1 Module 8 Fixed overhead analysis and reporting for control Lectures and handouts by: Shirley Mauger, MBA, HB Comm, CGA Management Accounting Fundamentals 2 Module 8 - Table of Contents 8.1 Overhead rates and standard costing 8.2 Fixed overhead budget and volume variances 8.3 Journal entries to record standard costs and variances 8.4 Computer illustration 8.4-1: Fixed costs in a flexible budget 8.5 Full income statement variance analysis 8.6 Decentralization in organizations 8.7 Segment reporting 8.8 Revenue variance and marketing expense analysis 8.9 Return on investment and residual income 8.10 Balanced scorecard 8.11 Other performance measures 1 N/A 2 3 4 Part Content 3 Module 8 - Table of Contents Review question: Variance analysis and journal entries Review question: Variance analysis, working backwards from data Review question: Segmented statements Review question: Segmented statements, ROI and residual income Review question: Sales and market variances (High low method) Review question: Multiple choice 5 6 7 8 9 10 Part Content

Transcript

1

Module 8

Fixed overhead analysis and

reporting for control

Lectures and handouts by:

Shirley Mauger, MBA, HB Comm, CGA

Management Accounting

Fundamentals

2

Module 8 - Table of Contents

8.1 Overhead rates and standard costing

8.2 Fixed overhead budget and volume variances

8.3 Journal entries to record standard costs and variances

8.4 Computer illustration 8.4-1: Fixed costs in a flexible budget

8.5 Full income statement variance analysis

8.6 Decentralization in organizations

8.7 Segment reporting

8.8 Revenue variance and marketing expense analysis

8.9 Return on investment and residual income

8.10 Balanced scorecard

8.11 Other performance measures

1

N/A

2

3

4

Part Content

3

Module 8 - Table of Contents

Review question: Variance analysis and journal entries

Review question: Variance analysis, working backwards from

data

Review question: Segmented statements

Review question: Segmented statements, ROI and residual

income

Review question: Sales and market variances (High low method)

Review question: Multiple choice

5

6

7

8

9

10

Part Content

2

4

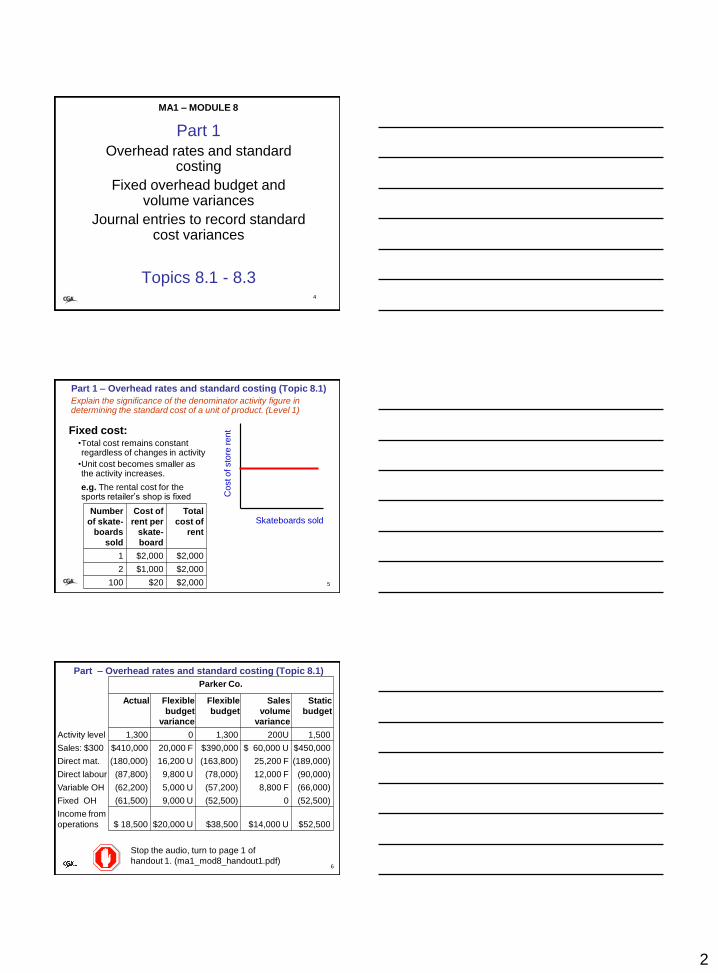

Part 1

Overhead rates and standard costing

Fixed overhead budget and volume variances

Journal entries to record standard cost variances

Topics 8.1 - 8.3

MA1 – MODULE 8

Part 1 – Overhead rates and standard costing (Topic 8.1)

Explain the significance of the denominator activity figure in determining the standard cost of a unit of product. (Level 1)

5

Fixed cost: •Total cost remains constant regardless of changes in activity

•Unit cost becomes smaller as the activity increases.

e.g. The rental cost for the sports retailer’s shop is fixed

Skateboards sold

Co

st o

f sto

re r

en

t

Number

of skate-

boards

sold

Cost of

rent per

skate-

board

Total

cost of

rent

1 $2,000 $2,000

2 $1,000 $2,000

100 $20 $2,000

6

Stop the audio, turn to page 1 of

handout 1. (ma1_mod8_handout1.pdf)

Part – Overhead rates and standard costing (Topic 8.1)

Parker Co.

Actual Flexible

budget

variance

Flexible

budget

Sales

volume

variance

Static

budget

Activity level 1,300 0 1,300 200U 1,500

Sales: $300 $410,000 20,000 F $390,000 $ 60,000 U $450,000

Direct mat. (180,000) 16,200 U (163,800) 25,200 F (189,000)

Direct labour (87,800) 9,800 U (78,000) 12,000 F (90,000)

Variable OH (62,200) 5,000 U (57,200) 8,800 F (66,000)

Fixed OH (61,500) 9,000 U (52,500) 0 (52,500)

Income from

operations $ 18,500 $20,000 U $38,500 $14,000 U $52,500

3

7

Handout 1, page 1

Part – Overhead rates and standard costing (Topic 8.1)

Parker Co.

