56

Maintenance Accounting Framework NATIONAL IMMOVABLE ASSET MAINTENANCE MANAGEMENT for immovable assets

Maintenance Accounting Framework

NATIONAL IMMOVABLE ASSET MAINTENANCE MANAGEMENT

for immovable assets

Maintenance accounting FraMework for immovable assets

Table of Contents

Maintenance accounting FraMework for immovable assets

PART A: PURPOSE, DEFINITIONS AND SCOPE 1

1. PURPOSE OF THIS FRAMEWORK 2

2. TERMS, DEFINITIONS AND ACRONYMS 2 2.1 Terms and definitions 2 2.2 Acronyms 8

3. SCOPE 8 3.1 Functional scope 8 3.2 Application of this Maintenance

Accounting Framework 9 3.3 Normative references 9 3.4 Limitations of this maintenance

accounting framework 10

4. BUILDING BLOCKS FOR THE MAINTENANCE ACCOUNTING FRAMEWORK 10

4.1 Standard Chart of Accounts (SCOA) 10 4.2 Asset hierarchy 11 4.3 Fair value basis of measurement of assets 12 4.4 Depreciated replacement cost methodology 12 4.5 Costing of maintenance activities 14

PART B: MAINTENANCE ACCOUNTING PROCESSES 16

5. ASSET RECOGNITION 17

6. ASSET MEASUREMENT 17 6.1 Initial measurement 17 6.2 Subsequent measurement 18

7. TREATMENT SUBSEQUENT TO INITIAL RECOGNITION 19 7.1 Treatment of expenditure subsequent

to initial recognition 19 7.2 Depreciation 21 7.3 Impairment testing, measurement and

recording 23 7.4 Reversal of impairment transactions 25

8. PLANNING AND BUDGETING FOR MAINTENANCE AND RENEWAL 26 8.1 Costing maintenance activities:

key principles 26 8.2 Maintenance prioritisation and

deferred maintenance 26

9. TRANSACTING AND RECORDING OF MAINTENANCE AND RENEWAL EXPENDITURES 27

9.1 Supply chain management 27 9.2 SCOA principles and recording of transactions 27

10. REPORTING ON ASSET CARE TRANSACTIONS AND OTHER MATERIAL EVENTS 27

10.1 Reporting for purposes of the Annual Financial Statements 27

10.2 Monitoring and evaluation of asset care at boardroom level 28

ANNEXURES 30

Annexure A: An example of determining the cost of immovable assets 30

Annexure B: An example of a shadow valuation 31

Annexure C: Examples of various depreciation methods 34

Annexure D: Examples of disclosures in the Annual Financial Statements 35• StatementsofFinancialPositionandFinancial

Performance • NotestotheAnnualFinancialStatements

Annexure E: Examples of ratio analysis for monitoring and evaluation 39• Assetconsumptionratio:• Assetsustainabilityratio• Assetrenewalfundingratio• %ofPPEandintangibleassetsimpaired• Repairsandmaintenanceasapercentage

of current replacement cost

Annexure F: SCOA examples 41

Annexure G: Illustrative examples of asset accounting transactions 43• Capitalisation • Recognition • Impairment • De-recognitionofanasset• Revaluationofanasset

Maintenance accounting FraMework for immovable assets1

PART A:

PURPOSE,DEFINITIONSANDSCOPE

2Maintenance accounting FraMework for immovable assets

1. PURPOSEOFTHISFRAMEWORK

This National Immovable Asset Maintenance Management Accounting Framework compliments the National Immovable Maintenance Management Standard. The principles of this framework are applicable to the accounting treatment and financial practices relating to the maintenance and renewal of all forms of public sector immovable assets. Notwithstanding this, the specific application of the framework is limited to assets under the custodianship of national and provincial government.

The overarching objective of this accounting framework is the establishment and effective functioning of a system of accounting that fairly presents the value, level of consumption, and current and future asset care needs of immovable asset portfolios. Specific objectives of this Framework include:

a. Describing of the scope of the accounting framework as it applies to immovable assets;b. The adoption of a suitable measurement basis for each accounting group of assets that fairly reflects the value vested in

immovable assets;d. Determining future asset renewal needs, and to adequately provide for future renewal funding needs through depreciation

charges; ande. Ensuring adherence to established principles of accounting with respect to the recognition of assets, measurement and

subsequent treatment of expenditure.

2. TERMS, DEFINITIONS AND ACRONYMS

2.1 TERMS AND DEFINITIONS

Terms employed in this Standard have the meanings as defined below:

TERM DESCRIPTIONAsset A resource owned or controlled by an entity as a result of past events and from which

future economic benefits or service potential are expected to flow to the entity.Asset hierarchy (IIMM) A framework for segmenting an asset base into appropriate classifications. The asset

hierarchy can be based on asset function; asset type or a combination of the two.Asset life (ISO 55000) Periodfromassetcreationtoassetend-of-life.Asset management (LGIAMG) Theprocessofdecision-making,planningandcontrolovertheacquisition,use,

safeguarding and disposal of assets to maximise their service delivery potential and benefits, and to minimise their related risks and costs over their entire life.

Asset Management Information System (LGIAMG)

A combination of processes, data and software applied to provide outputs required for effective asset management.

Asset management plan A documented plan developed for the management of one or a portfolio of assets thatcombinesmulti-disciplinarymanagementtechniques(includingtechnicalandfinancial)overthelifecycleoftheassetinthemostcost-effectivemannertoprovideaspecified level of service. The plan specifies approaches, programmes, projects, activities, resources, responsibilities and timeframes across the lifecycle of the asset(s) planned for, or over a timeframe appropriate for robust lifecycle planning. A significant component oftheplanisalong-termcashflowprojection.

Asset management objectives (IIMM)

Specific outcomes required from the implementation of the asset management framework.

Asset management practices (IIMM)

The asset management processes and techniques that an organisation undertakes, such as demand forecasting, developing and monitoring levels of service and risk management.

Asset management strategy (IIMM)

Thehighlevellong-termapproachtoassetmanagementincludingassetmanagementaction plans and objectives for managing the assets.

3Maintenance accounting FraMework for immovable assets

TERM DESCRIPTIONAsset management system (ISO 55000)

A management system for whose function is to establish the asset management policy and asset management objectives, as well as processes and organisational arrangements inclusive of structure, roles and responsibilities to achieve asset management objectives.

Asset register (LGIAMG) A record of asset information considered worthy of separate identification for both asset accounting and management purposes including inventory, historical, financial, condition and construction, technical and financial information about each.Note: the unit of account in an asset register is a component (see definition of a component).

Asset system (ISO 55000) Set of assets that interact or are interrelated.Asset type (ISO 55000) Grouping of assets having common characteristics that distinguish those assets as a

group or class.Audit (ISO 55000) Systematic, independent and documented process for obtaining audit evidence and

evaluating it objectively to determine the extent to which the audit criteria are fulfilled.Capacity (IIMM) Maximum output that can be produced or delivered using existing network or

infrastructure.Capital (financial concept of) Net assets of an organisation.Capital (physical concept thereof)

The productive capacity of an organisation as measured in depreciated replacement cost.

Capital expenditure Expenditure used to create new assets, increase the capacity of existing assets beyond their original design capacity or service potential, or to returns the service potential oftheassetorexpectedusefullifeoftheassettothatwhichithadoriginally.CAPEXincreases the value of capital asset stock.

Carrying amount (GRAP) The amount at which an asset is recognised after deducting any accumulated depreciation and accumulated impairment losses.

Capital upgrading Enhances the service potential of the asset or the economic benefits that can be obtained from use of the asset and may also increase the life of the asset beyond that initially expected.

Cash-generating assets (GRAP) Assets held with the primary objective of generating a commercial return.Change in accounting estimate (GRAP)

Is an adjustment of the carrying amount of an asset or a liability, or the amount of the periodic consumption of an asset, that results from the assessment of the present status of, and expected future benefits and obligations associated with, assets and liabilities. Changes in accounting estimates result from new information or new developments and, accordingly, are not corrections of errors.

Class of assets (GRAP) Is a grouping of assets of a similar nature or function in an entity’s operations that is shown as a single item for the purpose of disclosure in the financial statements.

Component (IIMM) A component (Note 1) is a specific part of a complex item (Note 2) that has independent physical or functional identity and specific attributes such as different life expectancy, maintenance and renewal requirements and regimes, risk or criticality.Note 1: A component is separately recognised and measured (valued) in the organisation’s asset register as an unique asset record, in accordance with the requirementsofGRAP17tocomponentiseassets.Note 2: A complex item is one that can be disaggregated into significant components. Infrastructure and buildings are considered complex items.

Competence (ISO 55000) The ability to apply knowledge and skills to achieve intended results.Condition (IIMM) The physical state of the asset.Condition assessment or condition monitoring (IIMM)

The inspection, assessment, measurement and interpretation of the resultant data, to indicate the condition of a specific component so as to determine the need for some preventive or remedial action.

4Maintenance accounting FraMework for immovable assets

TERM DESCRIPTIONConformity (ISO 55 000) Fulfilment of a requirement.Continual improvement (ISO 55 000)

Recurring activity to enhance performance.

Corrective maintenance Maintenance carried out after a failure has occurred and intended to restore an item to a state in which it can perform its required function. Corrective maintenance can be planned or unplanned. Refer to Appendix A.

Critical assets (IIMM) Those assets that are likely to result in a more significant financial, environmental and social cost in terms of impact on organisational objectives and service delivery.

