MetLife Inc. (“MetLife”) restructure and consolidation.

Policyholder reasonable expectations and service quality is unlikely to be impacted by

the transfer since no changes to existing third party agreements, reinsurance and/or

other internal and external operational arrangements are directly linked to the

transfer.

Given that MEL & MetLife CY share the same ultimate shareholders there is no

difference in terms of the route down which equity contributions can potentially be

made if and when required. MEL has an A+ rating from S&P which is partly

predicated on S&P’s view of the strategic importance of MEL to MetLife Inc. while

MetLife CY has no rating. MetLife CY’s portfolio post-transfer will be part of an entity

of higher strategic importance to MetLife hence it is not expected to enjoy less

support from the parent company than it currently does.

MetLife Portfolio Transfer IA | Page 6

Having considered the impact of the transfer on policyholders, and assuming that all conditions

required prior to the transfer as listed above are met, it is my opinion that the proposed transfer:

will not have a material adverse impact on the security of existing MEL’s

policyholders

will not have a material impact on the security of MetLife CY’s transferring

policyholders

will not affect the contractual obligations of with and without profit and unit-linked

policyholders

will not materially affect the policyholder reasonable expectations of with-profit

policyholders

will not be materially disadvantageous to any of the with-profit policyholders, groups

of policyholders and/or to policyholders as compared with shareholders

will not adversely affect the service quality of MEL’s and MetLife CY’s transferring

policyholders

MetLife Portfolio Transfer IA | Page 7

3 Overview of MetLife Europe Limited

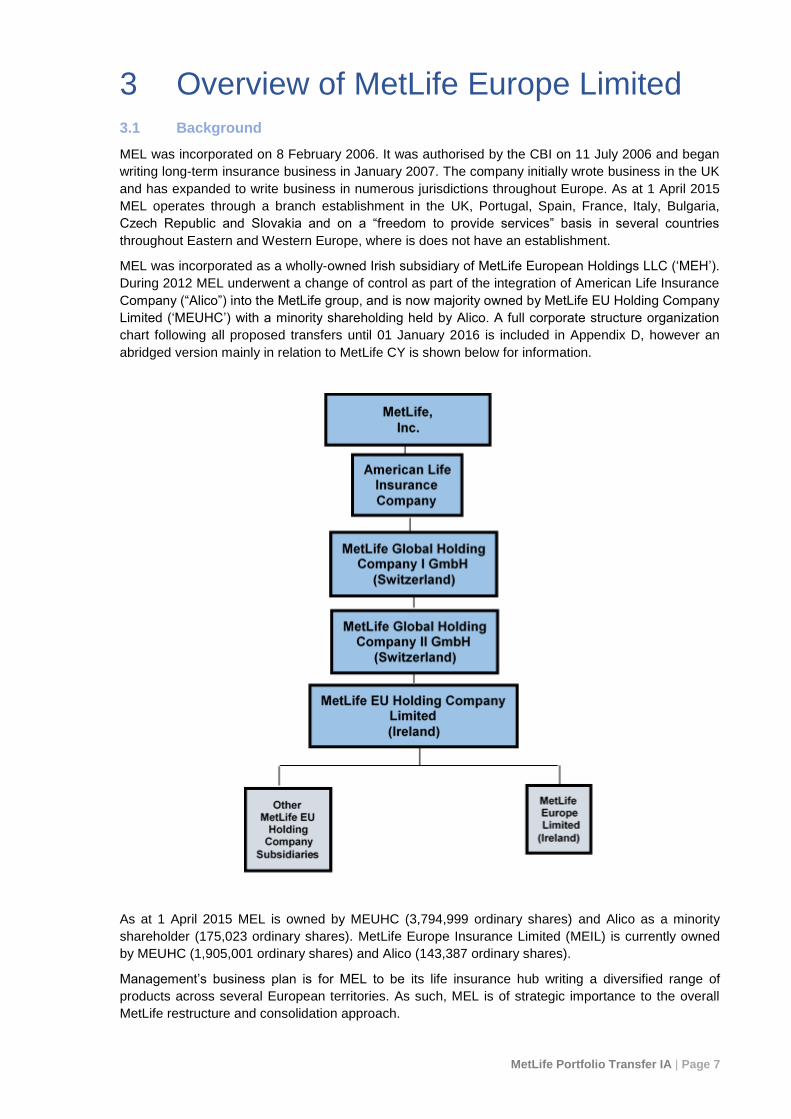

3.1 Background

MEL was incorporated on 8 February 2006. It was authorised by the CBI on 11 July 2006 and began

writing long-term insurance business in January 2007. The company initially wrote business in the UK

and has expanded to write business in numerous jurisdictions throughout Europe. As at 1 April 2015

MEL operates through a branch establishment in the UK, Portugal, Spain, France, Italy, Bulgaria,

Czech Republic and Slovakia and on a “freedom to provide services” basis in several countries

throughout Eastern and Western Europe, where is does not have an establishment.

MEL was incorporated as a wholly-owned Irish subsidiary of MetLife European Holdings LLC (‘MEH’).

During 2012 MEL underwent a change of control as part of the integration of American Life Insurance

Company (“Alico”) into the MetLife group, and is now majority owned by MetLife EU Holding Company

Limited (‘MEUHC’) with a minority shareholding held by Alico. A full corporate structure organization

chart following all proposed transfers until 01 January 2016 is included in Appendix D, however an

abridged version mainly in relation to MetLife CY is shown below for information.

As at 1 April 2015 MEL is owned by MEUHC (3,794,999 ordinary shares) and Alico as a minority

shareholder (175,023 ordinary shares). MetLife Europe Insurance Limited (MEIL) is currently owned

by MEUHC (1,905,001 ordinary shares) and Alico (143,387 ordinary shares).

Management’s business plan is for MEL to be its life insurance hub writing a diversified range of

products across several European territories. As such, MEL is of strategic importance to the overall

MetLife restructure and consolidation approach.

MetLife Portfolio Transfer IA | Page 8

3.2 Nature of Business

MEL is authorised by the CBI to undertake life assurance business in the following classes:

Class I: life assurance and contracts to pay annuities on human life; (Occupational

Pension policies are reported under Class I as per Irish Regulations)

Class III: life assurance and contracts to pay annuities, linked to investment funds;

Class IV: individual and group permanent health insurance.

During September 2012 MEL received permission following a Variation of Permissions (‘VoP’)

process with the CBI to extend its authorization and is now eligible to write the following business:

Class VI: capital redemption operations based on actuarial calculations whereby, in

return for single or periodic payments agreed in advance, commitments of specified

duration and amount are undertaken. This business is written in Italy.

Classes 1 and 2: non-life supplementary insurance, in particular insurance against

personal injury including incapacity for employment, insurance against death resulting

from an accident and insurance against disability resulting from an accident or

sickness.

Historically MEL’s primary focus has been to write predominantly unit-linked business with investment

performance guarantees. However, more recently MEL has begun to write non-linked investment and

protection business.

From late 2010 onwards MetLife commenced a global restructuring project to integrate the Alico

businesses with its own existing businesses. In Europe the project also focussed on preparing

MetLife’s EEA operations for Solvency II.

In 2012 MetLife completed its first cross border mergers and portfolio transfers into MEL and where

appropriate its non-life sister company MEIL. As of 1 April 2015 the following transfers have been

completed.

