Make tax season less taxing. 1 4 4 Incentive Stock Option (ISO) plans can provide you with the benefit of favorable capital gains, but can be complicated with respect to tax. To determine your tax-reporting requirements, follow the steps outlined in this document. If you are unsure if your plan is an ISO, you can easily determine this by looking up your grant type on NetBenefits ® , under your Plan Summary page. Information to help you determine your 2013 tax-reporting requirements Your Incentive Stock Option Plan TAX

Transcript

Make tax season less taxing.

14

4

Incentive Stock Option (ISO) plans can provide you with the

benefit of favorable capital gains, but can be complicated with

respect to tax. To determine your tax-reporting requirements,

follow the steps outlined in this document. If you are unsure if

your plan is an ISO, you can easily determine this by looking up

your grant type on NetBenefits®, under your Plan Summary page.

Information to help you determine your 2013 tax-reporting requirements

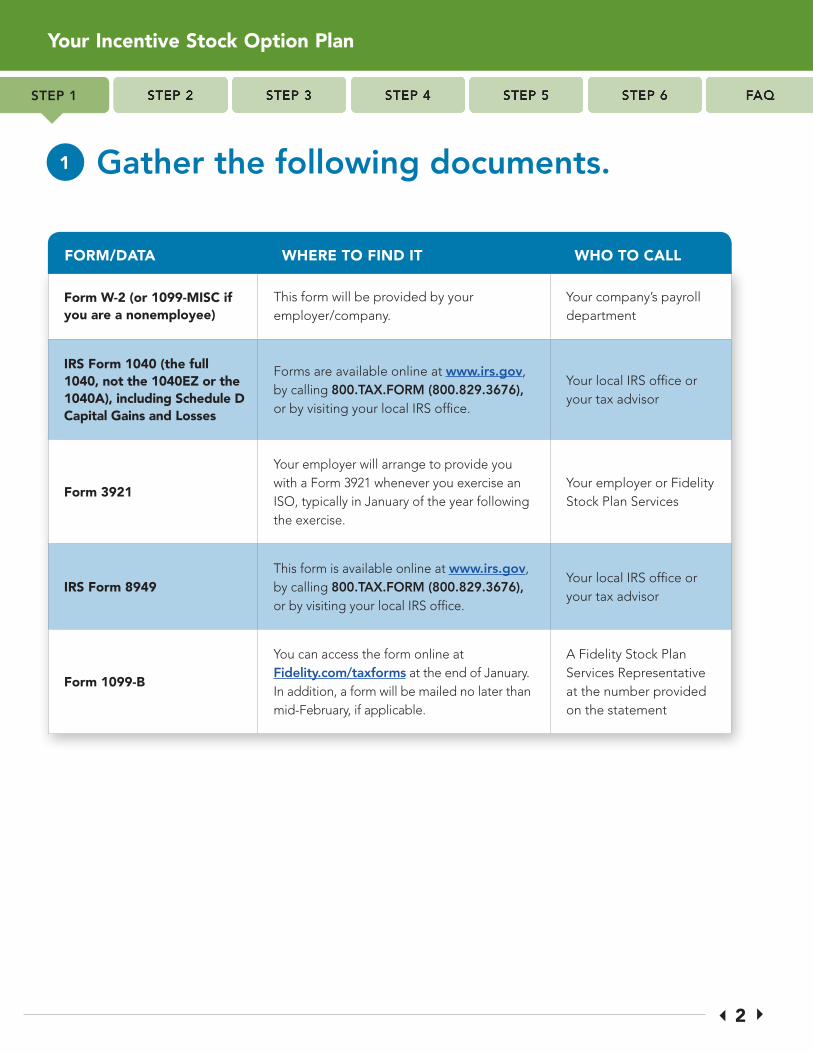

This form will be provided by your employer/company.

Your company’s payroll department

IRS Form 1040 (the full 1040, not the 1040EZ or the 1040A), including Schedule D Capital Gains and Losses

Forms are available online at www.irs.gov, by calling 800.TAX.FORM (800.829.3676), or by visiting your local IRS office.

Your local IRS office or your tax advisor

Form 3921

Your employer will arrange to provide you with a Form 3921 whenever you exercise an ISO, typically in January of the year following the exercise.

Your employer or Fidelity Stock Plan Services

IRS Form 8949 This form is available online at www.irs.gov, by calling 800.TAX.FORM (800.829.3676), or by visiting your local IRS office.

