117

| Date post: | 28-Jul-2016 |

| Category: |

Documents |

| Upload: | c-madhavaiah |

| View: | 36 times |

| Download: | 1 times |

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

CONTENTS

MANAGEMENT TRENDSAn International Bi-Annual Referred Journal of Department of

Business ManagementVol. 10, No. 1-2 June-December - 2013

MANAGEMENT TRENDS

Management Dynamics and Bhagwad Gita 1Nageshwar Rao & Ram Pravesh Rai

A Study of Impact of Strategic CSR as an Integral Tool ForExpanding Rural Markets Through : A Case Study of Hindustan Uniliver Ltd. 19Jayrajsinh D. Jadeja & Kedar Shukla

IFRS and Related Implications 27Daksha Pratapsinh Chauhan

Exploring the Role of Lean Accounting : A Step Ahead from Traditional Costing 34Vineeta Arora & G. Soral

Disclosure Pattern of Valuation Principles of Raw MaterialInventory in Indian manufacturing Industry (Special reference to AS-2) 44Shurveer S. Bhanawat & Abhay Jaroli

Influence of Effectiveness of Leadership on Satisfaction ofLeadership in Public and Private Insurance Sectors 56Dasari Pandurangarao, Gella Sireesha & Devarapalli Rajasekhar

Impact of Brand Association on Soft Drinks Purchase Decision onIndian Consumers 69Syed Irfan Shafi & C. Madhavaiah

Relationship Between Working Capital Management and Profitability :A Case Study 79Shailesh N. Ransariya

Role of Panchayati Raj Institutions in the Rural Development Programme 88Brijendra Pradhan & Amit Singh Rathore

Impact of FII on Indian Stock Market 96Himani Gupta

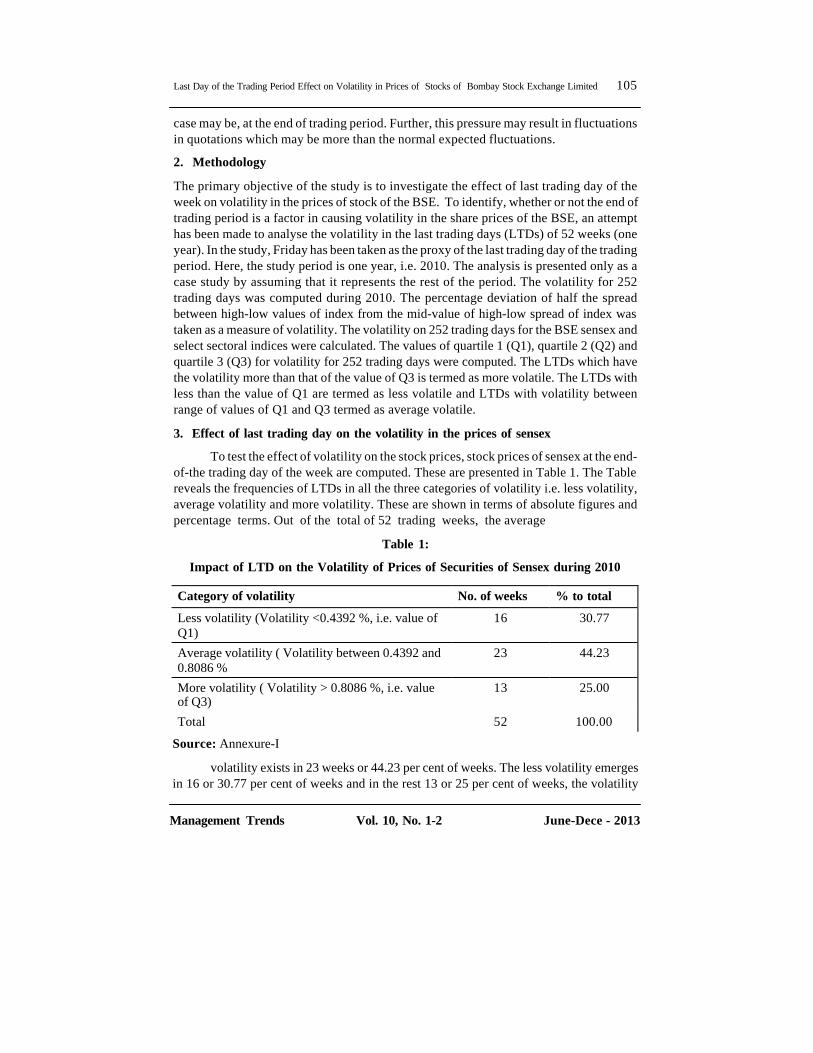

Last Day of the Trading Period Effect on Volatility in Pricesof Stocks of Bombay Stock Exchange Limited 104Venkataramanaih. M

Employee Engagement - A Key to Organizational Success 111Viralkumar Shilu

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

Bhagavad-Gita was written thousands of years ago. It enlightens us on all thefacets of management dynamics leading us towards a harmonious and blissful state ofaffairs in place of the conflict, tensions, poor productivity, and absence of motivation andso on, common in most of Indian enterprises today. In Gita, the process of the ascent ofman from a state of utter dejection, sorrow and total breakdown and hopelessnessto a state of perfect understanding, clarity, renewed strength and triumph is revealed.What makes the Gita a practical psychology of transformation is that it offers us the toolsto connect with our deepest intangible essence, and we must learn to participate in thebattle of life with right knowledge. "Freed from attachment, fear and anger, absorbed inme and taking refuge in me, purified by the penance of knowledge, many have attainedunion with My Being." (Gita 4:10). Effective management is not limited in its applicationonly to business or industrial enterprises but to all organisations where the aim is to reacha given goal through a manager with the help of available physical and human resource.The manager's role can be briefly summed up as:

l Developing vision and enabling & enacting to realise such vision

l Establishing the institutional excellence and building an innovative organisation

Management Dynamics and Bhagwad Gita 1

Management Dynamics and Bhagwad Gita

Nageshwar Rao*

Ram Pravesh Rai**

* Pro-Vice Chancellor, IGNOU, New Delhi** Assistant Professor, School of Journalism Mass Communication and New Media, Central

University of Himachal Pradesh, Dharamshala-, H.P.

Abtract : Bhagavad-Gita was written thousands of yearsago. It enlightens us on all the facets of managementdynamics leading us towards a harmonious and blissful stateof affairs in place of the conflict, tensions, poor productivity,and absence of motivation and so on, common in most ofIndian enterprises today. In Gita, the process of the ascentof man from a state of utter dejection, sorrow and totalbreakdown and hopelessness to a state of perfectunderstanding, clarity, renewed strength and triumph isrevealed. This paper aims to analyse Bhagwat Gita in contextof various facets of management dynamics. More specifically,the paper analyses the issues relating to visionary approach,innovation, mind power, self-management, value orientedwork culture, motivation, leadership etc.

Keywords: Management Dynamics, Bhagwad Gita, India

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

l Developing human resources

l Team building and teamwork

l Delegation, motivation and communicationl Cultivating the art of leadership

l Reviewing performance and taking corrective steps

This paper aims to analyse Bhagwat Gita in context of various facets of managementdynamics. More specifically, the paper analyses the issues relating to visionaryapproach, innovation, mind power, self-management, value oriented work culture,motivation, leadership etc.

Visionary Approach

Vision is a tremendously powerful force in any walk of life, but in business it isessential. A vision is a target towards which leaders aim their energy and resources. Theconstant presence of the vision keeps a leader moving despite various forces ofresistance: fear of failure; emotional hardships, such as negative responses fromsuperiors, peers, or employees; or 'real' hardships, such as practical difficulties orproblems in the industry. Equally important, a vision, when shared by employees, cankeep an entire company moving forward in the face of difficulties, enabling and inspiringleaders and employees alike. Moving toward the same goal, individuals work together ratherthan as disconnected people brought together because of having been hired coincidentallyby the same organization. The Gita gives a 'vision of total life' which is deeper and broaderthan the western concept of vision. Here, Lord Krishna counsels Arjuna on developing abroader 'vision of life' for attaining success and happiness. "The quality of our actions andreactions depend upon our 'vision of life' as envisaged in the Gita. A narrow vision is divisive,a broad vision is expansive, and the supreme vision is all inclusive.

'The Vision of Life' is extensively explained by Lord in Gita. As explained inchapter 18th, the three temperaments (gunas)- Satva, Rajas and Tamas fluctuate and mixin different proportions in our bosom to create differences among individuals in term ofknowledge, karma or works, buddhi or understanding, dhriti or fortitude, and happiness.Now a days ,the vision about Happiness is gaining vital role both for employees andmanagement. Lord enlightens Arjuna with the three types of happiness (good, passionateand dull i.e. sattvic, rajasic and tamasic) in verses. The 'sattvic happiness' is arisingout of the inner self- control and consequent self- perfections which, though painful andarduous in the beginning, is enduring in the long run, in contrast with the fleeting joysprovided by sense tickling. To discuss the different job perspective for the same job andhow the perspective affects the assignment, we may look at a small story. Three stone-cutters were engaged in erecting a temple. The contractor asked them what they weredoing. The response of the three workers to this innocent-looking question is illuminating:

'I am a poor man. I have to maintain my family. I am making a living here,' said thefirst stone-cutter with a dejected face.

