20

2

The global FinTech market is huge: according to estimates from the Statista Digital MarketOutlook the transaction value of the global FinTech markets has reached US$2.6 trillion in2016 and will continue to grow to almost US$7 trillion in 2021.

Digital Payments is the biggest segment with US$2.2 trillion transaction value in 2016,leaving Business and Personal Finance far behind. By 2021 however, Personal Finance willhave grown significantly as more people, especially in developing regions like China, willadopt the new technology to gain access to a financial service system previously barred tothem due to their lower income.

This also leads to China being expected to be the biggest FinTech market from 2017 on witha transaction value of nearly US$3 trillion before the U.S. with US$2 trillion in 2021.

Management Summary (1/2)

The Authors

Various parties are supporting the growth of this promising market, and in 2016 the globalFinTech companies were able to attract US$25 billion in funding deals from thousands ofinvestors.

FinTech business models evolve mainly around reducing transaction costs significantly andthus potentially provide financial advantages to all involved parties. They also lower entrybarriers, e.g. in the Wealth Management market where a lot of offers do not require aminimum investment or only a low one or in the CrowdFunding space where people nowcan get funding that they where not able to get before.

Still, most people in the U.S. and Germany do not know what the term “FinTech” is or means,but a high share of people use widespread services like internet payment providers. Thebiggest barrier to adopt some of the new technologies like Mobile Payments are fear offraud and the worry about data security.

Dev worked in various sectors, such asDigital Marketing, FinTech, Insurance andConsumer Goods after completing hisstudies in New Zealand and London.Ksenia studied Finance in Hamburg andEngineering Management in Russia andjoined Statista after several years inconsulting.

Combined they have over 10 yearsexperience as analysts.

We wish you a valuable and insightfulreading experience.Dev Mehta Ksenia Striapunina

3

Financial technology currently looks very promising when bundled with e-Commerce, asAlibaba’s financial products have demonstrated recently. The largest FinTech investmentdeal in 2016 was secured by Alibaba affiliate Ant Financial, which raised US$4.5 billion andhas been valued by investors at US$60 billion.

Key segments of the FinTech market are:› Blockchain technology developing crypto-currencies and instant transaction solutions› Mobile payments rapidly changing the payment instrument landscape› P2P lending improving small business and private financing and operating at a lower cost

than traditional lenders, i.e. banks› Wealth and portfolio management for personal investors with portfolios of all sizes

Major players in the industry, along with Ant Financial in China are U.S. headquarteredcompanies like Robo-Advisors Betterment and Wealthfront, payment providers Venmo andStripe, and various lenders and loan marketplaces like OnDeck, Prosper, Lending Club andSoFi.

The revenue migration from traditional banking institutions to FinTech companies currentlyremains on a modest level, as young companies are still gaining momentum and growingtheir customer base. Nevertheless, FinTech expansion is now supported by major U.S. banksthat have made a strategic decision to incorporate FinTech solutions into their businessmodel as well.

Management Summary (2/2)

4

Banking has traditionally been one of the sectors most resistant to technological disruption.Over the years, the industry had built a robust business model aided by favourableregulations and a general consumer inertia against switching providers. However, thefinancial crisis of 2008 triggered a sudden upsurge in FinTech start-ups across the world.Public anger at the established banking system, stringent regulations imposed on lending inthe post crisis period and complacency by banks, created a conducive environment forFinTech growth.

The term FinTech essentially refers to the disruption caused by the use of technology in thefinancial services industry. Technology focused start-ups are now beginning to offer theproducts and services that were only provided by banks in the past. The last decade haswitnessed the rise of various start-ups that have laid down a strong challenge to the majorglobal banks in various areas including payments, lending, wealth management and retailbanking. Moreover, large technology and e-Commerce companies such as Google, Amazon,Facebook, Apple and Alibaba (GAFAA) are also leveraging their massive reach, technologicalcapabilities and the ability to deliver exceptional customer experience, to break into theFinTech industry.

