39

M&A and Private Debt Market Observations Where We’re Going the Rest of 2020 & Review of 2019

M&A and Private Debt Market Observations

Where We’re Going the Rest of 2020

& Review of 2019

I. BCA Introduction

II. 2020 Outlook

I. Economic Activity

II. M&A Activity

III. Private Equity

IV. Debt Markets

III. Industry Spotlight

I. Managed IT Services

II. Food and Beverage

III. E-Commerce

IV. A Closer Look

I. SPACs

V. 2019 M&A Market Review

VI. 2019 Middle Market Review

VII. 2020 Strategic Planning

VIII. Conclusions

IX. Contact Us

Table of Contents

Click the link to go directly to the section

2

Bravaldo Capital Advisors A Boutique M&A and Corporate Finance Advisory Firm

• Focus on underserved LowerMiddle Market companieswith sales of $10M-300M

• Provide three main lines ofservice:

• Sell-Side Advisory

• Buy-Side Advisory

• Corporate Finance

• Offer a unique advisorymodel addressing businesspositioning and readinessissues

BCA Introduction

3

• Seller Advisory Services - Advising private business owners regarding the sale,recapitalization, or divestiture of businesses.

• Buyer Advisory Services - Advising client companies regarding acquisition searches,valuation, structuring, negotiations and raising capital to affect acquisitions.

• Placements of Debt - Assisting client companies in recapitalizing/raising senior andmezzanine/subordinated debt capital.

• Other Advisory Services - ESOP exit advisory, strategic exit planning consulting,management buyouts, acquisition or divestiture of specific purpose commercialreal estate, distressed sale process - bankruptcy and non-bankruptcy.

BCA Services

BCA Introduction

4

Key Differentiators

• Selective about engagements - focus on 5-7 high quality transactions per year

• Referral driven from trusted advisors

• Senior professionals working in a team format able to devote personalized hightouch involvement with each client

• Wide range of industry experience with focus on certain sized transactions facingcommon set of readiness issues

• Process driven approach tailored for each engagement that reduces execution riskand maximizes value

• International reach with cross-border expertise/relationships and multi-lingualteam members

• Network of 5,000+ contacts including financial and strategic buyers andtrusted advisors in professional communities throughout the country

BCA Introduction

5

The Bravaldo Capital Advisors Team is a senior deal team with extensive knowledge andinsight into the full life cycle of M&A efforts. This depth of skill and expertise acrossindustries, when combined with the client-focused approach, offers our clientsunparalleled service during the engagement.

Bravaldo Capital Advisors Meet Our Team

BCA Introduction

Don Bravaldo, CPAPresident

Mark HeymanSenior Vice President

Brady OsborneSenior Associate

Eric StreseAssociate

Janine McPartlandOffice Manager

Jeanne PearsonBusiness Development

Associate

JP JobinBusiness Development

Associate

Barath RaoAnalyst Intern

George MacConnellSr. Board Advisor, Operations

Bob ThomasSr. Board Advisor, Operations

Jeff CohenSr. Board Advisor, Operations

Paul CarmodySr. Board Advisor, Technology

Bret SperlingSr. Board Advisor

Rick HigdonSr. Board Advisor, Sell-Side

Eric JacobsBoard Advisor, Sell-Side

Oliver DunatovBoard Advisor, Buy-Side

6

2020 M&A Activity Summary

COVID-19 Recession

Strategic M&A

The COVID-19 pandemic has had devastating effects on both the U.S. and globaleconomy. Consumer activity dropped significantly due to shutdowns, and manycountries saw rapid increases in unemployment, sparking recessions worldwide.

The pandemic largely disrupted M&A activity, with many companies inwardly focusedon enduring the pandemic rather than acquiring new enterprises. The number of Q2deals declined drastically, with many being terminated. Some deals on hold, however,are expected to resume post-pandemic.

Private equity groups (“PE”, “PEG”, or “PEGs”) initially spent the pandemic internally,focused on helping their current portfolio companies survive. Halfway through Q2, PEGsbegan to return to market and invest in industries thriving from the pandemic.

Financing in 2020 tightened in Q2, with most of the lending being PPP loans and otherforms of government relief. As the economy has begun to reopen, liquidity hasimproved, and leverage multiples have started to rebound but are still nowhere near2019 standards.

While many industries took a hit from the pandemic, others were able to flourish. Forexample, Managed IT Services, Food and Beverage, and E-Commerce valuations allremained healthy despite the uncertainty.

7

2020 Outlook

Strategic M&A

Strategic M&A

Private Equity

Debt Markets

Industry Highlights

Gross domestic product decreased at a 32.9% annualizedrate last in Q2 2020, the largest drop since the U.S.government started keeping records in 1947. The economycontracted at a 5.0% pace in Q1 2020 and fell into recessionin February. Although economic activity picked up in Maydue to easing of lockdown orders, momentum has sloweddue to uncertainties caused by COVID.

2020 Outlook: Economic ActivityCOVID-19 Recession

With COVID-19 cases climbing dramatically, U.S. economicrecovery will be slow. As a result of consumer and businessspending plummeting in Q2, the U.S. economy suffered itshardest hit since the Great Depression. With stay-at-homeorders initially going into effect to halt the spread of thevirus, more than five years of growth have been effectivelywiped out.

