MADE TO MEASURE Tolley ® Summer Budget 2015 IHT, Trusts and Estates Free in-depth, practical guidance on the Summer Budget For more in-depth analysis on the Summer Budget, visit tolley.co.uk/summerbudget

Transcript

MADE TO MEASURE

Tolley® Summer Budget 2015 IHT, Trusts and EstatesFree in-depth, practical guidance on the Summer Budget

For more in-depth analysis on the Summer Budget, visit tolley.co.uk/summerbudget

Tolley® takes every care when preparing this material. However, no responsibility can be accepted for any losses arising to any person acting or refraining from acting as a result of the material contained in these notes.

All rights reserved. No part of these notes may be reproduced or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of Tolley.

Whilst some of the links within this document resolve to publicly available websites, other links into documents within Tolley®Guidance are subscription sensitive. If you do not have a subscription to Tolley®Guidance then you can request a free trial tolley.co.uk/summerbudget

Simon Groom, Director of Tax Content Creation

During a 30 year career, mainly spent in training students for the ATT and CTA examinations, Simon has played a small role in starting the careers of many a tax professional, and during the last 9 years at Tolley he has spent most of that time leading the Tax Examinations business. He is now responsible for all of the tax content within Tolley, a role which means his appearances in the classroom are few and far between, but are probably more enjoyable for it.

During his career he spent time as a student at Arthur Young (now part of EY) where he qualified as a Chartered Accountant, and Financial Training (now Kaplan) where he discovered a love of all things tax, which made studying and passing the ATII (now CTA) exams that little bit easier. He returned to EY in 2000, to work in their National Tax Training Team, and whilst there became a member of Council of the Association of Taxation Technicians (ATT), following many years of lecturing for them on student conferences, and as a volunteer on various committees. Re-reading this paragraph and seeing all the name changes makes the 30 year career seem even longer!

Whilst at the ATT he played a role in developing the examination structure and syllabus, and latterly was chairman of their Membership Steering Group, and a member of the Audit Committee.

He joined Tolley in 2006 and is now Director of Tax Content Creation.

Request your free TolleyGuidance trial

Summer Budget 2015

Somehow, the official title of Summer Budget 2015 initially sounds subconsciously appealing; the use of the word “summer” brings to mind Wimbledon, strawberries and cream, long evenings with BBQ aromas in the background. Then the second word kicks in and the illusion is ruined. The other view in the office was that it sounded a bit like the song Summer Nights from the film, Grease – cue an impromptu penning of some budget related lyrics and a quick rendition by a hastily assembled Tolley choir – you can see the result here, https://youtu.be/TlYAyqN0F_U, not bad for the first take!

When everyone’s thoughts are turning to summer breaks this was exactly what we didn’t want, another raft of proposals to get to grips with – maybe it wouldn’t be that detailed?

If anyone had hopes of an easy ride they were soon dashed when it became apparent that there would be some fairly major changes to digest on the tax front. Included in the announcements were changes to the rules for “non-doms”, restrictions to tax relief on pensions for high earners (as well as the announcement of a green paper on fundamental reform of pensions), as well as the much heralded change to the way that the family home would be treated for IHT purposes. It became clear very quickly that this was not a budget that was tidying up a few loose ends.

It was clear that Mr Osborne wanted to take the opportunity to revisit the election manifesto as he declared “that’s how we were elected, and is exactly what we will do”, before stating that this was a “big Budget for a country with big ambitions”.

Once again, he proved himself to be a fan of statistics, rattling off an eye watering number of facts and figures, which he claims show that “Britain has turned a corner”. He also got in the, now obligatory, reference to sunshine and fixing the roof, not to mention 3 references to that old favourite, “Northern powerhouse”.

Inevitably, it was the announcements on welfare that raised the noise levels on the benches opposite, although the Speaker had to intervene to quieten the government benches when Mr Osborne announced the proposal for the National Living Wage – Iain Duncan-Smith found this particularly pleasing judging by his rather animated reaction!

In March it was suggested that he had chosen to spend £1m on a fund to commemorate the 600th anniversary of the Battle of Agincourt, solely so that he could weave in a dig at Ed Miliband. This time it was Boris Johnson in the firing line with a quip about his “campaign bunker” in a measure announcing funds for the renovation of the RAF’s Group Fighter Command Centre. He doubled his money by adding a more topical comment referencing the recommended expansion of Heathrow, with “the days when aeroplanes flew freely over the skies of west London.”

