68

MACROECONOMICS II INVESTMENT DEMAND (SPENDING) II 1 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

MACROECONOMICS II

INVESTMENT DEMAND

(SPENDING) II

1 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

From the Desired Capital Stock to Investment

• Remember that, there are two opposing

channels through which the capital stock

changes over time!

• Gross Investment refers to the total

purchase or construction of new capital

goods over each period of time, say a year.

2 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

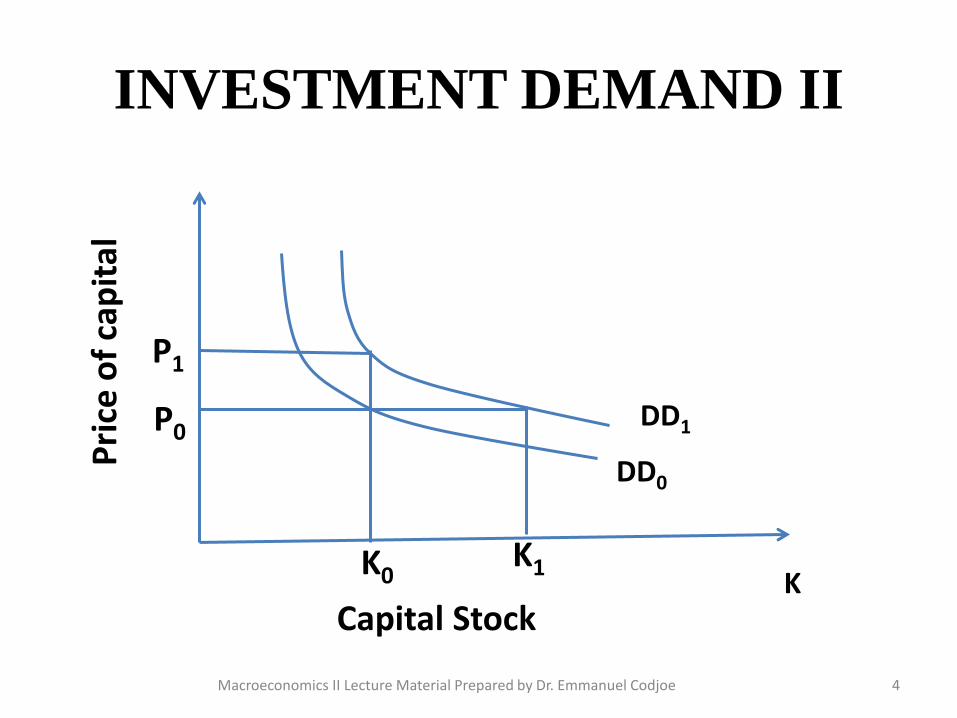

We also know that an increase in the capital stock

can be illustrated with a rightward shift in the

demand for capital schedule (DD0 to DD1) in the

figure below.

At the initial K0, Pk is just high enough to

generate enough investment, I0. In the short-run,

an increase in Pk to P1 increasing investment flow

to I1.

3 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe 4

K0 K1

K

P0

P1

Pri

ce o

f ca

pit

al

Capital Stock

DD1

DD0

INVESTMENT DEMAND II

Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe 5

I0 I1 I

P0

P1

Pri

ce o

f ca

pit

al

Investment Flow

INVESTMENT DEMAND II

But in the long run the supply of new

capital is very elastic, so eventually the

increase in demand will be met without

much change in price.

6 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

• Changes in the capital stock arise

depending on the magnitudes of gross

investment and depreciation.

• The change in the capital stock from one

period to another, say over a year is termed

net investment.

• This can be expressed algebraically as:

7 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

is gross investment

capital stock at beginning of year t, and

capital stock at the beginning of year t+1

tttt KIKK 1

tI

tK

1tK

8 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

The equation above can be used to illustrate

the relationship between the desired capital

and investment. Rewriting, we obtain:

tttt KIKK 1

tttt KKKI 1

9 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

The equation states that gross investment

equals net investment plus depreciation.

Suppose firms use information available at

the beginning of year t about expected future

MPK and the user cost of capital and

determine the desired capital stock, K*, they

want by the end of year t.

