76

Managerial Accounting 2nd Edition J. O'Callaghan

Managerial Accounting2nd Edition

J. O'Callaghan

Managerial Accounting

by:J. O'Callaghan

Copyright © 2002 John Wiley & Sons, Inc. All rights reserved.

John Wiley & Sons, Inc.New York

0471413658

Due to electronic permissions issues, some material may have been removed from this chapter,though reference to it may occur in the text. The University of Phoenix has determined that thecontent presented herein satisfies the requirements for this course.

ii

Table of Contents

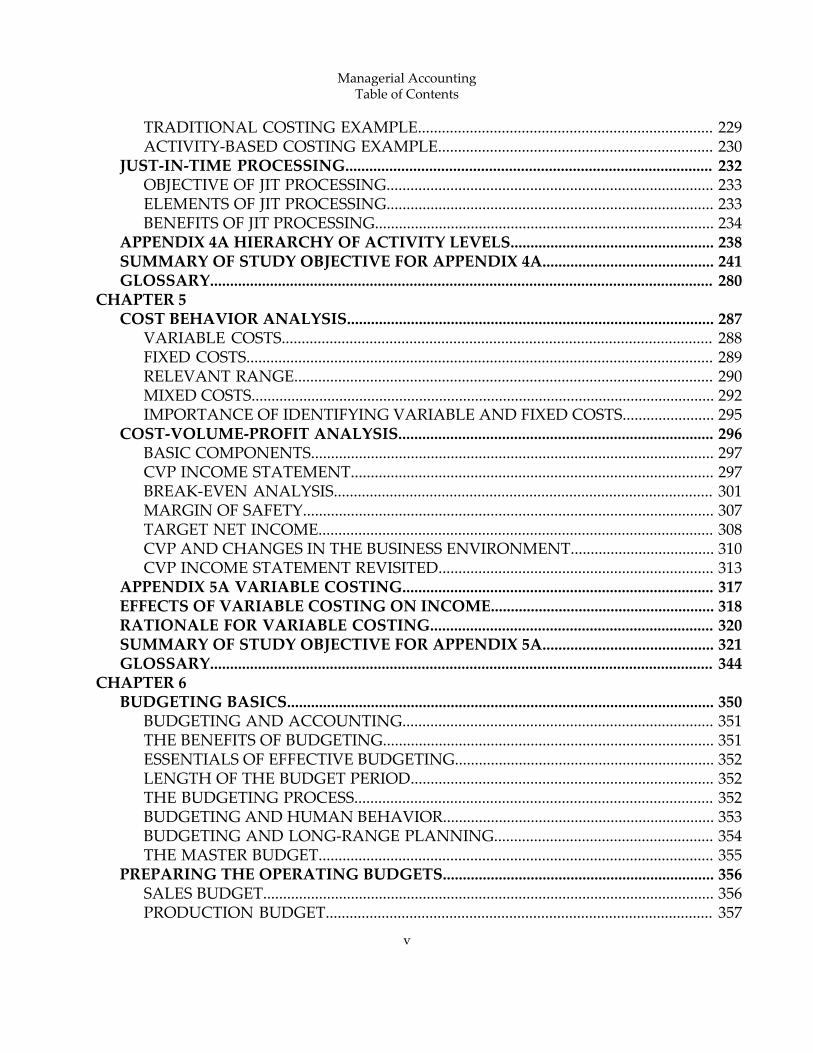

CHAPTER 1MANAGERIAL ACCOUNTING BASICS............................................................................. 5

COMPARING MANAGERIAL AND FINANCIAL ACCOUNTING........................... 6ETHICAL STANDARDS FOR MANAGERIAL ACCOUNTANTS............................... 7MANAGEMENT FUNCTIONS........................................................................................... 7

MANAGERIAL COST CONCEPTS....................................................................................... 9MANUFACTURING COSTS............................................................................................... 9PRODUCT VERSUS PERIOD COSTS............................................................................... 11

MANUFACTURING COSTS IN FINANCIAL STATEMENTS..................................... 13INCOME STATEMENT...................................................................................................... 13BALANCE SHEET............................................................................................................... 16COST CONCEPTS‐A REVIEW.......................................................................................... 18

CONTEMPORARY DEVELOPMENTS IN MANAGERIAL ACCOUNTING............. 20SERVICE INDUSTRY TRENDS......................................................................................... 20VALUE CHAIN MANAGEMENT.................................................................................... 22

APPENDIX 1A ACCOUNTING CYCLE FOR A MANUFACTURING COMPANY... 27WORK SHEET........................................................................................................................... 28CLOSING ENTRIES................................................................................................................ 30SUMMARY OF STUDY OBJECTIVE FOR APPENDIX 1A............................................. 32GLOSSARYū 67

CHAPTER 2COST ACCOUNTING SYSTEMS......................................................................................... 72

JOB ORDER COST SYSTEM.............................................................................................. 73PROCESS COST SYSTEM................................................................................................... 73

JOB ORDER COST FLOW...................................................................................................... 75ACCUMULATING MANUFACTURING COSTS.......................................................... 76ASSIGNING MANUFACTURING COSTS TO WORK IN PROCESS......................... 78ASSIGNING COSTS TO FINISHED GOODS.................................................................. 89ASSIGNING COSTS TO COST OF GOODS SOLD........................................................ 90SUMMARY OF JOB ORDER COST FLOWS.................................................................... 90

REPORTING JOB COST DATA............................................................................................ 92UNDER‐ OR OVERAPPLIED MANUFACTURING OVERHEAD................................ 93

INTERIM BALANCES........................................................................................................ 93YEAR‐END BALANCE....................................................................................................... 94

GLOSSARY.............................................................................................................................. 130CHAPTER 3

THE NATURE OF PROCESS COST SYSTEMS............................................................... 136USES OF PROCESS COST SYSTEMS............................................................................. 136

