12/16/2015 Magic Quadrant for Unified Communications for Midsize Enterprises, North America http://www.gartner.com/technology/reprints.do?id=12EHP0XC&ct=150505&st=sg 1/13 Magic Quadrant for Unified Communications for Midsize Enterprises, North America 5 May 2015 ID:G00270849 Analyst(s): Megan Marek Fernandez, Sorell Slaymaker VIEW SUMMARY Midsize businesses have evergreater choice in premisesbased unified communications, with providers extending features and gotomarket channels while trying to maintain ease of use and consistency. Midmarket IT planners should evaluate UC providers' delivery capabilities, not just their solutions. Market Definition/Description This document was revised on 11 May 2015. The document you are viewing is the corrected version. For more information, see the Corrections page on gartner.com. Unified Communications This Magic Quadrant evaluates the premisesbased unified communications (UC) solutions geared for the midmarket. The primary benefit of UC is to improve user productivity and to enhance business processes. Gartner defines UC products (equipment, software and services) as those that facilitate the use of multiple enterprise communications methods to obtain that productivity goal. UC products integrate communications channels (media), networks and systems, as well as IT business applications and, in some cases, consumer applications and devices. UC offers the ability to significantly improve how individuals, groups and companies interact and perform. The UC products may be composed of a single vendor (standalone) suite, or enterprises/businesses may deploy a portfolio of integrated applications and platforms spanning multiple vendors. In many cases, UC is deployed to extend and add functionality to established communications investments. UC products are used by individuals to facilitate personal communications, and by enterprises to support workgroup and collaborative communications and business workflows. Some UC products may extend UC beyond a company's boundaries: to enhance communications between organizations, and to support interactions among large public communities or for personal communications. UC applications are increasingly being integrated with, or offered in concert with, collaboration applications to form unified communications and collaboration (UCC) solutions; in some cases they are also being integrated with business applications and workflows, something Gartner calls "communicationsenabled business processes." It is useful to divide UC into six broad communications product areas: Telephony — This area includes fixed, mobile and soft telephony, as well as the evolution of Internet Protocol (IP)PBXs. This category includes options for voice and video that bypass traditional connectivity methods, such as direct Internetbased connections. Conferencing — This area includes infrastructure for voice (audio) conferencing, videoconferencing, Web conferencing that includes document and application sharing capabilities, and various forms of unified conferencing capabilities. Messaging — This area includes email, which has become an indispensable business tool, voice mail and various approaches to unified messaging (UM). Presence and instant messaging — IM allows individuals to send text and other information to others or to groups in real time. Presence services allow individuals to see the status of other people and resources. Clients — Unified clients enable access to multiple communications functions from a consistent interface. These may take different forms, including thick desktop clients, thin browser clients and clients for mobile devices (such as smartphones and tablets), as well as specialized clients embedded within business applications. Communicationsenabled applications — This broad group of applications has directly integrated communications functionality. Key application areas include collaboration, contact center and notification; also consolidated administration, reporting and/or analytics tools. The Midmarket Profile Gartner provides the following profile to highlight how common midmarket characteristics can shape UC purchasing behaviors. Gartner defines the midmarket as organizations with between 100 and 999 EVIDENCE This research is based, in part, on: Feedback from Gartner inquiries Providers' responses to questionnaires specific to this Magic Quadrant Interviews with the providers' channel partners Interviews with the providers' customers Oneonone briefings with the providers Generally available information, news and data in financial and industry publications Discussions with Gartner peers in relevant research communities Gartner management critique and peer review, and vendor review and confirmation EVALUATION CRITERIA DEFINITIONS Ability to Execute Product/Service: Core goods and services offered by the vendor for the defined market. This includes current product/service capabilities, quality, feature sets, skills and so on, whether offered natively or through OEM agreements/partnerships as defined in the market definition and detailed in the subcriteria. Overall Viability: Viability includes an assessment of the overall organization's financial health, the financial and practical success of the business unit, and the likelihood that the individual business unit will continue investing in the product, will continue offering the product and will advance the state of the art within the organization's portfolio of products. Sales Execution/Pricing: The vendor's capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel. Market Responsiveness/Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor's history of responsiveness. Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization's message to influence the market, promote the brand and business, increase awareness of the products, and establish a positive identification with the product/brand and organization in the minds of buyers. This "mind share" can be driven by a combination of publicity, promotional initiatives, thought leadership, word of mouth and sales activities. Customer Experience: Relationships, products and services/programs that enable clients to be successful with the products evaluated. Specifically, this includes the ways customers receive technical support or account support. This can also include ancillary tools, customer support programs (and the quality thereof), availability of user groups, servicelevel agreements and so on. Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure, including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis. Completeness of Vision Market Understanding: Ability of the vendor to understand buyers' wants and needs and to translate

Transcript

12/16/2015 Magic Quadrant for Unified Communications for Midsize Enterprises, North America

Magic Quadrant for Unified Communicationsfor Midsize Enterprises, North America5 May 2015 ID:G00270849

Analyst(s): Megan Marek Fernandez, Sorell Slaymaker

VIEW SUMMARY

Midsize businesses have evergreater choice in premisesbased unified communications, with providersextending features and gotomarket channels while trying to maintain ease of use and consistency.Midmarket IT planners should evaluate UC providers' delivery capabilities, not just their solutions.

Market Definition/DescriptionThis document was revised on 11 May 2015. The document you are viewing is the corrected version.For more information, see the Corrections page on gartner.com.

Unified Communications

This Magic Quadrant evaluates the premisesbased unified communications (UC) solutions geared forthe midmarket. The primary benefit of UC is to improve user productivity and to enhance businessprocesses. Gartner defines UC products (equipment, software and services) as those that facilitate theuse of multiple enterprise communications methods to obtain that productivity goal. UC productsintegrate communications channels (media), networks and systems, as well as IT business applicationsand, in some cases, consumer applications and devices.

UC offers the ability to significantly improve how individuals, groups and companies interact andperform. The UC products may be composed of a single vendor (standalone) suite, orenterprises/businesses may deploy a portfolio of integrated applications and platforms spanningmultiple vendors. In many cases, UC is deployed to extend and add functionality to establishedcommunications investments.

UC products are used by individuals to facilitate personal communications, and by enterprises tosupport workgroup and collaborative communications and business workflows. Some UC products mayextend UC beyond a company's boundaries: to enhance communications between organizations, and tosupport interactions among large public communities or for personal communications. UC applicationsare increasingly being integrated with, or offered in concert with, collaboration applications to formunified communications and collaboration (UCC) solutions; in some cases they are also being integratedwith business applications and workflows, something Gartner calls "communicationsenabled businessprocesses."

It is useful to divide UC into six broad communications product areas:

Telephony — This area includes fixed, mobile and soft telephony, as well as the evolution ofInternet Protocol (IP)PBXs. This category includes options for voice and video that bypasstraditional connectivity methods, such as direct Internetbased connections.

Conferencing — This area includes infrastructure for voice (audio) conferencing,videoconferencing, Web conferencing that includes document and application sharing capabilities,and various forms of unified conferencing capabilities.

Messaging — This area includes email, which has become an indispensable business tool, voicemail and various approaches to unified messaging (UM).

Presence and instant messaging — IM allows individuals to send text and other information toothers or to groups in real time. Presence services allow individuals to see the status of otherpeople and resources.

Clients — Unified clients enable access to multiple communications functions from a consistentinterface. These may take different forms, including thick desktop clients, thin browser clients andclients for mobile devices (such as smartphones and tablets), as well as specialized clientsembedded within business applications.