10 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

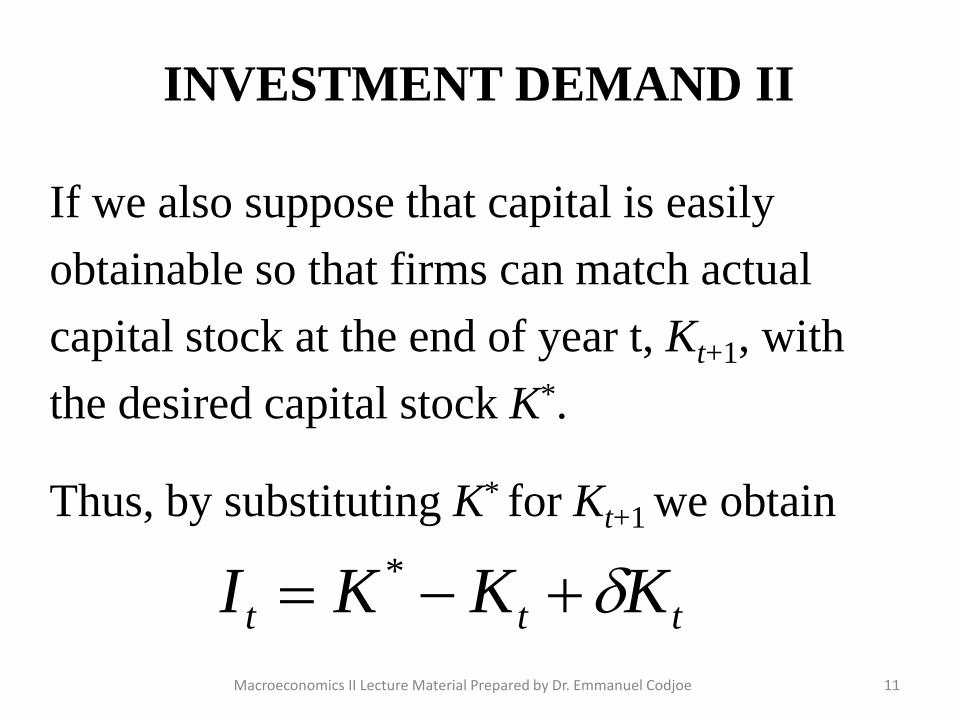

INVESTMENT DEMAND II

If we also suppose that capital is easily

obtainable so that firms can match actual

capital stock at the end of year t, Kt+1, with

the desired capital stock K*.

Thus, by substituting K* for Kt+1 we obtain

ttt KKKI *

11 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

The amount of depreciation that occurs

during a year is determined by the

depreciation rate and the initial capital stock.

The desired net increase in the capital stock

over the year depends on factors, such as

taxes, interest rates, and the expected future

MPK that affect the desired capital stock.

12 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

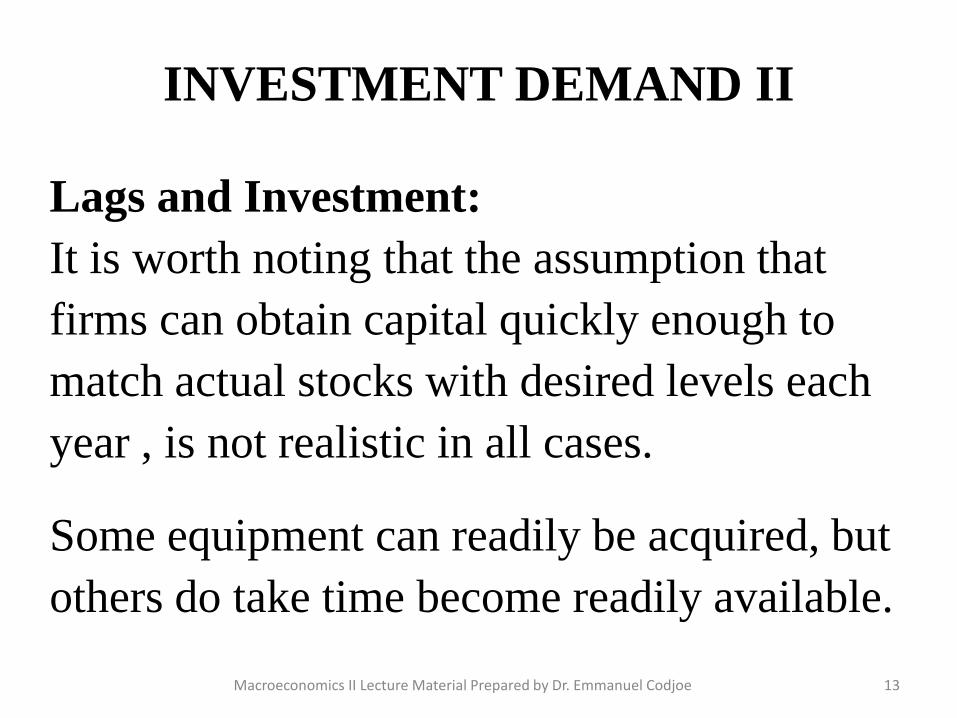

INVESTMENT DEMAND II

Lags and Investment:

It is worth noting that the assumption that

firms can obtain capital quickly enough to

match actual stocks with desired levels each

year , is not realistic in all cases.

