Management AccountingIssues in interpreting its nature and change

Cristiano Busco a,∗, Paolo Quattrone b, Angelo Riccaboni a

a Universita di Siena, Faculty of Economics, Piazza S. Francesco 7, Siena, Italyb Saıd Business School and Christ Church, University of Oxford, Park End Street, OX1 1HP Oxford, UK

Keywords: Management accounting; Change and stability; Nature of management accounting; Heteromogeneity

1. Introduction

“I definitely agree we need to improve our processes of integration within [MEGOC], we shallcommunicate better and engage more effectively in day-to-day operations . . . at present, despite thesix common strategic imperatives, each business line is a kingdom on its own, we know that . . .

However, I have heard we are introducing a new system called Balanced Scorecard that run withinthe SAP’s platform [MEGOC’s Enterprise Resource Planning system] and allows us to monitorthe achievement of our strategic imperatives along four different perspectives of analysis. Let’s seewhat it is like, and its impact on the job as I wouldn’t like to change my existing working practices

126 C. Busco et al. / Management Accounting Research 18 (2007) 125–149

because someone on the Board has fallen in love with the flavour of the month during a trainingcourse in London . . .” (Operating Manager).

Middle-East Gas and Oil Company (MEGOC) is a large corporation operating in the oil and gasindustry. The company is owned by the national government and the revenues generated constitute alarge part of the GDP of that country.1 In 2002, following a call from the government for companiesto take some action to improve the local economy and increase the revenue generated for the country,MEGOC’s executive management board redefined the strategic direction of the company “to significantlyincrease its contribution to the country’s revenue needs and [. . .] consistently promote the developmentof the local economy” (MEGOC’s mission statement).

One of the concerns evoked by MEGOC’s operating manager relates to whether change is good to haveor should be resisted. He also questions the novelty of the proposed new technical solution, the BalancedScorecard (BSC) in this case, asking whether it is the result of transitory fads and fashions or of moreprofound reflections on effective organizational needs for such a new system, and on its effects on thecorporation and its employees.

The quote reported above and the brief description which followed it are illustrative of many of thethemes that the literature on management accounting change has been addressing in these last few years,and that we also intend to recall and systematize in this paper, which opens the second ManagementAccounting Research Special Issue on Management Accounting Change.

In doing so we believe that the first building block of our systematizing effort concerns the issue ofwhat and who drives management accounting change and whether this is some hidden structural force,some clear individual agency, an opaque combination of the two or even something else. The operatingmanager rightly evokes ideals which are often mobilized for prompting change: ‘integration’ (see Buscoet al., 2006; Dechow and Mouritsen, 2005; Hansen and Mouritsen, 1999), various ‘imperatives’ andslogans (see Quattrone and Hopper, 2001, 2005, 2006), and so forth. Are these the drivers of change? Arethey the result of broader environmental, contextual and institutional forces (see, for instance, Baines andLangfield-Smith, 2003; Carmona et al., 1998) or the product of individual visions which are translatedinto the framing attempt of the Balanced Scorecard (see Bloomfield and Vurdubakis, 1997)?

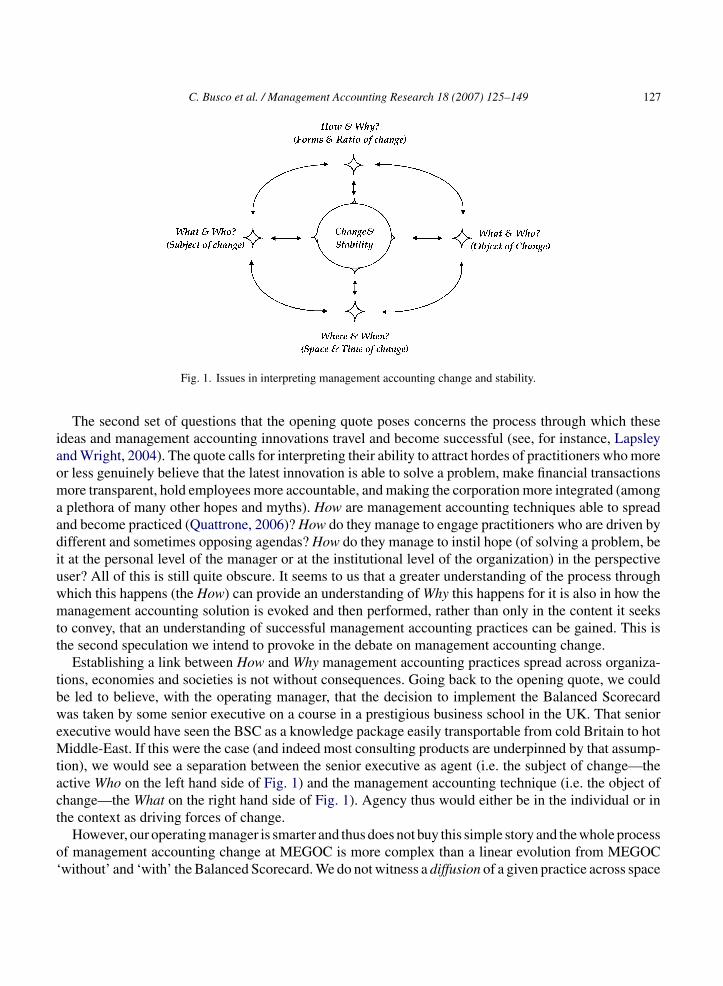

Addressing these issues and offering some material for reflection is the first building block of thesystematization we intend to offer in this piece (see Fig. 1).2

1 This is the disguised name of a company, the analysis of which will be used for illustrative purposes along the wholepaper. The insights from the MEGOC case are based on a longitudinal study conducted by one of the authors. From May 2003 toDecember 2005 we had the opportunity to collect empirical evidence through interviews, observations, participations in meetingsand internal workshops. Overall, we conducted 32 interviews with managers and employees operating in various Divisions ofMEGOC. The company is divided into seven major Divisions (or business lines): Exploration and Producing; Gas Operations;Refining, Marketing and International; Engineering and Operations Services; Law; Finance; and Industrial Relations. Thesebusiness lines are headed up by Corporate Heads at the Senior Vice President level, and all report to the President and CEO. Inaddition, support functions such as Corporate Planning, Information Technology, Human Resources and Management Services(where the internal consulting department is located) also report directly to the President and CEO of MEGOC.

2 This figure has been used by one of the authors in other papers (e.g. Quattrone and Hopper, 2001) but with different polesof interaction. What seems interesting though is that whatever issue one intends to study from a constructivist perspective, thisis always made of various concepts which appear as being in opposition and in need of being rethought under different terms.We begin in this paper by looking at issues of ‘agency’ in studying management accounting change, but this is done only forillustrative purposes and to follow the linearity of the paper for agency is indeed part also of the other poles constituting thefigure which are not sequential but all affecting issues of management accounting change.

C. Busco et al. / Management Accounting Research 18 (2007) 125–149 127

Fig. 1. Issues in interpreting management accounting change and stability.

The second set of questions that the opening quote poses concerns the process through which theseideas and management accounting innovations travel and become successful (see, for instance, Lapsleyand Wright, 2004). The quote calls for interpreting their ability to attract hordes of practitioners who moreor less genuinely believe that the latest innovation is able to solve a problem, make financial transactionsmore transparent, hold employees more accountable, and making the corporation more integrated (amonga plethora of many other hopes and myths). How are management accounting techniques able to spreadand become practiced (Quattrone, 2006)? How do they manage to engage practitioners who are driven bydifferent and sometimes opposing agendas? How do they manage to instil hope (of solving a problem, beit at the personal level of the manager or at the institutional level of the organization) in the perspectiveuser? All of this is still quite obscure. It seems to us that a greater understanding of the process throughwhich this happens (the How) can provide an understanding of Why this happens for it is also in how themanagement accounting solution is evoked and then performed, rather than only in the content it seeksto convey, that an understanding of successful management accounting practices can be gained. This isthe second speculation we intend to provoke in the debate on management accounting change.

