Page 1

CHAPTER V

Management of Interest Rate Risk and

Liquidity RIsk

The changes in interest rates and liquidity problems in the Post-

Reform Period havc pavet1 thc w a y for risks of different dimensions and

this has afTected the bzu~k's perlbrrnance and operating results. The

following analysis focuses on these aspects.

(a) Interest Rate Risk Assessment and its Management

Interest Rate Risk normally means changes in the interest

income due to changes in the rate of interest which will ultimately

affect the value of 1)ank's assets, liabilities and off-balance sheet

instrurncnts. A fall i n itilcresi rate may adversely affect the interest

income from atlvances. Hut tlrposits will have to bo carried at higher

cost till their maturity if they have already been mobilized for long'term

tenure on fixed interest basis.

The Interest Rate Risk Management of the banks can be studied

by analysing the growth of Interrst Income, Interest Expenses, Spread

and Burden and also by analysing the Interest Rate Sensitivity of the

banks.

Interest Expense to Interest Income Ratio

This ratio has a direct impact on the profitability of the banks as

it reflects the efficiency of raising resources and their deployment. It

shows the proportion of' interest Income expended on the payment of

interest. In all other banks except in IOB the ratio shows an increase

Page 2

dur ing thc pcriotl of s tudy . In I 0 1 3 t he proportion of ln tcrcs t Expense

to Interest lncorne is vcry high du r ing t h e y e a r s 1992-93 and 1993-94

(i.e. 92 .28 pcr c e n t and 85.83 per c e n t respectively) and t h e bank has

sufferrtl loss dur ing I h r sillnc. pc.~.~otl (oidc. 'l'ablc 1V (24)).

Table V (1)

Interest Expense to Interest Income Ratio of the Selected

Banks from 1991-92 to 2001-02

Year .. Name .- - of the Selected Banks IOU UUI FB SIB D L 6 81 90 62.82 60.87 62.65 61.11

- -- -- - - 75.42 73.39 66.67

1993-94 X S 83 69 14 68.53 71.01 66.67

1994-95 76.38 63.74 67.46 70.06 67.3 1

~ -~

1995-96 71.37 76.02 64.87 74.94 67.80 69.05

~ ~~ - ~

1996-97 72 72 77.03 66.85 81.52 77.06 76.80

1097-98 72.7 1 7 5 10 67.37 80.34 76.99 75.37

~~~ .. .-

71.00 89.87 78.00 79.58

~~ ~ .- .

'72 89 71 13 79.48 74.84 75.46

2000-0 1 60 96 68 49 07 35 74.21 72.22 77.40

..~ ~

200 1-02 66.71 73.51 74.80 76.24

~ p~ - .. -

lnterest I I90 17.13 26.66 24.88 31.13

Interest 2337 22.35 27.76

Source ( 'onl l~~led and Coniputed lio111 Ar~li~lal llepo~ts of the Selected Banks

Page 3

By the year 2001--02, the ratio has been reduced to 69.41 per

cent. In FB the ratio was high during the year 1998-99 as compared to

other years and the bank could earn only an extraordinary low profit

during the same year (vide. 'Table 1V (24)).

The Average An~lual Growth (AAG) rate of Interest Expenses and

lnterest Income of Private Sector Banks is higher than that of the

Public Sector Banks. l'he AAG of Interest Expense of all other banks

except IOU is higher than the AAG of lnterest Income. From this

analysis it can be inferred that the Interest Spread (Interest lncome -

Interest Expense) of the banks are showing a declining trend.

Non-Interest Income to Non-Interest Expense Ratio

'I'hc Non-Interest 11lcornc of the banks should be sumcient to

meet the Non-interest. Expense, otherwise it would become a burden for

the banks. tlere thc ratio indicales as to what extent the Non Interest

Expense can be covered by the Non-lnterest Income. Except in IOB

and UBI, the proportion of Non-lnterest lncome to Non-Interest

Expense of other banks is showing a consistent increase during the

period of study. In IOB, the ratio which was 46.13 per cent in the year

1991-92 has been rctluced to 17.85 per cent during the year 1992-93,

the loss-ln:rkirig yc;lr. l'hc r:ltio rc:~-r~;~inctl low in sornc years and by the

end of 2001-02 the same has reached a level of 41.81 per cent. In the

case of UUI thc ratio ranges [jetween 22.69 per cent lo 32.79 per cent

over the years. The low ratio reveals high burden of the bank.

Page 4

In SI.YI', I'U, SIB and L)l,B the ratio has increased from 22.70 per

cent, 21.67 per cent, 28.57 per cent and 22.22 per cent respectively in

the year 1991-92 to 43.07 per cent, 53.01 per cent, 59.48 per cent and

64.84 per cent respccl.ively by the year 2001-02. In the declining

interest rate era the t ~ a n k s are concentrating more on the Non-Interest

Income to sustain ancl increase the profit.

Table V (2) Non-Interest Income to Non Interest Expense Ratio of the

Selected Banks from 1991-92 to 2001-02 (Per cent)

7-- . _ - . ~ .- I

Source C'on~piled and Co~i~puted tiotii Annual Reports of the Selected Banks

Year ~

Name of the Selected Banks DLB 22.22

SIB 28.57

-

F B 21.67

.-

~ .-~ LOB ~ . ~ - T - "b , 46.13 23.12

.

S UI'

~-

1996-97 37 35 26.68 53 3 9 27.85 36.36

-~

1997-98 42.21 35.20 51.1 1 3 1.33 38.46

1998-99 57.07 31.09 33.33

1999-2000 -17 56 20.42 25.89 49.44 44.3 1 46.30 ~ ... ~~ - -- ~

2000-0 1 1 30 43 ? X 3 0 23.60 41.53 40.33 44.07

-- .. . ~~~ - --.-. .

2001-02 ~ / 4.1 07 1 4 I 8 I 32.7') 53.01 50.48 64.84

- . ~

18.96 19.31 3R.91 39.54 49.24 Non lntcrcst

lnco~nc 30 22 15.30 22.84 23.10 27.35

Expense - ~ ~ ~

1991-92

1992-93

~-

22.70

17.85

.. .. -. -

30. 00

28.57

40.91

25.00

38.60 33.13

+- ..

30 58

- --

32.50

28.38

- ~ -

2557

1993-94

1994-95

27.27

36.52

57.93 1995-96

53.23

.

40.32

25.26

4.181

.- ~~ ~ ~

4 1.70

- ---

33.42

~~~~~

36.49

~ ~

37.86 26.50 23.35

Page 5

A s compared to the Public Sector Banks, the Private Sector

Banks under studv have been able to increase the Non-Interest Income

to cover the Non-Interest Expenses during the period of study.

Net Interest Income (Net Interest Margin)

Asset Liability Management focuses its emphasis on the growth

of Market Value of Equity (MVE) and improvement in Net Interest

Income (NIII. Optimising Net Interest Income is one of the objectives of

ALM. NII or Spread is the difference between Interest Income and

Interest Expense. NII of the bank should be adequate to leave certain

profits for the bank after having adjusted the Burden (Difference

between Non-Interest Expense and Non-Interest Income]. For the

industq-wise comparison of a bank's performance Net Interest Margin

(NII as a percentage of Total Fund) is used.

Net Interest Income to Total Fund Ratio (Spread)

The impact of deregulation of interest rate and competition

among banks with regard to interest rate in the Post-Reform Period can

be revealed from the declining Net Interest Income to Total Fund Ratio

of the selected banks (Table V (3)). The declining interest rate in the

Post-Reform Period on both deposits and advances has reduced the

Spread of the banks. In IOB the ratio is very low in the beginning of

the period of study when compared to other banks. In the year

1992-93 the Spread of IOB is lower than the Burden (vide. Table V(4)).