Some equipment can readily be acquired, but

others do take time become readily available.

13 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

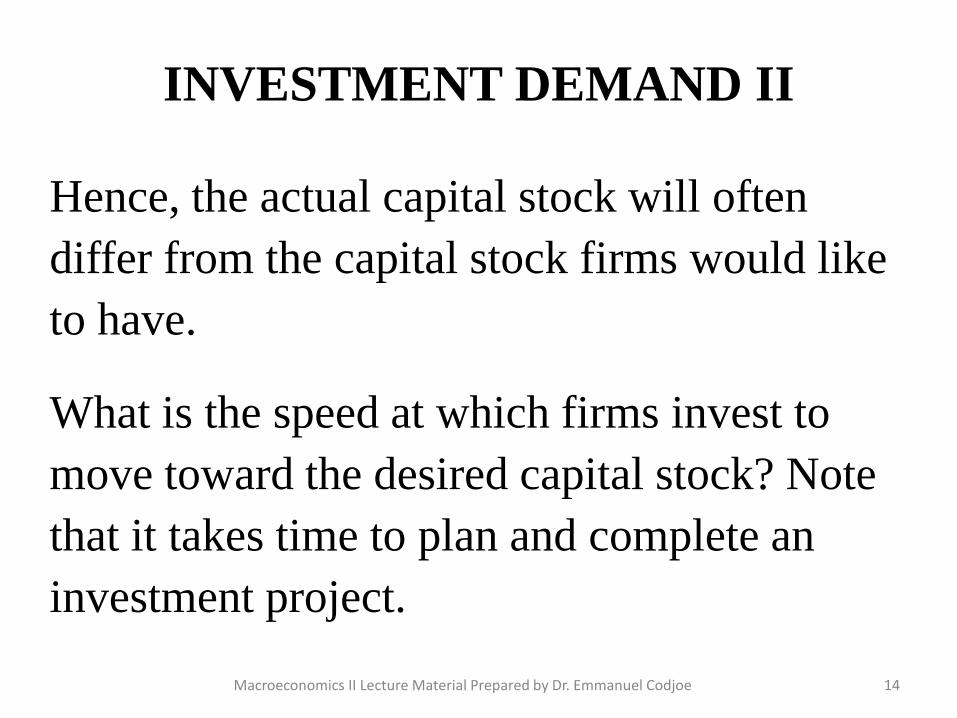

INVESTMENT DEMAND II

Hence, the actual capital stock will often

differ from the capital stock firms would like

to have.

What is the speed at which firms invest to

move toward the desired capital stock? Note

that it takes time to plan and complete an

investment project.

14 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Also, investing quickly is likely to be more

expensive than gradual adjustments of the

capital stock.

Thus, we would not expect to observe firms

adjusting their capital stocks to the long-run

desired level instantatenously.

15 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

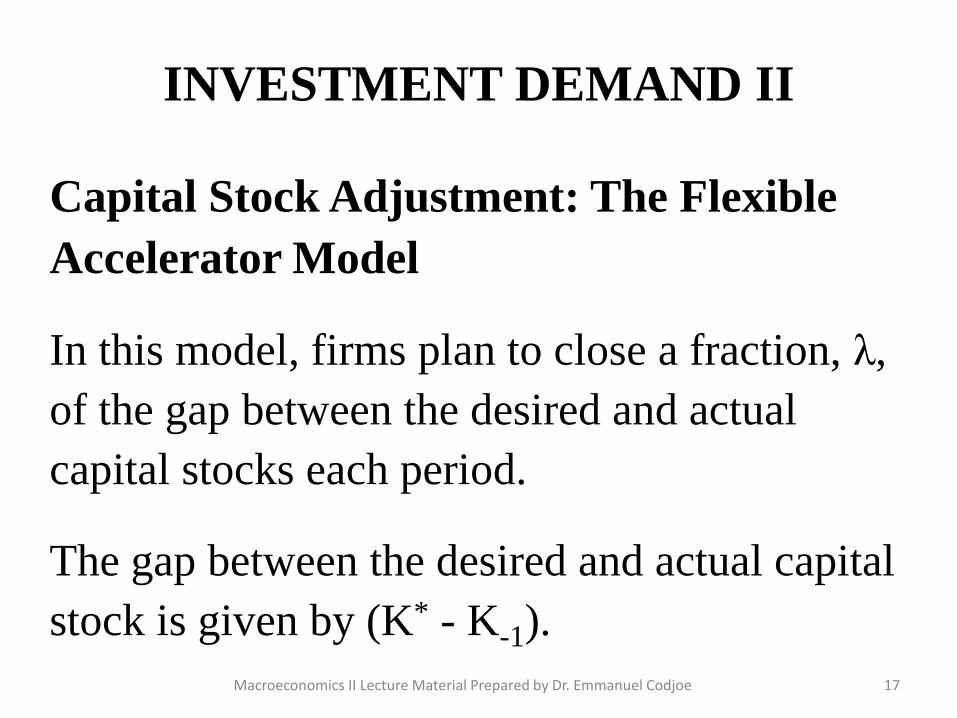

INVESTMENT DEMAND II

Capital Stock Adjustment: The Flexible

Accelerator Model

The basic notion behind this model is that the

larger the gap between the existing capital

stock and the desired capital stock, the more

rapid a firm’s rate of investment.