2012 portfolio transfers Spain and Portugal

2012 three way cross border merger from an Italian and Irish company into MEL

2013 cross border merger from France to MEL and portfolio transfer to MEIL

2013 UK portfolio transfers to MEL and MEIL

2014 cross border merger from Bulgaria into MEL

2015 cross border mergers from Czech Republic and Slovakia to MEL with portfolio

transfers to MEIL.

The European Participating Business (‘EPB’) includes benefits with participation dependent on

investment performance (and for certain Portuguese products, on other items of technical profit). The

participation is formulaic rather than discretionary, with a defined bonus calculation and reference

investment portfolios of fixed income assets to support the participation. The benefits on these

products also offer guaranteed minimum annual increases.

A detailed breakdown of the Long-Term Business by country is provided in the tales below:

MetLife Portfolio Transfer IA | Page 9

Table 3.1 MEL Lines of Business

(FIGURES AS AT 31/12/2014 IN €000)

TERRITORY POLICY COUNT Irish Solvency I

Liabilities

Regular Annualised

Premium Single Premium

UK * 212,176 7,124,737 97,278 731,479

Spain 1,355,909 406,802 58,099 15,766

Italy 1,285,388 260,253 37,908 33,356

Portugal 297,842 424,821 35,214 17,761

France 1,022,609 246,994 133,839 -

Total 4,173,924 8,463,607 362,337 798,362

*This includes the FOS, ML and MIL business

MEL has a range of reinsurance treaties in place both with a number of third parties, with credit rating

of A and above, and also with some intra-group counterparties. The key reinsurance treaties currently

in place are summarised as follows:

Conventional risk transfer treaties on Risk & Projection (‘R&P’) business – quota-

share, individual surplus, catastrophe excess of loss;

Multinational captive treaty on R&P business – MetLife via MEL acts an intermediary

between a multinational client’s subsidiary company in Europe and the captive insurer

of said multinational client. MEL’s role is to act as the direct writer ceding risks into

Alico for retrocession to the client captive;

Distribution driven treaties on R&P business – some of the commercial partners who

reinsurance entity, with minimal retention of risk by MEL; and

Intra-group reinsurance treaties with MetLife entities – for UK unit-linked products

with investment guarantees (“VA”), UK fixed term annuities, French term life

business, UK group life and lapse swaps on whole of life and endowment contracts in

various territories.

3.3 Investment & Capital Management

Investment management of MEL’s linked policyholder funds is provided by external fund managers.

MEL’s other assets are managed through an agreement with MetLife Investments Limited.

Non-linked assets are managed by MetLife Investments Limited subject to asset-liability matching

(“ALM”) guidelines set by the MEL Investment Committee. The non-linked invested assets of

portfolios are classed as either interest sensitive or otherwise. Each investment portfolio is then

subject to ALM Guidelines, covering asset type, currency, quality, target mix, concentration limits, and

duration targets (of particular importance for interest sensitive portfolios).

The Board of MEL has set a range of constraints on the target solvency positions to facilitate the risk

management of the business. These capital constraints are detailed below:

Sufficient capital must be held to ensure the financial implications associated with any crystallisations

of risks to which it is exposed can be met in full.

Following Solvency II implementation, the target capital will be based in relation to Solvency II ratios.

As stated in the MEL Risk Strategy and Appetite documentation, MEL's current target solvency capital

ratio is 125% of the Solvency Capital Requirement ('SCR')

Dividend Policy Considerations – Proposed dividends will be considered by the Board of MEL on a

case by case basis, taking into account the expected capital position over a 12 month time horizon

and the risks to that capital position, but in any case will not result in the Company going below the

target ongoing solvency level.

MetLife Portfolio Transfer IA | Page 10

3.4 Administration & Governance

MEL operates using a mixed administration business model with a number of key services being

provided by third parties. Whilst several key in-house functions are being supported by outsourced

services, significant in-house resources in the areas of Operations, Product Development, IT and

Finance, Risk Management and Actuarial are spread across MEL’s head office in Dublin and the

branch offices spread out through-out Europe. Any outsourced service to key functions is provided by

group-internal outsourcers.

MEL operates a management framework designed to actively control and facilitate the ongoing

management of the risks and opportunities to which it is exposed. The objective of the framework is to

ensure that effective risk management is integrated into the business practices and systems at all

levels within the business. To ensure this is adhered to, all branch businesses are required to report

back to the MEL Chief Risk Officer on at least a weekly basis and to the MEL Executive Risk

Committee every month. The results of the branch risk assessments are consolidated by the Risk

Function in Dublin. The Board ensures that the risk management and internal controls reflect the risk

appetite and that there are adequate arrangements in place to ensure that there is regular reporting to

the Board on compliance with the risk appetite.

MetLife Portfolio Transfer IA | Page 11

4 Overview of American Life Insurance Company (CY) Ltd

4.1 Background & History

Alico Cyprus was established in 1955 and operated as a branch of the American Life Insurance

Company (“Alico US” or “Alico”) in the Cypriot life insurance market for more than 50 years. After

Alico’s acquisition by MetLife in November 2010, the Alico Cyprus branch became part of MetLife, and

the trademark was changed to MetLife Alico. The Branch’s ultimate controlling party is MetLife.

MetLife is a global insurance group, US domiciled, founded in 1868 and operating through

subsidiaries and affiliates in over 50 countries. After the acquisition of Alico in 2010, MetLife became

a global insurance provider servicing around 90 million customers all over the world. The Alico Cyprus

branch was part of the Alico acquired business.

MetLife has undergone a global restructuring project and as part of this global restructuring project,

the insurance portfolio, assets, liabilities and business relationships were transferred from the Branch

of American Life Insurance Company to the company MetLife CY in 2013. The remainder of this

section outlines background information around MetLife CY’s structure, business, financial position

and operations. MetLife CY currently operates in Cyprus as a subsidiary of Alico US. It is required to

satisfy reporting and reserving requirements in line with the local Cypriot insurance regulations.

4.2 Nature of the Business

MetLife CY’s insurance portfolio includes traditional policies where the policyholder is entitled to

participate in the company profits (“with-profit” policies) such as whole of life, endowment, deferred

annuity products, non-profit individual life products (whole of life, endowment and term assurance

products) and rider (supplementary) policies, as well as unit-linked, personal accidents, group

annuities, group life and group medical products.

The in-force portfolio as at 31 December 2014 included 69,661 individual and group life, and accident

and health policies corresponding to €37 million of annual premiums including rider premiums.