Current replacement cost (IIMM)

The cost the entity would incur to acquire the asset on the reporting date. The cost is measured by reference to the lowest cost at which the gross future economic benefits could be obtained in the normal course of business or the minimum it would cost, to replace the existing asset with a new modern equivalent asset (not a second hand one) with the same economic benefits (gross service potential) allowing for any differences in the quantity and quality of output and in operating costs.

Decommissioning (IIMM) Actions required to take an asset out of service.Deferred Maintenance The portion of planned maintenance work necessary to maintain the service potential of

an asset that has not been undertaken in the period in which such work was scheduled to be undertaken.

Depreciable amount (GRAP) The cost of an asset, or other amount substituted for cost, less its residual value.Depreciated replacement cost (IIMM)

The replacement cost of an asset less accumulated depreciation calculated on the basis of such cost to reflect the already consumed or expired economic benefits of the asset.

Depreciation (GRAP) Depreciation is the systematic allocation of the depreciable amount of an asset over its useful life.

Disposal (IIMM) Actions necessary to decommission and dispose of assets that are no longer required.Economic life (IIMM) The period from the acquisition of the asset to the time when the asset, while physically

able to provide a service, ceases to be the lowest cost alternative to satisfy a particular level of service. The economic life is at the maximum when equal to the physical life, however obsolescence will often ensure that the economic life is less than the physical life.

Exchange transactions (GRAP) Transactions in which one entity receives assets or services, or has liabilities extinguished, and directly gives approximately equal value (primarily in the form of cash, goods, services, or use of assets) to another entity in exchange.

Facility (IIMM) A complex comprising many assets (e.g. a hospital, water treatment plant, recreation complex, etc.) which represents a single management unit for financial, operational, maintenance or other purposes.

Failure Modes, Effects and Criticality Analysis (IIMM)

Asystematic,logicalrisk-basedmaintenanceapproachaimedatmaximisingthereliabilityof plant and equipment assets.

Fair value (GRAP) The amount for which an asset could be exchanged, or a liability settled, between knowledgeable, willing parties in an arm’s length transaction.

Incident (ISO 55 000) Unplannedeventoroccurrenceresultingindamageorotherloss.Life (LGIAMG) A measure of the anticipated life of an asset or component; such as time, number of

cycles, distance intervals etc.Impairment loss (GRAP) Animpairmentlossofacash-generatingassetistheamountbywhichthecarrying

amount of an asset exceeds its recoverable amount.Impairment loss of a non-cash-generating asset (GRAP)

Is the amount by which the carrying amount of an asset exceeds its recoverable service amount.

5Maintenance accounting FraMework for immovable assets

TERM DESCRIPTIONInfrastructure assets (LGIAMG) Stationary systems forming a network and serving whole communities, where the

system as a whole is intended to be maintained indefinitely at a particular level of service potential by the continuing replacement and refurbishment of its components.

Incident (ISO 55000) Unplannedeventoroccurrenceresultingindamageorotherloss.Inventories (GRAP) Inventories are assets: (a) in the form of materials or supplies to be consumed in

the production process; (b) in the form of materials or supplies to be consumed or distributed in the rendering of services; (c) held for sale or distribution in the ordinary course of operations; or (d) in the process of production for sale or distribution.

Level of service (IIMM) Levels of service statements describe the outputs or objectives an organisation or activity intends to deliver to customers.

Life (of an asset) The period over which benefits are derived from the use or availability of an asset.Lifecycle (IIMM) The time interval that commences with the identification of the need for an asset and

terminates with the decommissioning of the asset or any liabilities thereafter.Lifecycle asset management Encompasses all asset management strategies and practices associated with an asset

or group of assets that results in the lowest lifecycle cost necessary to achieve stated service requirements within acceptable risk parameters.

Lifecycle cost (IIMM) The total cost of an asset throughout its life including planning, design, construction, acquisition, operation, maintenance, renewal and disposal costs.

Maintenance All actions, planned and unplanned, intended to ensure that an asset performs a required function to a specific performance standard(s) over its expected useful life by keeping it in as near as practicable to its original condition, including regular recurring activities to keep the asset operating, but specifically excluding renewal. Note: Maintenance also specifically excludes restoring the condition or performance of an asset following a recognised impairment event, which would be classified as either renewal or upgrading, depending on the circumstances.

Maintenance of capital Expenditure to ensure that the productive or operating capacity of the asset base is maintained over time. The value vested in capital assets is maintained when the organisation has at least as much capital at the end of the period as it had at the beginning thereof.

Maintenance expenditure Recurrent expenditure as required to ensure that the asset achieves its intended useful life. Maintenance is funded through the organisation’s operating budget, and such expenditureisexpensedintheorganisation’sStatementofFinancialPerformance.

Maintenance plan (LGIAMG) Describes the planned and unplanned maintenance actions for an asset, facility or portfolio of assets, with intended delivery methods and schedules, budget requirements and responsible parties.

Maintenance objectives (IIMM) Objectives for what maintenance has to achieve to ensure the assets are in the right condition to meet the needs of the organisation. Maintenance performance measures and targets are the means of assessing whether the maintenance objectives are being met.

Maintenance standards (LGIAMG)

The standards set for the maintenance service, usually contained in preventive maintenance schedules, operation and maintenance manuals, codes of practice, estimating criteria, statutory regulations and mandatory requirements, in accordance with maintenance quality objectives.

Maintenance strategy (IIMM) Identifies the tactics and tools that will be used to deliver the maintenance plan, as well as defining the maintenance roles and responsibilities.

Material (GRAP) Omissions or misstatements of items are material if they could, individually or collectively, influence the decisions or assessments of users made on the basis of the financial statements. Materiality depends on the nature or size of the omission or misstatement judged in the surrounding circumstances. The size of the information item, or a combination of both, could be the determining factor.

6Maintenance accounting FraMework for immovable assets

TERM DESCRIPTIONModern equivalent asset (IIMM) Themostcost-efficientassetcurrentlyavailablethatwillprovideequivalentfunctionality

to the asset that will be replaced (or are currently being valued using the DRC methodology).

Monitoring (ISO 55000) Determining the status of a system, a process or an activity.Non-cash-generating assets (GRAP)

Assetsotherthancash-generatingassets.

Non-exchange transactions (GRAP)

Transactionsthatarenotexchangetransactions.Inanon-exchangetransaction,anentity either receives value from another entity without directly giving approximately equal value in exchange, or gives value to another entity without directly receiving approximately equal value in exchange.

Objective (Adjusted from ISO 55000)

Result to be achieved at strategic, tactical or operational level. Objectives can be set in a variety of domains or outcome areas (e.g. economic, social or environmental outcomes), or can relate to elements of the organisation (e.g. corporate or units in the organisation), or can relate to processes, services, products, programmes and projects.

Obsolescence (Optimised Decision-Making Guidelines)

The asset can no longer be maintained, or suffers a loss in value due to a decrease in the usefulness of the asset, caused by technological change, or changes in people’s behavioural patterns or tastes, or environmental changes.

Optimised decision-making (IIMM)

Two definitions are: (1) A formal process to identify and prioritise all potential solutions with consideration of financial viability, social and environmental responsibility and cultural outcomes and (2) an optimisation process for considering and prioritising all options to rectify existing or potential performance failure of assets. The process encompassesNPVanalysisandriskassessment.

Performance (ISO 55 000) Measurable result of either quantitative or qualitative nature that can relate to the management of activities, processes, products or services, systems or organisations.

Performance measure (IIMM) A qualitative or quantitative measure used to measure actual performance against astandardorothertarget.Performancemeasuresareusedtoindicatehowtheorganisation is doing in relation to delivering levels of service.

Performance monitoring (LGIAMG)

Continuous or periodic quantitative and qualitative assessments of the actual performance compared with specific objectives, targets or standards.

Policy (Adjusted from ISO 55 000)

Intentions and direction of an entity as formally expressed in a documented statement approved by top management and communicated throughout the entity.

Predictive action (ISO 55 000) Action to monitor the condition of an asset and predict the need for preventative or corrective action. Also referred to condition monitoring or performance monitoring.

Preventative action (ISO 55 000) Action to eliminate the cause of a potential nonconformity or other undesirable potential situation.

Preventative maintenance Maintenancecarriedoutatpre-determinedintervals,orcorrespondingtoprescribedcriteria, and intended to reduce the probability of failure or the performance degradationofanitem.Preventativemaintenanceisplannedorcarriedoutonopportunity.

Process (ISO 55 000) Set of interrelated or interacting activities which transforms inputs into outputs.Property, plant and equipment (PPE) (GRAP)

Property,plantandequipmentaretangibleitemsthat:(a)areheldforuseintheproduction or supply of goods or services, for rental to others, or for administrative purposes; and (b) are expected to be used during more than one reporting period.

Recoverable amount (GRAP) The higher of an assets fair value less costs to sell and its value in use.Reliability-centred maintenance (IIMM)

A process for optimising maintenance based on the reliability characteristics of the asset.

Remaining useful life (IIMM) The time remaining until an asset ceases to provide the required service level or economic usefulness.

7Maintenance accounting FraMework for immovable assets

TERM DESCRIPTIONRenewal Expenditure on an existing asset which returns the service potential of the asset or

expected useful life of the asset to that which it had originally. Note 1: Renewal can include works to replace existing assets or facilities with assets or facilities of equivalent capacity or performance capability.Note 2: Expenditure on renewals is funded through the organisation’s capital budget, andsuchexpenditureisrecognisedintheorganisation’sStatementofFinancialPosition.

Residual value (GRAP) Is the estimated amount that an entity would currently obtain from disposal of the asset, after deducting the estimated costs of disposal, if the asset was already of the age and in the condition expected at the end of its useful life.

