27

Managed Account Solutions SM : Benefit from a personalized investment plan to help you reach your financial goals <Insert Firm Logo Here>

| Date post: | 27-Dec-2015 |

| Category: |

Documents |

| Upload: | gwenda-bishop |

| View: | 217 times |

| Download: | 0 times |

Managed Account SolutionsSM:

Benefit from a personalized investment plan to help you reach your financial goals

<Insert Firm Logo Here>

22

1

2

3

Agenda

Managed Account Basics

Key Managed Account Solutions Potential Benefits

Is Managed Account Solutions Right for You?

33

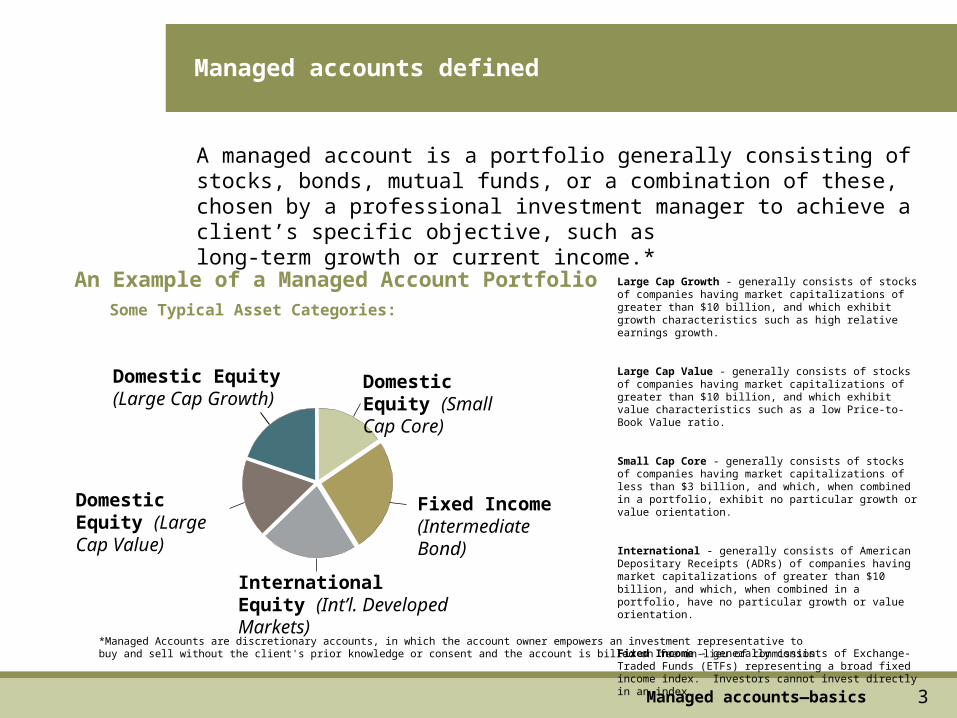

Managed accounts defined

A managed account is a portfolio generally consisting of stocks, bonds, mutual funds, or a combination of these, chosen by a professional investment manager to achieve a client’s specific objective, such as long-term growth or current income.*

International Equity (Int’l. Developed Markets)

Domestic Equity (Small Cap Core)

Fixed Income (Intermediate Bond)

Domestic Equity (Large Cap Value)

Domestic Equity (Large Cap Growth)

An Example of a Managed Account PortfolioSome Typical Asset Categories:

Large Cap Growth - generally consists of stocks of companies having market capitalizations of greater than $10 billion, and which exhibit growth characteristics such as high relative earnings growth.

Large Cap Value - generally consists of stocks of companies having market capitalizations of greater than $10 billion, and which exhibit value characteristics such as a low Price-to-Book Value ratio.

Small Cap Core - generally consists of stocks of companies having market capitalizations of less than $3 billion, and which, when combined in a portfolio, exhibit no particular growth or value orientation.

International - generally consists of American Depositary Receipts (ADRs) of companies having market capitalizations of greater than $10 billion, and which, when combined in a portfolio, have no particular growth or value orientation.

Fixed Income - generally consists of Exchange-Traded Funds (ETFs) representing a broad fixed income index. Investors cannot invest directly in an index.

Managed accounts—basics

*Managed Accounts are discretionary accounts, in which the account owner empowers an investment representative to buy and sell without the client's prior knowledge or consent and the account is billed on fee in-lieu of commission.

44

Managed accounts are like mutual funds in that….

They are managed by professional investment managers who monitor the portfolio to stay on top of new opportunities.

Each has a clearly defined objective.

Each is compared against a benchmark (or index) which will identify the progress being made towards your investment goals.