Managerial AccountingTable of Contents

iii

SIMILARITIES AND DIFFERENCES BETWEEN JOB ORDER COST AND PROCESSCOST SYSTEMS................................................................................................................. 138PROCESS COST FLOW.................................................................................................... 140ASSIGNMENT OF MANUFACTURING COSTS—JOURNAL ENTRIES................ 140

EQUIVALENT UNITS........................................................................................................... 145WEIGHTED‐AVERAGE METHOD................................................................................ 145REFINEMENTS ON THE WEIGHTED‐AVERAGE METHOD.................................. 146PRODUCTION COST REPORT....................................................................................... 148

COMPREHENSIVE EXAMPLE OF PROCESS COSTING............................................. 149COMPUTE THE PHYSICAL UNIT FLOW (STEP 1).................................................... 149COMPUTE EQUIVALENT UNITS OF PRODUCTION (STEP 2).............................. 150COMPUTE UNIT PRODUCTION COSTS (STEP 3)..................................................... 151PREPARE A COST RECONCILIATION SCHEDULE (STEP 4)................................. 152PREPARING THE PRODUCTION COST REPORT..................................................... 153

FINAL COMMENTS.............................................................................................................. 155APPENDIX 3A FIFO METHOD........................................................................................... 162EQUIVALENT UNITS UNDERFIFO................................................................................. 162

ILLUSTRATION................................................................................................................. 163COMPREHENSIVE EXAMPLE........................................................................................... 164

COMPUTE THE PHYSICAL UNIT FLOW (STEP 1).................................................... 165COMPUTE EQUIVALENT UNITS OF PRODUCTION (STEP 2).............................. 166COMPUTE UNIT PRODUCTION COSTS (STEP 3)..................................................... 167PREPARE A COST RECONCILIATION SCHEDULE (STEP 4)................................. 168PREPARING THE PRODUCTION COST REPORT..................................................... 169

FIFO AND WEIGHTED‐AVERAGE................................................................................... 171SUMMARY OF STUDY OBJECTIVE FOR APPENDIX 3A........................................... 171GLOSSARY.............................................................................................................................. 207

CHAPTER 4ACTIVITY‐BASED COSTING VERSUS TRADITIONAL COSTING........................ 213

TRADITIONAL COSTING SYSTEMS............................................................................ 213THE NEED FOR A NEW COSTING SYSTEM.............................................................. 214ACTIVITY‐BASED COSTING.......................................................................................... 215

ILLUSTRATION OF TRADITIONAL COSTING VERSUS ABC................................ 217UNIT COSTS UNDER TRADITIONAL COSTING...................................................... 217UNIT COSTS UNDER ABC.............................................................................................. 217COMPARING UNIT COSTS............................................................................................ 221

ACTIVITY‐BASED COSTING: A CLOSER LOOK......................................................... 224BENEFITS OF ABC............................................................................................................ 224LIMITATIONS OF ABC.................................................................................................... 225WHEN TO SWITCH TO ABC.......................................................................................... 226VALUE‐ADDED VERSUS NONVALUE‐ADDED ACTIVITIES................................ 226

ACTIVITY‐BASED COSTING IN SERVICE INDUSTRIES......................................... 228

Managerial AccountingTable of Contents

iv

TRADITIONAL COSTING EXAMPLE.......................................................................... 229ACTIVITY‐BASED COSTING EXAMPLE..................................................................... 230

JUST‐IN‐TIME PROCESSING............................................................................................ 232OBJECTIVE OF JIT PROCESSING.................................................................................. 233ELEMENTS OF JIT PROCESSING.................................................................................. 233BENEFITS OF JIT PROCESSING..................................................................................... 234

APPENDIX 4A HIERARCHY OF ACTIVITY LEVELS................................................... 238SUMMARY OF STUDY OBJECTIVE FOR APPENDIX 4A........................................... 241GLOSSARY.............................................................................................................................. 280

CHAPTER 5COST BEHAVIOR ANALYSIS............................................................................................ 287

VARIABLE COSTS............................................................................................................ 288FIXED COSTS..................................................................................................................... 289RELEVANT RANGE......................................................................................................... 290MIXED COSTS.................................................................................................................... 292IMPORTANCE OF IDENTIFYING VARIABLE AND FIXED COSTS....................... 295

COST‐VOLUME‐PROFIT ANALYSIS............................................................................... 296BASIC COMPONENTS..................................................................................................... 297CVP INCOME STATEMENT........................................................................................... 297BREAK‐EVEN ANALYSIS............................................................................................... 301MARGIN OF SAFETY....................................................................................................... 307TARGET NET INCOME................................................................................................... 308CVP AND CHANGES IN THE BUSINESS ENVIRONMENT.................................... 310CVP INCOME STATEMENT REVISITED..................................................................... 313

APPENDIX 5A VARIABLE COSTING.............................................................................. 317EFFECTS OF VARIABLE COSTING ON INCOME........................................................ 318RATIONALE FOR VARIABLE COSTING....................................................................... 320SUMMARY OF STUDY OBJECTIVE FOR APPENDIX 5A........................................... 321GLOSSARY.............................................................................................................................. 344

CHAPTER 6BUDGETING BASICS........................................................................................................... 350

BUDGETING AND ACCOUNTING.............................................................................. 351THE BENEFITS OF BUDGETING................................................................................... 351ESSENTIALS OF EFFECTIVE BUDGETING................................................................. 352LENGTH OF THE BUDGET PERIOD............................................................................ 352THE BUDGETING PROCESS.......................................................................................... 352BUDGETING AND HUMAN BEHAVIOR.................................................................... 353BUDGETING AND LONG‐RANGE PLANNING....................................................... 354THE MASTER BUDGET................................................................................................... 355

PREPARING THE OPERATING BUDGETS.................................................................... 356SALES BUDGET................................................................................................................. 356PRODUCTION BUDGET................................................................................................. 357