2020 Outlook

Source: Reuters, “COVID-19 crushes U.S. economy in second quarter; rising virus cases loom over recovery”

8

3.8% 2.7% 2.1% 1.3% 2.9% 1.5% 2.6% 2.4%

-5.0%

-31.7%-40%

-30%

-20%

-10%

0%

10%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

Per

cen

tage

ch

ange

(%

)

20192018

U.S. Employment

Current Economic Conditions GDP

Layoffs have also dramatically increased as a result of thepandemic. Millions of people lost their jobs in Q2, with theunemployment rate jumping to 14.7% in April, the highestlevel since the Great Depression. Consequently, Congresshas passed four spending bills amounting to several trilliondollars in stimulus to mitigate the effects of unemploymentand help strengthen consumer spending. Since thepandemic has lasted longer than originally anticipated,another round of stimulus may be necessary.

% Change GDP

2020

Q1 North American M&A deal value totaled approximately $400.8 billion across 3,169 transactions, whichrepresented a 25.1% decline in deal value year-over-year and 2.6% gain in deal volume. M&A activity was able toreach this amount since most Q1 deals had already closed pre-pandemic. However, as the quarter progressed,there was a shortage of large deals because of corporate pull-back due to virus concerns. Q2 saw continueddeclines with a total of $336.8 billion across 2,025 transactions, declines of 33.1% and 26.7% respectively from Q22019.

2020 Outlook: M&A Activity

2020 Outlook

Source: PitchBook Q1 2020 North American M&A Report PitchBook Q2 2020 North American M&A Report *As of 6/30/2020

9

$1

,72

2.8

$1

,15

0.4

$7

04

.7

$1

,04

0.1

$1

,14

6.7

$1

,31

4.0

$1

,22

9.2

$1

,75

6.0

$2

,00

6.7

$2

,15

9.2

$1

,93

3.1

$2

,38

9.2

$2

,23

2.0

$7

80

.9

10,168

8,837

6,961

8,832

10,127 11,157

10,546

13,162 14,150

12,904

12,953

13,514 12,702

5,460

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020*

Deal value ($B) Estimated deal value ($B) Estimated # of deals closed

Dea

l Val

ue

($B

)

Dea

l Co

un

t

M&A Activity by Year

2020 Outlook: M&A ActivityEBITDA Multiples

In Q1 2020, North American valuations slightly dipped with the medianEV/EBITDA multiple finishing at 9.8x. As the effects of the pandemic came intoplay in Q2, valuations increased to 10.5x, largely because of median deal sizesincreasing in the healthcare, tech, and oil and gas sectors. Valuation issues werecommon in Q2, as it proved challenging to value assets during the COVID-19 era.

Source: PitchBook Q2 2020 North American M&A Report

10

EV/EBITDA in North America- for Transactions $25 to $1B

8.9x

9.2x9.1x

9.5x

10.1x10.2x

9.4x

10.1x

8.0x

8.5x

9.0x

9.5x

10.0x

10.5x

2012 2013 2014 2015 2016 2017 2018 2019

EV/E

BIT

DA

Mu

ltip

le

Year

8.9x9.0x 9.1x

9.4x

10.1x 10.0x

9.6x

9.9x

10.5x

8.0x

8.5x

9.0x

9.5x

10.0x

10.5x

11.0x

2012 2013 2014 2015 2016 2017 2018 2019 2020*

EV/E

BIT

DA

Mu

ltip

le

Year

Median North American EV/EBITDA Multiples

*As of 6/30/2020

2020 Outlook

2020 Outlook: M&A ActivityTerminated Deals

Many large deals have been called off or expect to becalled off due to the pandemic. Most notably, XeroxHoldings Corp called off its $37 billion acquisition of HPInc. As of June 25th, 2020, total value of terminateddeals has reached $103 billion. Many terminated dealsin the first half of 2020 were negotiated and pricedpre-COVID. The deals negotiated in the second half of2020, however, will reflect the impact of the pandemicand will likely carry out to completion.

There has also been much debate as to whetherCOVID-19 constitutes a material adverse effect (MAE).In one of the more extreme cases, REIT Simon PropertyGroup terminated its acquisition of Taubman Centers,Inc. on the grounds that Taubman suffered an MAE anddid not react appropriately to support its operations. Inresponse, Taubman claimed REIT Simon’s terminationwas invalid, and the deal is now heading to court.

2020 Outlook

Source: Capital IQ, “More than $100B of M&A Deals Terminated Amid ‘New World Order’ of COVID-19”

11

Most at Risk through COVID-19

2020 Outlook

The most resilient sectors will see an influx of growth capital and acquisitions, while at-risk businesses will likely seeincreased distressed M&A activity. Billions of dollars remain on the sidelines looking to be invested in companiesdepending on performance and industry characteristics.

Source: The Journal Record, “M&A Outlook 2020 and COVID-19 Update”

12

Most Resilient through COVID-19

2020 Outlook: M&A ActivityM&A Market and Sector Predictions

2020 Outlook: M&A ActivityForecast Timeline

NowRest

of 2020

2021

Sidelined deals will resume, with potential for price adjustments and changes to deal structure

Leverage multiples will decrease, requiring bonus equity to fund the transaction

Acquirers reevaluate priorities (new strengths and weaknesses)

Industry consolidation may increase (vertical and horizontal integration)

Distressed/discounted acquisition opportunities will rise

Divestitures of non-core businesses to raise cash

Companies will embrace digital transformations

Restructuring of balance sheet; recapitalizations

Expedited industry roll-ups

Expedited divestiture of weaker portfolio companies

Increase in exits for business owners who survived the pandemic, but no longer want to continue

Resumption of 2020 transactions that were sidelined

Source: The Journal Record, “M&A Outlook 2020 and COVID-19 Update”

13

2020 Outlook

2020 Outlook: Private Equity

2020 Outlook

*As of 6/30/2020

14

Source: PitchBook Q2 2020 US PE Breakdown Summary

In Q1, U.S. private equity deal activity totaled $186 billion across 1.384 transactions, YoY gains of 6.0% and 7.3%respectively. Most of these deals had been fully negotiated prior to COVID-19, as many deals still in process duringthe pandemic have been called off or postponed. The impact of the pandemic became more apparent in Q2, withonly 784 more deals closing. Through the first half of 2020, 2,173 private equity deals were closed for a total of$327 billion, down nearly 20% from the first half of 2019.