Communicationsenabled applications — This broad group of applications has directly integratedcommunications functionality. Key application areas include collaboration, contact center andnotification; also consolidated administration, reporting and/or analytics tools.

The Midmarket Profile

Gartner provides the following profile to highlight how common midmarket characteristics can shape UCpurchasing behaviors. Gartner defines the midmarket as organizations with between 100 and 999

EVIDENCE

This research is based, in part, on:

Feedback from Gartner inquiriesProviders' responses to questionnaires specific tothis Magic QuadrantInterviews with the providers' channel partnersInterviews with the providers' customersOneonone briefings with the providersGenerally available information, news and data infinancial and industry publicationsDiscussions with Gartner peers in relevant researchcommunitiesGartner management critique and peer review, andvendor review and confirmation

EVALUATION CRITERIA DEFINITIONS

Ability to ExecuteProduct/Service: Core goods and services offered bythe vendor for the defined market. This includescurrent product/service capabilities, quality, featuresets, skills and so on, whether offered natively orthrough OEM agreements/partnerships as defined inthe market definition and detailed in the subcriteria.

Overall Viability: Viability includes an assessment ofthe overall organization's financial health, the financialand practical success of the business unit, and thelikelihood that the individual business unit will continueinvesting in the product, will continue offering theproduct and will advance the state of the art within theorganization's portfolio of products.

Sales Execution/Pricing: The vendor's capabilities inall presales activities and the structure that supportsthem. This includes deal management, pricing andnegotiation, presales support, and the overalleffectiveness of the sales channel.

Market Responsiveness/Record: Ability to respond,change direction, be flexible and achieve competitivesuccess as opportunities develop, competitors act,customer needs evolve and market dynamics change.This criterion also considers the vendor's history ofresponsiveness.

Marketing Execution: The clarity, quality, creativityand efficacy of programs designed to deliver theorganization's message to influence the market,promote the brand and business, increase awarenessof the products, and establish a positive identificationwith the product/brand and organization in the mindsof buyers. This "mind share" can be driven by acombination of publicity, promotional initiatives,thought leadership, word of mouth and sales activities.

Customer Experience: Relationships, products andservices/programs that enable clients to be successfulwith the products evaluated. Specifically, this includesthe ways customers receive technical support oraccount support. This can also include ancillary tools,customer support programs (and the quality thereof),availability of user groups, servicelevel agreementsand so on.

Operations: The ability of the organization to meet itsgoals and commitments. Factors include the quality ofthe organizational structure, including skills,experiences, programs, systems and other vehiclesthat enable the organization to operate effectively andefficiently on an ongoing basis.

Completeness of VisionMarket Understanding: Ability of the vendor tounderstand buyers' wants and needs and to translate

employees and annual revenue of less than $1 billion. The midmarket can further be segmented intothe lower midmarket (organizations with between 100 and 499 employees) and the upper midmarket(organizations with between 500 and 999 employees). The midmarket represents a large and fastgrowing segment of overall IT spending, with growth rates approximately one and a half times themarket average of 2.8% (see "Forecast Alert: IT Spending, Worldwide, 1Q15 Update"). While midsizebusinesses have many of the same business objectives as larger enterprises, they operate on a smallerscale and function with fewer IT assets and resources. These relative resource constraints imposeunique purchasing behaviors, and influence the success of UC solutions in the market and thesatisfaction of UC users. The following characteristics highlight unique midmarket UC buying behaviorsand purchasing criteria.

Ease of administration, management and use — Midsize businesses have fewer inhouse ITresources than their largeenterprise counterparts (see "IT Key Metrics Data 2015: Small andMidsize Enterprise Executive Summary") and have different expectations surrounding their UCsolutions. They therefore have a preference for solutions that offer straightforwardimplementations, consolidated administration and management tools. Tools that assist in trafficand network monitoring and control, and interfaces that are intuitive and easy to use, will featuregreater use by employees across the organization and result in solutions receiving highersatisfaction ratings.

Customer service and support quality — The top factors influencing buying behaviors in themidmarket are related to service levels (see "Market Insight: MidsizeBusiness Primer, 2014").Midsize businesses don't have enough internal resources to troubleshoot problems, so they arefairly dependent on the provider and/or their providers' partners. If a provider or channel partnerfails to be "easy to do business with" or delivers poor service, midmarket organizations exhibitlittle hesitation in replacing that provider or solution. Providers that demonstrate aboveaverageservice levels to their channel partners and/or customers will experience greater success andbrand loyalty. Consequently, channel programs (including the training, certifications, dealerregistration details, presales and postsales support) remain critical components of providers' gotomarket midsize enterprise UC success.

UC features — Midsize enterprise employees tend to be highly mobile and frequently havemultiple job responsibilities. Many midsize organizations expect solutions to enable users toextend business functions across desk phones, mobile devices, tablets and PCs. Furthermore,many midmarket IT leaders will expect UC applications to integrate with specific businessapplications and processes including collaboration, analytics, and reporting tools. The need forcustomization frequently exists, but IT planners often choose not to do this because they don'thave the money or resources to customize and then support the resulting solution.

Pricing — Midsize businesses rank reliability and service levels as the top factors that influence aninvestment decision, with pricing playing a less pivotal role. Essentially, as long as pricing is in areasonable band it generally does not drive the investment decision. If a UC solution's pricing fallsoutside of the band, however, the decision process will gather more roadblocks on the way toreceiving approval than it would within a large enterprise. In terms of addressing overall solutioncosts, midsize businesses prefer clear, straightforward, rightsized pricing proposals.

Magic Quadrant

Figure 1. Magic Quadrant for Unified Communications for Midsize Enterprises, North America

those into products and services. Vendors that showthe highest degree of vision listen to and understandbuyers' wants and needs, and can shape or enhancethose with their added vision.

Marketing Strategy: A clear, differentiated set ofmessages consistently communicated throughout theorganization and externalized through the website,advertising, customer programs and positioningstatements.

Sales Strategy: The strategy for selling products thatuses the appropriate network of direct and indirectsales, marketing, service, and communication affiliatesthat extend the scope and depth of market reach,skills, expertise, technologies, services and thecustomer base.

Offering (Product) Strategy: The vendor's approachto product development and delivery that emphasizesdifferentiation, functionality, methodology and featuresets as they map to current and future requirements.

Business Model: The soundness and logic of thevendor's underlying business proposition.

Vertical/Industry Strategy: The vendor's strategyto direct resources, skills and offerings to meet thespecific needs of individual market segments, includingvertical markets.

Innovation: Direct, related, complementary andsynergistic layouts of resources, expertise or capital forinvestment, consolidation, defensive or preemptivepurposes.

Geographic Strategy: The vendor's strategy to directresources, skills and offerings to meet the specificneeds of geographies outside the "home" or nativegeography, either directly or through partners,channels and subsidiaries as appropriate for thatgeography and market.

12/16/2015 Magic Quadrant for Unified Communications for Midsize Enterprises, North America

Vendor Strengths and CautionsAvayaAvaya is a U.S.based, privately held company with headquarters in Santa Clara, California andownership by private equity firms TPG and Silver Lake. Avaya reported 2014 revenue of $4.3 billion andan operating income of $197 million. Avaya offers a range of products targeting specific marketsegments. Avaya IP Office is the platform that Avaya positions in the midmarket, with scalability up to2,500 users.