The following table shows a breakdown of the Branch’s statutory reserves gross of reinsurance as at

31 December 2014 including provision in respect of outstanding insurance claims.

MetLife Portfolio Transfer IA | Page 12

Table 4.1 MetLife CY Cypriot SI Statutory Reserve

PRODUCT

STATUTORY RESERVE GROSS OF REINSURANCE –

Q4 2014

€million

With-profit - Business with reversionary and terminal bonuses 119.1

With-profit - Deferred annuities with Excess Interest Benefit and terminal bonus 70.8

With-profit - Business with Excess Interest Benefit Only 36.7

Non-profit business 10.0

Riders 1.7

Unit linked 26.8

Individual personal accident 3.1

Group life 2.6

Group Annuities 8.6

Group medical and personal accident 1.8

Group Personal Accident 1.0

Resilience reserve 27.4

Total 309.6

The with-profit portfolio consists of a mixture of whole of life and endowment (including pure

endowment) type products and deferred annuities. This group can be sub-divided into three

categories, namely:

- endowment/whole of life with reversionary (regular) and terminal bonuses (issued

prior to 2001)

- deferred annuities with Excess Interest Benefit and terminal bonus (closed to new

business in 2002), and

- endowment/whole of life/deferred annuity with Excess Interest Benefit only

For ease of reference in this report I have labelled the first two as participating business. Participating

business makes up the largest part of the life business and a large portion of these policies have

relatively high guaranteed rates of return varying for 4.25% to 6.0%.

The Excess Interest Benefit is essentially an additional benefit equal to the part of the return earned

on the underlying assets backing the portfolio over and above the technical interest rate after allowing

for expenses. This is defined in a formulaic way on policy documentation. The level of the announced

earned yield rate is determined each year by the Board of MetLife CY based on the investment

performance and on the advice of the Appointed Actuary. All declared benefits are guaranteed.

The older contracts offer a combination of reversionary and terminal bonuses without a minimum

guaranteed amount similar to UK with-profit contracts. Bonuses are expressed as a percentage of the

initial sum assured. There is also a block of deferred annuity contracts issued prior to 2002 that have

the Interest Benefit and Terminal Bonus features. The methodology applied by the MetLife CY to

calculate the amount of these additional benefits tends to be consistent from year to year. The

reversionary and terminal bonuses are declared on the entire participating business portfolio, as

opposed to on a per product basis. The reversionary bonuses are treated as additional paid up

benefits increasing the sum assured of the policy. Once declared, these are guaranteed for the

lifetime of the policy. In addition terminal bonuses may also be declared and are payable upon death,

surrender after the 10th policy anniversary or maturity. Terminal Bonuses are not included in the

surrender value of the Deferred Annuity contracts.

MetLife Portfolio Transfer IA | Page 13

The amount of annual discretionary benefits declared is determined by the Board of MetLife CY

based on the advice of the Appointed Actuary following an ALM study that takes into account the

projections of assets and liabilities to test the sustainability of bonus rates under specific scenarios, in

order to comply with the relevant Delaware regulations. This methodology is approved by the Board of

Directors of MetLife CY.

The following table outlines the reversionary bonus rates declared since 2002. As shown the declared

bonus rate reduced materially in past 10 years. Terminal Bonus rate was set at a flat rate of 15% for

2012, and 7.5% for 2013 and 2014.

Table 4.2 MetLife CY Reversionary Bonus Declared

YEAR 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

BONUS RATE

4.00% 3.50% 3.25% 3.00% 2.75% 2.50% 2.50% 2.50% 2.50% 2.00% 2.00% 0.00% 0.00%

MetLife CY has a range of reinsurance treaties in place, with a number of both intra-group and third

part counterparties. The key reinsurance treaties currently in place are summarized as follows:

Conventional risk transfer treaties for the in-force life portfolio – individual surplus;

Conventional risk transfer treaties for the in-force Permanent Total Disability portfolio

– quota - share;

Conventional risk transfer treaties for the in-force Dread Disease Riders and Group

Life business – quota- share;

4.3 Investment & Capital Management

MetLife CY’s assets are grouped into general account and separate account portfolios. The general

account portfolios include technical reserves, outstanding insurance claims and free assets and the

separate account portfolio includes the assets backing the unit-linked products. Each portfolio has its

own investment objective in line with the documented investment policy of MetLife CY constructed

and signed-off by the investment committee which includes the country manager. The investments

backing the liabilities consist of a mixture of investments such as Cyprus and other EU government

bonds, corporate bonds, mutual funds, Cyprus listed shares, property and short term deposits. The

investment portfolio includes no derivatives. Investment guidelines are in full compliance with

investment orders specified by the regulator. There are currently no ring-fenced funds in the

investment portfolio in relation to the with-profit business. The company’s management has

sponsored a project in relation to the general management of the participating policies in order to

enhance transparency and administrative ease of these contracts.

MetLife CY has been well capitalized in the recent years. The table below shows a comparison of the

company’s capitalisation ratio as at 31 December 2013 and the capitalisation ratio as at 31 December

2014.

Table 4.3 MetLife CY Capitalisation Ratio (Solvency I basis)

Q4 2013 Q4 2014

Total Assets 330.1 358.6

Total Liabilities 244.6 307.7

Excess capital 85.4 49.0

Required minimum solvency margin (RMSM) 13.9 16.1

Excess of Capital over and above RMSM 71.6 34.8

Capitalisation ratio (excess capital/RMSM) 616% 317%

MetLife Portfolio Transfer IA | Page 14

In terms of capital management, the MetLife CY’s strategy consists of targeting a higher level of

capital compared to the required solvency capital (200% of the regulatory solvency capital). Given the

change in regulatory condition across Europe and the adoption of Solvency II both assets and

liabilities will be based on a more realistic basis and the target solvency ratio will be defined at a pan-

European level for all subsidiaries throughout all European jurisdictions. The target level of solvency

under Solvency II basis is set to 125%. This figure would have probably been the same for the stand

alone MetLife CY Company following Solvency II implementation if the proposed transfer was not in

executed.

4.4 Administration & Governance

Similarly to MEL, MetLife CY administers business internally with some reliance on group internal

outsourcers for the key functions within the operation. This is likely to remain largely the same

following the implementation of the proposed transfer unless efficiencies will be identified that will

require diversion from the existing model. In such cases it is expected that the company will benefit

from economies of scale and ultimately this will be reflected on customer support hence it is not

expected to compromising existing client servicing and support.

MetLife CY operates a management framework which is designed to effectively assist decision

making in order to control and assess the risks and opportunities within the business. This ensures

that risk management is integrated within all the business processes. MetLife has a number of

Executive Committees, which meet on a regular basis to ensure compliance with the management

framework. The following table lists the committees including the Board of Directors that are currently

in place with their key roles:

MetLife Portfolio Transfer IA | Page 15

Table 4.3 MetLife CY Committees

COMMITTEES FOR SII

COMPLIANCE FUNCTIONALITY / ROLE

CORPORATE GOVERNANCE

Board of Directors

Oversight of the business on behalf of the shareholders. Adopts key business decisions.

Appoints executive directors, adopts business activities changes, structural/organizational changes, divided distributions capital increases etc.

Approves key transactions.

Presents the financial reports to the shareholder.

Investment Committee

Strategic direction and regular monitoring of asset allocation

Authorize or approve specific investments

Optimize investment returns within the limits of the Board approved risk appetite

Set the company’s annual investment plan

Finance and Risk Committee

Establish, approve and communicate risk appetite and tolerance

Review MetLife’s risk exposures

Review and discuss the results from risk management assessments

Audit Committee

Oversees the accuracy, completeness and timeliness of accounting and other documents and reports

The adequacy of the Company’s internal controls

Management systems and the methods for risk assessment

Management Committee

Oversee the Company’s operational and compliance risk management

Roll out enterprise risk self-assessment (ERSA)

Identify manage emerging risk, legislative and regulatory initiatives, sales practice and ethics and compliance programs.