Page 6

Table V (3)

Net Interest Income to Total Fund Ratio (Spread) of the

Selected Banks from 199 1-92 to 2001-02 ~ ~ -, - ~~~ .. ~ . ~

- - - I ~ ~ 7

Source: Compiled and Computed from Annual Reports of the Selected Banks

In SBT, UBI, FB, SIB and DLB the ratios which were 3.30 per

cent, 3.81 per cent, 3.22 pel- cent, 3.76 per cent and 3.85 per cent

respeclivelv in the year 1991-92 have been reduced to 2.58 per cent,

3.01 per cent, 2,72 per cent, 2.36 per cent, 2.28 per cent respectively

DLB 3.85

3.36

3.14

3.23

3.11

2.38

2.79

2.10

2.51

2.36

2.28

21.79

27.97

Year Name of the Selected Banks

by the year 2001-02 Thus ttir 1:111 in NIM is visible across all thc bank

SIB 3.76

SBT IOB UBI - - - 1991-92 1.72 3.81

FB 3.22

~~~ ~ ~ -~

1902-93 0.62 2 54

1993-94 2 41 1 .06 2 02

2.20

2.73

3.37

2.43

~

1994-95

1995-96

1996-97

2.65

2.89

- 3.05

- 3.70

~-

1997-98 2.93 2 3 0 3.17 1.89 2.55

~ - - --- 1998-99 2 I I 2 6 6 1.08 2.46 1 ~~ ~ ~ ~ ~ . . ~ - - -. --

1999-2000 2 27 2 10 2.73 2.37 2.65 ~- --

2000-0 1 3.13 2.68 2.88

200 1-02 '. 7 58 . 3 01 2.72 2.36

--- .~ -~ ~. ~- AAG 16.58 24.57 19.08

. - -.

2 63

-- 3 3 3

3 18

Ncl 111lcrcsl Illcollle

2 1 ~ u 1 1 d

2.1 l

1 79

~- -~ I!. 12

: ! 3 8 2.70

-. --

.-- .. 17.00 ~ ~ 4 ~ ~~ ---. 1138 ~

- -. 17.76

3.32

-~ .

3.40

3.41

p-

20.59 23.16

Page 7

categorics. Cost reduction is assuming great importance in this respect

and eveq bank will be required to consistently bring down its cost of

raising funds by arriving at an ideal deposit mix. Similarly, attention

will have to be paid to the reduction of Burden also.

Non Net Interest Expense to Total Fund Ratio (Burden Ratio)

The difference bctweeri Non-lnterest Expense and Non-Interest

Income is known as Burden as it is a negative figure.

Table V (4) Non Net Interest Expense to Total Fund Ratio (Burden) the

Selected Banks from 1991-92 to 2001-02 -- - (Per cent) r-- 1 -- I

Year Name of the Selected Banks

~- ~~~ . - 199 1 -92 r:r ~ ~ ~ "r~[~Tl 1992-93

- ~ ~- ~. .~ -. .- .~ -- 1993-94 3 73

- - - 1994-95 2 29 1 72 2.70 2.20 2.13 2.47

t . - . .- .- -- 1995-96 2.89 2.10 3.01 1.40 3.45 2.51

~-. - .- - 1997-98 1718 1.86 2.03

1998-09 2.29 1.88

199s-zoo0 ~~'

1.73 2.3 1 2.04 1.82

2000-0 1 2.00 2.53 2.73 2.07 1.95 --

200 1-01 1.84 3 00 2.3 1 1.92 1.43 1.70

I 1 X7 -

46 79 14.55 18.92 17.56 17.93 Non Ncl lntcrcsl

-- Expc~isc -~~ ~~

Total ftiiid 1 17 00 14 38 ~ .- ~ .. .- -- 17.76 20.59 23.16 27.97

Source: ('ontpiled arid C'ornputed fiorn A~lnual Reports of the Selected Banks

Page 8

Table V (4) reveals that the Non-Net Interest Expense to Total

Fund Ratio of the Selected Banks has decreased over the period of

study. In the year 1992-93 the Burden Ratio of IOB (i.e. 7.59 per cent)

was very much higher than their Spread Ratio (i.e. 0.62) and the bank

suffered heavy loss during that year. (vide Table IV (24)) In the year

1993-94 also the Burden Ratio of the bank was higher than the Spread

Ratio and the bank incurred loss during that year too.

When compared to the Public Sector Banks, the Private Sector

Banks have been able to reduce their Burden more by the end of the

period of study. A s the Net Interest Margin (Spread) of the banks is

declining in the Post-Reform Period it is only by reducing the Burden

that the banks can sustain and improve their profitability.

Spread, Burden and Profitability in the Post-Reform Period

From the above analysis it is revealed that the Net Interest

Income (Spread) of the banks has declined in the Post-Reform Phase

but the banks could increase and sustain the profit during the same

period by reducing the Burden.

In order to find out the influence of the Net Interest Income

(Spread) and Non Net lnterest Expense (Burden) on the performance of

banks the following hypothesis were formulated:

H 3 Though the Net Interest Income (Spread) is diminishing in the

Posr-Reform I'eriod the increasing Profitability of the Banks can

be attributed to the reducing Burden of the banks.

Page 9

Table V (5)

Spread, Burden and Profitabiliw: Pearson's Correlations

Details --

Spread anT~rofi tabi l i t~

-- -. -- Burden and Profitability

- -. . .- -

Source: Calculated from Table V (3) and Table V (4).

Karl Pearsons Coefficient of Correlation was applied to test the

hypothesis. From the 'Table V (5) it is inferred that only in IOB and FB,

Spread has significant positive correlation with Profit. In SBT, SIB and

DLB, Spread is negatively correlated though not significantly. But

there is significant negative correlation between Burden and Profit in all

the banks except in FR. Thus the Net Interest Income of the banks has

no significant positive correlation in the Post-Reform Period. But the

Burden is significantly correlated to Profit. Hence the hypothesis H3 is

substantiated.

This reveals that in the Post-Reform Period though the Net

Interest Income (Spread) is diminishing it is the reduction in the

Burden, which has helped the banks to improve their profitability.

Table V (6) shows the declining interest rates on Deposits and

Advances of more than one year in the Post-Refom Period. The

interest rate on Deposits of more than one year has decreased from 13

per cent in 1992 to 8 per cent bv the year 2002. The interest rate on

Page 10

Advances has tlecreasrtl St-otn 19 prr ccnt in 1992 to 12 per cent by the

end of March 2002

Source: A C:otnpe~ldiur~~ oF Inte~est. Itxcllange. Commission, other charges and latest

data on Banking. State Bank Institute of Rural Development, Hyderabad. March

2002 1) 20

Table V (6)

Interest Rates on Deposits and Advances - More than One Year

Fig. V(i) shows the declining interest rates on Deposits and Advances of

more than one year of the selected banks from the year 1991 -92 to

- ~rnleFest on Aclvn~~crs

19

- -- 17

14

15

16

14

13

12

11.25

12

12

IBrriocl

p~ ~- .

1992

.~ ~ ~

1993

~~~

i l l t r i i s t ~ I I i)cposits

~

13

~ . -- ~ ~~-~ --

I I

~ ~~ . , .. - - . . -- 1904 10

- ~~ -- .