Establishing a link between How and Why management accounting practices spread across organiza-tions, economies and societies is not without consequences. Going back to the opening quote, we couldbe led to believe, with the operating manager, that the decision to implement the Balanced Scorecardwas taken by some senior executive on a course in a prestigious business school in the UK. That seniorexecutive would have seen the BSC as a knowledge package easily transportable from cold Britain to hotMiddle-East. If this were the case (and indeed most consulting products are underpinned by that assump-tion), we would see a separation between the senior executive as agent (i.e. the subject of change—theactive Who on the left hand side of Fig. 1) and the management accounting technique (i.e. the object ofchange—the What on the right hand side of Fig. 1). Agency thus would either be in the individual or inthe context as driving forces of change.

However, our operating manager is smarter and thus does not buy this simple story and the whole processof management accounting change at MEGOC is more complex than a linear evolution from MEGOC‘without’ and ‘with’ the Balanced Scorecard. We do not witness a diffusion of a given practice across space

128 C. Busco et al. / Management Accounting Research 18 (2007) 125–149

and time, but its translation, i.e. a process by which the aim, nature and goal of the management accountinginnovations are constantly shifted, mediated and renegotiated: management accounting change alwaysentails a difference, a movement, a variation, in the nature of what is subject to change.3

If we were to think though that this translation stopped at some point in time (even for a nanosecond, seethe arguments in Quattrone and Hopper, 2006) we would be back to the issue of recognizing that we haveagents separated from the object of change. Thus, linking How management accounting changes (througha process of translation) to Why this happens implies a serious ontological question which concerns howto conceptualize the nature of management accounting, i.e. What is subject to (or object of) change.Indeed, the question can be also re-phrased in this way: if the process of translation necessarily needsto be thought as continuous, thus management accounting is never stabilized, for we would otherwisefall into a reification of subjects and object of change (with a clear move towards stabilization), howcan this constant movement be combined with the apparent stability of these managerial practices? Yet,assuming that management accounting innovations stabilize and gain a certain degree of functionalismwould limit the possibilities for these innovations to spread and diffuse. In other words, if budgeting isseen and theoretically conceived as something related to planning and operational control it would not beused (and theorized) as something instead related to organizational politics: its possibility of spreadingwill be limited and we would be editing a special issue on management accounting stability rather thanchange (see, on this matter, Granlund, 2001).

Indeed this is a theoretical conundrum for, on the one hand, Balanced Scorecard, Six-Sigma, ActivityBased Costing and the alike must appear quite concrete, stable, functional and homogeneous managementsolutions if they manage to mobilize millions of euros, dollars, pounds, etc., and if corporations are readyto invest considerable resources in consulting to have them implemented to the joy of consulting firms.On the other hand though, research shows how these are instead so fluid, unstable and heterogeneousthat it would appear miraculous to find the same management accounting technique implemented indifferent organizations in the same manner, with the same range of problems and implementation patterns.Furthermore, they rarely solve the problems for which they were initially mobilized. However, despite allof this, they are successful if by that one means that they manage to diffuse across the globe, industriesand sectors of the economy.

These questions, in our view, concern the nature of management accounting practices and systemsand thus call for a reflection on their nature, i.e. their ontology.4 Rather than looking for something‘else’, something which is contextual to the practice that is object of change or related to the actionof specific individuals (certainly legitimate paths of inquiry already successfully explored), we wantto reflect on a different level which may prove equally fruitful. It seems to us that in the very nature ofmanagement accounting (and of accounting tout court) there are already some elements for understandinghow accounting has the tendency to become what is not (Hopwood, 1987, p. 207). This thus prompts areflection on the What is object of change (and whether this relates in some way to the identity of thoseinvolved in the process of change, the Who; but we will debate this aspect later).

3 Latour defines it as follows: “A relation that does not transport causality but induces two mediators into co-existence” (2005).In accounting see the classic Robson (1991).

4 The definition of the term ‘ontology’ used in this paper is drawn from Laudan’s concept of “research tradition” (1977, pp.78–81) and from its etymological analysis. As is widely known, the etymology of the term ‘ontology’ (Chambers, 1989) derivesfrom the Greek on, ontos (present participle of einai, to be) and logos (discourse). Thus ontology is a discourse, a reflection onthe essence of various entities with no intention of reaching a concluding point.

C. Busco et al. / Management Accounting Research 18 (2007) 125–149 129

This leads to the fourth point of reflection we want to offer to the reader of this paper, that is, Whereand When this change happens (and who is there to observe it). The initial quote and the other illustrativeanecdotes we will use from the MEGOC experience are yet again insightful. What the operating manageris telling us is that change may happen in specific spatial and temporal niches, so it may have begunsomewhere but not somewhere else. It may have begun in the mind of the senior executive but not yetin the department he works in or even in the whole corporation (‘every division is a kingdom on itsown’). This will lead our reflection on a methodological plane. There the matter concerns those who areobserving processes of management accounting change and whether in understanding these processes itis important to observe the phenomenon or instead speculate on the theoretical development which suchobservation may inspires rather than drive.

What we have described may be a call, we will argue, to develop an understanding of the multiplicity ofthe nature of management accounting systems which makes them appear always different but inevitablythe same (Burns and Scapens, 2000, quoting Lanza Tomasi di Lampedusa’s The Leopard). And thusthe last set of issues we will address are those of Change and Stability and how this dichotomy can beovercome, i.e. how they may coexist and thus how these categories are somewhat useless and in need ofurgent replacement.

Before providing a more conventional introduction to the papers in this Special Issue (see Section 7),we will debate issues of management accounting change along the lines represented in Fig. 1 (Sections2–6). This will constitute the structure of the paper and the flow of the arguments; but we recognize thatthese matters are never sequential and always intrinsically related to each other.

In summary, this paper has grander aims than simply introducing the contributions in this special issue.However, we only aim to provide some possible directions for systematizing issues concerning change,in general, and management accounting change, in particular, and thus our contribution to the debate ismore methodological and systematic that content driven. This will hopefully help clarify the choice of thepapers included in this Issue and their contribution to the understanding of the process of managementaccounting systems change, as well as the gaps which are left open for further research and speculation.

In order to make these complex and abstract issues intelligible we have decided to use MEGOC as anillustrative case, to which we will refer throughout the reminder of the paper.

2. What and who makes change happen? Issues of agency, structure and interaction

The opening quote of MEGOC’s operating manager interestingly points out one important issue inunderstanding management accounting change: who/what is the agent in the process? Is change promptedby a serious matter concerning his/her job and the vision of the corporation or the result of a trendyfashion which will last as long as the life of a butterfly? Is it necessitated by the implementation of a newinformation or cameral technology?

When interpreting management accounting change, one of the key issues that scholars have to addressseems to concern where to locate the agency prompting the whole process. In this respect, for instance,change factors have been identified in individuals, be these a human actor (e.g. a rational accountant whoidentifies a calculative issue normally addressed with ‘better’ systems, as is the case of our MEGOCoperating manager or the character of Johnson and Kaplan’s plot, 1987) or a non-human actant (e.g.the irruption of a new IT system entailing a need for a new accounting system as part of a broaderorganizational change, cf. Granlund and Malmi, 2002). Some other works have instead sought to identify

130 C. Busco et al. / Management Accounting Research 18 (2007) 125–149

these prompting factors in broader contextual issues, related to certain institutional pressures, politicaldecisions economic imperatives, and some combination of them (e.g. Hopper and Powell, 1985; Carmonaet al., 1998).

The irruption of Giddens’ Structuration Theory in the management accounting literature (e.g. Burnsand Scapens, 2000; Busco et al., 2006; Macintosh and Scapens, 1990; Modell, 2003; Scapens, 1994) hascertainly sought to overcome this dichotomy. Several works have searched for more complex interactionsbetween management accounting systems and organizational, institutional and contextual factors. In thisrespect, for instance, Burns and Scapens (2000) have argued that the incomplete isomorphism betweenmanagement accounting systems as rules (i.e. stable but inanimate templates) and as routines (i.e. concretepractices which evolve over time) is what enable the link between the institutional context and the realmof actions. Management accounting systems are thus, and at the same time, rules, routines and roles(i.e. the network of organizational positions) which change in the constant interaction between contextualfactors and human actions (see also Busco et al., 2006; Lukka, 2007). They embed norms and institutionalfactors which are mediated by human actions through routines.5

Analogously, the wave of studies inspired by Actor-Network Theory (e.g. Chua, 1995; Briers and Chua,2001; Dechow and Mouritsen, 2005; Jones and Dugdale, 2002; Robson, 1991, 1992) has been partiallydriven by similar desires to overcome dichotomies between structure and agency which are exemplifiedin Latour’s call (2005) for a ‘flat sociology’, where, in solving the problems of the social, the notion ofcontext must be abandoned or, at least, reformulated in ‘flatter terms’.