$7

48

.0

$3

29

.5

$1

37

.3

$2

84

.1

$3

40

.7

$3

76

.7

$4

31

.0

$5

31

.2

$5

06

.9

$6

07

.8

$6

21

.7

$7

56

.4

$7

95

.2

$3

26

.7

3,509

2,754

1,897

2,7963,157

3,5503,401

4,2344,454 4,477

4,821

5,495 5,428

2,173

0

1,000

2,000

3,000

4,000

5,000

6,000

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020*

Deal value ($B) Estimated deal value ($B) Estimated # of deals closed

Dea

l Val

ue

($B

)

Dea

l Co

un

t

Private Equity Deal Activity by Year

2020 Outlook: Private EquityValuations and Transaction Multiples

2020 Outlook

15

Despite the pandemic-induced crisis, Q2 valuations in PE lower middle market transactions remainedunchanged from Q1 (it is important to note that there were only 31 completed deals in the dataset).These transactions likely involved some combination of fully digested propositions by buyers pre-COVID,industry sectors with decent visibility throughout the pandemic, and buyers willing to use more equitythan in the past to close.

Source: GF Data® August 2020 M&A Report

6.8x

7.2x 7.3x7.1x

7.4x 7.4x

0

20

40

60

80

100

5.0x

5.5x

6.0x

6.5x

7.0x

7.5x

8.0x

Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020

Nu

mb

er o

f Tr

ansa

ctio

ns

EV/E

BIT

DA

Mu

ltip

le

Quarter

EBITDA MultiplesPrivate Equity Transactions with Enterprise Values $10M-$250M

EV/EBITDA Number of transactions

2020 Outlook

2020 Outlook: Private EquityLeverage Multiples

16

Source: GF Data® August 2020 Leverage Report

2.9x4.0x

0.6x

0.3x

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

Platform Add-ons

Private Equity Debt Multiples Platforms vs. Add-ons (2020 YTD)

Sr Debt/EBITDA Sub Debt/EBITDA

3.0x 3.3x 3.0x 3.2x 3.3x

0.8x0.9x

0.8x 0.8x 0.5x

0.0x

1.0x

2.0x

3.0x

4.0x

2016 2017 2018 2019 2020 YTD

Private Equity Debt Multiples Total by Year

SR DEBT/EBITDA SUB DEBT/EBITDA

Leverage data in 2020 has reflected two drastically different quarters. Q1 represented an accommodatingleverage environment, while Q2 represented a more conservative environment impacted by the pandemic. Asthe pandemic progressed, aggregate debt levels pulled back dramatically, with total debt falling from 3.9x to 3.3xand senior debt falling from 3.4x to 2.8x. Average debt in unitranche deals declined as well, from 3.6x to 3.0x,and average debt from commercial banks plummeted, falling from 4.0x to 2.6x.

2020 Outlook

2020 Outlook: Private EquityComposition of Financing

17

Source: GF Data® August 2020 Leverage Report

43.0% 44.5% 39.9% 43.6% 42.5%

12.2% 10.8%11.2% 10.1% 6.5%

44.8% 44.7% 48.9% 46.4% 51.0%

0%

25%

50%

75%

100%

2016 2017 2018 2019 2020 YTD

Equity and Debt Contribution by Year

Senior Debt Sub Debt Equity

Equity has represented a larger proportion of the average capital structurein 2020, increasing by almost 5% from the previous year. Closing dealsrequired buyers to “over-equitize” because of the more conservativelending environment. The average equity contribution for 2020 of 51%breaks out into 48.7% in Q1 and nearly 8% higher at 56.5% in Q2.

2020 Outlook: Private EquityHolding Time and Exits

2020 Outlook

Source: PitchBook Q2 2020 US PE Breakdown Summary

18

0%10%20%30%40%50%60%70%80%90%

100%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2017 2018 2019 2020

Year

PE Exits ($) by Type

Corporate acquisition IPO SBO

%

*As of March 31st, 2020

Ho

ldin

g Ti

me

Year

s

0

1

2

3

4

5

6

7

2012 2013 2014 2015 2016 2017 2018 2019 2020*

Year

Median PE Holding Time (years) by Size

Similarly to the 2008 financial crisis, PEGs have resorted to increasing the amount of equity used in buyouts. The difficulties

of obtaining leverage and closing deals has led U.S. PEGs to sit on large amounts of cash, also known as “dry powder”.

Currently, PEGs are estimated to be holding nearly $1.5 trillion in dry powder. Market uncertainty will likely lead to

alternative types of investments such as PIPE deals or minority deals rather than buyouts. PEGs also appear to be extending

their holding periods rather than exiting their investments at a significantly discounted value. Shown below are the tracking

of median PE holding times by size and PE exits by type. It is likely that overall median PE holding time will continue to

increase.