Risk (IIMM) The effect of uncertainty on objectives. Risk events are events which may compromise the delivery of the organisation’s strategic objectives.

Risk controls (IIMM) Measures to manage or mitigate identified risks.Risk exposure (IIMM) The level of risk to which an organisation is exposed to. Risk exposure is a function of

the probability of an occurrence times the impact of that occurrence.Risk management (IIMM) The application of a formal process that identifies the exposure of an entity to service

performance risk and determines appropriate responses. Risk register (IIMM) A record of information that stipulates risks identified, the levels of risk exposure before

and after implementation of risk controls, and details of appointed risk owners as a minimum.

Routine maintenance (IIMM) Day to day operational activities to keep the asset operating (replacement of light bulbs, cleaning of drains, repairing leaks, etc.) and which form part of the annual operating budget, including preventative and periodic maintenance.

Statement of Financial Performance

TheStatementofFinancialPerformance,alsoknownasanincomestatement,showsthe revenue and expenses of an organisation over a period of time.

Statement of Financial Position TheStatementofFinancialPosition,alsoknownastheBalanceSheet,presentsthefinancial position of an entity at a given date. The statement comprises three main components, these being assets, liabilities and equity, and gives users of financial statements insight into the financial soundness of an entity in terms of liquidity risk, financial risk, credit risk and business risk.

Unplanned maintenance (IIMM) Corrective work required in the short term to restore an asset to working condition so that it can continue to deliver the required service or to maintain its level of security and integrity.

Useful life (GRAP) The useful life of an asset is the period over which an asset is expected to be available for use by an entity or the number of production or similar units expected to be obtained from the asset by an entity.

Value in use (GRAP) Thepresentvalueoftheasset’sremainingservicepotentialofanon-cash-generatingasset or the present value of the estimated future cash flows expected to be derived from the continuing use of an asset and from its disposal at the end of its useful life of a cash generating asset.

8Maintenance accounting FraMework for immovable assets

2.2 ACRONYMS

Acronyms relevant to this Standard include:

ABC Activity-basedCosting

AFS Annual Financial Statements

AM Asset Management

CAPEX Capital Expenditure

CIDB Construction Industry Development Board

CRC Current Replacement Cost

DRC Depreciated Replacement Cost

ERF Economic Reporting Framework

FAR Fixed Asset Register

FMECA Failure Modes, Effects and Criticality Analysis

GFMAM Global Forum for Maintenance and Asset Management

GRAP GenerallyRecognisedAccountingPractice

IAS International Accounting Standards

IDMS Infrastructure Delivery and Management System

IIMM International Infrastructure Management Manual

IPSAS InternationalPublicSectorAccountingStandards

IPWEA InstituteofPublicWorksEngineeringAustralia

ISBN International Standard Book Number

ISO International Standards Organisation

LGIAMG Local Government Infrastructure Asset Management Guidelines

OPEX Operating Expenditure

PAS PubliclyAvailableStandard

PPE Property,PlantandEquipment

RUL RemainingUsefulLife

SANS South African National Standards

SCM Supply Chain Management

SCOA Standard Chart of Accounts

3. SCOPE

3.1 FUNCTIONALSCOPE

This framework focusses on the financial and accounting aspects of asset care activities, these being maintenance and renewal, from the planning for and budgeting of maintenance, renewal or replacement, through to recording, reporting, monitoring and evaluation. Specific objectives include:

a. to realistically quantify asset care (maintenance and renewal) needs, both now and in the future;b. to properly plan, budget and spend on asset care in a manner that supports fiscal stability, effective service delivery and a

stable, robust maintenance industry;c. to provide for sufficient depreciation to fund asset renewal; ord. where sufficient funding is not available or is very constrained, to clearly understand the risks and costs associated with

deferred maintenance and renewals.

To achieve the above, this maintenance accounting framework adopts a componentised approach to assets, which requires guidance on the manner in which assets are recognised and measured.

9Maintenance accounting FraMework for immovable assets

Operating budget OPEX

SCO

A Statement of Financial Performance

Plan Budget Transact Record Report Evaluate

Capital budget CAPEX GL Statement of Financial

Position

This framework should be read in conjunction with the National Immovable Asset Maintenance Management Standard and the MaintenancePlanningGuidelineforPublicBuildings.

3.2 APPLICATIONOFTHISMAINTENANCEACCOUNTINGFRAMEWORK

This framework encompasses all immovable assets under the custodianship of national and provincial government. Notwithstanding this, the principles documented in this framework are able to be applied to all forms of public sector immovable assets.

3.3 NORMATIVE REFERENCES

The following documents, in whole or in part, are normatively referenced in this Standard:

• RelevantstandardsofGenerallyRecognisedAccountingPractice,withspecificreferencetoGRAP17:Property,PlantandEquipment.

• RelevantInternationalAccountingStandards(IAS),withspecificreferencetoIAS16:Property,PlantandEquipment.• National Treasury. Chart of Accounts. • National Treasury. Guidelines for Implementing the Economic Reporting Format, September 2009• National Treasury. Chart of accounts, December 2014.• National Treasury. Accounting Manual for Departments. The Standard Chart of Accounts and Systems.• NationalTreasury.StandardChartofAccountsProjectSummaryReport.2013.• NationalTreasury.PublicFinanceManagementActNo.1OF1999• NationalTreasury.GuideforAccountingOfficersPublicFinanceManagementAct• NationalTreasury.BudgetFormatsGuideforthePreparationoftheEstimatesofProvincialRevenueandExpenditure.2015.• National Immovable Asset Maintenance Management Standard • MaintenancePlanningGuidelineforPublicBuildings• Descriptive Accounting, IFRS Focus. 19th edition• NationalTreasury.MFMACircularNo.71,UniformFinancialRatiosandNorms.• GovernmentofWesternAustralia.DepartmentofLocalGovernmentandCommunities.LocalGovernmentOperational

Guidelines. Number 18 – June 2013. Financial Ratios.• InstituteofManagementAccountants.ImplementingActivity-BasedCosting,2006.• JournalofBusinessCaseStudies.UtilizingActivity-BasedCostingToManageTheMaintenanceFunctionInAManufacturing

Company• National Treasury. Costing Methodology Guideline for Local Government.• National Treasury Regulations for departments, trading entities, constitutional institutions and public, 2005• National Treasury Gazette 35939• National Treasury. Supply Chain Management A Guide For Accounting Officers / Authorities, 2004

10Maintenance accounting FraMework for immovable assets

3.4 LIMITATIONSOFTHISMAINTENANCEACCOUNTINGFRAMEWORK

National Treasury regularly issues circulars and directives to update and clarify requirements as they change. This framework does not deal with these but rather focuses on principles and techniques.

4. BUILDINGBLOCKSFORTHEMAINTENANCEACCOUNTINGFRAMEWORK

4.1 STANDARDCHARTOFACCOUNTS(SCOA)

SCOA comprises the coding of items used for classification, budgeting, recording and reporting of receipts and payments within the financial system. It serves to facilitate and systematise the recording of all transactions and is directly linked to the Economic Reporting Format (ERF). The coding structure comprises eight segments. A selection must be made from each of these segments when a transaction is recorded in the financial system; i.e. all segments must be used for recording any given transaction.

TABLE 1: SCOA SYSTEM OF SEGMENTATION

SEGMENT MAIN PURPOSECONSIDERATIONS TO ESTABLISH APPROPRIATE CLASSIFICATION

CODE IN THE SEGMENTS

Infrastructure segment

To identify whether or not a spending item relates to infrastructure and to show the type of infrastructure it relates to

Does the transaction relate to an infrastructureornon-infrastructureasset?

Project segment

To identify whether or not a payment is part of a projectDoes the transaction relate to a specific project and if so, what type of project?

Objective segment

To identify the programme / activity against which any given transaction should be recorded. The segment reflects a department’sprogrammeandsub-programmestructureinasmuchdetail as is required both for reporting and management purposes

Against which programme / activity should the transaction be recorded?

Fund segmentTo identify the source of funding from which payments are effected, and the nature of receipts

Against which source of funding should the payment be allocated and against which source should the receipt be allocated?

Item segmentTo record receipt and payment transactions as well as transactions in assets and liabilities

Whatisthenatureofthepaymentand what is the nature of the receipt?

Asset segmentTo identify asset classes to which a transaction is allocated when the purpose relates to an asset or the use of an asset.

Does the transaction relate to an asset or the use of an asset and if so, which class of asset?

Responsibility segment

To identify the cost centre of any given transaction. As the location of cost centres varies across departments, depending on their organisational structure, this segment is not standardised and each department maintains the segment

To which cost centre should the transaction be allocated?

Regional segment

To identify which region benefits from government spending

In which region does the service get delivered and in which region is the beneficiary that benefits from the transaction?