Your local IRS office or your tax advisor

Form 1099-B

You can access the form online at Fidelity.com/taxforms at the end of January. In addition, a form will be mailed no later than mid-February, if applicable.

A Fidelity Stock Plan Services Representative at the number provided on the statement

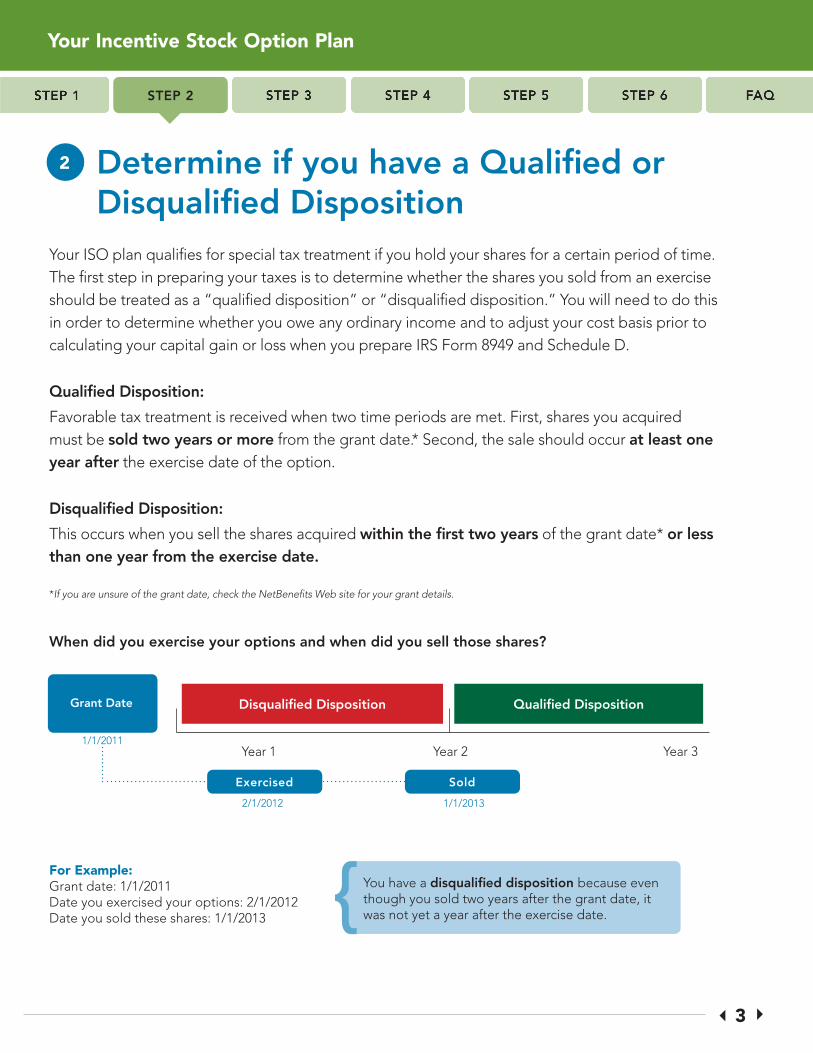

Your ISO plan qualifies for special tax treatment if you hold your shares for a certain period of time. The first step in preparing your taxes is to determine whether the shares you sold from an exercise should be treated as a “qualified disposition” or “disqualified disposition.” You will need to do this in order to determine whether you owe any ordinary income and to adjust your cost basis prior to calculating your capital gain or loss when you prepare IRS Form 8949 and Schedule D.

Qualified Disposition:

Favorable tax treatment is received when two time periods are met. First, shares you acquired must be sold two years or more from the grant date.* Second, the sale should occur at least one year after the exercise date of the option.

Disqualified Disposition:

This occurs when you sell the shares acquired within the first two years of the grant date* or less than one year from the exercise date.

* If you are unsure of the grant date, check the NetBenefits Web site for your grant details.

Determine if you have a Qualified or Disqualified Disposition

2

When did you exercise your options and when did you sell those shares?