2020 Outlook

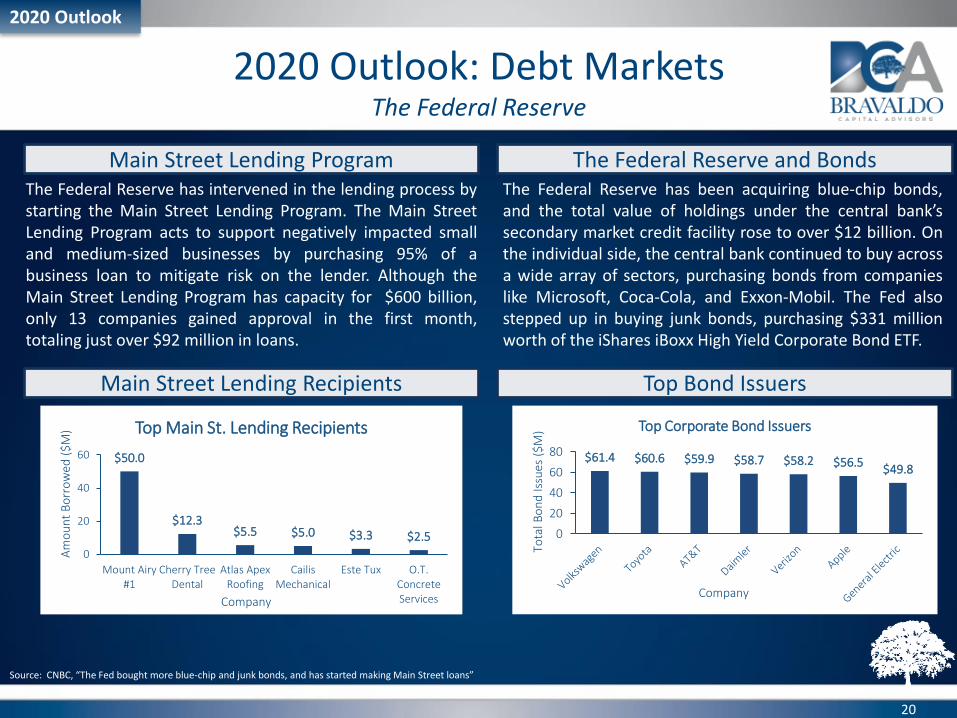

2020 Outlook: Debt MarketsPPP and Lending

Source: S&P Global Market Intelligence, “Bankers showing ‘tough love’ in commercial lending amid COVID-19 uncertainty”Forbes, “Simplifying the PPP Loan Forgiveness Process”

19

Excluding PPP, other loans have been declining since April.Due to increased risk and uncertainty, banks are being asconservative as possible, especially with new customers.Many bankers are uncertain as to what losses are going tolook like, and as a result, have tightened their standards onC&I, commercial real estate, and consumer loans.

To alleviate economic distress caused by COVID-19, the U.S.government instituted the Paycheck Protection Program(PPP) to help small businesses. Since the launch of theprogram, 5,500 lenders have made a total of 4.9 millionloans totaling $521 billion to fund small businesses thatwould have otherwise failed. These loans have preservedover 51 million jobs nationwide (84% of the nation’s smallbusiness payroll) throughout the pandemic.

Total Loans and Leases

Paycheck Protection Program (PPP) Other Loans

Consumer & Industrial (C&I) Loans

2020 Outlook

2020 Outlook: Debt MarketsThe Federal Reserve

Source: CNBC, “The Fed bought more blue-chip and junk bonds, and has started making Main Street loans”

20

The Federal Reserve has been acquiring blue-chip bonds,and the total value of holdings under the central bank’ssecondary market credit facility rose to over $12 billion. Onthe individual side, the central bank continued to buy acrossa wide array of sectors, purchasing bonds from companieslike Microsoft, Coca-Cola, and Exxon-Mobil. The Fed alsostepped up in buying junk bonds, purchasing $331 millionworth of the iShares iBoxx High Yield Corporate Bond ETF.

The Federal Reserve has intervened in the lending process bystarting the Main Street Lending Program. The Main StreetLending Program acts to support negatively impacted smalland medium-sized businesses by purchasing 95% of abusiness loan to mitigate risk on the lender. Although theMain Street Lending Program has capacity for $600 billion,only 13 companies gained approval in the first month,totaling just over $92 million in loans.

