Please refer to the important disclosures and analyst certification on inside back cover of this document, or on our website www.macquarie.com.au/research/disclosures. ASIA Buying deeply out of favour stocks Property is a sector with a quirk: In developed markets, it tends to be a defensive sector that provides stable yield, as it is comprised mostly of stocks whose NAVs are commercial and retail buildings with long-term leases. In emerging markets however, property refers primarily to residential developers. Those which do commercial and retail usually GRQ¶W JHW WHQDQW FRPPLWPHQW XQWLO completion, a risk their peers in developed markets would never bear. That makes them riskier than the average, and indeed property is a ³KLJK EHWD´ sector in most emerging markets. The chart to the right shows the difference in returns of WZR ³KLJK EHWD´ HPHUJLQJ market property sectors: Chinese property stocks have come all the way back from their crisis lows. But Indian property stocks remain almost as depressed as they were then. Surely there is at least one gem in something so out-of-favour « Continued on page 2 Mark Matthews +65 6601 0841 [email protected]25 April 2011 Macquarie Capital Securities (Singapore) Pte. Limited Guanxi ,GHDV IURP DFURVV 0DFTXDULH DQG EH\RQG « Inside India: pgs. 2-3 . Given its sensitivity to oil, India has held up well, with the key stock market gauge up 1.4% ytd and back near its 2008 high. But property stocks there are a different story, down 17% ytd and 70% since the peak. Homes beyond the affordability of the middle class, lack of working capital and scandal all explain it. ,W¶V WKH SHUIHFW HQYLURQPHQW to search for deeply oversold survivors. Rose among thorns pgs. 4-6 . The city with the greatest demand for office space LQ ,QGLD LV QHLWKHU 0XPEDL QRU 'HOKL ,W¶V %DQJDORUH with over 8m sqft leased out last year, and 8-10m expected this year. Unlike the others where residential prices are at all-time highs, in Bangalore they are still 20% below peak, and a growing middle class wants to buy. A pure Bangalore play, Prestige Estates (PEPL IN, Rs140, TP Rs210) has 30% of its NAV in offices, 13% in retail, and the remainder in residential. The stock is at a 47% discount to NAV, with a free cash flow yield of 11% this year and 16% next. The debt to equity ratio is 0.3x, and yielding assets generate income which more than covers interest costs. Plus: Gold pgs. 7-10 . There is fresh interest in gold from endowment funds and income funds. Is this the last leg up or the start of another wave? Inflation and energy pgs.10-13 . Around the world there is evidence high commodities prices are pinching the consumer. Yet Macquarie oil economist Jan Stuart says with emerging market demand still strong (and a good chance of supply interruption in the Middle East), oil prices will stay high or go higher. Your scribe would remain long energy stocks in Asia. Upcoming events pg. 14 , Interesting articles pgs.15-19 . Hang Seng Composite Property & Construction Index vs. Bombay Stock Exchange Realty Index, relative performance past 3 years Source: Bloomberg, Macquarie Research, April 2011 This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

Transcript

Please refer to the important disclosures and analyst certification on inside back cover of this document, or on our website www.macquarie.com.au/research/disclosures.

ASIA

Buying deeply out of favour stocks

Property is a sector with a quirk:

In developed markets, it tends to be a defensive sector that provides stable yield, as it is comprised mostly of stocks whose NAVs are commercial and retail buildings with long-term leases.

In emerging markets however, property refers primarily to residential developers. Those which do commercial and retail usually completion, a risk their peers in developed markets would never bear. That makes them riskier than the average, and indeed property is a sector in most emerging markets.

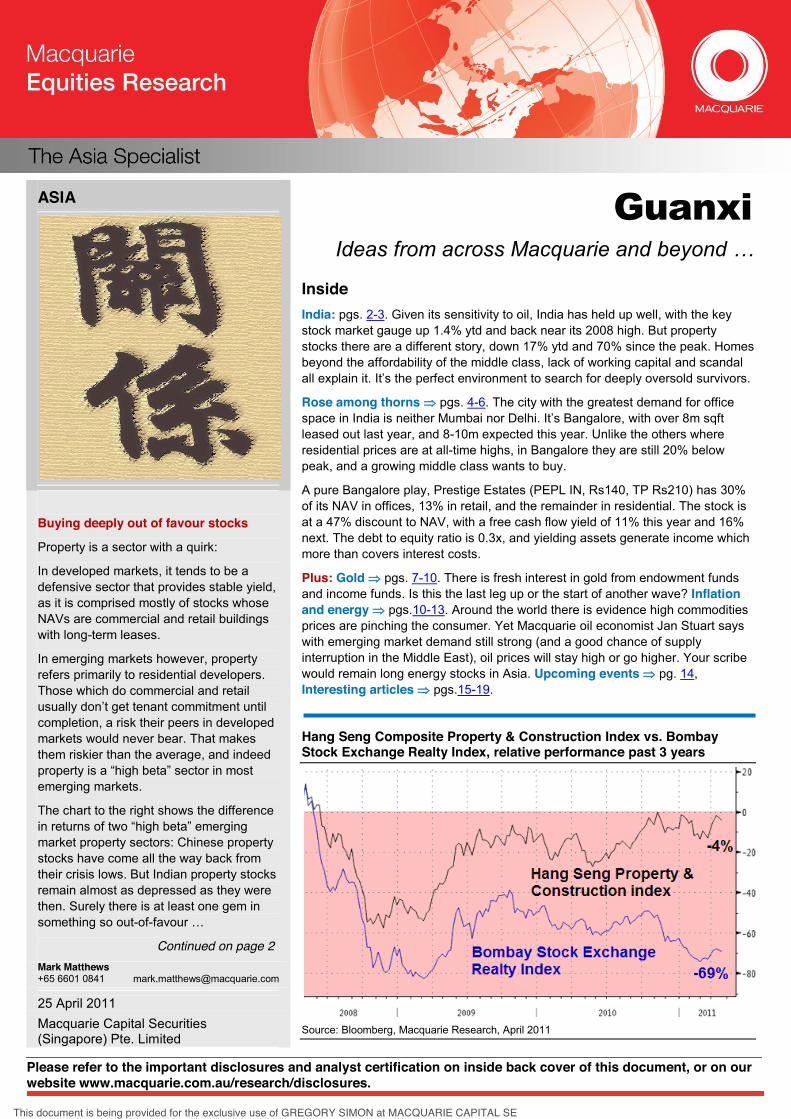

The chart to the right shows the difference in returns of market property sectors: Chinese property stocks have come all the way back from their crisis lows. But Indian property stocks remain almost as depressed as they were then. Surely there is at least one gem in something so out-of-favour

25 April 2011 Macquarie Capital Securities (Singapore) Pte. Limited

Guanxi

Inside India: pgs. 2-3. Given its sensitivity to oil, India has held up well, with the key stock market gauge up 1.4% ytd and back near its 2008 high. But property stocks there are a different story, down 17% ytd and 70% since the peak. Homes beyond the affordability of the middle class, lack of working capital and scandal all explain it. to search for deeply oversold survivors.

Rose among thorns pgs. 4-6. The city with the greatest demand for office space with over 8m sqft leased out last year, and 8-10m expected this year. Unlike the others where residential prices are at all-time highs, in Bangalore they are still 20% below peak, and a growing middle class wants to buy.

A pure Bangalore play, Prestige Estates (PEPL IN, Rs140, TP Rs210) has 30% of its NAV in offices, 13% in retail, and the remainder in residential. The stock is at a 47% discount to NAV, with a free cash flow yield of 11% this year and 16% next. The debt to equity ratio is 0.3x, and yielding assets generate income which more than covers interest costs.

Plus: Gold pgs. 7-10. There is fresh interest in gold from endowment funds and income funds. Is this the last leg up or the start of another wave? Inflation and energy pgs.10-13. Around the world there is evidence high commodities prices are pinching the consumer. Yet Macquarie oil economist Jan Stuart says with emerging market demand still strong (and a good chance of supply interruption in the Middle East), oil prices will stay high or go higher. Your scribe would remain long energy stocks in Asia. Upcoming events pg. 14, Interesting articles pgs.15-19.

Hang Seng Composite Property & Construction Index vs. Bombay Stock Exchange Realty Index, relative performance past 3 years

Source: Bloomberg, Macquarie Research, April 2011

This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

Macquarie Research Guanxi

25 April 2011 2

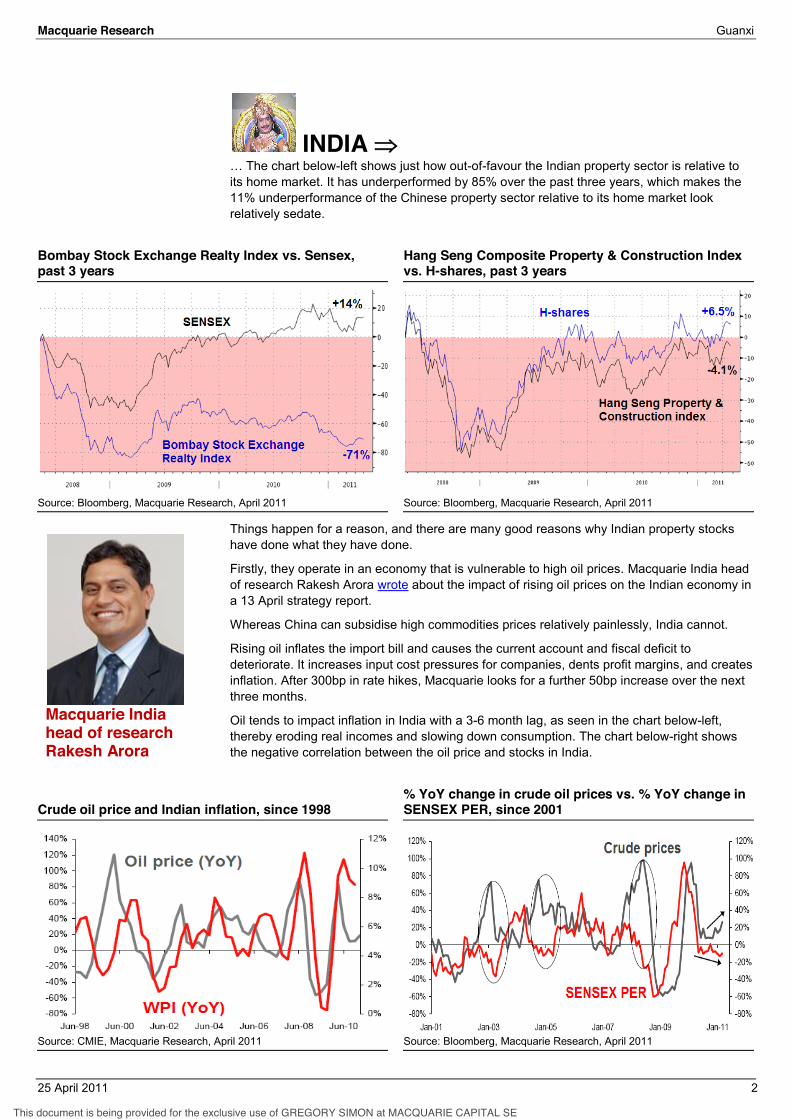

INDIA -left shows just how out-of-favour the Indian property sector is relative to

its home market. It has underperformed by 85% over the past three years, which makes the 11% underperformance of the Chinese property sector relative to its home market look relatively sedate.