Year 1 Year 2 Year 3

Disqualified Disposition Qualified Disposition

For Example: Grant date: 1/1/2011 Date you exercised your options: 2/1/2012Date you sold these shares: 1/1/2013

Grant Date

exercised Sold

You have a disqualified disposition because even though you sold two years after the grant date, it was not yet a year after the exercise date.{

1/1/2011

2/1/2012 1/1/2013

STep 2

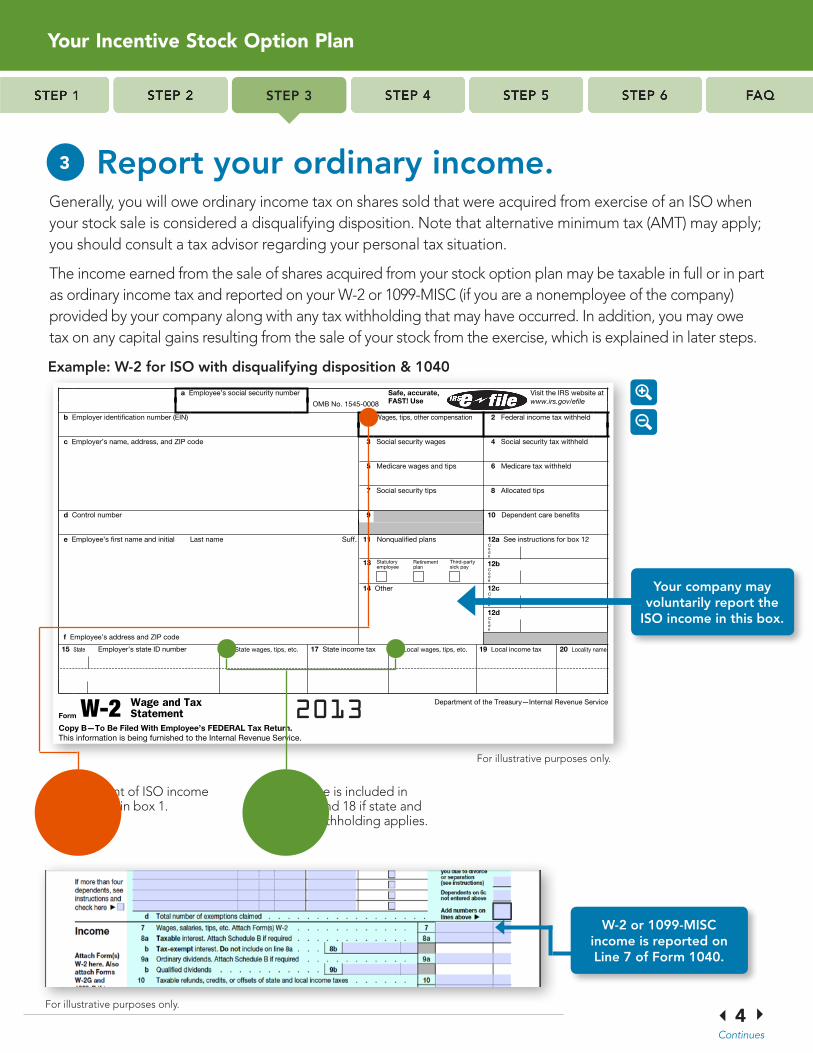

Generally, you will owe ordinary income tax on shares sold that were acquired from exercise of an ISO when your stock sale is considered a disqualifying disposition. Note that alternative minimum tax (AMT) may apply; you should consult a tax advisor regarding your personal tax situation.

The income earned from the sale of shares acquired from your stock option plan may be taxable in full or in part as ordinary income tax and reported on your W-2 or 1099-MISC (if you are a nonemployee of the company) provided by your company along with any tax withholding that may have occurred. In addition, you may owe tax on any capital gains resulting from the sale of your stock from the exercise, which is explained in later steps.

Report your ordinary income.3

44

4Your Incentive Stock Option Plan

STep 3

a Employee’s social security number

OMB No. 1545-0008

Safe, accurate, FAST! Use

Visit the IRS website at www.irs.gov/efile

b Employer identification number (EIN)

c Employer’s name, address, and ZIP code

d Control number

e Employee’s first name and initial Last name Suff.

f Employee’s address and ZIP code

1 Wages, tips, other compensation 2 Federal income tax withheld

3 Social security wages 4 Social security tax withheld

5 Medicare wages and tips 6 Medicare tax withheld

7 Social security tips 8 Allocated tips

9 10 Dependent care benefits

11 Nonqualified plans 12a See instructions for box 12Co d e

12bCo d e

12cCo d e

12dCo d e

13 Statutory employee

Retirement plan

Third-party sick pay

14 Other

15 State Employer’s state ID number 16 State wages, tips, etc. 17 State income tax 18 Local wages, tips, etc. 19 Local income tax 20 Locality name

Form W-2 Wage and Tax Statement 2014

Department of the Treasury—Internal Revenue Service

Copy B—To Be Filed With Employee’s FEDERAL Tax Return. This information is being furnished to the Internal Revenue Service.