16 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Capital Stock Adjustment: The Flexible

Accelerator Model

In this model, firms plan to close a fraction, λ,

of the gap between the desired and actual

capital stocks each period.

The gap between the desired and actual capital

stock is given by (K* - K-1).

17 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Capital Stock Adjustment: The Flexible

Accelerator Model

The plan of the firm is to add to last period’s

capital stock, K-1, a fraction λ of the gap (K* -

K-1) so that the actual capital stock at the end

of the current period K is given by:

18 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Capital Stock Adjustment: The Flexible

Accelerator Model

To increase the capital stock from K-1 to the

level of K indicated by the equation above, the

firm has to achieve the amount of net

investment, I ≡ K - K-1.

19 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

)( 1

*

1 KKKK

INVESTMENT DEMAND II

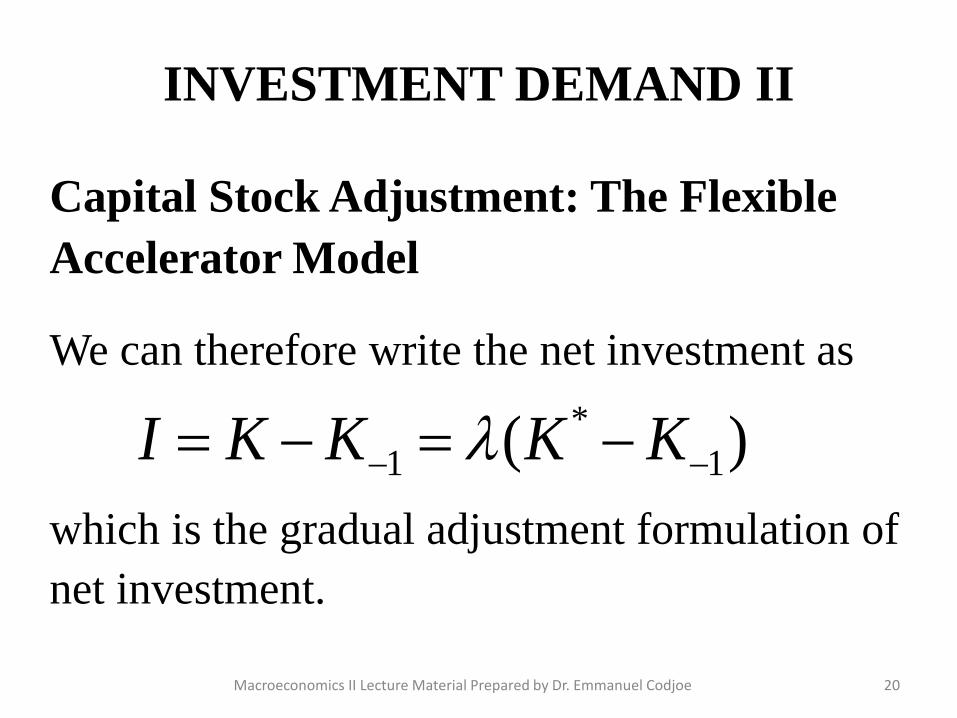

Capital Stock Adjustment: The Flexible

Accelerator Model

We can therefore write the net investment as

which is the gradual adjustment formulation of

net investment.

20 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

)( 1

*

1 KKKKI

INVESTMENT DEMAND II

Capital Stock Adjustment: The Flexible

Accelerator Model

Note that there is distinction between net

investment, which is what is stated above, and

gross investment, which in addition to the

above includes depreciation.

21 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Capital Stock Adjustment: The Flexible

Accelerator Model

The equation for net investment above shows

how current investment spending is

determined by the desired stock of capital, K*,

and the actual stock of capital, K-1.

22 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Capital Stock Adjustment: The Flexible

Accelerator Model

Thus, any factor that increases the desired

capital stock increases the rate of investment;

an increase in expected output, a reduction in

real interest rate, or an increase in tax credit.