Within MEGOC, the national imperative for ‘making the company a strategy focussed organization’(see Kaplan and Norton, 2001, 2004) was eventually translated into six imperatives to be followed bythe whole corporation: (1) Transform Corporate Performance; (2) Optimize the Corporate Portfolio; (3)Maximize Revenues by Capturing Oil Growth Opportunities; (4) Protect the Future Market for Oil; (5)Leverage the Oil and Gas Resources to expand the National Economy; and (6) Prepare the Workforce forthe Future. Once these were defined, several divisions and departments of MEGOC began the implemen-tation of the BSC. Ideals such as performance, optimization, maximization and the like, are somethingone cannot be against (Hansen and Mouritsen, 1999) for they present an appeal which is difficult to resistand thus they do seem ‘imperatives’ no one can oppose.

What makes management accounting an interesting locus to speculate on issues of agency in changeprocesses is exemplified in the MEGOC case by the conspicuous lack of understanding and ignorance ofthe content, key features and function of the BSC in the company. People referred to these ideals and tothe BSC without having a clear idea of what they were. Yet, the extent to which its deployment (or betterthe deployment of the multiple scorecards) had fostered organizational integration within MEGOC was(and still is) questionable before, during and after the implementation. Even at the end of the processof deployment, the BSC failed to achieve what it was supposed to deliver, i.e. a greater integration.

5 Similar problems have been addressed in the Information Systems literature where, for instance, the notion of ‘technologyin practice’ (Orlikowski, 2000) has viewed technologies as enactments of given structures in order to see them not as ‘systems’out there, i.e. external or independent of human agency, but as the result of the interaction between structure and agency,which does allow the change of the IT artifact in directions which are not predetermined. However, if “people’s situatedand recurrent use of a technology simultaneously enact multiple structures along with a technology-in-practice” (Orlikowski,2000, p. 411) then the heuristic value of the notion of ‘structure’ is questionable (cf. Thompson, 1989; Giddens, 1989) giventhat there are as many technologies-in-practice as people enacting the structure (as Fig. 2 in Orlikowski, 2000, suggests). Asimilar argument can be made for Barley and Tolbert (1997). This argument is explored in greater details in Quattrone andHopper (2006).

C. Busco et al. / Management Accounting Research 18 (2007) 125–149 131

Integration, as much as the BSC, was constantly referred to and evoked but always absent, never achievedand always in the making. However, and paradoxically, this constant failure and continuous unstablesituation made these ideals and the BSC ever present.

The illustration which follows may clarify the point. The ability of the BSC to be present in workingrelationships, although being absent ‘in practice’, is well illustrated by the way in which it engaged withthe Finance division of MEGOC. The BSC was generally perceived within the Finance organization asan ‘operational tool’ (“it was invented by an engineer [Kaplan], wasn’t it?” commented a managementaccountant), which some business lines were eventually implementing—supervised by the CorporatePlanning area. Although the average awareness on the BSC features was probably higher than in otherdivisions, within the Finance organization it was interpreted as a non-core initiative and, most importantly,often perceived as potentially disrupting for existing working practices. Talking to Finance experts theimpression was that there were more important and valuable things to care about. A senior accountantstated:

“I know some business lines are implementing the Balanced Scorecard with the help of CorporatePlanning or external consultants, but we do not get involved with that, we don’t even have our ownscorecard at present . . . Ultimately, what is the linkage between the scorecard and the budget? Ido not see it, yet. Here we do not flex the budget: once it is finalized, that’s it (!) . . . so we betterconcentrate on that, as well as on the accountability reviews. Indeed, you can say we focus on oneperspective [financial], and we are happy to leave the other three to the rest of the company (!)”.

Significantly, also the way in which MEGOC came across the BSC was an object of speculation andstory telling (see the quote in the prologue). Several managers within MEGOC knew the BSC (or someBSCs) was (were) there in the organization but they could not fully explain its (their) origins, and reasonsfor implementation. Frequently, managers ended up discussing advantages and disadvantages of the BSCin its absence, i.e. they speculated around the ideal of ‘translating strategy into action’ but the BSC wasnot yet a working technology with a clear identity and features for them—although this may have alreadyoccurred within other corners of MEGOC (see Quattrone and Hopper, 2006 for a similar situation withreference to information technologies). People referred to the BSC in its absence.

However, despite this hetaerae nature, its lack of clarity and (paradoxically) possibly because the wholeidea was fuzzy and obscure, the BSC was able to gain organization-wide visibility by mobilizing networksof relations with users and other organizational information systems.

This posits an interesting question in terms of agency for something which is perceived as potentiallyabsent and surely obscure, something which is always different from itself when observed in differentorganizational settings, but manages to spread and become present. So what is the driver of change andwho is eventually there to prompt and steer it? And, if the BSC is so evanescent, the questions to be asked,as is argued later in the paper, are: how and why does change happen? what is subject to it and who? andwhere and when does it happen?

A popular quote from Latour may provide some interesting insights on these issues. He asks whether:

“you can, with a straight face, [keep] . . . hitting a nail with and without a hammer, boiling waterwith and without a kettle, fetching provisions with or without a basket, walking in the street withand without your clothes, zapping a TV set with or without a command, slowing down a car withor without a speed-bump, keep track of your inventory without a list, run your company with orwithout book-keeping . . .” (2005, p. 71).

132 C. Busco et al. / Management Accounting Research 18 (2007) 125–149

This quote tells us a few things. The first of these is that every agent is an actor-network (see Latour,2005) for her or his agency is diffused and not stably located in a centre from which change is thoughtto be prompted. The second is that the nature of what is subject of, and to, change is also diffused.If the actor is conceived as an actor-network then agency and an object’s identity do not reside eitherin an individual or in an object but in a chain of relations. We enter into the realm of what Law andSingleton (2005) calls a ‘semiotic ontology’ where the nature of a thing is made in nests of references,in patterns of absences and presences. Everything is much more complex than a linear view of changepresupposes and implies. This view would conceive, say, MEGOC without the BSC at a certain pointin time and with it at a later point in time (see Quattrone and Hopper, 2001 and Andon et al., 2007,for an extended discussion of the problematic notion of linear change), with the clear corollary thateverything would be clearly identifiable: agencies, rationales for change, objects and subject of change andso forth.

This point is quite fundamental with respect to a theory of change, a theoretical framework which aimsto explain change rather than stability, stabilization and finite institutionalization, and it can be illustratedfurther with another example. Think of a criminal organization such as the Mafia (as the three authors ofthis paper are Italian we are possibly the only ones allowed to use this example without being criticized aspolitically incorrect!). If one assumes that this superstructure exists then there is little room for resistance.The matter is very simple: who resists is killed. End of story. But if one assumes that Mafia does notexist6 then change is at least thinkable.

We thus face an interesting paradox: if one assumes a linear view of space and time in which changehappens, for instance, as an interaction between structure (e.g. Mafia) and agency (e.g. those who fight it),then we are theorizing stability or, at best, a process of institutionalization which leads to the replicationof the status quo. If one assumes that the agents and the entities subject to change are definite, thereis little room for thinking about change: change, in these conditions, is not thinkable and thus it is notpossible. There is no progress and only conservatism. There is no theory of change but only of stability,stabilization and equilibrium.

Thus, interpreting the nature and change of management accounting cannot rely on notions of structureand agency as explaining factors because if one assumes their finite existence this only explains tendenciestowards stability. Notions of structure and agency are, thus, the problems rather than the solution toproblems of management accounting change: change is thinkable only if there is a gap within and betweenthese two entities. Without gaps, without this lack of isomorphism, without some kind of contradiction(see Nor-Aziah and Scapens, 2007), without some kind of incompleteness in the interpretation of thenature of management accounting (see Quattrone, 2000, 2006) there is no room for change: changecannot even be thought. Change requires an absence, a lacuna which can be mobilized and which canmobilize. This is why, in the MEGOC case, it is not surprising that the BSC was often referred to in itsabsence.