This budget was Mr Osborne at his most bullish, and as expected, it delighted his supporters and dismayed his opponents. There will be plenty for both sides to debate in the coming months.

Our tax writers, editors and technical teams have been hard at work throughout the afternoon, evening and night preparing the summaries that you can access from here, the aim being to tell you not only what has changed and why it is important, but also what it means for you. As always I am indebted to everyone for their hard work tonight – we hope that you find it useful.

Summer Budget 2015 — IHT, trusts and estates overviewOn 8 July 2015 the Chancellor delivered his first Budget for the Conservative government. The provisions relating to inheritance tax, trusts and estates are set out below.

Increased IHT nil rate band for main residence

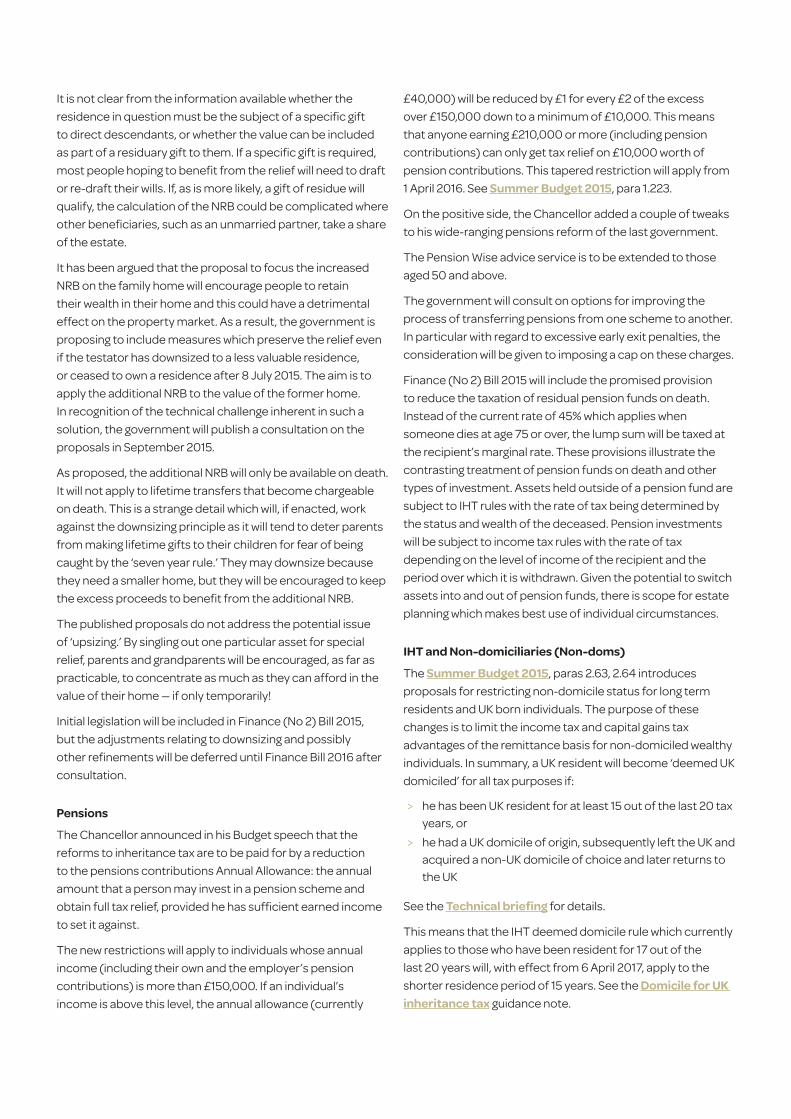

The Chancellor confirmed in his Budget speech the pre-announced proposal to introduce an additional IHT nil rate band (NRB) for the main residence. It will be available with effect from 6 April 2017 when a residence is passed on death to one or more direct descendants, such as children or grandchildren. Direct descendants include a step-child, adopted child or foster child. The extra allowance will be phased in as follows:

TAX YEAR ADDITIONAL NRB

2017–18 £100,000

2018–19 £125,000

2019–20 £150,000

2020–21 £175,000

The basic nil rate band will now remain at £325,000 until 5 April 2021, and thereafter the two elements of the NRB will increase together in line with the Consumer Price Index.