11Maintenance accounting FraMework for immovable assets

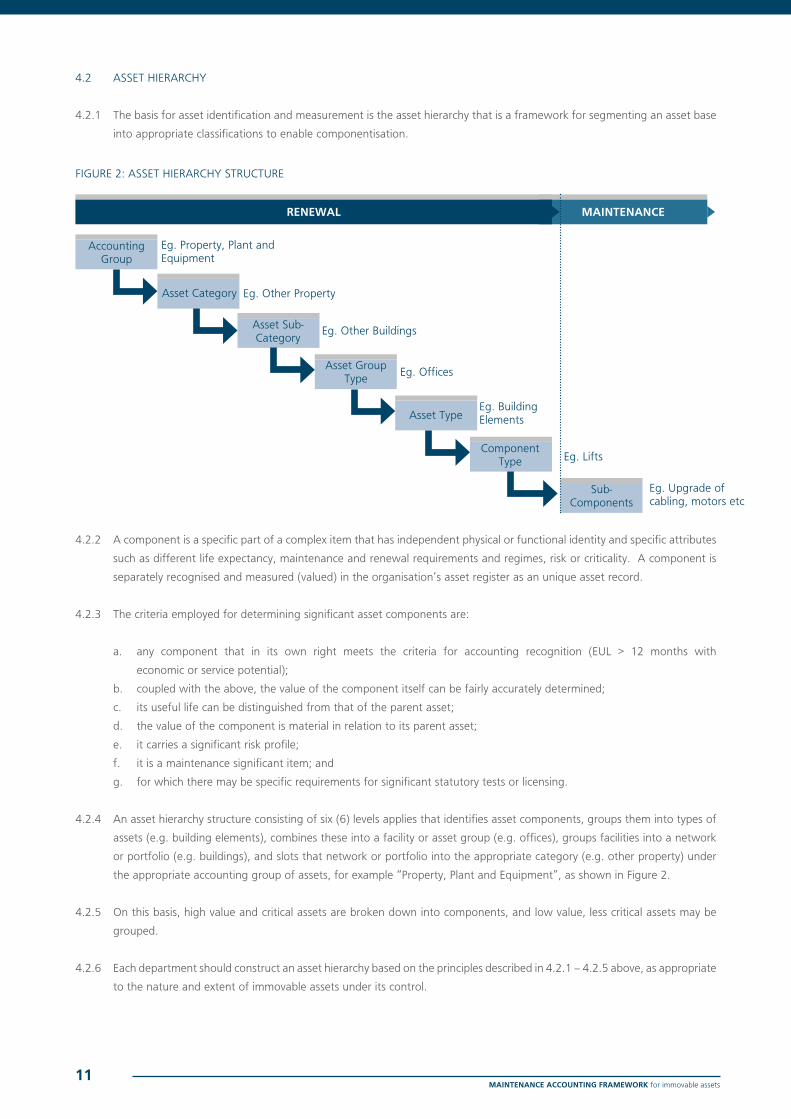

4.2 ASSETHIERARCHy

4.2.1 The basis for asset identification and measurement is the asset hierarchy that is a framework for segmenting an asset base into appropriate classifications to enable componentisation.

FIGURE2:ASSETHIERARCHySTRUCTURE

MAINTENANCERENEWAL

Accounting Group

Eg.Property,PlantandEquipment

Asset Category Eg.OtherProperty

AssetSub-Category Eg. Other Buildings

Asset Group Type Eg. Offices

Asset TypeEg. Building Elements

Component Type Eg. Lifts

Sub-Components

Eg.Upgradeofcabling, motors etc

4.2.2 A component is a specific part of a complex item that has independent physical or functional identity and specific attributes such as different life expectancy, maintenance and renewal requirements and regimes, risk or criticality. A component is separately recognised and measured (valued) in the organisation’s asset register as an unique asset record.

4.2.3 The criteria employed for determining significant asset components are:

a. any component that in its own right meets the criteria for accounting recognition (EUL > 12 months with economic or service potential);

b. coupled with the above, the value of the component itself can be fairly accurately determined; c. its useful life can be distinguished from that of the parent asset; d. the value of the component is material in relation to its parent asset; e. it carries a significant risk profile; f. it is a maintenance significant item; and g. for which there may be specific requirements for significant statutory tests or licensing.

4.2.4 An asset hierarchy structure consisting of six (6) levels applies that identifies asset components, groups them into types of assets (e.g. building elements), combines these into a facility or asset group (e.g. offices), groups facilities into a network or portfolio (e.g. buildings), and slots that network or portfolio into the appropriate category (e.g. other property) under theappropriateaccountinggroupofassets,forexample“Property,PlantandEquipment”,asshowninFigure2.

4.2.5 On this basis, high value and critical assets are broken down into components, and low value, less critical assets may be

grouped.

4.2.6 Each department should construct an asset hierarchy based on the principles described in 4.2.1 – 4.2.5 above, as appropriate to the nature and extent of immovable assets under its control.

12Maintenance accounting FraMework for immovable assets

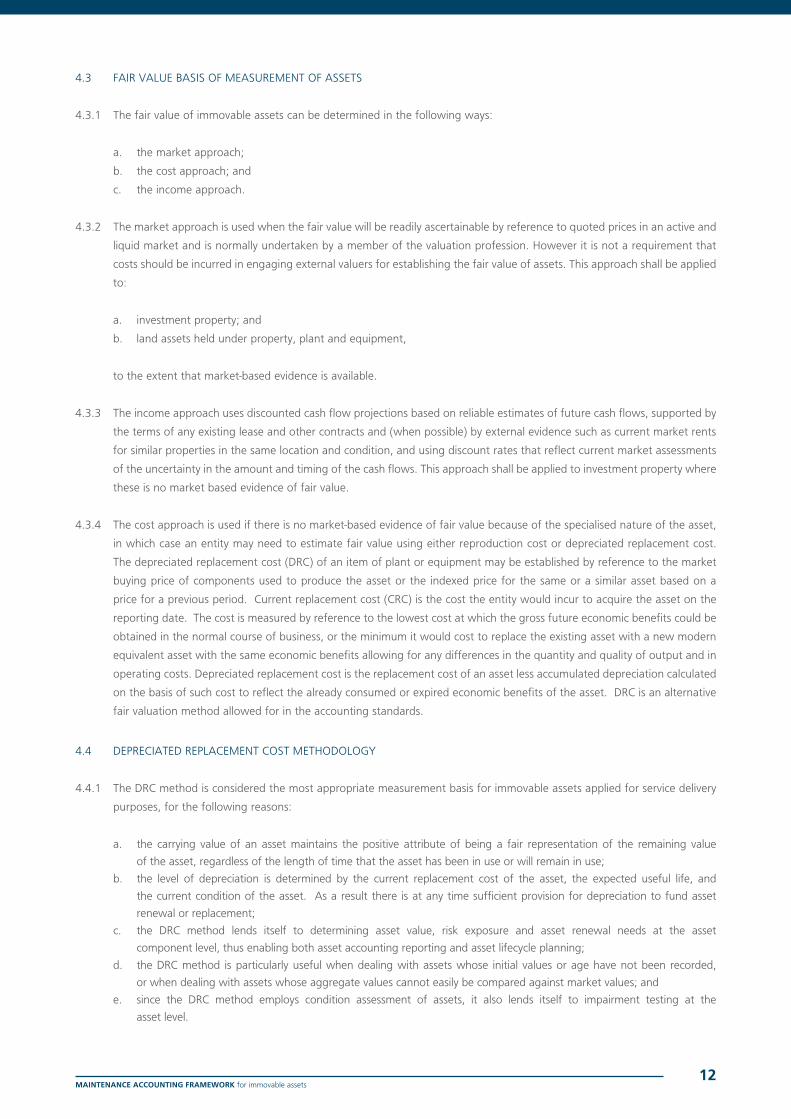

4.3 FAIRVALUEBASISOFMEASUREMENTOFASSETS

4.3.1 The fair value of immovable assets can be determined in the following ways:

a. the market approach; b. the cost approach; and c. the income approach.

4.3.2 The market approach is used when the fair value will be readily ascertainable by reference to quoted prices in an active and liquidmarketandisnormallyundertakenbyamemberofthevaluationprofession.Howeveritisnotarequirementthatcosts should be incurred in engaging external valuers for establishing the fair value of assets. This approach shall be applied to:

a. investment property; and b. land assets held under property, plant and equipment,

totheextentthatmarket-basedevidenceisavailable.

4.3.3 The income approach uses discounted cash flow projections based on reliable estimates of future cash flows, supported by the terms of any existing lease and other contracts and (when possible) by external evidence such as current market rents for similar properties in the same location and condition, and using discount rates that reflect current market assessments of the uncertainty in the amount and timing of the cash flows. This approach shall be applied to investment property where these is no market based evidence of fair value.

4.3.4 Thecostapproachisusedifthereisnomarket-basedevidenceoffairvaluebecauseofthespecialisednatureoftheasset,in which case an entity may need to estimate fair value using either reproduction cost or depreciated replacement cost. The depreciated replacement cost (DRC) of an item of plant or equipment may be established by reference to the market buying price of components used to produce the asset or the indexed price for the same or a similar asset based on a price for a previous period. Current replacement cost (CRC) is the cost the entity would incur to acquire the asset on the reporting date. The cost is measured by reference to the lowest cost at which the gross future economic benefits could be obtained in the normal course of business, or the minimum it would cost to replace the existing asset with a new modern equivalent asset with the same economic benefits allowing for any differences in the quantity and quality of output and in operating costs. Depreciated replacement cost is the replacement cost of an asset less accumulated depreciation calculated on the basis of such cost to reflect the already consumed or expired economic benefits of the asset. DRC is an alternative fair valuation method allowed for in the accounting standards.

4.4 DEPRECIATEDREPLACEMENTCOSTMETHODOLOGy

4.4.1 The DRC method is considered the most appropriate measurement basis for immovable assets applied for service delivery purposes, for the following reasons:

a. the carrying value of an asset maintains the positive attribute of being a fair representation of the remaining value of the asset, regardless of the length of time that the asset has been in use or will remain in use;

b. the level of depreciation is determined by the current replacement cost of the asset, the expected useful life, and the current condition of the asset. As a result there is at any time sufficient provision for depreciation to fund asset renewal or replacement;

c. the DRC method lends itself to determining asset value, risk exposure and asset renewal needs at the asset component level, thus enabling both asset accounting reporting and asset lifecycle planning;

d. the DRC method is particularly useful when dealing with assets whose initial values or age have not been recorded, or when dealing with assets whose aggregate values cannot easily be compared against market values; and

e. since the DRC method employs condition assessment of assets, it also lends itself to impairment testing at the asset level.