2 Nageshwar Rao & Ram Pravesh Rai

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

'Well, I work because I want to show that I am the best stone-cutter in the country,'said the second one with a sense of pride.

'Oh, I want to build the most beautiful temple in the country,' said the third onewith a visionary gleam.

Their jobs were identical but their perspectives were different. What Gita tells usis to develop the visionary perspective in the work we do.The innovation

Today, organizations are witnessing an unsurpassed change in an increasinglyglobal, dynamic and competitive marketplace. Their aim is similar to one another that areachieving sustainable competitive advantage and long-term success over competitors.But the road to reach out there is severe and more than easy to say. In order to be competitivein this dynamic business environment, organizations have to be agile, embrace creativityand innovative. These latter two, creativity and innovation, are the "motto" for everybusiness enterprise today. These are the new management mantras that, as Peter Druckerindicated are critical to growth in a competitive environment without which companiesstall and die. This is the reality of today's relentless business environment. And this realityleads us to most elusive asset of any company, namely the Human Capital.

It is just simply because an organization's creativity and innovation level totallydepend on the potential of their people. This brings an implication for HR professionalsto set their agenda and to design systems for attracting, developing, retaining talentand engaging them towards getting the most of their human capital potential. Itseems that the only way is to nurture organizational learning, teamwork and collectiveintelligence by stimulating free-flow of ideas along with a disciplined and methodicalapproach to continuous improvement. Knowledge and experience are tacit when they arehoused in the minds of the employees. Once the knowledge is written down in some formit is explicit. Structural capital is the ability to convert tacit knowledge into explicitknowledge so that the organization is able to retain knowledge.

Managing the knowledge and talent of human resource in favour of organisation isa great path towards innovation. This concept deals with maximizing the available collectiveknowledge and relevant level of talents in an organization. Thus the emphasis should be onacquiring talents by means of attracting and selecting candidates wisely and retaining themtoo. Managing the talents towards innovation followings may be the common steps:

Planning of talent needs

Selecting the best talents

Boosting up productivity

Motivating themTraining for updating skills and knowledge

Measures to retain them

Developing culture to enjoy talent mobility across the organization etc

Management Dynamics and Bhagwad Gita 3

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

Now it is very clear that this the game of mind power therefore first of all it becomesimportant to understand that the human brain and the mind are not the same things. Boththe mind and mind power are purely a non-physical consciousness (spiritual) that is onlycapable of thought, while the brain is the physical tool that the mind uses to carry out aportion of its intended purpose. The studies have shown that the average person utilizesonly about 10% of their brains capability so, what about the other 90%? The spiritualprinciples say that this 90% can be tamed by Dhyan Yoga and Ananda that is widelydiscussed in Gita. Thus the power of the human mind is unlimited in its potential for anykind of innovation.

It is difficult to derive such kind of formula that defines how innovation takesplace. But on the basis of critical observation the innovation process can be derived as:

EXHIBIT: 1 STEPS IN INNOVATION PROCESS

According to Gita, happiness or enjoying the job is the key factor to create groundfor innovation. By this way it is possible to achieve a life of purpose without much struggleand stress if the perceptions of joy can be developed. By implementing some simpleprinciples, and following proven, time tested strategies to enhance mind function anddevelopment, one finds that one can literally "attract" and "allow" success to flow in.Many scientific studies and experiments have been done on the subject of human mindpower and proved that the ability of mind power to reverse and heal illness and diseasethat the medical community had previously labelled as irreversible has been developedby Spiritual faith and Dhyan Yoga. Would our Creator have provided us with mind powerthat he had no intention for us to use? That is a valid question. It is a simple formula like

4 Nageshwar Rao & Ram Pravesh Rai

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

any other extremely simple things that our Creator has provided us with. Man has convertedthis extremely simple concept into extremely complex because their believes are coveredwith Maya, and so these simple things have become out of reach of the average person,there are proven and simple means of developing the human mind to consciously andconsistently achieve by following the simple rules that our creator has told us to do. Thelessons given by Lord Krishna in the Bhagavad-Gita are the way to achieve self-realizationand to realize the ultimate truth. These are very basic Universal principles (SpiritualLaws) that support and have proven that the average human does have the ability tocreate unlimited mind power. Becoming aware of, and developing the understanding of,exactly how these basic principles operate, are the first steps toward realizing our owntrue potential to do so. Thus, on the basis of principles propounded in Gita the followingformula can be illustrated to develop one's innovative capability:

Knowledge+ Thought+ Vision +Will power+ Happiness + Action = InnovativeCapability

The Mind Power

Wise selection and optimal utilization of resources is the important lesson ofmanagement science. An instance to justify this statement may be seen when just beforethe Mahabharata War, Duryodhana chosen Sri Krishna's large army for his help whileArjuna selected Sri Krishna's wisdom for his support. This episode gives us a clue forbeing an effective manager ? the former chose numbers, the latter, wisdom or mindpower. In the contemporary management scenario, mind power is strategic to managers.It assumed that managers should be strong and mentally fearless, hence, many of themanagement training programme focuses on this. An untrained mind is very weak andunstable, as a result even a small obstacle coming in its way may make it lose initiative.Sri Krishna also mentioned that for one who has conquered the mind, the mind is thebest of friends, but for one who has failed to control their mind, the mind will be thegreatest enemy. In the chariot of the body, the five horses represent the five senses(tongue, eyes, ears, nose and skin). The reins, the driving instrument, symbolize themind, the driver is the intelligence, and the passenger is the self. Managers should usetheir will power and Dhyan to control the mind (the driving instrument), they shouldnot let the mind to be controlled by the senses. Sri Krishna described that from anger,complete delusion arises, and from delusion bewilderment of memory. When memoryis bewildered, intelligence will be lost and when intelligence is lost one falls down(B.G. 2.63).The psychology or sound mental health of human resource is a peculiarfactor of any organisation as well as any human activity. An expert describes soundmental health as that state of mind which can maintain a calm, positive poise or regainit when unsettled in the midst of all the external vagaries of work life and social existence.Now it becomes very important not only for managers but for all of us to develop ourmind power and tackle its impediments to sustain it. The Gita tells us that how theimpediments can be tackled, which can be illustrated as follows:

Management Dynamics and Bhagwad Gita 5

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

EXHIBIT: 2 Monitoring and Controlling the Impediments to Mind Power throughGita's Way

The speed, greed, ambition and competition are the driving forces of today's rat-race environment. This lead to the erosion of one's ethico-moral fibre which supersedesthe value system as a means in the entrepreneurial path like tax evasion, undercutting,spreading canards against the competitors, entrepreneurial spying, instigating industrialstrife in the business rivals' establishments etc. Although these practices are taken asnormal business hazards for achieving progress, they always end up as a pursuit of mirage- the more the needs the more the disappointments.

Gita tells us how to get rid of this universal phenomenon by prescribing thefollowing mantras:

l Cultivate sound philosophy of life

l Identify with inner core of self-sufficiency

l Get out of the habitual mindset towards the pairs of opposites

l Strive for excellence through work is worship.

l Build up an internal integrated reference point to face contrary impulses and emotions

l Pursue ethico-moral rectitude

Cultivating this understanding by a manager would lead him to emancipation fromfalsifying ego-conscious state of confusion and distortion, to a state of pure and free mindi.e. universal, supreme consciousness wherefrom he can prove his effectiveness indischarging whatever duties that have fallen to his domain.

6 Nageshwar Rao & Ram Pravesh Rai

Impediments tomind power

Bhakti Yoga

Peace

Detachment

Satisfaction

Karma Yoga

l Frustrationand anger

l Envy

l Anguishness

l Greed

l Egotism

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

Bhagawan's advice is relevant here:

"tasmaatsarveshukaaleshumamanusmarahyuddha cha"

'Therefore under all circumstances remember me and then fight' (Fight meansperform your duties)

Self-Management

A manager always thinks to play all the roles very effectively but faces someimpediments to be effective in his job. Here, Bhagwat Gita proclaims that 'you should tryto manage yourself'. It means managing the self is very critical. Unless the Managerreaches a level of excellence and effectiveness that sets him apart from the others whomhe is managing, he will be merely a face in the crowd and not an achiever. The despondentposition of Arjuna in the first chapter of the Gita is a typical human situation which maycome in the life of all. Sri Krishna by sheer power of his inspiring words raised the levelof Arjuna's mind from the state of inertia to the state of righteous action, from the state offaithlessness to the state of faith and self-confidence. These are the powerful words ofcourage, of strength, of self-confidence, of faith in one's own infinite resource, of theglory in the life of active people.