1995

~ -~ ~~

~ . ~ ~ -

10

- -

1990 I ? _

~ ~~

I V) 7 t - 12 I

-- ~

1998

~ ~ -- ~

1990

~- ~

10.5

~~~ ~-

0.5

- ~ - I ~ ~ . - ~~. -

2000 8 . 5

~ - 200 1

- ~~ ~~

2002

~

9.0

~~.~ . -~

8.0

- - - 1 ~-

Page 11

191 Fig V( 1)

lnterest Rates on Deposits and Advances of More than One Year from1991-92 to 2001-02

0

199) '13 24 95 96 97 98 9'2 2000 2001 2002

Years

Analysis of lnterest Rate Sensitivity Statement

Thr change in interest rates that will lead to losses for the bank

is termed as Market or Interest Rate Risk. Both rising or falling

interest rates may lead lo losses in any bank. All investments,

advances, deposits, borrowings, purchased funds etc., that mature

within a specified time frame are interest rate sensitive. Similarly, any

principal repayment 01- loan is also rate sensitive if the bank expects to

receive it within the time horizon. The Reserve Bank of India has

implemented the simplest method of constructing a maturity ladder of

Rate Sensitive Assets (RSA) and Rate Sensitive Liabilities (RSL) to

manage the risk arising from maturity or repricing mismatches.

Page 12

In each maturity buckets (1-28 days, 29 days to 3 months etc.)

when interest sensitive assets exceed interest sensitive liabilities in a

particular maturity range, the bank is asset sensitive in a scenario

where interest rates are going to fall and as a result may sustain losses.

On the other hand, if the rate sensitive liabilities exceed the rate

sensitive assets, losses are likely from rising interest rates.

From April 1990 onwards, every bank has to prepare a Gap

Report by grouping Rate Sensitive Assets, Liabilities and Off-Balance

Sheet Positions into tirne buckets according to the residual maturity or

the next repncing period whichever is earlier. The gaps reflected by the

respective time buckets will denote the extent or the measure of

Interest Rate Risk.

By analysing the statement of Interest Rate Sensitivity in the

months of March 2000 and 2001, it is revealed that up to 3 year time

buckets, mainly a negative gap persists. A negative gap where RSL is

more than KSA will prove to be advantageous, if a t the stage of

repricing, interest rates have declined as it will result in an increase in

Net Interest Income. If Rate Sensitive Assets are more than Rate

Sensitive Liabilities, the gap is positive.

A positive gap is an indication that if repricing takes place at the

end of the time bucket, an increase in interest rates will be beneficial

and it will result in increase in the Net Interest Income. When the gap

is zero or nil, it implies that if' repricing take place at the end of the time

Page 13

bucket suggested, the risk is nil. In the declining interest rate scenario

a negative gap is beneficial for the banks.

By analvsing the gap up to 3 year time buckets in (Table V (7)), it

is revealed that in March 2000 a negative gap exists in SBT, except in

the time bucket of 1 to 28 days. In IOB and UBI, except in the time

buckets of 1 to 28 days and 6 months to 1 year a negative gap exists.

In FB a negative gap exists up to the 3 year time bucket except in the

time buckets of 29 davs to 3 months. In SIB except in the time bucket

of 3 months to 6 months and 1 to 3 years, a negative gap exists.

A s per Table V ('7'1 in March 2001, a negative gap exists in SBT in

the time buckets of 20 days to 3 months, 3 months to 6 months and 1

to 3 years. In IOB a negative gap exists only in the time bucket of 29

days to 3 months and 3 months to 6 months. In UBI except in the time

buckets of 3 to 6 months and 1 to 3 years a negative gap exists.

Under the category of Private Sector, FB has negative gap in the

time bucket of 3 to 6 months, 6 months to 1 year and 1 year to 3 years.

In SIB, except in the time buckets of 6 months to 1 year a negative gap

exists in all other time buckets. In DLB a negative gap exists in 1 to 28

days, 29 days to 3 months and 6 months to 1 year.

To know the immediate effect of Interest Rate Risk, gaps up to 3

years is considered as most relevant. The negative gap existing in the

time buckets of the selected banks has helped them to sustain the NII

and improve profitability during the last 3 years of the period of study.

Page 15

I

March 200 1

Figorcs in brackcls sl~ow Gap as a percent to Risk Sensitive Assets Sonrcc: Co~llpilcd and Conlpulcd from ALM Rcporls of tl~e Selcclcd Banks

Page 16

Impact of Deregnlation of Interest Rate Structure

Table V (8) shows the opinion of branch managers regarding the

impact of deregulation of interest rate. 75 per cent of the managers

contacted are of the opinion that the deregulation of interest rate has

adversely afTec:ted the business of their branches and 25 per cent of the

bank managers have not experienced this.

Table V (8)

Impact of Deregulation of Interest Rate Structure -

Particulars

I I (Per cent) (Per cent)

/rn~ilizing s a G i s due to low interest i 38 62

Dereg~lation of interest rate adversely affected the 1 75 I

I rate i

25

--- due consideration to branches

while 6xing interest rates

Source: Survey Report

While 38 per cent of the managers find it difficult to mobilize

savings, 62 per cent did not find any difficulty in mobilizing savings in

the declining interest rate scenario. 65 per cent of the managers

interviewed opine that the Head Office is giving due consideration to the

peculiar nature of the branches such as, competition, business climate

erc. while fixing interest rates. But 35 per cent of the managers have

not agreed to this

Page 17

Earning Capacity of the Branches

The long run sustenance of the banks depends on their ability to

earn Net Interest Income (NIII and this will ultimately improve the

Market Value of Equity (MVE) or the Net Worth of their business.

Table V (9) NII/Non NII Earning Capacity of the Branches

i o n b ~ y ~ t a e e Frequency Per centage Frquenq

Ability of the branch to earn NII

- Ability of the

1 7 i -, i

Source: Survey Report

Table V (9) shows various factors regarding the NII (Spread) about

which the branch managers have expressed their opinion. 51.6 per

cent of the branch managers responded to the question that they were

able to earn Net Interest Income (Spread) every year in their branches

while 36.7 per cent were able to earn Net Interest Income only in some

years. 11.7 per cent of the managers admitted that they have not been

able to earn Net Interest Income (Spread) for the last 10 years.

Only 25 per cent of the bank branches are able to earn Non-Net

Interest Income every year. Majority of the managers (65 per cent) are

of the opinion that their Non-Interest Income has been sufficient to

cover Non-Interest Expense onlv in some years. In 10 per cent of the

Page 18

branches, the Non-Nrt interest incorne has not been always sufficient

