22

1 MABS Performance Monitoring Reports

1

MABS Performance Monitoring Reports

2

What Is The Monthly Product Performance Report?

Shows the performance of the bank’s microfinance product, particularly the size, quality, and profitability of its microfinance operations.

3

Importance of The Monthly Product Performance Report

Enables management to regularly monitor the performance of the microfinance product and the accomplishments of the microfinance unit.

4

Format of The Report

Consists of two parts: the product performance data and the statement of income and expenses.

Allows banks to either report only the direct or incremental expenses of their microfinance product, or include the indirect expenses.

Compares the performance of the product during the current month and the previous month.

5

Sources of Information

Product performance data are sourced from the MIS reports.

Data for the statement of income and expenses are sourced from the bank’s financial statements.

6

Who Prepares the Report?

The Microfinance Supervisor or the branch bookkeeper.

The report should be completed as soon as the branch monthly financial statements have been prepared.

Should be reviewed by the branch bookkeeper or accountant and by the branch manager before its submission to head office.

7

Who Gets the Report?

• The bank president or general manager

• RBAP-MABS

One copy each of the Portfolio At Risk report and the AO Performance Report should always be attached to the report.

8

Format of the Report

Product Performance Data

• Shows the size and quality of the bank’s microfinance

operation

Statement of Income and Expense

• Shows whether the bank is making money from its

microfinance operation

9

Performance Data Report

10

Financial Data

11

Source Documents for Performance Data

• Portfolio at Risk Report (PARR)

• MABS Monthly Report (MMR)

• Performance Report by Account Officer (PRAO)

• Total Interest Collected From MFU (TICMFU)

• Schedule of Deposit Liabilities by Size of Account (SDLSA)

