92

Macroeconomics I E_EBE1_MACEC Prof. dr. Eric Bartelsman 26 & 27 februari 2018

Macroeconomics IE_EBE1_MACEC

Prof. dr. Eric Bartelsman26 & 27 februari 2018

Overview

• Introduction to Business Cycles– Aggregate Demand and Aggregate Supply

• Aggregate Demand Curve– Keynesian Cross– Money Demand and Money Supply– IS-LM model

• Aggregate Supply• Stabilization Policy

The model of aggregate demand and supply

• the paradigm most mainstream economists and policymakers use to think about economic fluctuations and policies to stabilize the economy

• shows how the price level and aggregate output are determined

• shows how the economy’s behavior is different in the short run and long run

Income = Expenditures (slide from Economic Challenges, week 3 Macro)

Tesla’s, Y

Arbeidsuren, L

P*Y

w*L

Aggregate demand

• The aggregate demand curve shows the relationship between the price level and the quantity of output demanded.

• For this chapter’s intro to the AD/AS model, we use a simple theory of aggregate demand based on the quantity theory of money.

• Chapters 11-13 develop the theory of aggregate demand in more detail.

The Quantity Equation as Aggregate Demand

• From Chapter 4, recall the quantity equationM V = P Y

• For given values of M and V, this equation implies an inverse relationship between P and Y :

The downward-sloping AD curve

An increase in the price level causes a fall in real money balances (M/P),causing a decrease in the demand for goods & services.

Y

P

AD

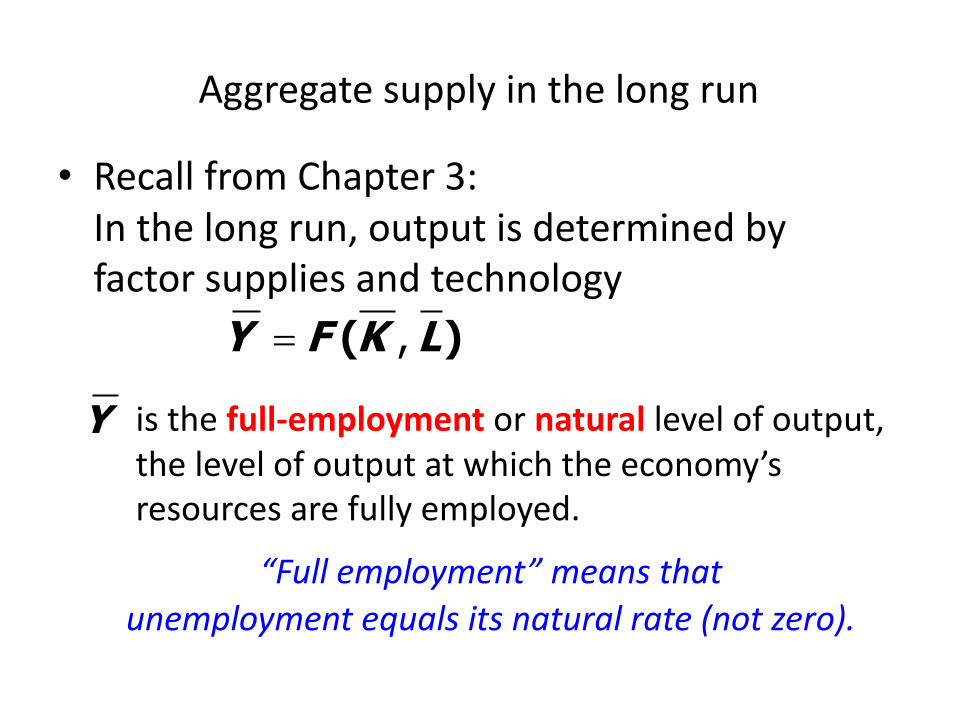

Aggregate supply in the long run

• Recall from Chapter 3: In the long run, output is determined by factor supplies and technology

,= ( )Y F K Lis the full-employment or natural level of output, the level of output at which the economy’s resources are fully employed.

Y

“Full employment” means that unemployment equals its natural rate (not zero).

The long-run aggregate supply curve

Y

P LRASdoes not

depend on P, so LRAS is vertical.