Managed accounts—basics

55

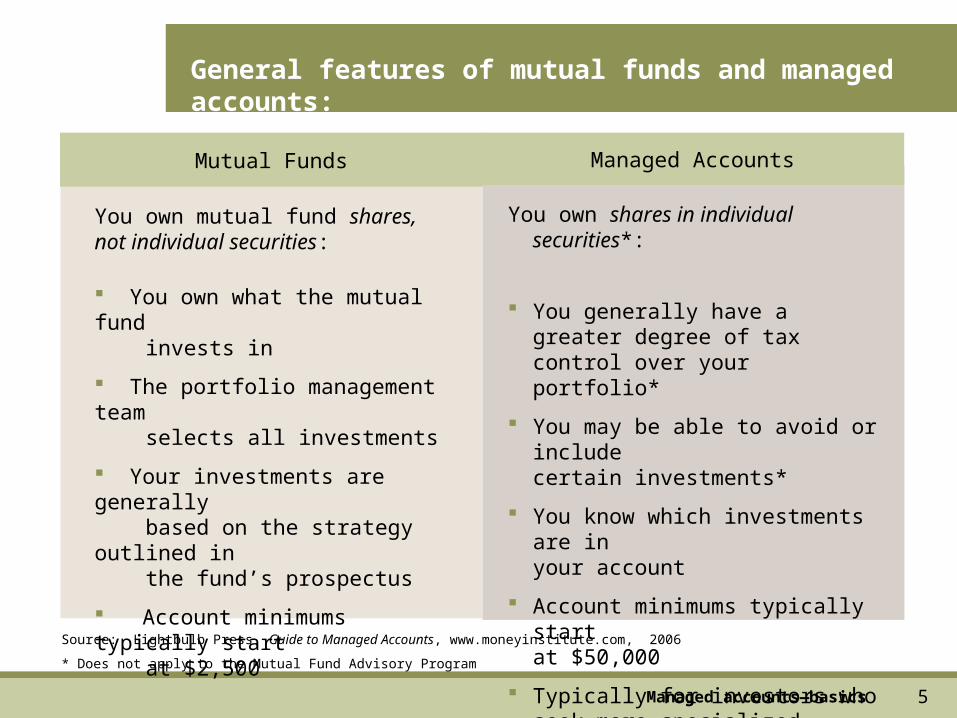

General features of mutual funds and managed accounts:

Source: Lightbulb Press, Guide to Managed Accounts, www.moneyinstitute.com, 2006

* Does not apply to the Mutual Fund Advisory Program

Mutual Funds Managed Accounts

You own mutual fund shares, not individual securities:

You own what the mutual fund invests in

The portfolio management team selects all investments

Your investments are generally based on the strategy outlined in the fund’s prospectus

Account minimums typically start at $2,500

You own shares in individual securities*:

You generally have a greater degree of tax control over your portfolio*

You may be able to avoid or include certain investments*

You know which investments are in your account

Account minimums typically start at $50,000

Typically for investors who seek more specialized portfolios and investment advice

Managed accounts—basics

66

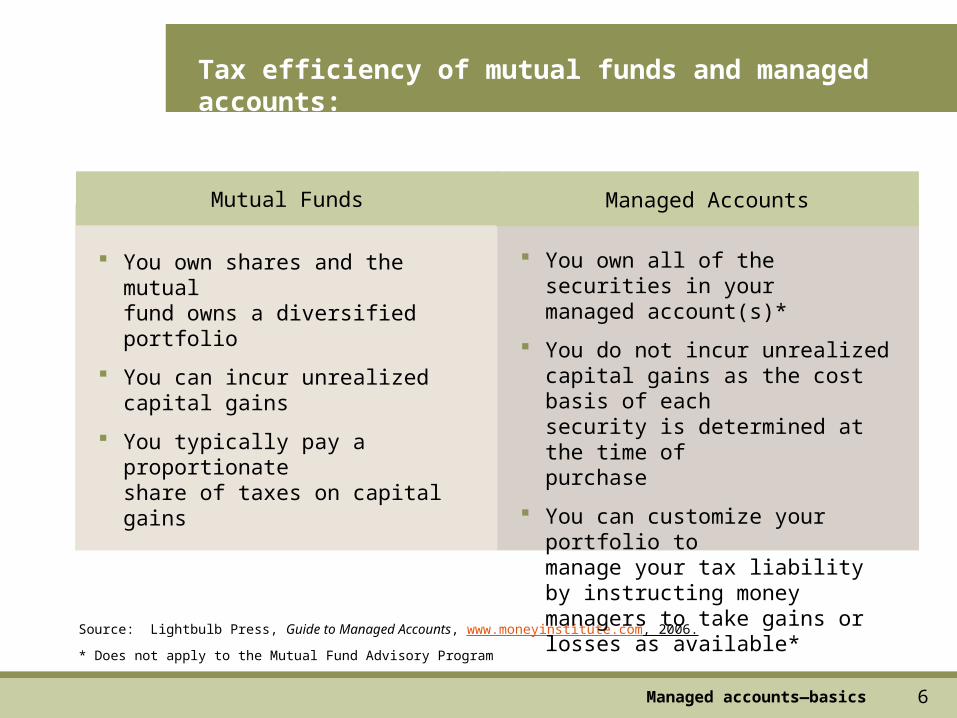

Tax efficiency of mutual funds and managed accounts:

Source: Lightbulb Press, Guide to Managed Accounts, www.moneyinstitute.com, 2006.