13Maintenance accounting FraMework for immovable assets

4.4.2 TheDRCapproachrequiresinformationontheexpectedusefullife(EUL),residualvalue(RV),currentreplacementcost(CRC),andremainingusefullife(RUL)ofeachoftheassetcomponents.DRCisthencalculatedasfollows(assumingthatthe straight line method of depreciation applies):

FIGURE3:CALCULATINGDRC

Carrying value

Accumulated depreciation

Depreciated replacement cost

Assumed deterioration curve (in this case, straight line)

Depreciable amount

Residual value

Curr

ent r

epla

cem

ent c

ost

Estimated useful life

Remaining useful life

Annu

al

depr

ecia

tion

char

geEn

d of

repo

rting

pe

riod

where: CRC: Current Replacement Cost DRC: Depreciated Replacement Cost EUL: EstimatedUsefulLife RUL: RemainingUsefulLife RV: Residual Value

Note: An RV of zero can be used in the above formula to determine the DRC of assets that do not have an RV.

4.4.3 The CRC is the product of an appropriate unit rate and the extent of the component, and represents the cost of replacing the asset. The unit rate is based on the cost of replacing the asset under consideration with a modern equivalent asset which has the same functional capacity.

4.4.4 The depreciable portion of an asset is determined by subtracting the residual value from the CRC. The depreciated replacement cost (DRC) is established by proportionately reducing the depreciable portion based on the fraction of the remaining useful life over the expected useful life.

4.4.5 In the event that the entity must measure (value) an existing for the first time, such as when the asset in question has been transferred to this entity from another entity, but the age of the asset is not known, it still remains possible to calculate DRC. In such a case the condition of the asset is assessed using the asset condition rating scale described in the MaintenancePlanningGuidelineforPublicBuildings.EachconditiongradecarriesanindicativemedianRUL,allowingforcalculation of the DRC, as follows:

DRC = x (CRC – RV) + RVRULEUL

14Maintenance accounting FraMework for immovable assets

FIGURE4:USINGDRCTODETERMINECARRyINGVALUEWHERETHEAGEOFTHEASSETISUNKNOWNCu

rren

t rep

lace

men

t co

st/c

ondi

tion

grad

e

Remaining useful life

Very

poo

rPo

orFa

irG

ood

Very

goo

dAccumulated depreciation

Depreciated replacement cost

Assessed condition: good, adopt median ofRULrangeforthis condition grade(58%)

Depreciable amount

Residual value

100-71% 70-46% 45-26% 25-11% 10-0%

4.5 COSTING OF MAINTENANCE ACTIVITIES

4.5.1 Each entity shall cost the full scope of activities comprising the maintenance function to:

a. understand the true cost associated with asset maintenance; b. budget appropriately for asset maintenance; c. make informed decisions on appropriate service standards and lifecycle strategies, and to d. support the drive towards progressive improvements in efficiency.

4.5.2 Costs assigned to cost objectives are classified as either direct or indirect costs. A direct cost is a cost that can be specifically associated with particular service, function or activity based on actual consumption. It is directly related to the cost objective. Indirect costs are those which are not directly attributable to the output, are often referred to as overheads and are normally incurred for multiple services. Indirect costs need to be apportioned to the cost objective.

4.5.3 EachentityshallemploytheActivity-BasedCosting(ABC)methodologythatmeasurestheboththedirectandindirectcostsof activities associated with the rendering of a service, and assigns cost based on the resources each activity consumes.

4.5.4 The four steps involved in designing an ABC system for asset maintenance are:

a. Identify the work activities performed by people and equipment in relation to asset component type; b. Identify the elements of cost and performance measures; c. Determine the relationships between the various activities and elements of cost; and d. Identify and measure the activity drivers that determine the work load and cause accumulated activity costs to

flow to other activities or to the services.

4.5.5 The work activity identification exercise should be guided by materiality and the objectives of the ABC system. Examples of typical maintenance work activities include:

15Maintenance accounting FraMework for immovable assets

TABLE2:TyPICALMAINTENANCEACTIVITIES

PREDICTIVE MAINTENANCE PREVENTATIVE MAINTENANCE CORRECTIVE MAINTENANCEIssue works order Issue works order Issue works orderIssue notice of service interruption, if applicable

Issue notice of service interruption, if applicable Issue work permit, where appropriate

Issue work permit, where appropriate Issue work permit, where appropriate Emergency or temporary services provision, as appropriate

Prepareequipment Prepareequipment PrepareequipmentUndertakeinspection/diagnostictesting Order parts Order partsFurther testing if applicable, e.g. laboratory analysis of sample materials Performwork Performwork

Analysis of inspection/diagnostic/predictive results Inspection of results Inspection of results

Report on results.of inspection/diagnostic activity and/or issuing of safety/compliance certificate/license

Return asset to operation Return asset to operation

Close works order Close works order Close works order

4.5.6 Typical elements of maintenance costs are indicated below. The general ledger is typically the source of information about these cost elements, but it does not break those cost elements down by activity performed – this is the purpose of cost accounting, using the ABC methodology to reassign these expenses into activity costs using resource drivers.

a. salaries, employee benefits and overtime; b. staff training; c. protective clothing, d. rental/lease of workshop or depot space; e. vehicles and other specialist capital equipment; f. general tools and equipment; g. parts and other consumables; h. contractors; i. electronic maintenance management system (e.g. annual licensing fees); j. utilities (e.g. water and electricity); k. general administration (including management, customer support center, administrative support, office

stationary, communication expenses etc.); and l. laboratory testing.

Assign the expense data contained in the general ledger to activities. This assignment is determined by the relationships between the various work activities and the elements of cost. The elements of cost or resource pools can be assigned to activities by assigning them in some directly measurable manner (e.g. maintenance via a work order).

4.5.7 Activity drivers are the usage-based variables that explain the behaviour andmagnitude of activity costs. They reflectthe consumption of expenses by activities and the consumption of activities by other activities, products, or services. An example of a cost driver is the number of direct labour hours required to perform the maintenance work.

4.5.8 Withthecostdriversidentified,thenextstepistomeasuretheextentthereof(e.g.thenumberofworkordersforeachcategory and the associated direct labour hours).

4.5.9 The process of cost allocation can be performed once cost drivers have been measured. The value associated with each cost driver must be calculated, and the average cost to perform the defined activity be determined. These values inform the charge out rates used in allocating costs according to the cost drivers in each category of maintenance.

4.5.10Withthecategoriesofmaintenancefunctionsdefinedalongwiththeaccompanyingactivitiesineachcategoryandtheircosts, the unit cost per work order can be calculated. This unit cost can then be utilised to generate the cost allocation for each work order type and provide a more accurate depiction of the maintenance cost associated with each activity.

16Maintenance accounting FraMework for immovable assets

PART B:

MAINTENANCEACCOUNTINGPROCESSES

17Maintenance accounting FraMework for immovable assets

5. ASSET RECOGNITION

5.1 An immovable item is recognised as an immovable asset if:

a. it is a resource controlled by the entity as a result of past events; b. it is probable that future economic or service benefits will flow to the entity, over more than one reporting

period; and c. the item has a cost or value that can be measured reliably.

The general recognition criteria apply to both initial and subsequent recognition.

5.2 Theidentificationofcomponentsformsthebasisfortherecognitionandde-recognitionofimmovableassets.Thesignificantparts of an immovable asset must be identified on initial recognition. The following criteria should be applied:

a each component must meet the criteria for accounting recognition; b. its value is material in relation to its parent asset and can be reliably measured; c. its useful life and/or criticality can be clearly distinguished from that of its parent asset; and/or d. itisasignificantelementofthedepartment’sprevailinglife-cyclestrategyforcapitalrenewal.

TheMaintenancePlanningGuidelineforPublicBuildingsprovidesadditionalguidanceondeterminingthecomponentsofafacility.

5.3 The asset hierarchy adopted, inclusive of a list of components indicating the estimated useful life and residual value, if applicable,foreachcomponent,shallbeincludedinanannexuretotheAssetManagementPolicy.

6. ASSETMEASUREMENT

6.1 INITIALMEASUREMENT

6.1.1 The general rule is that immovable assets that qualify for recognition are initially measured at cost. The cost of immovable assets is the amount of cash or cash equivalents paid or the fair value consideration given to acquire an asset at the time of its acquisition or construction.

6.1.2 The following items are elements of cost:

a. its purchase price, including import duties and non-refundable purchase taxes, after deducting trade discounts and rebates;

b. any costs directly attributable to bringing the asset to the location and condition necessary for it to be capable of operating in the manner intended by management. Examples of directly attributable costs are:

• costsofemployeebenefits(asdefinedintheStandardofGRAPonEmployeeBenefits)arisingdirectly from the construction or acquisition of the item of property, plant and equipment;• costs of site preparation;• initial delivery and handling costs;• installation and assembly costs;• costs of testing whether the asset is functioning properly, after deducting the net proceeds from selling any items produced while bringing the asset to that location and condition (such as samples produced when testing equipment); • professional fees; and

c. the initial estimate of the costs of dismantling and removing the item and restoring the site on which it is located, the obligation for which an entity incurs either when the item is acquired or as a consequence of having used the item during a particular period for purposes other than to produce inventories during that period.