Managerial AccountingTable of Contents

v

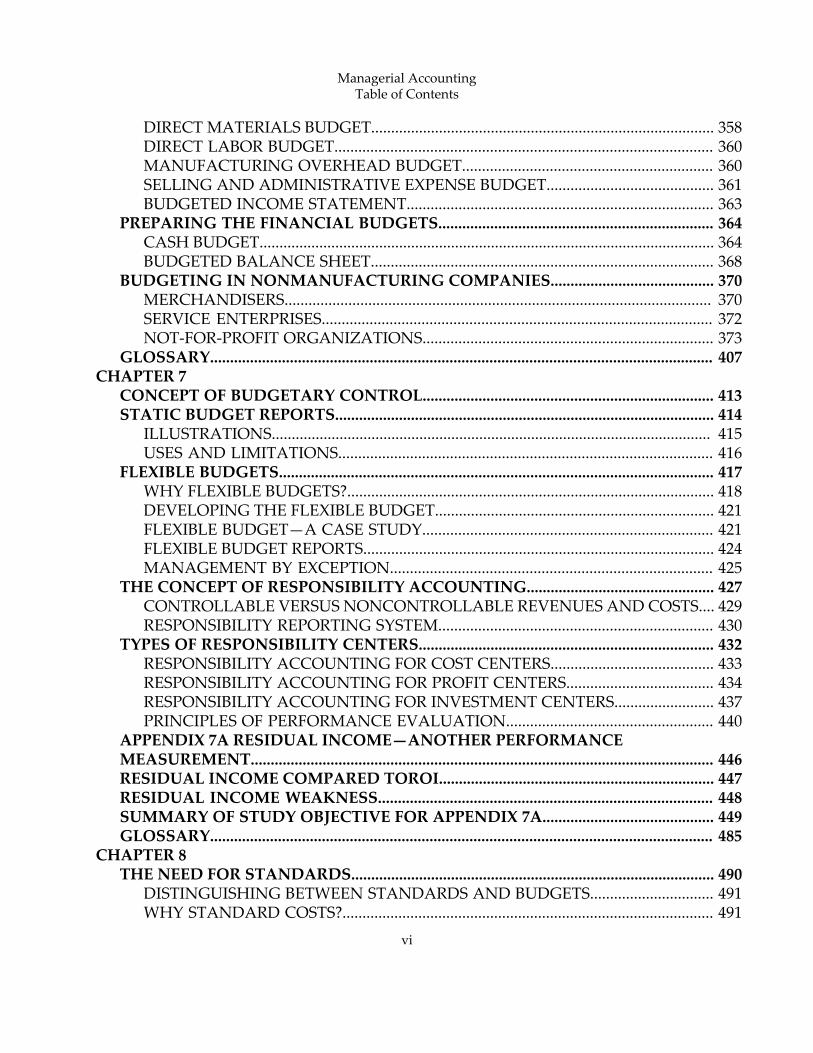

DIRECT MATERIALS BUDGET...................................................................................... 358DIRECT LABOR BUDGET............................................................................................... 360MANUFACTURING OVERHEAD BUDGET............................................................... 360SELLING AND ADMINISTRATIVE EXPENSE BUDGET.......................................... 361BUDGETED INCOME STATEMENT............................................................................. 363

PREPARING THE FINANCIAL BUDGETS..................................................................... 364CASH BUDGET.................................................................................................................. 364BUDGETED BALANCE SHEET...................................................................................... 368

BUDGETING IN NONMANUFACTURING COMPANIES......................................... 370MERCHANDISERS........................................................................................................... 370SERVICE ENTERPRISES.................................................................................................. 372NOT‐FOR‐PROFIT ORGANIZATIONS......................................................................... 373

GLOSSARY.............................................................................................................................. 407CHAPTER 7

CONCEPT OF BUDGETARY CONTROL......................................................................... 413STATIC BUDGET REPORTS............................................................................................... 414

ILLUSTRATIONS.............................................................................................................. 415USES AND LIMITATIONS.............................................................................................. 416

FLEXIBLE BUDGETS............................................................................................................. 417WHY FLEXIBLE BUDGETS?............................................................................................ 418DEVELOPING THE FLEXIBLE BUDGET...................................................................... 421FLEXIBLE BUDGET—A CASE STUDY......................................................................... 421FLEXIBLE BUDGET REPORTS........................................................................................ 424MANAGEMENT BY EXCEPTION................................................................................. 425

THE CONCEPT OF RESPONSIBILITY ACCOUNTING............................................... 427CONTROLLABLE VERSUS NONCONTROLLABLE REVENUES AND COSTS.... 429RESPONSIBILITY REPORTING SYSTEM..................................................................... 430

TYPES OF RESPONSIBILITY CENTERS.......................................................................... 432RESPONSIBILITY ACCOUNTING FOR COST CENTERS......................................... 433RESPONSIBILITY ACCOUNTING FOR PROFIT CENTERS..................................... 434RESPONSIBILITY ACCOUNTING FOR INVESTMENT CENTERS......................... 437PRINCIPLES OF PERFORMANCE EVALUATION.................................................... 440

APPENDIX 7A RESIDUAL INCOME—ANOTHER PERFORMANCEMEASUREMENT.................................................................................................................... 446RESIDUAL INCOME COMPARED TOROI..................................................................... 447RESIDUAL INCOME WEAKNESS.................................................................................... 448SUMMARY OF STUDY OBJECTIVE FOR APPENDIX 7A........................................... 449GLOSSARY.............................................................................................................................. 485

CHAPTER 8THE NEED FOR STANDARDS........................................................................................... 490

DISTINGUISHING BETWEEN STANDARDS AND BUDGETS............................... 491WHY STANDARD COSTS?............................................................................................. 491