Main Street Lending Recipients

Main Street Lending Program The Federal Reserve and Bonds

Top Bond Issuers

$61.4 $60.6 $59.9 $58.7 $58.2 $56.5$49.8

0

20

40

60

80

Tota

l Bo

nd

Issu

es (

$M

) Top Corporate Bond Issuers

Company

$50.0

$12.3$5.5 $5.0 $3.3 $2.5

0

20

40

60

Mount Airy#1

Cherry TreeDental

Atlas ApexRoofing

CailisMechanical

Este Tux O.T.ConcreteServices

Am

ou

nt

Bo

rro

wed

($

M) Top Main St. Lending Recipients

Company

Industry Spotlight: Managed IT Services

Industry Spotlight

21

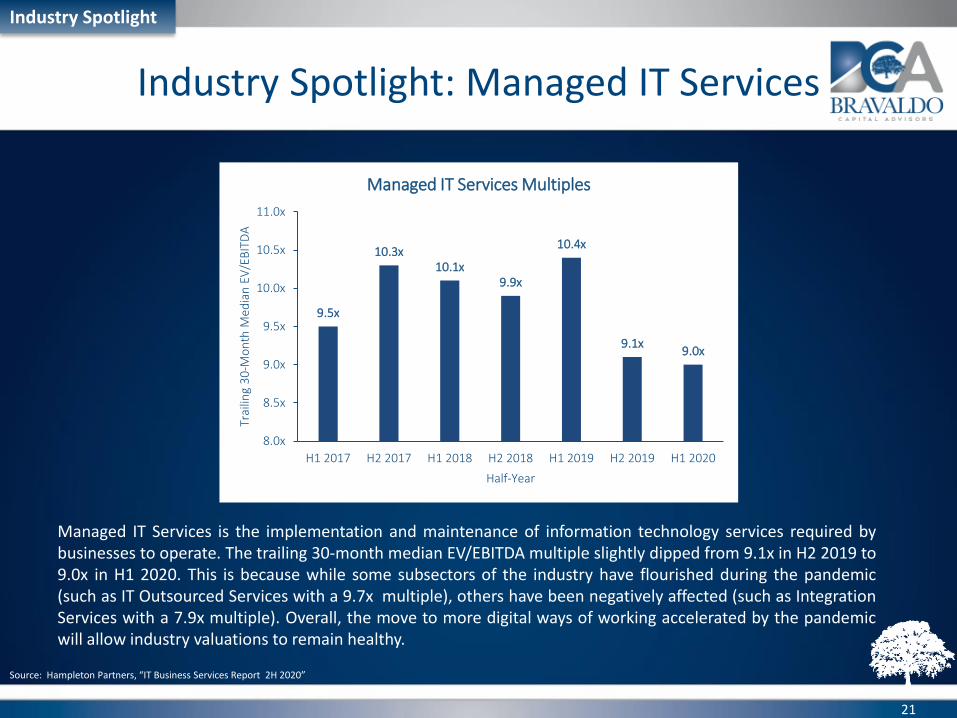

Managed IT Services is the implementation and maintenance of information technology services required bybusinesses to operate. The trailing 30-month median EV/EBITDA multiple slightly dipped from 9.1x in H2 2019 to9.0x in H1 2020. This is because while some subsectors of the industry have flourished during the pandemic(such as IT Outsourced Services with a 9.7x multiple), others have been negatively affected (such as IntegrationServices with a 7.9x multiple). Overall, the move to more digital ways of working accelerated by the pandemicwill allow industry valuations to remain healthy.

Source: Hampleton Partners, “IT Business Services Report 2H 2020”

9.5x

10.3x10.1x

9.9x

10.4x

9.1x9.0x

8.0x

8.5x

9.0x

9.5x

10.0x

10.5x

11.0x

H1 2017 H2 2017 H1 2018 H2 2018 H1 2019 H2 2019 H1 2020

Trai

ling

30

-Mo

nth

Med

ian

EV

/EB

ITD

A

Half-Year

Managed IT Services Multiples

Industry Spotlight

22

14.0x 13.7x 13.7x12.7x

13.6x 13.2x14.2x 14.5x

11.2x

13.3x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

EV/E

BIT

DA

Mu

ltip

le

Year

Public Food and Beverage Trading Multiples

2018

In Q2, the Food and Beverage industry saw a lower number of transactions, but higher valuations compared toQ1. Most deal activity was in the Packaged Foods and Meats sector, accounting for 42% of industry transactionvolume. Strategic buyers dominated deal activity, accounting for 88% of all M&A activity in the space. PublicFood and Beverage companies traded at higher multiples in Q2 due to strong recovery from COVID-impactedQ1. The overall industry saw an increase in EV/EBITDA and EV/Revenue multiples of 19% and 13% respectively.

Source: Greenwich Capital Group, “Industry Update Food & Beverage Q2 2020”

2019 2020

Industry Spotlight: Food and Beverage

Industry Spotlight: E-Commerce

Industry Spotlight

23

With stay-at-home orders initially in place, many consumers created and reinforced online buying habits. Thesehabits will replace store and mall visits until a vaccine is in place, and they may even persist beyond thepandemic. As a result, e-commerce companies have seen significant growth during Q2. Valuations fell below thebroader market earlier this year but rebounded in Q2, as online consumer spending greatly increased. Overall,the public EV/EBITDA multiple for the industry finished Q2 strong at 17.1x.

Source: Peakstone, “E-Commerce Industry Insight June 2020”

Comparable Valuation Trends – EV/EBITDA

A Closer Look: SPACsSpecial Purpose Acquisition Companies

A Closer Look

24

Source: CNBC, “NYSE gets approval for cheaper IPO alternative for companies amid SPAC boom”Graph: Harvard Law School Forum on Corporate Governance, “Update on Special Purpose Acquisition Companies”

As the COVID-19 pandemic roils the market and causesextreme volatility, many companies have forgone thetraditional IPO process, choosing the SPAC route instead.Companies such as Nikola and DraftKings both went theSPAC route to get listed on exchanges, and PalantirTechnologies recently announced its plan to debut on anexchange with a direct listing as well. As of the end of Q2,there have been 67 SPAC offerings for a total around $12billion this year, far surpassing any other year.

$2.1

$3.5

$2.6 $2.5

$3.4 $3.5 $3.3 $3.4$3.9

$8.1

0

1

2

3

4

5

6

7

8

9

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

SPA

C P

roce

eds

($B

)

SPAC Proceeds by Quarter ($B)

2018 2019 2020Year

What are SPACs?

SPACs in 2020

Special purpose acquisition companies (SPACs) arebackdoor ways for companies to issue new shares and getlisted on exchanges. SPACs are blank-check companiesformed to raise capital to finance a merger or acquisition.Typically, they must complete the deal within two years, orthey face liquidation and must return their funds toinvestors. The target firm of the SPAC is then taken publicthrough the acquisition. The SPAC route is seen as a cheaperalternative to the initial public offering (IPO) process.

2019 M&A Activity Summary

Deal Flow and Value

Strategic M&A

The global M&A market reached $3.33 trillion in deal value across 19,322 deals, a 6.9%decrease in value and a slight dip in volume from 2018. The U.S. accounted for thehighest portion of deal value at 47.2%, the highest share since 2001.