12

Portfolio at Risk Report

� Primary report that indicates the quality of the

loan portfolio of the MFU

� An aging report that shows the overdue amount

and portfolio at risk

� Also shows the total number of outstanding

borrowers, the corresponding outstanding loan

balance and their percentages

� Estimates the PAR ratio

13

Portfolio at Risk Report

14

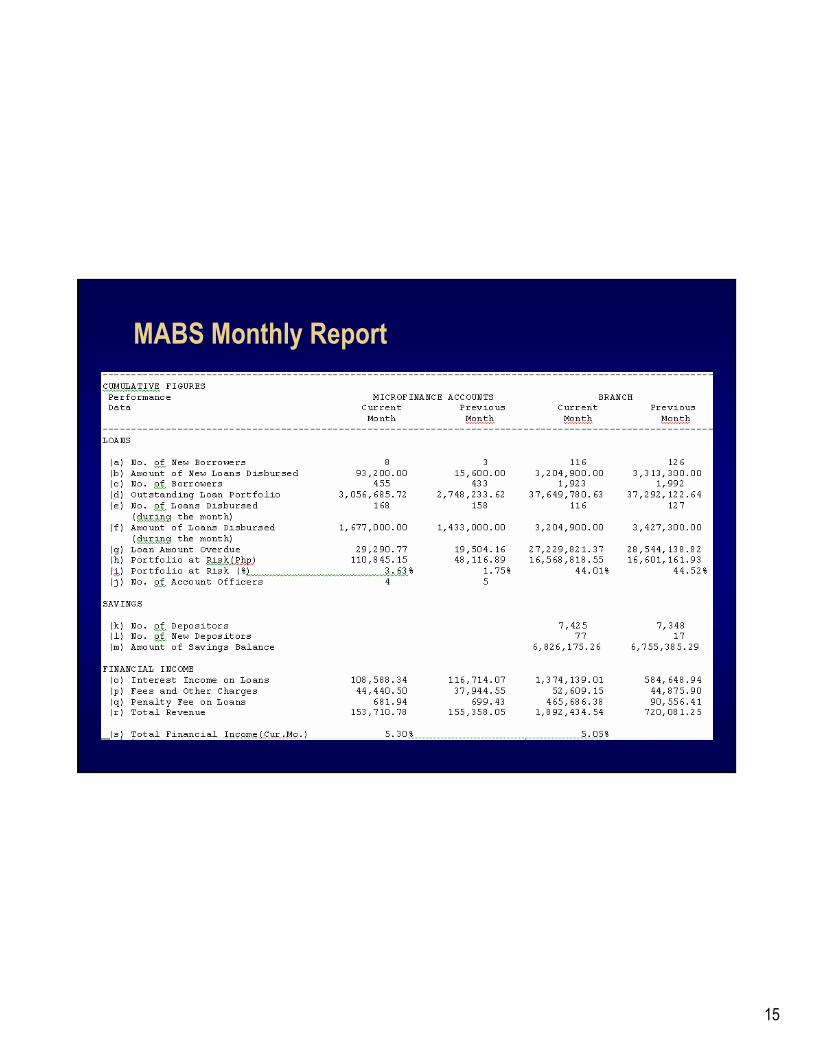

MABS Monthly Report

• Compares the results of current month’s operations

vs. those of previous months

• Compares the performance of the microfinance

product vs. other products of the branch

• Shows comparative figures (loans, deposits, and

financial income) between two succeeding periods

• Shows all loan accounts with outstanding balance

15

MABS Monthly Report

16

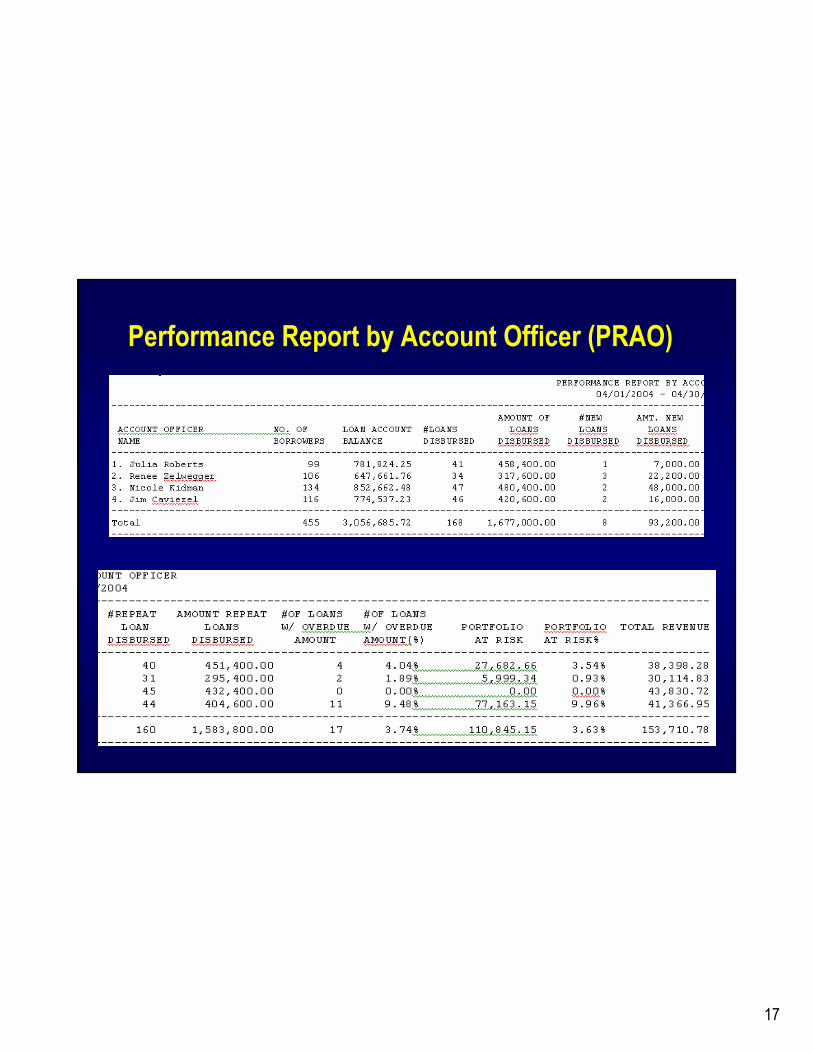

Performance Report by Account Officer (PRAO)

� Shows the performance of each AO and the microfinance unit of the branch as a whole

� Comes handy if the bank has an existing incentive scheme

� Summarized by (according to) account officer

� AO performance indicators include:

o # of loans, new and repeat

o amount disbursed and revenue generated

o overdue amount and portfolio at risk

17

Performance Report by Account Officer (PRAO)

18

Total Interest Collected from MFU

• Summary of interest and other charges collected

within the specified date range, grouped by account

officer

– Shows the income generated by each AO and the

microfinance unit of the branch as a whole

19

Total Interest Collected from MFU

20

Schedule of Deposit Liabilities by Size of Account

� Shows sizing of the deposit accounts e.g. regular savings, current account, time deposit, etc…

� This report is used to established baseline deposit data and also the source to determine the net change in deposit levels.

� This is a standard report submitted to PDIC (RB FORM 2A –Schedule 05)

21

Schedule of Deposit Liabilities by Size of Account

22

These materials were made possible through the support provided by the U.S. Agency for International Development/Philippines under the terms of the contract no. 492-C-00-98-0008-00. The opinions expressed herein are those of the author(s) and do not necessarily reflect the views of the U.S. Agency for International Development.