Managerial AccountingTable of Contents

vi

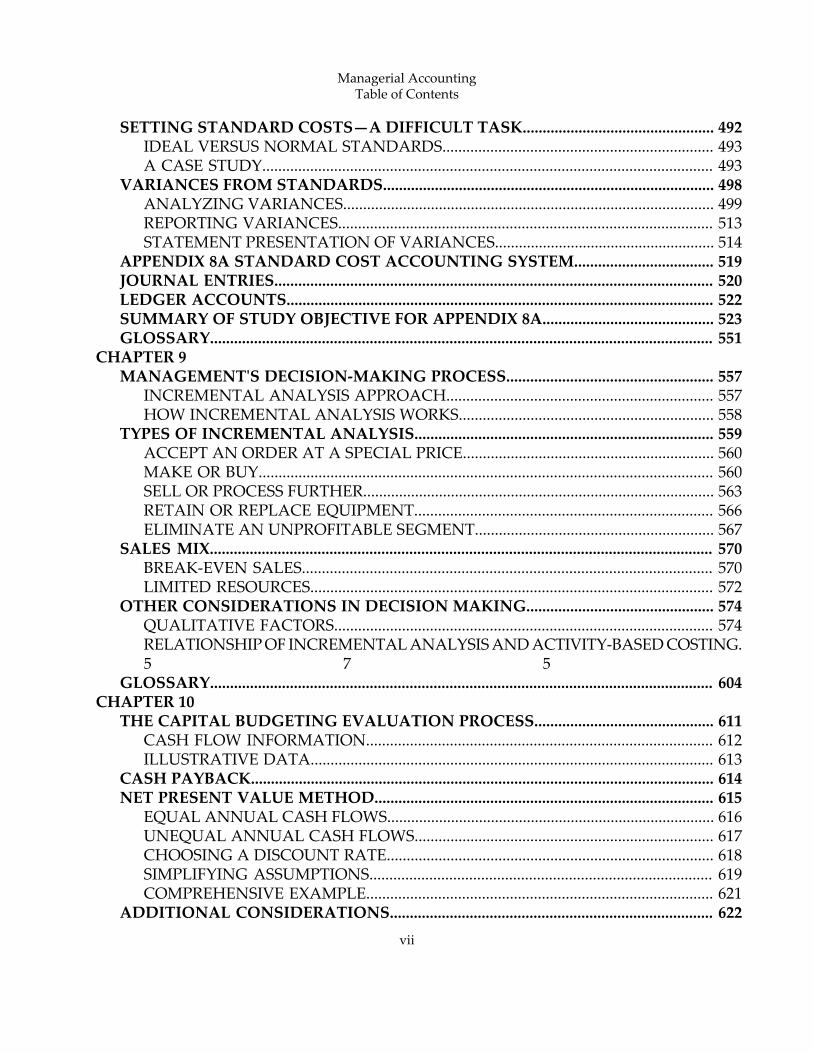

SETTING STANDARD COSTS—A DIFFICULT TASK................................................ 492IDEAL VERSUS NORMAL STANDARDS.................................................................... 493A CASE STUDY................................................................................................................. 493

VARIANCES FROM STANDARDS................................................................................... 498ANALYZING VARIANCES............................................................................................. 499REPORTING VARIANCES.............................................................................................. 513STATEMENT PRESENTATION OF VARIANCES....................................................... 514

APPENDIX 8A STANDARD COST ACCOUNTING SYSTEM................................... 519JOURNAL ENTRIES.............................................................................................................. 520LEDGER ACCOUNTS........................................................................................................... 522SUMMARY OF STUDY OBJECTIVE FOR APPENDIX 8A........................................... 523GLOSSARY.............................................................................................................................. 551

CHAPTER 9MANAGEMENT'S DECISION‐MAKING PROCESS.................................................... 557

INCREMENTAL ANALYSIS APPROACH................................................................... 557HOW INCREMENTAL ANALYSIS WORKS................................................................ 558

TYPES OF INCREMENTAL ANALYSIS........................................................................... 559ACCEPT AN ORDER AT A SPECIAL PRICE............................................................... 560MAKE OR BUY.................................................................................................................. 560SELL OR PROCESS FURTHER........................................................................................ 563RETAIN OR REPLACE EQUIPMENT........................................................................... 566ELIMINATE AN UNPROFITABLE SEGMENT............................................................ 567

SALES MIX.............................................................................................................................. 570BREAK‐EVEN SALES....................................................................................................... 570LIMITED RESOURCES..................................................................................................... 572

OTHER CONSIDERATIONS IN DECISION MAKING............................................... 574QUALITATIVE FACTORS............................................................................................... 574RELATIONSHIP OF INCREMENTAL ANALYSIS AND ACTIVITY‐BASED COSTING.5 7 5

GLOSSARY.............................................................................................................................. 604CHAPTER 10

THE CAPITAL BUDGETING EVALUATION PROCESS............................................. 611CASH FLOW INFORMATION....................................................................................... 612ILLUSTRATIVE DATA..................................................................................................... 613

CASH PAYBACK.................................................................................................................... 614NET PRESENT VALUE METHOD..................................................................................... 615

EQUAL ANNUAL CASH FLOWS.................................................................................. 616UNEQUAL ANNUAL CASH FLOWS........................................................................... 617CHOOSING A DISCOUNT RATE.................................................................................. 618SIMPLIFYING ASSUMPTIONS...................................................................................... 619COMPREHENSIVE EXAMPLE....................................................................................... 621