Bombay Stock Exchange Realty Index vs. Sensex, past 3 years

Hang Seng Composite Property & Construction Index vs. H-shares, past 3 years

Source: Bloomberg, Macquarie Research, April 2011 Source: Bloomberg, Macquarie Research, April 2011

Things happen for a reason, and there are many good reasons why Indian property stocks have done what they have done.

Firstly, they operate in an economy that is vulnerable to high oil prices. Macquarie India head of research Rakesh Arora wrote about the impact of rising oil prices on the Indian economy in a 13 April strategy report.

Whereas China can subsidise high commodities prices relatively painlessly, India cannot.

Rising oil inflates the import bill and causes the current account and fiscal deficit to deteriorate. It increases input cost pressures for companies, dents profit margins, and creates inflation. After 300bp in rate hikes, Macquarie looks for a further 50bp increase over the next three months.

Oil tends to impact inflation in India with a 3-6 month lag, as seen in the chart below-left, thereby eroding real incomes and slowing down consumption. The chart below-right shows the negative correlation between the oil price and stocks in India.

Crude oil price and Indian inflation, since 1998

% YoY change in crude oil prices vs. % YoY change in SENSEX PER, since 2001

Source: CMIE, Macquarie Research, April 2011 Source: Bloomberg, Macquarie Research, April 2011

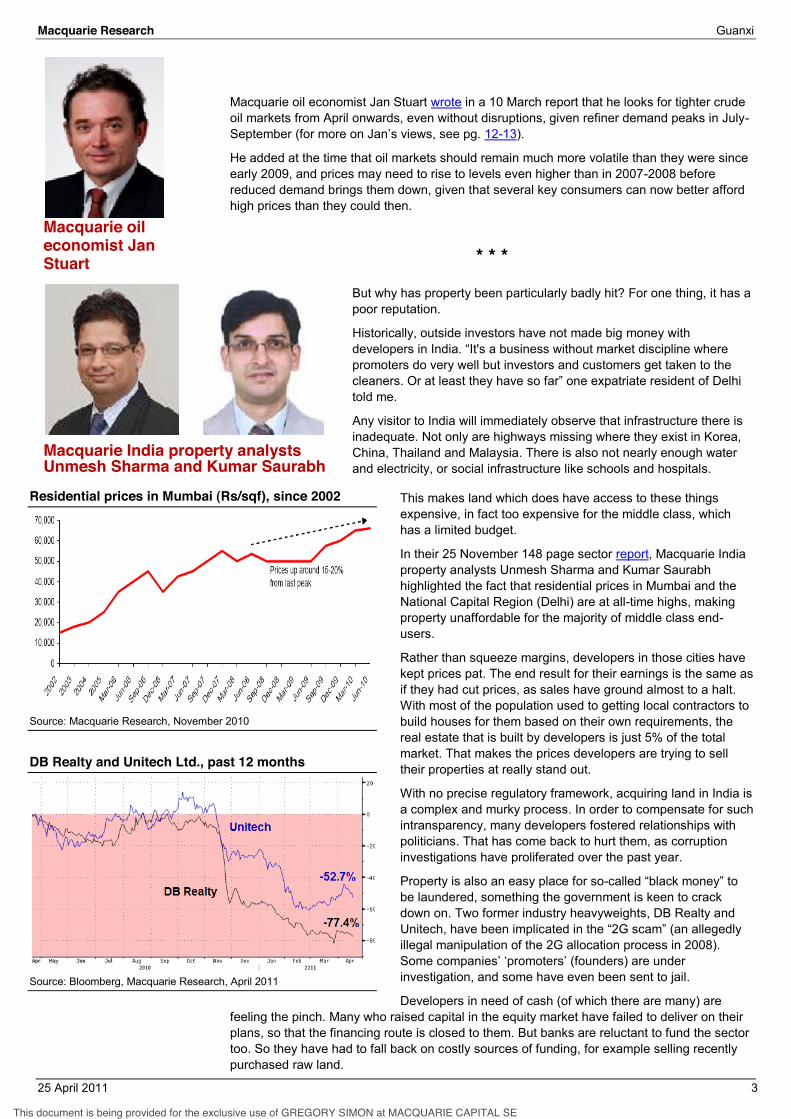

Macquarie India head of research Rakesh Arora

This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

Macquarie oil economist Jan Stuart wrote in a 10 March report that he looks for tighter crude oil markets from April onwards, even without disruptions, given refiner demand peaks in July-September (fo 12-13).

He added at the time that oil markets should remain much more volatile than they were since early 2009, and prices may need to rise to levels even higher than in 2007-2008 before reduced demand brings them down, given that several key consumers can now better afford high prices than they could then.

* * *

But why has property been particularly badly hit? For one thing, it has a poor reputation.

Historically, outside investors have not made big money with It's a business without market discipline where

promoters do very well but investors and customers get taken to the

told me.

Any visitor to India will immediately observe that infrastructure there is inadequate. Not only are highways missing where they exist in Korea, China, Thailand and Malaysia. There is also not nearly enough water and electricity, or social infrastructure like schools and hospitals.

This makes land which does have access to these things expensive, in fact too expensive for the middle class, which has a limited budget.

In their 25 November 148 page sector report, Macquarie India property analysts Unmesh Sharma and Kumar Saurabh highlighted the fact that residential prices in Mumbai and the National Capital Region (Delhi) are at all-time highs, making property unaffordable for the majority of middle class end-users.

Rather than squeeze margins, developers in those cities have kept prices pat. The end result for their earnings is the same as if they had cut prices, as sales have ground almost to a halt. With most of the population used to getting local contractors to build houses for them based on their own requirements, the real estate that is built by developers is just 5% of the total market. That makes the prices developers are trying to sell their properties at really stand out.

With no precise regulatory framework, acquiring land in India is a complex and murky process. In order to compensate for such intransparency, many developers fostered relationships with politicians. That has come back to hurt them, as corruption investigations have proliferated over the past year.

Property is also an easy place for so-be laundered, something the government is keen to crack down on. Two former industry heavyweights, DB Realty and Unitech, have been implicillegal manipulation of the 2G allocation process in 2008). Some compan (founders) are under investigation, and some have even been sent to jail.

Developers in need of cash (of which there are many) are feeling the pinch. Many who raised capital in the equity market have failed to deliver on their plans, so that the financing route is closed to them. But banks are reluctant to fund the sector too. So they have had to fall back on costly sources of funding, for example selling recently purchased raw land.

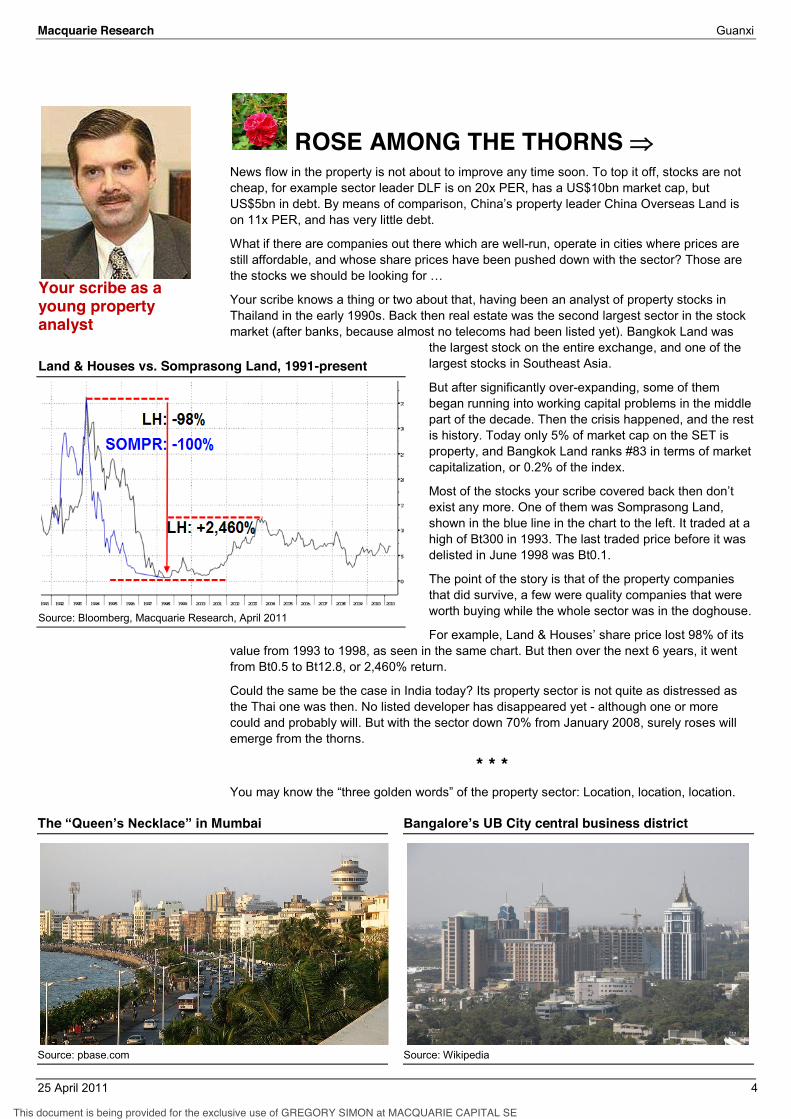

Macquarie oil economist Jan Stuart

Macquarie India property analysts Unmesh Sharma and Kumar Saurabh Residential prices in Mumbai (Rs/sqf), since 2002

Source: Macquarie Research, November 2010

DB Realty and Unitech Ltd., past 12 months

Source: Bloomberg, Macquarie Research, April 2011

This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

ROSE AMONG THE THORNS News flow in the property is not about to improve any time soon. To top it off, stocks are not cheap, for example sector leader DLF is on 20x PER, has a US$10bn market cap, but US$5bn in debt. By means of comparison, is on 11x PER, and has very little debt.

What if there are companies out there which are well-run, operate in cities where prices are still affordable, and whose share prices have been pushed down with the sector? Those are

Your scribe knows a thing or two about that, having been an analyst of property stocks in Thailand in the early 1990s. Back then real estate was the second largest sector in the stock market (after banks, because almost no telecoms had been listed yet). Bangkok Land was

the largest stock on the entire exchange, and one of the largest stocks in Southeast Asia.

But after significantly over-expanding, some of them began running into working capital problems in the middle part of the decade. Then the crisis happened, and the rest is history. Today only 5% of market cap on the SET is property, and Bangkok Land ranks #83 in terms of market capitalization, or 0.2% of the index.

Most of the stocks your scribe exist any more. One of them was Somprasong Land, shown in the blue line in the chart to the left. It traded at a high of Bt300 in 1993. The last traded price before it was delisted in June 1998 was Bt0.1.

The point of the story is that of the property companies that did survive, a few were quality companies that were worth buying while the whole sector was in the doghouse.

For example, Land & Houses lost 98% of its value from 1993 to 1998, as seen in the same chart. But then over the next 6 years, it went from Bt0.5 to Bt12.8, or 2,460% return.

Could the same be the case in India today? Its property sector is not quite as distressed as the Thai one was then. No listed developer has disappeared yet - although one or more could and probably will. But with the sector down 70% from January 2008, surely roses will emerge from the thorns.