Set policies and parameters related to underwriting, product, insurance and reinsurance risks.

It should be noted that there are certain proposed changes in relation to the risk committees in order

to meet the risk, audit and compliance reporting requirements of MEL’s Executive Risk Committee.

Following the proposed transfer, the local committees and management framework will integrate into

MEL’s risk management framework. The local Risk Officer and other key function holders will undergo

specific training to ensure compliance with MEL’s risk governance and reporting standards.

MetLife Portfolio Transfer IA | Page 16

5 Outline of the Transfer

5.1 Background

The proposed portfolio transfer of MetLife CY forms a step in a wider reorganisation of the MetLife

Group’s businesses in Europe in preparation for Solvency II, which comes into effect in 2016, arising

from which ultimately, MEL will be the principal MetLife Company in Europe authorized to carry on life

assurance business and class 1 and 2 non-life business. Also arising from this project, MEIL will be

the principal MetLife Company in Europe authorised to carry on non-life insurance business apart

from Class 1 and class 2.

MetLife has undergone a global restructuring project and as part of this global restructuring project,

the insurance portfolio, assets, liabilities and business relationships have been transferred into MEL

over the last few years. The intended group restructure of MetLife CY will be to transfer its insurance

portfolio, assets, liabilities and business relationships to a Cypriot branch of MEL. Only assets equal

to Total Liabilities will be transferred to MEL from MetLife CY.

5.2 Policies Transferred & Associated Liabilities

All the insurance liabilities of MetLife CY, including any outstanding liabilities relating to risks that have

already crystalised such as pending claims, will transfer to the Cypriot branch of MEL via a court

approved legal process. MEL will need to issue 1 share of nominal value of €1 each at a premium, to

MetLife Cyprus Hold Co as consideration for the transfer. The premium will be based on the fair value

of the receiving business immediately following the transfer determined by a methodology that will be

agreed between MEL and MetLife CY. The following table summarises the characteristics of the

transferring policies.

Table 5.1 MetLife CY in-force portfolio

PRODUCT TYPE CYP SI GROSS

RESERVES

NO. OF CONTRACTS*

PREMIUM SIZE (€)

With-profit - Business with reversionary (regular) and terminal bonuses 119.1 4983 3.2

With-profit - Deferred annuities with Excess Interest Benefit and terminal bonus 70.8 2521 2.3

With-profit - Business with Excess Interest Benefit Only 36.7 5484 6.4

Non-profit business 10.0 6224 2.5

Riders 1.7 0 0.9

Unit linked 26.8 4084 5.6

Individual personal accident 3.1 44233 5.8

Group life 2.6 277 1.7

Group Medical 1.8 278 6.8

Group Annuities 8.6 9 0.6

Group Personal accident 1.0 1568 1.2

5.3 Assets Transferred

The portfolio transfer assumes to transfer only insurance assets and liabilities of MetLife CY. Under

the Business Transfer Agreement (BTA) sufficient assets to cover transferring Total Liabilities will be

transferred to MEL. Only assets equal to the Total Liabilities will be transferred to MEL. Following the

transfer MetLife CY is expected to pay a dividend in 2016. This dividend does not affect the

transfer as it will be based on the residual assets of the company following the transfer to

MEL. The dividend will be payable to MetLife EU Holding Company Limited (Ireland) (“MEUHC”). The

dividend payment is not yet finalised.

MetLife Portfolio Transfer IA | Page 17

5.4 Transfer Costs

The costs in relation to the transfer will not be directly or indirectly transferred to policyholders of MEL

or MetLife CY. The costs will be borne entirely by the shareholders of both companies.

5.5 Tax Impact of Transfer

I have received confirmation form MEL’s tax department that the business transferred from MetLife

CY to the MEL Cypriot branch will continue to be subject to Cypriot tax as is currently applicable to

MetLife Cyprus. The expectation is that emerging profit will not change from being subject to Cyprus

tax and that no additional Irish tax will be applicable.

In relation to policyholder tax exemption on premiums payable, it is not expected that the treatment of

policyholder premium will be subject to change from Cypriot tax authorities.

MetLife Portfolio Transfer IA | Page 18

6 Financial Impact

6.1 Solvency II Comparisons

The proposed transfer will be carried-out based on Solvency II compliant calculations. Following the

proposed transfer date (01 January 2016), Solvency II will be in full implementation throughout

Europe hence all financial impacts have been considered under Solvency II. The following tables

summarise the projected Solvency position of MEL pre and post transfer as at proposed transaction

date and based on the latest YE2013 ORSA report that has been submitted to the local regulator:

Table 6.1 MEL Solvency II Balance Sheet

MEL BALANCE SHEET (€M) MEL* MEL* + CZK, +

HUN

MEL* + ON-

SHORING

WITHOUT

EVOLUTION(1)

MEL* + ON-

SHORING, +CZK

+ HUN +CYP, +

ROM

31-Dec-14 31-Dec-15 31-Dec-16 31-Dec-16

Assets

Non Linked 2,415.3 3,360.7 3,096.0 3,840.8

Linked 6,270.3 7,541.2 7,721.2 8,374.2

Reinsurance Asset & Other 309.8 197.0 69.0 105.8

Total Assets 8,995.5 11,099.0 10,886.2 12,320.8

Liabilities

Technical Provisions 7,008.0 8,793.7 8,209.8 9,472.3

Corporate Reserves 373.6 387.4 387.4 387.4

Deferred Tax Liabilities 154.2 195.4 312.1 312.1

Other (OH Expense Allowance) 83.3 84.0 85.6 85.6

Total Liabilities 7,619.0 9,460.6 8,994.9 10,257.4

Own Funds (Available Net Assets)

Opening Own Funds 1,151.7 1,376.4 1,601.2 1,638.5

Project Evolution Transfer in 0.0 365.2 0.0 126.0

Net Income in period (after tax) 224.7 -103.2 290.1 298.9

Capital injections / (Dividends) 0.0 0.0 0.0 0.0

Closing Own Funds 1,376.4 1,638.5 1,891.3 2,063.4

Solvency

SCR 539.8 688.0 984.1 1,121.2

Solvency ratio 255% 238% 192% 184%

Excess / (shortfall) over SCR 836.7 950.5 907.2 942.2

(1) Evolution refers to the project of restructuring MetLife’s businesses in the EU; On-shoring refers to the option of

replacing the current reinsurance arrangement with MetLife Reinsurance of Bermuda through an appropriate

derivatives programme executed by MEL

(2) MEL* above includes the transfer of MetLife Bulgaria which occurred on 31 December 2014 and MetLife

Slovakia, which at time of the ORSA production was also expected to transfer on the 31 December 2014. The

actual transfer of MetLife Slovakia occurred on 1 April 2015

The above table is based on the YE2013 ORSA report hence the figures appearing are projected

based on data and assumptions as at YE2013 and assuming all planned transfers to MEL are

successfully implemented, including the transfer of MetLife CY to MEL. For this reason the figures for

2014 cannot be matched with the respective figures in table 2.1. It should be noted that the Transfer

in relation to Bulgaria, Slovakia and the Czech Republic have already been executed and that even if

the transfers for Hungary and Romania are not executed for any reason, the capitalisation of MEL will

still be higher than the target limit following the potential transfer of MetLife CY. Proceeding with the

on-shoring option referred to above basically changes the MetLife entity where the hedge is held. The

better hedged MEL is the less capital it will need to hold. There is operational risk around any hedging

programme which MEL is well aware of and which in the first instance will be mitigated by strong

controls.