Avaya IP Office has two versions, the Avaya IP Office Platform for up to 2,000 users across 32 sites andAvaya IP Office Select for up to 2,500 users across 150 sites, both of which can run on a single server.Both platforms support a comprehensive UC suite for voice, video, IM, presence, mobility, UM,audio/videoconferencing and Web conferencing, and desktop integration. IP Office can run inside avirtual machine, on a dedicated server or on an appliance. Avaya IP Office Web Manager is theadministration and support software that comes with IP Office to manage licensing, devices,moves/adds/changes, and ongoing support through a single Web URL. The latest version of Avaya IPOffice is 9.1, which added additional features for security, voice quality monitoring, whiteboarding andgreater conferencing scalability.

Midsize businesses that have an existing investment in Avaya or Nortel telephony should consider IPOffice, because Avaya offers aggressive discounts to upgrade legacy systems with the entire UC suiteas part of the deal. Midsize enterprises whose requirements are for a strong contact center,sophisticated telephony or high security should also evaluate Avaya.

Strengths

Avaya has a comprehensive unified communication and contact center portfolio with a robustfeature set that is well integrated across features. It can meet the needs of midsize businesseswith complex communication requirements and those that want to support a broad range ofendpoints.

Avaya has substantial brand recognition, with a long history of providing telephony in the NorthAmerican market.

Simplification of the IP Office suite enables the quoting, installation and support processes to bestreamlined and less confusing to Avaya's channel partners and customers.

Cautions

In some instances, Gartner client statements of work show that Avaya and its partners chargeabove the industry average for customization and integration into thirdparty applications.

Avaya continues to receive a financial rating of Caution from Gartner because its revenue showsongoing yearoveryear decline. Avaya's margins have increased as it cuts costs to improve

12/16/2015 Magic Quadrant for Unified Communications for Midsize Enterprises, North America

To implement its increased focus on the midmarket, Avaya has undergone midmarket leadership,channel and program enhancements during the past several years. The company now needs tomaintain consistent leadership and midmarket program structures to keep the trust of its channelpartners and ensure that they lead with an Avaya solution.

CiscoCisco is a U.S.based public company with headquarters in San Jose, California. Cisco reported $47.1billion in revenue in 2014, with approximately $3.8 billion coming from its Collaboration division. Ciscowas an early provider of voice over IP (VoIP), because it entered the telephony market without thelegacy time division multiplexing (TDM) customer base that heritage vendors have. Its UC solution isbuilt on its flagship Cisco Unified Communications Manager and brings together IP communications,customer care, conferencing, voice messaging, mobility, presence and IM, telepresence andcollaborationenabled applications.

Cisco has created a bundled solution for the midmarket, called the Business Edition 6000 (BE6000). TheBE6000 bundles the hardware, software and support tools into a single package, which simplifies thequoting, implementation and support processes. Cisco has three BE6000 offerings: the BE6000S for the25 to 150user market, requiring only core UC applications; the BE6000M for up to 1,000 users thathave standard UC requirements; and the BE6000H for up to 1,000 users who have multiple devices andhave robust UC requirements, including the full audio/videoconferencing and Web conferencing suite.Cisco offers integrated SIP trunking, with the Cisco Session Border Controller (SBC) embedded in itsrouter and the voice functionality integrated into the management suite. Cisco is also aggressivelymarketing its Jabber client as an alternative to Microsoft Lync.

Midsize businesses with existing investments in Cisco infrastructure, or those with advanced video oradvanced UC functionality requirements that are not price sensitive, should consider Cisco.

Strengths

Cisco has been successful with the BE6000 solution across the midmarket by bundling thehardware and licensing and offering a full suite of robust UC collaboration capabilities.

Cisco has a significant base of channel partners that sells the entire set of Cisco products. Cisco ispresent in the majority of midmarket enterprises as the network vendor and this relationship canbe leveraged to sell adjacent UC solutions.

Cisco is offering attractive hybrid onpremises and cloud options, through its Hosted CollaborationSolution (HCS), for those enterprises wishing to keep their telephony onpremises and migrateconferencing, IM and other UC services to the cloud. Cisco also has agreements for transferringlicenses from onpremises to hosted environments.

Cautions

While Cisco has made a lot of progress in simplifying its offering through the BE6000 bundle,configuration for advanced capabilities, customization and integration into thirdparty systems canbe complex.

Choosing Cisco as the solesource provider for UC and the data network can lead to reducednegotiating leverage and higher service and maintenance costs.

Cisco is typically priced higher at the low end of the midmarket (organizations with between 100to 499 employees) than its competitors. While Cisco released its BE6000S in December 2014 toaddress this, early indications are that it is still priced about 20% higher than the market averagefor basic UC requirements.

DigiumDigium, the privately owned original developer of the opensource Asterisk software, was founded in1999. Since its inception, Digium, as well as other communications providers, have leveraged Asteriskto build and position opensource communications solutions. Based on the Asterisk platform, Digiumpositions Switchvox, a prepacked, offtheshelf UC solution geared for organizations with fewer than250 employees (although the solution can scale beyond 250). Digium's general Asterisk solution (thetoolset that can be customized to create a UC solution) is not included in this evaluation because it isnot available as an offtheshelf product.

The Switchvox appliance is available in multiple versions to support customers in the segment for lessthan 500 users. The solution provides telephony, audioconferencing, UM, IM/presence, recording, faxand basic Web RealTime Communication (WebRTC)based video capabilities. Digium does not offerWeb conferencing functionality. Administration is done through a browserbased portal hosted on eachSwitchvox appliance and configured through a simple GUI. Switchvox is compatible with standardsbased SIP phones, and Digium offers a range of its own branded phones and supports tight integrationwith thirdparty phones from Polycom and snom technology for specific conferencing or DigitalEnhanced Cordless Telecommunications (DECT) requirements. Digium is transitioning the Switchvoxplatform to run on the newer Asterisk 13 engine, with the launch of the Switchvox 6.0 solutiontentatively slated for early 3Q15. This platform move is expected to enable greater efficiency andplatform stability.

Consider Digium's Switchvox solution if your organization has fewer than 250 employees, is highlypricesensitive and is looking for basic UC functionality.

Strengths

Digium extends all Switchvox capabilities to users as part of the offering. This streamlines the bidprocess, eliminates the need for partners to position potentially complex licensing bundles, and

12/16/2015 Magic Quadrant for Unified Communications for Midsize Enterprises, North America

encourages use of the solution's UC applications across the business.

The Switchvox solution is highly price competitive, with bids frequently coming in at onehalf oronethird the price of competitors' offers.

Digium's Switchvox solution benefits from some of the momentum generated by its opensourceAsterisk. For customized applications (for example emergency notification or alarm systems),Switchvox customers can frequently rely on Asteriskbased developers to create a customextension if desired. Furthermore, solution innovations and a loyal partner community bound byAsterisk help to push the Switchvox solution and its channel partner programs.

Cautions

Switchvox could face challenges in effectively meeting the needs of organizations with more than250 employees. While Switchvox can scale beyond 250 users (on the largest appliance support iscommitted to up to 600 users), it is difficult to estimate the use of functionality (given thateveryone has access to all features) and guarantee adequate service levels beyond a certainthreshold. Switchvox Release 6.0 (slated for early 3Q15) will run on Digium's newer Asterisk 13engine, which will add increased efficiency.

While Switchvox can be configured to run in a virtualized environment, Digium does not yet offersupport in virtualized configurations.

Digium's Switchvox has some functionality limitations that might be an obstacle for organizationswith specific requirements. Switchvox does not offer Web conferencing and currently supports onlylimited videoconferencing capabilities, so organizations desiring these functions will have tointegrate thirdparty solutions.