Actual Flexible

budget

variance

Flexible

budget

Sales

volume

variance

Static

budget

Activity level 1,300 0 1,300 200U 1,500

Sales: $300 $410,000 20,000 F $390,000 $ 60,000 U $450,000

Direct mat. (180,000) 16,200 U (163,800) 25,200 F (189,000)

Direct labour (87,800) 9,800 U (78,000) 12,000 F (90,000)

Variable OH (62,200) 5,000 U (57,200) 8,800 F (66,000)

Fixed OH (61,500) 9,000 U (52,500) 0 (52,500)

Income from

operations $ 18,500 $20,000 U $38,500 $14,000 U $52,500

Module 7 review – Calculate all

variances

8

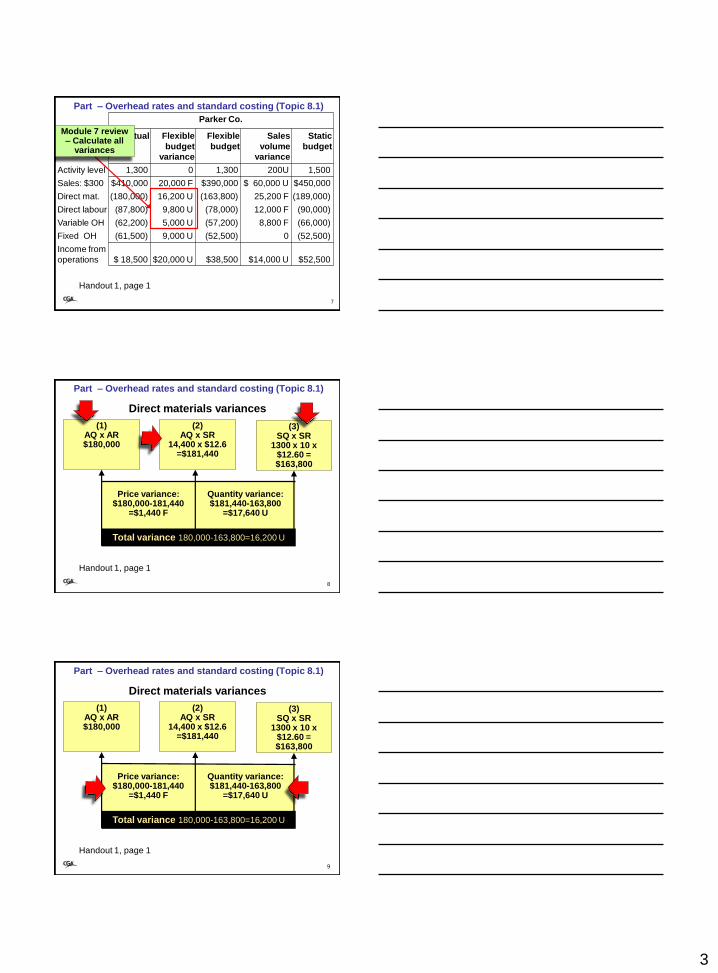

Part – Overhead rates and standard costing (Topic 8.1)

Quantity variance:$181,440-163,800

=$17,640 U

Price variance:$180,000-181,440

=$1,440 F

Direct materials variances

(1)AQ x AR$180,000

(3)SQ x SR

1300 x 10 x $12.60 = $163,800

Total variance 180,000-163,800=16,200 U

(2)AQ x SR

14,400 x $12.6=$181,440

Handout 1, page 1

9

Part – Overhead rates and standard costing (Topic 8.1)

Quantity variance:$181,440-163,800

=$17,640 U

Price variance:$180,000-181,440

=$1,440 F

Direct materials variances

(1)AQ x AR$180,000

(3)SQ x SR

1300 x 10 x $12.60 = $163,800

Total variance 180,000-163,800=16,200 U

(2)AQ x SR

14,400 x $12.6=$181,440

Handout 1, page 1

4

10

Part – Overhead rates and standard costing (Topic 8.1)

Efficiency variance:$78,000 – 78,000

= 0

Rate variance:$87,800 – 78,000

= $9,800 U

Direct labour variances

(1)AQ x AR$87,800

(3)SQ x SR

1300 x 5 x $12 = $78,000

Total variance 87,800 – 78,000 = $9,800 U

(2)AQ x SR

6500 x $12 = $78,000

Handout 1, page 1

11

Part – Overhead rates and standard costing (Topic 8.1)

Efficiency variance:$57,200 – 57,200

= 0

Spending variance:$62,200 - $57,200

= $5,000 U

Variable overhead variances

(1)AQ x AR$62,200

(3)SQ x SR

5 x 1300 x $8.80 = $57,200

Total variance $62,200 – 57,200 = $5,000 U

(2)AQ x SR

6500 x $8.80 = $57,200

Handout 1, page 1

12

Handout 1, page 1

Part – Overhead rates and standard costing (Topic 8.1)

Parker Co.

Actual Flexible

budget

variance

Flexible

budget

Sales

volume

variance

Static

budget

Activity level 1,300 0 1,300 200U 1,500

Sales: $300 $410,000 20,000 F $390,000 $ 60,000 U $450,000

Direct mat. (180,000) 16,200 U (163,800) 25,200 F (189,000)

Direct labour (87,800) 9,800 U (78,000) 12,000 F (90,000)

Variable OH (62,200) 5,000 U (57,200) 8,800 F (66,000)

Fixed OH (61,500) 9,000 U (52,500) 0 (52,500)

