P. K. SIKDAR'SADVANCE LEARNING 23C, EKDALIA PLACE I(OLKATA - 700019 M • 9830165501 Web: www.pks.l.com Management Accounting Decision Making! Enterprice Perio1'1IUince Management Question I. What ill 1m What are the steps involved in Jm Answer Operation of JIT Oust -in-time) concept: A JIT approach is a collection of ideas and philosophy that streamline a company's production process activities to such an extent that waste of an kinds viz. :material and labour is systematically driven out of the process. Just in Time Technique enables a company to ensure that it receives products I spare partsl materials from its suppliers on the exact date and at the exact time when they are nI!-'<ied. lIT refers to a system in which materlals arrive exactly as they needed. With a JIT system a company must eNure it receives materials from its suppller on the exact date and at the exact time when they are ,needed., Por thiJ reason 1tJe purchasing staff must investigate and evaluate every supplier, eliminate those, that could notJi;eep up with the The stept! involved arc' , , Suppliet' The Purchasing Depanment must eva.lWlte and investigate every supplier and eliminate tilose who could not keep up with tile delivery dates.' lingineeringlltaff mU$t visit suppller sites and examine their processes, not only to see if they can reliably :/lhip high-qwdity parts but also to provide them with engineering IIIlsiItmce to bring them up to a higher standard ol proc.tuct. Supplier JnfOl'll'llltlonSyalem: The firm must install a system. which is lUI simple lUI a lax :machine or lUI advanced as anelectroruc data interchange system or linked computer systems, that communicates with suppliers Ill! to exactly how much of spedfied parts are to be sent to the company. Direct Delivery: Deliverles should be sent straight to ,the production floor for immediate use in manufactured products, so that no time spent in inspecting the parts for defects. Drivers, who bring supplies of materials, drop them off at the specific :machines that will use the materials first. This can be illulltrated with the example of three Parts are first processed by machine, A which fe;c!d to :machine B. Then B processes these parts and then C Kanbans are located between the machines. As long as Kanban containers are not full the workers Ilt machine A continues to produce parIS placing them in Kanban contldner. When the Kanban container is full, the worker stope producing and recommences when a part has been removed. A sinUlar process Applies between the operation of mad'dNl B II.'Id C ThIs process can result in idle time to a certain extent within the ceIL but the }IT philosophy is hued on the thinIdDc that it is m.ore beneficial to absorb IIIhort run idle time than adding inventory during these periods. During idle time workers perform preventive maintenance on their machine. Question.2! How doe. JlT belp in Ihadening Nt-liP and operation times? Answet' Outline the JIT approach lor shortening IIeklp and operation time<>. ' Long set-ups and operation time involve indirect costs like product obBolesa::ru."e, inventory carrying costs, and many defective products (becaU8e problems DIlly not be dls4.'Ovenld until a laJ'ge number of items have already been completed). This problem will be resolved under )IT 'by adopting the following llteptl. Test data: A videotape of a typical Nt " prepared for analyBis purposes. EvaluatiOl1l A team of indUlltrlaJ enatneen and !IIIICbine, WJers exIIll\ine this tape, spotl:ing II.'Id gradually elbninating steps that contribute to a langthy __up. Motion IIJ1d time Study; By eIhniJ1.aUna production slept! and improving others after A nwnber of iterations, it is possible to achieve substantially lower __up titileI'than before. Effects: Reduction in seklp time hu the fo1Iawingeffects: Reduction in the amount of work-in-proa!I8, Reduction in the;number of products that can be produced before, defects are identified II.'Id &ed, thereby reducing scrap costs. Quetti0n3 Explain in brief the JlT appmach for teducins WIP inverdory. Answer JIT approach for reducing WlP inventory: At times, there may be huge differer1ces between the operating speeds of different machines.l1tis affects cost in following manner: Work-in-process inverdory builds up in front of tpe • Defective produced by an upt!tream machine may not be discovered until, the next downstream operator finds them later. By that time, the upstream machine D'lay .have created more detective ,Parts, all of which must now be destroyed or reworlced.. In JIT philoIIophy, there are two wayt to resolve the above, problems. 1. Kanban Card: It III a card that a dDwn stream machine saruIa to, each upstream machine that feedt it with parts. authoril,iDg, the production of just enough components to fulfill the prodI;action re.quin:meI:dI. This 1II.aJso Ialfi't, as "pull- these carda lIIe initiated at the end of the production process pul1ing work authorizatiOns through the produCtlmx syslSL WlP cannot pile up since it can he only with kanban allthorb:.ation. 2. Worldng Cella: A WOrkItIa cell is • small cluster of macbines, can be run by a single machine operator. The establllllunent of worlcing celli huthe following advantages: • The individual mad'dNl opetator takes each output part from ::nachine to :machine within the cell and thus there is no way for WlP to build up between machines. . • The operator can immediately identify defective output which otherwise is difficult for each machine of the cell The smaller machines WJed in II machine cell' are generally mul:" sUr,,?Jer than th£o large autotnated machinery they replace. Hence maintenance C\ilIIbI are reduced. ••• It is much easier to reconfigure,the production facility when it is necessa.iy to produce different products, avoiding the large expense of careful1y repositiQning and a:JigtVng equipmetlt Question 4: Wb,It Is Bade Plum, Ac:counting? CtwacteristiCl ,. Crilkillm of Back flush Costing. What an! DIfficulties of BKk flush eo.ting? Answer ' Companies may have inventory despite using Jli.U-bHime om production meIhod. Companies that record costs directly in cost' of goods sold can U8e a method called back costing to transfer any costs back to the 1

Transcript

P K SIKDARSADVANCE LEARNING 23C EKDALIA PLACE

I(OLKATA - 700019 M bull 9830165501

Web wwwpkslcom Management Accounting Decision Making Enterprice Perio11IUince Management

Question I What ill1m What are the steps involved in Jm Answer Operation of JIT Oust -in-time) concept A JIT approach is a collection of ideas and philosophy that streamline a companys production process activities to such an extent that waste of an kinds viz material and labour is systematically driven out of the process Just in Time Technique enables a company to ensure that it receives products I spare partslmaterials from its suppliers on the exact date and at the exact time when they are nI-ltied lIT refers to a system in which materlals arrive exactly as they needed With a JIT system a company must eNure ~t it receives materials from its suppller on the exact date and at the exact time when they are needed Por thiJ reason 1tJe purchasing staff must investigate and evaluate every supplier eliminate those that could notJieep up with the deliverY~tes-The stept involved arc Suppliet Bv~ The Purchasing Depanment must evalWlte and investigate every supplier and eliminate tilose who could not keep up with tile delivery dates Suppliet~eThe lingineeringlltaff mU$t visit suppller sites and examine their processes not only to see if they can reliably lhip high-qwdity parts but also to provide them with engineering IIIlsiItmce to bring them up to a higher standard ol proctuct Supplier JnfOlllllltlonSyalem The firm must install a system which is lUI simple lUI a lax machine or lUI advanced as anelectroruc data interchange system or linked computer systems that communicates with suppliers Ill to exactly how much of spedfied parts are to be sent to the company Direct Delivery Deliverles should be sent straight to the production floor for immediate use in manufactured products so that no time spent in inspecting the parts for defects Drivers who bring supplies of materials drop them off at the specific machines that will use the materials first This can be illulltrated with the example of three ~ Parts are first processed by machine A which fecd to machine B Then B processes these parts and then C Kanbans are located between the machines As long as Kanban containers are not full the workers Ilt machine A continues to produce parIS placing them in Kanban contldner When the Kanban container is full the worker stope producing and recommences when a part has been removed A sinUlar process Applies between the operation of maddNl B IIId C ThIs process can result in idle time to a certain extent within the ceIL but the IT philosophy is hued on the thinIdDc that it is more beneficial to absorb IIIhort run idle time than adding inventory during these periods During idle time workers perform preventive maintenance on their machine

Question2 How doe JlT belp in Ihadening Nt-liP and operation times Answet Outline the JIT approach lor shortening IIeklp and operation timeltgt Long set-ups and operation time involve indirect costs like product obBolesarue inventory carrying costs and many defective products (becaU8e problems DIlly not be dls4Ovenld until a laJge number of items have already been completed) This problem will be resolved under )IT by adopting the following llteptl

Test data A videotape of a typical Nt prepared for analyBis purposes EvaluatiOl1l A team of indUlltrlaJ enatneen and IIIICbine WJers exIIlline this tape spotling IIId gradually elbninating steps that contribute to a langthy __up Motion IIJ1d time Study By eIhniJ1aUna ~ production slept and improving others after A nwnber of iterations it is possible to achieve substantially lower __up titileIthan before Effects Reduction in seklp time hu the fo1Iawingeffects Reduction in the amount of work-in-proaI8 Reduction in thenumber of products that can be produced before defects are identified IIId amped thereby reducing scrap costs

Quetti0n3 Explain in brief the JlT appmach for teducinsWIP inverdory Answer JIT approach for reducing WlP inventory At times there may be huge differer1ces between the operating speeds of different machinesl1tis affects cost in following manner

Work-in-process inverdory builds up in front of tpe slowest~ bull Defective ~ produced by an upttream machine may not be discovered until the next downstream macbin~

operator finds them later By that time the upstream machine Dlay have created more detective Parts all of which must now be destroyed or reworlced In JIT philoIIophy there are two wayt to resolve the above problems