Interactive IntelligenceInteractive Intelligence is a provider of collaboration, communications and customer engagementsoftware solutions and cloud services. The company was founded in 1994 and had approximately $343million in revenue and just over 2,000 employees in 2014. Interactive Intelligence offers both premisesbased and cloud solutions, with approximately half of the 2014 orders generated from each deliverymodel. The company's headquarters is located in Indianapolis, Indiana, U.S.

Interactive Intelligence positions the Customer Interaction Center (CIC) IP communications softwaresuite as its premisesbased UC solution. The solution includes contact center applications, callprocessing, voice mail, UM, fax server and presence functionality. CIC does not natively support Webconferencing or videoconferencing, so thirdparty solutions must be bridged for full UC functionality.CIC integrates with Microsoft Lync, Microsoft Exchange, IBM and Salesforce for additional functionality.CIC applications can be administered from a single management interface called InteractionAdministrator (IA). This interface can be installed as a desktop application, or can be accessed via aWeb browser. CIC supports a range of mobile clients (Android, BlackBerry, Apple iPhone and iPad) andin 2014 added support for new Polycom and AudioCodes phone models (SIP phone endpoints).

Consider the CIC solution if you are looking for a contactcenterbased UC offering and seeking anoffering with the potential to satisfy custom call processing applications. Additionally, CIC could beconsidered when looking to augment Microsoft Lync with telephony functionality, or considering hybridpremises/cloud implementations.

Strengths

Interactive Intelligence enables flexible deployment approaches including premisesbased, cloudor hybrid delivery options. The company has invested in cloud delivery (it currently has 12 datacenters deployed worldwide) and positions flexible delivery to its user base as organizationalbusiness needs change.

CIC supports tight integration with Microsoft for its collaboration functionality. IT plannerscommitted to Microsoft for certain communications elements can leverage Interactive Intelligencefor contact center and voice capabilities.

Interactive Intelligence's CIC suite uses Web services and provides a common set of applicationdevelopment, management and reporting tools across a range of its applications. Its efficient useof server resources and consistent administrative and management tools across applications makethe system particularly appealing to IT decision makers.

Cautions

Interactive Intelligence has fewer channel support resources than some of its competitors, whichmeans that issues requiring escalation can sometimes take more time to resolve.

Interactive Intelligence's CIC does not provide native Web conferencing or videoconferencingcapabilities, which potentially increases the solution's cost and the complexity of the sales cycle fororganizations desiring these capabilities and needing to consider thirdparty options. CICintegrates with Microsoft Lync for this functionality.

Interactive Intelligence's CIC solution is most costeffective when there are central businessrequirements for contact center capabilities. Organizations not using CIC to support their contactcenter requirements will find the solution, and the prices for its other applications, expensive andmisaligned with their needs.

MicrosoftMicrosoft generated revenue of $86.8 billion in fiscal year 2014. Commercial revenue (including itsLync/Skype for Business UC business) contributed $49.6 billion.

Microsoft positions Lync Server 2013 (Lync was rebranded to "Skype for Business" in 1H15) as itspremisesbased UC offering. Skype for Business, combined with Microsoft Exchange, provides a

12/16/2015 Magic Quadrant for Unified Communications for Midsize Enterprises, North America

complete set of UC features including full conferencing capabilities, IM/presence, email, UM andtelephony functionality. Skype for Business enables mobile device support for Windows Phone, iOS andAndroid clients; BlackBerry devices are not supported. For collaborationenabled conference rooms,Microsoft partners with Smart, Polycom and Crestron for purposebuilt collaboration devices for Skypefor Business and Microsoft Surface Hub. Microsoft also offers Office 365 within a larger Office suiteincluding Skype for Business and Exchange Online, as well as Skype (for consumers); it continues tobridge the gap between Skype for Business and Skype. In December 2014, it added support for videocalling between the (then) Lync clients and Skype.

Consider Skype for Business if you rely on or have significant investments in Microsoft Officeapplications and Exchange for email, and existing enterprise licensing agreements, and have acollaborationcentric workforce. Ensure you have the required IT resources in place to manage theoffering and that Skype for Business's limited telephony capabilities can meet your needs.

Strengths

Skype for Business continues to become more tightly integrated with consumer Skype, enablingthe company to position both businesstobusiness and businesstoconsumer collaborationcapabilities and to further embrace social collaboration.

Microsoft's success with email (Exchange) and other business/desktop applications uniquelypositions it to integrate Skype for Business with business processes and applications that canimpact collaboration and workflows and improve processes.

Microsoft has a wide reach, strong brand recognition and a growing base of certified channelpartners for Skype for Business. It continues to train and certify new channel partners and expandthe UC and voice capabilities of existing partners to grow solution expertise. These brand andchannel certification efforts, together with its installed base of email and desktop users, earns itfrequent consideration in UC bids — even outside of its large enterprise "sweet spot."

Cautions

Implementing Skype for Business Server can be a complex endeavor, which strains the ITresources of most midmarket organizations. Implementations require hardware, software andservices from multiple providers. Most Skype for Business channel partners' position hardwarefrom multiple vendors and obtain software licensing through a separate party. The complexityassociated with licensing, hardware elements and service and support means that Skype forBusiness Server might prove to be too complex for many midsize organizations.

While Microsoft continues to enhance the telephony functionality of Skype for Business, the voiceuser feature set is still not on a par with legacy telephony solutions. Users report the voicereliability can be subpar. IT planners should ensure a proper network evaluation is performed for atelephony implementation. Most deployments of Skype for Business telephony are combined withthe existing PBX, rather than a replacement for it.

Microsoft's main focus is on a servicebased UC approach (Skype for Business Online as part of itsOffice 365 portfolio) for the midmarket, as opposed to a premisesbased approach. This meansthat the architecture and positioning of Skype for Business Server 2015 can be better suited tolarger organizations.

MitelMitel is a global, publicly traded company, with headquarters in Ottawa, Ontario, Canada and annualrevenue of $1.1 billion. Mitel's UC portfolio has a number of products following the merger with Aastrain 2013; however, MiCollab remains its flagship product for UC within North America.

Within North America, Mitel positions MiVoice Business and MiCollab as the complete UCC offering forthe midsize enterprise market. MiVoice Business delivers call control, hot desking and endpoints, andMiCollab delivers the UC functionality that enables collaboration, including the UC client; presence; IM;audio, Web and video collaboration; and UM. The solutions can be deployed in various cloudconfigurations (private cloud, public cloud and hybrid cloud), since all deployment options utilize thesame software stream.

Mitel also positions a combined version in North America, MiVoice Business Express, which supports upto 500 users and features a single virtual appliance composed of MiVoice Business, MiCollab andMiVoice Border Gateway (SBC). Mitel was an early leader in both UC server and client virtualization, andthe solutions support integrated provisioning, administration and maintenance functionality.

Organizations looking for a fully integrated UC solution at an attractive price supporting multisiteconfiguration and flexible cloud options should consider Mitel's MiCollab UC solution.

Strengths

The Mitel MiVoice and MiCollab solutions provide a mature and comprehensive software suite.They are based on a common software architecture that can be distributed, or centralized in adata center. The solutions run on industrystandard servers and are certified on VMwarevirtualized environments. The same solutions are also available as cloud offerings.

Integration flexibility is a core strength of Mitel, whether to thirdparty applications fromcompanies such as Microsoft, Google or Salesforce, or to SIP trunking through its own sessionborder controller that is fully integrated with its product and management suite.

Mitel's channel initiatives (its focus on programs and support for its channel partners) combinedwith its rebranding initiative (the October 2014 rebrand launch) position it to grow its midmarketUC business and reach a broad array of midsize businesses across North America. As part of thechannel changes, partners are rewarded for their credentials and capabilities (including verticalexpertise) instead of only being rewarded for sales volumes.

