26

briefing 27 April 2017

briefing27 April 2017

C

Contents

The Domestic EconomyBox A: The Opportunities for E-commerce in the Retail Sector

The Labour Market and InflationBox B: An Empirical Analysis of Food Price Pass-through in Singapore

The International Economy

Macroeconomic PoliciesBox C: The Currency Interchangeability Agreement: Fifty Years On

B

Ch

apte

rs

1

2

Optimal Control in the Monetary Model of SingaporeA

The Role of Exchange Rates in International Price Adjustment

Using Cost-Benefit Analysis in Developed and Developing Countries: Is it the Same?

Spe

cial

Feat

ure

s

3

4

RESTRICTED

International Economy

Some Improvement In Global Growth

Global GDP Growth

2017F 2018F

Total* 4.0 4.0G3* 1.8 1.7

US 2.2 2.4Japan 1.3 1.0Eurozone 1.7 1.5

NEA-3* 2.2 2.2Hong Kong 2.1 2.1Korea 2.5 2.5Taiwan 2.0 2.0

ASEAN-4* 4.7 4.7Indonesia 5.2 5.4Malaysia 4.4 4.4Philippines 6.4 6.3Thailand 3.3 3.3

China 6.5 6.2India** 7.3 7.6

GDP Growth Forecasts (%)

Global growth has regained some traction.

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2014 2015 2016

Pe

r C

en

t

YOY

QOQ SAAR

Q4

Source: CEIC, Consensus Economics, Apr 2017 and EPG, MAS estimates

* Weighted by shares in Singapore’s NODX.

** Figures are reported on a Financial Year basis; FY2017 refers to the period from April 2017 to March 2018.

In the G3, activity has strengthened amid improving sentiment, despite rising policy uncertainty.

Global Economic Policy Uncertainty and OECD Business Confidence

Global Manufacturing PMI andOECD Leading Indicator

99.6

99.8

100.0

100.2

100.4

100.6

49

50

51

52

53

54

2014 Jul 2015 Jul 2016 Jul 2017

Ind

ex (

Am

plit

ud

e A

dju

ste

d),

SA

Ind

ex, >

50

=Exp

ansi

on

Mar

OECD Leading Indicator (RHS)

50

100

150

200

250

300

350

96

97

98

99

100

101

102

2008 2010 2012 2014

Ind

ex (

3M

MA

)

Ind

ex

2016 2017Mar

OECD Business Confidence

Global Economic Policy Uncertainty Index (RHS)

Global Manufacturing

PMI

External demand re-emerges as a growth driver in Asia

Contribution to Growth of NEA-3 and ASEAN-4 Imports by Product Category

Contribution to Growth inAsia-8 Total Demand

2015 Q2 Q3 Q4 2016 Q2 Q3 Q4

-2

0

2

4

6

% P

oin

t C

on

trib

uti

on

to

YO

Y G

row

th

External Demand

Gross Capital Formation

Govt Consumption

Private Consumption

2012 2013 2014 2015 2016

-15

-10

-5

0

5

10

% P

oin

t C

on

trib

uti

on

to

YO

Y G

row

th

Consumption Goods Intermediate Goods

Capital Goods Total Imports

Q4

RESTRICTED

Domestic Economy

Cyclical Impulses And Structural Trends

Domestic economic growth has seen some improvement.

EPG’s Economic Activity Index

2014 Q3 2015 Q3 2016 Q3 2017

96

98

100

102

104

106

Ind

ex (

20

14

=10

0),

SA

Q1

Trade-related

Domestic-oriented

Overall

Modern Services

Singapore’s GDP Growth

2014 Q3 2015 Q3 2016 Q3 2017

-6

-3

0

3

6

9

12

15

Pe

r C

en

t

YOY

QOQ SAAR

Q1** Advance Estimates

Going forward, the cyclical uplift in the electronics sector will be a key support of demand.

Domestic vs Trade-oriented Growth in Singapore

2015 Q2 Q3 Q4 2016 Q2 Q3 Q4

-4

0

4

8

12

16

% P

oin

t C

on

trib

uti

on

to

QO

Q S

AA

R G

row

th

Trade-related Domestic-oriented

Modern Services Others

Global Chip Sales by Region

2013 2014 2015 2016 2017

-20

-10

0

10

20

30

YOY

% G

row

th

Feb

Asia Pacific

Worldwide

G3

Singapore’s role in the global IT chain has evolved, alongside a dynamic export basket.