1 Kanban Card It III a ~ card that a dDwn stream machine saruIa to each upstream machine that feedt it with parts authoriliDg the production of just enough components to fulfill the prodIaction requinmeIdI This 1IIaJso Ialfit as pull- ~IIiince these carda lIIe initiated at the end of the production process pul1ing work authorizatiOns through the produCtlmx syslSL WlP cannot pile up since itcanhe ~ted only with kanban allthorbation

2 Worldng Cella A WOrkItIa cell is bull small cluster of macbines w~ can be run by a single machine operator The establllllunent of worlcingcelli huthe following advantages

bull The individual maddNl opetator takes each output part from nachine to machine within the cell and thus there is no way for WlP to build up between machines

bull The operator can immediately identify defective output which otherwise is difficult for each machine of the cell The smaller machines WJed in II machine cellare generally mul sUrJer than thpoundo large autotnated machinery they replace Hence maintenance CilIIbI are reduced bullbullbull It is much easier to reconfigurethe production facility when it is necessaiy to produce different products avoiding the large expense of careful1y repositiQning and aJigtVng equipmetlt

Question 4 WbIt Is Bade Plum Accounting CtwacteristiCl Crilkillm of Back flush Costing What an DIfficulties of BKk flush eotingAnswer

Companies may have so~ inventory despite using JliU-bHime om production meIhod Companies that record costs directly in cost of goods sold can U8e a method called back flu~h costing to transfer any costs back to the

1

P K SIKDARS ADVANCE LEARNING 23C EKDAUA PLACE

KOLKATAmiddot 700019 M - 9830165501 -2shy

Web wwwpksalcom inventory accounts if necessary

2 Back flush costing is a method that works backward from the output to assign manufacturing costs to work-inshyprogress inventories

3 The term backflUllh is used because costs are flushed back through the production process to the points at which inventories remain

4 Backflush costing avoids detailed accounting transaction 5 In convention product costing system costs are assigned with the movement of the products from direct materials to

work- in -progress to finished goods H_ever in backflUllh costing we fOCUll first on the output of the organisation and work backwards to allocate costs between costs of goods sold and inventories No separate accounts are maintained for work-in-progress in backflush accounting

6 CIMA defines it WI Cost Accounting sytjem Which focuses on the output of an organisation and then works back to attribute costs to stock and cost of sales

7 Traditional CWiting systems use sequential tracking ie costtng methods are synchronilled with physical sequences of purchases and production Backpush costing which is also referred to as delayed costing or post deduct costing focuses on output and then works back to apply manufacturing costs to units sold and to inventories

There are tWo basic Justifications for the system (1) To remove the incentive for managers to produce for inventory In conventlonaisystem managers try to add to operating income by producing units not sold In absorption costing fixed overhead ~ which would otherwise be expenses for the period get inventorised (if) To increase the focus of the managers on planflwide goal rather than on individual sub - unit goals For example a production manager may be Intmetted In Increasing machine utiiisatian at an individual work center and thlamp step may not be compatible to aVera1I organisational objective Crlticll1l of BadcftUllh CoetIng Costing system does not strlcty adhere to generally accepted principles of external reporting The advocates of backflush costing dte the materiality concept to counter argue these charges They claim that if InventorJes are low or not subject to Significant change from one ~ period to the next the results of backflush costing will not differ materially from results of the system that adhere to generally accepted accounting principles Olar~ClI of companies adopting Bade flUllh CostIng The companies adopting baddlush costing often meet the following three conditions 1 Management wants a simple accounting system and no detailed tracking of ~ material and direct labour through

a series of operations la required 2 Each producthu a set (If IIt8rKWd cost 3 Materlallnv~ levels are either low or constant H inventories are low the bulk of manufacturing COSE will flow into costs of goods sold and it is not deferred as invenlnry cost Backflush costing III espedally attractive In companies that have low Inventories resulting fromIT Difficulties of BaqdlUllh Costing 1 Backflush costing does not strict1y adhere to generally accepted accounting Principles of external reporting 2 The critics of backflush costing primarily emphuls on the absence of audit Trails 3 It does not pinpoint the IIIe of resources at esch step of the production proces9 4 Backflush costing Is suitable only for JIT Production system with virtually no ~material Inventory and minimum

work-in-process inventories It Is 1_ Feasible OtherwIse Bade flushing In a JlT SywtemBack flushing requires no data entry of any kind until a finished product Is completed At that time total amount of Information of finished product Is entered into computer lnlormatlon Is also fed based on bill of materials which shows list of components that should have been used In the production process ThIs Is subtracted from the beginning invenlnIY balance to arriving at the amount of inventory that should have been left now in hand Back flushing is good becallle data entry occurs once in the entire production process However there are some serious limitations of back flushing that must be corrected before it will work properly 1 Production reporting The total production figure entered must be correct or otherwlse wrong component types and quantities will be subtracted from stock ThIs Is a partlcuIar problem when there is high turnover or a low level of training to the production staff that records thts ttIformatton which leads to errors 2 Scrap reporting bull All abnormal scrap must be diligently traclced and will not be charged to Inventory Since scrap can occur anywhere in a production process a lack (If attention by any of the production staff can iesult In an inaccurare Inventory Once again high production turnover or a low level of employee training increIIIIes thlamp problem 3 Lot tradng Lot tracIng ill almost very difficult In beck flushing syslmn It Is required when a manufacturer needs to keep records of which production lots were WIled to create a product in cue all items in a lot must be recalled Only a picldng system can adequately record dIIs information Some computer systmn allows picldng and beck flushing systmn to coexist so that picks transactions for lot tracing purpose can still be entered In the computer Lot tracing may then still be possible if the right software is available however thlamp feature Is generally present only on high-end systems 4 Inventory accuracy It becomes difficult to know accurallely the Inventory balance IIIgt in a back flushing system data is fed into the system only once day ThIs makes it difficuIt to maintain an accurate set of inventory records In the warehouse Back f1U11h costing eltmlnates separate raw material and work-tn-progress account There is single Raw material in process Account (RIP) The RIP account is used only for tracking of the cost of raw materials Under JIT system materials ~

immediately placed into process For this reason there is no need to record it under separate Inventory account Combining direct labour and overhead into one category is a second feature of back flush costing Back flush costing combines labour costs with overhead costs in a temporary account called conversion cost controL This account accumulates the actual conversion cost on debit side and applied conversion cost on the credit side

Question 5 Define Material Requirement Planning (MRP) Answe 1 Material Requirement Planning is a computerised Production Scheduling System providing a basis for production

dlCisions 2 It progressively translates the forward schedule of final product requliements (the master production schedule) into

the n~mbers of sub- assemblies components and raw materials requited at each stage of the manufacturing cyclt

I P K SIKDAR8 ADVANCE LEARNING

23C ltIOALIA PLACE KOL)9lA 70001 9

Mmiddot 30165501 - 3shyWeb wwwpksalcom

3 in other words MRP involves input planning based on output budget

Question 6 List the almJ and benefit (objectives) of Matertalllequlrement PIannlng Answer 1 To determine quantity and timing of finished goods proouction as per the master production schedule 2 To ascertain quantity of raw materials sub-assemblies and components required for budgebd production based on

bill of materials 3 To compulle the inventories work-in-progress batch sizes and manufacturing and packaging lead ~ 4 To control inventory by ordering bought-in componems and raw materials in relation to the orders received or

forecast 5 To forecast the inventory poIIition period-by-period for a future time period of a DWufacturing operation 6 To geIVe lIS an inventory infoimatIon system helpful in plannins for raw malmials andeompooents parts 7 To generate purchase requisition notes and purchase orders through computer syatem automatically

Question 7 What are the pre-nquiaites for succesful operation of MllP S)8tem Answer 1 Production Schedule The Jatest production and purdwinc schedules prepared Ihould be strictly adhered to Day-toshyDay change from predetermined schedules will cause chaos Z Standard MIterial Input The raw materials sub-asllemblies and componenlll required for production should be predetermined in quantifilble terms Standards lIbould be set for the coIl8umption quantity quality mix and yield of raw materials for every unit of the finIalIed output 3 Workers cooperation Woddorce must be apprised of the sysUmt and the need for absolute adheren the schedules prepared AIso necessary internal control syatem should be developed to ensure the total adherence to the schedule 4 Accuracy of data Accuracy of the data supplied is vital to the MRP system Adherence to the purchase and production schedule becomes difficult in the abselve of accurate data