12/16/2015 Magic Quadrant for Unified Communications for Midsize Enterprises, North America

Mitel's channel partners are familiar with selling and supporting its telephony solutions, but somelack experience in installing and supporting the full UC solution set. Enterprises interested in a fullUC suite should check their partners' certifications, experience and references.

Mitel provides UC licensing bundles that can change regularly, and therefore cause confusion. Mitelcustomers and channel partners need to ensure they understand precisely what is included withtheir license bundle.

Mitel is utilizing a strategy of growth through acquisition and is evaluating making additionalcommunications acquisitions to complement its existing product portfolio and grow its geographicfootprint. This strategy could pose challenges for the company in terms of integrating multipleassets, certifying new partners and developing and supporting multiple solutions with limitedresources.

NECNEC is a global provider of IT services and products with its headquarters in Tokyo, Japan. NEC's 2014revenue was $29.5 billion.

NEC positions two UC platforms for the midmarket: Univerge 3C, a softwarebased solution thatoperates across premises, cloud or hybrid environments; and UC for Enterprise (UCE), which wasinitially positioned in the large enterprise market but now scales down to support users in the 500 to1,000user segment. UC for Business (UCB), utilized on the SV8000 series communications servers, hasbeen retired and replaced with NEC's UCE on the SV9000 series (NEC's softwarebased telephonyplatform). The SV9300 platform is targeted specifically at the midmarket. UCE is primarily a strongtelephony platform with UC features bundled in, while the Univerge 3C is designed for organizationslooking for a full UC software suite.

Midmarket businesses looking to highly customize their UC applications in particular industry segmentswill be attracted to NEC's verticalspecific expertise. NEC targets the education, government,healthcare, hospitality and transportation verticals.

Strengths

NEC has sustained its strength in specific vertical markets, such as hospitality, healthcare,government and education, with standardized solutions. It provides appropriate businessspecificcustomization through its standard Webbased interfaces and its Communication Enabled BusinessProcesses (CEBP)based development platform.

NEC's channel partners report strong support for sales and service. Its channel partners andcustomers benefit from rapid response times when preimplementation or postimplementationissues arise.

All UC features are included in NEC's communication products, which simplifies license bundles.Additionally, there are no extra licensing costs for disaster recovery.

Cautions

NEC's brand recognition for UC in North America is lagging behind that of its competitors. Toincrease mind share in the midmarket, NEC needs to continue advancing its brand recognition andgrowing its midmarket installed base.

Some of NEC's North American channel partners are not certified on Univerge 3C, while othershave extremely limited experience in installing and supporting it. Buyers interested in Univerge 3Cshould ensure they will be working with a partner with the appropriate certifications andexperience.

NEC technology is robust, but, with marketing strategies controlled by personnel based at theheadquarters in Japan, it can be slow to adapt to changing market requirements — such as thosefor virtual and cloud solutions.

ShoreTelShoreTel is a developer of business communications solutions, including corporate IP telephony, UC,mobility and contact center applications. It offers premisesbased functionality through its ShoreTel14.2 platform and hosted telephony through its ShoreTel Sky service. The company reported revenue of$339.8 million for fiscal year 2014.

ShoreTel positions ShoreTel 14 as its premisesbased platform. Its architecture is an appliancebaseddistributed design. The individual appliances operate independently, but are collectively managed andconfigured within a single ShoreTel Director Web application that scales to 20,000 users. The solutionsupports virtualized call control (new with update 14.2). The ShoreTel Director Web administrationapplication is supported on Windows Server and via virtualization with VMware. User administrationintegrates IP telephony, UM, IM, audioconferencing (up to 1,000 ports, plus the ShoreTel CollaborationService Appliance, which supports 200 audio ports), Web conferencing and collaboration (applicationsharing for Windows, iPad and iPhone), video (pointtopoint and pointtothird party) and mobility.

Consider ShoreTel if you have a distributed office environment and are looking for a reliable UC solutionin which ease of use, ease of management and ease of implementation are more important thanbreadth and depth of features.

Strengths

ShoreTel's solution is consistently praised by clients Gartner speaks to for being easy to use, easyto manage and involving a straightforward implementation process. This simplicity aligns with thecapabilities of many ITresourceconstrained midmarket organizations.

12/16/2015 Magic Quadrant for Unified Communications for Midsize Enterprises, North America

ShoreTel is expanding its integration with thirdparty providers to enhance functionality beyond itsportfolio. It interoperates well with Microsoft Lync and is expanding its Innovation Network to offerbetter interoperability for SIP trunking, fax solutions and wallboards. ShoreTel integrates with 70business applications related to CRM, ERP, HR and other functions.

ShoreTel has a strong base of North American channel partners with broad coverage acrossvertical industries. Furthermore, ShoreTel has a solid channel program in place to support itspartner base, utilizing both twotier and nontiered support. ShoreTel's partners report that thecompany is easy to do business with and that both presales and postsales support is favorable —which translates into generally positive response times to enduser inquiries.

Cautions

ShoreTel has been slow to release its new multitenant platform for cloud, premises and hybriddeployments with a common client. The integrated platform continues to take a significant amountof time to bring to market, but is tentatively scheduled for a 3Q15 release. To date, ShoreTel hasextended limited portions of its Sky portfolio to premisesbased ShoreTel customers, includingmobility, fax and UM capabilities.

ShoreTel's UC features will satisfy the functionality requirements of most midsize businesses,especially lower midmarket organizations; however, the ShoreTel solution is not as featurerich assome of its competitors. For example, its conferencing capabilities (video, audio and Web) mightnot meet the requirements for some customized or robust functionality.

ShoreTel has fewer resources (portfolio, human and financial) to leverage than many of itsmidmarket UC competitors. It doesn't have significant pull through from sales of other technology,unlike some of its competitors leveraging networking, software or contact center technology, forexample. Furthermore, its annual product revenue is on a smaller scale (less than $200 million in2014). This means the company has to be careful with resource prioritization.

ToshibaToshiba, based in Tokyo, Japan, is a global provider of electronics products across business andconsumer markets. The company's products include information and communications equipment andsystems, Internetbased solutions and services, electronic components and materials, power systems,industrial and social infrastructure systems, and household appliances. Toshiba's America InformationSystems, Telecommunication Systems Division focuses on business communications solutions for smallor midsize businesses (SMBs). For its 2014 fiscal year, Toshiba reported revenue of ¥6,502.5 billion or$63.2 billion.

Within North America, Toshiba positions IPedge and UCedge in its midmarket UC portfolio. IPedge is anIP telephony solution built on a Linuxbased platform and is available in three versions to support usersof various sizes across the SMB market. The IPedge 1.6.2 release includes external federation withMicrosoft Lync. Conferencing is supported in the IPedge server through the integrated IPedge Meetingsolution, which provides Webbased meetme audio/videoconferencing and Web collaboration, UM andIM/presence. The solution also features Microsoft Outlook calendar integration. UCedge is Toshiba'sclient, supporting Android, iOS, Windows and Mac. All clients are interoperable via the ExtensibleMessaging and Presence Protocol (XMPP) and synchronized via the cloud (Google Drive), includingcontacts, presence and IM.

Consider Toshiba if you are looking for a reliable, more telephonycentric offering geared to smallerenvironments — specifically the small business or the smaller end of the midmarket range.

Strengths

Toshiba's customers and partners consistently report that its solutions are generally reliable andinclude the features most lowend midsize businesses desire, or use, to support their businesscommunications.