When Arjuna got over his despondency and stood ready to fight, Sri Krishna gavehim the gospel for using his spirit of intense action not for his own benefit, not for satisfyinghis own greed and desire, but for using his action for the good of many, with faith in theultimate victory of ethics over unethical actions and truth over untruth. Arjuna respondsby emphatically declaring that all his delusions were removed and that he is ready to dowhat is expected of him in the then situation. Sri Krishna's advice with regard to temporaryfailures in actions is 'No doer of good ever ends in misery'. Every action should produceresults: good action produces good results and evil begets nothing but evil. The Gitafurther explains the theory of "detachment" from the result which enables to analyse thesituation more objectively and accurately and stresses on importance of self-managementor personal management first before managing the others i.e. human resource management(HRM). Self-management includes all aspects of management of oneself such as managinglife, time, stress, anger, fear and self-control etc. In explaining the position of a self-realized person, the Gita stressed the aspects such as controlling the mind, determination,giving up sense gratification, being free from attachment and hatred, body and mindcontrol, power of speech, free from false ego, false pride and anger as essential part ofself-management

Value Oriented Work Culture

Work culture means vigorous and arduous effort in pursuit of a given or chosentask. When Sri Krishna rebukes Arjuna in the strongest words for his unmanliness andimbecility in recoiling from his righteous duty it is nothing but a clarion call for thehighest work culture. Poor work culture is the result of tamoguna overtaking one's mindset.Sri Krishna stinging rebuke is to bring out the temporarily dormant rajoguna in Arjuna.

Management Dynamics and Bhagwad Gita 7

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

The Gita elaborated two types of Work Ethic viz. divine work culture and demonic workculture. Daivi work culture - means fearlessness, purity, self-control, sacrifice,straightforwardness, self-denial, calmness, absence of fault-finding, absence of greed,gentleness, modesty, absence of envy and pride. Asuri work culture - means egoism, delusion,desire-centric, improper performance, work which is not oriented towards service. It is tobe noted that mere work ethic is not enough in as much as a hardened criminal has also avery good work culture. What is needed is a work ethic conditioned by ethics in work.

Often people comment that the central message in Bhagwat Gita is about the notionof karma yoga. It will be very useful to understand how this issue is laid out in the Gita.First of all Lord Krishna establishes a paradigm that there is nothing called "the state ofinaction". He clearly says in chapter 3 that there is nothing likes akarma (no action orinaction). Why did he say that? Because only then we will focus on the issue of how to dowork correctly. It is natural then for us to ask how to do work. He says enjoy completedegree of freedom and total joy while engaging in work. That is the idea. While we are inthe thick of work can we enjoy? Gita emphatically replies in the affirmative. Krishna goesto the extent of saying that with such a perspective to work, we may realize that evenwhen we do a lot of work, we do not feel like indeed engaging in any.

Management is all about doing work, doing it efficiently and ensuring that resultsfollow. Viewed from this perspective, Gita offers counter-intuitive ideas on these issues.The axioms of work have been proposed in Gita is also relevant in modern managementstyle. There are four aspects to this, which is brought out in this famous shloka in Gita:

H$_©Ê`odm{YH$mañVo _m \$cofw H$XmMZ & "Karmanye Vadhikaraste Ma Phaleshu Kadachana,

_m H$_©\$choVw^y©: _m Vo g“moñËdH$_©{U && Ma Karma Phala Hetur Bhurmatey SangostvaAkarmani"

When one is told that he/she has to do the work, he/she does not ask for results orbother about what causes these results, the normal tendency in some cases is to say, "wellin that case, I am not interested in doing the work". The last component takes away thatpossibility. Since in Gita, the notion of non-work or inaction is not a feasible alternative,the last component makes sense. The most difficult part is the second and the thirdcomponent. How can someone do the work and yet not have the right for results? Thisrequires some more articulation and understanding of the idea.

We are told that we need to work for results. Why is then Lord Krishna advocatingthe antithesis of this? In order to get this clear, let us trace some side effects of working forresults. Many of us with some work experience will be able to relate to these side effects:

l Result orientation can make one wary of failures, we may refuse to undertake greatactivities. It is much in news that student ended his life because he did not clear theexam.

l We have a tendency to excessively focus on ends instead of means. This is what mostworking in Multi-National Companies are busy doing. Modern day managers spendsignificant time to manager "performance reports" rather than "performance" itself.

8 Nageshwar Rao & Ram Pravesh Rai

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

l In order to be good in managing the performance report, "process orientation" mustgive way for "result orientation"

l What are results at the end of the day? They are issues of the future about which wespend our time in the present. Therefore, we may tend to escape the dynamics of"present" and go after "future"

The apparent confusion that we have in understanding this shloka is that when wesay you have no right to the results, it merely suggests that take off your pre-occupationwith results and have a process orientation. We have the right to work only but never to itsfruits. Let not the fruits of action are your motive. Nor let our attachment be to inaction.The first half of this verse is a simple factual statement, which each one of us experiencesin the day to day life. One cannot have an absolute authority over the final outcome of anyaction. There is always a possibility of discrepancy between expected result and actualresult. Thus 'Karmanyevadhikaraste' becomes a scientific statement. There is no wonderthat strategic planning methods like 'SWOT Analysis' acknowledge the same scientificfact. SWOT analysis is a strategicplanning method used to evaluate the Strengths,Weaknesses, Opportunities, and Threats involved in a project or in a business venture.Strengths/ Weaknesses are intrinsic characteristics of the business. Opportunities/ Threatsare impacts of external elements.) Lord Krishna propels Arjuna to perform his duties,while staying selflessness to success or failure; not thinking of the fruit of action - once inthe field of activity and relinquishing attachment. He who gives up all desires and movesfree from attachment, egoism and thirst for enjoyment, attains peace which is the mostessential thing in life. When the work perspective developed in our thought with antecedentmind set passes through the pipe line of the karma principle the consequences would bedifferent, this can be illustrated as:

EXHIBIT: 3 Value Oriented Work Culture

Management Dynamics and Bhagwad Gita 9

Ethical values

Cultural Values

Human values

Organisational values

Professional effectiveness

Ethical behaviour

Institutional commitments

Job satisfaction

Inculcation of Karma

o No Expectation of results

o Emphasis on working

o Moral duty o Selfless action

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

This should not be seen as antithesis to Management by Objectives (MBO) andManagement By Results. It tells us that we should build a work culture wherein valuesoccupy an important place. The inculcation of ethical values,cultural values,organisationalvalues and human values in Karma will give effective results.

Motivation

Dedication for work means to 'work for the sake of work'. The Gita tells us not tomortgage the present commitment to an uncertain future. If we are not able to measure upto this height, then surly the fault lies with us and not with the teaching. It has beenpresumed for long that satisfying lower needs of a worker like adequate food, clothingand shelter, recognition, appreciation, status, personality development etc are the keyfactors in the motivational theory of Maslow. It is the common experience that the spiritof grievances from the clerk to the Director is identical and only their scales andcomposition vary. It should have been that once the lower-order needs are more thansatisfied, the Director should have no problem in optimising his contribution to theorganisation. But more often than not, it does not happen like that; the eagle soars highbut keeps its eyes firmly fixed on the dead animal below. On the contrary a lowly paidschool teacher, a self-employed artisan, ordinary artistes demonstrate higher levels ofself- realization despite poor satisfaction of their lower- order needs.

This situation is explained by the theory of Self-transcendence or Self-realisationpropounded in the Gita. Self-transcendence is overcoming insuperable obstacles in one'spath. It involves renouncing egoism, putting others before oneself, team work, dignity,sharing, co-operation, harmony, trust, sacrificing lower needs for higher goals, seeingothers in you and yourself in others etc. The portrait of a self-realising person is that he isa man who aims at his own position and underrates everything else. On the other hand theSelf-transcenders are the visionaries and innovators. Their resolute efforts enable them toachieve the apparently impossible. They overcome all barriers to reach their goal. TheGita further advises to perform action with loving attention to the divine which impliesredirection of the empirical self away from itsegocentric needs, desires, and passions forcreating suitable conditions to perform actions in pursuit of excellence. It is found that allwork irrespective of its nature have to be directed towards a single purpose that is themanifestation of essential divinity in man/woman by working for the good of all beings -lokasangraha. . The same motivation is given by Sri Krishna in the Third Chapter of Gitawhen He says that 'He who shares the wealth generated only after serving the people,through work done as a sacrifice for them, is freed from all the sins. On the contrary thosewho earn wealth only for themselves, eat sins that lead to frustration and failure.'