Question 8 What do you mean by E1lP7 What are the features of ERP It What are its beJjflts1 Answer 1 ERP refers to software which integrates all departments and functiOIl8 across a company into a single computer system that can serve all those needs of dfHerentdepartments 2 It combines all computerised departmerns together with the help of a singJe integtallltl software program that uses a single database so that various departments can more _lly Ihare Information and communkate with each other Integrated ERP fadlities company-wlde information integration covering all functional areal like DWufacturing seJJing and dtstribution payables ReceIvables inventory accounts hUDWl resoUrces etc HRP provides complete integration of system notonly aQOlll department but also IIa08II companies under the same management Custom$ Service ERP perform core activities and increases customer service tbereby augmenting the corporate image Information Sharb1g ERP bridges the Information gap across organisatiorts Project Management ERP is the solution for better project management Kom Fadlitles ERP a110ws IUtomatk introduction of technologies like IDectronic Fund TlIInSler (EFT) Electronic ota interchange (BDl) ~Video conpounderencing E- Commerce etc Business Dedeion MaIdq SoIIIdonII ERP provides busu- intelUgence tools like Decision Support systems (DSS) Executive Information System (JIS) Reporting DetaMining and early Warning systems lt Robots)for enabling people to make better dedsions it elIminallllllOlt buIineII problems lib mallerial shortage productivity enhancemants customer service Cash management inventory problema quality probIemi prompt delivery etc Futuristic ERP not only adm- the current requirements of the company but also provides the opportullity of continually improving and refining buJineIs pnxenea

Question 9 What are the bmeIIta of BllPt Answer The benefits IIlIsilIi from ERP are Product CoItiJIamp ERP II)8tmn supports advanIes c081lns methoda like Standard Costing Actual Costing ActIvity based costing thereby help in ~tion of cost of productli accurately Cost MonitorIDg and Control ERP can integrate all costing methods and information with finance nus proVides the company with esseotIal flnandal information for mooitoring and controlling costs Planning and M The ERPmiddot1I)8tmn simpllfies- compllcated logistics and helps in planning for aIid managing different divisioIl8 in different 10catkms lIS a ampingIe unit Information Flow The advanced utility of the ERP system helps in processing the flow of product and financial information in several dfHerentways Efficient Datlbue Mmlpment The ERP II)8tmn iVdamp in the effident managing of dabl on warehouses suppliers customers etc requ1red to run an orgmUzation~ely and profitllbly Inventory ManIpment inventory reporting supports all reporting of spedficand general types of stock tIIIIlIlacti Iilce stock transfers re-classificatinn ID changes and phyWa1 inventory result AIso ERP can IDUUIge stock and purchase requisitioIl8 selection of appropriate locations for receiptB inventory valuation warehouse management and cost accounting bull Customer Satisfadlon ERP II)8tmn defines the JogIatic procesaes flexiblf and effkiendy to deliver the right product from the right warehouse to the right customer at the right time-every Ii- thereby satisfying the cuatomers It also supports planning transportation confirmation dispatcl and proof of delivery processing Adclitionally it eIl8U1eS better after sales service Competitive Edge ERP system helps a Company to gain the competitive Edge by lta) Enablins the COIDpIJY to respond quickly and accurately to change in marlcet conditkms (b) improving busineas process (c) ensuring quality control (d) improved and objective production planning and (e) Offering internet Extranet SolUtiOIl8

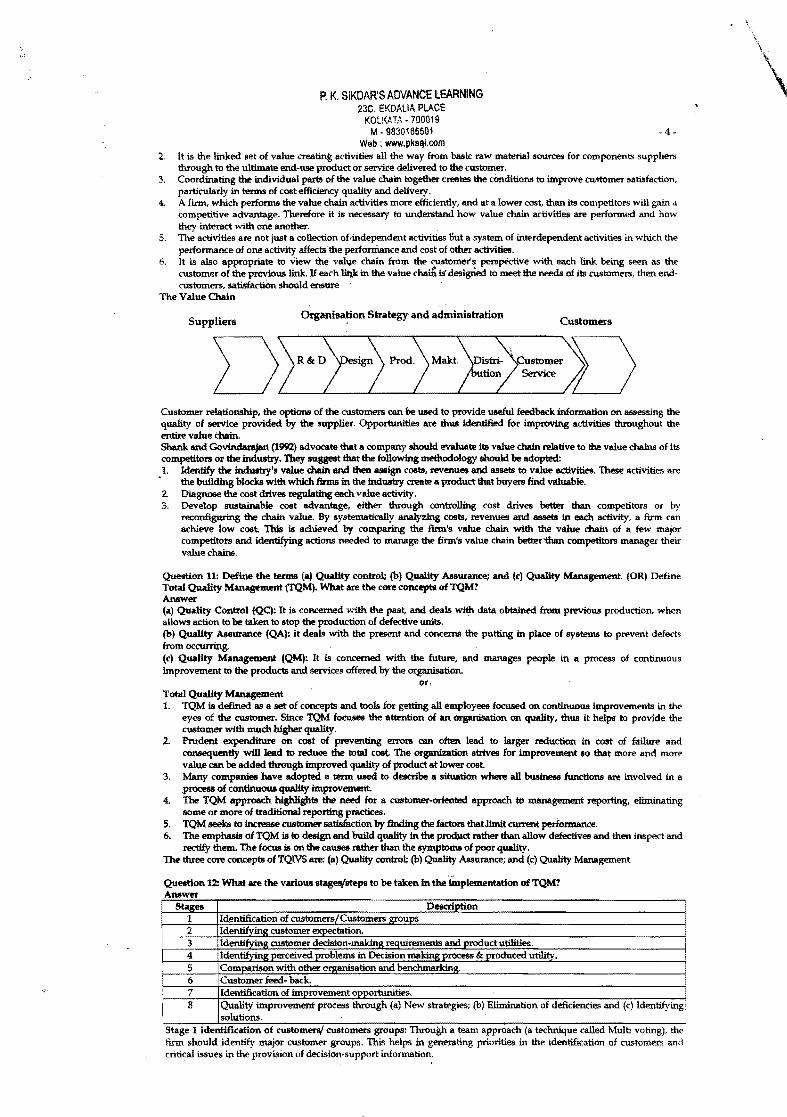

Question 10 What is Value awn ~ it basic ~ for systematic euDJne for ill utivities1 Answer V ALUll CHAIN Value awn is the aeries of interoa1 procesaes or activity a company performs bull to produce its product to desigITiUl product to deliver its product to support iUl Product 1 Increasing attention is now being given to value chain lINIlysis lIS a means of Increasing customer satisfltction and

managing costs more effectively

P K SIKDARS ADVANCE LEARNING 23C EKDALIA PLACE

KOllltATA - 700019 M - 9830165501 -4shy

Web wwwpkslIlcom 2 It is the linked set of value creating activities all the way from basic raw material sources for components suppliers

through to the ultimate end-use product or service delivered to the customer 3 Coordinating the individual parts of the value chain together creates the conditions to improve customer satisfaction

particularly in terms of cost efficiency quality and delivery 4 A firm which performs the value chain activities more efficiently and at a lower cost han its competitors will gain a

competitive advantage Therefore it is necessary to understand how value chain activities are performed and how they interact with one another

5 The activities are not just a collection ofindependent activities liut a system of interdependent activities in which the performance of one activity affectsthe performance and cost of other activities

6 It is also appropriate to view the vallie chain from the customers perspective with each link being seen as the customer of the previous link If each llisk in the value chafu isdesigned to meet the needs of its customers then endshycustomers satisfaction should ensure

The Value Chain

Organiea~on Strategy and administrationSupplier8 Customers

Customer relationship the options of the customers can be used to provide useful feedback information on lISSessing the quality of service provided by the supplier Opportunities are thus identified for improving activities throughout the entire value chain Shank and Govindaraja1 (1992) advocate that a company should evaluate itl value chain relative to the value chains of its competitors or the industry They lIIlsgest that the fol1owing methodology should be adopted 1 Identify the industrys value chain and then assign cosb revenues and assets to value activities These activities are

the building bloclcs with which firms in the industry create a product that buyers find valuable 2 DiAgnose the cost drives regulating each value activity 3 Develop sustainable cost advantage either through controlling cost drives better than competitors or by

reconfiguring the chain value By systematically analyzing costl revenues and assets in eadI activity a firm can achieve low cost 1lIis is achieved by comparing the firms value chain with the value chain of a few major competitots and identifying actions needed to manage the firms value chain bettermiddotthan competitors manager their value chains

Question 11 Define the tennB lta) QuaHty control (b) Quality Al8urance and (c) Quality Management (OR) Define Total Quality Management (TQM) What are the core concepts of TQM Answer (a) Quality Control (QC) It is concerned with the past and deals with data obtained from previous production when allows action to be taken to stop the production of defective units (b) Quality Alaurance (QA) it deals with the present and concerns the putting in place of systems to prevent defects from occurring (e) Quality Management (QM) It is concerned with the future and IlUIIUlges people in a process of continuous improvement to the produCtlil and services offered by the organisation

or Total Quality Management 1 TQM is defined as a set of conceptlil and tools for getting all employees focused on continuous Improvements in the

eyes of the customer SlnceTQM focuses the attention of an organisation on quality thus it helps to provide the customer with much higher quality

2 Prudent expenditure on cost of preventing errors can often lead to larger reduction in cost of failure and consequently will lead to reduoe the total cost The organization strives for improvement so that more and more value can be added through improved quality of product at lower cost

3 Many companies have adopted a term used to describe a situstion where all business functions are involved in II process of continuous quality improvement

4 The TQM approach highligbb the need for a customer-oriented approach to mansgement reporting eliminating some or more of traditional reporting practices

S TQM seeks to increase cuslnrner satislaction by finding the factors thatJimit CUlTelt perfonnarue 6 The emphasis of TQM is to design and build quality in the prodllct rather than allow defectives and then inspect and

rectify them The focus is on the causes rather than the symptoms of poor quality The three core concepts of TQIVS are (a) Quality control (b) Quality Assurance and (c) Quality Management