North American M&A value came in at $2 trillion for 2019, 12% lower than 2018’srecord level. Median deal size in North America grew from $51 million in 2018 to $76million in 2019, and the EV/EBITDA median multiple ended the year at 10.1x, toppinglast year’s multiple of 9.4x, and in line with those of 2016/2017.

Private equity groups paid high prices in 2019 with their $300 billion of freshly raisedcapital. They continued to invest in non-cyclical businesses such as healthcare andsoftware, accounting for 39.2% of deal activity.

Middle market deal value totaled $374 billion across 2,687 deals through September2019, putting 2019 on track to surpass 2018’s record highs. Deal activity was verystrong, with median deal size at $205 million despite lower-priced add-on acquisitionsrising to 69% of all deal flow.

Technology continued to remain active with its increasing necessity, and recurring revenues and scalability made tech firms highly desirable M&A targets. With growing necessity of modern tech, traditionally non-technology companies aimed to acquire technology and knowledge rather than develop it in-house.

25

Strategic M&A

North America

Private Equity

Middle Market

Sector Highlights

2019 M&A Market Review

• Globally in 2019, there were 19,322 deals totaling$3.33 trillion., down 6.9% from 2018’s record yearof $3.58 trillion in deal value.

• Deal making decreased in the second half of 2019,down 24.2% in value compared to the first half.

• The U.S accounted for 47% of global M&A value,representing the country’s highest share since 2001.Europe’s share fell to 23%.

• European cross-border deal activity fell from $1.35Tin 2018 to $1.27 trillion in 2019. This decrease wasdriven by a sharp drop in APAC (Asian PacificAdvisory Committee) investments.

• North American cross-border activity inboundtransaction value in 2019 was $296 billion, a 24.4%increase from 2018. Outbound transaction valuewas $335 billion, a 3% decrease from 2018.

• Strategic buyers have closed on average three timesmore global M&A transactions per year than privateequity.

The Global M&A MarketM&A Value by Quarter

2019 M&A Market Review

*In this analysis, data is based on transactions over $5M andfrom Mergermarket’s M&A deals database. Deals withundisclosed deal values are included where the target’srevenue exceeds $10M. Deals where the effective stakeacquired is less than 30% will only be included if the value isgreater than $100M.

Source: Mergermarket Global and Regional M&A Report FY 2019; Mergermarket Monthly M&A Insider January 2019

26

$571 $762 $626 $763 $955 $917

$963$1,041

$743$758

$1,080 $980

$839

$870

$717$717

$790$666

$826

$1,201

$959$954

$754$771

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

2014 2015 2016 2017 2018 2019

Year

Global Quarterly Breakdown*2014-2019

Q1 Q2 Q3 Q4

Dea

l Val

ue

(US

$B

)

North American Deal Activity

2019 North American deal value totaled $2.0 trillion. The number of deals was around 11,000, a 12.3%decline from 2018’s record year yet healthy given 2019’s geopolitical uncertainty and concerns about animpending U.S. downturn. The median EV/EBITDA multiple was 10.1x, driven by several factors includinglarger deal sizes (which tend to command higher multiples), a low interest rate environment, and increasedcompetition for deals. The second half of 2019 finished strong with the largest deal of the year, Bristol-MyersSquibb’s acquisition of drug-maker Celgene, closing in the fourth quarter.

2019 M&A Market Review

Source: PitchBook 2019 Annual North American M&A Report

27

$1

,16

6.0

$7

07

.0

$1

,03

8.8

$1

,14

6.0

$1

,32

8.2

$1

,19

8.3

$1

,77

8.7

$2

,03

0.5

$2

,17

6.8

$1

,99

3.5

$2

,35

2.6

$2

,01

3.2

8,740

6,873

8,725

10,003

11,040 10,475

13,062 14,004

12,720 12,646

12,890

11,304

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

$0

$500

$1,000

$1,500

$2,000

$2,500

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Deal value ($B) Estimated deal value ($B) Deal count Estimated # of deals closed

Dea

l Val

ue

($B

)

Dea

l Co

un

t

North American Deal Activity by Year

For North American transactions under $500 million, 2019 saw median deal size rise by $25 million, up by 49%.Several key factors drove this trend toward larger deals, including a 53% increase in private equity platformacquisitions where PEGs were willing to pay up for attractive assets and increased corporate purchases of mature,more attractive VC-backed companies, seen as cost-effective ways to acquire technologies rather than develop themorganically. With a healthy fundraising environment and large corporate cash positions, both private equity andstrategic acquirers continued to have large amounts of capital ready to deploy.

North American M&A Deal SizeTransactions under $500M

2019 M&A Market Review

Source: PitchBook 2019 Annual North American M&A Report

28

$33 $30

$36

$31

$42

$50 $51

$76

$0

$10

$20

$30

$40

$50

$60

$70

$80

2012 2013 2014 2015 2016 2017 2018 2019

Med

ian

M&

A D

eal S

ize

($M

)

Year

Median M&A Deal Size ($M)North American Transactions under $500M

% of M&A Deal Value by Deal SizeNorth American Transactions under $500M

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015 2016 2017 2018 2019

Year

$250M-$500M$100M-$250MUnder$100M

%

North American M&A Deal ValuationsEBITDA Multiples

2019 M&A Market Review

In 2019, North American EV/EBITDA deal multiples surpassed levels seen in 2018,coming back inline with 2016/2017 valuations. Contributing factors stemmedfrom a low interest rate environment, intense competition for deals, and largertransactions in the healthcare and media industries.