It is in this light that the counsel 'yoga karmasukausalam' should be understood.Kausalam means skill or method or technique of work which is an indispensable componentof work ethic. Yoga is defined in the Gita itself as 'samatvam yoga uchyate' meaningunchanging equipoise of mind. Tilak tells us that performing actions with the specialdevice of an equable mind is Yoga. By making the equable mind as the bed-rock of allactions Gita evolved the goal of unification of work ethic with ethics in work, for without

10 Nageshwar Rao & Ram Pravesh Rai

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

ethical process no mind can attain equipoise. The principle of reducing our attachment topersonal gains from the work done or controlling the aversion to personal losses enunciatedin Ch.2 Verse 47 of the Gita is the foolproof prescription for attaining equanimity. Thecommon apprehension about this principle that it will lead to lack of incentive for effortand work, striking at the very root of work ethic, is not valid because the advice is to bejudged as relevant to man's overriding quest for true mental happiness. Thus while thecommon place theories on motivation lead us to bondage, the Gita theory takes us tofreedom and real happiness. Is it not what the total quality management (TQM) philosophyis also arguing about? Further, it may be asked, why do we want to take the fixation fromresults and instead concentrate on the work itself? The simple answer to it is that by doingdo it lets you literally "get lost in work". When one gets lost into work, the traditionalbarriers of efficiency and motivation are broken and the individual treads into extraordinaryperformance born out of inspiration. Perhaps, that is how a Nobel Laureate or a greatscientist or a visionary leader would have spent several years of his/her time.

We often say when we do very interesting things in life, "I never knew how timepassed" That is a good indication of our ability to practice Karma Yoga. This is neither anunknown or impossible idea to mankind. Every day we all practice this when we havedeep sleep. We rise from the deep sleep and remark that we had a sound sleep. By thatwhat it means is no matter what sound others made in the vicinity I continued to sleep.Therefore it is hardly surprising that we can draw such alternative ideas and thoughtsfrom Gita. However, in order to benefit from this immensely, in the domain of management,we need to step out of the world of rationality and tread into unknown areas. Perhaps anearest reference to this idea in modern day is "out of the box" thinking or thinking"without" the box. This in itself is a paradigm shift in perception that we need to make inour own mind.

One of the biggest problems that we are facing in our daily life, professional workand personal life is that we don't seem to enjoy what we are doing. There was no wordlike boredom in the dictionary about 400 years - 600 years ago. Today the children say "Iam bored". Young professionals want to adopt the western model of "weekend getaway".We need weekend getaways if work is perceived as drudgery and an avoidable aspect ofour life. Such a perspective can never get the best from work place that modern businessmanagement is worried about. What is this boredom? Why does it happen? Because wedon't enjoy what we are doing, we get bored. The basic tenet of Gita is antithesis to thisidea that work could be drudgery. First understand there is nothing like state of no work.We cannot run away from work as there is nothing called "no work".

Further, if we always calculate the date of promotion or the rate of commissionbefore putting in our efforts, then such work is not detached. It is not "generating excellencefor its own sake" but working only for the extrinsic reward that may (or may not) result.Working only with an eye to the anticipated benefits, means that the quality of performanceof the current job or duty suffers - through mental agitation of anxiety for the future. Infact, the way the world works means that events do not always respond positively to our

Management Dynamics and Bhagwad Gita 11

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

calculations and hence expected fruits may not always be forthcoming. It is also criticisedthat not seeking the business result of work and actions makes one unaccountable. In fact,the Bhagavad-Gita is full of advice on the theory of cause and effect, making the doerresponsible for the consequences of his deeds. While advising detachment from the avariceof selfish gains in discharging one's accepted duty, the Gita does not absolve anybody ofthe consequences arising from discharge of his or her responsibilities. Attachment toperishable gives birth to fear, anger, greed, desire, feeling of "mine" and many othernegative qualities. Renounce attachment by regarding objects for others and for servingothers. Depend only on wisdom (not body, nor intellect), and the dependency on theworld will end. Renouncing attachment is the penance of knowledge, which leads to HisBeing - Truth, Consciousness and Bliss. (B.G.4.10) Thus the best means of effectiveperformance management is the work itself. Attaining this state of mind (called "nishkamakarma ") is the right attitude to work because it prevents the ego, the mind, from dissipationof attention through speculation on future gains or losses.

There have been many studies examining staff motivation and here are few examplesof what commonly employees feel about their motivational needs or factors:

" The working environment - poor or inadequate equipment or work facilities

" Working Conditions - too hot, too cold, no breaks, long hours ,rest etc.

v Social Interaction - isolation, socialisation discouraged etc

v Job Security - redundancies, feeling not part of company etc

v Skill or intellectual use -inability or discouragement to use intellectual or skill

v Promotional prospects and job title - lack of promotion, others promoted but notthem

v Responsibility - not allowed to work off own initiative

v Recognition and appreciation - lack of praise or recognition for achievement

v Trust and respect - treated as a machine

v Participation in decision making - not allowed to get involved with company

v A sense of belonging - Salary - pays poor for job they are doing

v Management issues - conflicts with management, etc

This situation is explained by the theory of self-transcendence propounded in theGita. Self-transcendence involves renouncing egoism, putting others before oneself,emphasizing team work, dignity, co-operation, harmony and trust - and, indeed potentiallysacrificing lower needs for higher goals. "There are signals from inside; there are voicesthat yell out. This is a path, one of the ways that we try to teach self-actualization and thediscovery of self. The discovery of identity comes via the impulse voices, via the abilityto listen to your own guts, and to their reactions and to what is going on inside of you." .

12 Nageshwar Rao & Ram Pravesh Rai

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

The great teachings of "Gita" come into play, these philosophies teach you all about, howyou should do your duty, how you should lead your life etc. These "Gita" teachings weregiven by "Lord Sri Krishna" to his disciple "Arjuna" on the battle field of Kurukshetra inHaryana state of India in ancient times. "Arjuna" was involved in a war against his enemies(some of them his own relatives too) but he refused to do his duty of fighting a righteousbattle as he got infatuated & started thinking of his enemies as his own near & dear ones.He told his master "Lord Sri Krishna" that he is going away from the war & do not wantto fight on the battle field. Arjuna's mentalhealth became weak & he got deeply depressed.To overcome his disciple Arjuna's depression & to motivate him to fight a righteous war,"Lord Sri Krishna" gave the great teachings of "Gita" to his disciple "Arjuna". Afterlistening to all these great teachings, Arjuna's mental health became well & he becamemotivated & energetic to fight the war.

The Bhagavad-Gita was delivered by Sri Krishna to boost Arjuna's declining morale,motivation, confidence to his (Arjuna) intra-personal conflict, which was to fight or notto fight the war at Kurukshestra. Thus the transformation of Arjuna from a self-centred,restless person to a conscious, peaceful person is a case of effective motivation. As shownin the table, the condition of Arjuna before Krishna's voice was

Exhibit: 4 Motivation Process in Gita

Arjuna before Gita's Voice Gita Professes Arjuna after Gita's voice

u Disappointed u Bhakti yoga u Enthusiastic

u Fear of sin u Karma yoga u No fear

u In dilemma u Jnana yoga u Static mind

u Away from duty u Raj yoga u Motivated towards duty

u Unable to think u Wisdom u Increase in ThinkingCapability

u Family attachment u Duty Consciousness u Detached from familybond

u Disturbed Peace u Immortality of soul u Peaceful brain

very critical but the analysis of the individual character of Arjuna reveals thatArjuna was the great warrior and able to face toughest circumstances. But the real timesituation at the battle field made his condition critical and after the Gita process he againbecomes well motivated towards his goal. This instance shows the key role of motivationalfactor. Hence, the Gita is all about motivation process. And the modern managementprinciples also support the importance of motivation as key factor. Now it becomes clearthat whether we acquire power, position, money, good mental and physical health etc, butmotivation is badly required to unite all our inner power and transform our self toenthusiastically face the challenges before us.

Management Dynamics and Bhagwad Gita 13

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

Leadership

The wisdom of the Bhagavad Gita contains many leadership lessons that are similarto contemporary leadership theories and practices. Many contemporary leadership topicssuch as emotional intelligence, situational leadership, character and integrity were alreadydiscussed in the Bhagavad Gita thousands of years ago. These topics were discussed in aphilosophical context, as management science as we know today did not exist then. It isalso intriguing to find other management concepts embedded in the Gita. Thousands ofyears before Frederick W. Taylor defined work and worker, and Peter F. Drucker definedknowledge and knowledge worker, the topics of work and knowledge were already in theBhagavad Gita.. He suggests that the Gita provides advice on mission and core values,the development of new capabilities, the importance of developing business connectionsand communication, and the duty of managers to maintain a purpose-centric perspective."Whatever the excellent and best ones do, the commoners follow," says Sri Krishna in theGita. The visionary leader must be a missionary, extremely practical, intensively dynamicand capable of translating dreams into reality. This dynamism and strength of a true leaderflows from an inspired andspontaneous motivation to help others. "I am the strength ofthose who are devoid of personal desire and attachment. O Arjuna, I am the legitimatedesire in those, who are not opposed to righteousness," says Sri Krishna in the 10thChapter of the Gita.