* * *

The Q in Mumbai UB City central business district

Source: pbase.com Source: Wikipedia

Land & Houses vs. Somprasong Land, 1991-present

Source: Bloomberg, Macquarie Research, April 2011

Your scribe as a young property analyst

This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

Macquarie Research Guanxi

25 April 2011 5

-largest city in population terms, with 5.4m people. It is the third largest in GDP terms, at around US$80bn. It is also the only property market that Unmesh Sharma likes. Because it is in the South of India and far away from the border with Pakistan

including aeronautics and satellite technology. From that infrastructure sprang the IT industry for which it is so well-known today.

That makes it tech-dependent and therefore less diversified economically than Delhi or Bombay, but for the present time that is no bad thing. There has been a pick-up in hiring in Bangalore in the past year, and wages rose 15-24% after a 2-year lull. The city is also by far the most welcoming business location in the South. It is cosmopolitan and the easiest destination for non-South Indians to migrate to, which gives it an ethnically diverse and deep talent base.

Bangalore had the largest demand for office space in India last year with over 8m sqft leased out, and expectations are for 8-10m sqft this year. The residential property market also has the fundamental support of the IT industry, with end-users at 80% of demand, vs. 50% in Mumbai, according to Unmesh Sharma. Unlike Mumbai which is surrounded by the sea, Bangalore has plenty of land, and therefore there is less speculation and prices go up less rapidly. The bottom in

came six to nine months after those of the Mumbai and Delhi markets. So in Mumbai prices are now 20% above 2007 levels and volumes have ground to a halt, while in Bangalore they are 20% below where they were then and every quarter volumes rise about 10-15%.

. Prestige Estates (PEPL IN, Rs140, Outperform, TP: Rs210) is a real estate company that does business in Bangalore only. The company listed only in October last year with an IPO price of Rs183; the share price is Rs140 today. Its market cap is US$1bn, and it has traded US$2.4m since then. Twelve analysts follow the company, as opposed to the 41 who cover DLF.

Macquarie research and sales colleagues have visited their sites and attest to the fact that Prestige has quality products delivered on-time. For example, the UB

District. It is owned by UB (United Breweries, the owner of Kingfisher products, which is headquartered in Bangalore), and Prestige is the project contractor. Indeed most of income comes from the commercial segment, which is 30% of NAV, while retail is 13%, and the remainder is residential.

The debt to equity ratio is 0.3x, and yielding commercial and residential assets generate annuity income which more than covers interest costs. The free cash flow yield is 11% in FY12 (beginning April 2011) and 16% FY13 (beginning April 2012). Government Investment Corporation of Singapore owns about 5% of the stock. PER at 24x is very high, but your scribe thinks back to Thai property in

1998. PERs were even higher (due to the absence of profits) and NAV discounts even tighter (because companies had reduced their land banks). The stocks still went up many multiples.

Residential prices in Bangalore (Rs/sqf), since 2002 Prestige Estates discount to NAV, since listing

Source: Bloomberg, Macquarie Research, April 2011 Source: Wikipedia

Map of India

Source: wsup.com

Prestige Estate homes

Source: Prestige Estates

This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

Macquarie Research Guanxi

25 April 2011 6

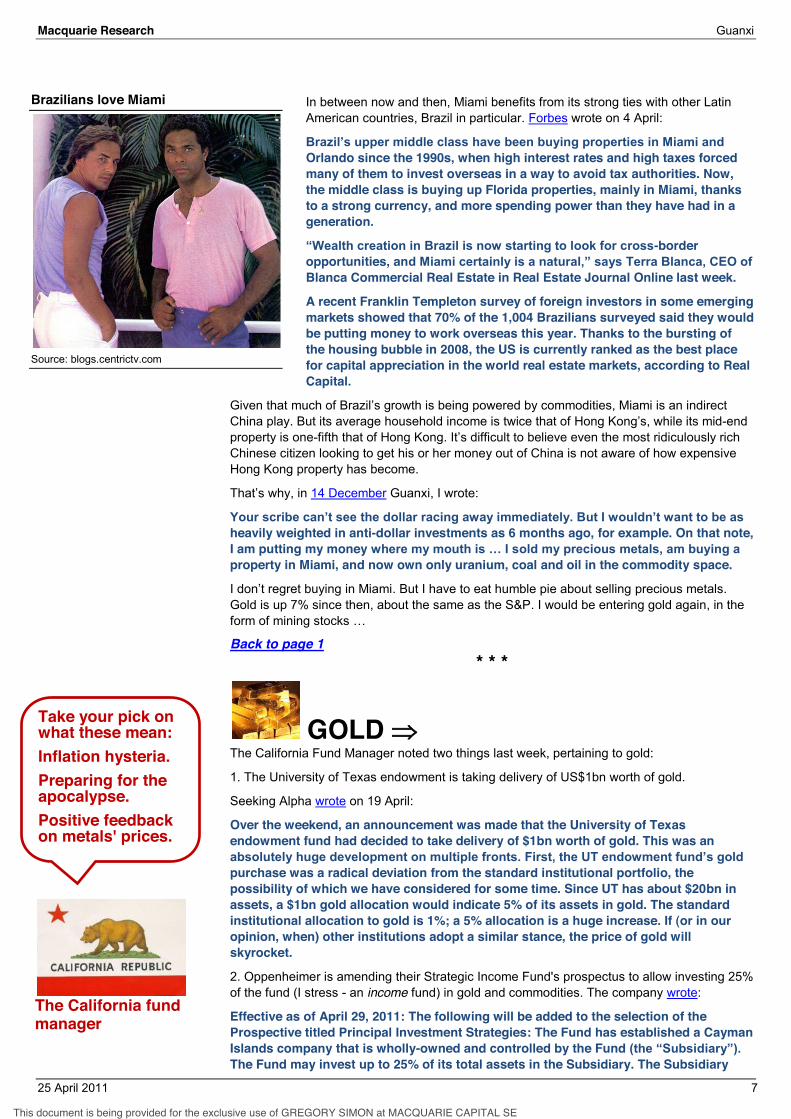

The stock trades at a 47% discount to NAV, which is basically in-line with the sector.

Indian property stocks discount to NAV

Source: Macquarie Research, April 2011

sum-of-the-parts based Rs210 target price is

the highest on the street (the average is Rs176). His 25-page November 2010 initiation report on the stock can be read here.

Back to page 1 * * *

PROPERTY Speaking of property, Business Insider magazine has produced foreclosure images o Frightening Satellite Tour Of America's Foreclosure Wastelands . The image for Miami can be seen to the left, with the red dots indicating homes in foreclosure. 1 in 14 homes were in foreclosure based on filings received in 2010.

But the chart to the left below shows that at these prices Miami looks like a good long-term investment, especially when compared to property in places like Hong Kong, as seen in the chart to the left. And perhaps when Fidel Castro eventually passes away, it will portend good things for Miami, as about one third of its residents are of Cuban extraction.

Miami vs. Hong Kong physical property prices, since 2005 Percent of population claiming Cuban ancestry, 2000

Source: Case-Shiller, Centaline, Macquarie Research, April 2011 Source: Bloomberg, Macquarie Research, April 2011

Miami properties in foreclosure in 2010

Source: businessinsider.com, Google Maps

NAV/share (Rs)

Source: Macquarie Research, November 2010

This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

In between now and then, Miami benefits from its strong ties with other Latin American countries, Brazil in particular. Forbes wrote on 4 April:

Orlando since the 1990s, when high interest rates and high taxes forced many of them to invest overseas in a way to avoid tax authorities. Now, the middle class is buying up Florida properties, mainly in Miami, thanks to a strong currency, and more spending power than they have had in a generation.

-border opportunities, anBlanca Commercial Real Estate in Real Estate Journal Online last week.

A recent Franklin Templeton survey of foreign investors in some emerging markets showed that 70% of the 1,004 Brazilians surveyed said they would be putting money to work overseas this year. Thanks to the bursting of the housing bubble in 2008, the US is currently ranked as the best place for capital appreciation in the world real estate markets, according to Real Capital.

Given that China play. But its average household income is twice that of -end property is one-fifth that of Hong Kong believe even the most ridiculously rich Chinese citizen looking to get his or her money out of China is not aware of how expensive Hong Kong property has become.

, in 14 December Guanxi, I wrote:

heavily weighted in anti-dollar investments as 6 months ago, for example. On that note, I am putting my money property in Miami, and now own only uranium, coal and oil in the commodity space.

in Miami. But I have to eat humble pie about selling precious metals. Gold is up 7% since then, about the same as the S&P. I would be entering gold again, in the form of mining stocks

Back to page 1 * * *

GOLD The California Fund Manager noted two things last week, pertaining to gold:

1. The University of Texas endowment is taking delivery of US$1bn worth of gold.

Seeking Alpha wrote on 19 April:

Over the weekend, an announcement was made that the University of Texas endowment fund had decided to take delivery of $1bn worth of gold. This was an

purchase was a radical deviation from the standard institutional portfolio, the possibility of which we have considered for some time. Since UT has about $20bn in assets, a $1bn gold allocation would indicate 5% of its assets in gold. The standard institutional allocation to gold is 1%; a 5% allocation is a huge increase. If (or in our opinion, when) other institutions adopt a similar stance, the price of gold will skyrocket.

2. Oppenheimer is amending their Strategic Income Fund's prospectus to allow investing 25% of the fund (I stress - an income fund) in gold and commodities. The company wrote:

Effective as of April 29, 2011: The following will be added to the selection of the Prospective titled Principal Investment Strategies: The Fund has established a Cayman Islands company that is wholly-owned and controlled by the Fund The Fund may invest up to 25% of its total assets in the Subsidiary. The Subsidiary

The California fund manager

Take your pick on what these mean: Inflation hysteria. Preparing for the apocalypse. Positive feedback on metals' prices.

Brazilians love Miami

Source: blogs.centrictv.com

This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

invests primarily in commodity-linked derivatives (including commodity futures, financial futures, options and swap contracts) and exchange traded funds related to

Gold is up six-fold in the past decade. Are these newsbytes the sign of a top, or of the last stage spike up? Your scribe put that question to vario

Stephen Harris, our Canada strategist, has been a gold bull for years. He wrote:

Gold is about investment demand - driven by low real US short rates and long term sovereign risk fears. I think it still has legs. There are far too many sceptics and doubters out there for this to be the peak. But for a pension fund to take physical delivery - that is just bizarre.

Gregory Simon of Macquari :

These stories mark the beginning of a market-led return to hard money. Gresham's Law: Bad money will drive good money out of circulation. It is not a bubble because gold is money, commodity money backed by natural law, while the US dollar is fiat money backed by legal tender laws. The price of two monies is determined by the demand for each one with US legal tender laws currently giving US dollar fiat

money a handicap over commodity gold money thus slowing down the market's current efforts to return to hard money.

Economists often refer to demand for money as "velocity". It can be influenced by many things, one being expected real returns. In the 1970s demand for the US dollar began to collapse due to price inflation resulting from monetary base inflation (debasement). Hence velocity of US dollar money spiked, while velocity of gold fell.

Then-Fed Chairman Volcker saw US dollar velocity was approaching hyperinflation and raised the Fed Funds rate to a high of 20% in May 1981. This caused a complete reversal of the demand for US dollar, while demand for gold naturally fell.