Source: PitchBook 2019 North American M&A Report

29

EV/EBITDA in North America- for Transactions $25 to $1B

8.9x

9.2x9.1x

9.5x

10.1x10.2x

9.4x

10.1x

8.0x

8.5x

9.0x

9.5x

10.0x

10.5x

2012 2013 2014 2015 2016 2017 2018 2019

EV/E

BIT

DA

Mu

ltip

le

Year

Top Sectors in North AmericaWhich Sectors Were Most Attractive in 2019?

Source: Mergermarket Deal Drivers Americas FY 2019Graph: PitchBook 2019 Annual North America M&A Report

Business-to-business (B2B) services ranked asthe most active sector in North America for2019. B2B services represents one of thelargest sectors of the global economy andconsists of about 400,000 businesses in theU.S. alone. The high number of M&A deals inthis space was largely because the sectorconsists of many asset-light, people-heavybusinesses, providing low capitalrequirements for deals.

Following B2B services, IT and B2C serviceshad 1,946 and 1,645 deals, respectively. TheIT sector was driven mainly by businesses thatview M&A as the primary form of businessgrowth, which has led to strong M&A activityyear in and year out. B2C services also had asignificant number of deals in 2019; total dealvolume, however, in the sector decreased by18% from the year prior.

2019 M&A Market Review

30

3,074 2,256 2,912 3,432 3,979 3,729 4,648 4,951 4,344 4,239 4,467 3,568

1,6141,280 1,532 1,831 2,044 2,032 2,534 2,628 2,382 2,283 2,010 1,645

498373 528 589 592 537 698 532 512 504 484 319

777661 860 972 958 904 1,144 1,323 1,243 1,222 1,261 974

860 735 949 1,078 1,182 1,127 1,503 1,712 1,572 1,550 1,665 1,221

1,502 1,246 1,547 1,625 1,842 1,741 2,039 2,289 2,210 2,302 2,459 1,946

415 322 397 476 443 405 496 569 457 546 544 333

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

B2B B2C Energy Financial Services Healthcare IT Materials & Resources

North American M&A activity (#) by sector%

The Middle Market*2019 Trends

Echoing the sametrends seen withrevenue growth, only48% of middle marketcompanies addedworkers during 2019

Growth Rates Recover in the 4th Quarter Employment Rates Recover in the 4th Quarter

*Note: The National Center for the Middle Market (NCMM) defines the “Middle Market” as companies with annual revenues ranging from $10M to $1B.

Revenue Employment

Middle market annualrevenue grew by 7.5%in 2019, with strongperformance in Q4 thatwas 2% higher than Q3driven by strong holiday

season sales, and by businesses in the financial andhealthcare sectors. While lower sales were reported duringmost of 2018 and the first half of 2019, middle marketgrowth continued to outpace the larger market, with theS&P 500 growing at just 4.3% over the same period. A slightmajority of middle market companies (55%) expectedgrowth to continue in 2020 by a rate of around 4.9%, lowerthan the 5.9% expected for same period in 2018.

for an overall growth rate of 5%. Employment rates fellsharply to 4.1% during Q3 but rebounded to 5.4% duringQ4. Nonetheless, hiring rates were below those seen overthe last two years. Based on forecasts from the end of2019, hiring was expected to slow during 2020 with only42% of firms expected to expand their workforce and anoverall growth rate during the year of 3.5%.

2019 Middle Market Review

Source: NCMM 4Q 2019 Middle Market Indicator

31

In 2019, U.S. middle market deal activity reached new highs in both deal amount and value. Private equity groups closed3,577 deals totaling $507.3 billion in value. Middle market dealmakers ignored recession fears, macroeconomic tradetensions, and global uncertainty and continued to complete deals at a record-setting level. Additionally, dealmakers aimed toutilize the low-interest-rate environment, which had been extended by three rate cuts from the Federal Reserve. As definedby PitchBook, “Middle Market” includes U.S. transactions in sizes ranging from $25 million - $1 billion.

The Middle Market (U.S.)2019 Review – Private Equity

Source: PitchBook 2019 Annual US PE Middle Market Report

32

2019 Middle Market Review

$1

66.

4

$7

4.8

$1

91.

7

$2

04.

6

$2

43.

6

$2

33.

9

$3

54.

5

$3

16.

6

$3

12.

3

$3

82.

3

$4

43.

1

$5

07.

3

1,280

713

1,309 1,450

1,8751,601

2,155 2,2162,355

2,564

3,092

3,577427

$0

$150

$300

$450

$600

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Deal Value ($B)

Estimated Deal Value ($B)

Estimated # of Deals Closed

Dea

l Val

ue

($B

)

Dea

l Co

un

t

Middle Market PE Deal Activity by Year

Year

Timing MattersQuarterly EBITDA

As illustrated above, entering the market at the right time can be critical in obtaining maximum valueand achieving a large multiple. Valuations can spike or dip not only in response to the qualities of thetarget business, but also to cyclical factors and other economic, political, and industry factors that affectdemand and ability to achieve desired returns.