' X ensc. to cover the Non Interest C p

ALM Concept at Branch Level

A bank's profitability or rarnings normally depends on two

sources i.e. Net Intercsl income:. IN11) arld Off Balance Sheet Items (fees

chargcd on sprc.iSic s c lv~c r s rrndrred such as issuance of Lcllers of

Credit, Bank Guarantrrs , Hiring of Lockers, Demat Accounts, Cash

Management of Corporates etc)

Table V (10)

Internal Factors Influencing Profitability of Banks

I-- . --

Source Survey ~ e ~ o ; 1

Earnings based on Net Interest income is normally influenced by

internal factor s such as

1. Pricing oi Produt ts

2. Product Mix, a r ~ d

3. Asset ()~~;ility.

Table IV (10) shows va rous factors arranged in order of

preference rxprrssed by the respondents. Bank managers are of

opinion that saving assets from i~ecoming NPA (Asset Quality) is the

most important factor which will influence the profitability of banks. In

Page 19

the deregulated environment, fixing proper interest rate (pricing of

products) is corisiderrd :-lnothrr important factor affecting the Net

lnterest Incolnr ant1 profitability of banks. Decision of the banks

Mix) also inlluerices the profitability of banks.

Table V (1 1)

External Factors Influencing Banks' Earnings / Profitability

-. - -~ .

Business (.limate 4.80

~~. ~ - Interest Rate Risk. 4.07

~ .~~~ k?--i Liquidity Risk - ~- .~ ~

Behaviour of Monetary and Autl.~ority

-- - - ~~ ---- ~- ~ ~

6 / ('apital Adequacy Risk

i__i . .. . _ - .

Source: Survey Report

Due to the introduction of various Prudential Norms in the Post-

Reform period, various factors which were outside the control of the

banks become pretiorr~inarit in influencing bank's profitability.

According to the survey report a s given in Table V ( l l ) , competition

among the balks, changes in the business climate and lnterest Rate

Risk are the three important factors that are influencing the

profitability or earning capacity of the banks. Liquidity Risk and the

Page 20

norms prescribed by the RBI from time to time also affect the

profitability of the banks to a certain extent.

@) Liquidity Risk Assessment and its Management

Measuring and managing liquidity needs are vital activities of

Commercial Banks. By assuring a bank's ability to meet its liabilities

as they become due, Liquidity Management can reduce the probability

of developing adverse situations. Banks normally keep their liquid

funds in Cash and Balance with RBI, Balance with other banks, Money

at Call and Short Notice and also in Investments. To meet the liquidity

gap, banks adjust their surplus / deficit by investing the surplus funds

in short / long term securities and by disinvesting securities or by

borrowing funds from the: market to meet the shortfall.

Composition of Liquid Fund:

Liquid Funds of a bank normally include cash in hand and

balance with RBI, Balance with other banks, Money a t Call and Short

Notice and Investments. The Composition of Liquid Fund (Table V (1 1))

reveals that banks are increasing their investment by keeping the Cash

and Balance with the Reserve Bank of India at the minimum. Except in

IOB in all other banks the Cash and Balance with the RBI was high at

the beginning of the period of study.

A s the RBI has reduced the SLR and CRR requirements from

38.50 per cent and 15 per cent in 1991-92 to 25 per cent and 5.5 per

cent by the year 2001-02, banks have obtained more funds for

deployment.

Page 21

Table V (12) Composition of Liquid Funds of the Selected Banks from 1991-92 t o 2001-02

B:tnli / Partic~~lars AAC

. _ r..-8. -..A R 1- . , , a ,,IILL ,,ilh R R : 8.04

al call a Sl~on Nolicc Investments ?I 49

. . ~

100 I'?;<II and Balance with RBI

I Money a: call a Sbort Notice 47 17 108 1 I I I V C S ~ I I ~ C I I ~ S 19.16

Total I Cash and Balancc with RBI I 9.59 1 Moncy ;I[ ci~ll a Sllort Nolicc 38 46

URI

FR

111vcst111c11ts 'lol;~l Cash and Balancc with RBI Moncy ;II c;~ll 21 Sl~orl Nolicc I ~ ~ v c s l ~ ~ ~ c n l s Tolill Cash and Balance with RBI

SIB Investments 1 24.80 1 64.41 1 63.16 1 6736 1 7152 1 67.96 / 74.35 1 68.34 1 67.80 1 77.12 / 77.59 1 70.32 I Total 23.24 l i)O 100 100 100 100 100 li)o loo 100 100 100

Money at call a Shor( Notice 149.16 1.00 3.45 5.79 0.86 6.56 5.15 13.52 17.23 10.01 10.95 19.97

I8 27 16.64 8.46

45.41 24.37 IX.')O 8.94

D1.B

67 51 100

40.93 4.39 54.6') 100

34.59

Source: Compiled and Computed from Annua l Repor ts of t h e Selected Ranks

Cash and Balance with RBI Money at call a Sllort Notice Investmenls Tol:ll

71 25 100

3300 439 6261

100 33.39

16.85 59.38 29.18 25.78

76 30 100

34.43 0.45 5 2 100

2686

35.35 9.09 55.56 100

67 6 100

2259 3.43 73.99 100

27.62

33.91 6.96 59.13 100

62.50 100

26.06 11.08 62.86

100 25.48

26.32 8.77 6 9

100

6603 100

16.54 13.66 69.80

100 20.51

26.03 6.39 67.58

100

34.20 8.12 57.68 100

66.14 1 67.35 63.60 100

12.28 3.75

83.97 100

12.87

100 14.02 7.56 78.42

100 18.14

21.28 26.64 52.08 100

100 13.43 8.25 78.33 100

14.97

72 00 100 7.46 6.12 86.42 100

11.46

17.10 21.59 61.31

100

76.23 100

10.37 4.94 84.69 100 9.71

23.65 15.86 60.48

100

17.81 6.07 76.1 1 100

11.70 7.63 7.67 100

12.14 9.62 78.24 100

Page 22

In the light of high NPA level with the banks, a high portion of the

additional funds obtained due to the reduction in reserve requirements,

were deployed by the banks in Investments. The sharp rise in the

proportion of Investment of the selected banks reveals this. In SBT,

IOB and UBI, the proportion of Investments in Total Liquid Fund has

increased from 55.15 per cent, 75.81 per cent and 67.51 per cent in

1991-92 to 76.18 per cent, 80.61 per cent, and 76.23 per cent

respectively by the year 2001-02. In the category of Private Sector

Banks the ratio has increased from 54.69 per cent, 64.41 per cent and

55.56 per cent in FB, SIB and DLB respectively in the year 1991-92 to

84.69 per cent, 70.32 per cent and 78.24 per cent respectively by the

year 200 1-02.

Changes in the Statutory Liquidity Ratio (SLR) and Cash Reserve

Ratio (CRR) in the Post-Reform Period

In order to ensure adequate liquidity with banks as well as

reasonable growth in the supply of bank credit in the economy both

SLR and CRR are being maintained by the banks as per the

instructions of RBI.

Under section 42 (1) of the RBI Act 1934 Scheduled Commercial

Banks are required to maintain with the RBI a Cash Reserve Ratio in

certain proportion of their Net Demand and Time Liabilities (NDTL)

between 3 per cent to 15 per cent.

Page 23

Table V (13) Reserve Requirements Prescribed by RBI for Commercial Banks

from 1991-92 to 2001-02

~ ~ - ~ S T a t u t O ~ ~ ~ ~ Liquidity Ratio Ratio

Source: Report on Trend arid Progress of Banks in India: various issues.

Similarlv as per section 24 of the Banking Regulation Act,