23 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

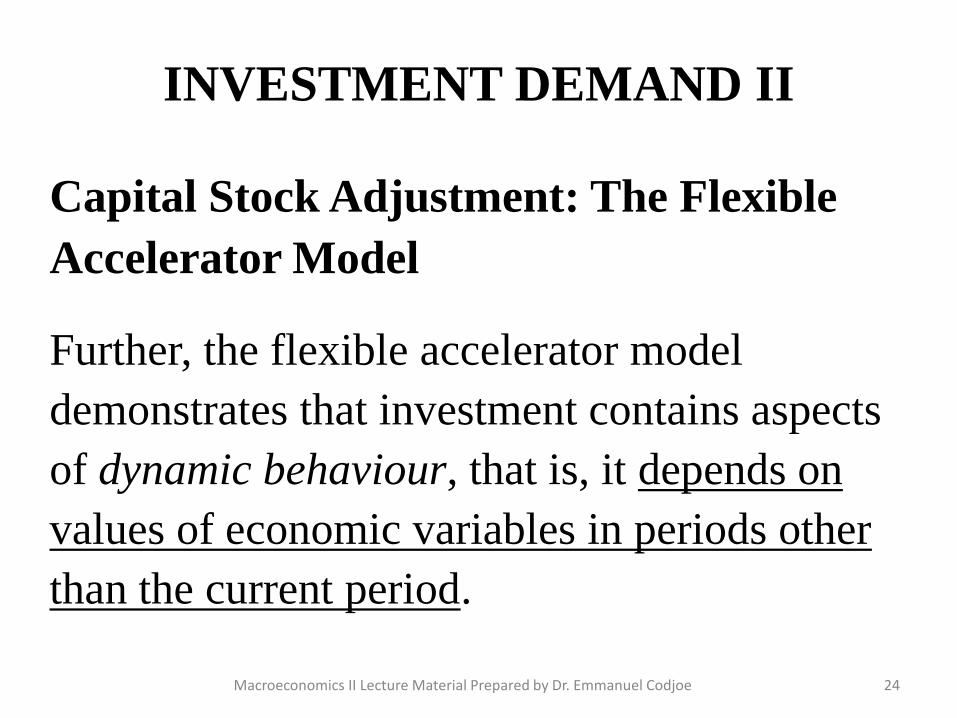

INVESTMENT DEMAND II

Capital Stock Adjustment: The Flexible

Accelerator Model

Further, the flexible accelerator model

demonstrates that investment contains aspects

of dynamic behaviour, that is, it depends on

values of economic variables in periods other

than the current period.

24 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

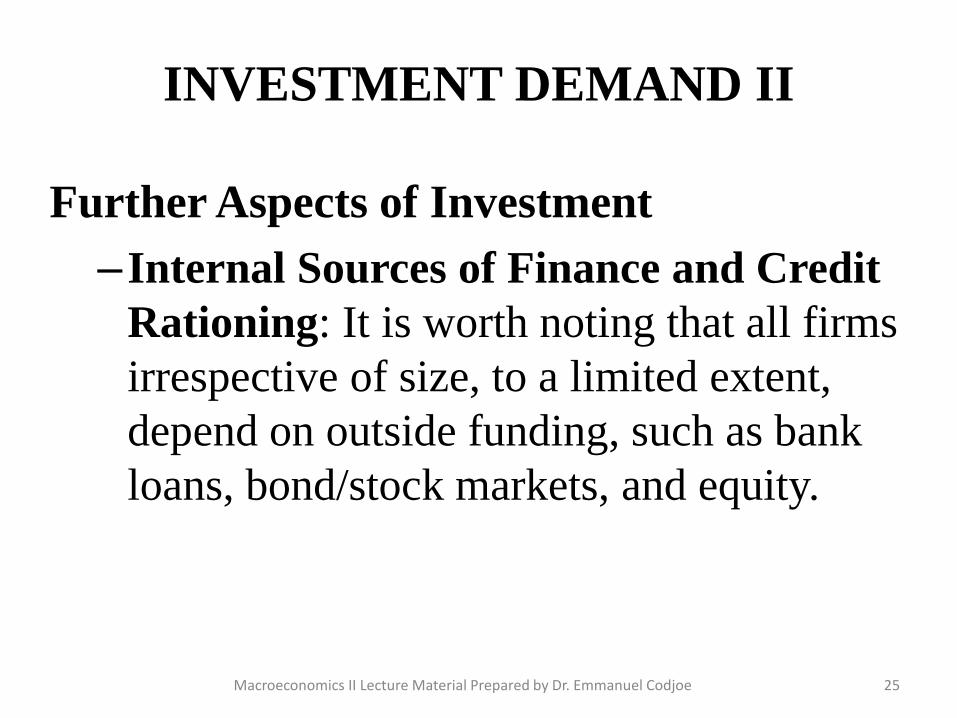

INVESTMENT DEMAND II

Further Aspects of Investment

–Internal Sources of Finance and Credit

Rationing: It is worth noting that all firms

irrespective of size, to a limited extent,

depend on outside funding, such as bank

loans, bond/stock markets, and equity.