After hearing 575 verses from Sri Krishna in the Bhagavad-Gita, Arjuna wasmotivated, energized and acted according to Sri Krishna's instruction. This is transformationleadership.It explained - "He (Arjuna) stood steady on the ground with bow and arrow inhand. He lifted his arms ready to fight the war". Sri Krishna demonstrated transformationalleadership qualities in developing and guiding Arjuna to victory in the war. The Gitarepresents the struggles encountered by all humans in everyday activities, including thestruggles of leadership. The Bhagavad Gita provides guidance to modern day leadersregarding important leadership qualities and vision of life which facilitates healthyorganizational behaviour and success.

Management needs those who practise what they preach. This is the leadershipquality prescribed in the Gita. The visionary leader must also be a missionary, extremelypractical, intensively dynamic and capable of translating dreams into reality. This dynamismand strength of a true leader flows from an inspired and spontaneous motivation to helpothers. "I am the strength of those who are devoid of personal desire and attachment. OArjuna, I am the legitimate desire in those, who are not opposed to righteousness" saysSri Krishna . Organizations whose leaders lack vision are doomed to work under theburden of mere tradition. They cannot prosper and grow as they are reduced to keepingthings the way they have always been. For leaders, a vision is not just a dream; it is areality that has yet to come into existence. Vision is palpable to leaders; their confidencein and dedication to vision are so strong they can devote long hours over many years tobring it into being. In this way, a vision acts as a force within, compelling a leader toaction. It gives purpose to a leader. Sensing purpose and commitment creates the power

14 Nageshwar Rao & Ram Pravesh Rai

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

of vision and inspire the leaders to respond and work. Warren Bennis, having spent manyyears working with leaders, concluded "while leaders come in every size, shape, anddisposition--short, tall, neat, sloppy, young, old, male, and female---every leader I talkedwith shared at least one characteristic: a concern with a guiding purpose, an overarchingvision. They were more than goal-directed" (Bennis, 1990). Peter Kreeft says that "to bea leader you have to lead people to a goal worth having-something that's really good andreally there" (Stewart, 1991). That essential "something" is the vision.

The relationship between leadership and the concept of yoga as propounded inGita is established below:

EXHIBIT: 5 LEADERSHIP AND GITA

Management Dynamics and Bhagwad Gita 15

An effective leader is one who judiciously blends knowledge, skills and values.The three types of yoga as propounded by Gita confers the same.This gives the leader notonly the mind power,right attitudeand innovative vision but also it promotes and strengthenshis ability to blend task orientation and people orientation(Managerial Grid)

The results of inner discipline and contemplation bring about tranquillity (prasad)in intellect, and from this tranquillity of the intellect gurgles out the 'happiness', which iscalled 'sattvic happiness'. The 'rajasic happiness' arises only when the sense organs aredirectly in contact with the sense- objects. In the beginning it is quite nectarine and alluring,but it creates in the enjoyer a sense of exhaustion and dissipation in the long run. Thistemporary happiness provided by the sense- objects is termed as the 'rajasic happiness'.In 'tamasic happiness', the permanent ever existing goal of life recedes to the backgroundon account of the non- apprehension of reality (nidra) and this results in simplesensegratifications at the flesh level. These kinds of pursuits incapacitate the intellect tothink out correctly the problems (alasya) that face it and to arrive at a right judgement.When theof the higher in us (pramada). Such a 'happiness', which deludes the soul, bothat the beginning and the end is termed as 'tamasic happiness'.

Values

Skills

Knowledge

ETHICS (Bhakti yoga)

WISDOM (Jnana yoga)

ACTION (Karma

LEADERSHI P

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

Conclusion:

The Bhagavad-Gita was delivered by Sri Krishna to boost Arjuna's declining morale,motivation, confidence to his (Arjuna) intra-personal conflict, which was to fight or not tofight the war at Kurukshestra Sri Krishna gave not only spiritual enlightenment to Arjuna (and to all of us) but also the art of self management, conflict management, stress &, angermanagement, transformational leadership, motivation, goal setting and many others aspectsof management which can be used as a guide to increase our managerial effectiveness.Unlike the western approach to managerial effectiveness, which focuses in exploring theexternal world of matter and energy, the Bhagavad-Gita recommends a managerialeffectiveness approach, which focuses on exploring the inner world of the self.

References:

o Robins, S.P. and Sanghi, S.: 2008, Organizational Behaviour (New Delhi: PearsonsEducation).

o Senge, P.M.: 1990, The Fifth Discipline (New York: Doubleday/Currency).

o Sharma, A. and Talwar, B.: 2004, 'Business excellence enshrined in Vedic (Hindu)philosophy', Singapore

o Management Review, 26(1), 1-19.

o Nutt, P.C. and Backoff, R.W.: 1997, 'Crafting Vision', Journal of Management Inquiry,Dec Issue, 309-14.

o Stewart, T. A.: 1991, "Why Nobody Can Lead America", Fortune, January 14, pp.44-45.

o Snyder, N.H. and Graves, M.: 1994, 'Leadership and vision - importance of goalsand objectives in leadership', Business Horizons

o Geus A. (1997), Till' Livillg Company, Harvard Business School Press

o Ashok, H. and M. Thimmappa. (2006). A Hindu worldview of adult learning in theworkplace.

o Advances in Developing Human Resources, 8(3), 329-336.

o Engardio, P. and J. McGregor. (2006). Karma capitalism. Business Week, October30.

o Greenleaf, R. (2002). Servant leadership: A journey into the nature of legitimatepower. Mahwah, NJ: Paulist Press.

o Harvey, A. (2007). Bhagavad Gita: Annotated and explained. In K. BurroughsBhagavad Gita. Woodstock, VT: Skylight Paths Publishing.

o Hee, C. (2007). A holistic approach to business management: Perspectives from theBhagavad gita. Singapore Management Review, 29(1), 73-84.

16 Nageshwar Rao & Ram Pravesh Rai

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

o Sharma, A. and B. Talwar. Business excellence enshrined in Vedic (Hindu)philosophy. Singapore Management Review, 26(1), 1-19.

o Bhattacharya, K.: 1995, 'Vedanta as Philosophy of Spiritual Life', in K. Sivaraman(ed.), Hindu Spirituality: Vedas Through Vedanta (Motilal Banarsidass, NewDelhi).

o Biberman, J. and M. Whitty: 1997, 'A Post Modern Spiritual Future for Work',Journal of Organizational Change Management 10(2), 130-138.

o Kalra, S. K.: 1997, 'Human Potential Management: Time to Move from Conceptof Human Resource Management', Journal of European Industrial Training 21(5),176-180.

o Kinjerski, V. M. and B. J. Skrypnek: 2004, 'De?ning Spirit at Work: FindingCommon Ground', Journal of Organizational Change Management 17(1), 26-42.

o Mirvis, P. H.: 1997, '''Soul Work'' in Organizations', Organization Science 8(2),193-206.

o Pandey, A. and R. K. Gupta: 2008, 'Spirituality in Management: A Review ofTraditional and Contemporary Thoughts', Global Business Review 8(1), 65-83.

o Woodman, R. W., J. E. Sawyer and R. W. Grif?n: 1993, 'Toward a Theory ofOrganizational Creativity', Academy of Management Review 18(2), 293-322.

o Md Mahbubur Rahim, Mohammad Quaddus and Mohini Singh (2011). GlobalBusiness: Concepts, Methodologies, Tools and Applications (pp. 1548-1561).

o Russon, C. & Russon, K. (2010). How the I Ching or Book of Changes can informwestern notions of theory of change. Journal of Multidisciplinary Evaluation,6(13), 193-199.

o Office of Internal Oversight Services. (2008). Review of results-basedmanagement at the United Nations. A/63/268. New York, NY: UN GeneralAssembly

o Bhagavad--?Gita:History's First Manual on Results--?Based Management CraigRusson International Labour Organization, Journal of Multi DisciplinaryEvaluation Volume 9,Issue 20, 2013

o Balodhi JP, Keshavan MS. Bhagavad Gita and Psychotherapy. Asian J Psychiatry.2011;4:300-2

o Jeste DV, Vahia IV. Comparison of the conceptualization of wisdom in ancientIndian literature with modern views: Focus on Bhagavad Gita. Psychiatry.2008;71:197-209

o Rao AV. The mind in Indian philosophy. Indian J Psychiatry. 2002;44:315-25

o Barlett A. and David,P.: 2000, 'Can Ethical Behaviour really exist in Business?',J ournal of Business Ethics, 23,199-209

Management Dynamics and Bhagwad Gita 17

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

Websites:

o www.sathyasai.org,

o www.en.wikipedia.org

o www.gitapress.org,

o www.vedanta.og,

o www.guruvayur.com

o www.bbt.org

o www.freeworldacademy.com

o www.bhagavad-gita.org

o www.bhagavad-gita.us.

o www.managementparadise.com

18 Nageshwar Rao & Ram Pravesh Rai

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

A Study of Impact of Strategic CSR as an Integral ToolFor Expanding Rural Markets ThroughA Case Study Of Hindustan Uniliver Ltd.