Question 12 What are the various stagessteps to be taken in the bnplementation of TQM Answer

7 Identification of im rovement 0 ortunities Quality improvement process through (a) New strategies (b) Elimination of deficiencies and (e) Identifying solutions

Stage 1 identification of customen customers groups Through a team approach (a technique called Multi voting) the firm should identify major customer groups This helps in generating priorities in the identification of customers and critical issues in the provision of decision-support information

8

I

- 1Btbullbullj -) )~i~JltC i_tMtI4Jrlt gtshy

nc EIltOJLlA PLACE KOLKATAmiddot700019

M bull 9630165501 _5shyWeb wwwpksalcom

1 Stage 2 identifying culItomer expectationa once the major customer groups are identified theit expectations are listed The qllStion to be answered Is- what does the JIlStomer expect from the firm Stage 3 Identifying cuatOIJ1lJ dedslon-maIdng requirementt and product Utilities Where the focus is on quality improvement the overriding need is to stay close to the customers and Follow their suggestions In this way a decision support system can be developed irworporating both financial and non--financial and non-financial information whlch seeks to satisfy user requirementsHence the firm finds out the answer to what are the customers decision-making requirements and product utilities The answerls sought by listing out inanagerial perceptions and not by actual interactlon with the customers Stage 4 Identifying perceived probl_ in dedalon-lIUIIdnamp proteM and produet Uttltties Using participative processes such as brainstorming and multi voting the finn seeks to Utt out _ of ~ where the greatest impact could be achieved through the implemmtation of improvements The firm identifies the anlWer to the question- what problem lUeltS do we perceive in the dedsUm-maJdng process Stage 5 Compmton with other orpntzIIIon and benduIIarIdna Detailed and syNmatlc internal deliberations allow the firm to develop a clear idea of their own IItlWIgtbIJ and weakneMes and of the __ of most signlftcant deficiency The benclunarldng exercisenow tha finn to how 0INr companieI are coping with IiDIilar problema and opportunities Stage 6 Customers Fee4bIIdc SIIIps 1 to 5 provide an information b(ue dewkgtplMSlt without reference to the customer This is rectified lit ~ 6 with a aurvey of ~tive cuaIo1nen whlch embnacel theit view on perceived problem areas interaction with the customera and oblaining their views halp the firm In correcting its own perceptions and refining its processes Stages 7 at 8 The identification of improvement opport1lIdtia and Implementation of Quality Improvement Process The outcomes of the customer 1IUlVey benchmarking and intemaI analysis provides the input for slages amp and ie identification of improVlllUlt opportunities and the implementation of II formal improvement process This is done through II six-atep process caIJed PRAISB for short

Question13 What is Pareto Analysis Outline Its use Answer (a) 1 P ARETO ANALYSIS is a rule that recommends fOCUB on the most important Mpectsof decision making in order to

simplify the procesll of dedsion making 2 It is based on the 8020 phenomenons firampt observed by ViHredo Pareto an Italian economist He notked that 80 of

the wealth of Milan was owned by 20 of its citizen This patlern of 8020 or approximations ~ 7030 can be observed in many different busineIIs situations

3 Main point is that II very I1IIAIl proportion of illem8 UBUII1ly accounts for the majority of value By concentrating on small pmportion of stock iIiem8 whlch jointly account for 80 of the total value a firm may be able to cOntrol most of its mohetary in~ in stocks

4 This phenomenon can be observed in many business situations the management can use this analysis in II number of different circumstances to atlrllct IJIIUIIgement attention to the key control mechanism

5 The lIllIIlysis of the compmys estimated total sales revenue might indicate that approximately 80 of its total sales revenue is eamed from llbout 20 of its product

6 This analysis is based on observations by Pareto that II small proportion of Items usually account for the majority of vlIlue

7 The management can UN it in II numllet of different circumstances to direct management IIttention to the key ~trol mechanism or planning aspecbl It helps clearly establish top priorities and to identify both profitable and unprofitable ~gets

80 of Result generated from 20 of Act 80 ofRevenue generated from 20 of products

bull 80 of cost of stock pnerafIedfrom 20 ofcastof inventory bull 80 of total cast generated from 20 of cast Drives bull 8Oof ReporIIed problem pnera1Id by 20 of underlying aluaes

b UsefuIneIIa of Pareto Analysia Pareto anaIym Is uaefId to

bull Prioritize problema goals and objectives bull Identify root cauaes

bull Select and define key performance improyement programs Maximize reampeIIlIh and product dewkgtptnent time Verify operating procedures and tlUUIUfacturln processes

bull Sales distribution of products or services Allocate physical financial and human resounea

Quation 14 Briefly detJeribe lOme bustnetII situatiON where Pareto ~Ylls can be appUed Answer- Pareto lIllIIlysis is applicable in the presentation of performance Indicators data through selection of representative process characteristics that truly determine or diredly or indirectly influence or confirm the desired quality or performance result or oulIome It is generally applicable to the following business situations 1 Product Pridttg Where a firm sells II number of products it may not be poesible to analyse rost-volume-price-profit

relationship for all products Panco AnaIylIis is used for analysing the firm estimated sales revenues from various products and it might indkate that IIpproximately 80 of its total sales 1eVenue Is earned from about 20 of ils products This helps top ~ to delegate the pricing decision for IIpproximately 80 of its products to the lower managerial levels Top ~t can concentrate on pricing decillion for the imporbmt 20 products whlch liTe euential for the companys aurvival Sophistica1eii pricing methodS can be adopted for the important products while (or other products castbased pricing methxls may be used

2 Customer Profltablllty Analysis The modem business thinking is to recopUse the customer and satisfy his requirements Hence instead of analysing products cuatomera can be analysed for theit relative profitability to the

P K SIKDARS ADVANCE LEARNING 23C EKDAUA PLACE

iltOLKATAmiddot7000i9 M 9830165501 -6

Web wllwpksalcom

organisation It is often found that approximately 20 of customers generate 80 of the profit Such analysis is useful for evaluation of the portfolio of customer profile and decision-making such as whether to continue serving a customer group What is the extent of promotion expenses to be incurred etc

3 ABC Analysis- Stock Coatrol In Raw Materia1stock controL it is found that only a few of the goods In stock make up most of the value About 80 of the materials value is due to high priced materials which constitute only 20 of the quantity These materials are classified into A B and C Categories based on their importance Control is directed primarily over j Category items by setting BOQ Stock Levels Surprise stock Verification procedures etc The outcome of such analysis is that by concentrating on small proportion of stock items that jointly account for 80 of the total value a firm will be able to control most of the monetary invesbnent in stocks

4 Activity Based Costing ActIvity BasEP Costing involves the identification of cost drives for various items of Overhead expenses GestezaJly 20 of tpe firms cost drivers are responsible 1m 80 of the total cost By analysing monitoring and controlling those costdrivers that attribute to high costs a better control and understanding of overheads will be obtained 0

5 Qclality Comol Pareto analysis ~ be extended to discoveY from an iUlIlIyJiis of defect report or customer complaints which Vital Few causes are ~iije for most of the reported problems Generally 80 of reported problems are traceable to 20 of the underlying causes By concentrating ones efforts on rectiiylng the vilal20 one can have the greatlst immediate impact on product quality Pareto Analysis intlicetls how frequently Nch type of failure (defect) occuts The purpose of the analysis Is to direct management attention to the area where the best returns can be achieved by solving most of quality problems perhaps just with a single action

Question 15 What is Penetration pricing What are the circumstances in which this polky can be adopted Answer Penetration Pricing 1 This pricing policy is in favours of using a low prP as the principal insIruIttent for penetrating IIUI8II markets early 2 It ill opposite to sldnuning prldng 3 The low pricing policy is introduced for the sake of kmg-tlr1l(sutvival and profitability and hence it has to receive

careful conskleratlon before Imp1ementation 4 It needs an analysts of the scope for market expansion and hence considerable amount of 1ISeIIlcll and fmecasting are ~ before detlmdning the price

5 Penetration pricing metll8 a price suitable for penetrating mass market lIB quickly as possible through lower price offers

6 This method is also used for pricing a new product In order to popularize a new product penetrating pricing policy Is used initially

7 The company may not earn profit by resorting to this policy during the Initial stage Later on the price may be iturelIsed u and when the demand pidts up

8 Penetrating pricing policy can also be adopted at any stage of the product life cycle for products whose market is approached with low initial price

9 The use of this policy by the existing concerns will discourage the new concerns to enter the market This pricing policy ill also known as middotstay-out-priclng Circumstances for adoption The three drcumstances In which penetrating pricing can be adopted are as under 1 When demand of the product is elastic to price in other words the demand of the product increases when price is

low 2 When there are SUbstantial88v1ng8 on large-scale production here Increampse in demand is sustained by the adoption

of low pricing policy 3 When mere is threat of competition The prices fixed at a low level act as an entry barrier to the prospective

competitors

Qclestion 16 What is Skimming pricing po8cy1 Answer- - Skimming price This term Is used in Pricin8 a new product Baskally there are two alten)atfves in pricing a new ptOduct One which calls 1m a relatively high price Is caJled SkImmIng price and other which calls for relatively low price Is called Penetration prPft The product should have some spedal features involving drastic departure from accepted mys of performing the service Por example Prestige Cooker was priced very high when it was first introduced In the country ~ product is Introduced with high price coupled with lar$e promotional expenses in the IlIIfly stages and lower prices at later stages SkImmIng pricing provides funds 1m financing expansion scheme Early hip prices may safeguard profits at IlIIfly stags but it may prevent quick sales to many potential buyers on whom companys future depends A policy of sldnuning pricing ill adopted under conditlon8 such as (8) a new product Is introduced In the market (b) there are a fuw producers (0) demand Is inelastic and (d) a sopldstkated product for use of rich and affluent customers