25 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Further Aspects of Investment

• Internal Sources of Finance:

–However, to a greater extent, most firms

depend on internal sources (retained

earnings, profits that are not paid out as

dividends) to finance investment.

26 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Further Aspects of Investment

• Internal Sources of Finance:

–This shows the close link between the

earnings of firms and their investment

decisions. This means the state of a firm’s

balance sheet, and not just the cost of

capital, is a financial determinant of

investment decisions.

27 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Further Aspects of Investment

–Internal Sources of Finance and Credit

Rationing: credit rationing occurs when

individuals cannot borrow even though

they are willing to do so at the existing

interest rates. This usually arises because

of risks associated with the borrower.

28 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Further Aspects of Investment

• Credit Rationing:

–This suggests that smaller firms are more

likely to face this constraint than larger

firms.

–Smaller sized firms do not have an

established reputation compared with

larger sized firms with a track record.

29 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Further Aspects of Investment

• Credit Rationing:

–Where firms are rationed in their access to

funding, then firms’ investment decisions

will be affected not only by the interest

rate but also the amount of funds saved out

of past earnings and by their current

profits .

30 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Further Aspects of Investment

• Irreversibility and the Timing of Investment Decisions:

–Distinguishing between “putty-putty” and “putty-clay”.

–“putty-putty” investments do have alternative uses, such as a warehouse, office buildings, etc.

31 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Further Aspects of Investment

• Irreversibility and the Timing of

Investment Decisions:

–“putty-clay” investment do have limited

options, and generally have to be put to

the use for which they are made, e.g.,

jetliner, thermal plants, processing plants .

32 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Further Aspects of Investment

• Irreversibility and the Timing of

Investment Decisions:

– the essence of “putty-clay” investments is

that they are irreversible. Once such a

capital is built, it can’t be used for much

except for its original purpose.

33 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

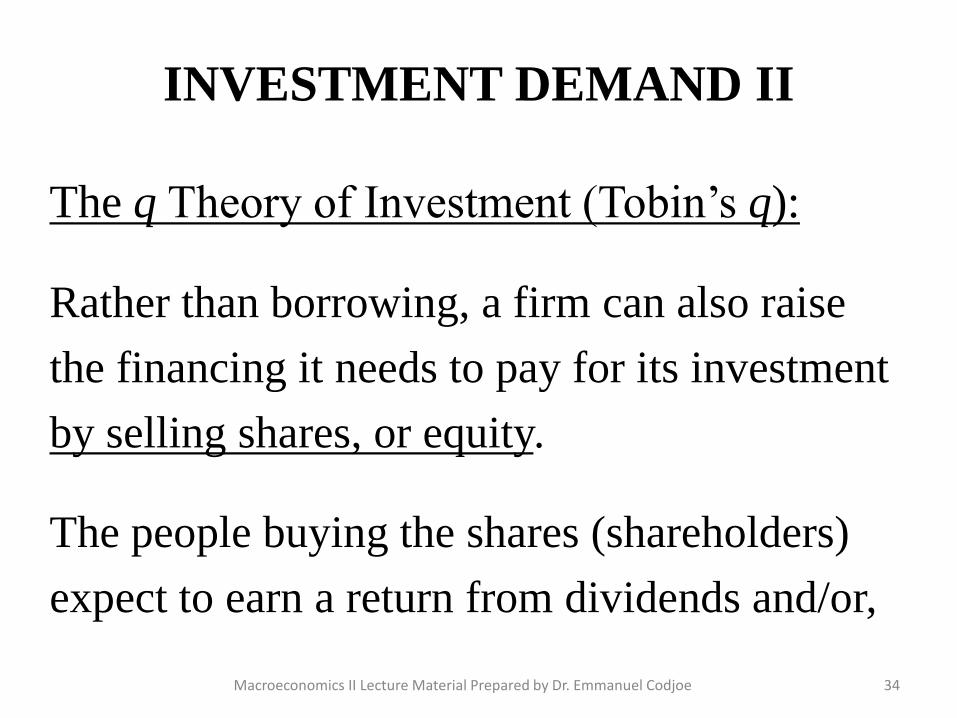

INVESTMENT DEMAND II

The q Theory of Investment (Tobin’s q):

Rather than borrowing, a firm can also raise

the financing it needs to pay for its investment

by selling shares, or equity.

The people buying the shares (shareholders)

expect to earn a return from dividends and/or,

34 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

The q Theory of Investment (Tobin’s q):

if the firm is successful, from the increase in

the market value of their shares, that is, capital

gains.