MetLife Portfolio Transfer IA | Page 19

Table 6.2 MetLife CY Projected Solvency II Coverage Ratio

€M 2014 2015 2016

Own Funds 113.2 125.3 143.2

SCR 32.3 32.0 32.1

Coverage Ratio 350% 392% 446%

Similarly to the MEL table, the above figures are based on projections as at YE2013 and therefore the

2014 figures cannot be matched with the respective figures in table 2.1. The projected Solvency II

coverage ratio for MetLife CY starts at 350% and escalates to 446% which is materially higher than

the projected coverage at MEL level. It should however be noted that although the projected figures

take into account new business and the run-off of the capital intensive with-profit business, it does not

factor in the dividend that MetLife CY is expected to pay to the MetLife Holding Company post the

MEL transfer. Additionally management have confirmed that if MetLife CY were to remain a

standalone entity and not form part of MEL, the Solvency position would not have been as in the

financial projections presented in the above table. Dividends would be paid out to reduce the

coverage to a target most likely similar to MEL's. It is worth noting that even though, post transfer, the

coverage ratio is at a lower level as part of MEL (184%), the absolute amount of excess own funds

over SCR is much greater in MEL. Additionally, MEL is a much bigger and more secure entity than the

stand alone MetLife CY Company, due to the large diversification of risks it enjoys. This would act in

favour to policyholder security.

6.2 Valuation Basis

In forming my opinion in relation to the proposed transfer I have mainly taken into account figures

derived under Solvency II basis as this will be the new regulatory basis in both jurisdictions at and

following the transfer date. MEL and MetLife CY management has also provided figures under both

Cypriot and Irish Solvency I basis, which I have took into account but not relied on them.

Table 6.3 Solvency Impact of MetLife Cyprus to MEL

Estimated Solvency Impact - MetLife Cyprus Cypriot Solvency I

Cypriot Solvency I

transferring to MEL

Cypriot Solvency I Remaining

Solvency II transferring

to MEL

all amounts in €m 31-Dec-14 31-Dec-14

Total assets 358.6 266.7 91.9 266.7

Total liabilities 307.7 307.7 0.0 266.7

Closing available assets 50.9 -41.0 91.9 0.0

Solvency capital requirement (RMSM / SCR) 16.1 16.1 n/a 43.6

Solvency ratio 317% -255% n/a 0%

Minimum solvency margin (100%/150%/100%)

16.1 16.1 n/a 43.6

Target solvency margin (200%/165%/125%) 18.5 18.5 n/a 54.4

Excess / (shortfall) over minimum 34.8 -57.1 n/a -43.6

Excess / (shortfall) over target 32.4 -59.5 n/a -54.4

The above table shows the shortfall of the transferring business of MetLife CY to MEL under Cypriot

and Solvency II. The shortfall mainly arises due to the fact that only assets equal to the Solvency II

liabilities are being transferred to MEL. Under Irish Solvency I the shortfall is material (€186.6m) due

to the more prudent regulatory requirements and this would have caused issues for MEL as existing

capital resources of MEL would be severely depleted, however I do not consider this an issue as

management confirmed that the transfer is not going to happen prior to Solvency II implementation.

The transfer is expected to happen on 1 January 2016 when Solvency II will be the only regulatory

requirement for MEL hence the only relevant shortfall is the one under Solvency II which stands at

MetLife Portfolio Transfer IA | Page 20

€54.4 million which can be comfortably covered by the available capital resources of MEL under

Solvency II basis without affecting MEL’s target Solvency II coverage ratio of 125%.

6.3 Conclusion

The proposed transfer of Total Liabilities of MetLife CY to MEL will be based on a Solvency II

compliant basis. Assuming that the conditions as listed in the Section 2.3 are fully met I do not expect

that the financial impact on MEL from the proposed transfer will be material. Even though the

coverage ratio following the proposed transfer will be at a lower level compared to the pre transfer

figure for MetLife CY, the absolute amount of excess own funds will be much higher.

MetLife Portfolio Transfer IA | Page 21

7 Risk Profile Changes

7.1 New Risks to MEL

MetLife CY is relatively small compared to the overall risk exposure of MEL. As at YE2014 the SCR

stated in respect of MEL is EUR493.6m while the corresponding figure for MetLife CY stands at

EUR43.6m, i.e. around 7% of the total MEL SCR as shown in table 7.1 below. Given the small size of

the Cyprus market compared to the combined MEL markets, the impact is expected to remain low

in the foreseeable future. There are however a number of areas which could potentially add

additional risk and should be considered and addressed at the MEL level in the short to medium term:

Negative GDP growth in 2014 combined with high unemployment rates could

materially affect projected new business levels, surrenders and lapses

If at any point with-profit fund segregation is considered, it could increase operation

costs and risks

Impact of bail-out and austerity measures will impact surrenders, lapses and new

business levels

Additional credit risk due to investments in Cyprus Government Bonds

Political risks due to the long-term situation with Turkey as well as the Troika

conditions and local market exposure to Greece

Lowering of interest rates in Cyprus and the Eurozone

7.2 Risk Profile Comparisons

For the purpose of this report we have considered that SCR and its components accurately reflect the

risk profile of the MEL and MetLife CY. The basis of these comparisons is taken out of the ORSA

report prepared by MEL for YE2013 which also includes the MetLife CY stand-alone solvency capital

requirements.

The following table summarises the SCR contributors of MEL and MetLife CY as at YE2014:

Table 7.1 SCR components (Amounts)

All figures are in €m MEL excl.

Cyprus MetLife Cyprus

MEL incl.