Qclestion 17 JlxpIain the term Ufecycle costing Answer It focuses on total cost (capital cost + revenue cost) over the products life including design CIMA defines life cycle costing as the practice of oblaining over their llfe time the best use of physical asset at the lowest cost of entity The term bull Life Cycle cost has been defined as follows It includes the costs associatls with acquiring using caring for and disposing of physical asset including the feasibility studies research design development Production maintenance replacement and disposal uwell as support training and operating costs generated by the acquisition use maintenance and replacement of permanent physical assets 1 Life cycle costing estimatls and accumuIatls costs over a products entire life cycle 2 The objective is to determine whether costs incurred at different stages ofdevelopment (planning designing amp

testing) manufacturing (conversion activities) and marketing (advertising distribution amp warranty) of the product will be recovered by revenue to be generated by the product over its life cycle

3 Life cycle costing provides an insight useful for understanding and managing costs over the life cycle of the product 4 In particular it helps to evaluate the viability of the product decides on pricing of the product at different stages of

product life cycle and often helps to estimate the value of the product to its users 5 When used in conjunction with target costing life cycle costing becomes a important tool for cost management

V 1 gt1rUl4t I4UVI4IIIII LCftlIIIII17 23C EKDALIA PLACE

KOLKATA 700019 M middot9630165501 _7

Web wwwpksalcom

6 Life cycle costing IlIIItimates and aaumulates costs over a products entire life cycle In order to determine whether the profits earned durtna the manufacturlng phase will cover the costs Incurred durtna the pre-and post ~g

middot1Ij stages 7 Identifying the costs Incurred durtna the different stages of a produdll life cycle provides an Insight Into

understanding and managing the total costs incUrred throughout its life cycle In particular life cycle costing helps management to understand the cost amsequences of developins and maIcing a product and to identify areas in which cost reduction efforts are llkely to be most effective

8 Most accounting syal8ml report on a period-by-period basis and product prob are not monitored over their life cycles In contrutproduct life cycle reporting Involves tracmacosts and revem on a prodld-by-product basis over several ~ periods throughout their life cycle

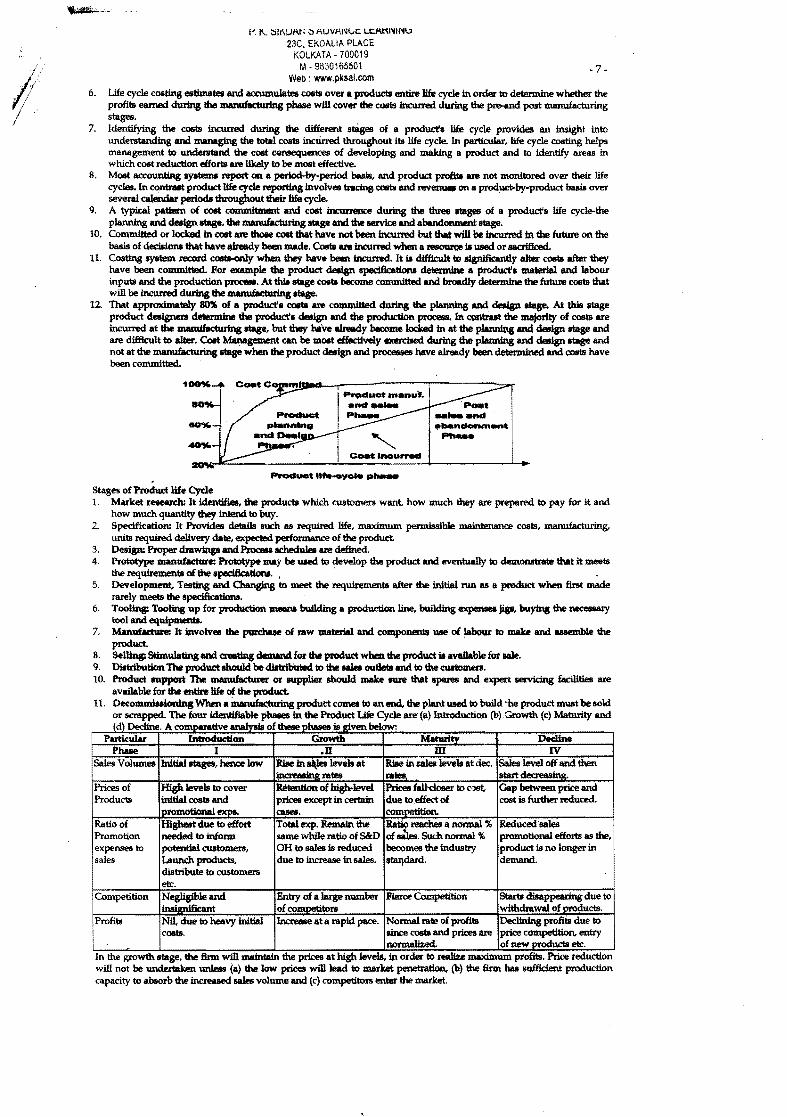

9 A typial pattern of cost commitment and cost incurrence durtna the three IIIaps of a products life cycle-the planning and design stage the manufacturlng stage and the aervice and abandOlllllllllt stage

10 Conunitled or locked In cost are those cost that have not been Incurred but that wW be Incurred In the future on the basis of dedsiOlllJ that have ~y been made Costs are Incurred when a retiIOIUa III used or IIIlCriBced

11 Costing system record costs-only when they have been Incurred It is difficult to fignificanlly aI- costs after lhey have been commited Por example the product dJIIiampn spedficatioN determine a products material and labour inputs and the production proalllll At this stage cotts become couunitred and broadly determine the future costs that will be incurred durtnathe ~ stage

12 That approximal8ly SO of a productl COIItI are conunitled durirIg the planning and deIign stage At this ltage product designers determine the produdl design and the production ptoCIlIIII In ~ the majorilyen of costs are Incurred at the mamifacturIng stage but they have amdy become locked In at the planning and deslgn stage and are difficult to alter Cost Management em be most effectively exercised durtna the planning and design ltage and not at the manufacturlng stage when the product dIlIIIlp and ptOCffiIlII have already been detmnined and costs have been committed

Stages of Prodlld life Cycle 1 Market reeeudl It identifilllll the products which customers want how much they are prepared to pay for it and

how much quantity they inlmld to buy 2 Specification It Providlllll details such lIS required life maximum permissible maintenance COBts manufacturing

units required delivery date expected performance of the product 3 Design Proper drawinp and~ achedulel are defined 4 Prototype ~r Prototype may be used to develop the product and eventually to demonstrate that it meets

the requirements of the spedftcatioN 5 Development TIlIIIting and Changing to meet the requirements after the initial run lIS a product when first made

rarely meets the spedflcationa 6 TooliJIg Toolina up for production sneena building a production line building expenteII jigI buylrls the necesaary

tool and equipmerda 7 Manufatturrlt involves the putchue of raw material and ~ use of labour to make and assemble the

product 8 SeJlint Stimulatingand creating demand for the proctwt when the proctwt it available lot sale 9 Distribution The product should be distributed to the sales oudetll and to tile CUItomera 10 Product IUpport The manufacturer or supplier should make sure that lparIlIII and expert IIlVicing fadIiIies are

available for the entire life of the product 11 DecoDllDillliordng When a ~ produtt comes to an end the plant used to build ile product must be sold

or saapped The four identifiable phaaes in the Product Life Cycle are (a) Introduction (b)Growth (c) Maturity and (d) Decline A comparatiVe analvsiI of theae Phases is Riven below

Partlcubr Introduction Growth Mturitv Decline Phale I U m IV

Sales Volumlllll Initial stagIliII hence low RIlle in+levels at rates

RIlle In saleIIlevels at dec rates

Sales level off and then start

Prices of Products

Higlilevels to cover initial COBUI and

lexps

ofhigh-level rices except in certain ases

Prices fa1tcloser to cJIlI due toeffect of competion

Gap betweert price and cost is further reduced

Ratio of Promotion expenses to sales

ffigbest due to effort needed to inform potential customers Launch products distribute to customers etc

otal expo Remain the same while ratio of SampD OR to sales is reduced due to Increase in sales

RatiflIIICbes a normal of 5Iiles Suchnonnal becomes the industry

staIJdardmiddot

Reduced sales promotional efforts as the product is no longer in demand

Competition Negligible and t

Entry of Illarge number of competitors

Fierce Competition Starts di8appearing due to withdrawal ofpro4Uctl

Profits Nil due to heavy initial costs

Increase at a rapid pace Normal rate ofprofits Iince costs and prices are normalized