How and Why this happens, how it is that an absence is able to mobilize and become presence; howthese absences are partially filled with meanings, rationales, agencies and so forth; is the theme of thefollowing section where it is argued that understanding these Hows sheds new light on understanding theWhys; i.e. the rationales underpinning the diffused agency.

6 Indeed the etymology of the term may come from the Arab maffia, which means ‘it does not exist’. We are grateful to RihabKhalifa for reassuring us of the etymological analysis.

C. Busco et al. / Management Accounting Research 18 (2007) 125–149 133

3. How and why change happens? The translation of management accounting as a communaleffort

In this section we want to link issues of agency in management accounting change, which werehighlighted above, with those of process (discussed this section) and its nature (discussed in the nextsection). If agency is diffused across a nest of relationships then how change happens is probably also inneed of rethinking and, arguably, rationales for management accounting change can equally be rethoughtas more fluid, multiple and multifaceted.7 Once again, we will use, in even greater scale, material fromthe MEGOC case, as this will help make these abstract claims more intelligible.

As normally happens with the deployment of any managerial innovation, the implementation of BSCwithin MEGOC was not easy. Scepticism was mounting in some parts of MEGOC, and this suggested oneof the divisions that pioneered the BSC implementation (Engineering & Operations Services—E&OS)to stimulate an internal debate on strategy by relying on the BSC jargon and metrics.

In 2004, some of the key customers of the division and several delegates from other business areas anddivisions of MEGOC gathered together with a large number of E&OS employees for a meeting calledthe Cafe.8 Few months after the E&OS cafe, a member of E&OS BSC team stated:

“What we did in our 2004 cafe was to illustrate the way in which the business line is attempting toalign its strategies and initiatives with corporate level strategic imperatives. Using the strategy mapas a guide, we relied on the BSC to describe the division’s objectives and the specific initiativesthat were about to be undertaken over the business plan period. The strategy map builds from ourmission statement – the reason we exist as an organization – which is to add value to [MEGOC]through the innovative solutions developed by our people”.

As the interview with the member of E&OS BSC team was progressing, he increasingly relied on theBSC rhetoric and visual aids to clarify his story:

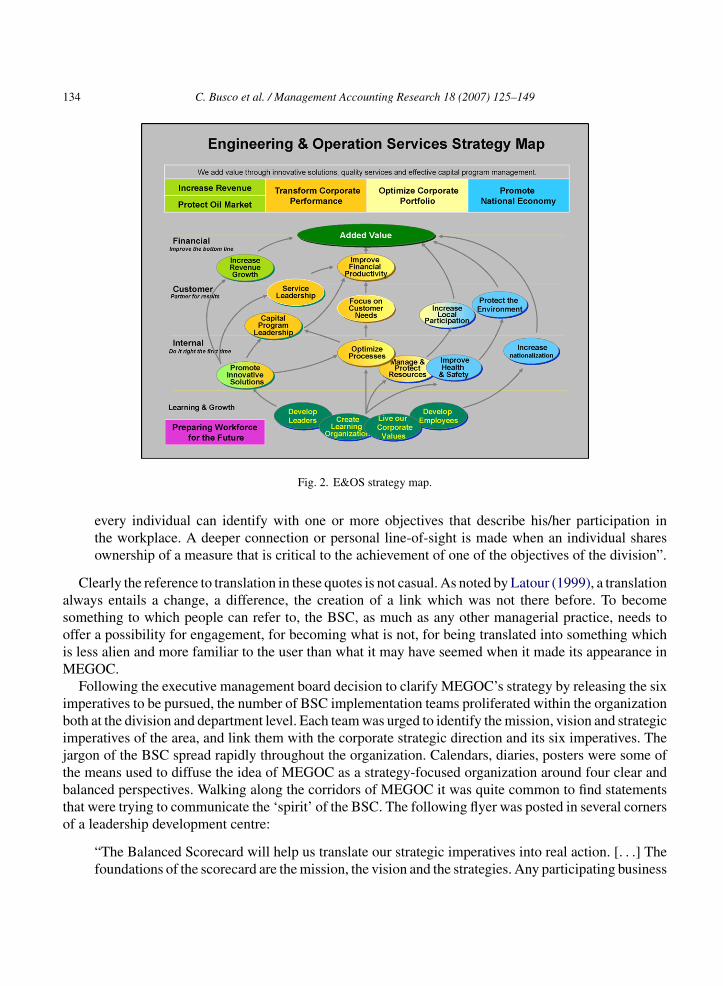

“as you can see [pointing at a chart on the training room—see Fig. 2], our key goal is to focus oncustomers needs. [. . .]. Like a good strategy for a winning soccer club, our strategy map is strongup the middle: goalie – midfielder – centre forward. Therefore we have these nine objectives [again,pointing at the chart] locked within cause and effect relationships with the aim to improve produc-tivity and achieve ‘best-in-class’ performance. Then, there are seven more supporting objectives toachieve increased revenue growth, to protect the oil market, to optimize the Corporate portfolio, andto support the national economy. Altogether these sixteen objectives complete the high-level viewof the strategy map of the division”.

And again:

“These are the objectives that were highlighted in the 2003 E&OS Operating Plan presentation.Horizontally the objectives are organized according to the four balanced scorecard perspectives;vertically they are organized by strategic imperatives. Like any good map, it has coordinates forboth longitude and latitude (!). [. . .] Strategy begins to be effectively translated into action when

7 This will also relate to the lack of clear starting and ending points, something which relates to space and time issues asdiscussed in Section 6.

8 Significantly, 680 out of 8650 employees of E&OS attended the meeting. Additionally, another 230 managers and employeesjoined the 2004 cafe from other business lines of MEGOC, as well as representatives from key customers of the company.

134 C. Busco et al. / Management Accounting Research 18 (2007) 125–149

Fig. 2. E&OS strategy map.

every individual can identify with one or more objectives that describe his/her participation inthe workplace. A deeper connection or personal line-of-sight is made when an individual sharesownership of a measure that is critical to the achievement of one of the objectives of the division”.

Clearly the reference to translation in these quotes is not casual. As noted by Latour (1999), a translationalways entails a change, a difference, the creation of a link which was not there before. To becomesomething to which people can refer to, the BSC, as much as any other managerial practice, needs tooffer a possibility for engagement, for becoming what is not, for being translated into something whichis less alien and more familiar to the user than what it may have seemed when it made its appearance inMEGOC.

Following the executive management board decision to clarify MEGOC’s strategy by releasing the siximperatives to be pursued, the number of BSC implementation teams proliferated within the organizationboth at the division and department level. Each team was urged to identify the mission, vision and strategicimperatives of the area, and link them with the corporate strategic direction and its six imperatives. Thejargon of the BSC spread rapidly throughout the organization. Calendars, diaries, posters were some ofthe means used to diffuse the idea of MEGOC as a strategy-focused organization around four clear andbalanced perspectives. Walking along the corridors of MEGOC it was quite common to find statementsthat were trying to communicate the ‘spirit’ of the BSC. The following flyer was posted in several cornersof a leadership development centre:

“The Balanced Scorecard will help us translate our strategic imperatives into real action. [. . .] Thefoundations of the scorecard are the mission, the vision and the strategies. Any participating business

C. Busco et al. / Management Accounting Research 18 (2007) 125–149 135

line develops a Strategy Map that describes the way in which objectives are linked in line with thestrategic imperatives. It helps us understand our strategy by looking at it from four perspectives:Financial, Customer, Internal Business, and Learning and Growth. It provides a snapshot of the wayin which activities are linked to and support each other. By studying this map, you will be able toidentify where you fit into the company’s plan for realizing its vision”.