Income from

operations $ 18,500 $20,000 U $38,500 $14,000 U $52,500

Budget and production

volume variances

5

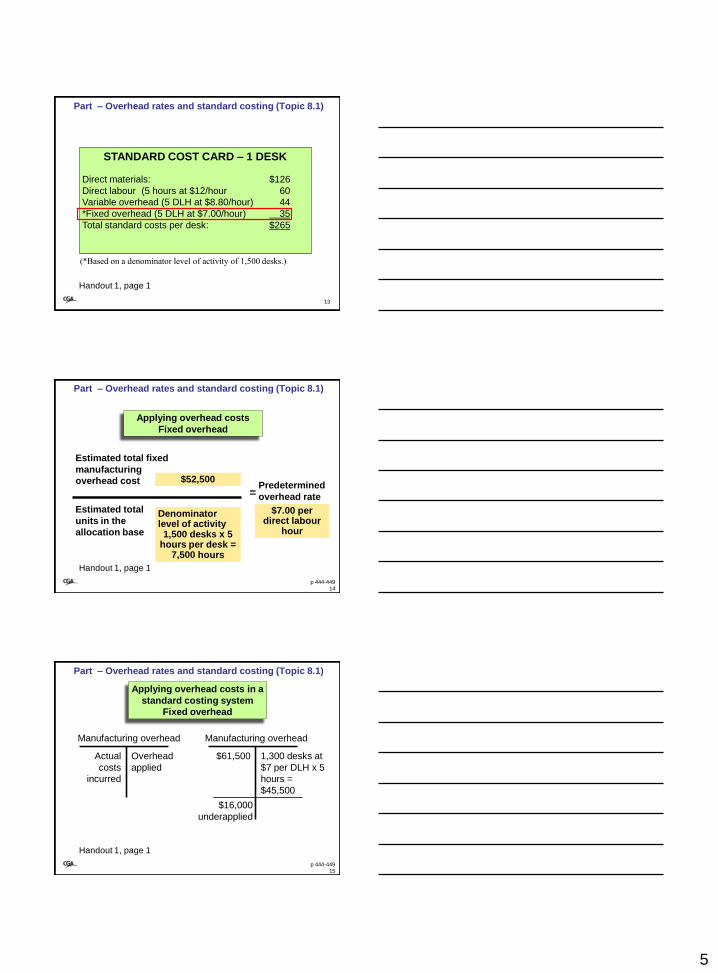

13

STANDARD COST CARD – 1 DESK

Direct materials: $126

Direct labour (5 hours at $12/hour 60

Variable overhead (5 DLH at $8.80/hour) 44

*Fixed overhead (5 DLH at $7.00/hour) 35

Total standard costs per desk: $265

(*Based on a denominator level of activity of 1,500 desks.)

Part – Overhead rates and standard costing (Topic 8.1)

Handout 1, page 1

Predetermined

overhead rate

Applying overhead costs

Fixed overhead

=

Estimated total fixed

manufacturing

overhead cost

Estimated total

units in the

allocation base

$52,500

Denominator level of activity1,500 desks x 5

hours per desk = 7,500 hours

$7.00 per direct labour

hour

14p 444-449

Part – Overhead rates and standard costing (Topic 8.1)

Handout 1, page 1

Applying overhead costs in a

standard costing system

Fixed overhead

Manufacturing overhead

Actual

costs

incurred

Overhead

applied

Manufacturing overhead

$61,500 1,300 desks at

$7 per DLH x 5

hours =

$45,500

$16,000

underapplied

15

Part – Overhead rates and standard costing (Topic 8.1)

Handout 1, page 1

p 444-449

6

Volume variance:(2)-(3)

Budget variance:(1)-(2)

Fixed overhead variances

(1)Actual cost

$61,500

(3)AU x SQ x SR

Total variance (1)-(3)

(2)BU x SQ x SR

Budgeted units = Denominator level of activity

Part 1 – Fixed overhead budget and volume variances

(Topic 8.2)Compute and properly interpret the fixed overhead budget and volume variances. (Level 1)

16Handout 1, page 1 p 444-449

Volume variance:(2)-(3)

Budget variance:(1)-(2)

Fixed overhead variances

(1)Actual cost

$61,500

(3)AU x SQ x SR

1,300 desks x 5 hours x $7=

$45,500

Total variance $61,500 - $45,500 = $16,000 U

(2)BU x SQ x SR

Budgeted units = Denominator level of activity

17

Part 1 – Fixed overhead budget and volume variances

(Topic 8.2)

Handout 1, page 1 p 444-449

Volume variance:(2)-(3)

Budget variance:(1)-(2)

Fixed overhead variances

(1)Actual cost

$61,500

(3)AU x SQ x SR

1,300 desks x 5 hours x $7=

$45,500

Total variance $61,500 - $45,500 = $16,000 U

(2)BU x SQ x SR

1,500 desks x 5 hours x $7=

$52,500

18

Part 1 – Fixed overhead budget and volume variances

(Topic 8.2)

Handout 1, page 1 p 444-449

7

Volume variance:(2)-(3)

Budget variance:$61,500 - $52,500 =

$9,000 U

Fixed overhead variances

(1)Actual cost

$61,500

(3)AU x SQ x SR

1,300 desks x 5 hours x $7=

$45,500

Total variance $61,500 - $45,500 = $16,000 U

(2)BU x SQ x SR

1,500 desks x 5 hours x $7=

$52,500

More was spent

than planned.

19

Part 1 – Fixed overhead budget and volume variances

(Topic 8.2)

Handout 1, page 1 p 444-449

Volume variance:$52,500 - $45,500 =

$7,000 U

Budget variance:$61,500 - $52,500 =

$9,000 U

Fixed overhead variances

(1)Actual cost

$61,500

(3)AU x SQ x SR

1,300 desks x 5 hours x $7=

$45,500

Total variance $61,500 - $45,500 = $16,000 U

(2)BU x SQ x SR

1,500 desks x 5 hours x $7=

$52,500

200 less units were

produced and sold.

20

Part 1 – Fixed overhead budget and volume variances

(Topic 8.2)

Handout 1, page 1 p 444-449

Part 1 – Journal entries to record standard costs and

variances (Topic 8.3)Prepare journal entries to record standard costs and variances. (Level 2)

Formal entries to record variances:

1. Raw materials purchases

2. Issuing raw materials to production

3. Incurrence of direct labour

4. Variable and fixed overhead (not demonstrated here)

Chapter 10 appendix 10B

21p 462-464

8

Part 1 – Journal entries to record standard costs and

variances (Topic 8.3)Prepare journal entries to record standard costs and variances. (Level 2)

Formal entries to record variances:

1. Raw materials purchases

2. Issuing raw materials to production

3. Incurrence of direct labour

4. Variable and fixed overhead (not demonstrated here)

Chapter 10 appendix 10B

Stop the audio, turn to Problem 10-27 p.477

In the textbook 22p 462-464

Accounts Payable Raw materials

DM price variance

Wages payable

DM quantity variance

Work in progress

DL efficiency varianceDL rate variance

23

Part 1 – Journal entries to record standard costs and

variances (Topic 8.3)

p 462-464

DR Direct materials AQ x SR 8,000 x $6.00

48,000

CR Direct materials price

variance AQ x (SR-AR) 8,000 x (6-5.75)

2,000

CR Accounts Payable AQ x AR 46,000

1. A total of 8,000 kilograms of material were

purchased at a cost of $46,000

24

Part 1 – Journal entries to record standard costs and

variances (Topic 8.3)

p 462-464

9

Accounts Payable Raw materials

46,000

DM price variance

2,000

48,000

Wages payable

DM quantity variance

Work in progress

DL efficiency varianceDL rate variance

25

Part 1 – Journal entries to record standard costs and

variances (Topic 8.3)

p 462-464

2. Issued 6,000 kilograms of materials to production

to produce 3,000 units

DR Work in processSQ x SR 3,000 x 1.5 x $6

27,000

DR Direct materials quantity

variance (AQ-SQ)xSR ( 6,000-(3,000x1.5))x$6

9,000

CR Direct materialsAQ x SR 6,000 x $6

36,000

26

Part 1 – Journal entries to record standard costs and

variances (Topic 8.3)

p 462-464

Accounts Payable Raw materials

46,000

DM price variance

2,000

48,000

Wages payable

DM quantity variance

9,000

36,000

Work in progress

27,000

DL efficiency varianceDL rate variance

27

Part 1 – Journal entries to record standard costs and

variances (Topic 8.3)

p 462-464

10

3. Recorded the direct labour wages for June

DR Work in processSQ x SR 3,000 x .6 x $12

21,600

DR Labour rate variance AQx(AR-SR) (10 x 160 x $12.50-$12)