Declining profits due to price competition entry of new products etc

In the growth stage the firm will mamtail the prices at high levels Ul order to realize DIOODum profits Price reduction will not be undertaken unIess (a) the low prices will lead to market pesebation (b) the firm has sufficient production capacity to absorb the increased sales volume and (c) competitors enter the market

__

P K SIKDARSADVANCE LEARNING

23C EKDAUA PLACE KOLKATA - 700019 8shy

M - 9830165501 Web wwwpksalcom

Re

1Decline nllO- Growthction

Time

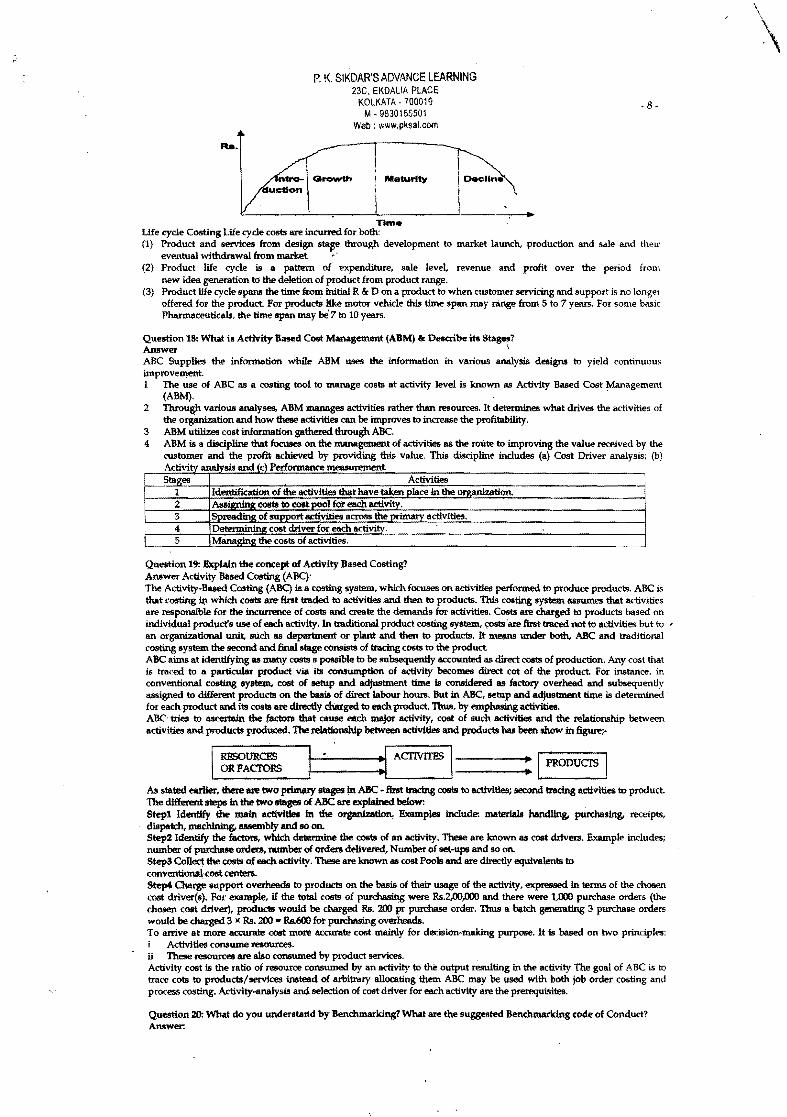

Life cycle Costing Life cycle costs are incurred for both (1) Product lind services (rom design stap through development to market launch production and sale and their

eventual withdrawal (rom market shy(2) Product life cycle is a pattern of expenditure sale level revenue and profit over the period from

new idea generation to the deletion of product from product range (3) Product life cycle spans the time from initial R amp D on a product to when customer servicing and support is no longer

offered for the product For products lUre motor vehicle this time span may range (rom 5 to 7 yelUS For some basic Pharmaceuticals the time span may be 7 to 10 years

Question 18 What is Artivity Based Cost Management (ABM) amp Describe its Stag Answ~ ABC Supplies the information while ABM UIIIS the information in vuious analysis designs to yield continuous improvement 1 The use of ABC as a costing tool to manage cOSts at activity level is known as Activity Based Cost Management

(ABM) 2 Through various analyses ABM manages activities ra~ than resources It determines what drives the activities of

the organizationand how these activities can be improves to increaampe the profitability 3 ABM utilizes cost information gathered through ABC 4 ABM is a discipline that focuses on the management of activities as the route to improving the value received by the

CllStom~ and the profit achieved by providing this value This discipline includes (a) Cost Driver analysiS (b) Activity Al ialvsis and (c) Performance measurement Stages Activities

1 Identification of the activities that have taken place in the organization 2 3

Assigning costs to COIIt pool for each activity S of support activities across the primary activities

4 5

COllt dti~ for each activity Managing the costs of activities

Question 19 Explain the concept of Activity Based Costing Answer Activity Based COIIting (ABC) The Activity-Based COIIting (ABC) ia a costing systenl which focuses on activities performed to produce products ABC is that costing ~ which COllts are first traded to activitiesand then to products This costing system assumes that activities are responmble for the incurrence of costs and create the demands for activities Costs are charged to products based on individual prodlcts use of each activity In traditional product costing system ~ostsare first traced not to activities but to bull an organizational unit sUch as department or plant and then to products It mellnS under both ABC and traditional costing system the second and final stage consists of tracing costs to the product ABC aims at identllying as many COIIts s posstble to be subsequently accounted as direct costs of production Any cost that is traced to a particular product via its consumption of activity becomes direct cot of the product For instance in conventional costing systeul COIIt of letup and adjustment time is considered as factory overhead and subsequently assigned to different products on the basis of direct labour hours But in ABC letup and adjustment time is determined for each product and its COIIts are directly charged to each product Thus by emphasing activities ABC tries to ascertain the factors that cause each major activity cost of such activitiel and the relationship between activities and products produced The relationship between activitleamp and products has been show in figureshy

LI~~R~p~~~CFS~RSJt-I~_middot-=--_--t+llI_ACTIVITFSJI= IPRODUcrs I As stated earlier there are two p~ IIIages In ABC - first tracing costs to activities second tracing activities to product The different steps in the two stages of ABC are explained below Stepl Identify the main activities in the organization Examples include materials handling purchasing receipts dispatch machining assembly and so on Step2 Identify the factors which determine the costs of an activity These are known as cost drivers Example includes number of purchase orders number of orders delivllell Number of set-ups and so on StepS Conect the costs ofeach activity These are known as cost Pools and are directly equivalents to conventionatcost centers Step4 Charge support overheads to products on the basis of their usage of the activity expre88ed In terms of the chosen cost driver(s) Por example If the total COllts of purchasing were Rs2OOooo and there were 1000 purchase orders (the chosen cost driver) products would be charged Rs 200 pr purchase order Thus a botxh generating 3 purchase orders would be charged 3 Rs 200 - Rs600 for purchasing overheads To arrive at more accurate cost more accurate cost mainly for decision-making purpose It is bIISed on two principles

Activities consume resources These resources are also consumed by product services

Activity COllt is the ratio of resource consumed by an activity to the output resulting in the activity The goal of ABC is to trace cots to productsservices instead of arbitrary allocating them ABC may be used with both job order costing and process costing Activity-analysis and selection of coat driver for each activity are the prerequisites

Question 20 What do you understarid by Benchmarking What are the suggetlted Benchmarking code of Conduct Answer

ii

I

P K SIKDS ADVANCE LEARNING 23C EKDALIA PLACE

I IltOLKATAmiddot700019

M - 9830165501 - 9shyWeb wwwpksalcom

1 Benchmarking is the process of identifying and learning from the best practices anywhere in the world 2 It is a powerful tool for continuoUli improvement in perfOIlklllllpounde 3 It involves comparing firms products services or activities against other best performing organizations either

internal or external to the firm The objective is to find out how the product service or activity can be improved and ensure that the improvements are implemented

4 It attempts to identify an activity that needs to be improved and firuiing a non-rival organization that is wnsidered to represent world-clus best practice and studying how it performJl the activity

Suggested Benchmarking Code of Conduct 1 Principle of Legality 2 Principles of Exchange 3 Principle of Confidentiality 4 Principle of Use 5 Principle of first part Contact 6 Principle of Third Party Contact 7 Principle of Preparation

Question 21 What are the Itapa In the proceI8 of BenclmarIdng Answer The pr_of benduDarldng Involva the following staga

Stage Deecri-ption 1 Planning

bull Determination of benchnlarking goal statement bull Identification of best perfOIlklllllpounde bull Establiahment of the benchmarking of process improvement team bull Definirur the relevant benchmarkIN measurement

2 Collection of Data and InfOrmation 3 Analysis of the findinRJ based on the data colJected in Staflf 2 4 Formulationand impJementation of recommendations 5 Constant monitorinst and