* Does not apply to the Mutual Fund Advisory Program

Mutual Funds Managed Accounts

You own shares and the mutual fund owns a diversified portfolio

You can incur unrealized capital gains

You typically pay a proportionate share of taxes on capital gains

You own all of the securities in your managed account(s)*

You do not incur unrealized capital gains as the cost basis of each security is determined at the time of purchase

You can customize your portfolio to manage your tax liability by instructing money managers to take gains or losses as available*

Managed accounts—basics

77

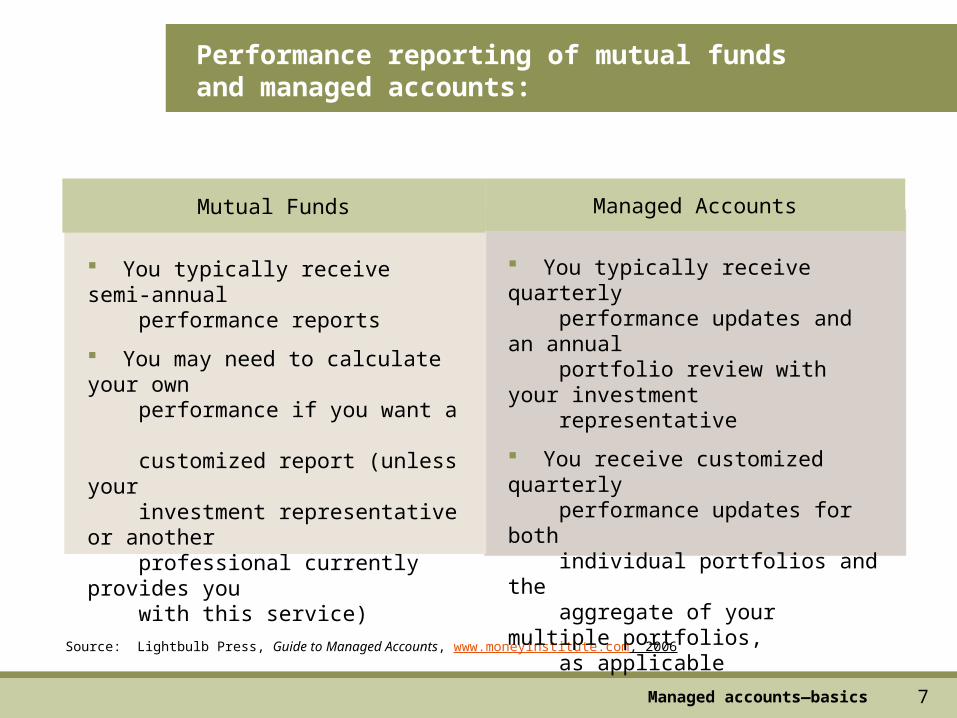

Performance reporting of mutual fundsand managed accounts:

Source: Lightbulb Press, Guide to Managed Accounts, www.moneyinstitute.com, 2006

Mutual Funds Managed Accounts

You typically receive semi-annual performance reports

You may need to calculate your own performance if you want a customized report (unless your investment representative or another

professional currently provides you with this service)

You typically receive quarterly performance updates and an annual portfolio review with your investment representative

You receive customized quarterly performance updates for both individual portfolios and the aggregate of your multiple portfolios, as applicable

Managed accounts—basics

88

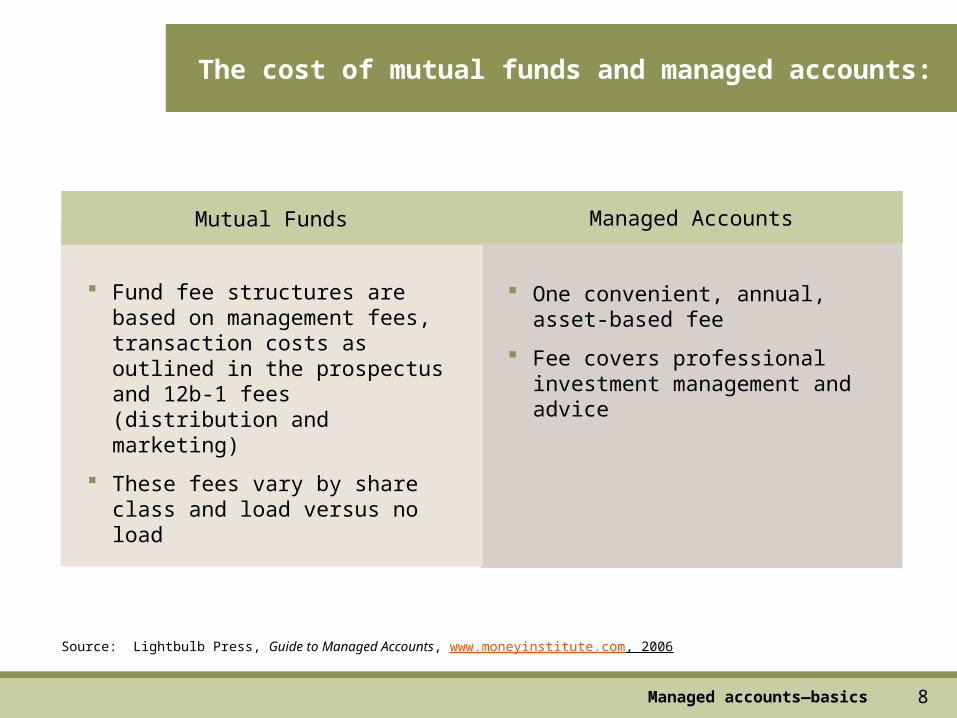

The cost of mutual funds and managed accounts:

Source: Lightbulb Press, Guide to Managed Accounts, www.moneyinstitute.com, 2006

Mutual Funds Managed Accounts

Fund fee structures are based on management fees, transaction costs as outlined in the prospectus and 12b-1 fees (distribution and marketing)

These fees vary by share class and load versus no load

One convenient, annual, asset-based fee

Fee covers professional investment management and advice

Managed accounts—basics

99

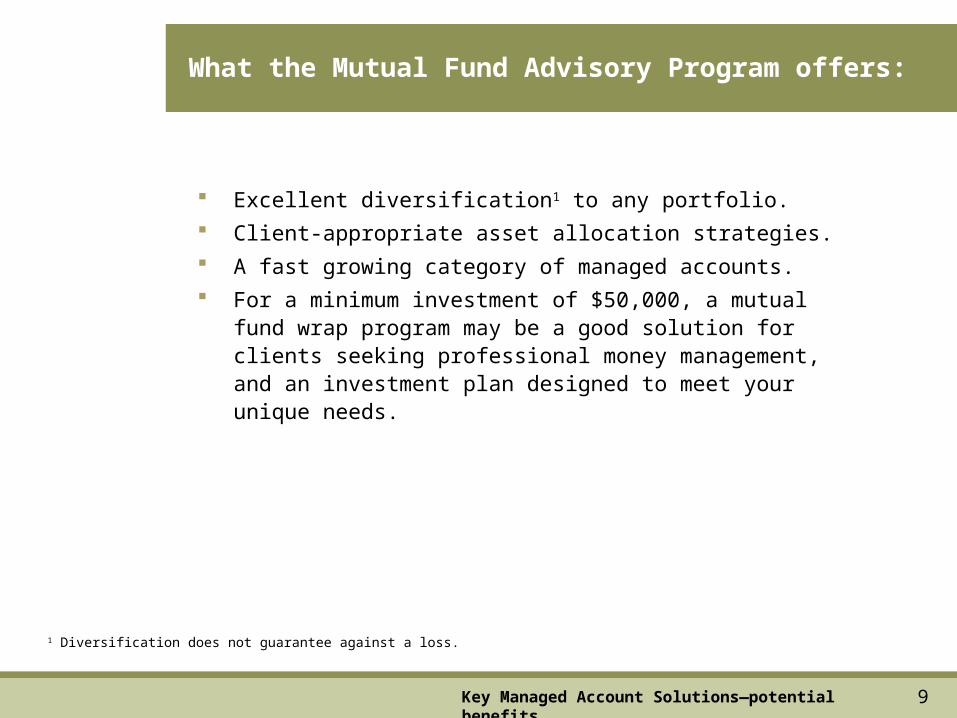

Excellent diversification1 to any portfolio.

Client-appropriate asset allocation strategies.

A fast growing category of managed accounts.

For a minimum investment of $50,000, a mutual fund wrap program may be a good solution for clients seeking professional money management, and an investment plan designed to meet your unique needs.

1 Diversification does not guarantee against a loss.

What the Mutual Fund Advisory Program offers:

Key Managed Account Solutions—potential benefits

1010

How can managed accounts benefit you?

Managed Account Solutions offers you:

An Individual Investment Plan

Access to professional money managers

A greater degree of tax control over your portfolio

Ongoing portfolio monitoring and rebalancing

A convenient, asset-based, annual fee

Key Managed Account Solutions—potential benefits

1111

Using managed accounts is like playing on a team

You = Team Owner

Investment Rep =Coach

Investment Manager =Players(s)

Accumulate wealth to achieve financial goals

Articulate your goals

Don’t have time or expertise to be the “coach”

Hired to help “owner” identify goals

Selects the right “players” (asset allocation & manager selection)

Ensures that “players” adhere to their positions

Provides feedback on how “players” are doing

Excel at respective positions

Contributes to a particular position (specific style with no style drift)