800

CR Labour efficiency variance(AQ-SQ) x SR ((10x160)-(3,000x.6))x$12

2,400

CR Wages payableAQ x AR 10x160x$12.50

20,000

28

Part 1 – Journal entries to record standard costs and

variances (Topic 8.3)

p 462-464

Accounts Payable Raw materials

46,000

DM price variance

2,000

48,000

Wages payable

DM quantity variance

9,000

36,000

Work in progress

27,000

21,600

20,000

DL efficiency variance

2,400

DL rate variance

800

29

Part 1 – Journal entries to record standard costs and

variances (Topic 8.3)

p 462-464

30

Part 2

Full income statement variance analysis

Decentralization in organizations

Segment reporting

Topics 8.5 - 8.7

MA1 – MODULE 8

11

Part 2 – Full income statement variance analysis (Topic 8.5)

Prepare an income statement incorporating variance analysis. (Level 2)

Part 2 – Full income statement variance analysis (Topic 8.5)

Sales $xxx

Cost of goods sold (standard costs) $xxx

Write off variances

Direct materials price and quantity xxx

Direct labour rate and efficiency xxx

Variable overhead spending and efficiency xxx

Adjusted cost of goods sold xxx

Variable selling and administration xxx xxx

Contribution margin xxx

Fixed manufacturing overhead xxx

Fixed selling and administration xxx

Net income $xxx

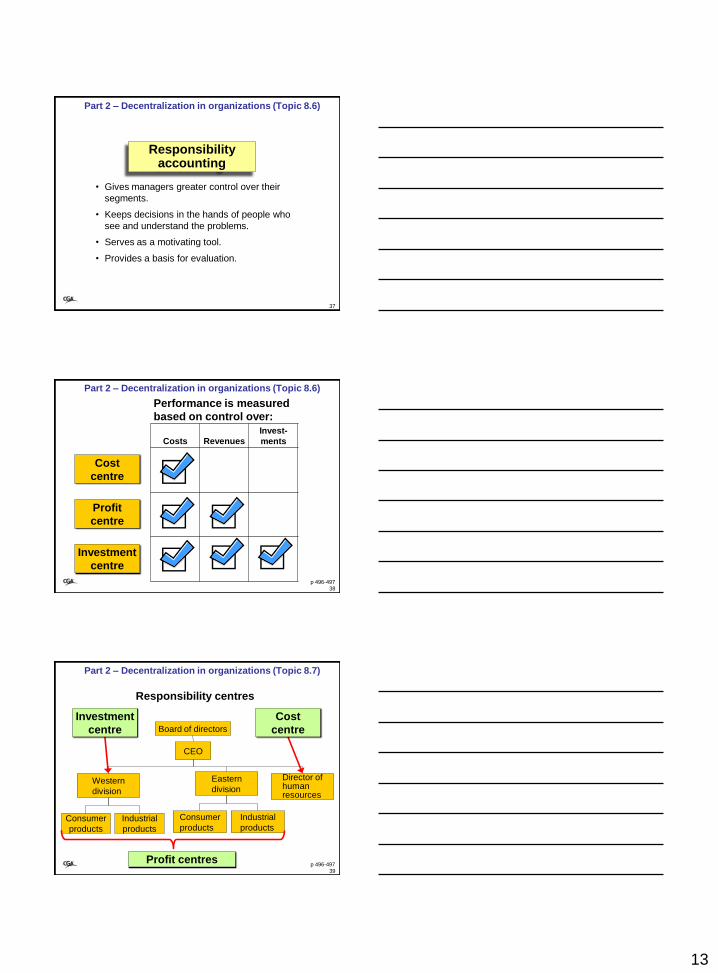

Part 2 – Decentralization in organizations (Topic 8.6)

Differentiate between cost centres, profit centres, and investment centres, and explain how performance is measured in each. (Level 2)

Board of directors

CEO

Western

division

Eastern

division

Director of human resources

Consumer

products

Industrial

products

Consumer

products

Industrial

products

DecentralizationDecision making is

spread throughout

the organization.

36p 496-497

13

Responsibility accounting

• Gives managers greater control over their

segments.

• Keeps decisions in the hands of people who

see and understand the problems.

• Serves as a motivating tool.

• Provides a basis for evaluation.

Part 2 – Decentralization in organizations (Topic 8.6)

37

Part 2 – Decentralization in organizations (Topic 8.6)

Performance is measured

based on control over:

Investment

centre

Cost

centre

Profit

centre

Costs Revenues

Invest-

ments

38p 496-497

Part 2 – Decentralization in organizations (Topic 8.7)