Y

( )= ,YF K L

Long-run effects of an increase in M

Y

P

AD1

LRAS

Y

An increase in M shifts AD to the right.

P1

P2In the long run, this raises the price level…

…but leaves output the same.

AD2

Aggregate supply in the short run

• Many prices are sticky in the short run. • For now (and through Chap. 13), we assume – all prices are stuck at a predetermined level in the

short run.– firms are willing to sell as much at that price level

as their customers are willing to buy. • Therefore, the short-run aggregate supply

(SRAS) curve is horizontal:

The short-run aggregate supply curve

Y

P

P SRAS

The SRAS curve is horizontal:The price level is fixed at a predetermined level, and firms sell as much as buyers demand.

Short-run effects of an increase in M

Y

P

AD1

In the short run when prices are sticky,…

…causes output to rise.

P SRAS

Y2Y1

AD2

…an increase in aggregate demand…

From the short run to the long run

Over time, prices gradually become “unstuck.” When they do, will they rise or fall?

Y Y>Y Y<Y Y=

rise

fall

remain constant

In the short-run equilibrium, if

then over time, P will…

The adjustment of prices is what moves the economy to its long-run equilibrium.

The SR & LR effects of DM > 0

Y

P

AD1

LRAS

Y

P SRASP2

Y2

A = initial equilibrium

AB

CB = new short-run

eq’m after Fed increases M

C = long-run equilibrium

AD2

Monetary Policy in a Recession

Y

P

AD1

LRAS

Y

P SRAS

Pn

Y1

A = initial recession

A

B

C

B = long-run equilibrium without monetary policy

C =eq’m after CB increases M

AD2

Overview

• Introduction to Business Cycles– Aggregate Demand and Aggregate Supply

• Aggregate Demand Curve– Keynesian Cross– Money Demand and Money Supply– IS-LM model

• Aggregate Supply• Stabilization Policy

The Keynesian Cross• A simple closed economy model in which income is

determined by expenditure. (due to J.M. Keynes)

• Notation: I = planned investmentE = C + I + G = planned expenditureY = real GDP = actual expenditure

• Difference between actual & planned expenditure = unplanned inventory investment

Elements of the Keynesian Cross( )C C Y T= -

I I=

,G G T T= =

( )E C Y T I G= - + +

=Y E

consumption function:

for now, plannedinvestment is exogenous:

planned expenditure:

equilibrium condition:

govt policy variables:

actual expenditure = planned expenditure

Graphing planned expenditure

income, output, Y

Eplanned

expenditureE =C +I +G

MPC1

Graphing the equilibrium condition

income, output, Y

Eplannedexpenditure

E =Y

45º

The equilibrium value of income

income, output, Y

Eplanned

expenditureE =Y

E =C +I +G

Equilibrium income

An increase in government purchases

Y

EE =Y

E =C +I +G1

E1 = Y1

E =C +I +G2

E2 = Y2DY

At Y1, there is now an unplanned drop in inventory…

…so firms increase output, and income rises toward a new equilibrium.

DG

Solving for DYY C I G= + +

Y C I GD = D + D + D

MPC= ´ D + DY GC G= D + D

(1 MPC)- ´D = DY G1

1 MPCæ ö

D = ´ Dç ÷-è øY G

equilibrium condition

in changes

because I exogenous

because DC =MPCDY

Collect terms with DY on the left side of the equals sign:

Solve for DY :

The government purchases multiplier

Example: If MPC = 0.8, then

Definition: the increase in income resulting from a $1 increase in G.In this model, the govt purchases multiplier equals 1

1 MPCD

=D -YG

1 51 0.8

D= =

D -YG

An increase in G causes income to increase 5 times

as much!

Why the multiplier is greater than 1

• Initially, the increase in G causes an equal increase in Y:DY = DG.

• But Y ÞCÞ further YÞ further CÞ further Y

• So the final impact on income is much bigger than the initial DG.

The IS curvedef: a graph of all combinations of r and Y that result in goods market equilibriumi.e. actual expenditure (output)

= planned expenditure

The equation for the IS curve is:

Y2Y1

Y2Y1

Deriving the IS curve

¯r Þ I

Y

E

r

Y

E =C +I (r1 )+GE =C +I (r2 )+G

r1

r2

E =Y

IS

DIÞ E

Þ Y

Why the IS curve is negatively sloped

• A fall in the interest rate motivates firms to increase investment spending, which drives up total planned spending (E).