ADDITIONAL CONSIDERATIONS................................................................................. 622

Managerial AccountingTable of Contents

vii

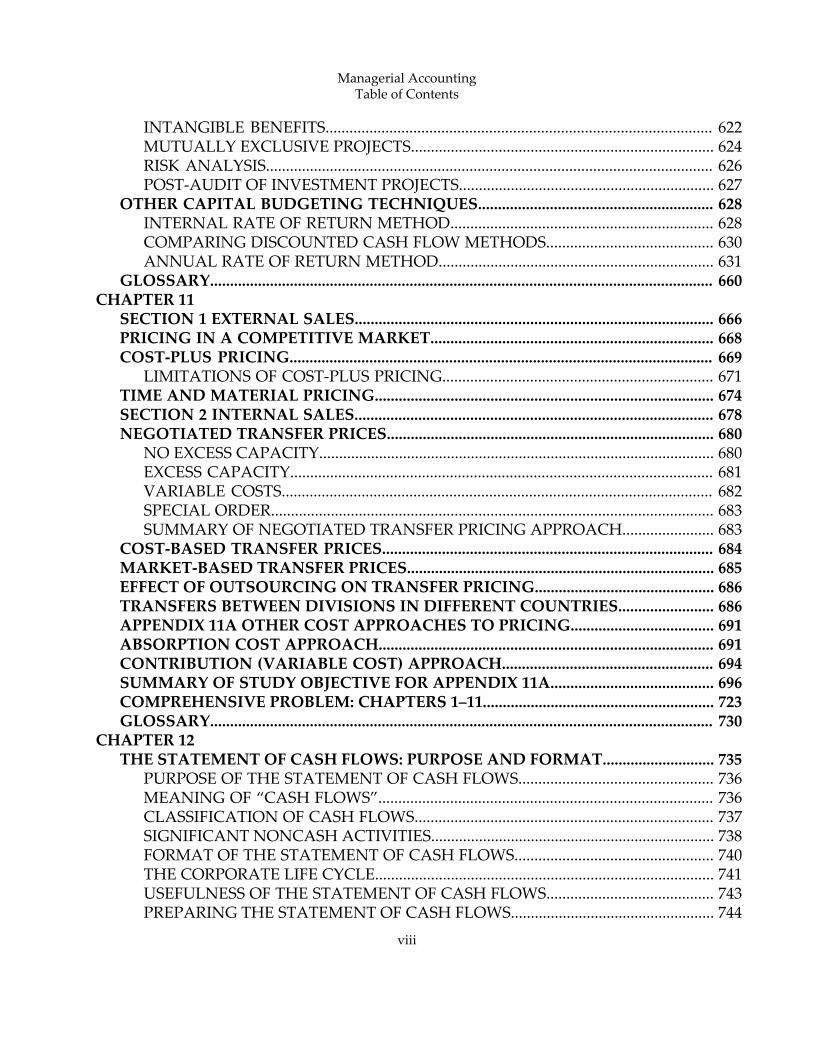

INTANGIBLE BENEFITS................................................................................................. 622MUTUALLY EXCLUSIVE PROJECTS............................................................................ 624RISK ANALYSIS................................................................................................................ 626POST‐AUDIT OF INVESTMENT PROJECTS................................................................ 627

OTHER CAPITAL BUDGETING TECHNIQUES........................................................... 628INTERNAL RATE OF RETURN METHOD.................................................................. 628COMPARING DISCOUNTED CASH FLOW METHODS.......................................... 630ANNUAL RATE OF RETURN METHOD..................................................................... 631

GLOSSARY.............................................................................................................................. 660CHAPTER 11

SECTION 1 EXTERNAL SALES.......................................................................................... 666PRICING IN A COMPETITIVE MARKET....................................................................... 668COST‐PLUS PRICING.......................................................................................................... 669

LIMITATIONS OF COST‐PLUS PRICING.................................................................... 671TIME AND MATERIAL PRICING..................................................................................... 674SECTION 2 INTERNAL SALES.......................................................................................... 678NEGOTIATED TRANSFER PRICES.................................................................................. 680

NO EXCESS CAPACITY................................................................................................... 680EXCESS CAPACITY.......................................................................................................... 681VARIABLE COSTS............................................................................................................ 682SPECIAL ORDER............................................................................................................... 683SUMMARY OF NEGOTIATED TRANSFER PRICING APPROACH....................... 683

COST‐BASED TRANSFER PRICES................................................................................... 684MARKET‐BASED TRANSFER PRICES............................................................................. 685EFFECT OF OUTSOURCING ON TRANSFER PRICING............................................. 686TRANSFERS BETWEEN DIVISIONS IN DIFFERENT COUNTRIES........................ 686APPENDIX 11A OTHER COST APPROACHES TO PRICING.................................... 691ABSORPTION COST APPROACH.................................................................................... 691CONTRIBUTION (VARIABLE COST) APPROACH..................................................... 694SUMMARY OF STUDY OBJECTIVE FOR APPENDIX 11A......................................... 696COMPREHENSIVE PROBLEM: CHAPTERS 1–11.......................................................... 723GLOSSARY.............................................................................................................................. 730

CHAPTER 12THE STATEMENT OF CASH FLOWS: PURPOSE AND FORMAT............................ 735

PURPOSE OF THE STATEMENT OF CASH FLOWS................................................. 736MEANING OF “CASH FLOWS”.................................................................................... 736CLASSIFICATION OF CASH FLOWS........................................................................... 737SIGNIFICANT NONCASH ACTIVITIES....................................................................... 738FORMAT OF THE STATEMENT OF CASH FLOWS.................................................. 740THE CORPORATE LIFE CYCLE..................................................................................... 741USEFULNESS OF THE STATEMENT OF CASH FLOWS.......................................... 743PREPARING THE STATEMENT OF CASH FLOWS................................................... 744

Managerial AccountingTable of Contents

viii

INDIRECT AND DIRECT METHODS........................................................................... 745SECTION 1 STATEMENT OF CASH FLOWS—INDIRECT METHOD..................... 747FIRST YEAR OF OPERATIONS—2002.............................................................................. 747

STEP 1: DETERMINE THE NET INCREASE/DECREASE IN CASH........................ 748STEP 2: DETERMINE NET CASH PROVIDED/USED BY OPERATINGACTIVITIES........................................................................................................................ 749STEP 3: DETERMINE NET CASH PROVIDED/USED BY INVESTING ANDFINANCING ACTIVITIES............................................................................................... 751STATEMENT OF CASH FLOWS—2002........................................................................ 752

SECOND YEAR OF OPERATIONS—2003........................................................................ 753STEP 1: DETERMINE THE NET INCREASE/DECREASE IN CASH........................ 754STEP 2: DETERMINE NET CASH PROVIDED/USED BY OPERATINGACTIVITIES........................................................................................................................ 754STEP 3: DETERMINE NET CASH PROVIDED/USED BY INVESTING ANDFINANCING ACTIVITIES............................................................................................... 756STATEMENT OF CASH FLOWS—2003........................................................................ 758SUMMARY OF CONVERSION TO NET CASH PROVIDED BY OPERATINGACTIVITIES—INDIRECT METHOD............................................................................. 758