We consider three major segments within the FinTech market:› Digital Payments› Business Finance› Personal Finance

FinTech disruptors challengetraditional banks

Evolution of FinTech

1: Peer-to-peer

FinTech 3.0FinTech 2.0FinTech 1.0

› Investment and collaboration by banks

› Incubators, accelerators and hackathons

› Regulatory Technology

› InsurTech (Insurance Technology)

› Beginning of interest in cloud, analytics and blockchain

› First wave of start-ups: P2P1 lenders, payment companies, Robo-Advisor

› Threat to banks

› First version of Bitcoin

› No collaboration between banks and start-ups

› Integration of traditional banking and start-ups

› Banking transactions packaged through APIs

› Increased involvement of blockchain technology

› Increased use of cloud based data

2006 2010 2014 2016

2016 2017

2,672

3%15%

93%

8%

15.9%2

5%

89%

2020

2,222

2018

3%

3,184

19%

2021

2%

80%

4,644

78%

3%12%

3,708

4,207

4%4%

85%

17%

2019

82%

5

Digital Payments include payments for consumer products and services which are madeover the internet, mobile payments at Point-of-Sale (POS) via smartphone applications aswell as cross-border Peer-to-Peer transfers between private users.

The following are not included in this segment: transactions between businesses (Business-to-Business payments), bank transfers initiated online (that are not in connection withproducts and services purchased online), and payment transactions at the Point-of-Salewhere mobile card readers (terminals) are used.

Within the Digital Payments segment three types of transactions can be differentiated:› Digital Commerce: Consumer transactions made via the Internet which are directly

related to online shopping for products and services. Online transactions can be madevia various payment methods (credit cards, direct debit, invoice, or online paymentproviders, such as PayPal and AliPay).

› Mobile Payments: Includes transactions at Point-of-Sale that are processed viasmartphone applications (so-called “mobile wallets”). Well-known providers of mobilewallets are ApplePay and Samsung Pay. The payment in this case is made by a contactlessinteraction of the smartphone app with a suitable payment terminal belonging to themerchant.

› P2P Money Transfers: Peer-to-Peer (P2P) money transfers are defined as money transfersmade over the Internet between private individuals. Cross-border payments andremittances are the most relevant segments for the FinTech market.

Digital Payments transaction value will reach US$4,644bn in 2021Digital Payments (1/2)

1: Only includes countries listed in the Digital Market Outlook 2: CAGR: Compound Annual Growth Rate/ average growth rate per year Source: Statista Digital Market Outlook 2016

Global1 transaction value in billion US$

Digital Commerce Mobile Payments P2P Money Transfer

6

By 2021 China leads in Digital Payments transaction value

Top 20 countries: transaction value in billion US$

Digital Payments (2/2)

1: CAGR: Compound Annual Growth Rate/ average growth rate per year Source: Statista Digital Market Outlook 2016

587

646

China 1,546

31

33

204

United Kingdom

153Germany 103

149

United States

Japan

256

1,194

123

37

36

72

29

25

25

Spain

16

15

18

4396

43

15

14

69

Saudi Arabia

Russia

137

64

77

Australia

89

52

51

35

South Korea

45

Netherlands

44

Canada

33

21

Indonesia

36

France

75

India

Brazil

Mexico

Italy

Argentina

Sweden

2016 2021

+10,6% p.a.

+19,8% p.a.

+15,7% p.a.

+20,4% p.a.

+12,1% p.a.

+17,0% p.a.

+16,8% p.a.

+14,8% p.a.

+22,1% p.a.

+21,2% p.a.

+24,8% p.a.

+17,8% p.a.

+13,5% p.a.

+16,1% p.a.

+17,6% p.a.

+11,5% p.a.

+13,1% p.a.

+23,4% p.a.

+11,7% p.a.

+8,7% p.a.

CAGR1 ’16-’21

7

The Business Finance segment refers to digital financial services for business customers. Inview of processing complexity, this market is normally focused on small- and medium-sizedenterprises (SMEs) and freelancers. Bank-independent credit allocation for SMEs throughprivate or institutional investors via online platforms (CrowdLending) is included.

Also included are CrowdInvesting models, which focus particularly on start-ups exchanginginvestment for company shares (“equity-based”), and CrowdFunding solutions that are usedfor non-monetary compensation, for example, product launches, music, art & film financing("reward-based").

Bank financing is not considered, neither are any financial aspects that reach beyond thescope of small and medium-sized enterprises or donation-based crowdfunding models.

CrowdLending Platforms (also: lending-based crowdfunding) enable small and medium-sized enterprises to get loans from single or multiple private and institutional investors viaan online brokering platform. On credit platforms, businesses can obtain small loans up to aset maximum value. As a rule, financing requests are analyzed by the provider via aninternal scoring system and are checked against additional minimum requirements such asturnover. Subsequently these financing requests can be invested in by private andinstitutional investors at an appropriate interest rate determined by the credit rating of thecompany.