The main residence NRB will be transferable to a surviving spouse or civil partner, in the same way as the existing nil rate band. Hence the Chancellor was able to claim that the effective inheritance tax threshold for a couple will rise to £1 million in 2020/21. It will be ‘transferable’ even where the first death occurs before 6 April 2017, and the second death occurs afterwards. It appears that where the family home has been left to the spouse or civil partner on the first death at any time before 6 April 2017, the additional NRB is effectively backdated.

The sting in the tail, which was not pre-announced, was that the additional NRB will be progressively withdrawn for estates valued at more than £2 million. It will be tapered away by £1 for every £2 that the net value of the estate exceeds that amount (after deducting liabilities but before reliefs and exemptions), so the relief is aimed squarely at the moderately wealthy, who hold a large proportion of their wealth in their home, and will not benefit the very rich.

The proposals as outlined in the TIIN introduce some interesting details and raise a number of questions too.

The relief applies to the deceased’s interest in a residential property which has been his or her residence at some point and is included in the estate at death. Where more than one residential property qualifies, the personal representatives will be able to choose which one should attract the additional NRB. Clearly the choice will be governed by the comparative values of the properties and who the beneficiaries are. Case law relating to CGT private residence relief on what constitutes a ‘residence’ will be persuasive.

Pauline Lonsdale, Inheritance Tax Manager, Tolley

Pauline joined Tolley in 2012 as writer and editor for the IHT, Trusts and Estates module of Tolley®Guidance. She has been an independent practitioner for many years engaged in personal tax, trusts and estates work. In addition to advising her own clients, she acts as consultant to solicitors and accountants, focusing on finding practical solutions to a broad range of private client problems. She now divides her time between her own tax practice and Tolley®Guidance.

Pauline is a member of the ICAEW, CIOT and STEP. She sits on the STEP Practice Committee and spent some time as a tutor for the STEP Diploma programme.

It is not clear from the information available whether the residence in question must be the subject of a specific gift to direct descendants, or whether the value can be included as part of a residuary gift to them. If a specific gift is required, most people hoping to benefit from the relief will need to draft or re-draft their wills. If, as is more likely, a gift of residue will qualify, the calculation of the NRB could be complicated where other beneficiaries, such as an unmarried partner, take a share of the estate.

It has been argued that the proposal to focus the increased NRB on the family home will encourage people to retain their wealth in their home and this could have a detrimental effect on the property market. As a result, the government is proposing to include measures which preserve the relief even if the testator has downsized to a less valuable residence, or ceased to own a residence after 8 July 2015. The aim is to apply the additional NRB to the value of the former home. In recognition of the technical challenge inherent in such a solution, the government will publish a consultation on the proposals in September 2015.

As proposed, the additional NRB will only be available on death. It will not apply to lifetime transfers that become chargeable on death. This is a strange detail which will, if enacted, work against the downsizing principle as it will tend to deter parents from making lifetime gifts to their children for fear of being caught by the ‘seven year rule.’ They may downsize because they need a smaller home, but they will be encouraged to keep the excess proceeds to benefit from the additional NRB.

The published proposals do not address the potential issue of ‘upsizing.’ By singling out one particular asset for special relief, parents and grandparents will be encouraged, as far as practicable, to concentrate as much as they can afford in the value of their home — if only temporarily!

Initial legislation will be included in Finance (No 2) Bill 2015, but the adjustments relating to downsizing and possibly other refinements will be deferred until Finance Bill 2016 after consultation.

Pensions

The Chancellor announced in his Budget speech that the reforms to inheritance tax are to be paid for by a reduction to the pensions contributions Annual Allowance: the annual amount that a person may invest in a pension scheme and obtain full tax relief, provided he has sufficient earned income to set it against.

The new restrictions will apply to individuals whose annual income (including their own and the employer’s pension contributions) is more than £150,000. If an individual’s income is above this level, the annual allowance (currently

£40,000) will be reduced by £1 for every £2 of the excess over £150,000 down to a minimum of £10,000. This means that anyone earning £210,000 or more (including pension contributions) can only get tax relief on £10,000 worth of pension contributions. This tapered restriction will apply from 1 April 2016. See Summer Budget 2015, para 1.223.