In fact, without entering into detailed and exhaustive representations of all the possible actions andconstructions that the BSC can enable, its simplicity was ‘marketed’ to offer a space to practice thetechnique and to make it suitable for everybody’s need. Managers at E&OS were not trying make every-thing clear and rigid, and they were not forcing anybody ‘to fall in love with the initiative of the month’.Rather, they were trying to engage potential future users who could eventually come to see the BSC asan opportunity for action. Thus, happenings such as the E&OS 2004 cafe and the workshop we attendedseemed to contribute to the diffusion of the BSC in a manner which is visually and methodologicallyengaging (see Quattrone, 2006). In this context, it is worth mentioning the way in which the member ofE&OS BSC team ended the workshop:

“. . . and now it is up to you, and your department leaders to find the proper objectives and measuresto make sure you can orient yourselves on the [MEGOC] strategic map, and show how you can addvalue along these longitude and latitude [while pointing at a chart reproduced on Fig. 3]”.

What we seemed to be witnessing in this recursive process of defining mission, vision and strategy isthe possibility of creating forms, links, objects and subjects of accountability. The form of the BalancedScorecard and how it seems to be offering space and time for its utilization (the How of management

Fig. 3. MEGOC’s “road ahead to achieve a better tomorrow”

136 C. Busco et al. / Management Accounting Research 18 (2007) 125–149

accounting change) becomes thus intertwined with the reason it is considered suitable for each organi-zational unit and individual within the organization (the Why). As illustrated by Alvesson and Willmott,2002, presenting the BSC as something which empowers offers the possibility of collectively definingthe identity of each organizational unit (see also Ezzamel et al., 2004). What we have here is the BSC’sability to enrol users because, by using the BSC, they are defining what and where they are, and whatrelationships they have with the other units in the organization. The BSC becomes a heuristic device;a learning machine (Hopwood, 1980) which is appropriated by managers for various reasons and aims.This introduces the following aspects we intend to speculate on in interpreting management accountingchange: What and Who is subject to change?

4. What and who is changing? From an epistemological to an ontological problem of change

In the MEGOC case, the BSC seems to be assuming an almost infinite set of features while failingto deliver integration and allowing each division to be a ‘kingdom on its own’. And still the BSC is outthere as an apparently coherent practice which people refer to and it is able to mobilize actions, as wehave already argued. Management accounting seems to be less than a real artifact (for it can theoreticallyassume infinite forms and never constrains entirely) but it is more than a mere social construction (for isnot malleable ad infinitum and it allows things to be done in certain ways and not others). It is only inthis space ‘in between’, the ‘real’ and the ‘constructed’ that a speculation on the nature of managementaccounting can take place.

This theoretical conundrum resembles what the contributions hosted in a recent special issue ofOrganization (2005) had to face in theorizing ‘objects’. As Law and Singleton (2005) noted in thatspecial issue, the strategy that scholars may follow to study the ‘strange objects’, i.e. strange artifactswhich do not easily fall within standard categories, may be two-fold. On the one hand, the difficulty inunderstanding their nature and evolution can be attributed to the observer. In this case, the complexity ofunderstanding the object can be termed ‘epistemological’ for the object simply means different things todifferent people and constitutes a means to establish communication between different communities ofpractices (see also Burns and Vaivio, 2001).

On the other hand, scholars may follow what Law and Singleton (2005) have termed an ‘ontologicalstrategy’, i.e. objects are complex per se not (only) because people interpret them differently. This onto-logical approach has been followed by a series of works in the area of Science and Technology Studies(STS) and Actor-Network Theory (ANT, e.g. Dugdale, 1999; de Laet and Mol, 2000; Mol, 1999). Inthe case of IT, for instance, Quattrone and Hopper (2006), have addressed the question of ‘What is IT?’,by exploring how a software best seller (SAP) paradoxically established its presence in a multinationalorganization by being absent as working technology in that corporation. The homogeneity of this systemwas not the result of a process of isomorphic adherence to a template or a set of rules but it was possiblethanks to the presence of a space offered by the IT system to experiment, mediate and thus attract diversity.The object assumed an identity (albeit unstable and precarious) because it attracted rather than reduceddiversity and difference. IT appeared homogeneous because it was heterogeneous in nature: hence theterm heteromogeneous.

Similarly, within MEGOC, the BSC has established its presence organization-wide by being absent asa working technology in several divisions and departments—such as the Finance organization and others.However, despite not using the technique, the majority of the people within these areas did engage with

C. Busco et al. / Management Accounting Research 18 (2007) 125–149 137

the BSC, although in its absence (“Indeed, you can say we focus on one perspective [financial], and weare happy to leave the other three to the rest of the company (!)”—[as cited earlier]). Eventually, it is thesimplicity entailed by the four perspectives of the BSC as well as the visual clarity of the strategy mapthat made such techniques performable within MEGOC. The BSC is performable not because it forcesusers in certain directions, but because it leaves the potential adopters free to enact the space which isoffered within it (“. . . and now it is up to you, and to your department leaders to find the proper objectivesand measures to make sure you can orient yourselves on the [MEGOC] strategic map, and show howyou can add value along these longitude and latitude”—as cited earlier). Eventually, it could be said thatdespite being developed under the umbrella (and the rhetoric) of the six corporate strategic imperativesthe BSC has made it possible to preserve each division of MEGOC as a ‘kingdom on its own’.

Thus, the ontology of the BSC is not clearly defined, but it is multiple and multifaceted. Despitethe metaphor of a map, which offers longitude and latitudes for objects to be classified univocally, theBSC does not easily fit within conventional spatiotemporal co-ordinates. For example, the BSC wasable ‘to attract’ divisions such as Human Resources and Information Technology for reasons that werequite different from E&OS or other functions (including Finance, where the ‘potential’ of the BSC wasre-discovered in a second stage—see the remaining paragraphs of this section).

Human Resources and Information Technology were among the first divisions to pioneer the BSCwithin MEGOC. Managers within these two areas were attracted by the opportunity to increase theirvisibility within the company as human capital and Enterprise Resource Planning systems were aboutto acquire greater importance through the logic of the BSC. Interestingly, the rhetoric of the BSC wasalso used to downplay the relevance of well-established accounting-driven practices within MEGOC,such as the budget and variance analysis. The following is the remark of an IT manager responsible fora knowledge management program labelled ‘shared values’:

“. . . although our crude [oil] and natural gas are invaluable assets, in today’s turbulent competitiveenvironment, [MEGOC] must compete not only through its physical resources, but also through itsintellectual and knowledge capital. Employees’ capabilities and motivation, information technol-ogy, customer relationships and quality improvements represent the main ground to improve ourcontribution to the Government and the community. In this context, the annual budget exercise is notsufficient anymore to manage effectively such heterogeneous resources at work. Financial metricsalone are inadequate to drive the organization when so much of the value creation comes fromthings other than inventory, plant or equipment. You teach us [pointing at one of the researchersconducting the interview] this has historically been the focus of companies’ financial statements,which in actual fact are not able to capture the value of intangible assets, yet”.

In line with the overall call of this paper for multiplicity and fluidity, it is also interesting to linkontological issues concerning What changes to those who are involved in this change. However, this timethe focus is less on the active role of the subject and more on the effects on individuals of managementaccounting change, i.e. a focus on Who is subject to change. This calls for a speculation on how thediffused agency and ontology of management accounting that we are debating in this paper also hasan effect on people and the way in which they see themselves when in interaction with these powerfulheteromogeneous objects.

At the beginning of 2005, the ideal of better integration among the different divisions of MEGOC wasstill on top of the agenda. Interestingly, given the original hostility to the BSC in the first stages of the BSCdeployment in the company, the Finance organization displayed an active role in fostering cooperation

138 C. Busco et al. / Management Accounting Research 18 (2007) 125–149

and knowledge sharing across the company by developing a series of workshops tailored to illustrate theimportance of relying on financial metrics and on Finance experts for achieving effective organizationalintegration. In doing so, the Finance organization decided to open “the door to other divisions to describethe way we can add-value to [MEGOC’s] operations, and contribute to the execution of the company’soverall strategic imperatives” (Finance manager). Several managers within Finance increasingly realizedthat the function needed a boost to “regain relevance within the company”. We had the opportunity toattend one of these workshops where a senior management accountant opened as follows:

“It is a pleasure to be here with you this morning to give you an overview of the Finance organization.Working for a big company like [MEGOC], we all get so busy in our own operations that we donot get much chance to interact with each other and learn what each of us has to offer towards theaccomplishment of the company’s corporate objectives. Many thanks to the [hosting department’s]coordinators for giving us this opportunity to speak to you today. My colleagues and I will help youopening up the Finance black box, as some of you have referred to us lately . . .”.