Business Finance segment mainly focus on SMEs1 and freelancersBusiness Finance (1/3)

1: small- and medium-sized enterprises 2: Only includes countries listed in the Digital Market Outlook 3: CAGR: Compound Annual Growth Rate/ average growth rate per year Source: Statista Digital Market Outlook 2016

2016 2017

195

3% 4%93%

4%

36.4%3

3%

93%

2020

120

2018

3%

282

3%

2021

3%

93%

565

93%

3% 4%

375

470

3%3%

93%

3%

2019

93%

Global2 transaction value in billion US$

CrowdLending CrowdFunding CrowdInvesting

8

CrowdFunding (also: reward-based crowdfunding) is a financing form independent fromfinancial institutions, location of the campaign creator or investor. Reward-basedcrowdfunding campaigns can be initiated for a wide range of different purposes such asproduct launches, art- and film-financing, scientific research etc. Usually there is a financinggoal defined by funding volume and time to reach this goal for every campaign. Thecampaign creator publishes engaging content (e.g. videos, text) that explains the goal andmotivation of the fundraising. Almost everyone can participate as an investor (prerequisite isonly a valid payment account).

The term CrowdInvesting (also: equity crowdfunding) defines a variety of transactions wherean unspecified number of investors come together in order to invest in a well-definedpurpose. The following segment exclusively considers “equity-based crowdfunding”;investments in equity shares or profit-related returns (for example, royalties or convertibleloans). CrowdFunding has become a popular financing option for startups and is consideredas part of venture capital financing. Well-known platforms in this area are EquityNet,CrowdCube and Seedrs.

China is by far the biggest marketfor Business FinanceBusiness Finance (2/3)

Source: Statista Digital Market Outlook 2016

Regional split: transaction value in billion US$

2021

348

3263

2016

29

157

5 9

2020

8297

1312

2018 2019

287

2017

222

2039

403

2046

United States China Europe

9

U.S. as second biggest market not even ¼ of Chinas size in 2021

Top 20 countries: transaction value in million US$

Business Finance (3/3)

1: CAGR: Compound Annual Growth Rate/ average growth rate per year Source: Statista Digital Market Outlook 2016

10

33

59

184

83

526

37

19

665

909

India

Turkey

South Korea

2,251

United Kingdom

Australia

11,841

1,533

2,239

Germany

Italy

France 5,051

5,441

13,953

Brazil

4,858

305

16,9464,251

United States 81,644

2,011

2,118

1,739

Japan

403,03896,749

881

2,169

South Africa

4,992

Israel

China

251

1,004

54

20

Argentina

397

Mexico

Sweden 1,358

Netherlands

Canada

1,286

1,456

Saudi Arabia

1,382

1,465

20212016

+42,3% p.a.

+90,4% p.a.

+125,2% p.a.

+52,5% p.a.

+104,3% p.a.

+84,6% p.a.

+30,1% p.a.

+20,8% p.a.

+74,0% p.a.

+94,3% p.a.

+83,9% p.a.

+152,7% p.a.

+116,2% p.a.

+149,8% p.a.

+26,7% p.a.

+171,9% p.a.

+33,3% p.a.

+35,9% p.a.

+74,5% p.a.

+51,2% p.a.

CAGR1 ’16-’21

10

Bank-independent distribution of credit between private borrowers and private orinstitutional investors via online marketplaces (so-called online Peer-to-Peer lendingplatforms) are included in the Personal Finance segment. Automated investment services(Robo-Advisors) that enable private investors to align their investment strategy or portfoliousing automated recommendations are also included.

Online marketplaces for classic bank loans or online brokers without automated orrecommendation-based advisory roles are not included in the Personal Finance market.

Marketplace Lending platforms offer private users the option to place requests for loans inan online marketplace to find private investors who would invest at an appropriate interestrate. Portals such as Lending Club, Zopa, auxmoney and Prosper apply a credit score and listthe financial requests by intended purpose before fixing a lending rate. One or moreinvestors can then serve the credit request. Although banks act in co-operation alongsidethe platform providers, the lending is done, in principle, without direct exposure, risk auditsor the formal requirements normally associated with credit lending. This is attractive formany users because the processes are expedited, there is less demanded in terms of theborrower’s creditworthiness and the conditions are often more flexible than with traditionalbank loans. Users are defined in this case as active borrowers on an online platform;applicants or investors who are only partially recorded as users are not included. Theamount of outstanding, short-term installments or consumer loans recognized during theapplicable year is used as a benchmark.