Fast-forward to today. Demand for US dollar has returned to the long-term trend, as can be seen in the chart to the left. As in the 1970s, the only event that can reverse the collapsing demand for dollar is increasing the return for holding it. That would mean the Fed once again spikes rates to above price inflation. But if the Fed raised reserve

requirements or the discount rate to achieve that, the effect on the mortgage market would be defaults and collapsing home prices. The Fed's balance sheet is updated regularly and can be seen on its website here. Within its total assets of US$2.6tr, the Fed holds US$1.3tr in treasuries and US$937bn in mortgage-backed securities. On the liabilities side, this is financed mainly through US$1tr of currency in circulation and US$1.5tr of reserve balances that Federal Reserve banks have on deposit at the Fed. An aggressive increase in interest rates risks breaking the Fed's balance sheet.

According to the Fed balance sheet reported gold holdings and monetary base, the monetary base would be back on a gold standard at $9,600, and I believe the market led return to a US dollar gold standard which is beginning to play out would be a relatively more orderly, and therefore more likely, scenario than another "Volcker Shock" event.

And

I'll pick answer #3. The US will be the last to get fully on board. Fringe investors were early, then big hedge funds, and now a few big institutions. But these are not mainstream signs. The next to move should be the big miners.

* * *

Macquarie Canada strategist Stephen Harris

Gold ounces that one US dollar can buy, since 1975

Source: Bloomberg, Macquarie Research, April 2011

Macquarie Tokyo salesperson Gregory Simon, and Boston salesperson Eric Wellmann

This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

Think about why people like gold. A lot of it is the legacy of gold standard currencies, a concept that is long since gone. So you hear arguments that "gold is a hedge against inflation". Actually no, this used to be true under gold standards, but

ny other.

nothing, which really for me breaks almost every rule of an investment.

I think an investment should return you money. In pro

how we value equities. We use a dividend discount model, which is really just another variant of the bond pricing model. Now try doing the same with gold. You can't.

So really - the only thing that makes it worth something is a pure extension of the greater fool theory - which is that "I'm willing to buy some of it

too ...".

Personally, your scribe is not as bearish on the US as are my American colleagues. Most people in the US seem to

on how to reduce it. Perhaps the negative outlook could even serve as a catalyst for them to come to agreement on

tes this bearish view on the US dollar.

Of note, the CBOE is back into very low territory, as seen in the chart to the left. 1998, when no one wanted to go near the baht. NPLs were over 30%, and much of the corporate sector was effectively insolvent. And look what the currency has done since, in the chart below-left.

However, if politics in the Middle East remain uncertain or get worse, if the peripheral skeletons pclosets again, and if interest rates remain low until some time next year at the earliest, it is easy to construe a picture of gold staying high or rising from here.

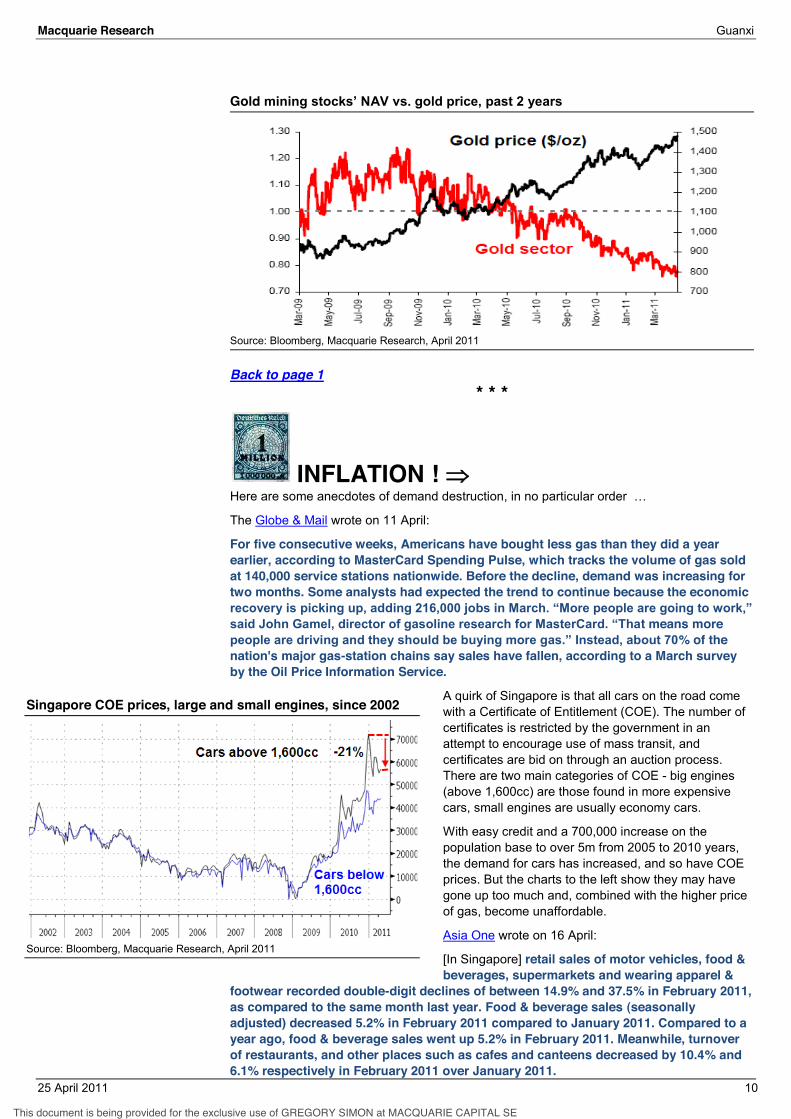

* * * forecast for gold this year is US$1,454/oz, next year US$1,487, and our long-

term assumption is US$1,649. The way to own gold in the mining stocks. Macquarie mining analyst Tony Lesiak wrote on 18 April:

Gold equities have significantly underperformed bullion and ETF's year to date, particularly those without significant silver exposure. Given the underperformance, the sector is currently on a free cash yield of 5.3% on 2012 metrics, with the sector trading at an average 28% discount to NAV on the forward curve, the lowest reading on record, and well below the two year average of 1.0x NAV. We currently forecast an average 37% return for the group over the next 12 months.

Barrick (ABX US, US$54.8, OP, curve commodity prices, Barrick, is trading at 12.4x PER and 8.7x CF, approximately 37% and 32% below the sector average on 2012 metrics, respectively. The stock trades at a 9% discount to its larger peers and a 27% discount to NAV parity.

End uses of gold, metric tonnes, 1975-2003

Source: Gold.org

Macquarie mining analyst Tony Lesiak

Large speculator net buying of US$ futures vs. US$ index, since 2001

Source: Bloomberg, Macquarie Research, April 2011

Thai baht, since 1991

Source: Bloomberg, Macquarie Research, April 2011

This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

INFLATION ! Here are some anecdotes of demand destruction, in no particular order

The Globe & Mail wrote on 11 April:

For five consecutive weeks, Americans have bought less gas than they did a year earlier, according to MasterCard Spending Pulse, which tracks the volume of gas sold at 140,000 service stations nationwide. Before the decline, demand was increasing for two months. Some analysts had expected the trend to continue because the economic

t means more % of the

nation's major gas-station chains say sales have fallen, according to a March survey by the Oil Price Information Service.

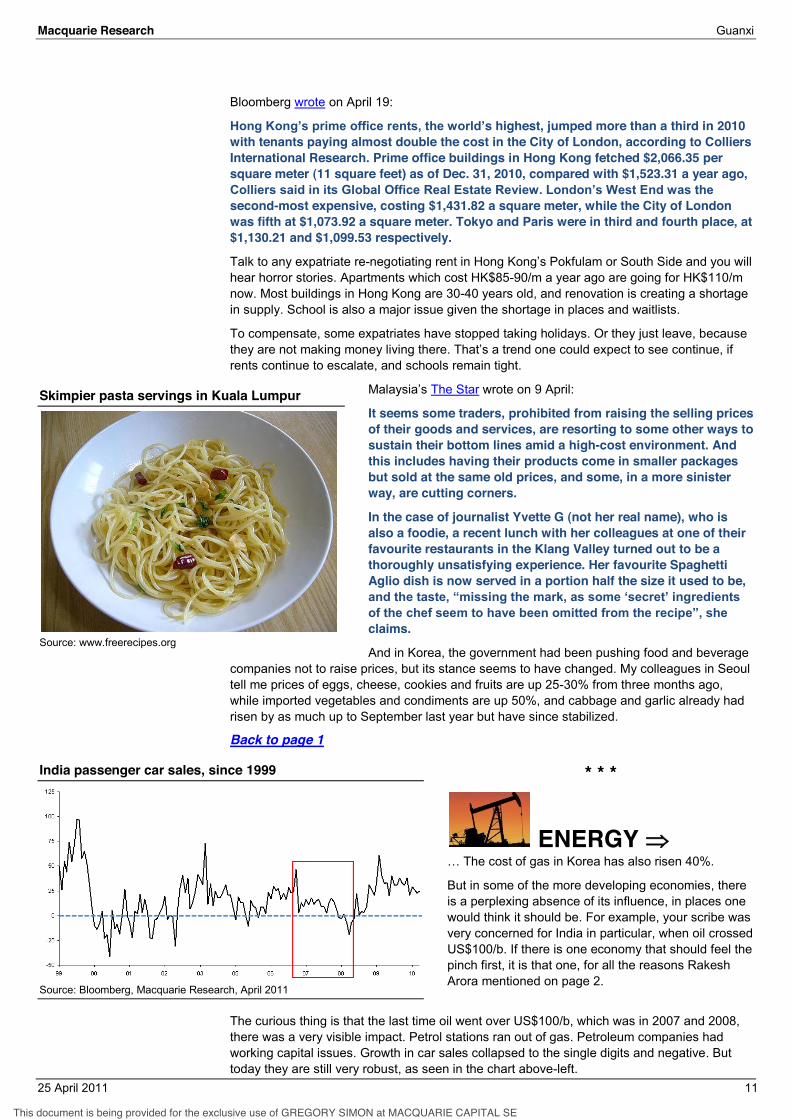

A quirk of Singapore is that all cars on the road come with a Certificate of Entitlement (COE). The number of certificates is restricted by the government in an attempt to encourage use of mass transit, and certificates are bid on through an auction process. There are two main categories of COE - big engines (above 1,600cc) are those found in more expensive cars, small engines are usually economy cars.

With easy credit and a 700,000 increase on the population base to over 5m from 2005 to 2010 years, the demand for cars has increased, and so have COE prices. But the charts to the left show they may have gone up too much and, combined with the higher price of gas, become unaffordable.

Asia One wrote on 16 April:

[In Singapore] retail sales of motor vehicles, food & beverages, supermarkets and wearing apparel &

footwear recorded double-digit declines of between 14.9% and 37.5% in February 2011, as compared to the same month last year. Food & beverage sales (seasonally adjusted) decreased 5.2% in February 2011 compared to January 2011. Compared to a year ago, food & beverage sales went up 5.2% in February 2011. Meanwhile, turnover of restaurants, and other places such as cafes and canteens decreased by 10.4% and 6.1% respectively in February 2011 over January 2011.

Singapore COE prices, large and small engines, since 2002

Source: Bloomberg, Macquarie Research, April 2011

This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

s highest, jumped more than a third in 2010 with tenants paying almost double the cost in the City of London, according to Colliers International Research. Prime office buildings in Hong Kong fetched $2,066.35 per square meter (11 square feet) as of Dec. 31, 2010, compared with $1,523.31 a year ago,

second-most expensive, costing $1,431.82 a square meter, while the City of London was fifth at $1,073.92 a square meter. Tokyo and Paris were in third and fourth place, at $1,130.21 and $1,099.53 respectively.