Question 22 What are the typa of Benchmarldng1 Answer Typet of BenchmaddDg- The benclunarking is a versatile tool that can be applied in variety of ways to meet a range of requirements The distinct types of benchmarks have been over a period of time Each has its own benefits and shortcomings and therefore each iI appropriate in certain cimmlatances then others The Benchmarking is of following as 1 Conlpetitive benchmarking 2 Strategic benchmarking 3 Global benchmarking 4 Process Benchmarking 5 Functional BenclunarIdng or Generic Benchmarking 6 Internal Benchmarking 7 External Benchmarking 1 Competitive ~ It involvesmiddotthe complUilon of competitors products proce88 and businefIs reaultll with own Benchmarking piIIl1IerII are drawn from the __ IMCtor However to protect confidentiality it is common for the companies to lIl1dertUe this type of btmclImarking through tradeaciationll or tJUrd parties 2 Strategic Benchmuldns it II IimiIar to the procea benchmarldng in nature but diffiInd ill illl IICOpe and depth It involves a systematic plOCeflll by which a company seeb to improI(e their overall performaRce by exaunining the longshyterm strategies It involva comparing high-level aspects such as developing new products andcompetencies etclaquo lt lt bull

3 Global Benchmarldna It 18 a benIhmarIdng tluQugh which distinction in international CIIkwe basineu procasa and trade practices IlCI08Ii COIIlpIUlie6 are bridamped and their IIWIiampation for businefIs plOCeflll iI~ are Ul1derIItood and utilized Globalization and advances in information tecbnQlogy leads to _ this type of eruhmarIdna 4 Proc_ BendmuIdcinamp It involvtS the comparison of an orpnizltion critiall buainesa pwcesaes and operatioN against best practice organization that performs similar work or deliver aUU1ar services For example how do boll practice organization plOCeflll ~s orders

5 Functional belIdImarIdrtg This type of ~ 18 uaed when organizationll iookto Itmclunark with partners drawn from different businees aectorI or areas of activity toftnd way of improving similar fanctions or work processes This sort of benchmarking can lead to innovation and dramatic improvements 6 Internal BenclunarIrin Intema1 beachmarkinginvolvts seeking partIlerll from within the same organization For example form business units klcated in different areas The main advantages of internal benchmarking are that IICcess 0

sensitive data and information are easier standudized data is oft2n readily aVaDabe and lllIWllly less time and resources are needed There may be fewer bIUriers to implementation as practices may be relatively easy to transfer across the same organization However real innovation may be lacking and best in claasltperfOrQUlIlCe is more libly to be found through external benchmarking lt 7 External BenchmarIriDs Extemd ~ invoIvts _king help of outside orpnizatiON that are known to be best in class Extemd benchmarking provides opportunitlell of leamIng ro)m those wh9 _ at the leading edge although it must be remembered that not every best practice solution can be middotlttransferred JIJ others In addition this type of oolpoundholalking may take up more time and resource to ensure the comparability of data and information the credibility of the findings and the development of sound recommendations The benchmarking can be eategoried into 1 Intra-group ~ In Intra group benchmarking the groups of companies in the same industry agree that similar units within the cooperating companies will pool data 01 their process The processes are benchmarked against each other at or operational level Improvement liask forces are established tT) identify and transfer ~t practice to all members of the group 2 Inter-Indultly benclmwldng in inter-indwltry benchmarking a non-laquogtrApeting bUlIineIIII with similar procestl is identified and asked to participate in a benchmarking exerci8e For example a publisher ofschoolbook may approach a publisher of university level books to establish a benchmarldng relatiolllllip Although two publishers are not in direct

P K SIKDARS ADVANCE LEARNUG

23C EKDALIA PLACE KOLlltATA - 700019

M - 0830165501 10 shyWeb wwwpksalcom

competition but there are obviously many similarities in their buSiness with respect to sources of supply distribution channels Each will be able to benefit from the experience of other and establish best practices in their common business processes

Question 23 Define Balance score Cards amp what are the four perspective of Balance Score card Answer A Scorekeeper the management accountant designs reports to help managers track progress in implementing strategy Many organisations have introduced a b~ score card approach to manage the implementation of their strategies The Balanced Scorecard The balanced scorecard translates an organisation mission and strategy into a set of performance measures that provides the framework for implementing the straegy The balanced scorecard does not focus solely on achieving financial objectives It also highlights the non-financial objectives that an organisltion must achieve to meet its financial objectives The Scorecard measure an organisation performance from four perspectives

Financial Customer Internal business processes and LeamIng and growth

A Companys strategy influences the measures it uses to track performance in each of ~ perspective Its called the balanced scorecard because it balances the use of finandal and nonfinandal performance measures to evaluate short-run and long-run perforJl1llIlte in a single report The balanced scorecard reduces managers emphasis on short-run linandal performance such as quarterly eantings Thats because the nonfinandaJ and oJllltional indicators such as product quality and customer satisfaction measure changes that a company is making for the long run The financial benefits of these long-run changes may not appear immediately in short- run eantings but strong improvement in non linandal measures is an indicator of tl(onomic value creation in the future For example an increase ~ customer satisfaction as measured by customer surveys and repeat purchases is a signal of higher sales and income in the future By balarui1g the mix of financial and non finandal measures the balanced scorecard broadners managements attention to short-run and long-run perfonnanoe The four Perspectives of thI BaWt~ed Scorecard 1 Ffnandal Perspective This perspective evaluates the Profitability of the strategy Because cost reduction relative to

competitors costs and salesgrowtb are chipsets key strategic initiatives the financial perspectives focuses on how much of operating income and return on capital results from reducing costs and selling more units of eXt

2 Customers Perspective This perspective identifies the targeted market segments and measures the companys success in these segments To monitor its growth objectives number of new customers and customers satisfaction

3 Internal businen pr()(ess Perspective This perspective foouses on internal operations that further the customers perspective by creating value for customers and further the financial perspective by increasing shareholder value Chipset determines internal business process improvement targets after benchmarking Ilgainst its main competitors

The internal busmess proceIIs perspective comprises three sub processes 1 The innovation process Creating products services and processes that will meet the needs of customers Chipset is

aiming at lowering costs and promote growth by improving the technology of its manufacturing 2 The operatiOll$ process Producing and delivering existing products and services that will meet the needs of

customers Chipsets strategic initiatives are (a) improYing manufacturing quality Reducing delivery time to customers and (c) Meeting specified delivery dates

3 Post sales Service Providing service and support to the customer after the sale of a product of service Although customers do not requiN much post sales service CX1 monitors how quickly and accurately CX1 is responding to customers service requests

Leaming and Growth Perspectives This perspective identifies the capabilities the organisation must excel at to achieve superior internal processes that create value for customers and shareholders Chipsets -hmning and growth perspectives emphasizes three capabiHties 1 Employee Capabilities measured using employee education and IIkIlllevels 2 Information system capabiUtIes measured by percentage of manufacturing processes with real-time feedback and 3 Motivation meuured by employee satisfaction and percentage of manufacturing and sales employees (line

employees) empowered to mange p~ses

Question 24 Define Tuget costing AnIIwer Target costing Is defined as a structured approach to determining the cost at which a proposed product with specified functionality and quality must be produced to generate a desired level of profitability at its anticipated selling price

Target Costing VIS Traditional coating Target COting traditional Costing

ProductionSpecification Production Speclfkation

t t Target Price and volume Product design

t t Target profit Estimated cost

t t Taret cost Tar cost

Product design Target price bull Target costing is a systematic approach to establish product cost goals based on market driven standards It is a strategic

management process for reducing costs at early stages of product planning and design Target costing begins with identifying customer needs and calculating an acceptable target sales price for the product Working backward from the sales price companies establish an acceptable target profit and calculate the target cost as follows

Target Cost Target Priee - Target profit Target costing is different from standard costing While target costs are determined by market driven standards (target sales price- target profit- Target cost) Standard costs are determined by design - driven standards with less emphasis on what the market will pay (engineered costs + desited markup - desired sales price) Target costing is a common practice in Japan where markets are eXtremely competitive The market determines the price

I

P -lt ~IKDARS ADVANCE LEARNING ~3C EKDAUA PLACE

KOLKATAmiddot700019 M bull 9830165501 -11shy

Wtib wwwpksalcom of products and there is a litae opportunity for the individual organizations to set prices Therefore controlling cost is

exlreillely important There are three cost reduction methods generally used in target costing (i) reverse engineering (ii) value analy~ and (iii) Process improvement Reverse engineering tears down the competitors products with the objective of discovering more design features that creal cost reductiOllS Value analyais attempts to assess the value placed on various placed on vanous product functiOllS by customers Ii the price customers are willihg to pay for a particular function is less than its cost the function is a candidal for e1imination Another possibility is to find ways to reduce cost of providing the function eg using common components Both reverse engineering and value analyais focus on product design to achieve cost reductions The processes used to produce and market the product are also s()tUCe5 of potential cost reduction Thus redesigning processes to improve their efficiency can also contribul to achieving the needed cost reductions

Question 25 The IWIin featuret of Target coating ampyIItem Answer The basic idea beneIlth target costing is that all product costs are p~ before a product even reaches the production floor For example types of malrials to be used in production method etc can be determined before actual production In these types of situation cost reduction focus of any company should be to review the costs of products while they are still in the design stage Every effort at the design stage is dooe to keep these costs to a minimum Target costing has been described iii a process that occurs in a competitive environment In which cost minimization is an inlportant component of profitability It is baaed on the promise that cost plaJmins cOat management and coat reduction must necessarily occur in the design development process of the product to minimize the total life cycle cost of the product All acceptable definition of target costing dOllllllOt exist following important deiinltions have been given Sakurai liIIYs Target costing can be defined u a cost management tool for reducing the overall cost of a product over its entire life cycle with the help of production ~ research and design marketing and accounting departments The main Features or followed in T Cos