• To restore equilibrium in the goods market, output (a.k.a. actual expenditure, Y) must increase.

The IS curve and the loanable funds model

S, I

r

I (r )r1

r2

r

YY1

r1

r2

(a) The L.F. model (b) The IS curve

Y2

S1S2

IS

Fiscal Policy and the IS curve

• We can use the IS-LM model to see how fiscal policy (G and T) affects aggregate demand and output.

• Let’s start by using the Keynesian cross to see how fiscal policy shifts the IS curve…

Y2Y1

Y2Y1

Shifting the IS curve: DG

At any value of r, GÞE ÞY

Y

E

r

Y

E =C +I (r1 )+G1

E =C +I (r1 )+G2

r1

E =Y

IS1

The horizontal distance of the IS shift equals

IS2

…so the IS curve shifts to the right.

11 MPC

D = D-

Y G DY

The Theory of Liquidity Preference

• Due to John Maynard Keynes.• A simple theory in which the interest rate

is determined by money supply and money demand.

Money supply

The supply of real money balances is fixed:

The picture can't be displayed.

M/Preal money

balances

rinterest

rate

The picture can't be displayed.

M P

Money demand

Demand forreal money balances:

M/Preal money

balances

rinterest

rate( )sM P

M P

L (r )

Equilibrium

The interest rate adjusts to equate the supply and demand for money:

M/Preal money

balances

rinterest

rate( )sM P

M P

( )M P L r= L (r )r1

How the CB raises the interest rate

To increase r, CB reduces M

M/Preal money

balances

rinterest

rate

1MP

L (r )r1

r2

2MP

The LM curve

Now let’s put Y back into the money demand function:

The LM curve is a graph of all combinations of r and Y that equate the supply and demand for real money balances.The equation for the LM curve is:

Deriving the LM curve

M/P

r

1MP

L (r ,Y1 )r1

r2

r

YY1

r1L (r ,Y2 )

r2

Y2

LM

(a) The market for real money balances (b) The LM curve

Why the LM curve is upward sloping

• An increase in income raises money demand. • Since the supply of real balances is fixed, there

is now excess demand in the money market at the initial interest rate.

• The interest rate must rise to restore equilibrium in the money market.

How DM shifts the LM curve

M/P

r

1MP

L (r ,Y1 )r1

r2

r

YY1

r1

r2

LM1

(a) The market for real money balances (b) The LM curve

2MP

LM2

The short-run equilibrium

The short-run equilibrium is the combination of r and Y that simultaneously satisfies the equilibrium conditions in the goods & money markets:

Y

r

IS

LM

Equilibriuminterestrate

Equilibriumlevel ofincome

The Big PictureKeynesianCross

Theory of Liquidity Preference

IScurve

LMcurve

IS-LMmodel

Agg. demand

curve

Agg. supplycurve

Model of Agg.

Demand and Agg. Supply

Explanation of short-run fluctuations

Chapter Summary1. Keynesian cross

– basic model of income determination– takes fiscal policy & investment as exogenous– fiscal policy has a multiplier effect on income.

2. IS curve– comes from Keynesian cross when planned investment

depends negatively on interest rate– shows all combinations of r and Y

that equate planned expenditure with actual expenditure on goods & services

slide 44

Chapter Summary3. Theory of Liquidity Preference

– basic model of interest rate determination– takes money supply & price level as exogenous– an increase in the money supply lowers the interest rate

4. LM curve– comes from liquidity preference theory when

money demand depends positively on income– shows all combinations of r and Y that equate demand

for real money balances with supply

slide 45

Chapter Summary5. IS-LM model

– Intersection of IS and LM curves shows the unique point (Y, r ) that satisfies equilibrium in both the goods and money markets.

slide 46

Macroeconomics IE_EBE1_MACEC

Prof. dr. Eric Bartelsman27 februari 2018

The intersection determines the unique combination of Y and rthat satisfies equilibrium in both markets.

The LM curve represents money market equilibrium.

Equilibrium in the IS-LM model

The IS curve represents equilibrium in the goods market.