During his speech, the senior management accountant surprisingly built on the BSC language, metricsand underlying logic to describe the reasons why Finance should be perceived as ‘a crucial partner in thebusiness’:

“The vision of the Finance organization is to be recognized as a responsive and effective busi-ness partner providing innovative financial expertise with a highly skilled, strongly motivated andempowered staff . . . I want to emphasize the word partner to you here because this is how we wantyou to see our organization: as your business partner, providing you as well as all the other operatingand support organizations within [MEGOC], with innovative financial expertise to meet your opera-tional needs and improve the quality of your economic decisions in line with the highest ethical andlegal standards and in accordance with top management’s general and specific directives. We arenot able to realize this vision and partnership on our own, by implementing our own initiatives . . .

This makes today’s presentation extremely important to us. If we succeed in encouraging you to callupon us for consultation, then we can truly become your business partner in achieving the corporatestrategic imperatives, as well as the key objectives included in your scorecards and business plans”(senior management accounting).

Interviews and observations within the Finance function provided evidence that interest was increasingin the BSC; a technique that was originally considered an ‘operational tool’ outside the scope of the Financeorganization, and for this reason largely ignored. This was not the case anymore. “We are currently inthe process of developing our own scorecard . . . we already started its implementation in some pilotdepartments within Finance”, stated a Finance manager, who then adds, “I guess it is time for us tofoster processes of interactions with the other divisions, which are all placing financial objectives at thetop of their scorecards and strategy maps . . .”. Finance experts perceived a growing interest in financialmeasures following the BSC implementation in several operating and service areas of the company, anddecided to build on this increasing focus on Finance to gain new relevance (and control) by introducinga full costing system within MEGOC.

The malleable BSC made malleable and permeable those who engaged with it. Thus, accountantsforgot their interest in budgets, which were not even flexed, and became ‘business partners’ and ‘experts’providing ‘innovative financial expertise’, rather than preparers of boring budget figures. They could trulyonly become so if another community was created, a community made of hybrids of all sorts (Caglio,

C. Busco et al. / Management Accounting Research 18 (2007) 125–149 139

2003; Burns and Baldvinsdottir, 2003), where it is no longer clear who is an accountant and whereaccounting is actually done. The authorship of the accounting is diffused as much as the ontology ofmanagement accounting, its agency and forms of translation.

Interestingly, Finance experts started to sell organization-wide their closeness and centrality withinthe BSC, which suddenly became a key source and object of trust to rely upon to promote the regainedrelevance of the Finance organization (Busco et al., 2006; Seal et al., 2004; Tomkins, 2001). Such inter-twined relationships between the BSC and the Finance organization were evoked as the senior managementaccountant addressed the workshop’s audience as follows:

“In each one of your scorecards you reach a point were operational metrics get translated in financialterms. Well, we can be your partner with you there, we can build with you an all new level of costawareness . . . We have a brand new ‘Full Cost Reporting Project’ that will improve corporate anddivisional performance through higher cost awareness. Current cost sheets include NDEs (net directexpenses) and support service costs. However these do not fully reflect the true costs required foreach organization to function . . . This new system will help fuel your scorecards with accuratenumbers, and help a better translation of operational achievement into bottom-line results”.

The sceptic accountant has become a BSC enthusiast: the work of fabricating the management account-ing technique (i.e. What is subject to change) goes hand in hand with the process of constructing the identityof those who are subject and objects of these new forms of accounting and accountability.

5. When and where change happens? And who is there to observe it? Alternative forms ofinterpreting change

Over the last two decades, as accounting began to be understood and interpreted as a situated,context-dependent practice, the management accounting literature has seen a considerable growth inboth fieldwork and case studies. Motivated by the quest for rich descriptions of accounting in action(Ahrens and Dent, 1998), case studies have been portrayed as a method that offers the researcher “thepossibility of understanding the nature of accounting in practice; both in terms of the techniques, pro-cedures, and systems, etc. which are used and the way in which they are used” (Ryan et al., 2002,p. 143).

It is commonly argued that extensive and longitudinal case studies enrich our understanding of thefield by providing detailed accounts of the intertwined relationships between organizational contexts andthe functioning of accounting (Ahrens and Dent, 1998; see also Burns and Scapens, 2000; Boudreauand Robey, 2005). Generally, this position is supported by the claim that longitudinal studies allow anunderstanding of the object under scrutiny to be developed – in the case of MEGOC the BSC – evolvesover time. However, the epistemological implications of this claim deserve a further discussion.

Although the features of the social context being studied, and its interplay with the accounting con-structions, can be interpreted only in light of the specific circumstances in which they unfold throughtime, a longitudinal case assumes a linearity of time and evolution which, for example, was not wit-nessed in MEGOC. The complex and continuous intertwining of various attempts of implementing theBSC(s) suggests that this technique assumed various evolutionary stages simultaneously and not neces-sarily progressively. MEGOC is so vast and its networks so diverse that the BSC implementation did notnecessarily follow the same pattern and pace within all the participating divisions and departments (for

140 C. Busco et al. / Management Accounting Research 18 (2007) 125–149

example the E&OS and the Finance divisions engaged with the BSC in quite different ways and withindifferent intra-organizational networks).

Therefore, despite the length of time spent within the organizational context researchers need toconfront the impossibility of fully representing and understanding the object of their enquiry as if itwas out there, evolving in front of them along a linear pattern. In the case of MEGOC, for example, theresearcher who developed the case could only offer a partial testimony of the events.9 In fact, the researcherdid not have access to the complete story, which was unfolding simultaneously in different corners of thecompany. The BSC(s) engaged differently with the various actors and centres within MEGOC, and everyattempt to account for that is unavoidably a limited and partial story in time and space.

Paraphrasing Mol (1999), it could be argued that the BSC represents a complex object made by“different versions, different performances, different realities that co-exist in the present” (p. 79). TheBSC is constantly defined by continuous acts of engagements through which it is performed (even in itsabsence) in various organizational time(s)–space(s). Therefore, the object did not need to ‘evolve’ overtime to change, but only required the enactment of different realities and connections with other differentpractices and systems at work (Law and Singleton, 2005). Within MEGOC change did not happen ona linear timeline that the researcher could monitor, but in a semantic network of relations that createdmultiple spaces and times whose richness is very difficult to account for (Quattrone and Hopper, 2001,2005, 2006).

We argue this has implications for the rationale of longitudinal case studies and for understandingissues of Where and When change happens. Information on the project’s length and data collected mayaid others to reflect on the interpretive journey the researcher undertook and the conclusions he hasachieved, but they cannot be perceived as comprehensive and wide-ranging accounts which illuminatethe processes of management accounting change—specifically the processes of BSC(s) implementationwithin MEGOC. Definitely, the passage of time was important for the researcher to gain an understandingof a practice such as the BSC, but it did not help to interpret in full what counts as an object, as well as theBSC ability to mobilize and engage with other elements (human and non-human) of the organizationalcontext.

Similarly, a manager from one of the divisions implementing the BSC had “mixed feelings on thescorecards ability to foster integration and cooperation throughout the organization, as well as on theprocess through which it was deployed, cascaded down to the different departments and, eventually, linkedto employees’ appraisal”. Although he claimed to “agree in principle with the idea of translating strategicimperatives into action through a balanced bunch of objectives and key indicators”, he emphasized thefact that the BSC was imposed in his department “without taking into account the existing organizationalculture and working practices”. In particular, he suggested:

“top management at both corporate and business line level should have built the business case forsuch an important process of change that affects performance measurement systems throughoutthe division. They should have better described to the employees how things will look after theimplementation and, eventually, they should have fostered support and commitment for changethrough effective communication and healthy dialogue within the division . . . Unfortunately, this isnot always the case, and the process slows down . . . Dealing with resistance to change representsfifty per cent of my time as a team member for the scorecard implementation in my department.