Talk to any expatriate re-hear horror stories. Apartments which cost HK$85-90/m a year ago are going for HK$110/m now. Most buildings in Hong Kong are 30-40 years old, and renovation is creating a shortage in supply. School is also a major issue given the shortage in places and waitlists.

To compensate, some expatriates have stopped taking holidays. Or they just leave, because they are not making money living thererents continue to escalate, and schools remain tight.

The Star wrote on 9 April:

It seems some traders, prohibited from raising the selling prices of their goods and services, are resorting to some other ways to sustain their bottom lines amid a high-cost environment. And this includes having their products come in smaller packages but sold at the same old prices, and some, in a more sinister way, are cutting corners.

In the case of journalist Yvette G (not her real name), who is also a foodie, a recent lunch with her colleagues at one of their favourite restaurants in the Klang Valley turned out to be a thoroughly unsatisfying experience. Her favourite Spaghetti Aglio dish is now served in a portion half the size it used to be,

claims.

And in Korea, the government had been pushing food and beverage companies not to raise prices, but its stance seems to have changed. My colleagues in Seoul tell me prices of eggs, cheese, cookies and fruits are up 25-30% from three months ago, while imported vegetables and condiments are up 50%, and cabbage and garlic already had risen by as much up to September last year but have since stabilized.

Back to page 1

* * *

ENERGY he cost of gas in Korea has also risen 40%.

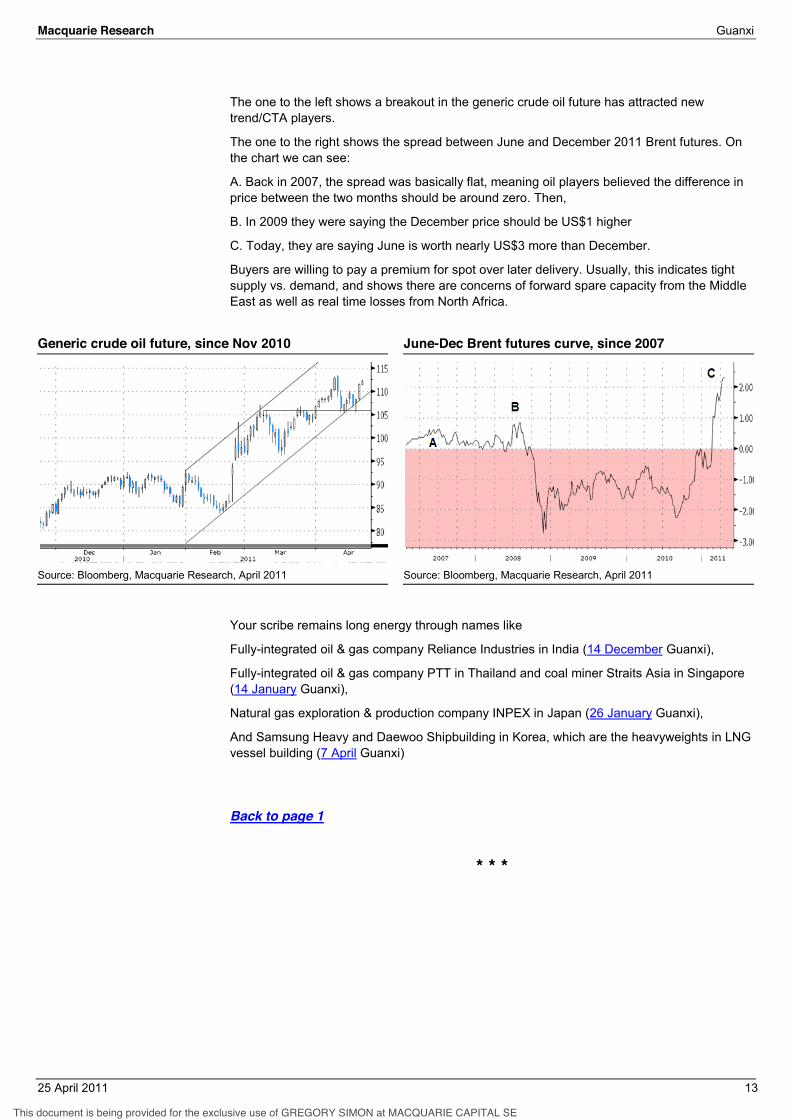

But in some of the more developing economies, there is a perplexing absence of its influence, in places one would think it should be. For example, your scribe was very concerned for India in particular, when oil crossed US$100/b. If there is one economy that should feel the pinch first, it is that one, for all the reasons Rakesh Arora mentioned on page 2.

The curious thing is that the last time oil went over US$100/b, which was in 2007 and 2008, there was a very visible impact. Petrol stations ran out of gas. Petroleum companies had working capital issues. Growth in car sales collapsed to the single digits and negative. But today they are still very robust, as seen in the chart above-left.

India passenger car sales, since 1999

Source: Bloomberg, Macquarie Research, April 2011

Skimpier pasta servings in Kuala Lumpur

Source: www.freerecipes.org

This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

When I asked colleagues in our Indian office why car sales have been so robust today, they said it is understandable. For one, average nominal income growth in the 3-4 years since the Global Financial Crisis has been 16%, which makes the consumer better able to consume.

Back then, banks were very aggressive in 2-wheeler and auto financing, but withdrew more or less completely when it became clear the developed world was in trouble during the Global Financial Crisis. The slowdown came very swiftly, and people went into a state of fear psychosis. One of the biggest lenders was ICICI Bank, their large international loans could not be rolled over, and onshore indiscriminate lending led to a large asset quality issue whereas their loan growth has basically been flat since then.

* * * Indeed it is precisely because of demand for energy in India, China and other emerging markets that oil could still go much highe

Macquarie oil economist Jan Stuart was in Singapore last week so I was able to catch up with him. Jan thinks demand weakness is seasonal at best and there will be a re-acceleration of demand in Asia in 2H. He expects global oil demand to grow 2.6% vs consensus at 1.5%.

His forecast for the average Brent crude price this year is US$117/b, US$120/b next year, US$119/b in 2013, and a long-term average of US$88/b. These forecasts are predicated on strong underlying trend demand growth in emerging markets, before it ultimately leads to demand destruction globally. For example, 12% YoY last year. Jan had forecast it to fall to 6% this year, but it is still in the double-digits so far this year.

On that note, on 7 April ExxonMobil hosted The Outlook for Energy: A View to 2030, which Macquarie oil & gas analyst Trevor Buchinski attended. The company said:

In 2005, OECD and non-OECD energy demand were essentially equal. However, gains in efficiency mean OECD demand will be flat between now and 2030, while non-OECD demand should increase by 45%. So by 2030, non-OECD demand should exceed OECD demand by 77%.

Global transportation demand is expected to rise by nearly 40% by 2030, driven by Asia Pacific where it is expected to double. The company projects light vehicles to rise from 800m today to 1.2bn, with more than a third of the new vehicles driven in China. Demand for commercial transportation is expected to grow by 30% in Europe and North America but more than double in Asia Pacific.

Energy demand, quadrillion BTUs, 1980-2030E Forecast global energy demand per sector, 2005-2030

Source: Exxon Mobil, Macquarie Research, April 2011 Source: Bloomberg, Macquarie Research, April 2011

Jan also thinks equity investors are far too complacent on the risk of supply disruption in the Middle East and North Africa. It is impossible to forecast who exactly will interrupt their exports, but if either Algeria or Oman did for example, there would be a huge spike in the oil price, to about US$150/b or so. He puts this chance at approximately 30%. Oil would however then fall quickly, on demand destruction.

The charts below suggests the oil market is worried.

This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

The one to the left shows a breakout in the generic crude oil future has attracted new trend/CTA players.

The one to the right shows the spread between June and December 2011 Brent futures. On the chart we can see:

A. Back in 2007, the spread was basically flat, meaning oil players believed the difference in price between the two months should be around zero. Then,

B. In 2009 they were saying the December price should be US$1 higher

C. Today, they are saying June is worth nearly US$3 more than December.

Buyers are willing to pay a premium for spot over later delivery. Usually, this indicates tight supply vs. demand, and shows there are concerns of forward spare capacity from the Middle East as well as real time losses from North Africa.

Generic crude oil future, since Nov 2010 June-Dec Brent futures curve, since 2007

Source: Bloomberg, Macquarie Research, April 2011 Source: Bloomberg, Macquarie Research, April 2011

Your scribe remains long energy through names like

Fully-integrated oil & gas company Reliance Industries in India (14 December Guanxi),

Fully-integrated oil & gas company PTT in Thailand and coal miner Straits Asia in Singapore (14 January Guanxi),

Natural gas exploration & production company INPEX in Japan (26 January Guanxi),

And Samsung Heavy and Daewoo Shipbuilding in Korea, which are the heavyweights in LNG vessel building (7 April Guanxi)

Back to page 1

* * *

This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

INTERESTING ARTICLES Wages and inflation 4 April: Inflation is back, with higher prices for food and fuel

prices are rising

arch 4 April: The Treasury paid out $1.1187tr. When the $65.898bn in tax refunds is deducted from that, the Treasury paid a net of $1.0528 trillion in federal expenses for March. That $1.0528 trillion in spending for March equaled 8.2 times the $128.179bn in net federal tax revenue for the month.

Subprime bonds 1 April: Subprime and other residential mortgage bonds that helped trigger the financial crisis are back in vogue with long-term investors, in the latest sign that American credit markets are healing after the worst downturn in a generation.

American free market 6 April: Confidence in the free market economy has dropped sharply in the past year, and is now lower than in China, according to a GlobeScan poll released today. The findings, drawn from 12,884 interviews across 25 countries, show that there has been a sharp fall in the number of Americans who think that the free market economy is the best economic system for the future.

US markets with QE2, QE3 or another stimulus by another name and risk runaway inflation. End it, and risk the collapse of the economy which very likely cannot stand on its own. The good news is that there is no real inflation, that being asset inflation.

Rolling Stone Magazine 11 April: From the real financial press: "The Real Housewives of Wall Street", Matt Taibbi, Rolling Stone, 11 April 2011 -- "Why is the Federal Reserve forking over $220m in bailout money to the wives of two Morgan Stanley bigwigs?"

SF Gate 10 April: The report of 216,000 new jobs in March is being touted as evidence that we're finally out of the woods. But in reality, we're still in the swamp and in danger of sinking. Consumers are 70% of the American economy, and consumer confidence is plummeting. It's weaker today on average than at the lowest point of the Great Recession.

LA Times 10 April: IKEA's US factory churns out unhappy workers. A union-organizing battle hangs over the IKEA plant in Virginia. Workers complain of eliminated raises, a frenzied pace, mandatory overtime and racial discrimination.

Reuters 10 April: The United States is beset by violence, racism and torture and has no authority to condemn other governments' human rights problems, China said on Sunday, countering U.S. criticism of Beijing's crackdown.

Cambridge University: Research suggests the importance of diversifying exports away from a handful of primary commodities to technology intense goods. It also suggests that resource abundant countries could manage the volatility better by investing oil revenues in sovereign wealth funds to use at a later date.

CNBC CNBC, said

ri.

The Telegraph 13 April: Debt-laden banks are the biggest threat to global financial stability and they must refinance a $3.6tr "wall of maturing debt" which comes due in the next two years, the International Monetary Fund said in its Global Financial Stability Report.