18Maintenance accounting FraMework for immovable assets

6.1.3 Capitalisation of costs ceases when the item is in the location and condition necessary for it to be capable of operating in the manner intended by management.

6.1.4 Examples of costs that are not to be included in the capital cost of an item of property, plant and equipment are:

a. costs of opening a new facility; b. costs of introducing a new product or service (including costs of advertising and promotional activities); c. costs of conducting business in a new location or with a new class of customers (including costs of staff

training); d. administration and other general overhead costs; e. costs incurred while an item capable of operating in the manner intended by management has yet to be

brought into use or is operated at less than full capacity; f. initial operating losses, such as those incurred while demand for the item’s outputs build up; and g. costs of relocating or reorganising part or all of the entity’s operations.

Refer to Annexure A for an example of determining the cost of immovable assets.

6.1.5 Whereanimmovableassetisacquiredthroughanon-exchangetransactionfromanon-governmententity,itscostmustbemeasured at its fair value as at the date of acquisition.

6.1.6 Thecostofaself-constructedassetisdeterminedusingthesameprinciplesasforanacquiredasset.Thecostofabnormalamountsofwastedmaterial,labourorotherresourcesincurredinself-constructinganassetisnotincludedinthecostofthe asset. Costs incurred to acquire an immovable asset through construction by way of a project that spans over more than one financial year should be accumulated and will be added to determine the cost of the ultimate asset once available for use based on the principles above. During the stage where the capital asset is being constructed, all costs will be shown as capital work in progress.

6.1.7 The allocation of costs to components (“componentisation”) is straight forwardwhere single components have beenestablishedorreplaced.However,forcomplexconstructionprojectscomprisingseveralcomponentsand/orcostelements,the breakdown into components and the method of allocation of the actual total project cost to components is to allocate actual costs by way of a shadow valuation using the DRC methodology.

6.1.8 Constructed assets shall be unbundled from source documents (such as ‘as built’ plans, bill of quantities, project close out reports, project invoices, etc.) by means of the shadow valuation method. In using this method, assets are componentised according to the asset hierarchy and approved unit rates established at the component level. Following determination of the values of the various components, they are adjusted on a pro rata basis to be in line with the actual total cost. Therefore, the components and associated amounts that are recorded in the asset register will not be reflected in the invoices per se, however, the total project costs will agree. Refer to Annexure B for an example of a shadow valuation.

6.2 SUBSEqUENTMEASUREMENT

6.2.1 After initial recognition, measurement of asset classes shall done as follows – note that the measurement model must be consistently applied to the entire class of assets:

19Maintenance accounting FraMework for immovable assets

TABLE3:MEASUREMENTMODELSAPPLIEDTOASSETCLASSES

ACCOUNTING GROUP ASSET CATEGORY MEASUREMENT MODEL COMMENTS

Property,plantandequipment

Normal buildings and building elements

Revaluation model: DRC N/A

Land associated with buildings Revaluation modelMarket, cost or income approach

Investment property Fair valueMarket, cost or income approach

Heritageassets

Element that can be replaced with modern equivalent assets

Revaluation model: DRC e.g. plumbing

Elements with particular historic character

Revaluation model: reproduction cost method

e.g. the sandstone wall of the UnionBuildings

6.2.2 In terms of the revaluation model, the immovable asset will be carried at fair value at the date of the revaluation less any subsequent accumulated depreciation and subsequent accumulated impairment losses, provided that its fair value can be measured reliably. Revaluations must be done on a regular basis to ensure that the carrying amount of the asset at the end of the reporting period does not differ substantially from the fair value at the end of the reporting period.

6.2.3 The frequency of revaluations depends upon the changes in the fair values of the items of immovable assets being revalued. Whenthefairvalueofarevaluedassetdiffersmateriallyfromitscarryingamount,afurtherrevaluationisnecessary.Ifanimmovableassetisrevalued,theentireclass,or“assetcategory”pertheassethierarchy,towhichthatassetbelongsshallbe revalued.

6.2.4 This approach is especially appropriate to immovable assets that typically have long lives (average of around 50 years) and high values – where the effects of escalation are material.

6.2.5 The advantages of adopting the revaluation method are as follows:

a. more realistic and accurate reporting on the value of the community’s assets, and, in general, improved solvency;

b. more realistic and accurate reflection of the condition of the asset portfolio, and accordingly improved decision- makingonlife-cyclemanagement(suchasmaintenanceandcapitalrenewal);

c. more realistic and accurate reflection of the value of infrastructure being consumed by the community – which better informs assessments of revenue needs and sustainability; and

d. in view of the above, improved transparency.

6.2.6 Based on the above, the revaluation model should be applied as far as possible.

7. TREATMENTSUBSEqUENTTOINITIALRECOGNITION

7.1 TREATMENTOFEXPENDITURESUBSEqUENTTOINITIALRECOGNITION

7.1.1 In many instances subsequent expenditure will be incurred on assets following initial measurement.

7.1.2 The impact of any given expenditure on a component recorded in the asset register must be examined. Subsequent expenditure is considered to be capital in nature if it extends the life of a component, or increases its service potential (for example its capacity or performance). All the expenditure that relates to actions to either operate or to enable the asset to achieve its intended useful life of components is expensed.

20Maintenance accounting FraMework for immovable assets

FIGURE5:TREATMENTOFSUBSEqUENTEXPENDITURE

Is it probable that the expense will create future economic benefits or service potential over and above that which the asset was designed for?

Add the expense to the carrying amount of the asset

Capitalise the expense

Recognise as an expense when it occurs

Operating expenditure

YES NO

7.1.3 Parts(orcomponents)ofsomeassetsrequireperiodicreplacement.Providedthattherecognitioncriteriaaremet,thecostsassociated with the following actions or outcomes shall be capitalised:

a. contributes to the increase in the useful life of an asset which is beyond the original useful life expectation; b. increase productivity of the asset; c. expands capacity of the asset; d. significantly reduces operating or maintenance costs whilst delivering the same or increased level and standard

of output; e. increase size; and f. change its shape and use.

7.1.4 Whencapitalisingsubsequentexpenditureofarenewalnature,theentityshall:

a. recognise the cost of replacing a component when that cost is incurred, if the recognition criteria are met, in the carrying amount of the asset; and

b. derecognise the carrying amount of the component that is replaced.

7.1.5 Examples of renewal include – provided that the intent is to extend useful life, not to increase capacity:

a. resurfacing of a road; b. relining of a furnace; and c. replacing the interior walls of a building.

7.1.6 Whenexpenditurerelatestosub-componentsatanylevelbelowthe6levelhierarchy,suchexpenditureisnotcapitalisedevenifthesub-componentsareexpectedtobeusedforaperiodlongerthantwelvemonths.Paintingofabuilding,orreplacingonlyaportionofadefinedcomponentwillbeclassifiedandtreatedasOperatingExpenditure(OPEX).

7.1.7 Theentityshallnotrecognisethecostsoftheday-to-dayservicingoftheassetinthecarryingamountoftheasset.Rather,thesecostsarerecognisedinsurplusordeficitasincurred.Costsofday-to-dayservicingareprimarilythecostsoflabourand consumables, and may include the cost of small parts. The purpose of these expenditures is often described as for the “repairsandmaintenance”oftheitemofproperty,plantandequipment.Thisexpenditureisofanoperationalorcurrentnature.

21Maintenance accounting FraMework for immovable assets

TABLE4:EXAMPLESOFTyPICALMAINTENANCEEXPENDITUREONSELECTEDCOMPONENTS

COMPONENT TYPICAL MAINTENANCE ACTIVITYWalls Filling of paint cracks. Repainting of walls.Electrical installation Replacement of individual sections of burnt wiring.

RoofRepair of worn waterproofing. Repainting of ceilings and roof tiles. Replacement of individual roof tiles.

Floor Replacement of individual cracked tiles.Fire protection Routine inspection and maintenance of fire protection every 2 yearsParking area Repainting of parking bay lines. Repair of loose paving blocks.Perimeter protection Replacement of individual broken panels.

7.2 DEPRECIATION

7.2.1 The aim of depreciation is to allocate the depreciable amount (original cost less the residual value) of an asset over its useful life (the period during which the depreciable asset will be used) to represent the consumption of assets. The depreciable amount is recovered through use, and the residual value is recovered through sale. The depreciation charge for each period is recognised in surplus or deficit unless it is included in the carrying amount of another asset.

7.2.2 In order to determine the amount of depreciation that should be realised, the following three aspects should be considered:

a. useful life; b. expected residual value; and c. the method of depreciation.

7.2.3 Depreciation commences from the date on which the asset is available for use (when it is in the location and condition necessary for it to be capable of operating in the manner intended by management). Depreciation of an asset ceases at the date that the asset is derecognised. Depreciation does not cease when the asset becomes temporarily idle or when it is retiredfromactiveuseandheldfordisposalunlesstheassetisfullydepreciated.However,iftheunit-of-productionmethodof depreciation is applied the depreciation charge can be zero while there is no production.

7.2.4 The following factors are considered in determining the useful life of an asset:

a. the expected usage of the asset, determined by referring to the asset’s expected capacity or physical output; b. the expected physical wear and tear (consumption), which depends on operational factors such as the number

of shifts for which the asset is to be used and the repair and maintenance programme, as well as the care and maintenance of the asset while idle;

c. the technical or commercial obsolescence arising from changes or improvements in production, or from a change in the market demand for the product or service output of the asset; and

d .legal or similar limitations on the use of the asset, such as the maturity dates of related leases (normally finance leases).