Ste Descri 1 2 3 4

Question 26 Tbe role of Cost atcountant8 role in a Target Coating Envirorunent Answer Cost ac~0b1tant8 role In a Target Coating Environment 1 The cost accountant should be able to provide for the other members of the design team a runniJ1g series of cost

estimalls based on initial demgn llketclles and activity-based costing reviews 2 The cost accountant helps the prefect team in capital budgeting decisiOllS 3 The cost accountant works with the design team to help it unders1and cost-benefit-trade ofEs of using dilierent design

or cost optiOllS in the new product 4 The cost accountant continues to compan a products actual cost to the target cost even after the design is completed

Question 17 DefIne Value Iogineerins7 Answer bull 1 Value engineering aims tll reduce non value - added coets by reducing the qWUtity Of cost drivers of nonvalueshy

added activities Por example to reduce rework coats The Company must reduce reworkmiddothours 2 Value engineering also ampeeb to reduce value -added costs by achieving greater efficiency in value- added activities

For example to reduce direct mmufacturing labor costs 3 A Value added cost is a cost that if e1imina1ld would reduce the actual or pcttceived value or utility (usefulness)

customers obtain from using the product or service 1 A NonvaIue added cost is a cost that if e1imina1ld would IlOl reduce the actual or perceived value or utility

(usefulnea) customers obtain from using the product or service It is a cost that the customer is unwilling to pay for Examples of nonva1ue- addedcosts are coats of reworking and repairing products

2 Value engineering is a ytItematU eYaluation ofallupeets of the cost structure of a product or service including research and development design of products and processes production marketing distribution and customer service with the objective of reducing costs while liIItiafying customer needs

6 It diliers from traditiOPal approadlet to cost Ieduction and cost control in that its focus is on the elimination of non value- added activities (eg waste) from the-~ess

7 Value engineering focuses on improving those qualities that the customer desires while reducing or e1iminating urmecessary moves queses setup and other activities that the custoller willllOt pay for

s The process is re-engineered to e1imina1 non-value added work and thefeDy enhance the value of the process to the customer

Question 28 ExplaiA COIIRpt of teaming Curve and State the areal iA which the application of learning curve theory can help a manufilCtUlJns orpnizIIlion7 Answer in case of a job which is repetitive in nature and the working time is not scheduled by the speed of machinery an individual is likely to become more confident and knowledgeable abeut his work iii he gains mOre experience AB a consequence of his learning effect he can do the job in less time than when he initially commenced the first job Ultimally when he has acquired more experience the leaming process will lend to stop The speeding up of a job with repeated performance is known u 1earning effect or learning curve effect The reduction in the required labour time thus can be quantified Leaming curve theory wu first developed in the Unilld StateS aircmft industry It has been extended to other labour-oriented industries and has been extended to no production activities such as marketing efforts Learning curve

effect is not only restricted to individual but it also applies to a group of workers How~er the 1earning effect is not an automatic natural phenomenon All production process win not show rate of increased effiderrcy and there may be cases where the differerues in the learning ralls will be substantial The quantitative average time per unit produced is normally COIISidered to be reduced by a colStilnt percentage every time total output of the product is doubled The following table the working of which is bftsed on 80 learrting effect can exemplify this

P K SIKDARSADVANCE LEARNING 23C EKDALIA PLACE

KOLlltATA - 700019 M - 9830165501 -12 shy

Web wwwpksaLcom

Number of Units (Cumulative)

Cumulative average time per unit in hours

total Time IncrellUIltal time for additional units

Learning curve theory can be used A To calculate the incremental costof making extra units of a particular products B To set standarde for labour C To prepare realistic production budge1iani to report labour cost variances D To quote contact price Direct labour cost and time as well as variable overhead costs which vary with direct labour hours are affected by leaming curve On the other hand ~ cOS will not be affected In case where absorption costing eyatem in vogue the fixed overhead applkaUon Ilte may be ~ due to higher production or use of capacity BesIdes the above cues where learning curve Will have effect dtredly a management accountant should bear in some other considerations such as 1 Sales promotion and advertising expenditUre 2 Delivery da1e commitments 3 Budgeting and lltandard cost 4 CIIIh budget 5 Work scheduling IUId overtime declsions and 6 Economics of scale The areu in which the Ueaden oIlemting curve can help bull manufamuing organtzation are 1 Improvement of ProdwtIvity As the experience Is gained the performance of worlcers improves time taken per unit

redUcei and thus his productivity goes up 2 COlt PredictiOnli Learning curve provides better cOS predictions to enable price quotations to be preferred for

potential orders 3 Work scheduling Learning curve enablell us to predict the inputs required more effectively and helps in the

preparation of accurate delivery schedilIes 4 Standarde setting If budgets and standards are set without cousiderlng learning curve it is meaningless because

variances will arise

Question 29- Briefly dill(U58 en curvilinear CVP analytill Answer In CVP analysis the usual aalumption Is that the total IIampieII line and variable cost line will have linear relationship that ill these llneI will be straight llneI However in IlCtual particle it ill unlikely to have a linear relationship for two reasons namely bull After the saturation point of the exiting demand the sales value may llhow a downward trend bull The a~unit variable cost declines initially reflecting the fact that as output increase the firm will be able to

obtain bulk diIIcountI on the purchase of raw materialll and can also benefit from diviIIion of labour When the plant is operated at further IIigher levels of output due to bottlenecks and variIIbJe cost per unit will tend to increase Thus the law of increase costs may opera1e and the variable cost per unit may increaampe after reaching a particular level of output

In such CSIIes the contribution will not increase in linear proportion ie based on the phenomenon of diminishing marginal productivity the total cOS line will no be straight polnIB as lllsumed but will be of curvilinear shape This optimum profit is earned at the point where the distance between sales and total cost is the greatest

Question 30- What 40 JOIl UJldentand by CVP analyaIa DlIIaa 1Iriefly the 1llllUlnpd0llll underlying etmeept Answer As the name ~ cOS volume profitCVP) anaIysIs Is the analysis of three varlabIes cost volume and profit Such an anaIysIs explores the relaliorlJbip between cOllIs revenue activity kMIs and the resulting profit It alms at measuring variations In cOS and volume CVP malyIIIIIla bue4 on the followfDg-umpdons 1 Changes In the levels of revenues and COIIts arise only because of changes in the number of product (or service) units

produced and oldfor example the number of televiIIion leis pIOIiuced and sold by SONY Corporation or the number of packages delivered by overnight Express The nwnber of output units III the only revenue driver and the only COlt driver just III a cOS driver is any factor that affects costs a revenuedriver III a variIIble such as volume that casually affects revenues

2 Total COIIts can be separated Into two components a fixed component that does not vary with output level and a variable componell1 that changes with respect to output level Furthermore variable COIIts include both direct variable costs and indirect variable costs of a product Similarly fixed costs include both direct fixed costs and indirect fixed costs of a product

3 When represented graphically the behaviors of total revenues and total costs are linear (DtIIning they can be repmented as a straight line) in relation to output lIvel within a relevant range (and time period)

4 Selling price variable cOS per unit and total fixed cost (within s relevant range and time period) are known and coustant

5 T he antilysis etther covers Ii single product or assumes that the prodllcOOn of different products when multiple products are sold will remain constant as the level of total units sold changes

6 All revenues and costs can be added subtracted and compared without taking into account the time value of money AstIumptions of cost-volume -proftt analysill The assumptions of cost-volume -profit are as followsshy1 All variables remain constant per unit 2 Asingle product or constant sales mix 3 Fixed costs do not change 4 Profits are calculated on variable cost basis 5 Total costs and total revenues are linear functions of output 6 The anaIysiII applies to relevant range only

I

- bulllIrWlt v IIIJVANt LIARNING 3C EKDALIA PLACE

IltOLKATA - 700019 M bull 983016550 13 shy

Web wwwpksalcom

Ii 7 Costs can be accuralely divided into fixed and variable components

8 The analysis applles only to short-tenp horizon

Question 31- Write short notes on Sealed Bid Pricing Answer 1 Competitive Pricing is prevalent when firms compete for jobs 01 the bIIIia of bids while quoting for specific

assignment or jobs eg government contracts speltialised work contracts etc 2 The bid constitutes the finns offer price The quotation is generally based on the incremental costs plus a reasoJlllble

mark-up 3 The finn objective in bidding is to get the contract This may mean that it hopa to fix its price lower than that of the

other bidding finns Pricing is bued 011 expectations of how competitors will price rather than on rigid relation based on the concems own coata or demand

4 If a low price is quoted in order to wiR the contract the finn may lose ita proflta and worsen ita situation On the other hand if it raises its prices chances of gaining the contract may be reduaed

5 ProbabWty analysis may be used to analyze the impIIct of various bid priceB This estimate ~ information or competitors trategies and hence the finn has to rely on conjecture trade gossip or past bidding history

QuHtion 32- Write a Ihort note on Pelformance Budget Answer 1 Performance Budgeting may be described l1li a budgetary system where the input costa are related to the performance