SECTION 1 STATEMENT OF CASH FLOWS—DIRECT METHOD.......................... 762FIRST YEAR OF OPERATIONS—2002.............................................................................. 762

STEP 1: DETERMINE THE NET INCREASE/DECREASE IN CASH........................ 764STEP 2: DETERMINE NET CASH PROVIDED/USED BY OPERATINGACTIVITIES........................................................................................................................ 764STEP 3: DETERMINE NET CASH PROVIDED/USED BY INVESTING ANDFINANCING ACTIVITIES............................................................................................... 769STATEMENT OF CASH FLOWS—2002........................................................................ 770

SECOND YEAR OF OPERATIONS—2003........................................................................ 771STEP 1: DETERMINE THE NET INCREASE/DECREASE IN CASH........................ 772STEP 2: DETERMINE NET CASH PROVIDED/USED BY OPERATINGACTIVITIES........................................................................................................................ 772STEP 3: DETERMINE NET CASH PROVIDED/USED BY INVESTING ANDFINANCING ACTIVITIES............................................................................................... 775STATEMENT OF CASH FLOWS—2003........................................................................ 776

USING CASH FLOWS TO EVALUATE A COMPANY................................................. 779FREE CASH FLOW............................................................................................................ 779CAPITAL EXPENDITURE RATIO.................................................................................. 781ASSESSING LIQUIDITY, SOLVENCY, AND PROFITABILITY USINGCASH FLOWS.................................................................................................................... 782

GLOSSARY.............................................................................................................................. 836CHAPTER 13

EARNING POWER AND IRREGULAR ITEMS.............................................................. 842DISCONTINUED OPERATIONS.................................................................................... 843

Managerial AccountingTable of Contents

ix

EXTRAORDINARY ITEMS.............................................................................................. 844CHANGES IN ACCOUNTING PRINCIPLE................................................................. 847COMPREHENSIVE INCOME......................................................................................... 849

COMPARATIVE ANALYSIS............................................................................................... 849HORIZONTAL ANALYSIS.............................................................................................. 851VERTICAL ANALYSIS..................................................................................................... 855

RATIO ANALYSIS................................................................................................................. 859LIQUIDITY RATIOS.......................................................................................................... 862SOLVENCY RATIOS......................................................................................................... 867PROFITABILITY RATIOS................................................................................................. 870

LIMITATIONS OF FINANCIAL ANALYSIS................................................................... 878ESTIMATES........................................................................................................................ 878COST....ū 878ALTERNATIVE ACCOUNTING METHODS............................................................... 879ATYPICAL DATA............................................................................................................. 879DIVERSIFICATION........................................................................................................... 879

GLOSSARY.............................................................................................................................. 931APPENDIX A

THE ANNUAL REPORT....................................................................................................... 935FINANCIAL HIGHLIGHTS................................................................................................. 936

Corporate Principles ......................................................................................................... 936Corporate Profile ............................................................................................................... 937

LETTER TO THE STOCKHOLDERS................................................................................. 937To Our Shareholders ........................................................................................................ 937Operating Report .............................................................................................................. 939

MANAGEMENT DISCUSSION AND ANALYSIS........................................................ 942Management's Discussion and Analysis of Financial Condition and Results ofOperations .......................................................................................................................... 942

FINANCIAL STATEMENTS AND ACCOMPANYING NOTES................................. 948Notes to Consolidated Financial Statements ................................................................ 953

AUDITOR'S REPORT............................................................................................................ 966Report of Independent Accountants .............................................................................. 967

SUPPLEMENTARY FINANCIAL INFORMATION....................................................... 967APPENDIX BAPPENDIX C

NATURE OF INTEREST....................................................................................................... 977SIMPLE INTEREST............................................................................................................ 978COMPOUND INTEREST................................................................................................. 978

SECTION 1 FUTURE VALUE CONCEPTS....................................................................... 979FUTURE VALUE OF A SINGLE AMOUNT..................................................................... 979FUTURE VALUE OF AN ANNUITY.................................................................................. 982SECTION 2 PRESENT VALUE CONCEPTS..................................................................... 985

Managerial AccountingTable of Contents

x

PRESENT VALUE VARIABLES.......................................................................................... 985PRESENT VALUE OF A SINGLE AMOUNT................................................................... 985PRESENT VALUE OF AN ANNUITY................................................................................ 988TIME PERIODS AND DISCOUNTING............................................................................ 991COMPUTING THE PRESENT VALUES IN A CAPITAL BUDGETINGDECISIONū 991GLOSSARY............................................................................................................................ 1000

APPENDIX DETHICAL BEHAVIOR FOR PRACTITIONERS OF MANAGEMENT ACCOUNTINGAND FINANCIAL MANAGEMENT............................................................................... 1001STANDARDS OF ETHICAL CONDUCT FOR PRACTITIONERS OF MANAGEMENTACCOUNTING AND FINANCIAL MANAGEMENT................................................. 1002

COMPETENCE................................................................................................................ 1002CONFIDENTIALITY....................................................................................................... 1002INTEGRITY....................................................................................................................... 1003OBJECTIVITY................................................................................................................... 1003RESOLUTION OF ETHICAL CONFLICT................................................................... 1003

AFTERWORDCASE‐1....ū 1007CARD‐MART SWIMS IN THE DOT‐COM SEA: JOB ORDER COSTING............. 1007

THE BUSINESS SITUATION......................................................................................... 1007CASE‐2....ū 1010CARD‐MART SWIMS IN THE DOT‐COM SEA: ACTIVITY‐BASED COSTING.. 1010

THE BUSINESS SITUATION......................................................................................... 1011CASE‐3....ū 1016CARD‐MART SWIMS IN THE DOT‐COM SEA: CAPITAL BUDGETING............ 1016