ISY

rLM

r1

Y1

Exercise: Shifting the IS curve

• Use the diagram of the Keynesian cross or loanable funds model to show how an increase in taxes shifts the IS curve.

Instant Poll

• An increase in taxes:– A. Shifts the IS curve to the left, by less than the

amount of a similar decrease in G– B. Shifts the IS curve to the right, by less than the

amount of a similar decrease in G– C. Shifts the IS curve to the left, by more than the

amount of a similar decrease in G– D. Shifts the IS curve to the right, by more than

the amount of a similar decrease in G

An increase in taxes

Y

EE =Y

E =C2 +I +G

E2 = Y2

E =C1 +I +G

E1 = Y1DY

At Y1, there is now an unplanned inventory buildup……so firms reduce

output, and income falls toward a new equilibrium

DC = -MPC DT

Initially, the tax increase reduces consumption, and therefore E:

Solving for DYY C I GD = D + D + D

( )MPC= ´ D - DY T

C= D

(1 MPC) MPC- ´D = - ´ DY T

eq’m condition in changes

I and G exogenous

Solving for DY :

MPC1 MPCæ ö-

D = ´ Dç ÷-è øY TFinal result:

The tax multiplierdef: the change in income resulting from a $1 increase in T :

MPC1 MPC

D -=

D -YT

0.8 0.8 41 0.8 0.2

D - -= = = -

D -YT

If MPC = 0.8, then the tax multiplier equals

IS11.

…Now a tax cut

Y

rLM

r1

Y1

IS2

Y2

r2

Consumers save (1-MPC) of the tax cut, so the initial boost in spending is smaller for DT than for an equal DG… and the IS curve shifts by

MPC1 MPC

T-D

-1.

2.

2.…so the effects on rand Y are smaller for DTthan for an equal DG.

2.

Policy analysis with the IS-LM model

We can use the IS-LM model to analyze the effects of• fiscal policy: G and/or T• monetary policy: M IS

Y

rLM

r1

Y1

causing output & income to rise.

IS1

An increase in government purchases

1. IS curve shifts right

Y

rLM

r1

Y1

1by 1 MPC

GD-

IS2

Y2

r2

1.2. This raises money demand, causing the interest rate to rise…

2.

3. …which reduces investment, so the final increase in Y

1is smaller than 1 MPC

GD-

3.

Exercise: Shifting the LM curve

• Suppose a wave of credit card fraud causes consumers to use cash more frequently in transactions.

• Use the liquidity preference model to show how these events shift the LM curve.

Instant Poll

• Using IS-LM, the increase in preference for cash results in a new equilibrium with:– A. higher r, higher Y– B. higher r, lower Y– C. lower r, higher Y– D. lower r, lower Y

2. …causing the interest rate to fall

IS

Monetary policy: An increase in M

1. DM > 0 shifts the LM curve down(or to the right)

Y

r LM1

r1

Y1 Y2

r2

LM2

3. …which increases investment, causing output & income to rise.

Interaction between monetary & fiscal policy

• Model: Monetary & fiscal policy variables (M, G, and T) are exogenous.

• Real world: Monetary policymakers may adjust Min response to changes in fiscal policy, or vice versa.

• Such interaction may alter the impact of the original policy change.

The Central Bank response to DG > 0

• Suppose Gov’t increases G.• Possible CB responses:

1. hold M constant2. hold r constant3. hold Y constant

• In each case, the effects of the DGare different:

If Gov’t raises G, the IS curve shifts right.

IS1

Response 1: Hold M constant

Y

rLM1

r1

Y1

IS2

Y2

r2If CB holds M constant, then LM curve doesn’t shift.

Results:

2 1Y Y YD = -

2 1r r rD = -

If Gov’t raises G, the IS curve shifts right.

IS1

Response 2: Hold r constant

Y

rLM1

r1

Y1

IS2

Y2

r2To keep r constant, CB increases Mto shift LM curve right.

3 1Y Y YD = -

0rD =

LM2

Y3

Results:

IS1

Response 3: Hold Y constant

Y

rLM1

r1IS2

Y2

r2To keep Y constant, CB reduces Mto shift LM curve left.

0YD =

3 1r r rD = -

LM2

Results:

Y1

r3

If Gov’t raises G, the IS curve shifts right.