Toshiba sells exclusively through its authorized Toshiba dealers and does not compete directlywith its partners. Channel partners report a high level of support from Toshiba and display aboveaverage loyalty to the company. Toshiba's National Accounts Program and Government AccountsProgram provide consistent presales and product support to its partner community, resulting infavorable partner response times (and favorable customer support) when support needs arise.

Toshiba's position in the consumer and electronics areas as a large provider of laptops and TVshelps the company with brand recognition and leverage in North America. Furthermore, significantfinancial backing from the global corporation helps to boost its credibility in some UC bids.

Cautions

Toshiba is not known for having premium phones or the most leadingedge, fullyfeatured UCsolutions. Its portfolio includes much of the functionality businesses require, but might not meetsome organizations' needs for more robust collaboration capabilities.

Toshiba and its channel partners have more experience in providing solutions to the smallbusiness and lowend midmarket segments. Certain limitations may exist for organizationsrequiring full UC functionality in the upper midmarket segment.

Toshiba's UCedge solution is relatively new (released during September 2014), and is in the earlystages of use. Toshiba and some channel partners may have limited experience in supporting thissolution, and Gartner has had limited feedback about it.

UnifyUnify (formerly Siemens Enterprise Communications), headquartered in Munich, Germany, is a privatelyowned joint venture between private investor The Gores Group and Siemens. Unify's 2014 revenue was$2.4 billion.

12/16/2015 Magic Quadrant for Unified Communications for Midsize Enterprises, North America

Unify's UC platform is OpenScape, with preconfigured applications for UC, contact center, sessionborder controller and management. OpenScape comes in two flavors for the midmarket: OpenScapeBusiness for the lower midmarket (100 to 500 users) and OpenScape Enterprise Express for the uppermidmarket (500 to 1,000 users). Both solutions provide voice, messaging, audioconferencing and Webconferencing, mobility, contact center, security and management applications. OpenScape Businesslacks native videoconferencing support, but supports video between Unify's OpenStage SIP phones orwhen used with OpenScape Web Collaboration, while OpenScape Enterprise Express supports video.

Although Unify's communication and collaboration solution, Circuit, is not explicitly evaluated in thisresearch (the solution is cloudbased), Gartner expects some elements of Circuit to be integrated intoUnify's premisesbased platforms during the second half of 2015.

Consider the OpenScape UC suite if your company is looking for a standardsbased, costeffective UCsoftware suite that can be extended as needed via integration with third parties.

Strengths

Unify offers vertical solutions for specific industry segments. For instance, OpenScape Xpert istargeted at financial services organizations and includes trading turrets. Unify has increased itsfocus on the healthcare, government (federal, state and local), higher education,manufacturing/automotive and finance/banking verticals.

OpenScape Business is costeffective, supports flexible configurations and comes with most of thefunctionality that midmarket enterprises require.

Circuit provides Unify with an emerging nextgeneration teamwork and collaboration story thatcan be leveraged to grow interest and excitement around the Unify brand and its premisesbasedOpenScape Business.

Cautions

Unify lacks strong visibility in the North American market and is still filling out its channel partnernetwork in this market — adding or renewing 47 strategic partnerships since January 2015. Unifywill have to improve its market awareness to be successful in the highly competitive NorthAmerican market.

During the past year, Unify has undertaken significant management and gotomarket changes.Unify has a relatively new senior executive team, which has announced that the company willundergo significant reductions in staff as it transforms into a software and services company. Itwill take time to complete these changes, which could disrupt the company's execution of itsstrategy.

While continuing to enhance its existing OpenScape portfolio, Unify is placing significant emphasison Circuit. The market demand and adoption of Circuit has yet to be determined.

Vendors Added and DroppedWe review and adjust our inclusion criteria for Magic Quadrants and MarketScopes as markets change.As a result of these adjustments, the mix of vendors in any Magic Quadrant or MarketScope maychange over time. A vendor's appearance in a Magic Quadrant or MarketScope one year and not thenext does not necessarily indicate that we have changed our opinion of that vendor. It may be areflection of a change in the market and, therefore, changed evaluation criteria, or of a change of focusby that vendor.

AddedThis is the first version of this Magic Quadrant, so all providers are new.

DroppedThis is the first version of this Magic Quadrant, so no providers have been dropped.

Inclusion and Exclusion CriteriaTo be included in this Magic Quadrant, solution providers must meet the following criteria:

Offer an onpremises unified solution that includes all of the following six UC areas either nativelyor through a partner: (1) telephony; (2) conferencing (audio, video and Web); (3) messaging(which can be offered via integration with email, voice mail and various forms of UM); (4)presence and IM; (5) clients for multiple environments; and (6) the ability to supportcommunicationsenabled applications.

The ability to integrate UC functions into a complete solution (can involve thirdparty products)and presented via a consistent interface.

The ability to generate significant interest in the midmarket (100 to 999employee) segment.

An offering that has significant market presence (defined as market share, differentiatinginnovation, and/or mind share) in North America.

Demonstrable UC for midmarket portfolio/products with references.

Evaluation CriteriaAbility to ExecuteGartner analysts evaluate UC product providers based on the quality, efficacy and overall maturity ofthe solutions, systems, tools and procedures that enhance individual, group and midsize enterprisecommunications. Ultimately, UC providers are rated on their ability and success in capitalizing on their

12/16/2015 Magic Quadrant for Unified Communications for Midsize Enterprises, North America

Product/Service: Core goods and services offered by the vendor for the midmarket. Thisincludes current product capabilities, quality, feature sets, skills and so on, whether offerednatively or through OEM agreements/partnerships as defined in the market definition and detailedin the subcriteria.

Overall Viability: Viability includes an assessment of the overall organization's financial health,the financial and practical success of the business unit, and the likelihood that the individualbusiness unit will continue investing in the product, will continue offering the product and willadvance the state of the art within the organization's portfolio of products.

Sales Execution/Pricing: The vendor's capabilities in all presales activities and the structurethat supports them. This includes deal management, ease of positioning UC licenses, competitivepricing and negotiation, presales support, and the overall effectiveness of the sales channel.

Market Responsiveness/Record: Ability to respond, change direction, be flexible and achievecompetitive success as opportunities develop, competitors act, customer needs evolve and marketdynamics change. This criterion also considers the vendor's history of responsiveness.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliverthe organization's message to influence the midmarket, promote the brand and business, increaseawareness of the products, and establish a positive identification with the product/brand andorganization in the minds of buyers. This mind share can be driven by a combination of publicity,promotional initiatives, thought leadership, word of mouth and sales activities.

Customer Experience: Relationships, products and services/programs that enable clients to besuccessful with the products evaluated. Specifically, this includes the ways customers receivetechnical support or account support. This can also include ancillary tools, customer supportprograms (and the quality thereof), availability of user groups, servicelevel agreements and soon.

Operations: The ability of the organization to meet its goals and commitments. Factors includethe quality of the organizational structure, including skills, experiences, programs, systems andother vehicles that enable the organization to operate effectively and efficiently on an ongoingbasis in the midsize enterprise UC market.