On the positive side, the Chancellor added a couple of tweaks to his wide-ranging pensions reform of the last government.

The Pension Wise advice service is to be extended to those aged 50 and above.

The government will consult on options for improving the process of transferring pensions from one scheme to another. In particular with regard to excessive early exit penalties, the consideration will be given to imposing a cap on these charges.

Finance (No 2) Bill 2015 will include the promised provision to reduce the taxation of residual pension funds on death. Instead of the current rate of 45% which applies when someone dies at age 75 or over, the lump sum will be taxed at the recipient’s marginal rate. These provisions illustrate the contrasting treatment of pension funds on death and other types of investment. Assets held outside of a pension fund are subject to IHT rules with the rate of tax being determined by the status and wealth of the deceased. Pension investments will be subject to income tax rules with the rate of tax depending on the level of income of the recipient and the period over which it is withdrawn. Given the potential to switch assets into and out of pension funds, there is scope for estate planning which makes best use of individual circumstances.

IHT and Non-domiciliaries (Non-doms)

The Summer Budget 2015, paras 2.63, 2.64 introduces proposals for restricting non-domicile status for long term residents and UK born individuals. The purpose of these changes is to limit the income tax and capital gains tax advantages of the remittance basis for non-domiciled wealthy individuals. In summary, a UK resident will become ‘deemed UK domiciled’ for all tax purposes if:

> he has been UK resident for at least 15 out of the last 20 tax years, or

> he had a UK domicile of origin, subsequently left the UK and acquired a non-UK domicile of choice and later returns to the UK

See the Technical briefing for details.

This means that the IHT deemed domicile rule which currently applies to those who have been resident for 17 out of the last 20 years will, with effect from 6 April 2017, apply to the shorter residence period of 15 years. See the Domicile for UK inheritance tax guidance note.

There is a further tightening of the rules for IHT purposes relating to those who leave the UK. Currently, a UK domiciled resident remains deemed domiciled for three years after leaving the UK, and one who has become deemed domiciled because of the 17 out of 20 years rule, must wait four years before losing the status. The new proposal is to extend that period to five years for a resident who leaves the UK.

The government will consult on the potential effects of these changes on the spousal election for UK domicile. See the Transfers to a non UK domiciled spouse or civil partner guidance note.

By increasing the scope of the deemed domicile rules, the government will widen the net for inheritance tax although the main targets for the changes are income tax and capital gains tax.

Non-doms will still have the opportunity to create excluded property trusts before becoming deemed domiciled under the 15 year rule. The trust itself will retain its general IHT exemption but there will be a new limitation relating to UK residential property (see below). Provided that the excluded property trust is also non-resident, it will not be subject to UK income and capital gains tax. However, the loss of non-dom status after 15 years for a settlor or beneficiary will result in his being taxed on the worldwide income or gains, and not just on those remitted.

In addition, the returning UK domiciliary, that is one who has acquired a foreign domicile but returned to the UK, will become UK domiciled again once he becomes UK resident. He will not be able to benefit from any favourable tax treatment of trusts created while he was a non-dom. In other words, excluded property trusts will never be available to those who were born with a UK domicile and return to the UK.

The government recognises that this is an extremely complex area and the new rules will be subject to consultation. See the technical briefing, paras 22, 23.

IHT rules on UK residential property

The Chancellor announced a further restriction to the advantages of non-dom status relating to UK residential property. A common tax planning technique for non-doms is to hold their UK property in an offshore company or partnership. By so doing, the UK situs asset is converted to excluded property because the asset becomes shares in an overseas company. As a result the non-dom avoids IHT on his residence in the UK because he is not subject to IHT on excluded (ie non UK) property.

A further refinement of the plan is for an excluded property trust to hold the shares of the offshore company that owns the property so that the exemption is retained after the individual has become deemed domiciled.

A technical briefing explains how this advantage will be curtailed. The rules will be amended so that all UK property will be subject to IHT in the same way that it applies to UK domiciled individuals. Legislation will provide that offshore companies or similar structures are not excluded property to the extent that they derive their value directly or indirectly from UK residential property. As a result, IHT on death will apply and relevant property charges will apply where the property is held in trust.