Commercial Banks in India are required to maintain, in addition to

Cash Reserve under section 42 of the RBI Act, a Statutory Liquidity

Ratio (SLR) in certain proportion of their Net Demand and Time

Liabilities (NDTL) between 25 per cent to 40 per cent in the form of

certain Liquid Assets.

Page 24

Fig V (2) Reserve Requirements Prescribed by RBI for Commercial

Banks from 1991-92 to 2001-02 60

Years

A S L R . CRR -t Total

Fig V(2) shows the SLR and CRR rates prescribed by the RBI from the

year 199 1 -92 to 200 1-02.

CRK and SLK have b ~ e n introduced mainly to safeguard the

interest of the depos~tors by ensuring that a part of the depositor's

money is kept in liquid form (under CRR requirement) and in near

liquid fornl of assets (under SLR requirement) as well as to regulate the

liquidity with banks w t h a view to control the money supply in the

economy Even though banks are free to mobilize deposits, they cannot

make use of all of them exclusively for lending and investment purpose

because of these regulatory requirements.

Page 25

It can be seen from Table V (13) that in the year 1991-92 the

total Reserve Requirements were 53.5 per cent (i.e, every Commercial

Banks had to keep 38.5 per cent in SLR and 15 per cent in CRR) and

the banks were left with only 46.5 per cent of the deposits for

deployment. The Reserve requirements show a sudden decrease

during the year 1996-97. The total Reserve requirements which were

45.50 per cent in 1995-96 have been reduced to 35.00 per cent in the

year 1996-97. By the year 2001-02 the SLR and CRR have been

continuously reduced and reached a level of 25 per cent and 5.5 per

cent respectively thus leaving sufficient funds (69.50 per cent) with the

banks for deployment.

Liquid h.md to Total Fund Ratio

This ratio reveals the percentage of Liquid fund maintained by

the banks during the period of study. The proportion of Liquid Fund to

Total Fund varies differentlv for different banks under study. In all

other banks except IOH, the ratio shows a declining trend during the

period. In IOB the ratio was only 38.881 per cent in the year 1991-92

and the same reached a level of 52.75 per cent by the end of the period

of study. FB keeps this ratio at a lower level from 1996-97 onwards as

compared to other banks and the ratio ranges between 51 per cent to

38 per cent during the period of study.

By comparing the Public Sector Banks with the Private Sector

Banks, it is revealed that Public Sector Banks have been keeping more

Page 26

funds in liquid form during the second phase of the Reform Period than

the Banks in the Private Sector

Table V (14) Liquid Fund to Total Fund Ratio of the Selected Banks

from 1991-92 to 2001-02 (Per cent)

1994-95 : 42.41

1995-96 ' 44.31

AAG Liquid Fund 17.41

Source: Compiled and Computed from Annual Reports of the Selected Banks.

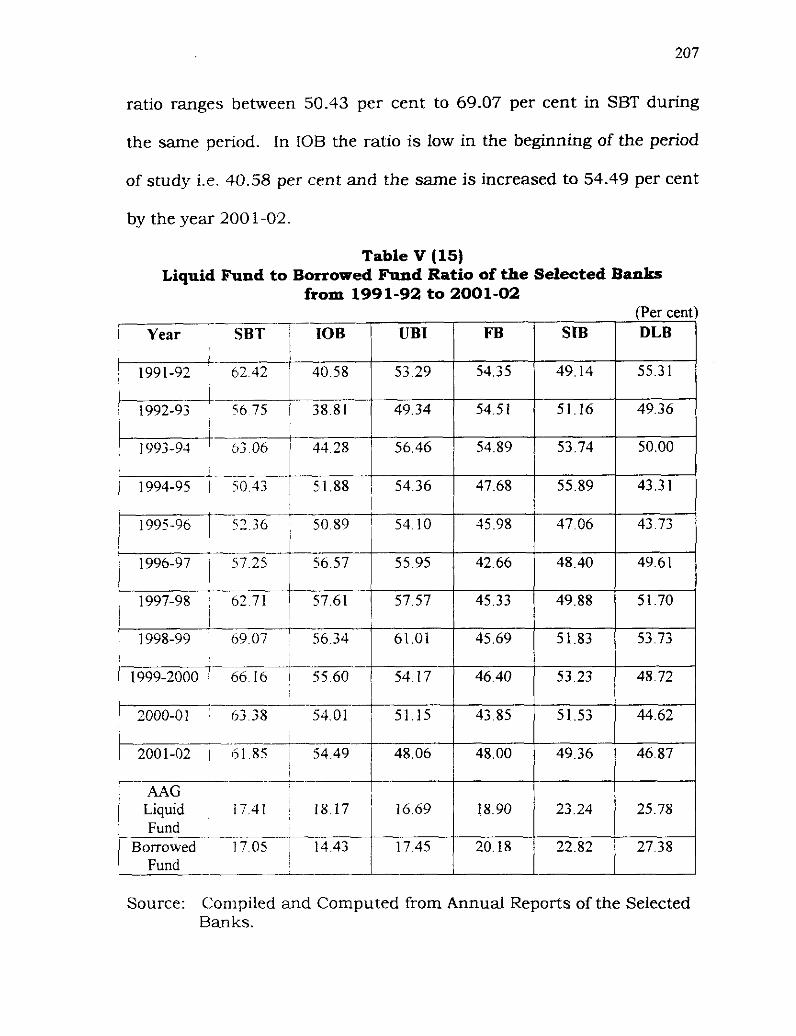

Liquid Fund to Borrowed Fund Ratio

This ratio reveals how much percentage of the borrowed funds is

kept by the banks in liquid assets. SBT keeps more funds in liquid

form as corrlpared to other banks during the period of study and the

Page 27

ratio ranges between 50.43 per cent to 69.07 per cent in SBT during

the same period. In IOR the ratio is low in the beginning of the period

of study i.e. 40.58 per cent and the same is increased to 54.49 per cent

by the year 200 1-02.

Table V (15) Liquid Fund to Borrowed Fund Ratio of the Selected Banks

from 1991-92 to 2001-02 -- (Per cent)

586 75 1 38.81

Source: Compiled and Computed from Annual Reports of the Selected Banks.

Page 28

In UBI, EPB and DL,B, the ratios show a declining trend over the

years where as in SIB the ratio shows a slight increase during the same

period. A s Liquid fund includes Investments, the increase in the ratio

is due to the increase in Investment. The Composition of ~ i q u i d Funds

of the selected banks (Table V (12)) has already revealed this.

Deployment

In case of surplus balance, banks have the option of either

maintaining cash balance or investing these excess funds in securities

or Loan Assets. By holding adequate cash reserve to eliminate

Liquidity Risk and by considering the income forgone while holding

cash balance. banks should make optimum use of its idle funds by

investing in such a way that the ylelds earned are higher. A s the SLR

and CRR have declined sharply during the Post-Reform Period,

especially in the second phase of Reform banks have sufficient funds

with them for deployment. The Advances to Borrowed Fund Ratio and

Investment to Borrowed Fund Ratio of the selected banks will reveal the

deployment pattern of the banks.

Advances to Borrowed Fund Ratio

This ratio shows the percentage of Advances deployed by the

banks out of the Borrowed Funds. In IOB, the Advances to Borrowed

Fund Ratio is high in the year 1991-92 (i.e. 57.42 per cent) as

compared to other banks and by the end of the year 2001-02 the same

reached the lowest position of 44.19 per cent. In all other banks the

ratio has shown an increasing trend over the years. Banks have been

Page 29

able to deploy more funds in Advances due to reduction in SLR and

CRR.

The AAC, of Advances of all other banks except IOB is higher than

the AAG of Borrowed funds during the period of study.

Table V (16)

Advances to Borrowed Fund Ratio of the Selected Banks

from 1991-92 to 2001-02

AAG ! 17.80 11.71 I

19.63 i

23.79 Advances : i

Borrowed 1 17.05 i 14.43 17.45 20.18 22.82 Fund ~

- (Per cent)

Source: Compiled and Computed from Annual Reports of the Selected Banks.

Year SBT T-708 I

SIB LIB1 DLB FB

Page 30

Investment to Borrowed Fund Ratio

Investlr~ent to Bol~owed Fund Ratio reveals the amount deployed

by the banks for Investment out of the Borrowed Funds. The ratios

show a n increasing trend during the period of study in all the selected

banks. In the category of Public Sector Banks, in SBT, IOB and UBI,

the ratios ha.ve increased from 34.42 per cent, 30.77 per cent and

35.97 per cent in 1991.-92 to 47.12 per cent, 43.92 per cent, and 36.46

per cent respectively by the year 2001-02.

Source: Compiled and Computed from Annual Reports of the Selected Banks.

Table V ( 17) Investment to Borrowed Fund Ratio of the Selected Banks

from 1991-92 to 2001-02

UBI

1991-92 34.42 , 30.77 1 35.97

-34 .15 2949 ! 35.15

1993-94 ' 1 1 . 3 7 j 40.33 43.08

FB

29.72

33.15

32.45

35.28

28.90

29.78

35.55

35.79

38.96

37.89

40.65

24.36

I

1 1994-95 1 35 99 ! 36.96 -..A - .

1995-96 1 33.43 i 36.81

36.75

33.81

SIB

31.65

32.3 1

36.20

39.98

31.98

35.99

36.09

35.14

41.05

39.98

34.71

24.80

(Per cent) DLB

30.73

29.18

32.46

29.31

25.22

25.84

31.70

32.50

37.08

34.65

36.68

29.18

36.94

1997-98 43 47 35.56 1 38.07 I

41.09 --

34.50

36.82 1 4 47 12 1 43.12 36.46

27.38