A Study of Impact of Strategic CSR as an Integral Tool For Expanding Rural Markets Through 19

Jayrajsinh D. Jadeja*

Kedar Shukla**

* Dean of Faculty of Management Studies at The M.S.University of Bardoa - VadodaraEmail : [email protected]

** Associate Professor of Marketing Management at GIDC Rofel Business School - VapiEmail : [email protected]

Abstract : Evolving from remaining just charitable orphilanthropic activity, of earlier days Corporate SocialResponsibility (CSR) has been a leading and emergingstrategic management concept of the modern days'management. There are sizable numbers of research papers,which lead to conclude that business organizations involvingin discharging their Social Responsibility and dutiestowards the society, not only helps to the society but it equallybenefits to the their own business organization directly andindirectly in achieving their business units goals. StrategicApproach of CSR advocates the discharge of the CSR in away, which helps the society and increase the "organizations'value" by benefiting in it's operations. During the last decaderesearchers' have attempted to measure the impact of theCSR activities on the various functions of the organizationlike Marketing, Finance , Human Resource, Production etc.Management literature review of the research papers revealsthat in India 'Rural Development' is one of the prime areaof concern for the business having great growth potential ,and many organizations choose the 'Rural Development' astheir area of discharging their CSR. Does a CSR investmentmake any sizable contribution in expanding market also inthe rural area for the organization or the industry? In thepresent research paper researchers' have attempted toanswer this question with the help of secondary data of theorganizations which has invested their CSR funds in to therural development.

Key Words : Corporate Social Responsibility ; RuralMarketing , Brand Image, Ethics

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

(I) Introduction

India's historic freedom struggle was characterized to a great extent by concernfor the problems like mass poverty, protection for farmers, artisans, inflation, the need forindustrialization and reconstruction of entire socio-economic life. During the period ofpost independence the image of Indian business leaders was under the criticism for notbeing sensitive towards the society. The perception of the society for them was of beingcapitalist and adopter of the many unfair practices for increasing profits. On one handthe business was and have been resting on the hoarding black marketing, adulteration,profiteering, unethical practices etc, on the other hand social responsibility concept wasalso emerging during that phase out of all the darkness. Business leaders like Shri. ArvindMafatlal had remarked that "Businessmen and industrialist should discharge their socialresponsibilities on a scale and on such diverse lines that they would go beyond therequirements of various law of the country, it is indeed important that the business growsthe majority of the human being settled at the villages of India, and benefits of the businessmust reach to them."

A group of the business leaders started believing that "The tarnished image of theprivate business can be improved and brightened only if it discharges social responsibilitieshonestly and as a matter of fact a moral duties."

Mid-seventy onwards Social responsibility of business has remained centralbusiness concept among the businessmen, researchers and academicians. With evolutionof business in India, India has turned to one of the fastest growing economy and so as, therole of CSR has also evolved and now it has not remained just a charitable activity of thebusiness but it has turned to the one of the most discussed and debated strategic businessmanagement concept."

In the present research paper , we have tried to understand the impact of strategicCSR on the business organizations' performance , which we have studied through thecase studies of the companies Proctor and Gamble and Hindustan Unilever Ltd.

(II) Research Methodology

For the study of Strategic CSR and it's impact secondary data analysis methodologyhas been used with the descriptive research analysis, Secondary data related to study hasbeen obtained from Hindustan Uniliver Ltd. and the same has been reproduced as a casestudy. It has been attempted to study the scope of strategic CSR and impact measurementthrough the secondary data analysis and descriptive research. Since the same has beenpresented as the case study no hypothesis has been formed.

(III) Review of Literature

(A) Corporate Social Responsibility as Strategic Management Concept.

The understanding of the Corporate Social Responsibility has been evolved withthe time and has widely understood as,

20 Jayrajsinh D. Jadeja & Kedar Shukla

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

Milton Friedman (Friedman, 1970). "There is one and only one social responsibilityof business - to use its resources and engage in activities designed to increase its profitsso long as it stays within the rules of the game, which is to say, engages in open and freecompetition without deception or fraud"

Peter Drucker (1984) , legend of Modern Management , remarked in his paper'The new meaning of corporate social responsibility (1984, California ManagementReview) "Social responsibility is the term used to assert or assign - leadership responsibilityof the businessman with respect to the "culture" of the community. - Responsibility forsocial impacts is a management's responsibility not because it is a social responsibilitybut because it is a Business responsibility."

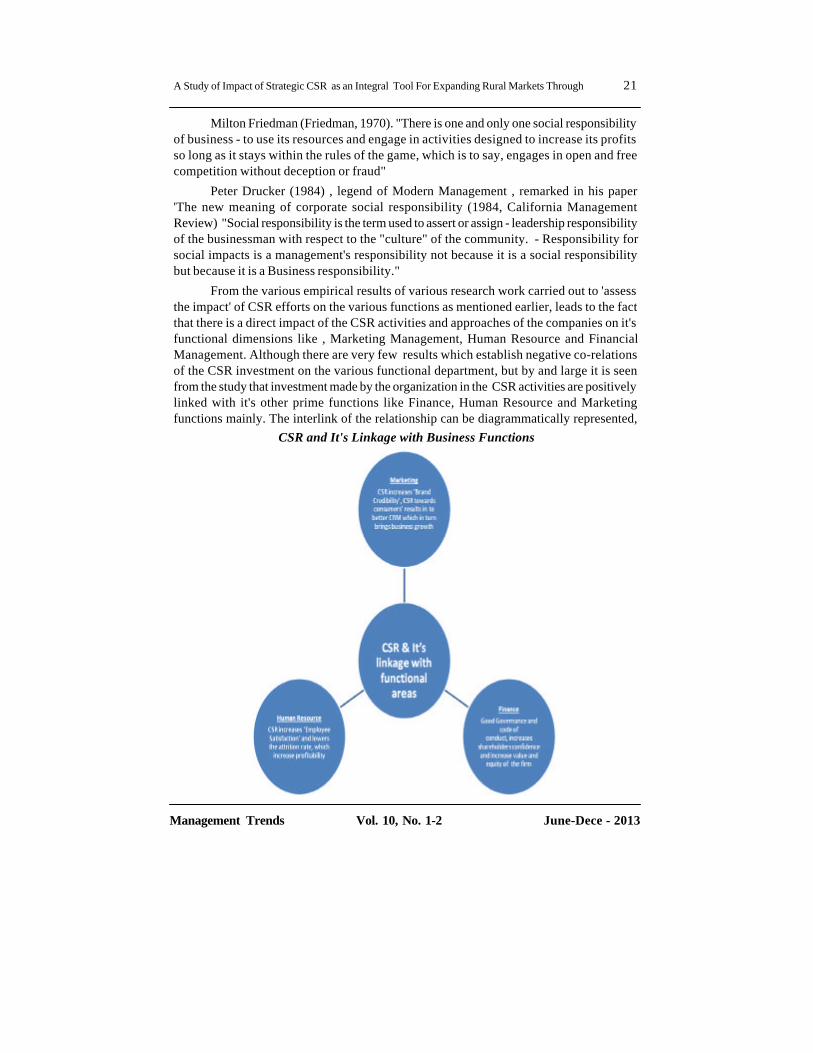

From the various empirical results of various research work carried out to 'assessthe impact' of CSR efforts on the various functions as mentioned earlier, leads to the factthat there is a direct impact of the CSR activities and approaches of the companies on it'sfunctional dimensions like , Marketing Management, Human Resource and FinancialManagement. Although there are very few results which establish negative co-relationsof the CSR investment on the various functional department, but by and large it is seenfrom the study that investment made by the organization in the CSR activities are positivelylinked with it's other prime functions like Finance, Human Resource and Marketingfunctions mainly. The interlink of the relationship can be diagrammatically represented,

CSR and It's Linkage with Business Functions

A Study of Impact of Strategic CSR as an Integral Tool For Expanding Rural Markets Through 21

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

(IV) CSR as Marketing Tool and It's Support in Expansion of Rural Market.

Host of research has been carried out to check the impact of CSR on MarketingFunction , to an extent the CSR efforts of the organization often faced the criticism of justand 'investment for marketing' or 'business investments.' Sighting some of them as,

Holt (1995) , Glazer and Konrad(1996)

Holt founds that consumers product choice sends the social signals regarding theirpersonality attributes, similarly Glazer and Konrad examine the role of social signals inthe realm of charitable behavior. Their model implies that purchasing CSR- Associatedproducts , is a specific method of making charitable donations - should also serve as asocial signal.