The Robo-Advisors segment contains private asset management providers who offerautomated online portfolios in which private investors can choose investment volumesdepending on their scope and private appetite for risk. Providers such as Wealthfront,Schwab Intelligent Portfolios and Betterment allow private and/or institutional investors toinvest their money (starting at very small amounts) in pre-existing portfolios which areautomatically managed by individually configured algorithms. The advantage of theseservices lie in the passive role of the investor, who may not want or cannot afford, ongoing,personal monitoring of their portfolio development. Such automated investment servicesallow for the possibility of reaching attractive returns with low starting capital and withoutspecific investment know-how, which stands in contrast to classic investments offered bytraditional banks.

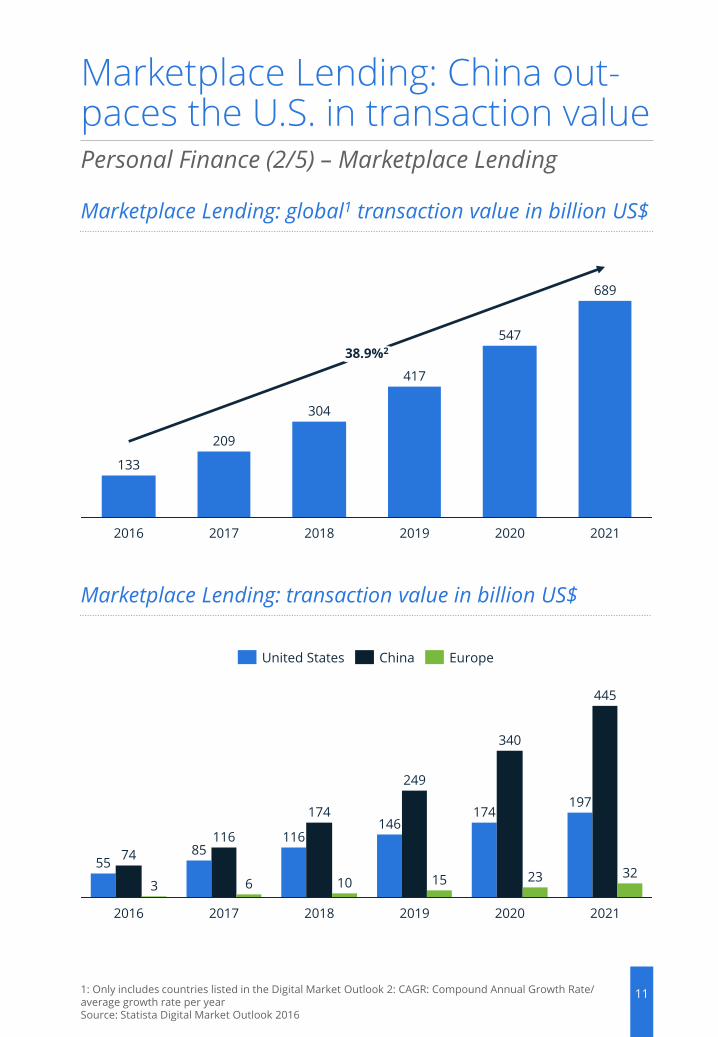

Marketplace Lending grows by almost 40% CAGR1 from 2016 to 2021, reaching a totalglobal2 transaction value of US$689bn. China is expected to be the biggest market withUS$445bn in 2021, followed by the U.S. with almost US$200bn. In all other countriesMarketplace Lending is not expected to be very big. The biggest growth driver is the growingnumber of users as average transaction values grow only by 5% CAGR1 from 2016 to 2021.