Key Managed Account Solutions—potential benefits

1212

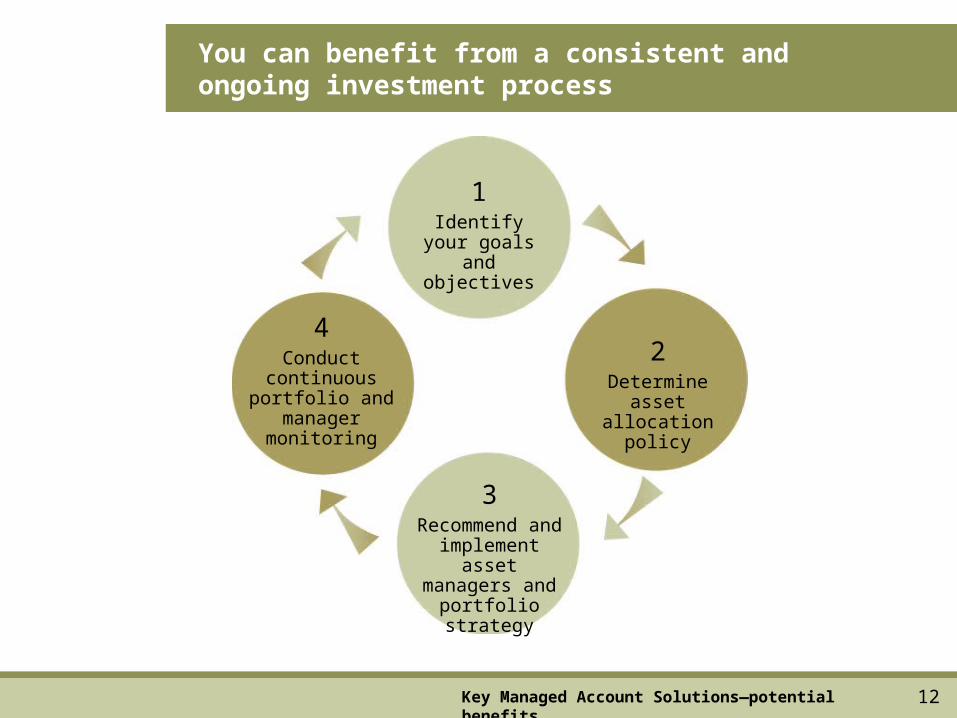

1Identify your

goals and objectives

3Recommend and implement asset managers and

portfolio strategy

2Determine asset allocation policy

4Conduct

continuous portfolio and

manager monitoring

You can benefit from a consistent and ongoing investment process

Key Managed Account Solutions—potential benefits

1313

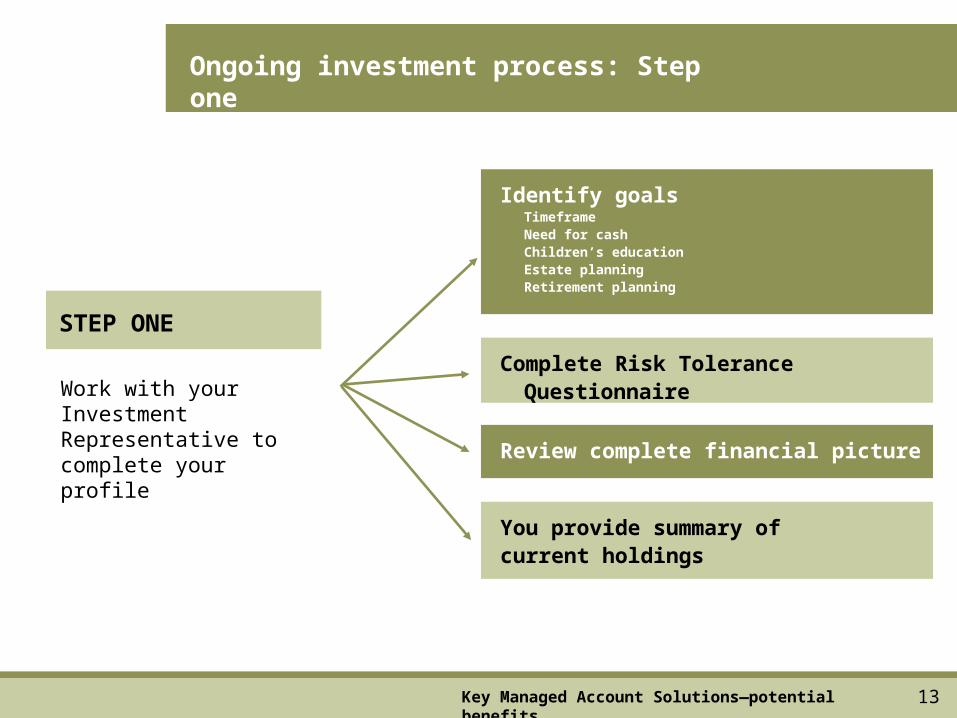

Ongoing investment process: Step one

Identify goalsTimeframeNeed for cashChildren’s educationEstate planningRetirement planning

Complete Risk Tolerance Questionnaire

Review complete financial picture

You provide summary of current holdings

Work with your Investment Representative to complete your profile

STEP ONE

Key Managed Account Solutions—potential benefits

1414

Identify and review gaps and style drift to:

Ongoing investment process: Step two

Current holdings assessmentand

risk tolerance review

Determine asset allocation policy

Select managers

Your Investment Representative determines your asset allocation policy

STEP TWO

Key Managed Account Solutions—potential benefits

1515

Follow a specific style

Monitor, evaluate, and sell investments

Analyze portfolioholdings and keep your investments on track

Ongoing investment process: Step three

Review and implement your plan

Review personalized strategy designed to help meet your unique needs

Agree upon plan

Implement your plan

Managers are selected and your investment plan is implementedManagers selected to:

STEP THREE

Key Managed Account Solutions—potential benefits

1616

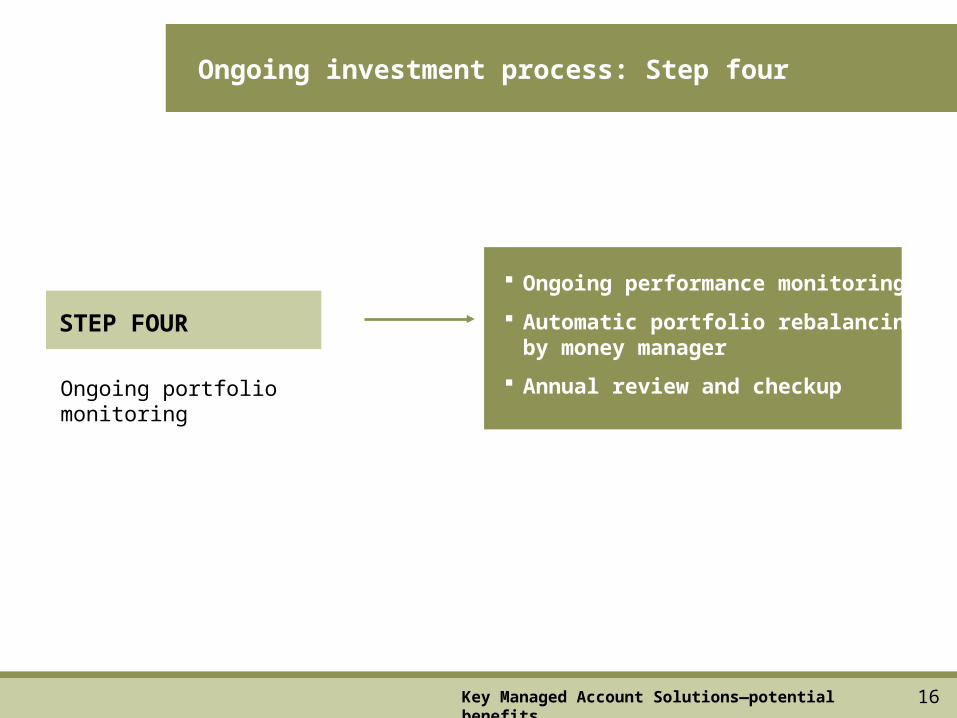

Ongoing investment process: Step four

Ongoing portfolio monitoring

STEP FOUR

Ongoing performance monitoring

Automatic portfolio rebalancing by money manager

Annual review and checkup

Key Managed Account Solutions—potential benefits

1717

Source: Ibbotson Associates: This image illustrates the effect of different growth rates on a static (unbalanced) portfolio over a 20-year period. In 1984, the target asset mix began with a 50% allocation to stocks and a 50% allocation to bonds. Past performance does not guarantee future results.

Stock allocation

Bond allocation

Po

rtfo

lio

we

igh

tin

gs

Target asset mix: 50% stocks/50% bonds

1984–2004

Why rebalancing matters

50%

72%

28%

75%

25%

58%

42%

55%

45%50%

0%

20%

40%

60%

80%

100%

1984 1989 1994 1999 2004

Because asset classes grow at different rates of return, it is necessary to periodically rebalance a portfolio to maintain a target asset mix.

Key Managed Account Solutions—potential benefits

1818

Importance of rebalancing 1984–2004

Because asset classes produce different rates of return, it is necessary to periodically rebalance your portfolio to maintain your target asset mix.

This chart illustrates the effect of different growth rates on a static (unbalanced) portfolio over a 20-year period. In 1984, the target asset mix began with a 50% allocation to stocks and a 50% allocation to bonds.

The proportion of stocks in the portfolio grew modestly through 1994 when it accounted for 58% of the portfolio. The bull market of the late 1990s helped propel the value of stocks, causing the portfolio to be over-weighted. By 2004 stocks accounted for 72% of the portfolio.

Asset classes associated with higher degrees of risk tend to have higher rates of return than less volatile asset classes. For this reason, a portfolio that is not rebalanced periodically may become more volatile (riskier) over time.

Government bonds are guaranteed by the full faith and credit of the United States government as to the timely payment of principal and interest, while stocks are not guaranteed and have been more volatile than bonds. This data assumes reinvestment of income and does not account for taxes or transaction costs.

Source: Small Company Stocks—Dimensional Fund Advisors, Inc. (DFA) U.S. Micro Cap Portfolio; Large Company Stocks—Standard & Poor’s 500® Index, which is an unmanaged group of securities and considered to be representative of the stock market in general; Intermediate-Term Government Bonds—5-year U.S. Government Bond.

Why rebalancing matters

Key Managed Account Solutions—potential benefits

1919

Non-rebalanced portfolio

Rebalanced portfolio

Jan. 1970 –Dec. 2004

Jan. 1980 –Dec. 2004

Jan. 1990 –Dec. 2004

How rebalancing can benefit you

Risk Return

Jan. 1970 –Dec. 2004

Jan. 1980 –Dec. 2004

Jan. 1990 –Dec. 2004

Source: Ibbotson Associates. Risk is measured by annualized standard deviation. Return is measured by compound annual return. The image compares the risk and return of portfolios that are rebalanced to those that are not rebalanced beginning at three different time periods. Risk and return are measured by annualized standard deviation and compound annual return respectively. Standard deviation measures the fluctuation of returns around the arithmetic average return of the investment. The higher the standard deviation, the greater the variability (and thus risk) of the investment returns. Past Performance does not guarantee future results.