7.2.5 The residual value of an asset is the estimated amount that an entity would currently obtain from disposal of the asset, after deducting the estimated costs of disposal, if the asset was already of the age and in the condition expected at the end of its useful life. If the residual value of an asset is equal to or exceeds its carrying amount at any time, no depreciation will be provided for on that asset unless and until the residual value declines below the carrying amount. The vast majority of immovable assets have negligible or no residual value.

7.2.6 The accounting standards require that the residual value and the useful life of an asset be reviewed at least at each re-porting date. If there is a change to the useful lives or residual values, the annual depreciation charge of the respective

22Maintenance accounting FraMework for immovable assets

immovable assets are adjusted and the assets are depreciated thereafter on the new remaining useful life and/or residual value. For any change in useful lives and residual values a change in accounting estimate should be disclosed in the annual financial statements. Such changes will be effective from the first day after the changes occurred (or prospectively). The opening balance of the accumulated depreciation is not adjusted because of the change in useful life or residual value.

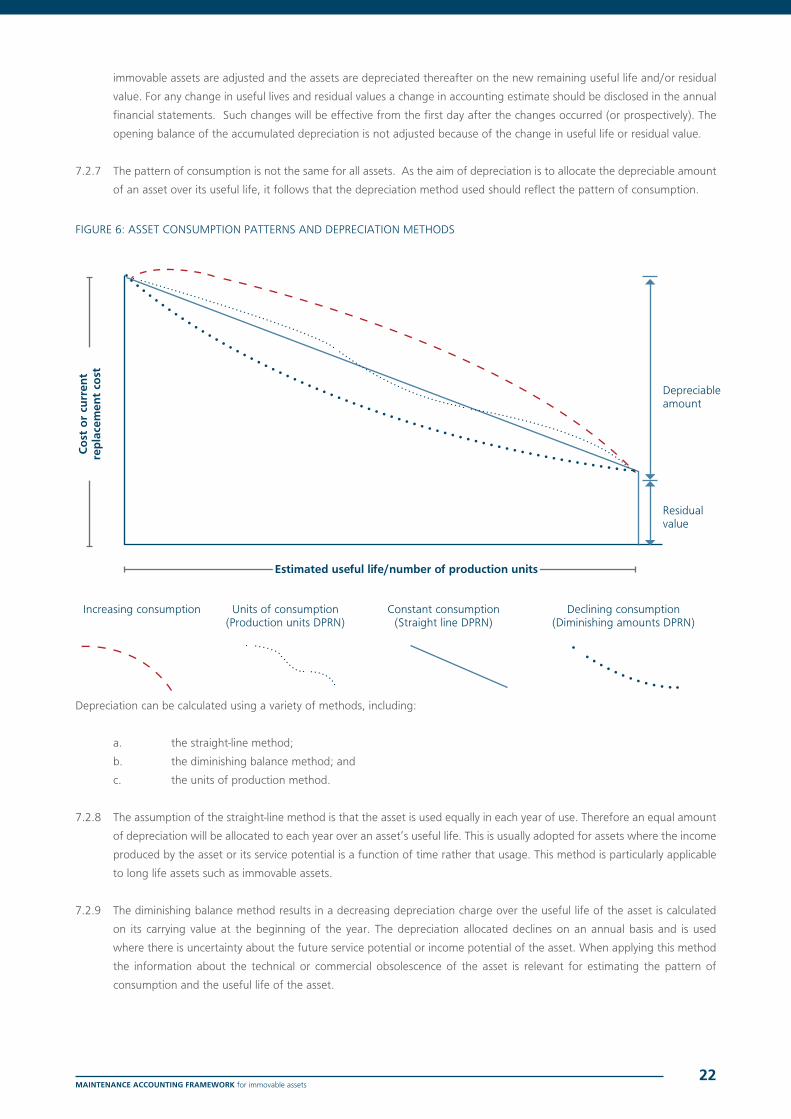

7.2.7 The pattern of consumption is not the same for all assets. As the aim of depreciation is to allocate the depreciable amount of an asset over its useful life, it follows that the depreciation method used should reflect the pattern of consumption.

FIGURE6:ASSETCONSUMPTIONPATTERNSANDDEPRECIATIONMETHODS

Cost

or c

urre

nt

repl

acem

ent c

ost

Estimated useful life/number of production units

Depreciable amount

Residual value

Increasing consumption Unitsofconsumption(ProductionunitsDPRN)

Constant consumption (StraightlineDPRN)

Declining consumption (DiminishingamountsDPRN)

Depreciation can be calculated using a variety of methods, including:

a. thestraight-linemethod; b. the diminishing balance method; and c. the units of production method.

7.2.8 Theassumptionofthestraight-linemethodisthattheassetisusedequallyineachyearofuse.Thereforeanequalamountof depreciation will be allocated to each year over an asset’s useful life. This is usually adopted for assets where the income produced by the asset or its service potential is a function of time rather that usage. This method is particularly applicable to long life assets such as immovable assets.

7.2.9 The diminishing balance method results in a decreasing depreciation charge over the useful life of the asset is calculated on its carrying value at the beginning of the year. The depreciation allocated declines on an annual basis and is used wherethereisuncertaintyaboutthefutureservicepotentialorincomepotentialoftheasset.Whenapplyingthismethodthe information about the technical or commercial obsolescence of the asset is relevant for estimating the pattern of consumption and the useful life of the asset.

23Maintenance accounting FraMework for immovable assets

7.2.10 The units of production method results in a depreciation charge that is based on the expected use or output of the asset. It provides the best approximation of the consumption of economic benefits or service potential but the total production units that the asset can produce in its life time and the total units that the asset can produce per annum must be identified. This method is most applicable to a manufacturing environment where machinery with defined production potential is used.

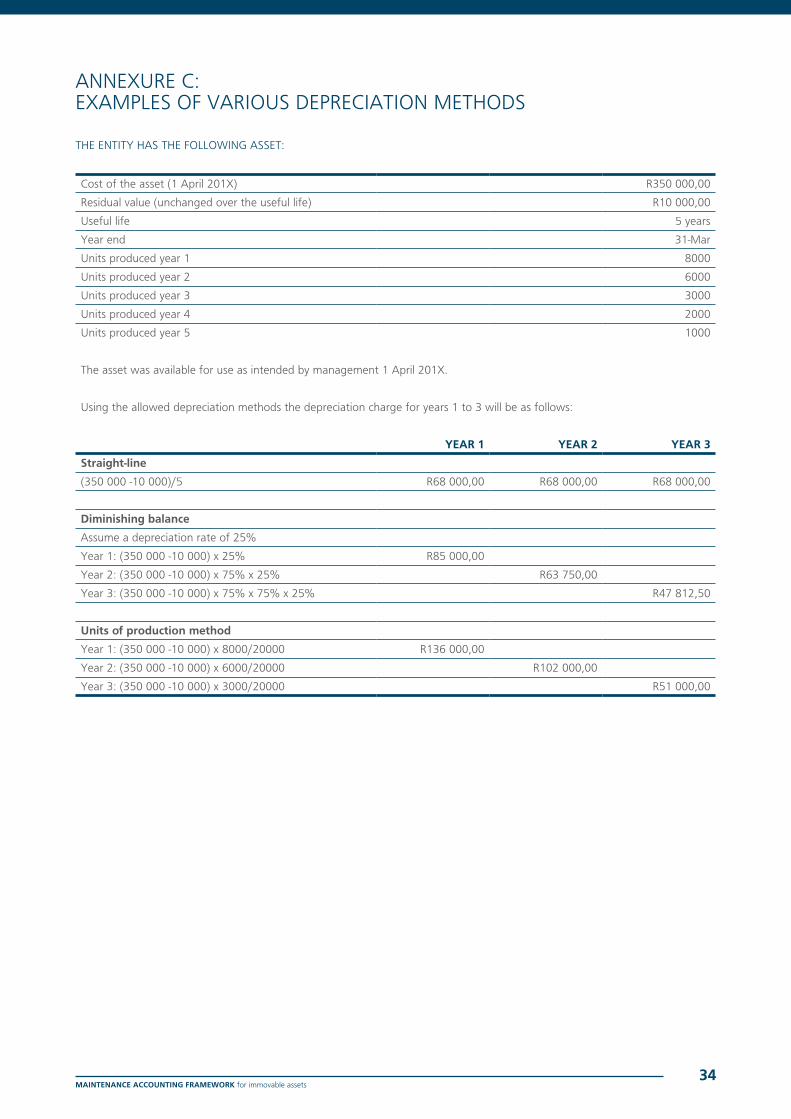

Refer to Annexure C for examples of the application of the various depreciation methods.

7.2.11 The depreciation method applied to an asset shall be reviewed at least at each reporting date (annually) and, if there has been a significant change in the expected pattern of consumption, the method shall be changed to reflect the changed pattern. A change in the depreciation method shall be accounted for as a change in an accounting estimate and disclosed as such in the AFS. Such changes will be effective from the first day after the changes occurred (or prospectively).

7.3 IMPAIRMENTTESTING,MEASUREMENTANDRECORDING

7.3.1 Each entity shall review assets for impairment when one of the indicators below occurs or at least at the end of each reporting period. In assessing whether there is any indication that an asset may be impaired, an entity shall consider as a minimum the following indicators:

a. External sources of information:• decline or cessation in demand; • decline in market value;• significantlong-termchangesinthetechnological,legalorgovernmentpolicyenvironment;• the carrying amount of the net assets of the entity is more than its market capitalisation; or• market interest rates have increased during the period, and those increases are likely to affect the discount

rate used in calculating an asset’s value in use and decrease the asset’s recoverable amount materially.•

b. Internal sources of information:• evidence of physical damage;• evidence of obsolescence;• significant changes with an adverse effect on the entity have taken place during the period, or are

expected to take place in the near future, in the extent to which, or a manner in which, an asset is used or is expected to be used, including an asset becoming idle, plans to dispose of an asset before the previously expected date, and reassessing the useful life of an asset as finite rather than indefinite;

• cash flow for maintenance cost of an asset is higher than originally budgeted;• ahalt inconstructioncould indicatean impairment.Whereconstruction isdelayedorpostponedtoa

specific date in the future, the project may be treated as work in progress and not considered as halted; or• evidence that indicates that the performance of an asset is, or will be, significantly worse than expected.