9 As suggested earlier, the insights from the MEGOC case are based on a study conducted by one of the authors.

C. Busco et al. / Management Accounting Research 18 (2007) 125–149 141

[. . .] Regrettably, not all managers within the division understand that resistance is a natural forcethat people use to maintain and stabilize any system they are working with, and the scorecard getssometimes trapped in such a lack of leadership”.

Translating strategy into action, making companies strategy focussed and enabling alignment andintegration are outcomes that the BSC promises to deliver (Kaplan and Norton, 2001). Whether the BSCimplementation succeeded to do this in MEGOC was questionable, as well as When and Where thishappened. The BSC was received unfavourably in some sections of MEGOC, but more favourably insome others. This was due to a variety of reasons ranging from a lack of clarity about the reasons forits introduction (“because someone on the Board has fallen in love with the flavour of the month duringa training course in London”—as cited earlier), to a failure to engage with well established account-ing practices, which eventually stimulated resistance within the Finance organization. Paradoxically,instead of integrating the company, the BSC was contributing to reinforce existing boundaries. Ironi-cally, the initial successful implementation of the BSC in some corners of the organization increasedthe disappointment of those managers who talked about it, without being part of the BSC deployment,yet.

The different business lines of MEGOC had the autonomy to decide whether implementing (or not) thescorecards in order to better align with the company’s overall strategic imperatives. The map was there(see Fig. 3), awaiting to be ‘performed’ and not simply followed. Eventually, divisions took differentroutes to practice the BSC. Some business lines decided to take a bottom–up approach by first pilotingthe BSC implementation in specific departments. In one such case, shop floor employees were deeplyengaged with the new technique at work, and they were soon familiar with its logic and jargon. Such abottom–up process of implementation favoured the creation of a sense of ownership and identificationamong the employees, as well as enabling it to reduce potential episodes of resistance. As claimed by adepartmental BSC team member:

“We started by brain-storming what we felt were the key objectives to be accomplished by thedepartment. That was a very useful exercise that allowed us to think about and, sometimes, re-thinkthe reasons why we were performing certain activities . . . [to understand] the need to operationalisethe suggested objectives, to identify the key performance indicators and to measure them. Finan-cial and non-financial measures helped us to quantify the statements that define the objectivesand allowed a better process of communication and identification by the potential owners of thosemetrics. Then targets were identified according to our perception of the successful levels of per-formance to be achieved, and potential initiatives were discussed across the department . . . I mustbe honest and say that we strongly felt ownership and responsibility for the implementation of thescorecard, which today gives us a sense of pride and distinctiveness – it is truly seen as our ownbaby . . .”.

Clearly, When and Where the BSC was taking shape was not easy to follow for either the researcher orthe practitioner. Understanding how and why the BSC could mobilize potential users and how they couldengage with it was not immediate. It took some time for the researcher as much as for the practitionersto understand that the BSC was not out there to do things, but offered a space and a time for change tohappen.

142 C. Busco et al. / Management Accounting Research 18 (2007) 125–149

6. Change and/or stability? The heteromogeneity of management accounting practices

Conceptualizing ‘change’ and/or ‘stability’ requires theorizing the nature of the ‘object’ that changes.Therefore, to interpret how management accounting (if not accounting tout-court) changes, we shall firstdiscuss the nature of management accounting practices, i.e. their ontology. This is particularly interestingespecially after the irruption of accounting studies drawing on various forms of post-structuralism whichhave questioned simplistic views of change and their current difficulties in theorizing at the same timethe malleability of practices and their immutability and sameness (see Thrift, 2004). Consequently, thechallenging issue now relates, not necessarily to the need for reconceptualizing change, but to how tolink these non-linear views of change with a new view of the object that is subject to change whichis, in the specific case, management accounting. In this respect management accounting practices canbe interpreted as ‘objects’ that can extend and mobilize networks of relations with users and otherorganizational information systems to construct organization-wide visibility.

Interestingly, the literature that relies upon Giddens’ Structuration Theory is sensitive to the temporalproblem of change. As claimed by Orlikowski with respect to information technologies, they are “neverfully stabilized or ‘complete’, even though we may choose to treat them as fixed, black boxes for a periodof time. By temporarily bracketing the dynamic nature of technology, we assign a ‘stabilized for now’status (Shryrer, 1993)” (Orlikowski, 2000, p. 411). This permits studies using Structuration Theory toaccord time a central role, whereby interactions between structure and action follow a linear and recursivepath in a progressive and ordered manner so that researchers are eventually able to account for situationsat time2 that always follow events at time1 (see DeSanctis and Poole, 1994; Orlikowski, 1996; Orlikowskiand Yates, 2002). However, how can we assume the stability of a practice (even for a limited period oftime) without reifying the practice itself and limiting enactment possibilities?

Management accounting practices are not necessarily a single, stable entity at a point of time, andchange and stability seem to co-exist in forms, relations and within spatiotemporal frames which arestill to be deciphered (cf. Granlund, 2001; Burns and Scapens, 2000). For example, as illustrated earlier,the BSC did not smoothly evolve over time (or space) but acquired different forms simultaneously indifferent parts of MEGOC. Moreover, BSC’s emergence as a working practice relied on human enactmentsand non-human praxis involving strategy maps drawing, cost calculations, physical measurement, andmanagement controls.

The perspective offered in this paper attempts to reconcile the apparent homogeneity of managementaccounting practices (such as the BSC) with the heterogeneity of their use, by recognizing that thesepractices are amenable to be flexible and malleable. Objects like the BSC can possess diversity andheterogeneity while being a homogeneous and operative technology. Management accounting (in thiscase, the BSC) appears homogeneous for it attracts and generates heterogeneous uses: its homogeneousnature is intrinsically linked to the heterogeneous nature of those (things and humans) that are attractedby it.

As we noted earlier, within MEGOC the BSC can be theorized as an absence which establishesa presence by mobilizing and attracting other actors and technologies. In this respect the BSC seeksvisibility in organizations as it emerges from multiple and continuous translations. Thus, the definitionof a BSC is neither stable nor singular across MEGOC’s time(s) and space(s), and this enables thismanagement accounting practice to drift across the different divisions and departments.

Management accounting techniques can be interpreted as ‘objects’, which maintain their homogeneitydespite and thanks to their heterogeneous use. Management accounting (the BSC, in this case) is thus

C. Busco et al. / Management Accounting Research 18 (2007) 125–149 143

an ‘heteromogeneous object’ (Quattrone and Hopper, 2006) whose ontology can be understood only byexploring how it is materialized in real or virtual forms, the way in which it relies on image or visualrepresentation to organize thinking and actions, how it appeals to the potential users by remaining at avery superficial level of abstract principles and linear visual forms, as well as its ability to become aworking space and time, which is offered to the users to perform and enact (see Ezzamel et al., 2004;Quattrone, 2006).

One of the features of the BSC within MEGOC was to embody and communicate issues of integrationand strategy execution in manners which are visually and methodologically engaging, without entering intoo detailed and exhaustive representations of all the possible actions. The simplicity of the map describedby E&OS managers during the workshop offered potential space(s) and time(s) to perform actions, topractice the BSC and make it work. Conversely, an attempt which would try to tell it all would not spreadas it would not be translatable and thinkable at the ‘eventual’ level of the practice (Johns, 1998); i.e.it would not engage the prospective user who could see a space and opportunity for action. Thus, it isthe simplicity entailed by the method and its visual clarity which make management accounting toolsperformable. Paradoxically, the BSC(s) are performable not because they force users to follow certaindirectives, but because they leave users free to enact that space which is offered by the technique.

Within MEGOC the BSC thus became objectified, not because it is made of inscriptions which make itan immutable mobile (as early studies in ANT would have argued), but because it attracts a heterogeneityof users. This is why management accounting can be interpreted as a heteromogeneous object; i.e. an objectwhich appears homogeneous and spreads across the organization, not because it is fixed and immutable,but because it attracts diversity and heterogeneity. The combination of the linearity exemplified by thevisual schematization of the content of the technique and its simplicity ignite a process of reference tosuch a technique (Quattrone, 2006). In other words, one needs to understand what makes an abstract setof inanimate scripts a practice (see also Ezzamel et al., 2004; Chenhall and Euske, in press), somethingwhich can be performed. This is what has happened in MEGOC where multiple BSC(s) and differentstrategy maps mushroomed in several organizational-wide networks under the ideal of integrating thecompany along six strategic imperatives and four balanced perspectives of analysis.