Varandarajan and Menon (1998)

They categorize CRM among CSR initiatives that "Do Better by Doing Good." Inother words, CRM not only increases the company's revenues but also contributes tosocietal welfare. They defined CRM as: 'The process of formulating and implementingmarketing activities that are characterized by an offer from the firm to contribute a specifiedamount to a designated cause when customers engage in revenue-providing exchangesthat satisfy organizational and individual objectives.'

Quattrone and Tversky (1984)

On attempt to study on , what specific motivations that drive the decision to purchasea CSR - associated product , they have found out that people often engage in behaviors inorder to signal to themselves that they possess a particular desire trait , even when thereare no social incentives.

Sen and Bhattacharya (2001)

Most companies than ever engage in CSR activities , however the Research by theSen. and Bhattacharya , shows that communicating about CSR activities does notnecessarily results in positive business effect always for the companies. Furthermore, itshows that the companies that are criticized the most in the area of CSR are also the onesthat are the criticized the most. However it is also found in their research that, productswith a CSR-association are extremely popular among the consumers.

However from the presented literature review it is leading to a clear conclusionthat CSR investments and approaches have a direct impact on the 'Marketing Functions'mainly to sump up we can say that,

l CSR investments build the strong and ethical Brand Value of the organizations.

l Specifically in India, though the base of Rural Market is wide enough the contributionin the business in low from the same, therefore many FMCG and Consumer durablecompanies uses corporate social responsibility concept in creating brand awarenessand expanding rural markets.

22 Jayrajsinh D. Jadeja & Kedar Shukla

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

l Consumers are often willing to buy the 'socially responsible products' or 'environmentalfriendly products.'

l Organizations have started diverting or minimizing advertisement expenditure tosocially responsible causes, there are results which favors that the same helps in buildingbrands and results in to higher profitability.

It's undoubted fact that the 'Corporate Social Responsibility' approaches of theorganization as well as , Socially responsible behavior of the 'Corporate' indeed has helpedthe 'brands' in reaching to the rural markets and expanding rural market which has almostsixty percentage of Indian population. As a result of that, not only Corporate SocialResponsibility has not only helped the society but it has also helped the business. Selectexamples of CSR supporting marketing and rural market expansion have been presentedhere in brief.

(IV) CSR of Hindustan Unilever Ltd. And It's Market Impact.

(a) A Case Study of Project Shakti' By Hindustan Uniliver Ltd.

HLL in the year 2001 estimated the rural consumer base for their products as 100million users by, 2005. With a mission of reaching them through the CSR by approachingminimum 100000 villages by the end of the year 2005, through the CSR "Project Shakti "

CSR Project Shakti for HLL as a strategic tool to reach rural consumers

A. PROJECT SHAKTI - Vision : Changing Lives in Rural India ; Mission: Reaching100000 villeges of India to reach 100 million consumers.

Project Shakti is HLL's rural initiative, which targeted small villages with populationof less than

2000 people or less. It seeked to empower underprivileged rural women byproviding income generating opportunities. Project Shakti launched with an aim toimprove the standard of living of the rural community, by providing health and hygieneeducation.

In general, underprivileged rural Indian women were target, who were needing asustainable source of income. Project Shakti has been a pioneering effort in creatinglivelihoods for rural women, organized in Self-Help Groups (SHGs), and improving livingstandards in rural India. Project Shakti has been providing critically needed additionalincome to these women and their families, by equipping and training them to become anextended arm of the company's operation.

Started in 2001, Project Shakti had been extended to more than 30000 villages in196 districts in 11 States during the year 2004, - Andhra Pradesh, Karnataka, Gujarat,Madhya Pradesh, Tamil Nadu, Chattisgarh, Uttar Pradesh, Orissa, Punjab, Rajasthan andMaharashtra. The respective state governments and several NGOs are actively involvedin the initiative.

A Study of Impact of Strategic CSR as an Integral Tool For Expanding Rural Markets Through 23

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

Project Shakti already had over 10,000 women entrepreneurs in its fold by theyear 2004. A typical Shakti entrepreneur earns a sustainable income of about Rs.1,000per month, which is double their average household income. Project Shakti is thus creatingopportunities for rural women to live in improved conditions and with dignity, whileimproving the overall standard of living in their families. In addition, it involves healthand hygiene programmes, which help to improve the standard of living of the ruralcommunity.

The project's ambit already covers about 15 million rural population. Plans arealso being drawn up to bring in partners involved in agriculture, health, insurance andeducation to catalyze overall rural development. Unilever has allied itself with the StateBank of India on a microfinance drive in Maharashtra and Karanataka. The pilot phasehas seen 12 of the Shakti Ammas who sell Unilever's goods act as providers of basicbanking services, and 1,000 accounts have been established thus far.

According to the company, 20% of households from the test regions have signedup, and nearly 80% of participants are women, generally seeking an "accessible" way toenter the category. "The objective is to bring about financial inclusion in rural areas,"Hemant Bakshi, HUL's executive director, sales and customer development. The ultimateintention is to roll out this offering across India in the next 12 months, utilizing some ofthe 43,000 existing Shakti Ammas.

(b) LIFEBUOY SWASTHYA CHETANA -- Health & Hygiene Education

Lifebuoy 'Swasthya Chetana' is the single largest rural health and hygieneeducational programme ever undertaken in India. Its objective was to reach rural consumersfor the lifebuoy soap by educating people about basic hygienic habits. It has beendeveloped around the insight that people mistakenly believe "visible clean is safe clean".The programme established the existence of "invisible germs" and the associated risk ofinfection. In India this is important, because diarrhoea, caused by invisible germs, is thesecond largest cause of death among children below the age of 5.

The campaign has been divided into various phases. In the initial phase, a HealthDevelopment Facilitator (HDF) and an assistant initiates contact and interacts with studentsand influencers of the community, like village community representatives, medicalpractitioners, school teachers etc. A number of tools like a pictorial story in a flip chartformat, a "Glo-germ demonstration", and a quiz with attractive prizes to reinforce themessage are used. The "Glo-Germ demonstration" is a unique tool to make unseen germsvisible and emphasize the need to adopt hygienic practices. The first interaction withstudents is then replicated with the rest of the community.

Started in 2002, the programme covered about 15000 villages in 8 states in it'sfirst phase like -- Uttar Pradesh, Bihar, Jharkhand, West Bengal, Orissa, Madhya Pradesh,Chattisgarh and Maharashtra; and touched about 70 million people, imparting hygieneeducation to over 25 million children.

24 Jayrajsinh D. Jadeja & Kedar Shukla

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

Post floods in Mumbai in 2005 , Hindustan Unilever Ltd took up a CSR task ofdistributing 1.5 Lakhs lifebuoy sops , through UNICEF. It is observed that the good willand brand image earned by the company through this very small investment and socialinitiative was way ahead of 20 sec prime time television advertisement , with a frequencynothing less that 15 times. Product Promotion benefits were derived was surplus.

(c) FAIR & LOVELY FOUNDATION -- Economic Empowerment of Women

The Fair & Lovely Foundation is HLL's initiative which aims at economicempowerment of women across India. It aims to achieve this through providing information,resources, inputs and support in the areas of education, career and enterprise. It specificallytargets women from low income groups in rural as well as urban India. Fair & Lovely, asa brand, stands on the economic empowerment platform and the Foundation is an extensionof this promise. The Foundation has renowned Indian women, from various walks of life,as its advisors. Among them are educationists, NGO activists, physicians. The Foundationis implementing its activities in association with state governments.

In India, low-income families, albeit unwillingly, tend to discriminate against girlchildren, in providing opportunities for education and enterprise, because of resourceconstraints. The support

provided by Fair & Lovely Foundation has been helping girl children availopportunities of higher education and acquire skills in appropriate professions. The seriesof projects that have been drawn up to achieve the vision of empowering women includethe areas of Career guidance , vocational professional trainings and education scholarship.

Launched in 2003, Fair & Lovely Foundation impacted the lives of about 5000women by 2005. And project also created brand awareness of fair and lovely and brandhas been now well recognized and accepted brand in the segment of the cosmetic products.

(IV) Conclusion.

Hindustan Unilever Ltd. Has effectively integrated corporate social responsibilitywith it's marketing function and strategic planning of CSR investment not only helped thesociety in the development but also supported company in reducing it's brand buildingcost through the advertisements and helped in reaching out millions of consumers'specifically in the rural area. Projects like 'Fair and Lovely Foundation' touched to the'emotional esteem' of the rural women and not only helped them in achieving their aspirationof growth but also supported the company in creating it's powerful brand awareness andimpact in the consumers' mind. Fair and Lovely cosmetic products are one of the mostrecognized and sold brand in their product category. It is also important to note here thatthe company has a thoughtful market and consumer analysis of the rural Indian marketand that has been linked to the strategic corporate social responsibility planning, whichproduced effective results as per the companies vision and not only that the, it has pushedcompetitors to copy the strategic move of integrating corporate social responsibility totheir marketing plans.