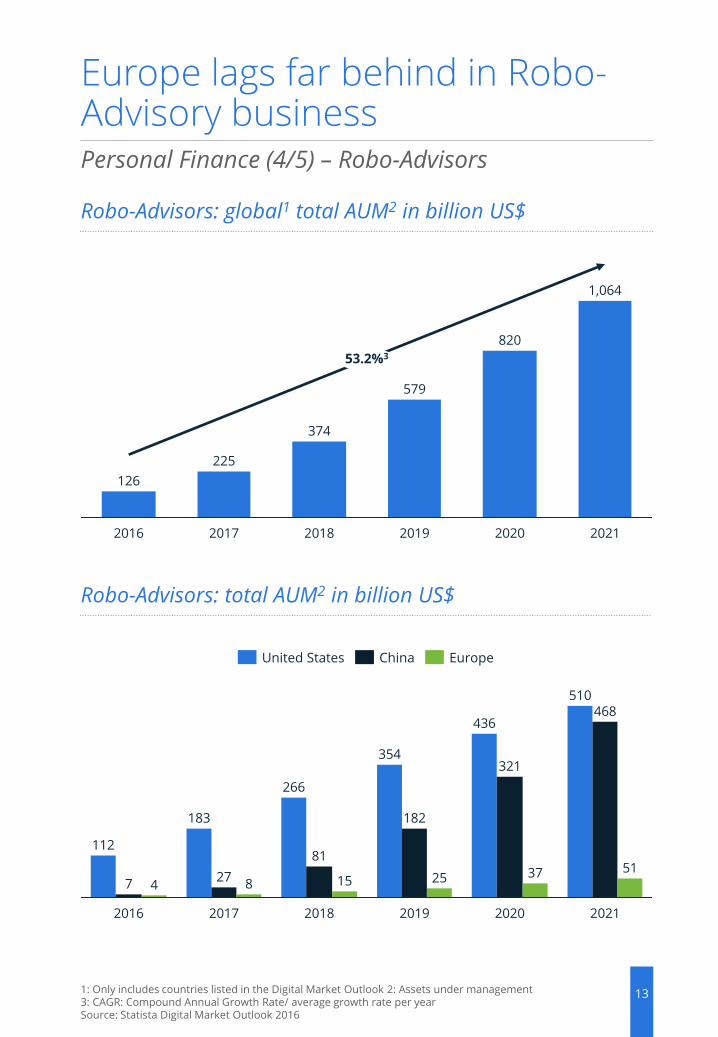

Robo-Advisors are expected to reach US$1064bn assets under management in 2021 whichis more than 50% average growth rate per year. Similar to Marketplace Lending the U.S. andChina are the biggest markets with US$510bn and US$468bn assets under managementrespectively. As users grow with 75% CAGR1 from 2016 to 2021 they drive the growth, whilethe average amount of assets under management shrinks by almost 13% average growthper year. This is due to the fact that early adopters are mostly high net worth individualswith a technical affinity, while mass market adoption especially in China and other lower-income countries drives down average investment sizes.

Personal Finance focuses on lending and investment servicesPersonal Finance (1/5)

1: Compound Annual Growth Rate/ average growth rate per year 2: Only includes countries listed in the Digital Market OutlookSource: Statista Digital Market Outlook 2016

2021

32

445

197

2020

2315

340

174

85

6

116

2016 2018

74

3 10

116

55

146

249

20192017

174

2021

547

304

2018

689

417

2020

38.9%2

20192017

209

133

2016

11

Marketplace Lending: China out-paces the U.S. in transaction value

Marketplace Lending: global1 transaction value in billion US$

Marketplace Lending: transaction value in billion US$

Personal Finance (2/5) – Marketplace Lending

1: Only includes countries listed in the Digital Market Outlook 2: CAGR: Compound Annual Growth Rate/ average growth rate per year Source: Statista Digital Market Outlook 2016