Source:

This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

Businessweek 14 April: There's always someone out there crying bubble, it seems; the trick is figuring out when it's easy money and when it's a shell game. Some bubbles actually do some good, even if they don't end happily. In the 1980s, the rise of Microsoft, Compaq, and Intel pushed personal computers into millions of businesses and homes and the stocks of those companies soared. Tech stumbled in the late 1980s, and the Valley was left with lots of cheap microprocessors and theories on what to do with them. The dot-com boom was built on infatuation with anything Web-related. Then the correction began in early 2000, eventually vaporizing about $6tr in shareholder value. But that cycle, too, left behind an Internet infrastructure that has come to benefit businesses and consumers.

In the 1980s, the rise of Microsoft, Compaq, and Intel pushed personal computers into millions of businesses and homes and the stocks of those companies soared. Tech stumbled in the late 1980s, and the Valley was left with lots of cheap microprocessors and theories on what to do with them. The dot-com boom was built on infatuation with anything Web-related. Then the correction began in early 2000, eventually vaporizing about $6tr in shareholder value. But that cycle, too, left behind an Internet infrastructure that has come to benefit businesses and consumers.

This time, the hype centers on more precise ways to sell. At Zynga, they're mastering the art of coaxing game players to take surveys and snatch up credit-card deals. Elsewhere, engineers burn the midnight oil making sure that a shoe ad follows a consumer from Web site to Web site until the person finally cracks and buys some new kicks.

This latest craze reflects a natural evolution. A focus on what economists call general-purpose technology steam power, the Internet router has given way to interest in consumer products such as iPhones and streaming movies. "Any generation of smart people will be drawn to where the money is, and right now it's the ad generation," says Steve Perlman, a Silicon Valley entrepreneur who once sold WebTV to Microsoft for $425m and is now running OnLive, an online video game service. "There is a goodness to it in that people are building on the underpinnings laid by other people."

"What are the implications of rising commodity prices for inflation and monetary policy?", by Charles L. Evans (president) and Jonas D. M. Fisher (Director of macroeconomic research), Chicago Fed, May:

The recent run-ups in oil and other commodity prices and their implications for inflation and monetary policy have grabbed the attention of many commentators in the media. Clearly, higher prices of food and energy end up in the broadest measures of consumer price inflation, such as the Consumer Price Index. Since the mid-1980s, however, sharp increases and decreases in commodity prices have had little, if any, impact on core inflation, the measure that excludes food and energy prices.

Scientific American 13 Dec 2007: the waste produced by coal plants is actually more radioactive than that generated by their nuclear counterparts. In fact, the fly ash emitted by a power plant a by-product from burning coal for electricity carries into the surrounding environment 100 times more radiation than a nuclear power plant producing the same amount of energy.

Spike Japan ot widely known, but the feckless, reckless, and soon to be penniless operator of the Fukushima Daiichi nuclear power plant, Tokyo Electric Power (TEPCO), built an eight-storey tribute to itself, Denryokukan The Hall of Electric Power deep in the heart of the Tokyo youth fashion mecca of Shibuya back in the Orwellian year of 1984, when the picking of the fruits of its tree of monopoly profits was good.

Scientific American 13 December: By burning away all the pesky carbon and other impurities, coal power plants produce heaps of radiation. Therefore coal ash is more radioactive than nuclear waste.

This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

Globalresearch.ca 14 April: Congress should shut down speculator casinos like the Chicago Mercantile Exchange and the NYMEX, while nationalizing the Four Horsemen and the monopoly food processors. We should form a US Energy Company and a US Food Processing Company which would focus on renewable energy and healthier diversified diet.

Business Insider 11 April: The UK's austerity program is hitting home, and coupled with soaring inflation is slamming the country's workforce. Disposable income has now fallen the most since 1921, excluding war time, according to Center for Economics and Business Research.

UK national debt 8 April: Britain s national debt is equivalent to £138,360 for every household in the country, it has been revealed. The Daily Mail reports that the national debt is National Statistics state that the total public sector debt is around £876bn - or £33,100 per household in the country. And if all the debt from the banks rescued by the State is taken into account, the figure rises to £2.3tn.

China

Reuters 13 April:

Chinese investors including the country's sovereign wealth fund may inject $13bn into Spanish banks, a government source said on Wednesday after Spain's premier met financial authorities in Beijing. There was no immediate comment from Beijing and it was not clear what terms would make the risk attractive to China, which has invested cautiously in overseas financial markets in the last couple of years partly to avoid any criticism it is squandering reserves.

In China, instructions are issued to the media and/or Internet companies by various central (and sometimes local) government authorities. Some have been leaked and posted online, such as at China Digital Times. Here is one of the odder ones: "State Council Information Office: Plans for Japanese to Immigrate to Hainan Island, China", April 2. From the Ninth Bureau of the State Council Information Office: All websites are asked to monitor interactive spaces and

Articles about cadmium pollution of rice in China, by Gong Jing (reporter), Century Weekly, April. Part one: How serious is cadmium pollution? Part two: Tracing the sources Part three: Fixing the problem

Other Asia

The Australian 8 April: The Fukushima nuclear disaster has spurred a jump of up to 10% in Japanese demand for liquefied natural gas and could move the oversupplied global LNG market into balance over the next year, industry experts say.

WSJ 11 April: Japan's economy minister is urging the nation to emerge from the shadow of self-restraint that has enveloped the country in the wake of the earthquake and tsunami, in an attempt to foster consumer spending and boost economic activity. "I think it's time to stop this feeling of self-restraint, and many ministers share that view with me," Economy Minister Kaoru Yosano said. Mr. Yosano's comments Friday represent the first official backlash against jishukuthe Japanese word for "self-restraint" which has become a buzzword over the past month. What started as an unspoken movement reflecting national solidarity, with people voluntarily turning off lights to conserve energy and organizations canceling events such as concerts, has threatened to bring Japan new trouble: a prolonged economic slump. Now, some Japanese are rebelling, as an anti-jishuku campaign has started to fan out, mainly across Tokyo.

This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

Yomiuri Shimbun 14 April: Prof. Koshun Yamaoka of Nagoya University pointed out that seismic activity in northern Chiba and southern Ibaraki Prefectures, which is also linked to the Philippine Sea plate, has increased."An earthquake could hit the Tokyo metropolitan area with its focus directly below the city. We'll have to observe the situation carefully," Yamaoka added. The professor anticipates the rise in seismic activity in eastern Japan will continue for four or five years.

He said magnitude-7 quakes "are likely to occur once or twice in the next month." "After that, they can be expected to happen once in two months. The occurrence of such huge earthquakes will gradually decrease to once in a half year. But the possibility remains that a magnitude-8 earthquake could happen at any time," Yamaoka warned.

New Temasek Review 11 April: Controversial PAP MP Wee Siew Kim has retired from politics. He has been a MP in Ang Mo Kio GRC for almost ten years. Mr Wee came into public spotlight when his daughter Wee Shu Min made disparaging remarks about a fellow Singaporean Mr Derek Wee on her blog in 2006.

Mr Wee, 35, a Singaporean who works for a multinational corporation, had written in his blog on Oct 12 that he was concerned about competition from foreign talent and the lack of job opportunities for older workers here, therefore he asked that the government try to be more understanding of such employment woes.

Ms Wee, then a second year Humanities in Raffles Junior College ridiculed Mr -

outcry in cyberspace, prompting Mr Wee Siew Kim to issue a half-hearted public apology.

David Streckfuss, Truth on Trial in Thailand: Defamation, Treason and Lèse-Majesté in New Mandala, 20 December 2010: There can be few institutions in the world so fundamentally important to a

is so limited, as the Thai monarchy.

6 coup and its aftermath has resulted in a flurry of criticism of its political machinations in the media and especially on the Internet (though less in traditional academic discourse), it is remarkable and not a little disheartening that after sixty years there exists only a single, critical academic biography of King Bhumibol - Paul

The King Never Smiles.

Within the much more restricted environment of Thailand, a small handful of academics and intellectuals the Thammasat University historian Somsak Jeamteerasakul and the veteran social critic Sulak Sivaraksa most prominent among them - have recently made the case for the democratic reform of the monarchy. The importance of the institution makes it striking, however, that they have not been joined by a larger number of academics and intellectuals, let alone politicians and the general public.

For it is possible to engage in such a discussion within the bounds of legality. This relative silence is all the more perplexing when the present reign is drawing to a close and there is an urgent need for rational consideration of how the monarchy needs to be reformed to create the truly democratic Thailand that all parties to the present conflict appear to advocate.

Neel Chowdhury wrote in TIME magazine on 25 April: After ferociously sucking jobs and investment out of Southeast Asia over the past two decades, the China Effect is now lifting once declining industrial hubs like Penang out of their long economic slump. The northern Malaysian state attracted $4bn in investment for its manufacturing sector in 2010, according to the Malaysian Investment Development Authority, a 465% jump from 2009.

This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

Tech Crunch 10 April: Peter Thiel. And Thiel the PayPal co-founder, hedge ociety

a difference, why not franchise it so more people can attend? Why not create 100 Harvastatus. In education your value depends on other people failing. Whenever

way to ignore that people are falling through the cracks, because you pretend

Frank Yu wrote in TechRice on 19 May: This Tech Industry expansion is for real or at least more substantial than the last dotcom surge [because]:

Companies like Facebook, Google and Zynga not only have millions of monthly active users, they have millions of dollars in revenue to show for it. So for companies like Twitter, Instagram and Foursquare that have many users but still little revenue, there is at least a potential for them to convert their communities into paying customers. In the 90s, many dotcoms that were created needed to burn millions of dollars in investment just to acquire new users from traditional brick and mortar industries.

In the first Internet bubble, New Media companies were trying to disrupt traditional brick and mortar businesses by converting their customers onto an online platform to buy groceries, book air flights, buy pet food, sell used goods

serve a social need that is unique to the medium.

s build and grow in a very different way than those in the 90s. Lean startup methodology entails building a business through the development of minimal viable products and letting user feedback guide further development and iteration in a rapid fashion.

With less need for large initial rounds of capital, startups can now subsist on seed investment or even bootstrap themselves with minimal revenue flow.

This new tech expansion also means that the IPO is not necessarily needed early in the lifecycle of a startup to get additional capital and an exit for some investors.

Back to page 1

* * *

This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

10 June (Moving averages, sentiment indicator, liquidity indicator, long-term PERs, thoughts from Macquarie strategists Matthias Joerss and Ralf Zimmermann, the view from Sydney).

25 June (Chinese Yuan: The Asian Crisis in reverse, technical bounce indicators fading, implications of rising wages in China, furniture maker Man Wah and packaging company Nine Dragons, value in up-side calls on the Hang Seng Index and H-shares, an analysis of North Korea).

1 July

8 July (Financial markets in the context of the Kübler-Ross Grief Cycle, US Weekly Leading Index vs. GDP growth and stock market performance, why 15 April was an inflection point, US Trend Indicator and World Leading Economic Indicator vs. Asian exports and earnings, reasons to like China A-shares, Banpu and CNOOC).

20 August (The rising cost of Chinese labour, a basket of lesser-known Indian infrastructure stocks on 16x PER have 20% CAGR, low bond and bank deposit yields make 8 telecom stocks with a solid average dividend yield 6.5% appealing, buy Japan for a dividends, Sell Taiwan PC makers).

27 August (German exports are China dependent, Toyota shuts domestic capacity, cigarette p ROE from 7.5% to 14.5% yet share price remains 50% below its highs, Williams R % Oscillator bearish US and Japan, bullish Europe and Asia ex-Japan).