11.3%12.1%

9.4%11.0%11.7%

8.8%

0%

2%

4%

6%

8%

10%

12%

14%12.8% 12.7%

11.1%

9.4%10.4% 10.1%

0%

2%

4%

6%

8%

10%

12%

14%

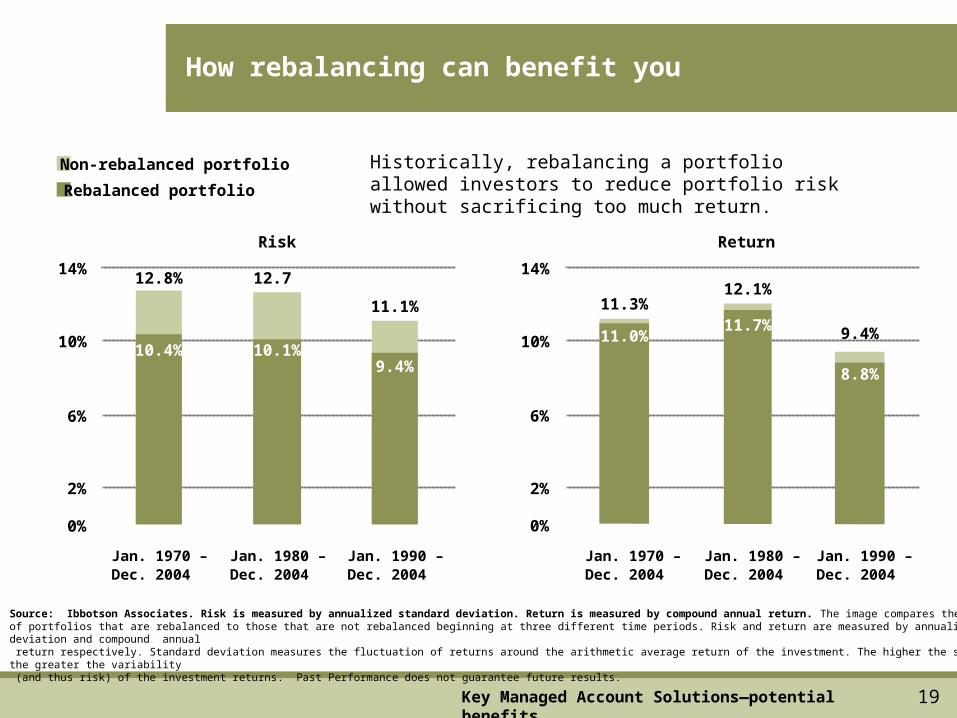

Historically, rebalancing a portfolio allowed investors to reduce portfolio risk without sacrificing too much return.

Key Managed Account Solutions—potential benefits

2020

Rebalancing versus not rebalancing

Historically, rebalancing a portfolio has allowed investors to reduce portfolio risk without sacrificing too much return.

Over time, your portfolio asset allocation policy can get disturbed by market ups and downs. For example, stocks tend to outperform bonds in the long run. Since stocks are riskier than bonds, a greater allocation to stocks can also increase the portfolio risk. Rebalancing is an essential account management tool that helps to keep the portfolio within the risk tolerance level that is comfortable for your asset allocation strategy.

This chart compares the risk and return of portfolios that are rebalanced to those that are not rebalanced beginning at three different time periods. Risk and return are measured by annualized standard deviation and compound annual return, respectively. Standard deviation measures the fluctuation of returns around the arithmetic average return of the investment. The higher the standard deviation, the greater the variability (and thus risk) of the investment returns.

The first set of portfolios begins in January 1970 and ends in December 2004, followed by the second set that begins in January 1980 and ends in December 2004, and finally the third set that begins in January 1990 and ends in December 2004. Each portfolio consisted of 60% stocks, 20% bonds, and 20% cash at the portfolio’s beginning date. Stocks consist of 33.3% large-cap, 33.3% small-cap, and 33.3% international stocks at each portfolio’s beginning date. The bond allocation consists entirely of 5-year U.S. government bonds, while the cash allocation consists of 30-day U.S. Treasury bills. The portfolios have been rebalanced semi-annually.

In all three portfolios, the rebalanced portfolio had a lower risk than the non-rebalanced portfolio. For instance, the rebalanced portfolio beginning January 1980 had a risk of 10.1%, which is only 79.5% of the 12.7% risk of the non-rebalanced portfolio. Although rebalancing was able to reduce the portfolio risk, the tradeoff was a slight reduction in returns. For example, the rebalanced portfolio beginning January 1980 had a return of 11.7%, which is 96.7% of the 12.1% return of the non-rebalanced portfolio.

Government bonds and Treasury bills are guaranteed by the full faith and credit of the United States government as to the timely payment of principal and interest, while stocks are not guaranteed and have been more volatile than bonds. International investments involve special risks such as fluctuations in currency, foreign taxation, economic and political risks, and differences in accounting and financial standards. This data assumes reinvestment of income and does not account for taxes or transaction costs.

How rebalancing can benefit you

Key Managed Account Solutions—potential benefits

Source: Large Company Stocks—Standard & Poor’s 500® Index, which is an unmanaged group of securities and considered to be representative of the stock market in general; Small Company Stocks—represented by the fifth capitalization quintile of stocks on the NYSE for 1926–1981 and the performance of the Dimensional Fund Advisors, Inc. (DFA) U.S. Micro Cap Portfolio thereafter; International Stocks—Morgan Stanley Capital International Europe, Australasia, and Far East (EAFE®) Index; Government Bonds—5-year U.S. Government Bonds; Cash—30-day U.S. Treasury Bill.