Board of directors

CEO

Western

division

Eastern

division

Director of human resources

Consumer

products

Industrial

products

Consumer

products

Industrial

products

Responsibility centres

Cost

centre

Profit centres

Investment

centre

39p 496-497

14

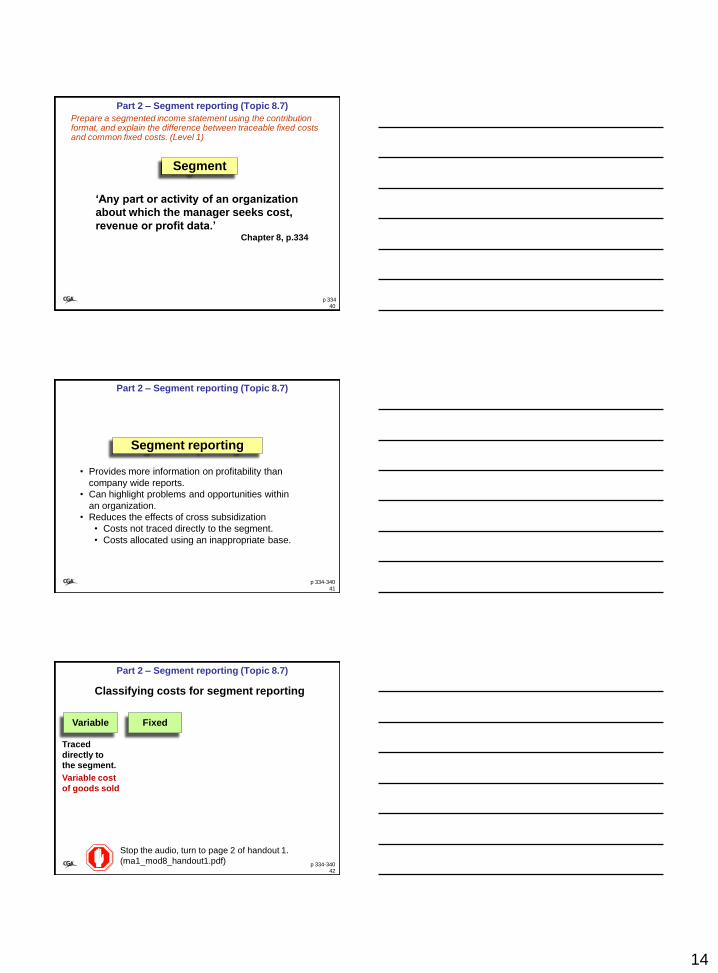

Segment

„Any part or activity of an organization

about which the manager seeks cost,

revenue or profit data.‟Chapter 8, p.334

Part 2 – Segment reporting (Topic 8.7)

40p 334

Prepare a segmented income statement using the contribution format, and explain the difference between traceable fixed costs and common fixed costs. (Level 1)

Part 2 – Segment reporting (Topic 8.7)

Segment reporting

• Provides more information on profitability than

company wide reports.

• Can highlight problems and opportunities within

an organization.

• Reduces the effects of cross subsidization

• Costs not traced directly to the segment.

• Costs allocated using an inappropriate base.

41p 334-340

Part 2 – Segment reporting (Topic 8.7)

Classifying costs for segment reporting

Traced

directly to

the segment.

Variable Fixed

Variable cost

of goods sold

Stop the audio, turn to page 2 of handout 1.

(ma1_mod8_handout1.pdf)42

p 334-340

15

Part 2 – Segment reporting (Topic 8.7)

Classifying costs for segment reporting

Traced

directly to

the segment.

Variable Fixed

Traceable Common

Supports more

than one segment

and not traceable

to any segment.

• Salary of the CEO

• Shared equipment

costs

Directly supports

the segment. Can

become common

as segments are

further divided.• Salary of the

segment manager.

43p 334-340

Part 2 – Segment reporting (Topic 8.7)

Classifying costs for segment reporting

Traced

directly to

the segment.

Variable Fixed

Common

Supports more

than one segment

and not traceable

to any segment.

Can be controlled

by the segment

manager.

CanNOT be

controlled by the

segment manager.

• Advertising for

that segment

• Depreciation of

plant facilities

Traceable

Discretionary Committed

44p 334-340

Part 2 – Segment reporting (Topic 8.7)

• Identifies what happens to profits as volume

changes.

• Useful for short run decisions such as temporary

uses of capacity. (chapter 12)

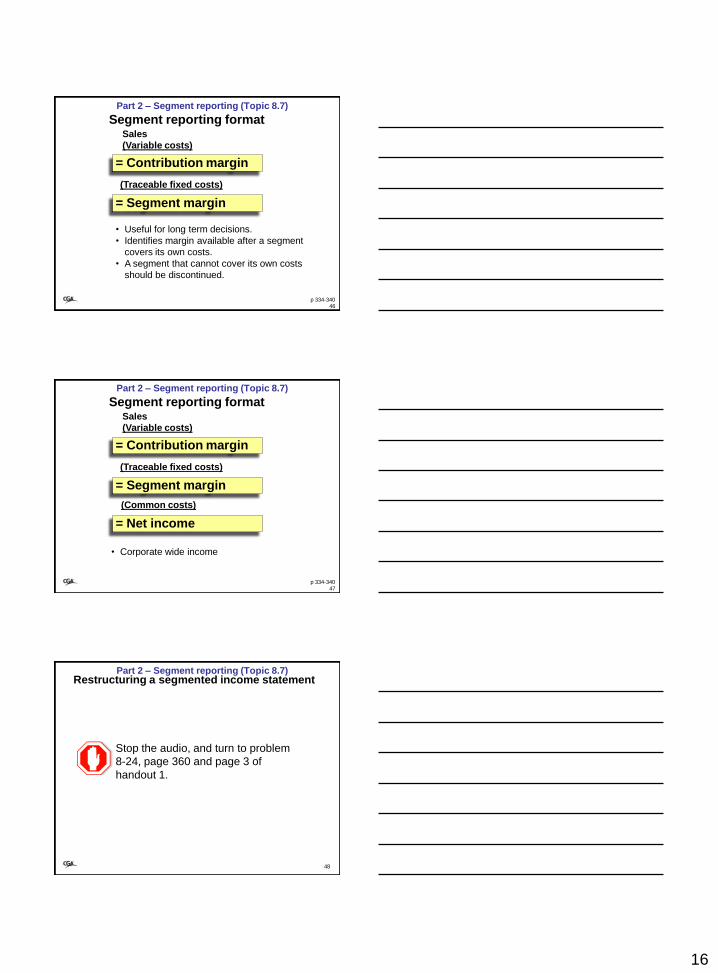

= Contribution margin

Sales

(Variable costs)

Segment reporting format

45p 334-340

16

Part 2 – Segment reporting (Topic 8.7)

• Useful for long term decisions.

• Identifies margin available after a segment

covers its own costs.

• A segment that cannot cover its own costs

should be discontinued.

= Contribution margin

Sales

(Variable costs)

(Traceable fixed costs)

= Segment margin

Segment reporting format

46p 334-340

Part 2 – Segment reporting (Topic 8.7)

= Contribution margin

Sales

(Variable costs)

(Traceable fixed costs)

= Segment margin

• Corporate wide income

Segment reporting format

= Net income

(Common costs)

47p 334-340

Part 2 – Segment reporting (Topic 8.7)

48

Restructuring a segmented income statement

Stop the audio, and turn to problem

8-24, page 360 and page 3 of

handout 1.