2013

The amount of ISO income is included in box 1.

ISO income is included in boxes 16 and 18 if state and local tax withholding applies.

Your company may voluntarily report the

ISO income in this box.

W-2 or 1099-MISC income is reported on Line 7 of Form 1040.

example: W-2 for ISO with disqualifying disposition & 1040

For illustrative purposes only.

For illustrative purposes only.

Continues

A236880

Sticky Note

None set by A236880

A236880

Sticky Note

None set by A236880

a439647

Sticky Note

MigrationPending set by a439647

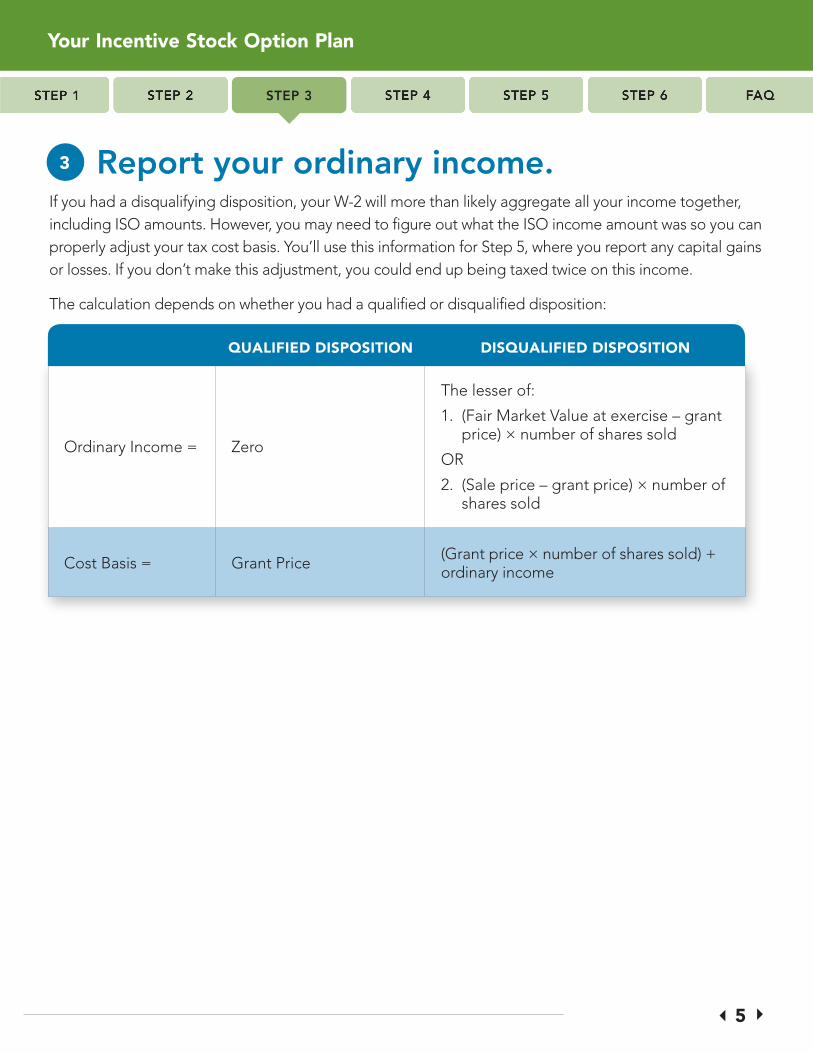

If you had a disqualifying disposition, your W-2 will more than likely aggregate all your income together, including ISO amounts. However, you may need to figure out what the ISO income amount was so you can properly adjust your tax cost basis. You’ll use this information for Step 5, where you report any capital gains or losses. If you don’t make this adjustment, you could end up being taxed twice on this income.

The calculation depends on whether you had a qualified or disqualified disposition:

Report your ordinary income.3

54

4Your Incentive Stock Option Plan

STep 3

Ordinary Income = Zero

The lesser of:

1. (Fair Market Value at exercise – grant price) × number of shares sold

OR

2. (Sale price – grant price) × number of shares sold

Cost Basis = Grant Price (Grant price × number of shares sold) + ordinary income

QuALIFIED DISPOSITIOn DISQuALIFIED DISPOSITIOn

64

4Your Incentive Stock Option Plan

Assemble information on the exercise and sale of your stock.