7.3.2 An impairment is recognised where the recoverable amount is less than the carrying amount, i.e. where its value has reduced. In turn, the recoverable amount is the higher of an assets fair value less costs to sell (the value if the asset were tobesoldtoathirdparty)anditsvalue-in-use(i.e.thevaluetotheentity).

7.3.3 There is however generally not an active market for assets of a specialised nature such as infrastructure and public amenities, and the value to the entity in such an instance is considered likely to be more than the sale value. Consequently, the recoverable amount is considered to be the same amount as the value in use to the entity.

7.3.4 Themodelusedforcalculatingthe“value-in-use”dependsonthetypeofimpairment,guidelinesforwhichareasindicatedin the following table.

24Maintenance accounting FraMework for immovable assets

TABLE5:DETERMININGVALUEINUSE

IMPAIRMENT INDICATORS DATA SOURCES TRIGGERS

VALUE-IN-USE(NON-CASH

GENERATING ASSETS)

VALUE-IN-USE(CASH GENERATING

ASSETS)

Utilisation – usage lower than norms/ design expectations, e.g. due to decline ornon-realisationofdemand

• Asset Register• Periodic

inspections • Annual

structured reviews with officials familiar with the assets

• Specific site surveys

• Operations reports

• Disaster reports

• Technical reports

• Assets under/not utilised (Gr 1 or 2) excluding new assets initially under-useaccordingtodesign expectations, or assets required for strategic redundancy.

ODRC – eliminate unused components, over-design–expressedas%ofDRC(based on unit rates for lower spec).

The following elements shall be reflected in the value in use calculation:• An estimate of the

future cash flows the entity expects to derive from the asset

• Expectations about possible variations in the amount or timing of those future cash flows

• The time value of money, represented by current market risk-freerateofinterest

• The price for bearing the uncertainty inherent in the asset, and

• Other factors, such as illiquidity, that market participants would reflect in pricing the future cash flows the entity expects to derive from the asset

Condition – worse than expected from normal wear and tear – e.g. due to damage, theft, vandalism, poor maintenance

• Condition grade worse than expected due to age (based on condition deterioration model), or where damaged, or unsafe.

DRC less cost of restoration /rectification-expressedas%ofDRC.

Functional performance – impaired core functionality

• Assets identified as beingsubstantiallynon-compliant (Gr 5) with the requirements

Optimised DRC – adjust system configuration for equivalent functionality (based on unit rates for lower performance).

Obsolescence – design no longer fit for purpose, excessive cost of operations

• Annual structured reviews

• Technical reports

• Stores reports

• Change in policy or regulatory environment

• Change in national policy or industry norms

• Spares and technical support not readily available

• Cost records and cost norms

Optimised DRC – eliminate obsolescent technology (DRC based on modern / new required configuration – expressedas%ofDRCguided by unit rates for modern spec).

25Maintenance accounting FraMework for immovable assets

FIGURE7:APPROACHTOIMPAIRMENTASSESSMENT,CALCULATIONANDDISCLOSURE

AMPolicyInterpretation

Non-cashgenerating Cash generating

Evidenceofimpairment?(Referto“indicators”) Evidenceofimpairment?(Referto“indicators”)

Detailed calculation of impairment amount ODRC, DRC or restoration method

Detailed calculation of impairment amount (based on value in use calculation of the future cash flows)

Recognise impairment and adjust carrying value in FAR

Disclose in AFS

Recognise impairment and adjust carrying value in FAR

Disclose in AFS

7.4 REVERSALOFIMPAIRMENTTRANSACTIONS

7.4.1 At each reporting date the entity shall assess whether there are any indications that impairment losses recognised in previous financial years have decreased or no longer exist. The recoverable amounts are calculated only on those assets where there are indications that impairment losses may have been reversed.

7.4.2 Where there has been a reversal of an impairment loss, the carrying amount is increased to its recoverable amount(providing that it does not exceed the carrying amount that would have been determined had no impairment loss been recognised in prior periods).

7.4.3 In assessing whether there is any indication that an impairment loss recognised in prior periods for an asset may no longer exist or may have decreased, the entity shall consider, as a minimum, the following indications:

a. External sources of information:• resurgence in demand; • increase in market value;• significantlong-termchangesinthetechnological,legalorgovernmentpolicyenvironmentthatwillhave

a favourable effect; or• market interest rates have decreased during the period, and those decreases are likely to affect the

discount rate used in calculating an asset’s value in use and increase the asset’s recoverable amount materially.

b. Internal sources of information:• significant changes with a favourable effect on the entity have taken place during the period, or are

expected to take place in the near future, in the extent to which, or a manner in which, an asset is used

Consider effect on useful life

26Maintenance accounting FraMework for immovable assets

or is expected to be used – these changes include costs incurred during the period to improve or enhance an asset’s performance, restructure the operation to which the asset belongs or a decision to use rather than dispose of an asset;

• a decision to resume construction of the asset that was previously halted before it was completed or in a usable condition; or

• evidence that indicates that the performance of an asset is, or will be, significantly better than expected.

8. PLANNINGANDBUDGETINGFORMAINTENANCEANDRENEWAL

8.1 COSTINGMAINTENANCEACTIVITIES:KEyPRINCIPLES

8.1.1 Immovableassetsshouldbeplannedandbudgetedforthroughouttheirlife-cycle,fromplanningthroughtodisposal,andthe results thereof documented in the entity’s asset management plan(s).

8.1.2 The following life-cycle activitiesmust be estimated for the current and following three financial years (medium termestimates)forallimmovableassetsinthe“paymentsofinfrastructurebycategory”table:

a. new and replacement assets; b. upgrades and additions; c. renewals (previously classified as rehabilitation, renovations and refurbishments); and d. maintenance and repair actions

8.1.3 Budgeting for asset maintenance shall be done on the basis of the demonstrated estimated current costs involved in achieving stated maintenance objectives. Budgeting shall not be based on historic budget provisions or some normative allocated percentage of the total operating budget.

8.2 MAINTENANCEPRIORITISATIONANDDEFERREDMAINTENANCE

8.2.1 InlinewithTheMaintenancePlanningGuidelineforPublicBuildings,whentherelevanttreasuryallocateslowerbudgetsthan requested, the lower budget allocation should be prioritised as follows:

a. firstly to preventative and condition-based maintenance for highly critical components and corrective maintenance for all components with a condition rating 1;

b. secondly to preventative maintenance of moderately critical components and deferred maintenance actions from the previous budget cycle; and

c. thereafter be allocated to the remaining corrective maintenance.

8.2.2 In the event that insufficient budget is available for maintenance, or that such budget is not fully spent in a financial period, the entity shall record the amount of deferred maintenance in its annual financial statements, and shall furthermore:

a. indicate the impact of insufficient spending on maintenance on the useful life expectations of assets; and b. indicate whether the lack of spending on asset maintenance has affected business operations, customer

commitmentsand/orlegislativerequirementsregardingtheavailabilityofasset-basedservices,andoperating income projections.

27Maintenance accounting FraMework for immovable assets

9. TRANSACTING AND RECORDING OF MAINTENANCE AND RENEWALEXPENDITURES

9.1 SUPPLyCHAINMANAGEMENT

9.1.1 The acquisition of goods and services, including the procurement of immovable assets (infrastructure and buildings) is done through the supply chain management as prescribed by the National Treasury.

9.1.2 Each entity shall implement and operate a supply chain management system in the manner prescribed by the National TreasuryintermsofthePublicFinanceManagementAct,supplychainmanagementregulations,theInfrastructureDeliveryManagement Standard to be finalised, and practice notes, circulars and guidelines as issued by the National Treasury from time to time.

9.1.3 All bid documents should specify clearly and precisely the work to be carried out, the location, the goods to be supplied, the place of delivery or installation, the schedule for delivery or completion, minimum performance requirements and the warranty and maintenance requirements, as well as any other terms and conditions.

9.2 SCOAPRINCIPLESANDRECORDINGOFTRANSACTIONS

9.2.1 The level of detail of transaction recording across all eight segments of SCOA lends itself to an ABC costing methodology.

9.2.2 Examples of recording renewal and maintenance transactions in SCOA are detailed in Annexure F.

10. REPORTINGONASSETCARETRANSACTIONSANDOTHERMATERIAL EVENTS

10.1 REPORTINGFORPURPOSESOFTHEANNUALFINANCIALSTATEMENTS

10.1.1 The objective of general purpose financial statements is to provide information about the financial position, financial performance and cash flows of an entity that is useful to a wide range of users in making and evaluating decisions about the allocation of resources.

FIGURE8:FINANCIALSTATEMENTS

END OF THE YEARONGOING STREAM OF BUSINESS ACTIVITYSTART OF THE YEAR

Assets – liabilities = net assets/(liabilities)

Income – Expenses = Surplus/(Deficit)

Operational Expenditures

Profitisameasureofperformance

Assess potential changes in economic resources

Assets – Liabilities = Net Assets/(Liabilities)

Capital Expenditures