THE BUSINESS SITUATION......................................................................................... 1016CASE‐4....ū 1019CARD‐MART SWIMS IN THE DOT‐COM SEA: TRANSFER PRICING ISSUES. 1019

THE BUSINESS SITUATION......................................................................................... 1019CASE‐5....ū 1022RICHLAND CIRCULAR CLUB PRO RODEO ROUNDUP......................................... 1022

THE BUSINESS SITUATION......................................................................................... 1022

Managerial AccountingTable of Contents

xi

Managerial AccountingTable of Contents

xii

Chapter 2

Job Order Cost Accounting

Navigator

• Scan Study Objectives

• Read Feature Story

• Read Preview

• Read text and answer Before You Go On

p.48 □ p.59 □ p.66 □

• Work Using the Decision Toolkit

• Review Summary of Study Objectives

• Work Demonstration Problem

• Answer Self‐Study Questions

• Complete Assignments

Managerial AccountingChapter 2

Page 69

STUDY OBJECTIVES

After studying this chapter, you should be able to:

1. Explain the characteristics and purposes of cost accounting.

2. Describe the flow of costs in a job order cost accounting system.

3. Explain the nature and importance of a job cost sheet.

4. Indicate how the predetermined overhead rate is determined and used.

5. Prepare entries for jobs completed and sold.

6. Distinguish between under‐ and overapplied manufacturing overhead.

Managerial AccountingChapter 2

Page 70

Feature Story

“ … AND WE'D LIKE IT IN RED”

Western States Fire Apparatus, Inc., of Cornelius, Oregon, is one of the few U.S. companiesthat makes fire trucks. The company builds about 25 trucks per year. Founded in 1941, thecompany is run by the children and grandchildren of the original founder.

“We buy the chassis, which is the cab and the frame,” says Susan Scott, the company'sbookkeeper. “In our computer, we set up an account into which all of the direct materialthat is purchased for that particular job is charged.” Other direct materials include the waterpump—which can cost $10,000—the lights, the siren, ladders, and hoses.

As for direct labor, the production workers fill out time tickets that tell what jobs they workedon. Usually, the company is building four trucks at any one time. On payday, the controllerallocates the payroll to the appropriate job record.

Indirect materials, such as nuts and bolts, wiring, lubricants, and abrasives, are allocated toeach job in proportion to direct material dollars. Other costs, such as insurance andsupervisors' salaries, are allocated based on direct labor hours. “We need to allocate overheadin order to know what kind of price we have to charge when we submit our bids,” she says.

Managerial AccountingChapter 2

Page 71

Western gets orders through a “blind‐bidding” process. That is, Western submits its bidwithout knowing the bid prices made by its competitors. “If we bid too low, we won't makea profit. If we bid too high, we don't get the job.”

Regardless of the final price for the truck, the quality had better be first‐rate. “The firedepartments let you know if they don't like what you did, and you usually end up fixingit.”

PREVIEW OF CHAPTER 2

The Feature Story about Western States Fire Apparatus described the manufacturing costsused in making a fire truck. It demonstrated that accurate costing is critical to the company'ssuccess. For example, in order to submit accurate bids on new jobs and to know whether itprofited from past jobs, the company needs a good costing system. This chapter illustrateshow these manufacturing costs would be assigned to specific jobs, such as the manufactureof individual fire trucks. We begin the discussion in this chapter with an overview of theflow of costs in a job order cost accounting system. We then use a case study to explain andillustrate the documents, entries, and accounts in this type of cost accounting system.

The content and organization of Chapter 2 are as follows.

COST ACCOUNTING SYSTEMS

Cost accounting involves the measuring, recording, and reporting of product costs. From thedata accumulated, both the total cost and the unit cost of each product is determined. The accuracyof the product cost information produced by the cost accounting system is critical to the successof the company. As you will see in later chapters, this information is used to determine whichproducts to produce, what price to charge, and the amounts to produce. Accurate product costinformation is also vital for effective evaluation of employee performance.