4

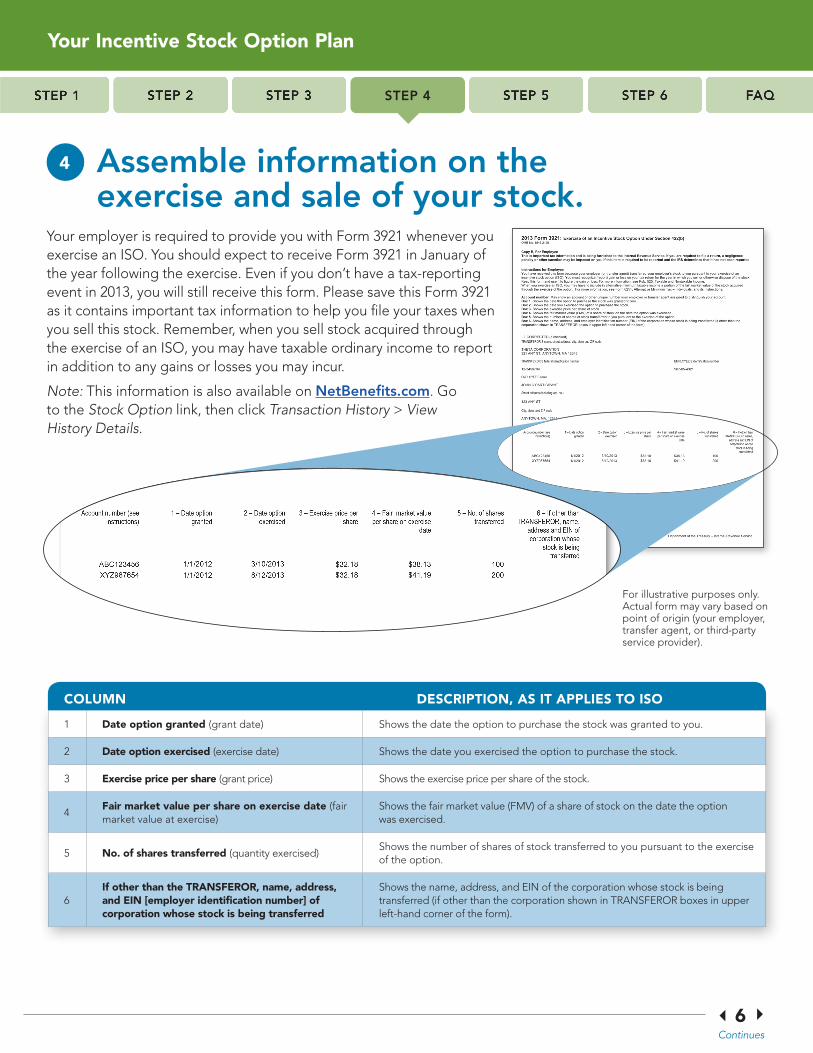

Your employer is required to provide you with Form 3921 whenever you exercise an ISO. You should expect to receive Form 3921 in January of the year following the exercise. Even if you don’t have a tax-reporting event in 2013, you will still receive this form. Please save this Form 3921 as it contains important tax information to help you file your taxes when you sell this stock. Remember, when you sell stock acquired through the exercise of an ISO, you may have taxable ordinary income to report in addition to any gains or losses you may incur.

Note: This information is also available on NetBenefits.com. Go to the Stock Option link, then click Transaction History > View History Details.

For illustrative purposes only. Actual form may vary based on point of origin (your employer, transfer agent, or third-party service provider).

1 Date option granted (grant date) Shows the date the option to purchase the stock was granted to you.

2 Date option exercised (exercise date) Shows the date you exercised the option to purchase the stock.

3 Exercise price per share (grant price) Shows the exercise price per share of the stock.

4Fair market value per share on exercise date (fair market value at exercise)

Shows the fair market value (FMV) of a share of stock on the date the option was exercised.

5 no. of shares transferred (quantity exercised)Shows the number of shares of stock transferred to you pursuant to the exercise of the option.

6If other than the TRAnSFEROR, name, address, and EIn [employer identification number] of corporation whose stock is being transferred

Shows the name, address, and EIN of the corporation whose stock is being transferred (if other than the corporation shown in TRANSFEROR boxes in upper left-hand corner of the form).