Electronics IIP and DX

2012 2013 2014 2015 2016 2017

70

80

90

100

110

120

130

140

Ind

ex (

20

12

=10

0),

SA

, 3M

MA

Mar

Electronics IIP

Rank Correlations of theTop 20 Exports

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

Co

rre

lati

on

Global Average =

0.29

Advanced Economies

Small, Open Economies

Regional Economies

Electronics DX

Box A: The Opportunities for E-commerce in the Retail Sector

Share of Country’s Consumer Goods Imports Supplied by Singapore

Korea

Other Asia, nes

India

Hong Kong

China

Vietnam

Indonesia

Philippines

Malaysia

Cambodia

Thailand

0 2 4 6 8

Per Cent

0

20

40

60

80

100

0 5 10 15 20 25

Inte

rnet

Pe

net

rati

on

(%

)

Ave. Growth in Consumer Goods Imports 2011–15 (%)

Philippines

Korea

Hong Kong

Malaysia

Thailand

Indonesia India

Cambodia

Vietnam

China

Market Potential: Growth in Consumer Goods Imports & Internet Penetration Rates

RESTRICTED

Labour Market and Inflation

Demand-side Inflationary Pressures Remain Muted

Activity in the labour market has remained soft.

Overall Employment Changes

H1 H2 H1 H2 H1 H2 H1 H2

-40

-20

0

20

40

60

80

Tho

usa

nd

Manufacturing Construction

Services Total

2013 2014 2015 2016

Labour Market Indicators

60

80

100

120

2013–15 Average H1 2016 H2 2016

Overall Recruitment Rate

Overall Unemployment Rate

Resident Unemployment

Rate

Overall Vacancies

Vacancy to Unemployed Persons Ratio

Overall Resignation

Rate

Inflation continued to trend up amid a pickup in the prices of oil-related items.

CPI-All Items and MAS Core Inflation

2007 2009 2011 2013 2015 2017Q1

-2

0

2

4

6

8

% Y

OY

CPI-All Items Inflation

MAS Core Inflation

Contribution to CPI-All Items Inflation

2015 Q2 Q3 Q4 2016 Q2 Q3 Q4 2017

-2

-1

0

1

2

% P

oin

t C

on

trib

uti

on

to

YO

Y I

nfl

atio

n

Services FoodPte Rd Trpt ex Petrol Oil-relatedOthers Accommodation

Q1

CPI-All Items Inflation

Imported food prices have risen but the pass-through to consumer food prices is more gradual

Components of Food Inflation for Consumers

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2016 Apr Jul Oct 2017

% Y

OY

Mar

Restaurant Food

Hawker Food

Fast Food

Non-cooked Food

Contribution to Imported Food Inflation

2016 Q2 Q3 Q4 2017

-6

-4

-2

0

2

4

Live Animals Meat & Meat PrepDairy & Eggs Fish & SeafoodCereal & Cereal Prep Veg & FruitSugar & Sugar Prep Coffee, Cocoa & SpicesAnimal Feed Misc Food

Jan–Feb

Overall Food & Live Animals

% P

oin

t C

on

trib

uti

on

to

YO

Y I

nfl

atio

n

Muted price pressures from discretionary services and retail goods.

Contribution toOverall Services Inflation

2015 Q3 2016 Q3 2017

-0.5

0.0

0.5

1.0

1.5

2.0

% P

oin

t C

on

trib

uti

on

to

YO

Y In

flat

ion

Essential Discretionary

Overall Services

Q1

Price Change forSelected Retail CPI Components

-2 0 2 4 6 8% YOY

Q4 2016

Q1 2017

Newspapers, Books & Stationery

Personal Effects

Alcoholic Drinks & Tobacco

Sch. Txtbooks & Study Guides

Med. Products, Appliances & Eqpt

Household Durables

Clothing & Footwear

Administrative price hikes could increase business costs but the pass-through to consumers is likely to be modest