21.49 / 19.16 Investment 1 i Borrowed 1 20.18

18.27

22.82 I

17.45 Fund , I !

Page 31

In the category of Private Sector banks, FB, SIB and DLB have

shown an increase in the ratio, from 29.72 per cent, 31.65 per cent and

30.73 per cent in 1991-92 to 40.65 per cent, 34.71 per cent and 36.68

per cent respectively by the year 2001-02.

The Average Annual Growth of Investment of the selected banks

is more than the Average Annual Growth of Borrowed Funds. In the

Post-Reform Period with the declining Reserve Requirements (in SLR

and CRR), banks have more funds in their hands and have invested

substantial portion of the Borrowed Funds in Investments in the light

of high NPA.

While comparing ,the deployment pattern of the selected banks

during the period of study certain inferences can be drawn.

1. Up to the year 1995-96 the Advances to Borrowed Fund Ratio of

SBT is higher as compared to other banks (Table V (16)). After

1995-96, SBT concentrated more in Investments and the

Investment to Borrowed Fund Ratio of SBT (Table V(17)) is higher

as compared to other banks from 1996-97 to 2001-02.

2. In IOB the Proportion of Advances to Borrowed Fund shows a

dec1inin.g trend during the period of study (Table V (16))

3. During the period of study (i.e. up to 1995-96) the Ratio of

Advancis to Borrowed Fund of UBI (Table V (16)) is low as

compared to other banks where as the proportion of Investment

to Borrowed Fund (Table V (17)) i s higher except in the last three

years than those of the other selected banks.

Page 32

4. After 1095-96 FB has concentrated more on lending and the

Advances to Borrowed Fund Ratio of FB (Table V (16)) is higher

as compared to other banks during the same period.

5 . In SIB the deployment of Borrowed Funds in Investments and

Advances increases proportionately during the period of study.

6 . The Investment to Borrowed Fund Ratio of DLB (Table V (16)) is

low a s compared to other banks during the period of study DLB

is concentrating more on Advances and the AAG of Advances of

DLB is h.igh as compared to that of other selected banks.

Liquidity Risk Management

Ensuring adequate profitability and liquidity are the two

objectives underlying the concept of Asset Liability Management. The

cause and effect of Liquidity Risk are primarily linked to the nature of

the Assets and Liabilities..

Assets commonly considered as liquid like government securities

and other moi~ey market instruments could also become non-liquid

when the market players are unidirectional. Under ALM approach,

liquidity is tracked through maturity or cash flow mismatches. The

maturity profile could be used for measuring the future cash flows of

banks in different time buckets. While the mismatches up to one year

would be relevant since these provide early warning signals of

impending liquidity problems, the main focus should be on the short-

term mismatches because in liquidity management, availability of time

to correct the situation is very important.

Page 33

Table V (1 8) Liquidity Gap Statement of the Selected Banks for March 2000 and March 2001 (Rs. in Crores)

Date / Bank

I -L-

M:rrch2000 SBT ! I

Total outl1ow ( A )

Total Inflow (B)

Mismatch (B-A)

Cumulative Mismatch

Mismatch as a Percent of Outflow Total ournow (A)

Total lnflow (B)

Mismatch (B-A)

Cumulative Mismatch

Mismatch as a I'ercent of Outflow Total Outflow (A)

Total lnflow (B)

Mismatch (B-A)

Cumulative Mismatch

Misrnatcl~ as a Percent orolllllow ... .. . . .~

1-14 6 months 1 year

821.77 563 16 383.09 252.65 ".:.:11 216.95 1 611.86 -704 9 , - 390 .12 I I i 24.86 1 261.81 1 -35205 -1056.11 / -2116.86 I I

1-3 ycaru

5110 20 .. . . .

4413.99

-102621

-3177.07

-18.86

1 1 122 I3

5390 24

-573 I .80

-4998.32

-51.54

13580.81

11140.12

-2440.69

-172.16

-17.07

Total 3-5 ycara

222 15 , 805 20 12434 58 / 0 1 e r 5

>ears

Page 34

- Total Outllo~v (A)

Total lntlow ( U )

Datc

Mismatch (B-A)

Cumulative Mismatch

Bank

Mismatch as a Percent of Outflow Total 011lflow (A)

Total Inflow (B)

Mismatch (B-A)

Cumulative Mismatch

Particuli~rs

Mismatch as a Percent of Outflow Tolal Ot~lflow (A)

1-14 I 15-28 / 29 days-

Total Inflow (B)

Misn~atch (B-A)

3 - 6

Cumulative Mismatch

6 months

Mismatch as a Percent of Outflow

days -

'167 09

207 47

-69 62

-I85 05

-18.97

-- 90.93

90.98

0.05

8.87

0.05

- 45.01

4855

3.54

55.64

7.86

3 months

1094 24

loo') 5')

-24 65

-20') 70

-2.25

I4975

78.23

-7152

62.65

-47.76

294.32

72.72

-221.60

-277.24

-75.2')

months

819.02

484 2 2

-1 34.80

-544 50

-4088

146.34

82.40

-63.94

-126.59

-43.69

142.42

95.55

-46.87

-324.11

-32.01

-1 year

980.83

414 51

-566 32

- I 110 82

-57.74

241.47

124.03

-1 17.44

-244.03

48.64

162.95

84.21

-78.74

-02.85

-48.32

1-3 years

3391.91

2li4')I

-1257 00

-2367 82

-37.06

1056.02

1228 78

172.76

-71.27

16.36

663.40

556.65

-106.75

-509.60

-16.00

3-5 ycars

254.39

080 I I

731.72

-1636 i n

287.64

242.81

787.20

544.39

473.12

224.20

32.86

260.07

227.21

-282.39

691.45

years

1636.10

447.80 I

-473.12

0.00

-27.75

282.30

0.00

281.96

(Contd.. .)

Page 35

Total

. 14482.67

I I I i I I I I I I Mismatch as a Percent I of Outflow Total Ol~lflow iAi

Total Inflow (B)

Mismatch (B-A)

Cumulative Mismatch

Mismatch as a Percent of Outflow Total elfl low (A)

Total Inflow (B)

Mismatch (B-A)

Cumulative Mismatch

Mismatch as a Percent of Outflow

3-5 years

1276.37

1-3 years

6342.71

1 791.63

-484.74

-2474.41

Over 5 years

1688.67

66.24 I 2!.5? 1 -39.54 I 4.66 1 8 1 -17.93 / -37.98 1 I46 53 1

3 - 6 msnths

814 06

29 di~ys - 3 montlls

074.20

Particnlars

~ --

'Toiai inflow (R) I 1 !8!2 I9 1 621.21 1 107 51 1 152 0 2

3630.76

5797 23

2166.47

2166.47

59.67

9846.66

7188.06

-2658.60

-2658.60

-27.00

6 months - 1 year

2085 32

Mismatch (B-A)

1 629 55 1 52054l

1-14 tlilys

~

-1485.77

-852 36

15-28 days

Tol:ll 011lflo!\' (4 ) 1000 09

722.10 1 -1137.31

-1989 67

i I

30294.49

30294.49

I

38977.74

38977.74

1046.93

1129.00

82.07

2248.54

7.84

455.41

400.48

-54.93

-2713.53

-12.06

51 I 2 5

i O 9 . 9 6 - 2 0 6 . 0 1 I 37.96

72210 / 832.06 Cumulative Mismatch

565.45 / 603.41

25x3 42

1483.34

-1 100.08

114846

-42.58

1544.20

2100.12

555.92

-2157.61

36.00

2714.91 1 4213.16

1552.78 ' 4058 55

12947.50

4932.53

-8014.97

-8183.28

-61.90

12720.66

16342.23

3621.57

517.79

28.47

-1 162.13

-13.07

-42.81

1951.70

667.09

-1284.61

-3442.22

-65.82

-154.61

-168.28

-3.67

5028.87

5367.31

338.44

-3103.78

6.73

I

623.15

5292.49

4669.34

-3513.91

749.31

3093.65

1841.71

-1251.94

-734.15

-40.47

2534.66

6048.57

3513.91

0.00

138.63

4336.59

5070.74

734.15

0.00

16.93

Page 36

Date days

Total Inflow (B) 1 9711 61

Mismatch (B-A) 177 45 1 17145 Cumulative Mismatch 1 h4ismatch as a Percent 22.37