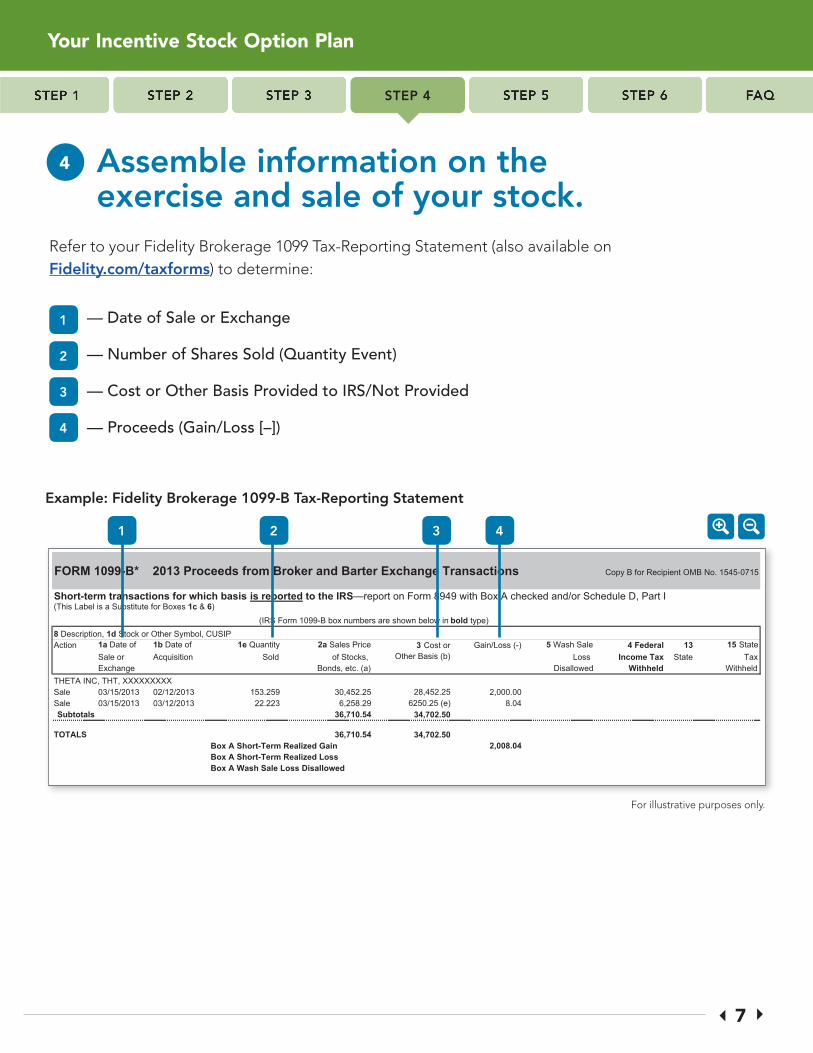

Refer to your Fidelity Brokerage 1099 Tax-Reporting Statement (also available on Fidelity.com/taxforms) to determine:

1

2

3

4

— Date of Sale or Exchange

— Number of Shares Sold (Quantity Event)

— Cost or Other Basis Provided to IRS/Not Provided

— Proceeds (Gain/Loss [–])

FORM 1099-B* 2013 Proceeds from Broker and Barter Exchange Transactions Copy B for Recipient OMB No. 1545-0715

(This Label is a Substitute for Boxes 1c & 6)

Action 1a Date of 1b Date of 1e Quantity 2a Sales Price 3 Cost or Gain/Loss (-) 5 Wash Sale 4 Federal 13 15 State Sale or Acquisition Sold of Stocks, Other Basis (b) Loss Income Tax State Tax