2121

Managed Account Solutions may be the solution to help you reach your goals

Do you have one or more of these attributes?

You have $50,000 or more to invest and or/retirement assets ready to roll-over

ASSETS

You are looking for a professional investment manager to help you reach your financial goals

EXPERIENCE

You are seeking a greater degree of tax control

TAX-EFFICIENCY

You recently inherited money, sold business, etc.

FINANCIAL EVENTS

Is Managed Account Solutions — right for you?

2222

The annual fee and what it covers

The convenient, annual fee covers:

Consultations with your investment representative

Development of your individual investment plan

Ongoing portfolio monitoring

Custody services

Commission-free transactions (thru investment managers)

Is Managed Account Solutions — right for you?

2323

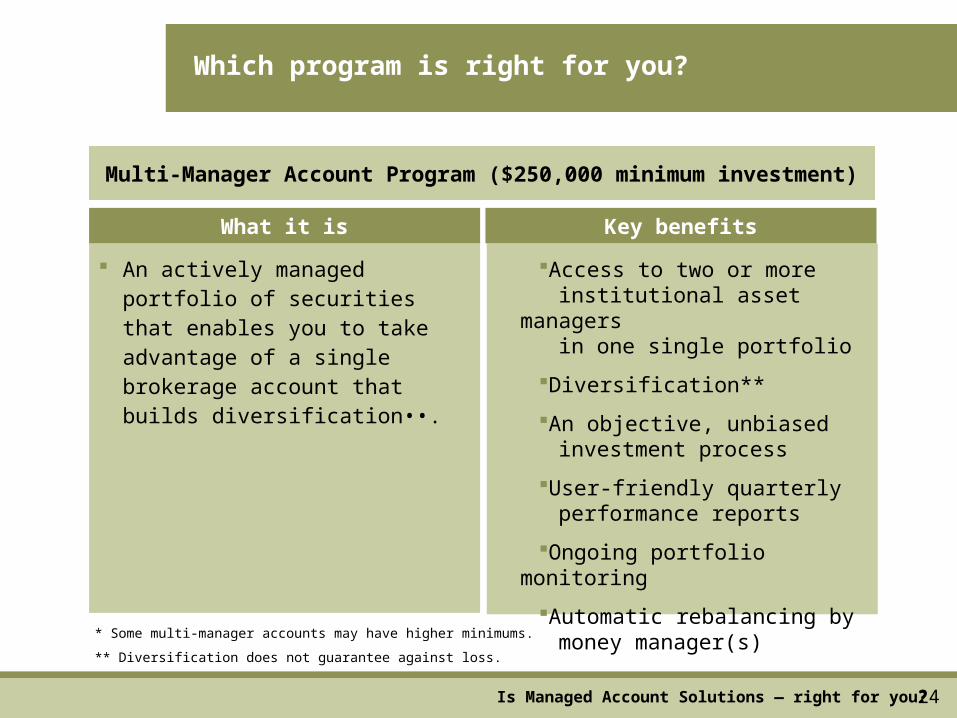

Which program is right for you?

Mutual Fund Advisory Program ($50,000 minimum investment)

A comprehensive program that gives you access to a wide range of carefully selected mutual funds

Access to actively managed investment solutions for a low minimum ($50,000)

An objective, unbiased investment process

User-friendly quarterly performance reports

Ongoing portfolio monitoring

Automatic rebalancing by money manager(s)

What it is Key benefits

Is Managed Account Solutions — right for you?

2424

* Some multi-manager accounts may have higher minimums.

** Diversification does not guarantee against loss.

Multi-Manager Account Program ($250,000 minimum investment)

An actively managed portfolio of securities that enables you to take advantage of a single brokerage account that builds diversification••.

Access to two or more institutional asset managers in one single portfolio

Diversification**

An objective, unbiased investment process

User-friendly quarterly performance reports

Ongoing portfolio monitoring

Automatic rebalancing by money manager(s)

What it is Key benefits

Is Managed Account Solutions — right for you?

Which program is right for you?

2525

Separate Account Program (typically investors with $500,000 or more)

A program that gives you the ability to place your assets in discretionary separate accounts managed by professional money managers and enables you to take advantage of a customized approach to investment planning

Access to professional asset management

An objective, unbiased investment process

Customization

Tax efficiency

User-friendly quarterly performance reports

Ongoing portfolio monitoring

Automatic rebalancing by money manager(s)

What it is Key benefits

Is Managed Account Solutions — right for you?

Which program is right for you?

2626

How to put Managed Account Solutions work for you

Schedule a meeting with your investment representative so he/she can help you create an individual investment plan.

Take advantage of an investment plan designed to help you reach your unique investment goals

Is Managed Account Solutions — right for you?

2727

Thank You!

<Investment Representative Name>

<Firm Name>

<Phone>

<Email Address>

National Financial’s Managed Account Solutions service is provided by Envestnet Asset Management, Inc. (“Envestnet”), a third-party provider of investment management services. National Financial does not provide investment advisory services in conjunction with the Managed Account Solutions service. Envestnet is not a corporate affiliate of National Financial.

425725.3 National Financial Services LLC, Member, NYSE, SIPC