3 September zero QoQ growth, believers and disbelievers in QE2, Chinese citizens positive on property for 1st time in 6 months, MSCI Asia ex-Japan Index has tracked its 50% retracement

not to buy Singapore property.

17 September (Chart breakouts in S&P, MSCI Asia ex-Japan, metals, Sing dollar, Clinton in 1994 vs. Obama in 2010, the value of call options, bull market in Southeast Asia, Korea as an emerging markets play, time to buy LG Display, 3 energy stocks).

29 September ng reshuffle of US economic policymakers, the attributes of platinum and palladium, North American Palladium, consumer stocks in Asia, CJ O Shopping, Singapore Exchange and Baidu).

14 October negative impact on Asian stock markets (if it reinvigourates the US economy), Mr. dollar futures as a leading indicator, quantitative analysis, Chinese Internet stocks are overvalued).

2 December the positive correlation between A shares and interest rates, vegetable producer China Minzhong will double capacity next year, Samsung is an indirect Apple play, Esso Thailand going into the black after 3Qs of losses).

14 December (large speculators buying dollars, changes in personalities at the Fed and the ECB in 2011, Keynesians vs. Austerians, US ISM manufacturing strength and our increased GDP forecast, do markets return to their mean or develop new means, impending supply/demand imbalance in oil, reasons to own Reliance Industries).

14 January ( longer coal prices are good news for Straits Asia, AIA is at the top end of fair value and an excellent funding short).

26 January (Three investments should do well in an environment of strong global growth and rising commodity prices: A KOSDAQ basket and/or KOSDAQ listed stock Melfas, Malaysia, which is commodity-rich and where foreign investment in

).

2 February as, China Mobile is a

giant value stock).

21 February ( r corn, wheat, potato and soybean prices, the Middle East, Macquarie quantitative screen ranks Thailand at the top of both developed and emerging markets, BIG C Supercentre.

3 March (Technicals of oil, the Middle East, the experience of the Iranian Revolution, questioning core assumptions, frontier markets the canaries in the coal mine).

7 April (Relationship between stocks, commodities, and Fed action, Chinese tightening coming to an end, seasonality in nt theme, a sweet spot for LNG, buy LNG vessel makers Samsung Heavy and

Daewoo Shipbuilding given 8% CAGR demand growth for LNG yet almost no vessels have been ordered since 2007.)

This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

Important disclosures: Recommendation definitions Macquarie - Australia/New Zealand Outperform return >5% in excess of benchmark return Neutral return within 5% of benchmark return Underperform return >5% below benchmark return Macquarie Asia/Europe Outperform expected return >+10% Neutral expected return from -10% to +10% Underperform expected return <-10% Macquarie First South - South Africa Outperform expected return >+10% Neutral expected return from -10% to +10% Underperform expected return <-10% Macquarie - Canada Outperform return >5% in excess of benchmark return Neutral return within 5% of benchmark return Underperform return >5% below benchmark return Macquarie - USA Outperform (Buy) return >5% in excess of Russell 3000 index return Neutral (Hold) return within 5% of Russell 3000 index return Underperform (Sell) return >5% below Russell 3000 index return Recommendations 12 months Note: Quant recommendations may differ from Fundamental Analyst recommendations

Volatility index definition* This is calculated from the volatility of historical price movements. Very high highest risk Stock should be expected to move up or down 60 100% in a year investors should be aware this stock is highly

speculative. High stock should be expected to move up or down at least 40 60% in a year investors should be aware this stock could be speculative. Medium stock should be expected to move up or down at least 30 40% in a year. Low medium stock should be expected to move up or down at least 25 30% in a year. Low stock should be expected to move up or down at least 15 25% in a year. * Applicable to Australian/NZ/Canada stocks only

Financial definitions All "Adjusted" data items have had the following adjustments made: Added back: goodwill amortisation, provision for catastrophe reserves, IFRS derivatives & hedging, IFRS impairments & IFRS interest expense Excluded: non recurring items, asset revals, property revals, appraisal value uplift, preference dividends & minority interests EPS = adjusted net profit / efpowa* ROA = adjusted ebit / average total assets ROA Banks/Insurance = adjusted net profit /average total assets ROE = adjusted net profit / average shareholders funds Gross cashflow = adjusted net profit + depreciation *equivalent fully paid ordinary weighted average number of shares All Reported numbers for Australian/NZ listed stocks are modelled under IFRS (International Financial Reporting Standards).

Recommendation proportions For quarter ending 31 March 2011 AU/NZ Asia RSA USA CA EUR Outperform 45.65% 65.72% 59.70% 43.02% 68.91% 51.16% (for US coverage by MCUSA, 14.36% of stocks covered are investment banking clients) Neutral 39.49% 19.00% 29.85% 53.09% 26.43% 35.73% (for US coverage by MCUSA, 17.55% of stocks covered are investment banking clients) Underperform 14.86% 15.28% 10.45% 3.89% 4.66% 13.11% (for US coverage by MCUSA, 0.00% of stocks covered are investment banking clients)

Company Specific Disclosures: Important disclosure information regarding the subject companies covered in this report is available at www.macquarie.com/research/disclosures.

Analyst Certification: The views expressed in this research accurately reflect the personal views of the analyst(s) about the subject securities or issuers and no part of the compensation of the analyst(s) was, is, or will be directly or indirectly related to the inclusion of specific recommendations or views in this research. The analyst principally responsible for the preparation of this research receives compensation based on overall revenues of Macquarie Group Ltd ABN 94 122 169 279 (AFSL No. 318062) (MGL) and its related entities (the Macquarie Group) and has taken reasonable care to achieve and maintain independence and objectivity in making any recommendations. General Disclaimers: Macquarie Securities (Australia) Ltd; Macquarie Capital (Europe) Ltd; Macquarie Capital Markets Canada Ltd; Macquarie Capital Markets North America Ltd; Macquarie Capital (USA) Inc; Macquarie Capital Securities Ltd and its Taiwan branch; Macquarie Capital Securities (Singapore) Pte Ltd; Macquarie Securities (NZ) Ltd; Macquarie First South Securities (Pty) Limited; Macquarie Capital Securities (India) Pvt Ltd; Macquarie Capital Securities (Malaysia) Sdn Bhd; Macquarie Securities Korea Limited and Macquarie Securities (Thailand) Ltd are not authorized deposit-taking institutions for the purposes of the Banking Act 1959 (Commonwealth of Australia), and their obligations do not represent deposits or other liabilities of Macquarie Bank Limited ABN 46 008 583 542 (MBL) or MGL. MBL does not guarantee or otherwise provide assurance in respect of the obligations of any of the above mentioned entities. MGL provides a guarantee to the Monetary Authority of Singapore in respect of the obligations and liabilities of Macquarie Capital Securities (Singapore) Pte Ltd for up to SGD 35 million. This research has been prepared for the general use of the wholesale clients of the Macquarie Group and must not be copied, either in whole or in part, or distributed to any other person. If you are not the intended recipient you must not use or disclose the information in this research in any way. If you received it in error, please tell us immediately by return e-mail and delete the document. We do not guarantee the integrity of any e-mails or attached files and are not responsible for any changes made to them by any other person. MGL has established and implemented a conflicts policy at group level (which may be revised and updated from time to time) (the "Conflicts Policy") pursuant to regulatory requirements (including the FSA Rules) which sets out how we must seek to identify and manage all material conflicts of interest. Nothing in this research shall be construed as a solicitation to buy or sell any security or product, or to engage in or refrain from engaging in any transaction. In preparing this research, we did not take into account your investment objectives, financial situation or particular needs. Before making an investment decision on the basis of this research, you need to consider, with or without the assistance of an adviser, whether the advice is appropriate in light of your particular investment needs, objectives and financial circumstances. There are risks involved in securities trading. The price of securities can and does fluctuate, and an individual security may even become valueless. International investors are reminded of the additional risks inherent in international investments, such as currency fluctuations and international stock market or economic conditions, which may adversely affect the value of the investment. This research is based on information obtained from sources believed to be reliable but we do not make any representation or warranty that it is accurate, complete or up to date. We accept no obligation to correct or update the information or opinions in it. Opinions expressed are subject to change without notice. No member of the Macquarie Group accepts any liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this research and/or further communication in relation to this research. Clients should contact analysts at, and execute transactions through, a Macquarie Group entity in their home jurisdiction unless governing law permits otherwise. Country-Specific Disclaimers: Australia: In Australia, research is issued and distributed by Macquarie Securities (Australia) Ltd (AFSL No. 238947), a participating organisation of the Australian Securities Exchange. New Zealand: In New Zealand, research is issued and distributed by Macquarie Securities (NZ) Ltd, a NZX Firm. Canada: In Canada, research is prepared, approved and distributed by Macquarie Capital Markets Canada Ltd, a participating organisation of the Toronto Stock Exchange, TSX Venture Exchange & Montréal Exchange. Macquarie Capital Markets North America Ltd., which is a registered broker-dealer and member of FINRA, accepts responsibility for the contents of reports issued by Macquarie Capital Markets Canada Ltd in the United States and sent to US persons. Any person wishing to effect transactions in the securities described in the reports issued by Macquarie Capital Markets Canada Ltd should do so with Macquarie Capital Markets North America Ltd. The Research Distribution Policy of Macquarie Capital Markets Canada Ltd is to allow all clients that are entitled to have equal access to our research. United Kingdom: In the United Kingdom, research is issued and distributed by Macquarie Capital (Europe) Ltd, which is authorised and regulated by the Financial Services Authority (No. 193905). Germany: In Germany, research is issued and distributed by Macquarie Capital (Europe) Ltd, Niederlassung Deutschland, which is authorised and regulated in the