“I don’t see why we should engage with Finance on our own scorecard . . . at present we feel we arein control of the metrics and numbers we developed and we do not want to argue, mediate or simplyjustify to others what we do around here . . . We have built a solid team here: our employees identifywith our strategy, at corporate planning they have learnt to appreciate our skills and initiatives and,finally, these guys [pointing at two members of the internal consulting organization] now feel athome within our premises . . .” (BSC team member).

The extent to which BSC (or better the multiple scorecards) deployment has fostered processes ofintegration within MEGOC is currently debated within the organization. When asked, organizationalmembers interpreted the results of the BSC implementation differently. For example, managers in theE&OS division celebrate the existence a new organizational map defined vertically by the company strate-gic imperatives and horizontally by the four balanced scorecard perspectives. Nevertheless, “longitudeand latitude coordinates are useless if employees are suddenly placed in the middle of the desert andthey are not told how to use the compass (!)” claimed a BSC team member from one of the divisionsimplementing the BSC. He was complaining that the BSC implementation lacked direction and supportat the shop floor, “where the objectives of the scorecard were struggling to be translated into measuresthat make sense to everybody”.

144 C. Busco et al. / Management Accounting Research 18 (2007) 125–149

Among those people who appreciated the outcomes achieved by the BSC implementation in MEGOC,one of the most frequent comments was that “the scorecards were smoothly rolled out in all sevenbusiness lines of the company” (operations manager). In so doing, “it was unquestionably fosteringprocesses of integration and knowledge sharing across the organization” (E&OS BSC team member).This was the case in the Finance organization that lately assumed the language, metrics and underlyinglogic of the BSC to ‘market’ itself as a crucial partner in the business and to promote a brand new full costmethodology.

In spite of that, other participants suggested that the BSC was creating further boundaries and separationamong MEGOC’s business lines, which were focussing on their own objectives and measures, andpursuing their own initiatives. Interestingly, a BSC team member of one of the MEGOC’s divisionshighlighted the absence of a corporate scorecard:

“with seven different divisional scorecards at work, and no corporate-wide scorecard in place, itis like playing the same sport but in different leagues . . . everybody wins, every business line isallowed to take its own actions and initiatives in light of the objectives to be achieved . . . SometimeI feel we miss the overall picture, and the six corporate [strategic] imperatives are not enough inthis respect”.

The absence of a corporate template is what allowed the BSC to persist as a practice which could beused in MEOC. If it had been implemented according to rigid guidelines, resistance would probably havestopped its deployment. Much better to leave it malleable, as this allows a nice and smooth combinationof change and stability.

7. The papers in this Special Issue

This Second Special Issue of Management Accounting Research on Management Accounting Changecomprises five papers, which all, directly or indirectly, touch on the issues that we have addressed in thispaper and represented in Fig. 1.

The first three papers in the sequence all relate their analyses to new institutional sociology whichhas been largely utilized in the management accounting literature on change. The paper by Ezzamel,Robson, Stapleton and McLean addresses issues of change by looking at accounting reforms in the UKschool sector. In their paper, the notion of accountability as an institution is seen as the medium andthe outcome of processes of accounting change. They analyse the interplay between rational and legit-imate notions of accountability, implied by the legal reforms of UK schools, and those ‘folk’ notionsof accountability, implied by the local professional norms and routines, which had kept participantsaccountable until the emergence of the new accountability regime. Ezzamel et al. (2007) are concernedwith the matter of assessing whether rational forms of accountability travel untouched and unchallengedfrom the reform discourse to the field of school education or instead are mediated by, and mediate,taken for granted accountability practices currently in operation in the organizational setting. The authorsutilize the notion (and practices) of accountability as a locus where global tendencies towards homo-geneization clash and/or intertwine with local and tacit forms of ‘giving accounts’. Their findings arethat organizational actors operate under different institutional realms ranging from being accountableonly to the ‘folk’ and local professional accountability, to virtually all of these sources of accountability,including the new societal demand for being financial efficient. Interestingly though, forms of financial

C. Busco et al. / Management Accounting Research 18 (2007) 125–149 145

accountability seem to be more pervasive than folk and local ones so that even these can no longer bearticulated if not in the numerary and monetary terms pertinent to the dominant discourse of efficiencyand value for money. This clearly entails the problem of understanding how some management account-ing techniques, discourses and rationalities are seen as more valid than others even in (local) contextswhere a strong (although ‘folk’) notion of accountability already exists. The paper also calls for a deeperunderstanding of how and why quantitative notions of accountability, i.e. accountabilities which are trans-lated into numerical metrics, win over qualitative ones which do not translate so easily into monetaryterms.

Similar concerns and approach are offered in the paper by Dambrin, Lambert and Sponem, whichalso looks at management accounting change utilizing a New Institutional Sociology perspective in orderto restate the need to move away from a functionalist perspective which views change as the result ofsome economic imperative. Drawing on the findings of Hasselbladh and Kallinikos (2000) they reflecton the explanatory power of the notion of decoupling to illustrate how processes of institutionalizationare never linear, with precise outcomes. They address this issue in the context of a firm operating in thepharmaceutical context where, they note, management accounting systems play a dual role in the processof change. On one hand, management accounting is the target of change, in line with a new institutionalapproach, for it is utilized to provide organizations with an aura of efficiency and rationality which canlegitimise them in the organizational field in which they operate. On the other, though, managementaccounting is also a vector of change. The authors thus offer a reflection on the notion of decouplingand how change can actually be implemented, rejected or decoupled through the practices currently inplace in the organization. The ideals driving change can generate new ones and consequently the processof change is never linear, functional or predetermined, but untidy: how changes are internalized acrossthe organization can vary and assume different forms. Change can be slowly implemented, rejected orceremonially accepted depending on the element of the management control system which is having aneffect on the organizational actors. Key in this process is the ambiguity (rather than the clarity) of theideal driving change.

The paper by Nor-Aziah and Scapens also reflects on the notion of loose coupling in the context ofthe corporatization of a Malaysian public utility. The study is concerned with understanding how andwhether general calls for greater efficiency are translated into daily accounting practices or become insteadloosely coupled from these general calls. They reflect on the notion of loose coupling, highlighting howloosely coupled budgets were not simply an automatic response to institutional forces driving accountingchange. It was instead the result of institutional contradictions which percolated into budgets making thema source of tension and conflict between operation managers and accountants, and thus loosely coupled.Institutional contradictions, power and trust relations, and issues of resistance help to shift the focus ofnew institutional approaches: from the context to the individual as agents of institutional change. Yet,loose coupling facilitates a combination of change and stability in the organization and thus permits thestable provision of the public service offered by the public utility. It limits the effects on the organizationof external factors calling for a restructuration of management accounting and organizational routines.

The other two papers in the Special Issue follow different theoretical routes, but are still closely relatedto issues of stability and change, agency, process of change and its impact on organizational relationships,and management accounting itself.

The paper by Thrane explores how the notion of organizational systems needs to be rethought inlight of different forms of organizing, self-organizing and contribution of the literature on managementaccounting change. The occasion for this exploration is given by the study of a network of indepen-

146 C. Busco et al. / Management Accounting Research 18 (2007) 125–149

dent Danish consultants who collaborate to boost their own business by combining a series of actionswhich are both competitive and cooperative. In this network, managerial accounting techniques, such astransfer pricing, act as a source of instability and create unintended organizational outcomes. For Thranechange happens in systems which are not linear, but dynamic and multidimensional. However, changeis not entirely free—but instead, it is dependent on the presence of path dependences and the influence(although unintended) of certain points of attraction which directs change. Differently from conventionalapproaches to change in management accounting and control, which view change as occurring withina specified organizational space (be this designed by a hierarchical organization, a market arrangement,or a more socially constructed notion of trust), the paper seeks to understand how management con-trol is part of the processes of change, but in ways which are unpredictable, though still dependenton the self-organizing paths emerging in the interorganizational network which establishes a ‘network-logic’.