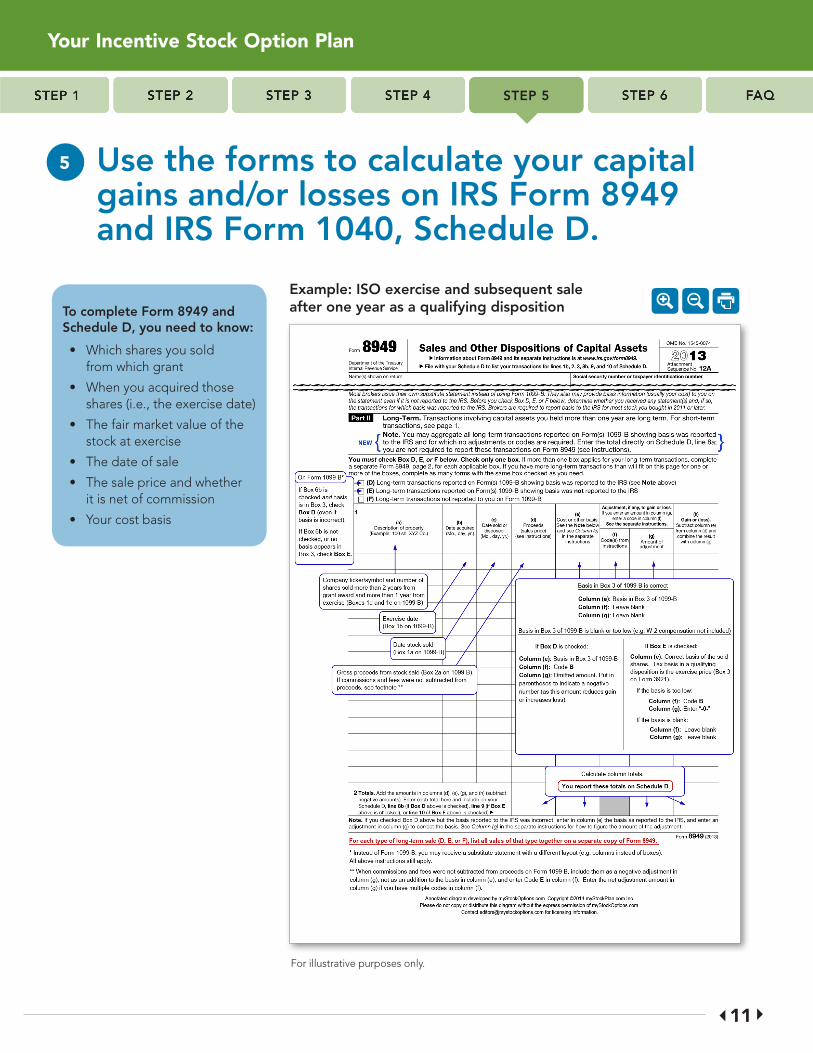

Use the forms to calculate your capital gains and/or losses on IRS Form 8949 and IRS Form 1040, Schedule D.

5

Even though the ordinary income may be reported on your W-2 or 1099-MISC, you still need to report the sale of the stock on Form 8949 and carry over the amounts to Schedule D.†

In preparation of completing these forms, consider the following:

1. How long did you hold the shares before you sold them? This determines which section of the 8949 to complete. Your holding period begins on the date you exercised your option.

Form 8949 is divided into two parts. Determine which section you will need to complete:

• Part I is for short-term capital gains or losses. Short term is defined as selling the stock less than one year from the date you acquired it.

• Part II is for long-term capital gains and losses. Long term is defined as holding the stock for more than one year from the date you acquired it.

Qualified dispositions are always considered long term; however, disqualified dispositions can be either short term or long term depending on how long you held the shares before selling them.

2. You need to figure out the ordinary income amount that may have been included in your W-2 or 1099-MISC so you can adjust your cost basis on Form 8949, if necessary. Go back to Step 3 for help.

†State and local taxes may also apply and the rules governing such taxes may vary from federal income tax rules. Please consult your tax advisor.

Continues

To complete Form 8949 and Schedule D, you need to know:

• Which shares you sold from which grant

• When you acquired those shares (i.e., the exercise date)

• The fair market value of the stock at exercise

• The date of sale

• The sale price and whether it is net of commission

• Your cost basis

For illustrative purposes only.

Use the forms to calculate your capital gains and/or losses on IRS Form 8949 and IRS Form 1040, Schedule D.

5

94

4Your Incentive Stock Option Plan

STep 5

example: ISO exercise and subsequent sale within one year as a disqualifying disposition

Continues

Use the forms to calculate your capital gains and/or losses on IRS Form 8949 and IRS Form 1040, Schedule D.

5

Your Incentive Stock Option Plan

STep 5

example: ISO exercise and subsequent sale after one year as a disqualifying disposition

For illustrative purposes only.

104

4

Continues

To complete Form 8949 and Schedule D, you need to know:

• Which shares you sold from which grant

• When you acquired those shares (i.e., the exercise date)

• The fair market value of the stock at exercise

• The date of sale

• The sale price and whether it is net of commission

• Your cost basis

Use the forms to calculate your capital gains and/or losses on IRS Form 8949 and IRS Form 1040, Schedule D.