17

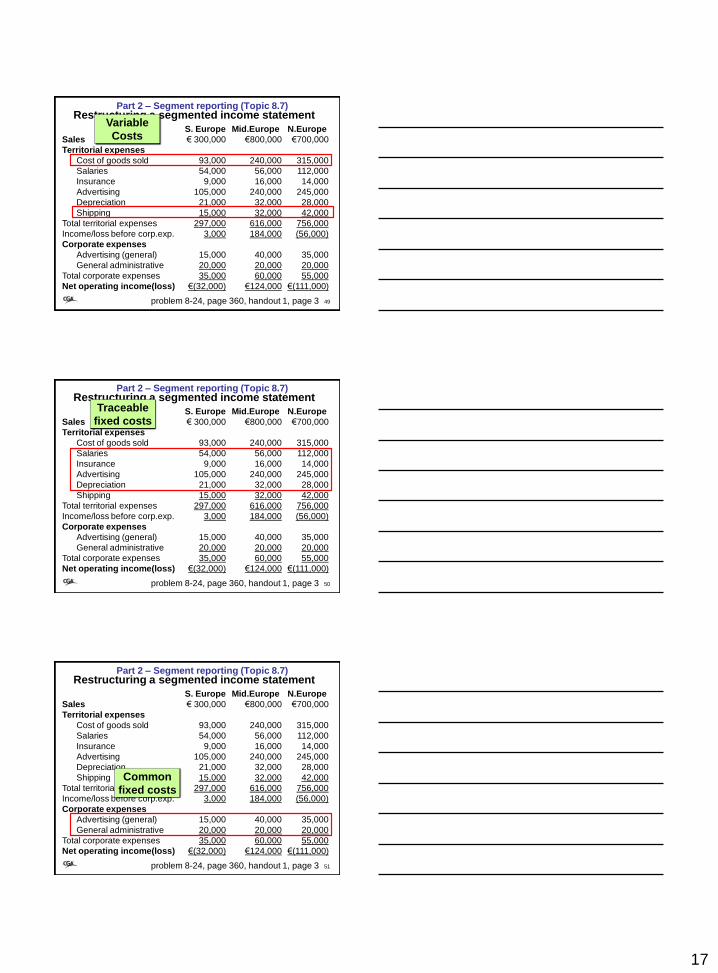

Part 2 – Segment reporting (Topic 8.7)

49

Restructuring a segmented income statement

S. Europe Mid.Europe N.Europe

Sales € 300,000 €800,000 €700,000

Territorial expenses

Cost of goods sold 93,000 240,000 315,000

Salaries 54,000 56,000 112,000

Insurance 9,000 16,000 14,000

Advertising 105,000 240,000 245,000

Depreciation 21,000 32,000 28,000

Shipping 15,000 32,000 42,000

Total territorial expenses 297,000 616,000 756,000

Income/loss before corp.exp. 3,000 184,000 (56,000)

Corporate expenses

Advertising (general) 15,000 40,000 35,000

General administrative 20,000 20,000 20,000

Total corporate expenses 35,000 60,000 55,000

Net operating income(loss) €(32,000) €124,000 €(111,000)

Variable

Costs

problem 8-24, page 360, handout 1, page 3

Part 2 – Segment reporting (Topic 8.7)

50

Restructuring a segmented income statement

S. Europe Mid.Europe N.Europe

Sales € 300,000 €800,000 €700,000

Territorial expenses

Cost of goods sold 93,000 240,000 315,000

Salaries 54,000 56,000 112,000

Insurance 9,000 16,000 14,000

Advertising 105,000 240,000 245,000

Depreciation 21,000 32,000 28,000

Shipping 15,000 32,000 42,000

Total territorial expenses 297,000 616,000 756,000

Income/loss before corp.exp. 3,000 184,000 (56,000)

Corporate expenses

Advertising (general) 15,000 40,000 35,000

General administrative 20,000 20,000 20,000

Total corporate expenses 35,000 60,000 55,000

Net operating income(loss) €(32,000) €124,000 €(111,000)

Traceable

fixed costs

problem 8-24, page 360, handout 1, page 3

Part 2 – Segment reporting (Topic 8.7)

51

Restructuring a segmented income statement

S. Europe Mid.Europe N.Europe

Sales € 300,000 €800,000 €700,000

Territorial expenses

Cost of goods sold 93,000 240,000 315,000

Salaries 54,000 56,000 112,000

Insurance 9,000 16,000 14,000

Advertising 105,000 240,000 245,000

Depreciation 21,000 32,000 28,000

Shipping 15,000 32,000 42,000

Total territorial expenses 297,000 616,000 756,000

Income/loss before corp.exp. 3,000 184,000 (56,000)

Corporate expenses

Advertising (general) 15,000 40,000 35,000

General administrative 20,000 20,000 20,000

Total corporate expenses 35,000 60,000 55,000

Net operating income(loss) €(32,000) €124,000 €(111,000)

Common

fixed costs

problem 8-24, page 360, handout 1, page 3

18

52

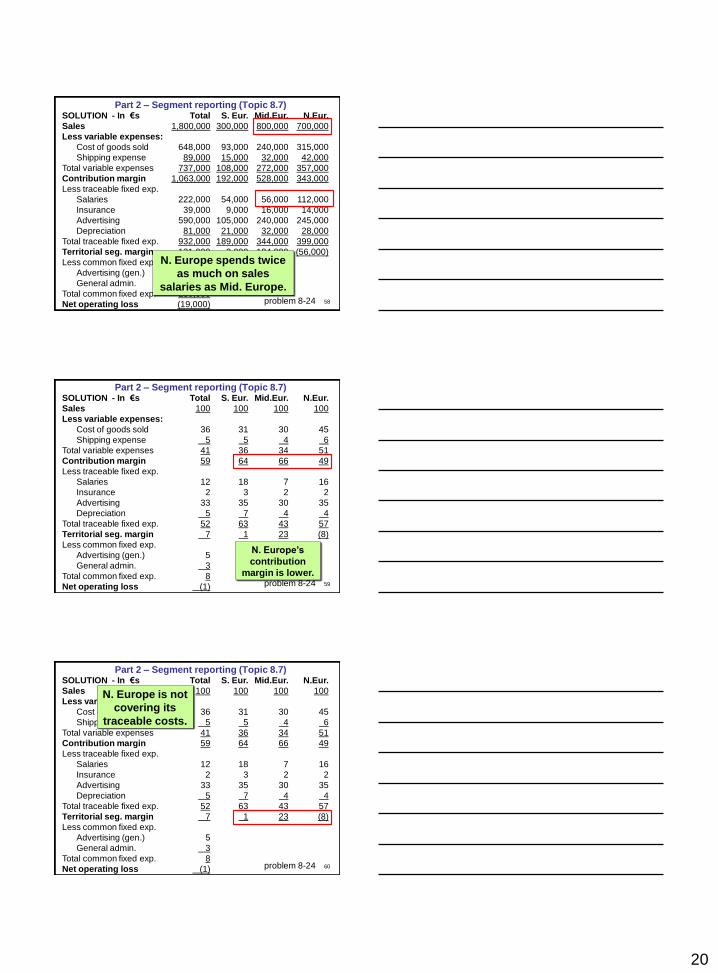

SOLUTION - In €s Total S. Eur. Mid.Eur. N.Eur.