Cyprus

Market risk 256.8 30.7 276.4

Counterparty default risk 46.4 8.0 54.4

Life underwriting risk 279.1 14.9 289.5

Health underwriting risk 19.3 4.5 22.2

Non-Life underwriting risk - - -

Diversification Benefits - 154.1 - 15.9 - 167.2

Basic Solvency Capital Requirements 447.6 42.2 475.3

Operational risk 46.1 1.4 47.5

Loss absorbing capacity of deferred taxes (LACDT) - - -

Solvency Capital Requirements 493.6 43.6 522.8

MetLife Portfolio Transfer IA | Page 22

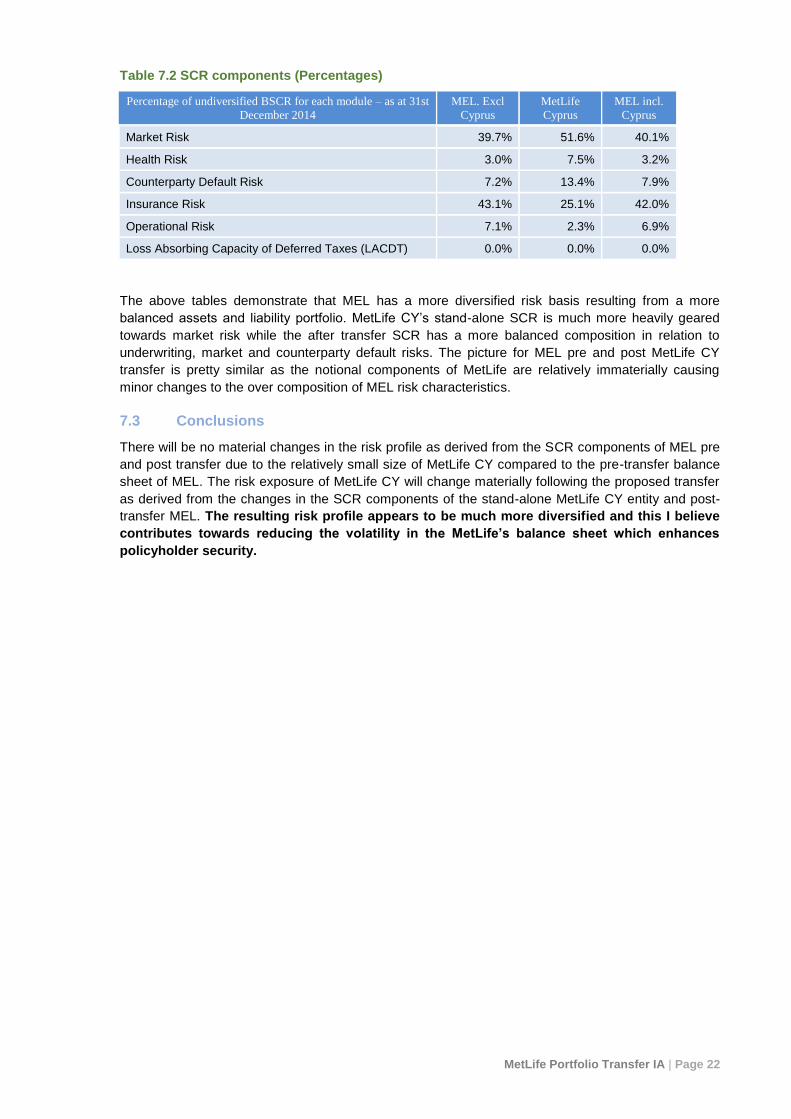

Table 7.2 SCR components (Percentages)

Percentage of undiversified BSCR for each module – as at 31st

December 2014

MEL. Excl

Cyprus

MetLife

Cyprus

MEL incl.

Cyprus

Market Risk 39.7% 51.6% 40.1%

Health Risk 3.0% 7.5% 3.2%

Counterparty Default Risk 7.2% 13.4% 7.9%

Insurance Risk 43.1% 25.1% 42.0%

Operational Risk 7.1% 2.3% 6.9%

Loss Absorbing Capacity of Deferred Taxes (LACDT) 0.0% 0.0% 0.0%

The above tables demonstrate that MEL has a more diversified risk basis resulting from a more

balanced assets and liability portfolio. MetLife CY’s stand-alone SCR is much more heavily geared

towards market risk while the after transfer SCR has a more balanced composition in relation to

underwriting, market and counterparty default risks. The picture for MEL pre and post MetLife CY

transfer is pretty similar as the notional components of MetLife are relatively immaterially causing

minor changes to the over composition of MEL risk characteristics.

7.3 Conclusions

There will be no material changes in the risk profile as derived from the SCR components of MEL pre

and post transfer due to the relatively small size of MetLife CY compared to the pre-transfer balance

sheet of MEL. The risk exposure of MetLife CY will change materially following the proposed transfer

as derived from the changes in the SCR components of the stand-alone MetLife CY entity and post-

transfer MEL. The resulting risk profile appears to be much more diversified and this I believe

contributes towards reducing the volatility in the MetLife’s balance sheet which enhances

policyholder security.

MetLife Portfolio Transfer IA | Page 23

8 Impact Assessment on Policyholders

8.1 Policyholders Affected

In my assessment of the impact of the proposed transfer of the MetLife CY portfolio to MEL I have

considered all the policyholders of the in-force portfolio of MetLife CY. This includes non-profit and

with-profit policyholders. The relative size in terms of in-force portfolio and related risks of the MetLife

CY portfolio compared to the existing and prospective business of MEL is not substantial hence any

impact on MEL existing and prospective policyholders is unlikely to be material.

Prospective benefits (future and outstanding) are clearly defined for both unit-linked and conventional

non-profit policyholders hence both pending and future benefits, for this group of policyholders are

unlikely to be affected from the proposed transfer. In relation to with-profit policyholders and given the

discretionary element in some future benefits, there could potentially be a higher probability of some

impact on future discretionary benefits for this group of policyholders. I have received confirmation

from management though that the legal terms of the scheme do not differentiate between with-profit

and other MetLife CY’s policyholders.

In my investigations to understand the potential impact I had various discussions and received

numerous documents around the mechanics and the process of bonus declarations. The

management of MEL sponsored a project the scope of which is to investigate the management of the

participating policies and propose a more transparent, with less discretion methodology for the bonus

declaration going forward. The first phase of the project is complete, under which a proposed formula

driven methodology has been adopted by the management. Phase two of the project is now under

way with the main scope to define and parameterise the formula to ensure that policyholders continue

to be equitably treated, policyholder reasonable expectations are met and no policyholders are

materially disadvantaged compared to the existing bonus methodology. It should however be noted

that the full process to be followed and in particular the assets to be under consideration for future

declarations is key in forming an opinion as to the fair treatment of the participating policyholders,

which will be formalised following the completion of phase two. Management has indicated that there

is no plan to communicate the change in bonus methodology to policyholders.

Management has indicated that there will be no change in the terms and conditions of all existing

policies following the transfer hence all contractual rights of existing policyholders will remain

unchanged. I have reviewed the terms of the draft legal transfer document and I consider that the

interests of the policyholder are appropriately protected. In particular in relation to with-profit

policyholders, any reasonable expectations of this group of policyholders are not expected to be

affected following the transfer as a result of the transfer itself. The results of phase two of the

participating business project and subsequent implementation of the recommendations/improvements

suggested will enhance clarity, security and fairness of future bonus declarations. This is not a direct

consequence of the transfer but a result of a work stream that was going to be implemented

irrespective of the proposed transfer. The transfer itself however could have potentially magnified any

issues that could have resulted from the lack of ring-fencing of the with-profit reference assets. This is

expected to be rectified following the completion of phase two of the participating business project.

Under Solvency II requirements the Company is not obliged to formally ring-fence the reference

assets of the with-profit policies with the MetLife CY’s characteristics as benefits under these

contracts are not defined in the same manner as the UK with-profit funds and the element of the with-

profit fund Estate does not exist. There will continue to be a regular internal hypothecation of assets to

the with-profits business in order to determine the corresponding investment returns, and hence

facilitate the relevant bonus declarations.