5

114

4Your Incentive Stock Option Plan

STep 5

example: ISO exercise and subsequent sale after one year as a qualifying disposition

For illustrative purposes only.

To complete Form 8949 and Schedule D, you need to know:

• Which shares you sold from which grant

• When you acquired those shares (i.e., the exercise date)

• The fair market value of the stock at exercise

• The date of sale

• The sale price and whether it is net of commission

• Your cost basis

Use IRS Form 8949 to calculate your capital gains and/or losses on IRS Form 1040, Schedule D.

6

124

4Your Incentive Stock Option Plan

STep 6

Gain or loss from the sale of the stock should be reflected on Form 8949 and Schedule D. How this is reflected is dependent on whether the sale is short term (less than one year from the date the stock was acquired to the date it was sold) or long term (more than one year from the date acquired to the date of sale).

For illustrative purposes only.

For illustrative purposes only.

example: Short-Term Gains or Losses

example: Long-Term Gains or Losses

Frequently Asked QuestionsQ: How do the tax implications of an ISO differ from those of a nonqualified or

nonstatutory stock option (NSO)?

A: An ISO receives beneficial tax treatment. You will not be subject to tax at the time of exercise of an ISO (although the difference between the fair market value of the stock at exercise and the amount you paid for the stock will generally be treated as taxable income for alternative minimum tax purposes). When you sell shares acquired by exercise of an ISO, your gain (or loss) will generally be treated as a capital gain (or loss), provided the shares are held for the longer of one year from the exercise date and two years from the grant date. If ISO shares exercised are held for the entire holding period, then the entire amount of any gain (or loss) upon your subsequent sale of those shares will be treated as a capital gain (generally long-term capital gain, given the holding period requirement for ISOs), and taxed at the generally favorable rates applicable to capital gains, rather than as ordinary income. (You should be aware, however, that the spread at exercise will be taken into account as alternative minimum taxable income.‡

In contrast, when you exercise an NSO, the difference between the fair market value of the stock at the time of exercise and your exercise cost will be treated as ordinary compensation income, and your employer will generally be required to withhold taxes at the time of your exercise. Upon your sale of the stock (whether at the time of exercise or some later date), your gain or loss (the sale proceeds minus your adjusted basis in the stock) will be subject to tax, generally as a capital gain (or loss), assuming you hold the stock as a capital asset.

Q: What is an Alternative Minimum Tax or AMT?

A: Congress created the AMT as an alternative form of federal income taxation to ensure that wealthy individuals and corporate taxpayers pay a fair share of federal income taxes. Its reach, however, now sometimes extends beyond the wealthy.

The AMT is a tax system that works in parallel with the regular federal income tax system — while some taxpayers use the regular system, others must use the AMT system. The AMT has its own set of forms, rates, rules, and brackets, and requires taxpayers to calculate their federal income tax using this system.

Exercising incentive stock options that are “deep in the money” (on which gain is usually deferrable and taxed as capital gain income) can potentially subject an individual to AMT. You will want to discuss this with a qualified tax advisor to see if this applies to you.

Your Incentive Stock Option Plan

FAQ

134

4‡Please see a tax advisor as to your specific tax amounts due.

Continues

Frequently Asked QuestionsQ: Why do I show a capital loss on my 1099-B from my exercise?

A: Generally speaking, amounts that appear as a loss on a 1099-B are usually as a result of a commission or fee that has been charged, along with any market-related loss on the stock sale.

Q: What is a wash sale?

A: A wash sale occurs when you sell shares at a loss and buy additional shares of the same security within a 61-day period, beginning 30 days before the sale and ending 30 days after the sale, including the date of the sale. If the sale results in a wash sale, generally you will not be able to deduct the resulting loss. For assistance with completing your tax return, please consult your tax advisor.

Q: Will I owe other taxable amounts beyond federal tax?

A: State and local taxes may also apply, and the rules governing such taxes may vary from federal income tax rules. Please consult your tax advisor for more information.

Go back to the Fidelity Resource Center

Tax laws are complex and subject to change. State and local taxes may also apply, and the rules governing such taxes may vary from federal income tax rules. Your actual income tax consequences depend on your individual circumstances. Therefore, you should always consult a qualified tax advisor regarding your own particular tax situation.