This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

Macquarie Research Guanxi

25 April 2011 22

United Kingdom by the Financial Services Authority (No. 193905). France: In France, research is issued and distributed by Macquarie Capital (Europe) Ltd, which is authorised and regulated in the United Kingdom by the Financial Services Authority (No. 193905). Hong Kong: In Hong Kong, research is issued and distributed by Macquarie Capital Securities Ltd, which is licensed and regulated by the Securities and Futures Commission. Japan: In Japan, research is issued and distributed by Macquarie Capital Securities (Japan) Limited, a member of the Tokyo Stock Exchange, Inc. and Osaka Securities Exchange Co. Ltd (Financial Instruments Firm, Kanto Financial Bureau (kin-sho) No. 231, a member of Japan Securities Dealers Association and Financial Futures Association of Japan). India: In India, research is issued and distributed by Macquarie Capital Securities (India) Pvt Ltd. Level 3, Mafatlal Centre, Nariman Point, Mumbai 400 021, INDIA, which is a SEBI registered Stock Broker having membership with National Stock Exchange of India Limited (INB231246738) and Bombay Stock Exchange Limited (INB011246734). Malaysia: In Malaysia, research is issued and distributed by Macquarie Capital Securities (Malaysia) Sdn. Bhd. (Company registration number: 463469-W) which is a Participating Organisation of Bursa Malaysia Berhad and a holder of Capital Markets Services License issued by the Securities Commission. Taiwan: Information on securities/instruments that are traded in Taiwan is distributed by Macquarie Capital Securities Ltd, Taiwan Branch, which is licensed and regulated by the Financial Supervisory Commission. No portion of the report may be reproduced or quoted by the press or any other person without authorisation from Macquarie. Nothing in this research shall be construed as a solicitation to buy or sell any security or product. Thailand: In Thailand, research is issued and distributed by Macquarie Securities (Thailand) Ltd, a licensed securities company that is authorized by the Ministry of Finance, regulated by the Securities and Exchange Commission of Thailand and is an exchange member no. 28 of the Stock Exchange of Thailand. The Thai Institute of Directors Association has disclosed the Corporate Governance Report of Thai Listed Companies made pursuant to the policy of the Securities and Exchange Commission of Thailand. Macquarie Securities (Thailand) Ltd does not endorse the result of the Corporate Governance Report of Thai Listed Companies but this Report can be accessed at: http://www.thai-iod.com/en/publications.asp?type=4. South Korea: In South Korea, unless otherwise stated, research is prepared, issued and distributed by Macquarie Securities Korea Limited, which is regulated by the Financial Supervisory Services. Information on analysts in MSKL is disclosed at http://dis.kofia.or.kr/fs/dis2/fundMgr/DISFundMgrAnalystPop.jsp?companyCd2=A03053&pageDiv=02. South Africa: In South Africa, research is issued and distributed by Macquarie First South Securities (Pty) Limited, a member of the JSE Limited. Singapore: In Singapore, research is issued and distributed by Macquarie Capital Securities (Singapore) Pte Ltd (Company Registration Number: 198702912C), a Capital Markets Services license holder under the Securities and Futures Act to deal in securities and provide custodial services in Singapore. Pursuant to the Financial Advisers (Amendment) Regulations 2005, Macquarie Capital Securities (Singapore) Pte Ltd is exempt from complying with sections 25, 27 and 36 of the Financial Advisers Act. All Singapore-based recipients of research produced by Macquarie Capital (Europe) Limited, Macquarie Capital Markets Canada Ltd, Macquarie First South Securities (Pty) Limited and Macquarie Capital (USA) Inc. represent and warrant that they are institutional investors as defined in the Securities and Futures Act. United States: In the United States, research is issued and distributed by Macquarie Capital (USA) Inc., which is a registered broker-dealer and member of FINRA. Macquarie Capital (USA) Inc, accepts responsibility for the content of each research report prepared by one of its non-US affiliates when the research report is distributed in the United States by Macquarie Capital (USA) Inc.

Available to clients on the world wide web at www.macquarieresearch.com and through Thomson Financial, FactSet, Reuters, Bloomberg, CapitalIQ and TheMarkets.com.

This document is being provided for the exclusive use of GREGORY SIMON at MACQUARIE CAPITAL SE

Asia Research Head of Equity Research John O’Connell (Global Co – Head) (612) 8232 7544 David Rickards (Global Co – Head) (44 20) 3037 4399 Chris Hunt (Asia – Head) (852) 3922 1119 Tim Smart (Asia – Deputy Head) (852) 3922 3565

Automobiles/Auto Parts Leah Jiang (China) (8621) 2412 9020 Linda Huang (Hong Kong) (852) 3922 4068 Clive Wiggins (Japan) (813) 3512 7856 Dan Lucas (Japan) (813) 3512 6050 Michael Sohn (Korea) (82 2) 3705 8644

Banks and Non-Bank Financials Ismael Pili (Asia, Hong Kong) (852) 3922 4774 Victor Wang (China) (852) 3922 1479 Alastair Macdonald (Japan) (813) 3512 7476 Mudit Painuly (India) (9122) 6653 3044 Suresh Ganapathy (India) (9122) 6653 3042 Chan Hwang (Korea) (822) 3705 8643 Alex Pomento (Philippines) (632) 857 0899 Matthew Smith (Malaysia, Singapore) (65) 6601 0981 Jemmy Huang (Taiwan) (8862) 2734 7530 Passakorn Linmaneechote (Thailand) (662) 694 7728 Apichet Kiatworakun (Thailand) (662) 694 7724

Insurance Scott Russell (Asia) (852) 3922 3567 Chung Jun Yun (Korea) (822) 2095 7222

Media and Internet Jiong Shao (China, Hong Kong) (852) 3922 3566 Steve Zhang (China, Hong Kong) (852) 3922 3578 Prem Jearajasingam (Malaysia) (603) 2059 8989 Alex Pomento (Philippines) (632) 857 0899

Oil, Gas and Petrochemicals Linda Huang (Hong Kong) (852) 3922 4068 Jal Irani (India) (9122) 6653 3040 Polina Diyachkina (Japan) (813) 3512 7886 Shawn Park (Korea) (822) 3705 8669 Sunaina Dhanuka (Malaysia) (603) 2059 8993 Trevor Buchinski (Thailand) (662) 694 7829 Pharmaceuticals and Healthcare Jonathan Hsu (Hong Kong) (852) 3922 4625 Abhishek Singhal (India) (9122) 6653 3052 Christina Lee (Korea) (852) 3922 3571 Chinnarat Boonmahanark (Thailand) (662) 694 7985 Property Callum Bramah (Asia) (852) 3922 4731 Eva Lee (China, Hong Kong) (852) 3922 3573 Eugene Cheung (Hong Kong) (852) 3922 4627 Unmesh Sharma (India) (9122) 6653 3170 Felicia Barus (Indonesia) (6221) 2598 8480 Hiroshi Okubo (Japan) (813) 3512 7433 Chang Han Joo (Korea) (822) 3705 8511 Sunaina Dhanuka (Malaysia) (603) 2059 8993 Alex Pomento (Philippines) (632) 857 0899 Tuck Yin Soong (Singapore) (65) 6601 0838 Elaine Cheong (Singapore) (65) 6601 0839 Corinne Jian (Taiwan) (8862) 2734 7522 Patti Tomaitrichitr (Thailand) (662) 694 7727 Resources / Metals and Mining Andrew Dale (Asia) (852) 3922 3587 Graeme Train (China) (8621) 2412 9035 Carol Cao (China, Hong Kong) (852) 3922 4075 Pelen Ji (China, Hong Kong) (852) 3922 4741 Christina Lee (Hong Kong) (852) 3922 3571 Rakesh Arora (India) (9122) 6653 3054 Adam Worthington (Indonesia) (852) 3922 4626 Albert Saputro (Indonesia) (6221) 515 7340 Polina Diyachkina (Japan) (813) 3512 7886 Chak Reungsinpinya (Thailand) (662) 694 7982 Technology Jeffrey Su (Asia) (8862) 2734 7512 Stephen Chow (China, Hong Kong) (852) 3922 3634 Lisa Soh (China) (852) 3922 1401 Nitin Mohta (India) (9122) 6653 3050 Damian Thong (Japan) (813) 3512 7877 David Gibson (Japan) (813) 3512 7880 George Chang (Japan) (813) 3512 7854 Jeff Loff (Japan) (813) 3512 7851 Michiko Kakiya (Japan) (813) 3512 7868 Yukihiro Goto (Japan) (813) 3512 5984 Daniel Kim (Korea) (822) 3705 8641 Benjamin Ban (Korea) (822) 3705 8659 Andrew Chang (Taiwan) (8862) 2734 7526 Daniel Chang (Taiwan) (8862) 2734 7516 Jimmy Hsu (Taiwan) (8862) 2734 7533 Kylie Huang (Taiwan) (8862) 2734 7528 Telecoms Keith Neruda (Asia) (65) 6601 0830 Tim Smart (China) (852) 3922 3565 Lisa Soh (China, Hong Kong) (852) 3922 1401 Riaz Hyder (Indonesia) (6221) 2598 8486 Nathan Ramler (Japan) (813) 3512 7875 Prem Jearajasingam (Malaysia) (603) 2059 8989 Joseph Quinn (Taiwan) (8862) 2734 7519 Best Waiyanont (Thailand) (662) 694 7993

Transport & Infrastructure Janet Lewis (Asia, Japan) (813) 3512 7475 Chang Han Joo (Korea) (822) 3705 8511 Sunaina Dhanuka (Malaysia) (603) 2059 8993 Utilities Adam Worthington (Asia) (852) 3922 4626 Carol Cao (China, Hong Kong) (852) 3922 4075 Jeff Evans (India) (9122) 3356 3053 Ayako Mitsui Boston (Japan) (813) 3512 7885 Prem Jearajasingam (Malaysia) (603) 2059 8989 Alex Pomento (Philippines) (632) 857 0899 Commodities Jim Lennon (4420) 3037 4271 Max Layton (4420) 3037 4273 Jan Stuart (1 212) 231 2485 Duncan Hobbs (4420) 3037 4497 Bonnie Liu (8621) 2412 9008 Graeme Train (8621) 2412 9035 Rakesh Arora (9122) 6653 3054 Data Services Andrea Dailly (Asia) (852) 3922 4076 Eric Yeung (852) 3922 4077 Economics Richard Jerram (Asia, Japan) (65) 6601 0842 Philip McNicholas (ASEAN) (65) 6601 0982 Richard Gibbs (Australia) (612) 8232 3935 Paul Cavey (China) (852) 3922 3570 Renee Chen (Hong Kong, Taiwan) (852) 3922 3597 Quantitative / CPG Martin Emery (Asia) (852) 3922 3582 Viking Kwok (Asia) (852) 3922 4735 Burke Lau (Asia) (852) 3922 5494 George Platt (Australia) (612) 8232 6539 Patrick Hansen (Japan) (813) 3512 7876 Ayumu Kuroda (Japan) (813) 3512 7569 Simon Rigney (Japan) (813) 3512 7872 Strategy/Country Michael Kurtz (Asia) (852) 3922 1403 John Woods (Asia) (852) 3922 4636 Mark Matthews (Asia) (65) 6601 0841 Peter Eadon-Clarke (Asia, Japan) (813) 3512 7850 Jiong Shao (China, Hong Kong) (852) 3922 3566 Rakesh Arora (India) (9122) 6653 3054 David Gibson (Japan) (813) 3512 7880 Chan Hwang (Korea) (822) 3705 8643 Kieran Calder (Malaysia) (603) 2059 8992 Yeonzon Yeow (Malaysia) (603) 2059 8982 Alex Pomento (Philippines) (632) 857 0899 Daniel Chang (Taiwan) (8862) 2734 7516 David Gambrill (Thailand) (662) 694 7753 Find our research at Macquarie: www.macquarie.com.au/research Thomson: www.thomson.com/financial Reuters: www.knowledge.reuters.com Bloomberg: MAC GO Factset: http://www.factset.com/home.aspx CapitalIQ www.capitaliq.com TheMarkets.com www.themarkets.com Email [email protected] for access

Asia Sales Regional Heads of Sales Robin Black (Asia) (852) 3922 2074 Chris Gray (ASEAN) (65) 6601 0288 Peter Slater (Boston) (1 617) 598 2502 Jeffrey Shiu (China & Hong Kong) (852) 3922 2061 Thomas Renz (Geneva) (41) 22 818 7712 Andrew Mouat (India) (9122) 6653 3200 Kenneth Yap (Indonesia) (6221) 515 1555 JJ Kim (Korea) (822) 3705 8799 Jason Lee (Malaysia) (603) 2059 8888 Chris Gould (Malaysia) (603) 2059 8888 Gino C Rojas (Philippines) (632) 857 0761 Greg Norton-Kidd (New York) (1 212) 231 2527 Luke Sullivan (New York) (1 212) 231 2507 Eric Roles (New York) (1 212) 231 2559 Sheila Schroeder (San Francisco) (1 415) 762 5001