2!5&!!~** Tol;~l 011tIlow ( A )

Total Inflow (B) 260.38

Mismatch (B-A) -177.74

Cumulative Mismatch

Mismatch as a Percent -39.75 of Outflow

Total Inflow (B) 112.12

Mismatch (B-A) -21.21 21.21 Cumulative Mismatch

Mismatch as a Percent of Outflow - - - - .

15-28 29 days- 3 - 6 days 3 months months -1 year

-363.36 -4Y0.30 109 1 . Y I

I 1 7 0 3 5 -18anar , I -768.71

years

68.74

0 .00

20.61 / 37529 5470.i*

1661.50 5470 08

1537.25

0.00

342.72

373.78 1717.08

563.07 1717.08

189.29 . 50.64

Source: Compiled and Computed from ALM Reports of the Selected Banks

Page 37

A s per the Prudential Norms set by RBI every bank has to ensure

that the net outgo of funds during the coming 28 days should not

exceed 20 per cent of the total outflow of cash. A huge negative gap in

1-14 days and 15-28 days buckets of liquidity analysis exposes the

liquidity crunch of the banks. The negative gap in other buckets

bevond 28 days also needs effective control. The gap limits will become

the prudential exposure limits for short term, medium term and long-

term scenario.

From the table V (18)) it is revealed that during the year 2000 as

on 3 1 March only The Dhanalakshmi Bank (DB) showed a negative gap

of more than 20 per cent in the gap limit of 1 to 14 days. In FB the

negative Gap in 1 to 14 days and 15 to 28 days buckets is below 20 per

cent i.e. well ~vithin the prudential limit set by RBI. In all other banks

the gap is positive in the time buckets of 1 to 14 days and 15 to 28

days. During the year 200 1 as on 3 1 March, Union Bank of India (UBI)

and the South India Bank (SIB) showed negative mismatch of more

than 20 per cent in the time bucket of 1 to 14 days and 15 to 28 days.

In DLB the gap is negative in 1 to 14 days but below the prescribed

norm of 20 per cent. I n all other banks the gap is positive in the same

bucket. No prudential limit is prescribed by RBI in time buckets for

more than 28 days. Banks are free to set high tolerance level for higher

time buckets. From ciiscussion with the Bank Management of the

selected ban:ks, it is revealed that generally banks keep negative

Page 38

mismatch up to 40 per cent in the time buckets of 29 days to 3 months

and over 3 months and up to 6 months.

From the Ratio Analysis and Liquidity Gap Statement Analysis it

can be inferred that the banks under study are not facing any liquidity

crunch. By k:eeping the idle funds at optimum level, banks have been

able to deploy more funds in Advance and Investment.

Liquidity Risk Management at the Branch Level

The Liquidity Risk Management at the branch level focuses on

the following aspects.

Mismatch at the Branch level

Only 28.3 per cent: of the respondents take into consideration the

maturity of deposits and advances while deploying funds. Majority of

the bank managers (63.4) do not consider the maturity of deposits and

advances while doing business. 8.3 per cent of the bank managers

contacted is of the opinion that it is not possible at the branch level to

consider the matching of Assets and liabilities.

Table V (19)

Loan Portfolio and Maturity of Deposit Match (Per cent)

-- - Yes

Consider matching of Deposits

and Advances at Branch level 28.3

Source: Survey Report

No

63.4

Not possible

8.3

Page 39

Deployment of h d s

The liquidity level .to be maintained by a bank should provide for

deposit withdrawals and accommodate any increase in credit demand.

When the profits are showing increasing growth rates banks would

prefer to maintain tigh~ter liquidity position by utilising the cash

balances for in.vestment or loan disbursals, which will further improve

its profitability levels.

Table V (20)

Preference for Deployment of Funds

1-_.

Source: Survey ~ e ~ o < - I

Opinion ionof Managers

~ e & ; i n ~ more funds in Investment

75 per cent of the managers interviewed, prefer to deploy the

funds for lending purpose. 25 per cent of the managers gave their

opinion that cieploy~ng more funds in Investments will bring better

results to the bank.

Embedded Option Risk

The unpredictability of deposit withdrawals, prepayment of loans,

changes in demand for loan and the uncertainty about volatility in

inter- institutional call and tern-market may lead to great Liquidity

Risk for the banks. Any liquidity problem due to heavy withdrawal of

deposits and pre-payment of loans may force banks to borrow large

Frequency

15

Percentage

25

Page 40

quantum of funds from inter-bank call market at high rates. If such

occurrences are frequent or for a prolonged period, it may seriously

affect the pi-ofitability of the banks. In order to reduce the embedded

option (premature withdrawal of Deposits or closure of Advances)

managers ol'fer different suggestions.

Table V (2 1) Embedded Option Risk

pa Precautions to be taken i

1 'c Commitment charge on Cash Credit 3.40

Per cent

b I

L I Eff'ectiveness.

Source: .s-;vey Report

- -- --

Chang~n_e Penal Interest

Majority of the bank managers (66.60 per cent) opined that by

30 00

persuasion unnecessary withdrawal or closure of funds can be reduced.

30 per cen3t of the managers recommended changing penal interest for

embedded option of customers while 3.4 per cent pointed out the

possibility of imposing commitment charge on Cash Credit not

withdrawn by the borrowers.

86.7 per cent of the respondents do not find any of these

precautions effective while 13.3 per cent are not confident of the

effectiveness of their suggestion.

Page 41

Table V (22) Maturity Pmffle of Foreign Currency Assets and Foreign Currency Liabilities of the Selected Banks for March 2000

and March 2001 (RE. in Lakha) Over 5 years

6 months - 1 year

16540

28-3 months 36707 6260

.- FC A 36251

- 16540 10977

1-3 years

29587

3-6 months

2229 11525

1-14 days

28695 18287

Total

82739 83708

-969 (-1.17%)

Year

2000

T~;;;;I j 10x141 j h312I i 1600x5 138414 10778

3-5 years 15-28 days

15108 1509

Gap

! :(;I3

-- I

Bank

SBT

Particulars

FCA FCL

r Fc:, Gap FC A / UBI FCI. 162961 32723 8 1 2 7 7 5 5 2 56205 7 5

6047 (1.33%) 24781 1

- - , - , - I 8l007 I 4.10XI 1 120577 j 5hh64 1 53660 / 33830 /

17508 5489

890

1127 -

13496

-

I

1

21715 52181

_I ~ , Gap 1 8487(;34.24*?6)

58871

2178 /

2001 Marc11

Soi~rcc:

- ~..

3669

5448

613 11152

29148 6877

82376 42827

79173 1 1763

- 8163 2925

11474 200

1074 1705

5921 1 27918 44634 49867 7330

44465 /

FB

SIB

.~ ~~

DLB

SBT

10B

UBI

FB

SIB

DLB

Stntislicnl

1252 4733

3689

453 42 1

39358 12387

54931 11159

53768 25854

4299 X070

7645 2633

2643 1136

FCA FCL Gap FCA FCL Gap FCA FCL Gap FCA FCL Gap -- FCA FCL Gap FCA FCL A n € !

1074 9796

3351 97

1700 1151

860 18512

30569 66475

56814 55267

123 15061

233 1 2687

3999 2792

- I 17303

15177

699

41689