Source: PitchBook 3Q 2019 US PE Middle Market Report

6.9x

7.3x

7.1x

7.7x

6.8x

7.3x

7.5x

7.1x

79

52

7366

88

69

5562

6.2x

6.7x

7.2x

7.7x

8.2x

8.7x

1Q 2018 2Q 3Q 4Q 1Q 2019 2Q 3Q 4Q

0

50

100

EV/E

BIT

DA

# o

f D

eals

Quarterly EBITDA MultiplesPrivate Equity Transactions with Enterprise Values $10M-$250M

EV/EBITDA # of Deals Closed

33

2019 Middle Market Review

5.5x 5.9x 5.8x 6.3x 5.9x

6.1x

7.3x

9.0x 8.8x

9.1x 8.8x

9.5x

(1.0x)

1.0x

3.0x

5.0x

7.0x

9.0x

11.0x

2003 - 2014 2015 2016 2017 2018 2019

EBIT

DA

Mu

ltip

le

Year

Enterprise Value/EBITDACompanies with Enterprise Value of $10M to $250M

$10M-$25M $25M - $50M $50M-$100M $100M-$250M

In 2019, companies with $10 million to $25 million total enterprise values had EV/EBITDAmultiples averaging 3.4x lower than that of companies with EV’s of $100 million to $250million. In 2018 and 2019, multiples in each increased slightly; companies with EV’s of $50million to $100 million, however, received reduced multiples from the previous year.

Size MattersLower Middle Market EBITDA Multiples

Source: GF Data® February 2019 M&A Report

Ent. Value:

34

2019 Middle Market Review

Strategic Planning

2020 Presidential Election

35

Source: Middle Market Growth, “How Will the 2020 Elections Impact M&A?”

With the upcoming presidential election in November, there could be significant changes to the M&A landscape if theWhite House flips. Below is an overview of potential changes following a flip in the White House.

• Corporate Tax Rate – The Tax Cuts and Jobs Act of 2017 simplified and lowered corporate income tax brackets froma range of 15%-35% to a flat 21% for all corporations. Under Biden’s proposed plan, corporate income tax ratewould rise to 28%.

• Capital Gains Taxes – There is a proposal on the table to increase the long-terms capital gains tax from 20% to39.6%. To achieve the same net proceeds in this scenario, it would require around a 32% higher sale price.

• Legislative Activity – If the Senate were to flip, legislative activity could pose a direct threat to M&A activity.Lawmakers would be encouraged to pass laws such as the Stop Wall Street Looting Act, which heavily regulatesprivate equity groups and restricts their activity.

• Healthcare – Healthcare will be an important topic as proposals to expand or reduce government involvement orfiscal support will be up for debate. Following a change in the White House, healthcare businesses could facestricter regulations from Democratic proposals, ultimately leading to reduced M&A activity.

Depending on the outcome of the presidential election, closing a deal in 2020 could be advantageous to avoid highertaxes and lower potential valuations, and to prevent increased capital gains taxes from cutting into transaction profits.

M&A Planning Where Are You in the Business Cycle?

Peak

Trough

Recovery

Boom

Recession Expansion

Time to Sell

Is 2020 the time to start a sale process?

Strategic Planning

2020 may still be a great year to sell a business depending on the ultimate impact that COVID-19 hason the broader U.S. economy. Both PEGs and strategic buyers have plenty of cash and easy access toadditional financing, and multiples remain near peak levels for quality companies.

36

ITR is forecasting a downward trend in U.S. Industrial production due to the impact of the shutdowns. The timing ofthe expected 2021 cyclical peak through 2022 cyclical peak is virtually unchanged. Decline in the U.S. NondefenseCapital Goods New Orders (excluding aircraft) 12MMT through May was not as severe as predicted. However,analysis of leading indicator movements suggests that raising expectations would be premature, as many downsiderisks remain. U.S. wholesale trade of both durable and nondurable goods are in Phase D (recession), and both willlikely finish 2020 around 9% below 2019 spending. The Trends 10 (graph above) summary provides a dynamic look atthe economy. Each major segment of the economy is shown in terms of where it is in the business cycle. The graphalso provides a view of the economy that is like a train, with sectors in the front facing peaks or valleys first whilesectors in the back have more time to react to what is coming.

Industry GrowthWhere is My Industry in the Cycle?

Strategic Planning

Source: ITR Insider 3-Year U.S. Outlook Report (July 2020)

37

ConclusionsM&A Outlook for 2020

While 2020 started off strong, the impact of COVID-19 on deal activity and the health of the economy during theremainder of the year is uncertain at this point. Upcoming November elections only exacerbate the level of marketuncertainty. Deal activity was slow during the first half of 2020 as market participants evaluated the virus’s impact.Both strategic and private equity buyers have record levels of cash on hand and are still hungry for growth, so dealactivity is expected to strengthen in the second half as people continue to adjust to this new normal.

M&A Market Outlook: Positive/Uncertain

• Private equity had a record year in 2019 and was able to handle the negative effects of the pandemic. PEGs willlook to put record stockpiles of dry powder to work and are willing to pay up for companies that had positiveCOVID impacts. Add-on acquisitions proved highly successful overall and will continue to be a central strategy.

• Financing initially tightened due to elevated risk stemming from COVID-19 but is slowly returning to normal levels.

• Change in deal structure will become more common in the form of earnout mechanisms. Earnouts will helpbridge the valuation gap between buyers and sellers during and post-pandemic.

• Global uncertainty due to COVID-19 will likely slow market activity. Many global sectors have been impacted bycostly supply chain disruptions and reduced consumer demand.

• Corporate carveouts are growing in popularity as conglomerates seek to rid themselves of divisions that havebecome less relevant to their core business.

• Baby boomers (70% of them) are expected to exit their businesses in the next decade. This will lead to 12 millionprivately held companies being available for sale, spurring M&A activity significantly.

• The upcoming presidential election will add even more uncertainty to the M&A market, as there could besignificant changes to the tax code.

Themes

Conclusions

38

*Note: Information in this report may not be published or used in any form without written permission from Bravaldo Capital Advisors or the original data provider.

Phone: 404-857-2221 ▪ Email: [email protected]

2839 Paces Ferry Rd SE, Suite 450, Atlanta, GA 30339

www.BravaldoCapitalAdvisors.com

Contact Us