8.2 Security of Benefits

A key consideration in determining the appropriateness of any such transfer is whether the security of

any group of policyholder benefits is affected following approval of the proposed transfer. Policyholder

security could be adversely affected by the transfer if benefits post transfer become less secure as a

direct consequence of the transfer itself. However I have not carried out a quantitative assessment of

whether the security is affected based on any one specific quantifiable measure as it is not possible to

MetLife Portfolio Transfer IA | Page 24

quantify all the aspects of policyholder security. Instead I have applied reasoned judgment based on

the interplay of factors involved to consider whether policyholders should be any more concerned for

the security of their benefits after the transfer. The main factors taken into consideration were:

Best-estimate liabilities and respective assets to be transferred and any changes in

the methodology and assumptions used for their valuation under MetLife CY

compared to MEL

The target solvency coverage under Solvency II and any potential difference between

MetLife CY and MEL

The Total Liabilities and respective assets as at Q4 2015 will be transferred from MetLife CY to MEL

at the proposed transfer date. These figures will not be available until after December 2015 hence any

conclusions have been drawn on the Total Liabilities information of the latest ORSA report which is

Q4 2013. The transfer will initially be based on the Q3 2015 Total Liability figure; however a final run

will be done based on Q4 2015 data to determine the value of assets to be transferred over to MEL.

MetLife CY have shared their detailed Solvency II model validation approach with me and I feel that

this will provide a comprehensive and appropriate validation of the valuation of Total Liabilities and

respective assets using methodology and assumptions in line with the appropriate regulation and

guidelines.

Table 8.1 Solvency II Transfer Impact to MEL (Based on YE2014 Figures)

YEAR 2014

ALL FIGURES ARE IN €M

MEL EXCL. CYPRUS

METLIFE CYPRUS

METLIFE CYPRUS TO

MEL

MEL INCL. CYPRUS

Investments (excluding unit-linked) 2,025.9 326.3 205.4 2,231.3

Investments (unit-linked, including variable annuities) 6,635.6 26.0 26.0 6,661.7

Other non-invested assets 447.7 31.7 31.7 479.4

Deferred Tax Assets 5.1 0.0 0.0 5.1

Reinsurance Assets 254.9 3.6 3.6 258.6

Total Assets 9,369.3 387.6 266.7 9,636.0

BEL 7,438.7 250.4 250.4 7,689.1

Risk Margin 138.5 11.2 11.2 149.7

Technical Provisions 7,577.3 261.6 261.6 7,838.8

Other Liabilities 485.2 5.1 5.1 490.3

Subordinated Debt Liabilities 0.0 0.0 0.0 0.0

Deferred Tax Liabilities 112.0 0.0 0.0 112.0

Total Liabilities 8,174.5 266.7 266.7 8,441.2

Available Assets 1,194.9 120.9 0.0 1,194.9

Recognition of Subordinated Debt as Eligible Assets 0.0 0.0 0.0 0.0

Net Deferred Tax Asset Limitation 0.0 0.0 0.0 0.0

Eligible Assets 1,194.9 120.9 0.0 1,194.9

Solvency Capital Requirement

Regulatory Minimum 493.6 43.6 43.6 522.9

Risk Appetite Target 617.0 54.4 54.4 653.7

Solvency Ratio 242.1% 277.6% 0.0% 228.5%

MetLife Portfolio Transfer IA | Page 25

Only assets equal to Total Liabilities will be transferred to MEL in relation to MetLife CY business

hence the SCR calculation at MetLife level is not relevant to the transfer. The solvency level of MEL

after transfer will be covered from existing resources at MEL level without support from the existing

Own Funds of MetLife CY. The target Solvency Ratio of MEL is 125% which would have most likely

been the target ratio of MetLife CY assuming the proposed transfer was not put forward. I understand

that the projected solvency coverage ratio for MetLife CY in 2016 would have been materially higher

than the corresponding coverage ratio of MEL following the proposed transfer as shown Table 6.2.

However, the projected solvency coverage ratio for MetLife CY is more theoretical as it ignores the

intended transfer through a dividend form to the parent company which will materially reduce the

projected solvency coverage ratio of MetLife CY to levels closer to the target solvency coverage ratio

defined at group level (125% of SCR). In addition to that, the amount of free capital on top of the

regulatory requirement at MEL level is materially higher and the risks are more diversified at multiple

levels which potentially reduces insolvency risk, warranting higher policyholder benefit security. I

therefore believe that MetLife CY existing policyholders are not materially disadvantaged from

the lower projected Solvency II coverage ratio at MEL following the proposed transfer.

8.3 Policyholder Reasonable Expectations

Policyholders tend to form expectations of benefits that will be received in the future. Part of these

expectations relate to the actual receipt of benefits upon claim and part relate to the actual amounts to

be received, especially for policies where the insurance provider’s discretion is involved e.g. in with-

profit policies. Policyholder expectations can be formed from the very outset of a policy based on the

initial policyholder documentation and communication. However, significant expectations can be

formed during the life time of with-profit policy based on the company practice of regular bonus

declarations and/or interest rate additions.

For non-profit policies where the benefit is normally largely fixed from the outset of the policy, the

policyholder expectations relate to a known benefit. For with-profit policies however the final benefit is

not fixed from the outset of the policy, and the with-profit policyholders form bonus expectations for

the future which are based on the past company practice of declaring bonuses.

Management indicated that the methodology and procedure of the bonus declarations and the

general management of the participating policies will not be altered as a direct result of the

transfer (i.e. the participating business review currently underway would have been required even in

the absence of the transfer). Future bonus rates will be declared based on similar principles as

prior to the transfer. The formulaic approach to be introduced will be parameterised in such a way

so that no group of participating policyholders will be materially disadvantaged hence reasonable

expectations are not expected to change as a result of the transfer.

For linked policies the main expectations of the future benefits are based on the underlying fund

management and fees this incurs, the investment policies, the unit pricing methodology and the

management fees charged by MetLife CY. My understanding from discussions with the management

is that none of these factors will change as a result of the proposed transfer.

MetLife CY’s portfolio will be part of a much larger operation with significantly higher significance to

the Group compared to the stand alone Cyprus operation. This development will increase capital

fungibility if required and will receive higher attention and reputational considerations for the

ultimate parent company and indirectly enhance the level of security enjoyed by MetLife CY’s

policyholders under the status quo scenario.

8.4 Operational Considerations

MEL and MetLife CY have various service agreements in place in order to administer and service

clients on a regular basis. Management has confirmed that the current agreements will not be

changed in any way to adversely affect customer satisfaction. In fact, enhanced efficiencies of

the resulting post-transfer operation could potentially enhance customer satisfaction. There may be

some minor changes to claims thresholds, reporting lines and some additional reports, but otherwise

MetLife Portfolio Transfer IA | Page 26

processes and procedures for claims handling and customer services are expected to remain to a

large extent as they currently are at MetLife CY level. This is in line with experience from previous

transfers across Europe into MEL.

8.5 Treating Customers Fairly

The treatment of policyholders will not be impacted in any way from the implementation of the

proposed transfer and I am satisfied following discussions with the management at both ends the

current fair treatment of policyholders will continue following the completion of the transfer.

8.6 Tax Implications

I have relied completely on tax specialist of MEL and MetLife CY to understand the implications of the

transfer on tax on policyholder benefits. My understanding is that there will be no impact on the rates

or structure in taxation of any future benefits received in relation to current in-force policies resulting

from the transfer.