China EuropeUnited States

12

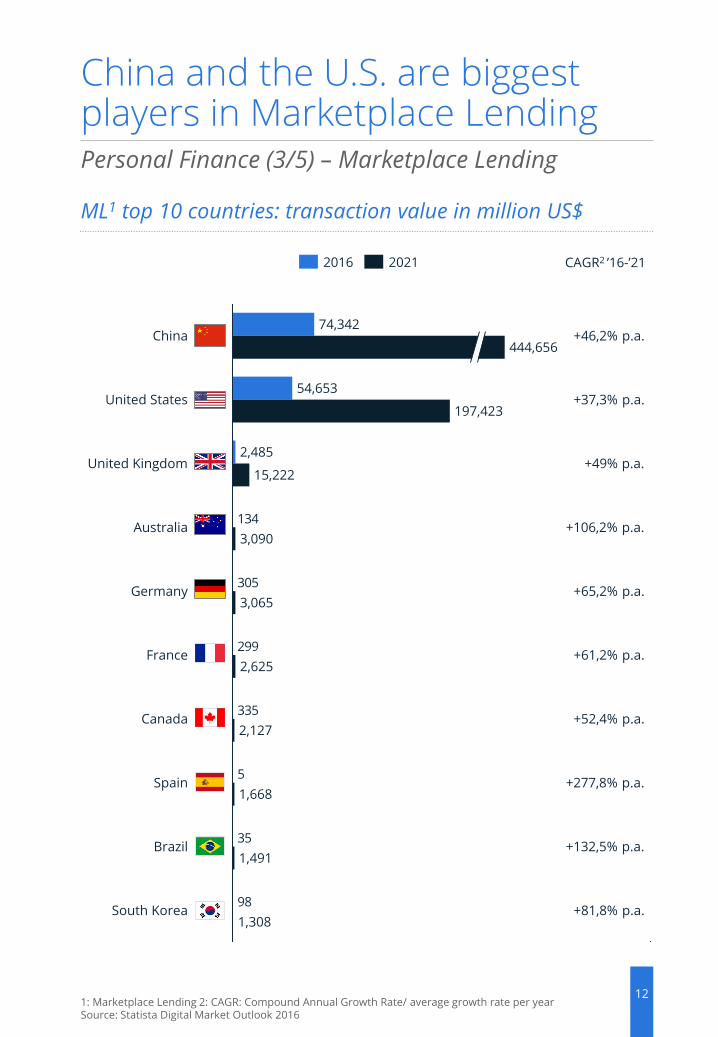

China and the U.S. are biggest players in Marketplace Lending

ML1 top 10 countries: transaction value in million US$

Personal Finance (3/5) – Marketplace Lending

1: Marketplace Lending 2: CAGR: Compound Annual Growth Rate/ average growth rate per year Source: Statista Digital Market Outlook 2016

98

35

5

335

299

305

134

South Korea

2,485

China

1,668

United States 54,653

1,308

3,065

Canada

Australia

France

444,656

Spain

Germany

Brazil

197,423

15,222

3,090

2,127

1,491

United Kingdom

74,342

2,625

2016 2021

+81,8% p.a.

+52,4% p.a.

+49% p.a.

+132,5% p.a.

+61,2% p.a.

+277,8% p.a.

+65,2% p.a.

+106,2% p.a.

+37,3% p.a.

+46,2% p.a.

CAGR2 ’16-’21

2021

51

468510

2020

3725

321

436

183

8

266

2016 2018

7 4 1527

112

354

182

20192017

81

2021

820

374

2018

1,064

579

2020

53.2%3

20192017

225

126

2016

13

Europe lags far behind in Robo-Advisory business

Robo-Advisors: global1 total AUM2 in billion US$

Robo-Advisors: total AUM2 in billion US$

Personal Finance (4/5) – Robo-Advisors

1: Only includes countries listed in the Digital Market Outlook 2: Assets under management 3: CAGR: Compound Annual Growth Rate/ average growth rate per year Source: Statista Digital Market Outlook 2016

China EuropeUnited States

14

Despite China‘s growth U.S. still leading in Robo-Advisors in 2021

RA1 top 10 countries: total AUM2 in million US$

Personal Finance (5/5) – Robo-Advisors

1: Robo-Advisors 2: Assets under management 3: CAGR: Compound Annual Growth Rate/ average growth rate per year Source: Statista Digital Market Outlook 2016

336

191

19

62

511

971

4,796

Germany 1,499

Hong Kong 1,970

Belgium 2,316

Australia

Singapore 6,155

Japan 6,511

1,486

Canada 10,990

United Kingdom 34,980

3,350

China

United States 111,653

6,635

467,831

509,555

2016 2021

+83,9% p.a.

+42,5% p.a.

+66,9% p.a.

+42,9% p.a.

+169,6% p.a.

+74,2% p.a.

+69,2% p.a.

+56,4% p.a.

+139% p.a.

+98,3% p.a.

CAGR3 ’16-’21

Marketplace Lending

15

Most prominent FinTech players can be found in Digital Payments

Digital Payments – representative key players

Business Finance – representative key players

Personal Finance – representative key players

CrowdLending CrowdInvestingCrowdFunding

Robo-Advisors

Mobile PaymentsDigital Commerce P2P Money Transfers

16

An online Statista-Survey from 2016 with 1,003 people in the U.S. and 1,004 people inGermany, shows that almost two thirds of U.S. citizens have not heard of the term FinTechbefore and only 14% have a clear idea of what it is. In Germany this difference is even morepronounced with only 6% having a clear idea of it and 76% that have never heard of FinTech.