When its share price is high, a firm can raise a

lot of money by selling relatively few shares. When

they are low, the firm has to sell more shares to

raise a given amount of money.

35 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

The q Theory of Investment (Tobin’s q):

James Tobin put forth this notion of

connecting the stock market and investment.

When the stock prices are high, firms have

many opportunities for profitable investment,

because these profit opportunities mean

higher future income for shareholders.

36 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

The q Theory of Investment (Tobin’s q):

Thus, when share prices are high we expect

firms to be more willing to sell equity to

finance investment, than when the share

prices are low. That is why a booming stock

market is good for investment.

37 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

The q Theory of Investment (Tobin’s q):

Thus, stock prices reflect the incentive to

invest. Tobin proposed that firms base their

investment decisions on the following ratio,

which is now called Tobin’ q.

38 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

The q Theory of Investment (Tobin’s q):

Tobin’ q =

39 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

Capital Installed ofCost t Replacemen

Capital Installed of ValueMarket

INVESTMENT DEMAND II

The q Theory of Investment (Tobin’s q):

The numerator of the Tobin’s q is the value of

the economy’s capital as determined by the

stock market.

The denominator is the price of that capital if

it were purchased in the present (today).

40 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

The q Theory of Investment (Tobin’s q):

If q > 1, then the stock market values

installed capital at more than its replacement

cost. Hence firm managers can raise the

market value of their firms’ stock by buying

more capital.

41 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

The q Theory of Investment (Tobin’s q):

If q < 1, then the stock market values

installed capital at less than its replacement

cost. In this case firm managers have no

incentive to replace the firms’ capital as it

wears out.

42 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

The q Theory of Investment (Tobin’s q):

Both the depreciation rate and the interest rate are related to the q. An increase in the depreciation rate or in the interest rate causes q to fall.

An increase in the depreciation rate means more funds are set aside to replace worn-out capital. An increase in the interest rate raises the cost of capital.

43 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

The q Theory of Investment (Tobin’s q):

As in the case of the neoclassical approach, the Tobin’s q is determined by current and expected future profits from installed capital.

Stated otherwise, if the MPK > cost of capital, then firms are earning profits on installed capital. These profits make the firms desirous to own more capital, which in turn raises the market value of the firm’s stock, => high value of q.

44 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

The q Theory of Investment (Tobin’s q):

The converse is also through: so start with MPK < cost of capital.

The advantage of Tobin’s q as a measure of the incentive to invest is that if reflects the expected future profitability of capital as well as the current profitability of capital.

45 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

The q Theory of Investment (Tobin’s q):

Consequently, Tobin’s q theory of investment emphasises that investment decisions depend not only current economic policies but also on policies expected to prevail in the future.

Take the case of corporate taxes and recently taxes on capital gains (earnings on assets).

46 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Residential Investment

•Residential investment includes the purchase

of new housing both by the people who plan

to live in it themselves and by landlords who

plan to rent it to others.

•To simply matters, we assume that all

housing is owner-occupied. 47 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Residential Investment

•Housing is distinguished as an asset because

of its long life. Because of this characteristic,

in general investment in housing in any one

year tends to be a small percentage of GDP.