Sales 1,800,000 300,000 800,000 700,000

Less variable expenses:

Cost of goods sold 648,000 93,000 240,000 315,000

Shipping expense 89,000 15,000 32,000 42,000

Total variable expenses 737,000 108,000 272,000 357,000

TOTAL 3,774,000 68,490U 3,842,490 448,290F 3,394,200

* rounded

78

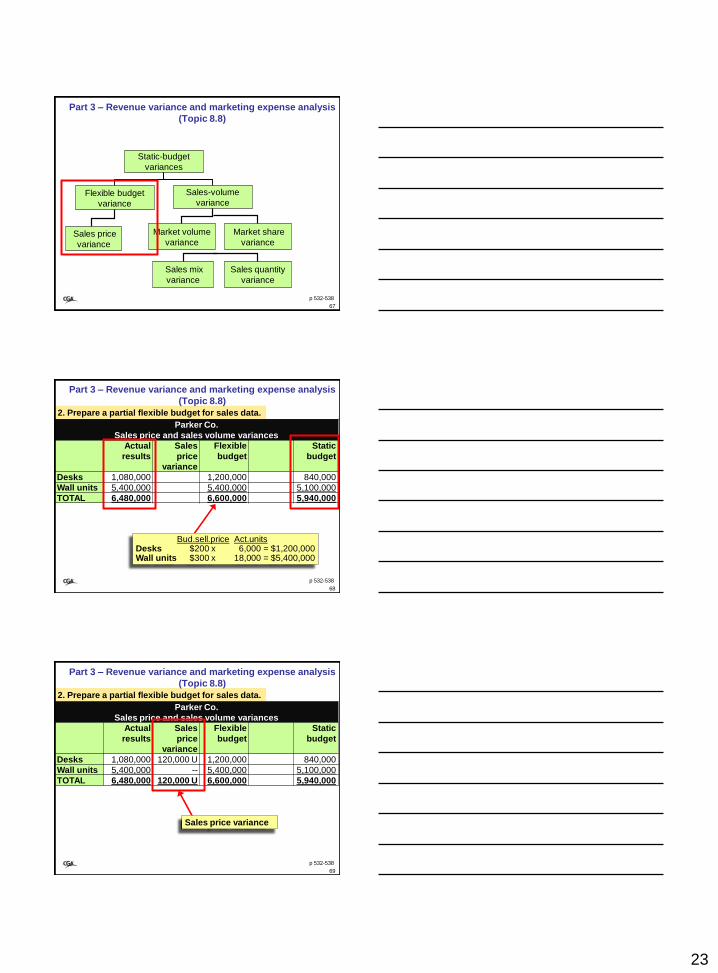

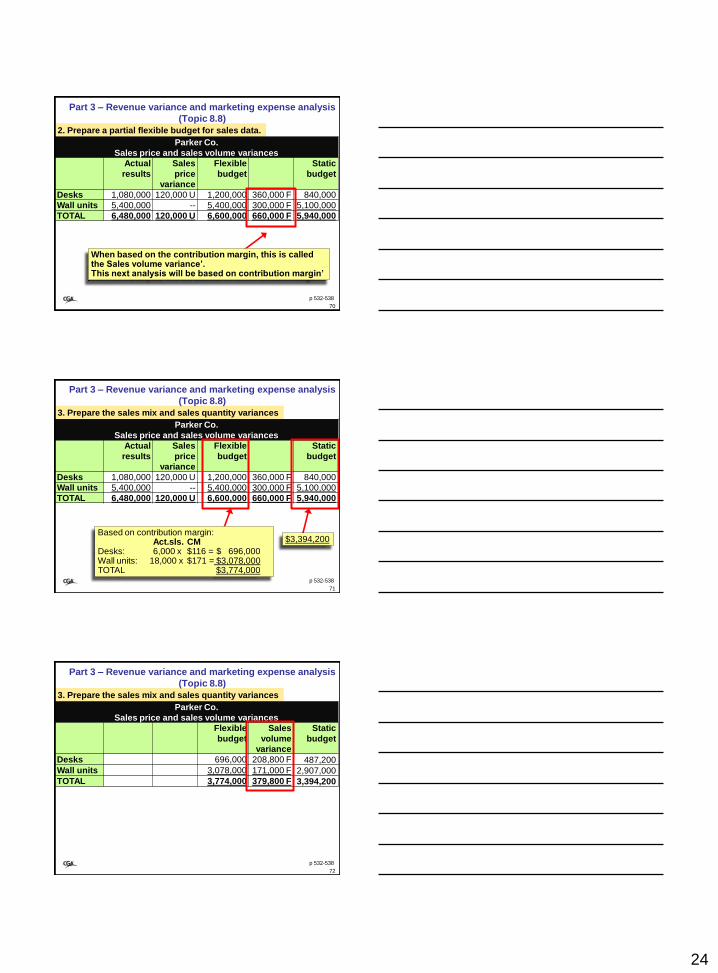

Part 3 – Revenue variance and marketing expense analysis

(Topic 8.8)