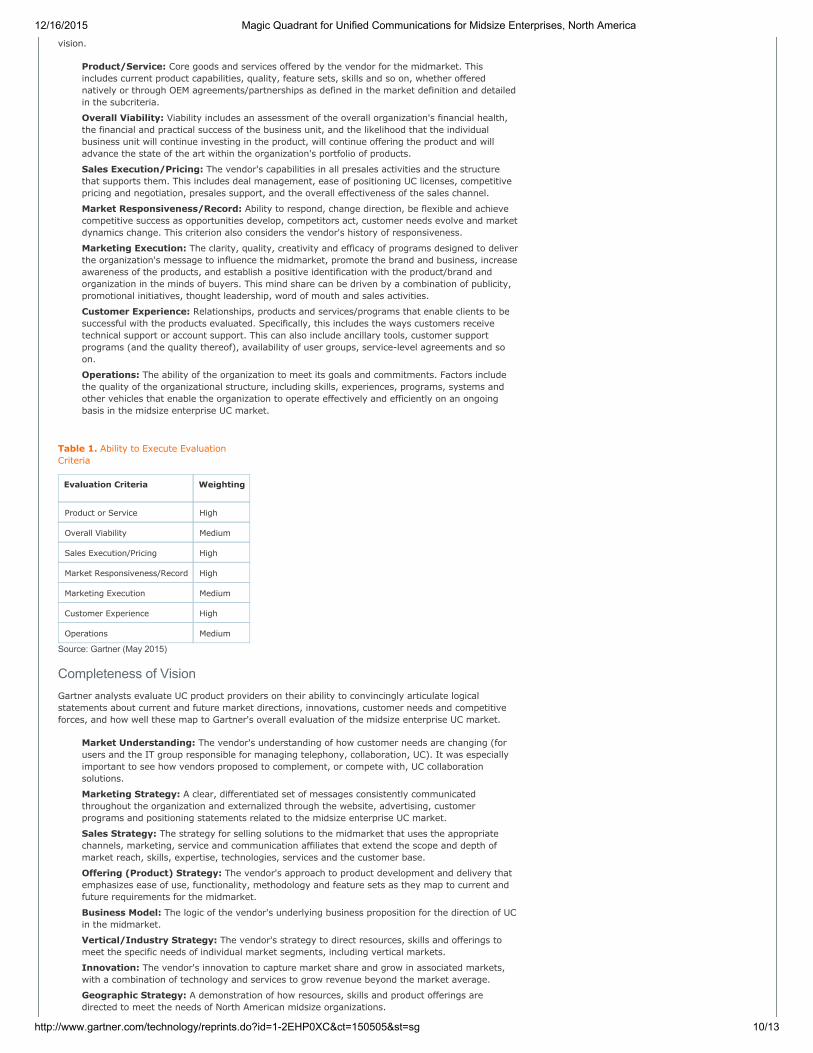

Table 1. Ability to Execute EvaluationCriteria

Evaluation Criteria Weighting

Product or Service High

Overall Viability Medium

Sales Execution/Pricing High

Market Responsiveness/Record High

Marketing Execution Medium

Customer Experience High

Operations Medium

Source: Gartner (May 2015)

Completeness of VisionGartner analysts evaluate UC product providers on their ability to convincingly articulate logicalstatements about current and future market directions, innovations, customer needs and competitiveforces, and how well these map to Gartner's overall evaluation of the midsize enterprise UC market.

Market Understanding: The vendor's understanding of how customer needs are changing (forusers and the IT group responsible for managing telephony, collaboration, UC). It was especiallyimportant to see how vendors proposed to complement, or compete with, UC collaborationsolutions.

Marketing Strategy: A clear, differentiated set of messages consistently communicatedthroughout the organization and externalized through the website, advertising, customerprograms and positioning statements related to the midsize enterprise UC market.

Sales Strategy: The strategy for selling solutions to the midmarket that uses the appropriatechannels, marketing, service and communication affiliates that extend the scope and depth ofmarket reach, skills, expertise, technologies, services and the customer base.

Offering (Product) Strategy: The vendor's approach to product development and delivery thatemphasizes ease of use, functionality, methodology and feature sets as they map to current andfuture requirements for the midmarket.

Business Model: The logic of the vendor's underlying business proposition for the direction of UCin the midmarket.

Vertical/Industry Strategy: The vendor's strategy to direct resources, skills and offerings tomeet the specific needs of individual market segments, including vertical markets.

Innovation: The vendor's innovation to capture market share and grow in associated markets,with a combination of technology and services to grow revenue beyond the market average.

Geographic Strategy: A demonstration of how resources, skills and product offerings aredirected to meet the needs of North American midsize organizations.

12/16/2015 Magic Quadrant for Unified Communications for Midsize Enterprises, North America

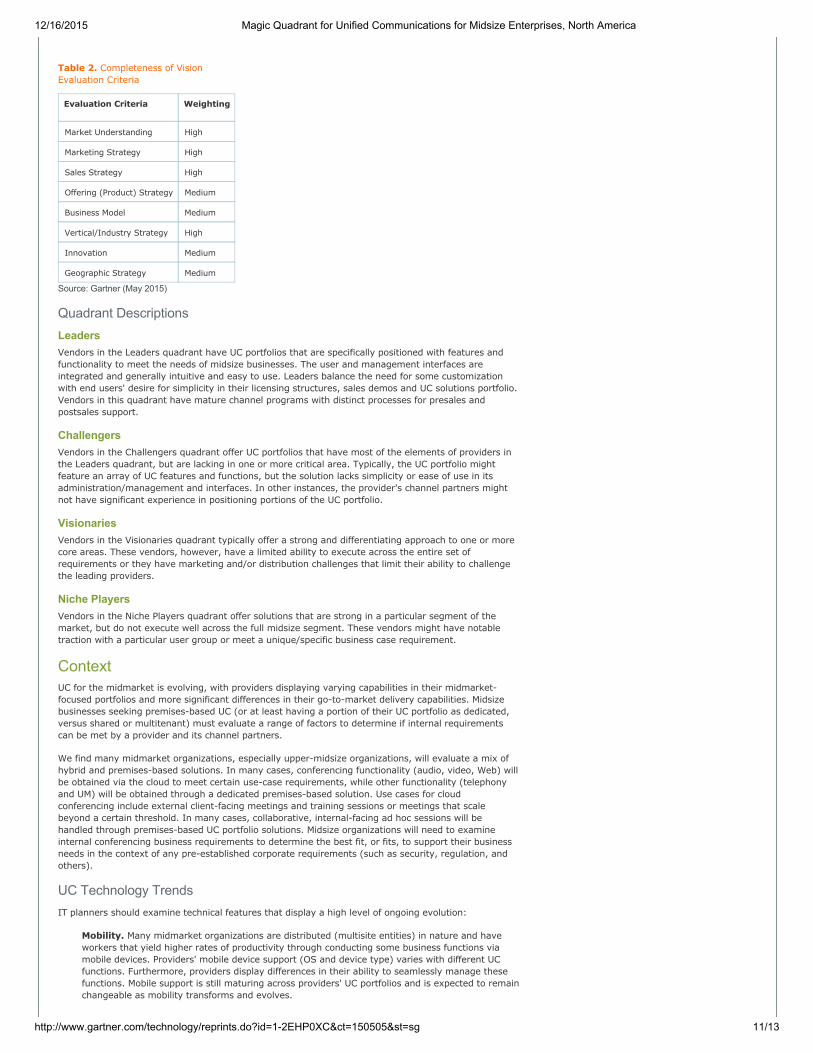

Table 2. Completeness of VisionEvaluation Criteria

Evaluation Criteria Weighting

Market Understanding High

Marketing Strategy High

Sales Strategy High

Offering (Product) Strategy Medium

Business Model Medium

Vertical/Industry Strategy High

Innovation Medium

Geographic Strategy Medium

Source: Gartner (May 2015)

Quadrant DescriptionsLeadersVendors in the Leaders quadrant have UC portfolios that are specifically positioned with features andfunctionality to meet the needs of midsize businesses. The user and management interfaces areintegrated and generally intuitive and easy to use. Leaders balance the need for some customizationwith end users' desire for simplicity in their licensing structures, sales demos and UC solutions portfolio.Vendors in this quadrant have mature channel programs with distinct processes for presales andpostsales support.