Again, the issue is highly complex potentially involving other taxes such as ATED, CGT and SDLT. A consultation will be published inviting views and representations. The intention is to make the changes effective on or after 6 April 2017.

Changes to IHT charges on trusts

The original draft Finance Bill 2015, published in December 2014, included legislation designed to counter pilot trusts, and revised the rules relating to the charges on relevant property trusts. The proposals were not included in the curtailed Finance Act in March 2015, but they will be introduced in Finance (No 2) Bill 2015.

The calculation of IHT principal and exit charges will be simplified by removing the requirement to include non-relevant property in the initial value to determine the rate of tax. This is a welcome amendment in light of the difficulty of obtaining historic valuations, particularly where, as in old Accumulation and Maintenance trusts, an initial value was not required when the trust was created. The new rule will apply to all charges arising on or after the date of Royal Assent regardless of when the trust was created.

In relation to pilot trusts, it is proposed that the calculation of 10 year and exit charges will take account of ‘same-day additions’. This means that where property is added on death to multiple trusts, (ie previously created pilot trusts), the calculation will effectively combine it into one trust, thus losing the benefit of multiple nil rate bands. The measure will apply to charges arising on or after the date of Royal Assent, but only to relevant property trusts or additions made on or after publication of the original draft legislation on 10 December 2014.

The new rules are disapplied to a will executed before 10 December 2014, where the death occurs before 6 April 2017. See the Pilot trusts and will planning guidance note for background information.

Changes were announced to the taxation of dividends for individuals. See Summer Budget 2015, para 2.57. The tax credit is to be abolished and individuals will benefit from a Dividend Tax Allowance of £5000. Dividend income above the allowance will be taxed at 7.5%, or 32.5% or 38.1% according to the individual’s personal rate of tax.

There is no mention of how this new system will apply to trustees. The worst case scenario is that a rate of 38.1% will apply to all dividends received by discretionary trusts (following the alignment of the trust rate with the individual additional rate). Presumably, the tax paid, at whatever rate, will go into the tax pool and become potentially repayable, thus changing the issues of a mismatch of tax rates in the tax pool. See the Making use of the tax pool guidance note.

RESEARCHNo matter what sort of organisation you work in, it’s hard to stay fully informed on all the important new tax cases and amendments to tax legislation. Your clients want you to be able to take advantage of new tax planning opportunities. Your employer needs to be sure that your advice reflects the latest changes to compliance rules.

You can trust Tolley’s comprehensive range of tax products to make it easier than ever to keep up-to-date with the constant changes in tax and find all the details you need. Tolley’s products are written by tax specialists for tax specialists and designed to suit the way you work.

Five reasons to rely on Tolley for your research

1. Authoritative, trusted, comprehensive information2. Flexible delivery: online, in print or both3. Pricing to suit the needs of your business4. Intuitive online search for faster results5. Enhanced with news alerts, updates and cross-references

TolleyLibraryFor the whole picture, including analysis and commentary plus cases and legislation, and the broadest choice of our books, looseleafs and magazines, subscribe to TolleyLibrary.

We’re proud that it’s the most user-friendly online library for tax and accountancy practitioners, containing the most comprehensive, up-to-date and trusted information. And you can manage your costs with subscriptions and payment options that fit the size and style of your business.

Blending the best of the traditional and the modern, we’ve built TolleyLibrary Light to give smaller practices online access to our most popular titles. It's easy to search, always up-to-date and keeps your costs in control – and you benefit from links to the relevant HMRC manuals. Opt in to regular news updates to keep in touch with the areas of tax that most interest you.

For more information on research visit tolley.co.uk/research

Undue risk is often the result of misunderstanding. Mistakes occur when the way ahead isn’t clear.

With us by your side, there’s no need to have sleepless nights fearing litigation for inaccurate or incorrect advice – or not meeting HMRC statutory requirements. We give you the tools to check that nothing slips your mind, and help us provide evidence that you have taken reasonable care.

Five reasons to choose Tolley for practical guidance

1. Written by tax experts, based on real-life experience2. Guidance that’s detailed, practical and reliable3. Information that’s robust, up-to-date and complete,

and stands up in court4. Acts as a simple refresher or a step-by-step guide 5. Modular format helps you to control your costs

TolleyGuidanceTolleyGuidance is written by tax experts, who use their knowledge and experience to explain how tax really works. Expand your understanding, refresh your knowledge and explore new areas of specialism.