58638 66636

17180 42658

27092

5106

5888 36917

-3 1029(-526.98) 25162 25258

-96 (-.38%) 3385 4354

-969(-28.62%) 97160 97334

-174 (-O.I8%) - 372790 364832

7958 (2.13%)

594 I 632

and 2000-01

574

11365 9984

428 5 44

16408 16877

71490 73067

~.. ~

842

1309

191 85

11386 992

35533 16998

--

13626 618

4090 188

2146 2189

FCA FCL Gap FCA FCL Gap FCA FCL

12322 3005

T:lblcs rcl;~liag to Batiks in Indi:~ (RBI) 1099-2000

255863 164673

91 190 (35.64%) __ 33279 54398

-2 I I I9 (413.46'%) 25540 243 10

1230 (4.82%) 9862 7822

2040 (20.68%)

35716 26126

Page 42

(c) Foreign Exchange Risk

Banks undertake operations in foreign exchange like accepting

deposits, making loans and advances and quoting prices for foreign

exchange transactions. Dealing in different currencies brings

opportunities as also risks. If the liabilities in one currency exceed the

level of assets in the s a n e currency, then the currency mismatch can

add value or erode value depending upon the currency movements.

The simplest way to avoid Currency Risk (Foreign Exchange Risk) is to

ensure that mismatches, if any, are reduced to zero or near zero.

The maturity profile of Foreign Currency Assets (FCA) and

Foreign Currency Liabilities (FCL) in Table V (22) revealed that in SBT,

IOB and SIB the risk is minimum. The currency mismatch is very high

in FB, followed by UBI and DLB, leading to high risk for the banks.

Table V (23) Computerisation and Awareness of ALM

(Per cent)

/Awarenessof~ tools Yes KO I

-. -- Details Fully computerised

I Partially

computerised

_ _ _ I I 1 Source: Survey Report

& I

60 per cent of the selected branches are fully computerised and

the Branches 1 60

1 Training to Managers I 60

40 per cent of the branches are partially computerised. 92 per cent of

40

40

the managers are aware of the ALM tools and techniques and 38 per

Page 43

cent of the other officers have the awareness of the ALM techniques.

Out of the selected branch managers 60 per cent have attended

training programmes in ALM.

ALM Concept at the Head Office Level

The head office of a bank, whether in the public or private sector,

is the virtual nerve centre that commands and controls the branches.

Strategies and policy level decisions are evolved at the head office and

the feed back after the branch level implementation of such strategies

and policies is collected and analysed by the departments at the head

office of the banks.

On the basis of an Interview Schedule, Structured Interviews

were conducted at the head office level of the banks under study, in

order to evaluate the implementation of ALM strategies. The following

information has been collected and consolidated.

According the RBI norms ALM as a concept has been introduced

in the selected banks in the years 1997, 1998 and 1999. SBT, IOB,

UBI and FB have separate ALM departments while SIB and DLB have

no separate departments for ALM process. In SIB and DLB it is co-

ordinated with the Planning Department of the concerned banks.

Every bank has Asset Lia.bility Committee (ALCo) support group to co-

ordinate Interest Rate Risk, Liquidity Risk and Credit Risk. All the

Assets and Liabilities of the selected banks have been covered under

the ALM system by the year 2000. The primary role of bank branches

in the ALM process is the timely submission of data to the head office.

Page 44

The ALM departments have admitted that in the case of old generation

Private Sector / Public Sector Banks, collection of data from the wide

network of branches spread along the length and breadth of the

country (mostly not fully computerized) has been a great challenge.

The short-term effectiveness of ALM process can be measured by

analysing Net Interest Income (NII) and long-term effect can be

measured by evaluating the Market Value of Equity (MVE). But no

bank has evolved a suitable technique to measure MVE as yet.

In order to quantify the Interest Rate Risk, the banks are

following the simplest method of Maturity Gap. Interest Rate

Sensitivity Statements are being prepared on a monthIy basis to assess

the Interest Rate Risk. Tolerance levels are fued by the banks for

fluctuations in Rate Sensitive Assets and Rate Sensitive Liabilities.

Normally, 25 per cent variation of NII of the previous financial year is

considered as a prudential limit by the banks.

In order to manage the long term Liquidity Risk, banks are

following both Asset Management (Sale of Securities) and Liability

Management (Borrowing funds when the need arises) and to manage

the short tern1 Liquidity banks prefer Cash Flow Approach rather than

Working Fund Approach. To avoid the liquidity crisis banks are

statutorily bound to maintain 5.5 per cent of its NDTL as balance with

RBI. Need based cash holding limits are fued f ~ r individual branches

and adhered to as f a r as possible by Head Offices.

Page 45

For the purpose of measuring the Liquidity Risk, Maturity Gap

method is followed in the banks. For this, banks have been classifying

the oufflows ;and inflows into time buckets as fured by the RBI and

Monthly Liquidity Statements are prepared by the head office of the

banks to measure the Liquidity Risk. RBI has fured tolerance levels in

negative misrriatch in the time buckets of 1 to 14 days and 15 to 28

days a s not more than 20 per cent. From discussion with the bank

officials, it IS revealed that banks have also fured higher tolerance level

in higher maturity buckets in order to analyse the Liquidity Risk i.e.

for 29 days to 3 m0nth.s (40 per cent), over 3 months and up to 6

months (50 per cent) over 6 months and up to one year (50 per cent)

and one year to 3 years (50 per cent).

In order to reduce the impact of embedded option (prepayment of

loans and premature closure of deposits) empirical studies have been

undertaken by the Head Office at their computerized branches. Based

on the behavic~ural pattern and Trend Analysis on historical data, the

Embedded Option Risk is factored in. From discussion with the

officials in the ALM section of the selected banks, it is revealed that as

a precaution for premature closure of deposits, banks are keeping

around 35 per cent of its Net Demand and Time Liabilities (NDTL) as

against the statutory requirement of 25 per cent in SLR securities.

In practice banks are not classifying their Deposits and Advances

on the basis of behavioural pattern. By analysing the behavioural

maturity profil'e banks have found that around 90 per cent of the

Page 46

deposits are renewed on maturity. Eight per cent of Off-balance Sheet

Items are default on due date. The banks under study are in the

piocess of evolving a contingency plan to overcome the specific liquidity

crisis, if any, ;arising due to changes in behavioural pattern of Deposits

and Advances.