p 532-538

27

Static-budget

variances

Flexible budget

variance

Sales-volume

variance

Sales price

variance

Market volume

variance

Market share

variance

Sales mix

variance

Sales quantity

variance

79

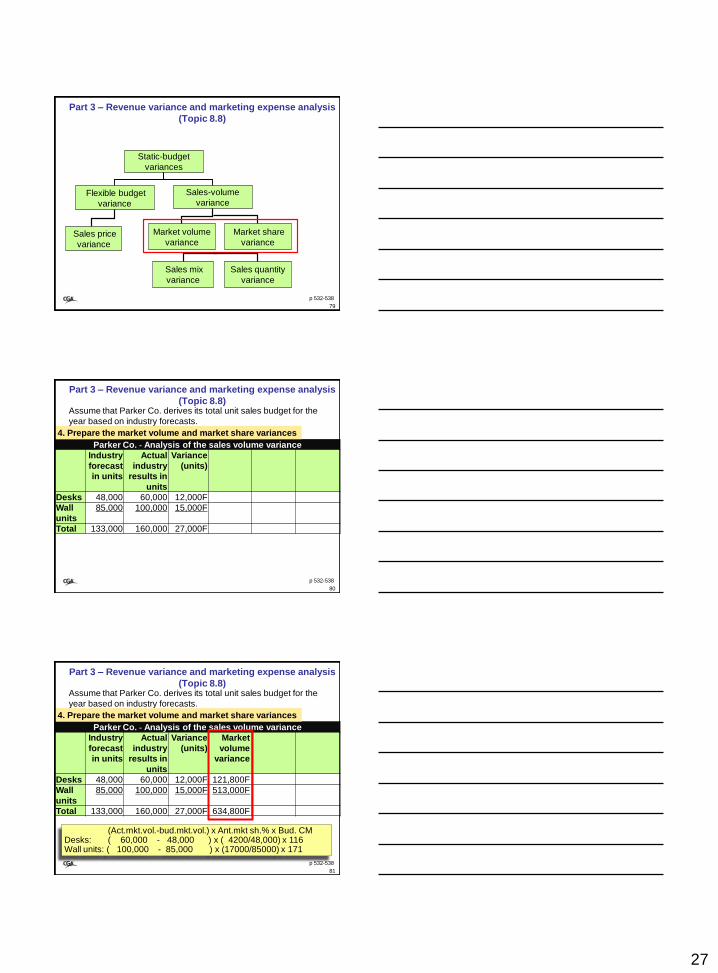

Part 3 – Revenue variance and marketing expense analysis

(Topic 8.8)

p 532-538

Assume that Parker Co. derives its total unit sales budget for the

year based on industry forecasts.

Parker Co. - Analysis of the sales volume variance

Industry

forecast

in units

Actual

industry

results in

units

Variance

(units)

Desks 48,000 60,000 12,000F

Wall

units

85,000 100,000 15,000F

Total 133,000 160,000 27,000F

4. Prepare the market volume and market share variances

80

Part 3 – Revenue variance and marketing expense analysis

(Topic 8.8)

p 532-538

Assume that Parker Co. derives its total unit sales budget for the

year based on industry forecasts.

Parker Co. - Analysis of the sales volume variance

Industry

forecast

in units

Actual

industry

results in

units

Variance

(units)

Market

volume

variance

Desks 48,000 60,000 12,000F 121,800F

Wall

units

85,000 100,000 15,000F 513,000F

Total 133,000 160,000 27,000F 634,800F

4. Prepare the market volume and market share variances

(Act.mkt.vol.-bud.mkt.vol.) x Ant.mkt sh.% x Bud. CMDesks: ( 60,000 - 48,000 ) x ( 4200/48,000) x 116Wall units: ( 100,000 - 85,000 ) x (17000/85000) x 171

81

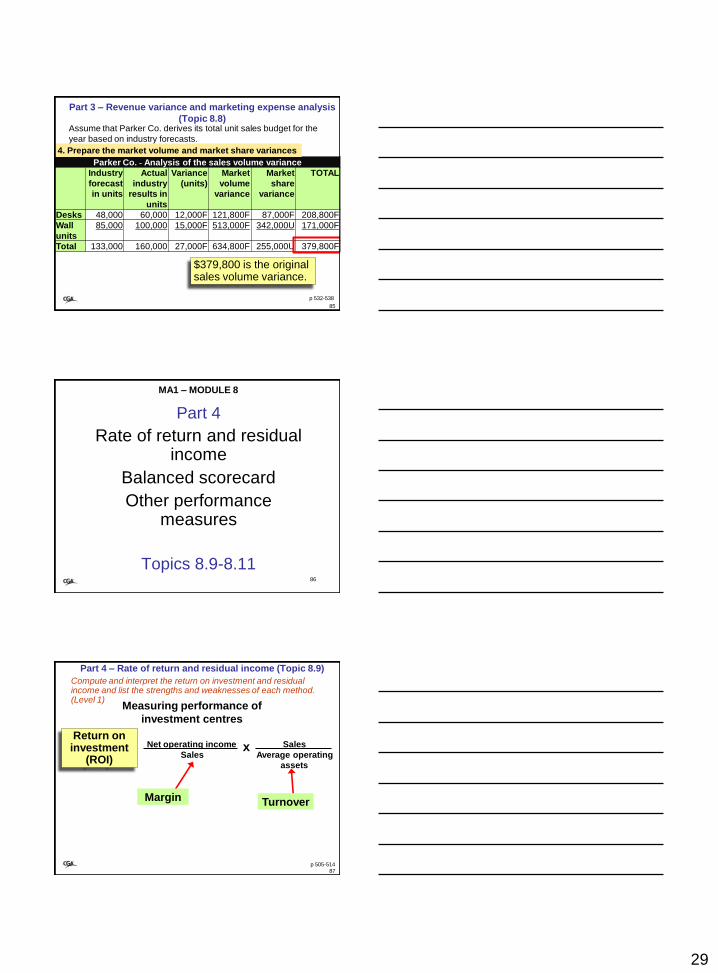

Part 3 – Revenue variance and marketing expense analysis

(Topic 8.8)

p 532-538

28

p 532-538

Assume that Parker Co. derives its total unit sales budget for the

year based on industry forecasts.

Parker Co. - Analysis of the sales volume variance

Industry

forecast

in units

Actual

industry

results in

units

Variance

(units)

Market

volume

variance

Desks 48,000 60,000 12,000F 121,800F

Wall

units

85,000 100,000 15,000F 513,000F

Total 133,000 160,000 27,000F 634,800F

4. Prepare the market volume and market share variances

82

• The total market size for desks has increased by 60,000-48,000=12,000 units

• Parker’s share of this is 8.75% (4200/48,000). That’s 1050 units• 1050 units x CM of $116 is $121,800 which means that Parker’s

share of the increase in the market size is $121,800.

Part 3 – Revenue variance and marketing expense analysis

(Topic 8.8)

Assume that Parker Co. derives its total unit sales budget for the

year based on industry forecasts.

Parker Co. - Analysis of the sales volume variance

Total 133,000 160,000 27,000F 634,800F 255,000U 379,800F

4. Prepare the market volume and market share variances

84

•Parker’s original forecast of 4200 units was 8.75% of the market. •At a market level of 60,000 units they should have sold (60,000x8.75%) 5,250 units to maintain their market share. •Instead they sold 6000 units. The increase of 750 units x $116 CM is $87,000 which is their increase in the share of the market for desks.

Part 3 – Revenue variance and marketing expense analysis

(Topic 8.8)

29

Assume that Parker Co. derives its total unit sales budget for the

year based on industry forecasts.

Parker Co. - Analysis of the sales volume variance