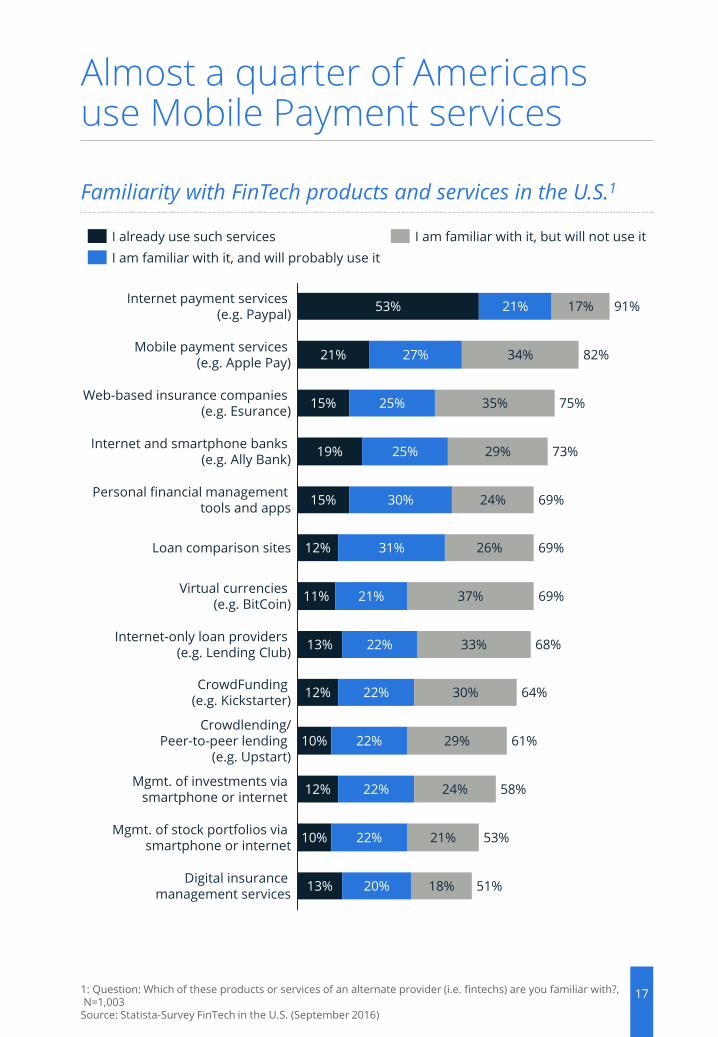

Although a lot of people have not heard of the term “FinTech” before, a lot more knowservices and companies providing FinTech services. 91% of respondents in the U.S. arefamiliar with Internet payment services like PayPal and 82% with Mobile Payment serviceslike Apple Pay. Other FinTech areas like CrowdFunding and –Lending, stock portfoliomanagement or digital insurance management services are less known. In Germany thedifference between familiarity of internet payment services and other FinTech services iseven more pronounced. While 92% are familiar with internet payment services, all otherFinTech products and services are known to less than 64%.

Another interesting difference between the U.S. and Germany is the usage of internetpayment services. While almost the same number of respondents are familiar with theseservices, 64% of Germans use them but only 53% of Americans. This is even more surprisingas the usage of other FinTech products in Germany is well below 10%, while some of themare more commonly used in the U.S., like internet and smartphone banks (44%), investmentmanagement via smartphone or internet (34%) or Mobile Payments (21%).

Awareness of FinTech is low in the U.S., but even lower in Germany

Awareness of the term “FinTech” in the U.S. vs Germany1

1. Question: Have you ever heard of so-called FinTechs before? 2: N=1,003 3: N=1,004Source: Statista-Survey FinTech in the U.S. (September 2016) and in Germany (June 2016)

18%

Never heard of it

23%

14%

76%

6%

63%

Heard of it, and have a clear idea of it

Heard of it, but don’t really know what it is

Germany3U.S.2

17

Almost a quarter of Americans use Mobile Payment services

1: Question: Which of these products or services of an alternate provider (i.e. fintechs) are you familiar with?,N=1,003

Source: Statista-Survey FinTech in the U.S. (September 2016)

Familiarity with FinTech products and services in the U.S.1

24%

21%

31%

Internet and smartphone banks (e.g. Ally Bank)