Estimates of fiscal policy multipliersfrom the US-DRI macroeconometric model

Assumption about monetary policy

Estimated value of DY/DG

Fed holds nominal interest rate constant

Fed holds money supply constant

1.93

0.60

Estimated value of DY/DT

-1.19

-0.26

Shocks in the IS-LM modelIS shocks: exogenous changes in the demand for goods & services.

Examples: – stock market boom or crash

Þ change in households’ wealthÞDC

– change in business or consumer confidence or expectations ÞDI and/or DC

Shocks in the IS-LM model

LM shocks: exogenous changes in the demand for money.

Examples:– Worry about safety of Banks increases demand

for money.– more ATMs or the Internet reduce money

demand.

EXERCISE:Analyze shocks with the IS-LM model

Use the IS-LM model to analyze the effects of1. a boom in the stock market that makes consumers

wealthier.2. after a bursting housing bubble, and fear of

banking crisis, people want more cash.

For each shock, a. use the IS-LM diagram to show the effects of the

shock on Y and r.b. determine what happens to C, I, and the

unemployment rate.

Instant Poll

• Using IS-LM, a boom in the stock market results in a new equilibrium with:– A. higher r, higher Y– B. higher r, lower Y– C. lower r, higher Y– D. lower r, lower Y

Instant Poll

• In the new equilibrium following the boom in the stock market:– A. C is higher, I is lower– B. C is higher, I is higher– C. C is lower, I is lower– D. C is lower, I is higher

EXERCISE:Analyze shocks with the IS-LM model

Use the IS-LM model to analyze the effects of1. a boom in the stock market that makes consumers

wealthier.2. after a bursting housing bubble, and fear of

banking crisis, people want more cash.

For each shock, a. use the IS-LM diagram to show the effects of the

shock on Y and r.b. determine what happens to C, I, and the

unemployment rate.

IS-LM and aggregate demand• So far, we’ve been using the IS-LM model

to analyze the short run, when the price level is assumed fixed.

• However, a change in P would shift LM and therefore affect Y.

• The aggregate demand curve(introduced in Chap. 10) captures this relationship between P and Y.

Y1Y2

Deriving the AD curve

Y

r

Y

P

IS

LM(P1)LM(P2)

AD

P1

P2

Y2 Y1

r2r1

Intuition for slope of AD curve:

P Þ¯(M/P)

Þ LM shifts left

Þr

ޯIޯY

Monetary policy and the AD curve

Y

P

IS

LM(M2/P1)LM(M1/P1)

AD1

P1

Y1

Y1

Y2

Y2

r1r2

The CB can increase aggregate demand:

M Þ LM shifts right

AD2

Y

r

Þ¯r

ÞIÞY at each

value of P

Y2

Y2

r2

Y1

Y1

r1

Fiscal policy and the AD curve

Y

r

Y

P

IS1

LM

AD1

P1

Expansionary fiscal policy (G and/or ¯T) increases agg. demand:

¯T ÞC

Þ IS shifts right

ÞY at each value of P

AD2

IS2

IS-LM and AD-AS in the short run & long run

Recall from Chapter 10: The force that moves the economy from the short run to the long run is the gradual adjustment of prices.

Y Y>Y Y<Y Y=

rise

fall

remain constant

In the short-run equilibrium, if

then over time, the price level will

The SR and LR effects of an IS shock

A negative IS shock shifts IS and AD left, causing Y to fall.

Y

r

Y

P LRAS

Y

LRAS

Y

IS1

SRAS1P1

LM(P1)

IS2

AD2AD1

The SR and LR effects of an IS shock

Y

r

Y

P LRAS

Y

LRAS

Y

IS1

SRAS1P1

LM(P1)

IS2

AD2AD1

In the new short-run equilibrium, Y Y<

The SR and LR effects of an IS shock

Y

r

Y

P LRAS

Y

LRAS

Y

IS1

SRAS1P1

LM(P1)

IS2

AD2AD1

In the new short-run equilibrium, Y Y<

Over time, P gradually falls, which causes•SRAS to move down.•M/P to increase, which

causes LMto move down.

AD2

The SR and LR effects of an IS shock

Y

r

Y

P LRAS

Y

LRAS

Y

IS1

SRAS1P1

LM(P1)

IS2

AD1

SRAS2P2

LM(P2)

Over time, P gradually falls, which causes•SRAS to move down.•M/P to increase, which

causes LMto move down.