A Study of Impact of Strategic CSR as an Integral Tool For Expanding Rural Markets Through 25

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

References :

1. Carroll, Archie B. (1991) The Pyramid of Corporate Social Responsibility: Towardthe Moral Management of Organizational Stakeholders, Business Horizons, July-August 1991

2. Drucker, P. F. (1984) 'The new meaning of corporate social responsibility', CaliforniaManagement Review, 26: 2, 53-63.

3. Holt, Douglas B. (1995), "How Consumers Consume: A Typology of ConsumptionPractices," Journal of Consumer Research, 22 (June), 1-16.

4. Varadarajan, R. P., and A. Menon (1988), "Cause-Related Marketing: A Coalignmentof Marketing Strategy and Corporate Philanthropy", Journal of Marketing, 52 (3),58-74.

5. Quattrone, G, A. and Amos T. (1984), "Casual Versus Diagnostic Contingencies:On Self-Deception and on the Voter's Illusion." Journal of Personality and SocialPsychology 46 (February), 237-248.

6. Sen, S., and C. B. Bhattacharya (2001), "Does Doing Good Always Lead to DoingBetter? Consumer Reactions to Corporate Social Responsibility", Journal ofMarketing Research. 38, 225- 243.

7. Website : http://www.hul.co.in/sustainable-living/

26 Jayrajsinh D. Jadeja & Kedar Shukla

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

Abstract : International Financial ReportingStandards (IFRS) are designed as a common global languagefor business affairs so that company accounts areunderstandable and comparable across internationalboundaries. They are a consequence of growing internationalshareholding and trade and are particularly important forcompanies that have dealings in several countries.They areprogressively replacing the many different national accountingstandards. The rules to be followed by accountants to maintainbooks of account which is comparable, understandable,reliable and relevant as per the users internal or external.IFRS began as an attempt to harmonies accounting acrossthe European Union but the value of harmonization quicklymade the concept attractive around the world.

On April 1, 2001, the new IASB took over from theIASC the responsibility for setting International AccountingStandards. During its first meeting the new Board adoptedexisting IAS and Standing Interpretations Committeestandards (SICs). The IASB has continued to developstandards calling the new standards International FinancialReporting Standards (IFRS).

IFRS are used in many parts of the world, includingthe European Union, India, Hong Kong, Australia, Malaysia,Pakistan, and GCC countries, Russia, South Africa, Singaporeand Turkey. As of August 2008, more than 113 countriesaround the world, including all of Europe, currently requireor permit IFRS reporting and 85 require IFRS reporting forall domestic, listed companies, according to the U.S. Securitiesand Exchange Commission.In this paper an attempt have beenmade to review the opinion of practicing charteredaccountants regarding IFRS and related implications. Thepaper recommend the need for developing a sufficientenvironment by the national level body to resolve ambiguityin the adoption and implementation process.Keywords : IFRS, Implications, India

Daksha PratapsinhChauhan*

IFRS and Related Implications

Professor, Head &Dean, Department of Commerce and Business Administration, SaurashtraUniversity, Rajkot - 360005 (India) Email: [email protected]

IFRS and Related Implications 27

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

I. Introduction

Accounting as a "language of business" communicate the financial results andhealth of an enterprise to various interested parties by means of periodical financialstatement like balance sheet, profit and loss account etc. like any other language accountingshould have its grammar and sets of rules of accounting standards. The main aim ofaccounting standard is to provide the standardized the diverse accounting policy so,comparability can be possible with high quality of transparency in accounting practices.

Financial statements prepared in different countries with different rules andregulation. So single set of globally accepted set of accounting standards were demandedfor comparison, analysis and interpretation globally.

The international accounting standard board is working in single set of high quality,understandable, enforceable and globly accepted IFRS. In order to achieve these objectivesthe IASB is coordinating the various stakeholders views on this area.

In this backdrop the ministry of corporate affairs (MCA) GOI set up a high-poweredcore group under the chairmanship of secretary (MCA) to study the impact of IFRSs andto understand the preparedness of the Indian companies for converging with IFRSs. Theroad map towers IFRS convergence for corporate from april1, 2011 has been finalized bythe ministry of corporate affairs in January, 2010.

Convergence also entails maintaining consistency with legal and regulatoryrequirements prevalent in the country. Towards this end, amendments need t be made toexisting laws and regulations, notably the companies act, 1956 provisions and schedulesthat detail the requirements of financial statements need to be harmonized with IFRSrequirements and converged Indian accounting standards need to be notified under section211 (3c) of the said Act. Additionally there are also issues relating to taxation under anIFRS converged environment.

There is also a need to improve awareness in general and build technical competencefor the accounting and auditing profession on IFRS. The ICAI has already included acomparative study of Indian accounting standards with international standards in itssyllabus for CA final advances accountancy and is alsooffering courses and seminars forits members to update them in the field. The RBI too has been holding periodical seminarsand workshops to educate its staff on IFRS provisions.

II. Review of Literature

A number of studies related to the objectives of this research have been publishedin recent years, which shall be considered as follows:

A research paper published by Shailesh.Gandhi, IIM- Ahmadabad, on GAPS inGAAP; issues in non-profit accounting and reporting in India (2005 March). This paperrecommends the need for developing a uniform accounting and reporting system for allNPO. In addition to this need for amendment in various act was recommended. In one of

28 Daksha Pratapsinh Chauhan

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

the speech given by Dr. K.C. Chakrabarty, Deputy governor of RBI at the national seminaron IFRS in Mumbai 11 Feb 2011 has given his view on importance of accounting standard,development of IFRS, lesson from the financial crisis and challenges for the implementationwere discussed. Tokar (2005) focuses on the impact of convergence on auditing firmsand concludes that achieving true convergence of accounting standards is a costly andtime-consuming objective, and will require a huge investment of money and a significantchange in the training of accounting student in near future.Jermakowicz and Gornik-Tomaszewski (2006) argue that the complexity of IFRS, coupled with the lack of guidanceand of a uniform interpretation, can hinder the transition to IFRS. In addition, Jermakowiczand Gornik-Tomaszewski (2006) provide evidence which indicates that many companieswould have not adopted IFRS if it were not mandatory. Ilse Maria Beuren, Nelson Hein,Roberto Carlos Klann (2008) analyzed the impact of differences between the InternationalFinancial Reporting Standards (IFRS) and Generally Accepted Accounting Principles inthe United States (US GAAP) in the economic-financial indicators of Englishcompanies.According to Karamanis and Papadakis (2008) Greek accountants and auditorsbelieve that the introduction of IFRS will improve the quality of the financial statementsprepared by Greek firms. In particular, they believe that the implementation of IFRSimproves the understandability, relevance, reliability and comparability of financialstatements. On the other hand, the respondents in the survey expressed some concernsregarding the difficulties they face when they implement IFRS.Susana Callao, CristinaFerrer, Jose I.Jarne, Jose A. Lainez (2009) discovered the quantitative impact ofInternational Financial Reporting Standards (IFRS) on financial reporting of Europeancountries and evaluates if this impact is connected with the traditional accounting systemin which each country is classified, either the Anglo-Saxon or the continental-Europeanaccounting system.Robyn Pilcher, Graeme Dean (2009) determined the impact financialreporting obligations and, in particular, the International Financial Reporting Standards(IFRS) have on local government management decision making, In turn, this will lead toobservations and conclusions regarding the research question: "Dose reporting under theIFRS regime add value to the management of local government?"Alfred Wagenhofer(2009) analyzed the challenges that arise from political influences and from the pressureto sustain a successful path in the development of standards. It considers two strategiesfor future growth which the International Accounting Standard Board (IASB) follows:the work on fundamental issues and diversification to private entities.Rudy A. Jacob,Christan N. Madu (2009) examined the academic literature on the quality of InternationalFinancial Reporting Standards (IFRS), formerly International Accounting Standards (IAS),which are poised to be the universal accounting language to be adopted by all companiesregardless of their place of domicile.John Goodwin, Kamran Ahemed (2010) examinedthe impact of Australian equivalents to international financial reporting standards (A-IFRS) on the accounts of small-, medium- and larger sized firms.Dennis W. Taylor (2010)compared the costs to financial statement prepares of making the transition to InternationalFinancial Reporting Standards (IFRS) relative to the benefits to financial statement usersfrom receiving "higher quality" IFRS-based information (measured as incremental value-

IFRS and Related Implications 29

Management Trends Vol. 10, No. 1-2 June-Dece - 2013

relevance for listed companies in the UK, Hong Kong and Singapore). These countrieshad different approaches to harmonization leading up to IFRS adoption.Graeme Wines,RonDagwell, Carolyn Windsor (2011) crirically examined the change in accounting treatmentfor goodwill pursuant to International Financial Reporting Standards (IFRS) by referenceto the Australian reporting regime.