The tax industry is renowned for its complexity and its speed of change. TolleyGuidance provides answers that are straightforward and up-to-date.

Find practical, technical commentary on unfamiliar areas, with easy-to-apply examples based on real-life cases. Get step-by-step help to tackle the issue, with simple to understand “how-to” guides and easy to complete template documents. For many of our clients, TolleyGuidance reduces their need to use external specialists, and that can only reduce your costs.

We’ve worked with tax practitioners to create a modular service so you can choose the subject areas that are right for your business. Whatever your question, on whatever aspect of tax, you can find guidance, tools and associated information quickly, easily and with an eye on controlling your costs.

For more information on practical guidance visit tolley.co.uk/practicalguidance

Passing your tax exams is just a part of your learning. Continuing professional development is important because it ensures you continue to be competent in your profession.

You can achieve a certain amount of learning ‘on the job’, but you need to bolster that with regular formal education and training. It’s certainly worth the time investment. Professionals who plan their skills development tend to make faster progress in their careers, in the direction they choose. Tolley’s professional development products and services make it easier, with a wide choice of subject matter and delivery routes.

In-PersonMeeting other practitioners is great for building contacts, and better still, helps you understand the current practice of tax and the requests you might face. That’s why there’s time for networking in our annual programme of popular half day CPD Seminars, as well as for hearing from our experts on the most topical issues across the industry.

OnlineBut when time is tight you might prefer to watch bitesize chunks of what’s going on in tax, accountancy and audit. Watch our monthly Online CPD Seminars, when it suits you, on whatever device you prefer. You can use them with your team to help them achieve their CPD requirements too. Our online tax law Webinars also let you pose questions to tax barristers and discuss the latest issues with other attendees in the live sessions, as well as watching again how and when you like.

Magazines and JournalsFor the ultimate in flexible learning, it’s hard to beat our magazines – Taxation, Tax Journal or Tax Adviser. Browse and learn, in print or online, across everything that’s going on. They’re the simplest way to make sure you’re always right up to date with what matters in your areas of tax.

Essential Business Development SkillsWhen you’re also involved in running the business, you may find that you need to arm yourself with skills beyond accountancy and tax. We developed our online webinars Essential Business Development Skills with accountancy and tax practice managers in mind, to give you ideas and advice on how to find and retain customers as well as manage staff and suppliers.

For more information on CPD visit tolley.co.uk/cpd

Whether you’re just starting out in tax or accountancy, or already have years of experience, its hard work gaining the qualifications you need to progress in your career. Tolley Exam Training can help you succeed in gaining those vital tax qualifications. We are experts in tax and our exam pass rates are the best in the industry. And we can help you right from the start, when you’re choosing the qualification that’s right for your experience and your interest.

Association of Taxation Technicians (ATT) qualificationOnce you’re working in tax compliance, you can demonstrate your competence with The Association of Taxation Technicians (ATT) exam. Tolley Exam Training gives you the choice of mixing traditional correspondence courses with live lectures and online training, so you can design your learning to fit your location and your work.

Chartered Tax Advisor (CTA) qualificationIf you want to widen your possible career routes then you also need to be able give advice to clients. The Chartered Tax Advisor (CTA) qualification from the Chartered Institute of Taxation is the highest level tax qualification in the UK. Our experts are on hand with practical advice on exam choices that can save you hours of study as well as helping you to succeed.

Advanced Diploma in International Taxation (ADIT)The Advanced Diploma in International Taxation (ADIT) meets the demand, both in and outside the UK, for a specialist qualification for international tax practitioners in the corporate area. It recognises that international tax advisers need to understand more than one tax system. So talk to us, we’re one of the very few bodies in the UK who can prepare you for the Advanced Diploma in International Taxation (ADIT).

For more information on qualifications visit tolley.co.uk/qualifications

The Front Line is where you stand face to face with HMRC and agree tax. It’s not a place to be alone. Not a place to go to unprepared.

As the UK’s only provider of critical tax information, in-depth reference, ground-breaking training and learning resources and unique market insight, Tolley is there by your side with four product families designed for tax professionals working on The Front Line.