AD2

SRAS2P2

LM(P2)

The SR and LR effects of an IS shock

Y

r

Y

P LRAS

Y

LRAS

Y

IS1

SRAS1P1

LM(P1)

IS2

AD1

This process continues until economy reaches a long-run equilibrium with

Y Y=

EXERCISE:Analyze SR & LR effects of DM

a. Draw the IS-LM and AD-ASdiagrams as shown here.

b. Suppose the CB increases M.Show the short-run effects on your graphs.

c. Show what happens in the transition from the short run to the long run.

d. How do the new long-run equilibrium values of the endogenous variables compare to their initial values?

Y

r

Y

P LRAS

Y

LRAS

Y

IS

SRAS1P1

LM(M1/P1)

AD1

The Great Depression

Unemployment (right scale)

Real GNP(left scale)

120

140

160

180

200

220

240

1929 1931 1933 1935 1937 1939

billi

ons o

f 195

8 do

llars

0

5

10

15

20

25

30

perc

ent o

f lab

or fo

rce

THE SPENDING HYPOTHESIS:

Shocks to the IS curve

• asserts that the Depression was largely due to

an exogenous fall in the demand for goods &

services – a leftward shift of the IS curve.

• evidence:

output and interest rates both fell, which is

what a leftward IS shift would cause.

THE SPENDING HYPOTHESIS:

Reasons for the IS shift• Stock market crash Þ exogenous ¯C– Oct-Dec 1929: S&P 500 fell 17%– Oct 1929-Dec 1933: S&P 500 fell 71%

• Drop in investment– “correction” after overbuilding in the 1920s– widespread bank failures made it harder to obtain

financing for investment• Contractionary fiscal policy– Politicians raised tax rates and cut spending to combat

increasing deficits.

THE MONEY HYPOTHESIS:

A shock to the LM curve• asserts that the Depression was largely due to

huge fall in the money supply.• evidence: M1 fell 25% during 1929-33.

• But, two problems with this hypothesis:– P fell even more, so M/P actually rose slightly

during 1929-31. – nominal interest rates fell, which is the opposite of

what a leftward LM shift would cause.

THE MONEY HYPOTHESIS AGAIN:

The effects of falling prices

• asserts that the severity of the Depression was

due to a huge deflation:

P fell 25% during 1929-33.

• This deflation was probably caused by the fall

in M, so perhaps money played an important

role after all.

• In what ways does a deflation affect the

economy?

THE MONEY HYPOTHESIS AGAIN:

The effects of falling prices• The stabilizing effects of deflation:• ¯P Þ(M/P) Þ LM shifts right ÞY• Pigou effect:

¯P Þ(M/P) Þ consumers’ wealth Þ C Þ IS shifts right ÞY

THE MONEY HYPOTHESIS AGAIN:

The effects of falling prices

• The destabilizing effects of expected deflation:

¯pe

Þ r for each value of iÞ I ¯ because I = I(r )

Þ planned expenditure & agg. demand ¯Þ income & output ¯

THE MONEY HYPOTHESIS AGAIN:

The effects of falling prices• The destabilizing effects of unexpected deflation:

debt-deflation theory¯P (if unexpected)

Þ transfers purchasing power from borrowers to lenders

Þ borrowers spend less, lenders spend more

Þ if borrowers’ propensity to spend is larger than lenders’, then aggregate spending falls, the IS curve shifts left, and Y falls

Chapter Summary1. IS-LM model

– a theory of aggregate demand– exogenous: M, G, T,

P exogenous in short run, Y in long run – endogenous: r,

Y endogenous in short run, P in long run – IS curve: goods market equilibrium– LM curve: money market equilibrium

slide 91

Chapter Summary2. AD curve– shows relation between P and the IS-LM model’s

equilibrium Y. – negative slope because P Þ¯(M/P ) Þr Þ¯I Þ¯Y

– expansionary fiscal policy shifts IS curve right, raises income, and shifts AD curve right.

– expansionary monetary policy shifts LM curve right, raises income, and shifts AD curve right.

– IS or LM shocks shift the AD curve.

slide 92