15%

75%

27% 34%

17%21%

Web-based insurance companies (e.g. Esurance)

25%

22%

26%

15%

58%

73%

12%

29%

82%

30% 69%24%

Internet payment services (e.g. Paypal)

Personal financial management tools and apps

35%

Mobile payment services (e.g. Apple Pay)

19%

91%53%

Mgmt. of investments via smartphone or internet

25%

22%

22%

68%33%

11% 21%

69%

Mgmt. of stock portfolios via smartphone or internet

12%

22%

Virtual currencies (e.g. BitCoin)

51%Digital insurance

management services20% 18%

53%10%

Crowdlending/Peer-to-peer lending

(e.g. Upstart)10% 29%

CrowdFunding (e.g. Kickstarter)

22%

Internet-only loan providers (e.g. Lending Club)

13%

21%

61%

30% 64%

13%

69%37%

Loan comparison sites 12%

I am familiar with it, and will probably use it

I already use such services I am familiar with it, but will not use it

18

In Germany, only internet payment services are widely used

1: Question: Which of these products or services of an alternate provider (i.e. fintechs) are you familiar with?,N=1,004

Source: Statista-Survey FinTech in Germany (June 2016)

Familiarity with FinTech products and services in Germany1

37%

10%

Mgmt. of investments via smartphone or internet

37%26%

Internet and smartphone banks (e.g. Ally Bank)

2%

40%12%

Digital insurance management services

Mgmt. of stock portfolios via smartphone or internet

41%3%

9%

3% 25%

28%

44%3% 12% 29%

Personal financial management tools and apps

49%12% 32%

Crowdlending/Peer-to-peer lending

(e.g. Upstart)54%

3%10%

41%

CrowdFunding (e.g. Kickstarter)

5%

55%4% 14%

Mobile payment services (e.g. Apple Pay)

15%

Internet-only loan providers (e.g. Lending Club)

17%

Loan comparison sites 7%

12%

4% 44%

19%

62%

60%

4% 64%

92%64%

37%

Internet payment services (e.g. Paypal)

60%

7%

14%

39%

63%

Virtual currencies (e.g. BitCoin)

13%

Web-based insurance companies (e.g. Esurance)

4%

37%

16%

48%

I already use such services I am familiar with it, but will not use it

I am familiar with it, and will probably use it

FINTECHStatista Report 2017

FinTech has become an important issue in the financial industry – more and more start-upsare being founded and also big banks increasingly use FinTech products. Most innovations arestill driven by the USA, but China is expected to take the lead in 2017.

Find out how big FinTech is, what business models it involves, what consumers think about itand who the big players in the market are.

Get the report for only $1,950

Market size Business modelsConsumer perspective

Blockchain

Case study: Ant Financial

Company profilesList of US start-ups & banks

in the area of FinTech

Any more questions?Get in touch with us quickly and easily. We are happy to help!

Daven PengCorporate Relations [email protected]

Contact (US) Contact (Europe)

Lodovica BiagiCustomer [email protected]

Released:

ImprintStatista ▪ Johannes-Brahms-Platz 1 ▪ 20355 Hamburg ▪ +49 40 413 49 89 0 ▪ www.statista.com

DisclaimerThis study is based on survey and research data of the previously mentioned sources. The forecasts and marketanalysis presented were researched and prepared by Statista with great care.

For the presented survey data, estimations and forecasts Statista cannot assume any warranty of any kind.Surveys and forecasts contain information not naturally representing a reliable basis for decisions in individualcases and may be in need of further interpretation. Therefore, Statista is not liable for any damage arising fromthe use of statistics and data provided in this report.

June 2017

Dev Mehta has over 10 years of experience working in various capacities forinternational market research, legal and consulting companies. Throughouthis career Dev worked in various sectors such as Defense, Digital Marketing,FinTech, Cards and Payments, Insurance and Consumer Goods.

Dev completed his Post Graduate Diploma from Massey University NewZealand, majoring in Business Management and a Masters in MarketingManagement from Middlesex University, London.

Dev Mehta

Ksenia Striapunina studied Business with focus on Finance in Hamburgand Engineering Management in Perm.

Before joining Statista as an Analyst she gathered experience intelecommunications, working for ER-Telecom and T-SystemsMultimedia Solutions and in financial markets, working as a consultant.

Ksenia Striapunina

Authors, imprint and disclaimer