•The theory of residential investment has two

parts to it. 48 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

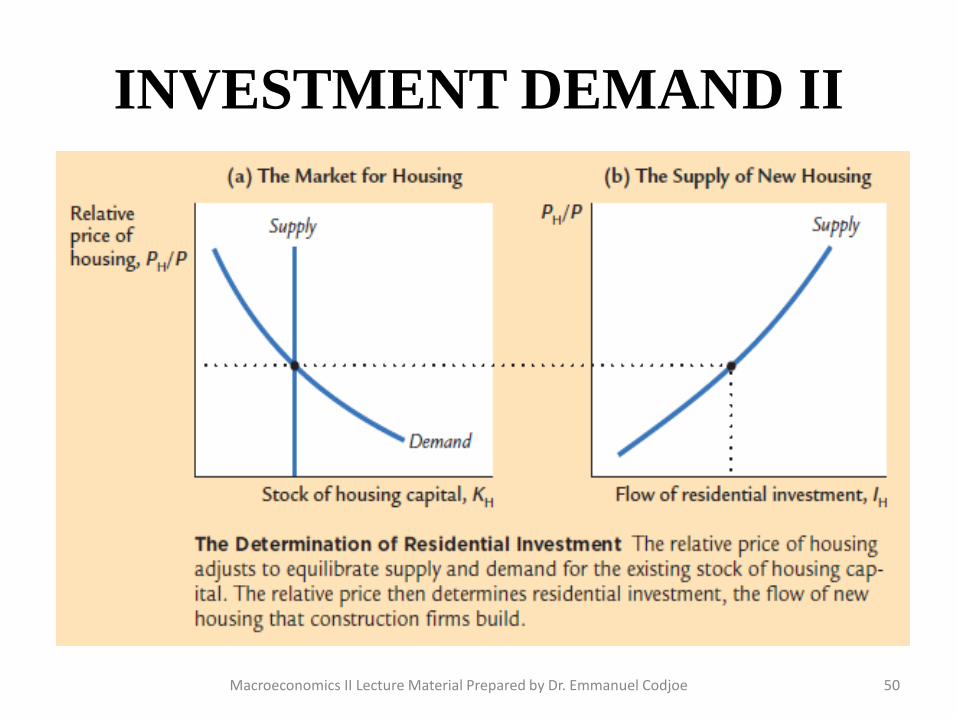

Residential Investment

•First, the market for existing stock of houses

determines the equilibrium housing price.

Second, the housing price determines the

flow of residential investment.

•At any point in time the supply of houses is

fixed, so supply is vertical. 49 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe 50

INVESTMENT DEMAND II

Residential Investment

•The demand for housing stock depends on the net real return obtained by owning housing.

•the gross return consists either of rent, if it is rented out, or of the implicit return that the house-owner receives by living in the house plus capital gains arising from increases in the value of the house.

51 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Residential Investment

•The cost of owning a house consists of

interest costs, here the mortgage interest rate,

plus any real estate taxes (property rates) and

depreciation.

•Net return is gross return less costs and any

taxes. 52 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Residential Investment

•The demand for housing is downward

sloping because at high prices people

downsize, house-share or become homeless.

•The equilibrium price is obtained through

the interaction of demand and supply.

53 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Residential Investment

•The supply of new housing is positively related to the price of houses. The higher the relative price of houses, the greater the incentive to build houses, and the more houses are built.

•The flow of new houses therefore depends on the equilibrium price set in the market for existing houses.

54 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Residential Investment

•Changes in Housing Demand: when there is change in the demand for housing, the equilibrium price changes, which in turn affects residential investment.

•The shift in demand occurs for several reasons (economic boom, increase in population size due to immigration, interest rates via mortgages, availability of credit)

55 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe 56

INVESTMENT DEMAND II

Inventory Investment

•Inventory investment represents the goods

that businesses put aside in storage.

•Typically, this is small percentage of GDP,

yet it is remarkably volatile.

•When there is an economic slump, firms run

down inventory.

57 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Inventory Investment

•Firms hold inventory for several

reasons.

•This section is left for student to

read on.

58 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Inventory Investment

Explaining Why Firms Hold Inventory

•The Accelerator Model asserts that

investment spending is proportional to

the change in output and is not affected

by the cost of capital.

59 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Inventory Investment

•More generally, the Accelerator Model

shows the relationship between the change in

output and the level of net investment.

•And as we have seen earlier, introduces a

dynamic relationship into the model of the

economy.

60 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Inventory Investment

•That is, . Much, but not

all of inventory investment can be

explained by the Accelerator Model.

•This relation links inventory investment to

the overall volatility of the economy.

61 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

)( 1 YYI

INVESTMENT DEMAND II

Inventory Investment

Anticipated vs. Unanticipated Inventory

•A distinction is made between anticipated

(desired) and unanticipated (undesired)

investment.

•When sales are low, inventories build up, this

constitutes unanticipated inventory investment.

62 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Inventory Investment

Anticipated vs. Unanticipated Inventory

•Where firms plan to build up inventories, then that is anticipated (desired) inventory investment, which adds to AD.

•Unanticipated inventory investment is therefore the result of unexpectedly low AD.

63 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Inventory Investment

Real Interest Rate

•Inventory investment also depends on the

real interest rate.

•How? This is explained by way of

opportunity cost.

64 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Inventory Investment

Real Interest Rate

•When a firm holds a good in inventory and

sells it in the future instead of the present, it

gives up the interest it could have earned

between today and tomorrow.

65 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Inventory Investment

Real Interest Rate

•When the real interest rate increases, it becomes more costly for firms to hold inventories, so rational firms reduce stock.

•Thus, high interest rates depress inventory investment

66 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Inventory Investment

Real Interest Rate

•Consequently, firms adopt just-in-time

inventory management techniques, whereby

inventories are kept closely in line with sales,

or aggregate demand.

67 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe

INVESTMENT DEMAND II

Inventory Investment

Real Interest Rate

•Inventory investment also depends on credit

conditions. Because many firms rely on bank

loans, when credit is hard to come by, they

cut back on inventories.

68 Macroeconomics II Lecture Material Prepared by Dr. Emmanuel Codjoe