8.7 Conclusions

Considering the impact of the proposed transfer on policyholders of MetLife CY and MEL, it is my

opinion that:

There will be no material adverse impact on the security of MetLife CY’s policyholders

transferring to MEL

There will be no material impact on in-force policyholders of MEL as these are listed

in various parts of this report

The policyholder reasonable expectations, contractual obligations and tax treatment

of transferring policyholders will not be affected as a result of the transfer

The proposed formulaic approach for setting bonus rates can be structured in a way

not to materially disadvantage any of the participating policyholders of MetLife CY

Service quality of MetLife CY’s policyholders will not be adversely affected as a result

of the proposed transfer

MetLife Portfolio Transfer IA | Page 27

9 Policyholder Communication Management have informed me that approval will be sought from the Regulator so that they will not

be required to inform existing MEL policyholders of the proposed transfer of MetLife CY. Given the

relative size of MetLife CY and that the poet transfer situation will not affect the risk profile and

capitalisation level of MEL I have no objection to this.

At the time of writing the report, the letters to be sent to existing MetLife CY’s policyholders were still

not finalised. I have reviewed the draft English version of the letters describing the proposal for the

transfer. Management has indicated that the content and structure will not change materially and I

have no issues with that.

Appendices

Appendix A | Page i

Appendix A: Marios Schizas CV

9.1 Background

Marios joined Lux in 2010 as the leader of the life insurance sector covering insurance and reinsurance

clients in Cyprus, Malta, UK and the Middle East. Previously to joining Lux, Marios worked in the UK for

Tillinghast Towers-Perrin, Ernst & Young and Bank of America. He has experience in mergers &

acquisitions mainly in the UK and is registered as an Appointed Actuary to a number of jurisdictions

including Cyprus. Marios is a Fellow of the Institute of Actuaries UK, having qualified in 2004 and he is also

a Fellow of the Cyprus Association of Actuaries. He also holds a BSc in actuarial Science from the London

School of Economics.

9.2 Experience

Marios is an experienced life actuary with exposure in a lot of European and Middle East markets. He

participated in M&A transactions in the UK and Europe and is the Appointed Actuary of a number of life

insurers and reinsurers. The following summarise the main experience items:

Appointed Actuary Roles in a number of jurisdictions

Actuarial reserve review responsibility for a number of insurance and Takaful companies

Modelling and Financial reporting work for local and international insurance and

reinsurance companies

Embedded Value reporting responsibility for listed and unlisted insurance companies

Solvency II assistance in all three pillars for EU registered insurance companies

Involved in the modelling of a number of M&A transactions and inherited estate projects in

the UK market

Product design and profit testing of investment and protection products

Appendix B | Page ii

Appendix B: Sources of Data

9.3 Sources of Data

The following list summarises the main information used in the analysis and conclusions presented

throughout this report. Reliance has also been placed on other documents, correspondence and

discussions between Lux, MetLife CY and MEL management.

NUMBER FILENAME DESCRIPTION

1 MetLife France Transfer - MEL Actuarial & Risk Transaction Report v2.2

Actuarial risk and transaction report for MetLife France

2 Project LESS - Bulgaria ARTR - Final v1.4 Actuarial risk and transaction report for MetLife Bulgaria

3 Project LESS - Czech Republic ARTR - Final v1.0 Actuarial risk and transaction report for Czech Republic

4 Project LESS - Slovakia ARTR - Final v1.5 Actuarial risk and transaction report for Slovakia

5 MEL ORSA_31 12 13_Refresh v1 5 clean MEL ORSA report as at 01 January 2014

6 IE Report Independent Expert Report for ML

7 EA 7 - 1st page MetLife CY 2014 Form EA7

8 EA 7 - 2nd page MetLife CY 2014 Form EA7

9 Facultative Cover EAE7 2014 MetLife CY 2014 Form EA7

10 MEL Asset and Liability Management Strategy October 2014 MetLife CY ALM strategy document

11 ALICO Cyprus Branch Form AR6 2013 English v11 MetLife CY AR6 for YE2013

12 MetLife Europe Limited 2013 Appointed Actuary Board Report v1 1 FINAL

MEL Appointed Actuary Report for YE2013

13 Asset Segregation Response by MEL's AA Response from MEL Appointed Actuary on asset segregation

14 MetLife Europe Limited - AA External Report - ML MIL to MEL Part VII v2 0

MEL Appointed Actuary Part VII transfer report of ML and MIL into MEL

15 MetLife Alico (Cy Ltd) - Signed Financial Statements Period Ended 31.12.2013

MetLife CY Financial Statements for YE2013

16 MetLife Europe Limited signed Financial Statements 31.12.13.pdf MEL Financial Statements for YE2013

17 0204_RP_Client_Brochure_12 MetLife CY policy documentation

18 0217_RP_Key_Features_15 MetLife CY policy documentation

19 0224_RP_TC_8 MetLife CY policy documentation

20 MEL - Schedule 4 Report - 31 Dec 2013 FINAL MEL Abstract of the valuation report prepared by the Appointed Actuary for YE2013

21 Product List Summary_SC_1212214 MetLife CY product list

22 AR FORMS 2013 final MetLife CY AR6 forms as at YE2013

23 AR Supplementary Notes 2013 draft v3 actuarial (29052014) - no track of changes

MetLife CY AR6 forms supplementary notes as at YE2013

24 MEL CBI Returns Final Forms Q3 2014 MEL forms for Q32014 submitted

25 MetLife Europe Limited signed CBI return 31 12 13 MEL CBI returns submitted for YE2013

26 2012 Annual Statutory Returns Additional Replies to GAD_No 3 Q&A between Cypriot Regulator and MetLife CY on WP policyholders

27 2012 Annual Statutory Returns Additional Reply to GAD_No 2 Q&A between Cypriot Regulator and MetLife CY on WP policyholders

Appendix B | Page iii

28 2012 Annual Statutory Returns Replies to GAD_No 1 Q&A between Cypriot Regulator and MetLife CY on WP policyholders

29 2012 Returns - Additional Comments by ICCS Q&A between Cypriot Regulator and MetLife CY on WP policyholders

30 2013 Annual Statutory Returns Replies to GAD_No 1 Q&A between Cypriot Regulator and MetLife CY on WP policyholders

31 2013 Annual Statutory Returns Replies to GAD_No 2 Q&A between Cypriot Regulator and MetLife CY on WP policyholders

32 Current Bonus Declaration Process_V4 Description of current bonus declaration method

33 ICCS Comments on the 2013 Returns Q&A between Cypriot Regulator and MetLife CY on WP policyholders

34 SoI - Comments on 2012 Stat Returns Q&A between Cypriot Regulator and MetLife CY on WP policyholders

35 2015 MEL General Accounts ALM Guidelines MEL Investment Guidelines

36 Investment Guidelines Cyprus 2014 Final MetLife CY Investment Guidelines

37 - MetLife European Group Reorganisation Overview - 19 01 2015 MetLife European re-organisation structures

38 Cyprus Transaction Design v1.0 Transaction design charts for transferring MetLife CY into MEL

39 Product List Summary_v4 Updated Product list summary for MetLife CY

40 objections - replies Objections and response to WP fund policyholders in the previous transfer from branch to company

41 objections - replies.pdf 3 Objections and responses to WP fund policyholders in the previous transfer from branch to company

42 Project Less - Objections Objections and responses to WP fund policyholders in the previous transfer from branch to company

43 Committees Localisation Cyprus SII proposed committees for MetLife CY for efficient system of Governance

44 MetLife Cyprus -participating business transfer options - 17 3 2015