ChallengersVendors in the Challengers quadrant offer UC portfolios that have most of the elements of providers inthe Leaders quadrant, but are lacking in one or more critical area. Typically, the UC portfolio mightfeature an array of UC features and functions, but the solution lacks simplicity or ease of use in itsadministration/management and interfaces. In other instances, the provider's channel partners mightnot have significant experience in positioning portions of the UC portfolio.

VisionariesVendors in the Visionaries quadrant typically offer a strong and differentiating approach to one or morecore areas. These vendors, however, have a limited ability to execute across the entire set ofrequirements or they have marketing and/or distribution challenges that limit their ability to challengethe leading providers.

Niche PlayersVendors in the Niche Players quadrant offer solutions that are strong in a particular segment of themarket, but do not execute well across the full midsize segment. These vendors might have notabletraction with a particular user group or meet a unique/specific business case requirement.

ContextUC for the midmarket is evolving, with providers displaying varying capabilities in their midmarketfocused portfolios and more significant differences in their gotomarket delivery capabilities. Midsizebusinesses seeking premisesbased UC (or at least having a portion of their UC portfolio as dedicated,versus shared or multitenant) must evaluate a range of factors to determine if internal requirementscan be met by a provider and its channel partners.

We find many midmarket organizations, especially uppermidsize organizations, will evaluate a mix ofhybrid and premisesbased solutions. In many cases, conferencing functionality (audio, video, Web) willbe obtained via the cloud to meet certain usecase requirements, while other functionality (telephonyand UM) will be obtained through a dedicated premisesbased solution. Use cases for cloudconferencing include external clientfacing meetings and training sessions or meetings that scalebeyond a certain threshold. In many cases, collaborative, internalfacing ad hoc sessions will behandled through premisesbased UC portfolio solutions. Midsize organizations will need to examineinternal conferencing business requirements to determine the best fit, or fits, to support their businessneeds in the context of any preestablished corporate requirements (such as security, regulation, andothers).

UC Technology TrendsIT planners should examine technical features that display a high level of ongoing evolution:

Mobility. Many midmarket organizations are distributed (multisite entities) in nature and haveworkers that yield higher rates of productivity through conducting some business functions viamobile devices. Providers' mobile device support (OS and device type) varies with different UCfunctions. Furthermore, providers display differences in their ability to seamlessly manage thesefunctions. Mobile support is still maturing across providers' UC portfolios and is expected to remainchangeable as mobility transforms and evolves.

12/16/2015 Magic Quadrant for Unified Communications for Midsize Enterprises, North America

WebRTC. Some providers, especially those without significant legacy investments in conferencingplatforms, are leveraging WebRTC for their conferencing functionality. The protocol is still in itsearly stages of development and therefore at the mercy of, and subject to, ongoing developments.As the protocol evolves, we expect greater use of WebRTC in enterprise conferencing functionality.In the near term, however, IT planners should ensure conferencing functionality meets therequirements to support their business activities.

UC solution administration and management. UC solutions are at varying stages of functionalintegration. Some elements of UC suites are tightly integrated with consolidated servers,administration tools and consistent user interfaces. Others display limited integration and createadditional complexity in terms of configuration, administration and management.

Delivery CapabilitiesIT planners should focus evaluation efforts on providers' midmarket delivery capabilities. Most providersin this evaluation sell to the midmarket exclusively through their channel partners. Some providersdisplay expertise in positioning and delivering solutions to a particular segment within the midmarket,while other providers have broad delivery capabilities with experienced channel partners selling andsupporting UC solutions across the entire midmarket. In some cases, solutions that were designed forvery small businesses might lack specific capabilities or channel partners with expertise in supportinglarger environments. Conversely, certain providers with longstanding expertise in large enterprisemarkets could face challenges meeting the requirements for straightforward, easytouse, integratedsolutions that channel partners can easily support in the midmarket. Successful providers balance theright mix of UC features and functionality against cost and complexity and have bestinclass channelprograms in place to support presales and postsales initiatives.

IT planners should consider several nonUC productspecific elements as part of their UC solutionevaluation:

Expertise of the partner/provider in installing the UC solution:Experience positioning the solution in organizations of similar size?

Appropriate certifications required to sell, install and support all elements of the solution?

Determine partner status — gold, platinum or premium — to ensure adequate responsetimes will be delivered by the provider to the partner to meet the requirements for highertiers of support.

Evaluate UC solution provider:Favorable Net Promoter Scores (NPS)?

Strong support and channel programs in place to support its solutions and channel partners?

Proven track record of delivering solutions in the midsize enterprise market segment?

Market OverviewLeaders

Providers in the Leaders quadrant — Cisco, Mitel, Avaya and ShoreTel — receive frequent considerationfrom midsize businesses evaluating UC solutions. These providers have features and functionalitydesigned to specifically meet the needs of most midsize businesses. Cisco displays a robust midmarketUC feature set, but displays a higher level of complexity in some of its positioning. ShoreTel excels inpositioning a solution with most of the functionality that most midsize businesses require, along withintuitive interfaces and easytoimplement appliances that are backed by experienced midmarketchannel partners. However, certain features are not as robust with ShoreTel as with other providers inthe Leaders quadrant. Mitel has a partner ecosystem and solution set that is wellsuited to midmarketorganizations, with growing expertise in seamless migration of customers to UC. Avaya continues toenhance and scale its midmarket portfolio, but faces challenges in receiving consideration fromnonlegacy Avaya prospects.

Challengers

NEC appears in the Challengers quadrant position with its softwarebased 3C solution set. 3C providesfunctionality suitable for most midmarket organizations, but NEC lacks a base of widespread NorthAmerican partners with significant expertise in positioning and supporting the solution to enablewidescale execution.

Visionaries

Microsoft and Unify appear in the Visionary quadrant. Microsoft has the potential to disrupt the marketwith its Lync offering, but the company hasn't broadly packaged Lync (phones, gateways, licenses) in away that meets most midsize organizations' needs for an easytoimplement, easytomanage solutionset that is positioned with straightforward pricing. Furthermore, Lync's telephony functionality is stillmaturing. Unify competes in the midmarket with its OpenScape Business and OpenScape Enterprisesolution sets. The company has undergone transitions with rebranding (renamed in 2H13), and hasexperienced organizational leadership changes followed by shifts and promotions in its North Americangotomarket channel strategies. Unify's solutions provide the features and functionality that mostmidsize organizations desire, but the organization lacks demonstrated execution in the North AmericanUC midmarket segment.

Niche Players

Providers in the Niche Players quadrant — Digium, Toshiba and Interactive Intelligence — displaystrengths in specific UC areas for the midmarket, but do not execute well across all areas. Interactive

12/16/2015 Magic Quadrant for Unified Communications for Midsize Enterprises, North America

Intelligence has traction with organizations requiring contact center functionality, but lacks someconferencing capabilities and lags behind in pricing and broader support to its channel partners. Toshibaexcels in meeting the needs of many lower midmarket organizations, but its UCedge collaborationsolution is in the early stages of adoption — with many partners lacking experience in positioning andsupporting the solution. Digium is noted for offering a solution that is packaged well for the smallbusiness market (integrated with functional licenses extended to all users across the organization) andpriced well for highly pricesensitive users; however, the solution lacks some native conferencingfunctionality and features some scalability limitations.