CPI-All Items and MAS Core Inflation

2007 2009 2011 2013 2015 2017

-2

0

2

4

6

8

% Y

OY

CPI-All Items Inflation

MAS Core Inflation

Q4

Forecast

Contribution to CPI-All Items Inflation

2016 Q2 Q3 Q4 2017 Q2 Q3 Q4

-2

-1

0

1

2

% P

oin

t C

on

trib

uti

on

to

YO

Y In

flat

ion

ServicesFoodPte Rd Trpt ex PetrolOil-relatedOthersAccommodation

Forecast

RESTRICTED

Macroeconomic Policy

Keeping the Economy on an Even Keel

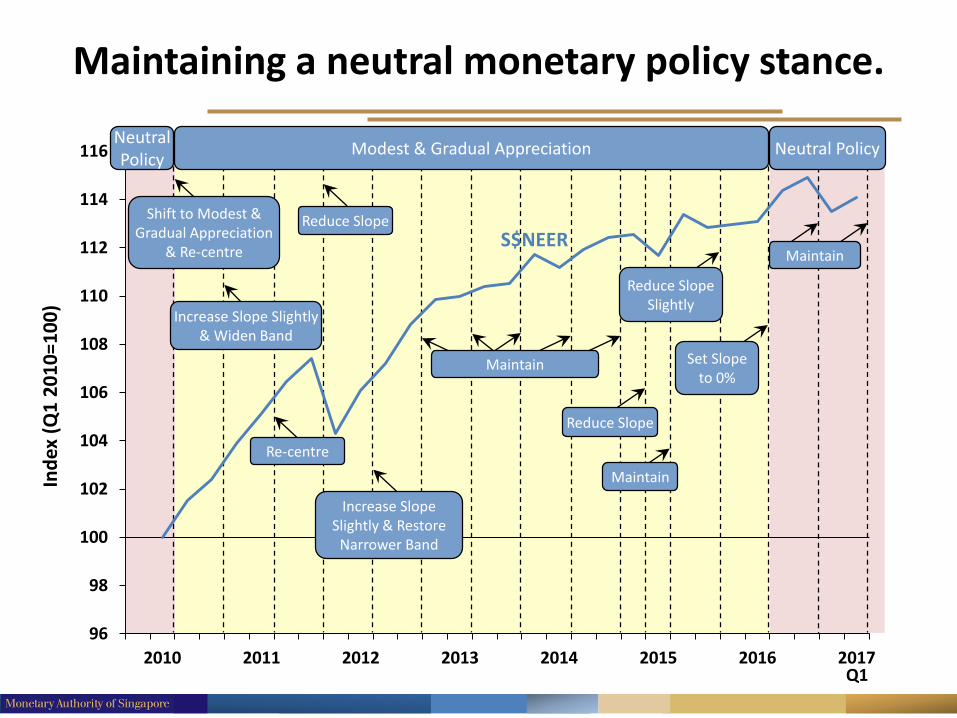

Maintaining a neutral monetary policy stance.

Q12010 2011 2012 2013 2014 2015 2016 2017

96

98

100

102

104

106

108

110

112

114

116

Ind

ex (

Q1

20

10

=10

0)

S$NEER

Neutral Policy

Increase Slope Slightly & Widen Band

Shift to Modest & Gradual Appreciation

& Re-centre

Re-centre

Reduce Slope

Increase Slope Slightly & Restore

Narrower Band

Maintain

Reduce Slope

Maintain

Modest & Gradual Appreciation

Set Slope to 0%

Reduce Slope Slightly

Maintain

Neutral Policy

The Currency Interchangeability Agreement: Fifty Years On

Box C

• AMBD and MAS collaborated on Box C to commemorate the 50th anniversary of the Currency Interchangeability Agreement. The Agreement came into force on 12 June 1967, when Brunei and Singapore began issuing their own currencies. Under the Agreement, both countries undertook to accept each other’s currency and to exchange it at par, without charge, into its own currency.

• This article highlights how the long history of exchange rate cooperation between Brunei and Singapore, which dates back to the 19th Century, laid the foundation for the Agreement in 1967. It also highlights how the Agreement has remained intact in the five decades since, as it has been compatible with macroeconomic stability in both countries and has helped to deepen economic and financial linkages between Singapore and Brunei.

Q&A

27 April 2017

RESTRICTED

Special Features

Optimal Control in the Monetary Model of Singapore

Special Feature A

• Special Feature A is an exposition of the optimal control facility that was recently added to the Monetary Model of Singapore (MMS), as part of EPG’s ongoing efforts to enhance its quantitative economic toolkit. This approach entails solving the model for the path of the policy instrument that would achieve macroeconomic stability.

• After describing how the optimal control policy is related to the literature on central bank loss functions, it is applied in a retrospective historical setting and the results are compared with actual outcomes.

• This exercise demonstrates both the usefulness and limitations of the optimal control approach. Specifically, the results are contingent on the set of macroeconomic forecasts and do not take into account uncertainty.

The Role of Exchange Rates In International Price Adjustment

Special Feature B

• In September 2010, Guido Mantega, the Brazilian finance minister, commented that “we are in the middle of a currency war”. In February 2017, US President Donald Trump called China “the grand champions at manipulation of currency.”

• Policymakers believe that a change in the exchange rate affects a country’s competitiveness, while academic studies typically assume that international prices are determined independently of nominal exchange rates.

• Professor Engel argues that nominal exchange rates do play a role in determining international prices and international competitiveness. Nonetheless, there is also a role for price adjustment, so competitiveness is by no means determined only by the value of the currency.

Prof Charles EngelDepartment of Economics,

University of Wisconsin,

USA

Using Cost-Benefit Analysis In Developed And Developing Countries: Is It The Same?

Special Feature C

• Properly accounting for the full costs of growththrough GDP and other indicators of nationalincome may prove too costly for developingcountries. Often, developing nations account forthese costs by carrying out cost-benefit analysis(CBA) on public projects.

• In this Special Feature, Professor Quah discusses thesimilarities and differences in the application of CBAin developed and developing countries. Thesedifferences arise from the operation of goods,labour and financial markets, as well as behavioursthat affect experimental design and results.

• Consequently, several issues and pitfalls relating toinvestment decision criteria, valuation techniques,and distributional considerations need to be bornein mind. CBA should only be used as a guide, andnot as the final or only arbiter of project proposals.

Prof Euston QuahDepartment of Economics,

Nanyang Technological

University, Singapore

Q&A

27 April 2017