Managerial AccountingChapter 2

Page 72

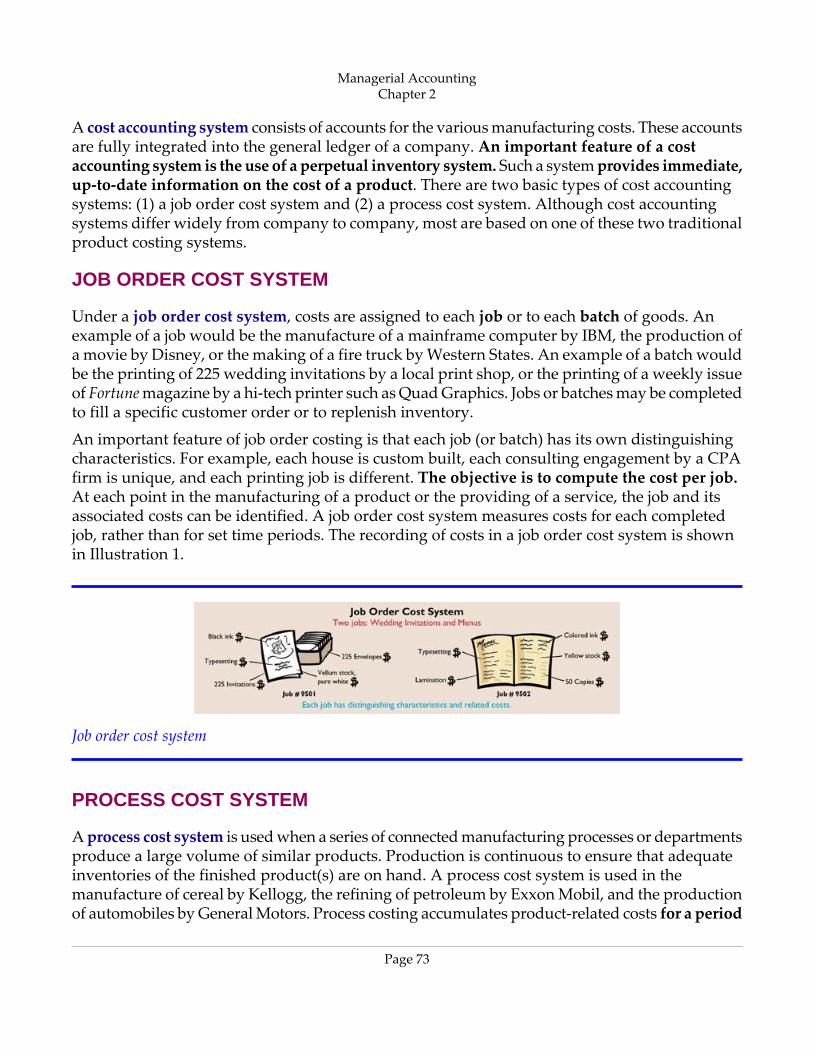

A cost accounting system consists of accounts for the various manufacturing costs. These accountsare fully integrated into the general ledger of a company. An important feature of a costaccounting system is the use of a perpetual inventory system. Such a system provides immediate,up‐to‐date information on the cost of a product. There are two basic types of cost accountingsystems: (1) a job order cost system and (2) a process cost system. Although cost accountingsystems differ widely from company to company, most are based on one of these two traditionalproduct costing systems.

JOB ORDER COST SYSTEM

Under a job order cost system, costs are assigned to each job or to each batch of goods. Anexample of a job would be the manufacture of a mainframe computer by IBM, the production ofa movie by Disney, or the making of a fire truck by Western States. An example of a batch wouldbe the printing of 225 wedding invitations by a local print shop, or the printing of a weekly issueof Fortunemagazine by a hi‐tech printer such as Quad Graphics. Jobs or batches may be completedto fill a specific customer order or to replenish inventory.

An important feature of job order costing is that each job (or batch) has its own distinguishingcharacteristics. For example, each house is custom built, each consulting engagement by a CPAfirm is unique, and each printing job is different. The objective is to compute the cost per job.At each point in the manufacturing of a product or the providing of a service, the job and itsassociated costs can be identified. A job order cost system measures costs for each completedjob, rather than for set time periods. The recording of costs in a job order cost system is shownin Illustration 1.

Job order cost system

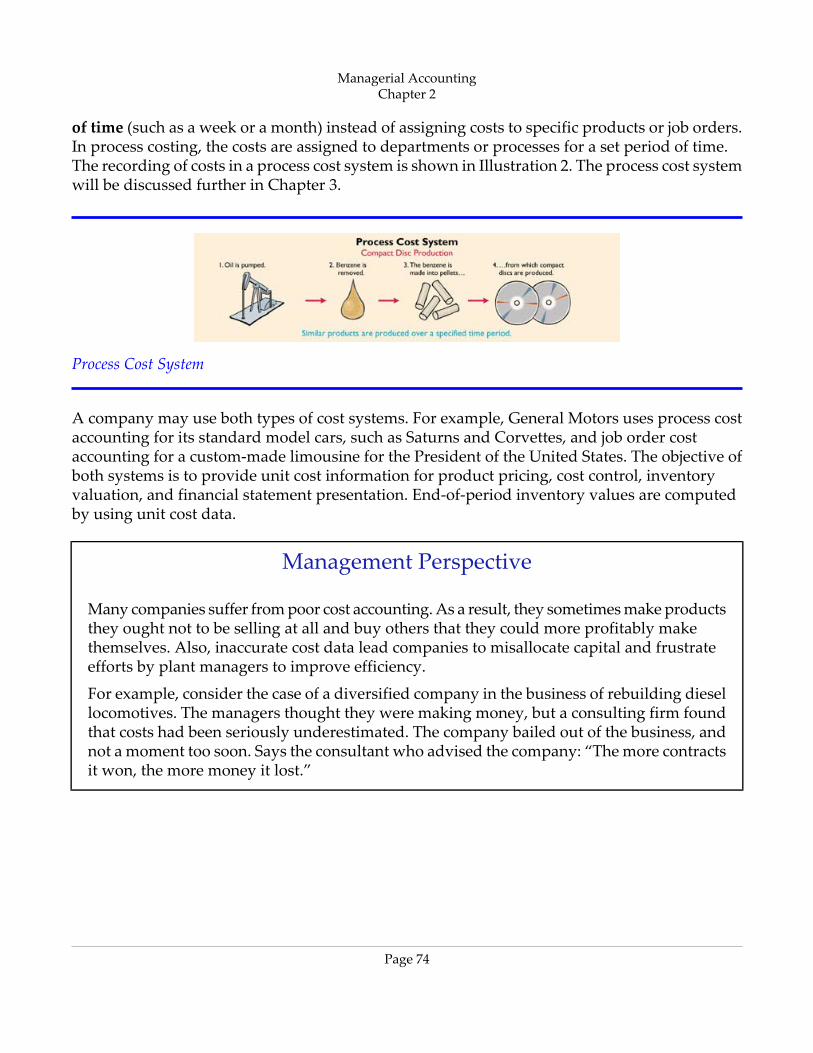

PROCESS COST SYSTEM

A process cost system is used when a series of connected manufacturing processes or departmentsproduce a large volume of similar products. Production is continuous to ensure that adequateinventories of the finished product(s) are on hand. A process cost system is used in themanufacture of cereal by Kellogg, the refining of petroleum by Exxon Mobil, and the productionof automobiles by General Motors. Process costing accumulates product‐related costs for a period

Managerial AccountingChapter 2

Page 73

of time (such as a week or a month) instead of assigning costs to specific products or job orders.In process costing, the costs are assigned to departments or processes for a set period of time.The recording of costs in a process cost system is shown in Illustration 2. The process cost systemwill be discussed further in Chapter 3.

Process Cost System

A company may use both types of cost systems. For example, General Motors uses process costaccounting for its standard model cars, such as Saturns and Corvettes, and job order costaccounting for a custom‐made limousine for the President of the United States. The objective ofboth systems is to provide unit cost information for product pricing, cost control, inventoryvaluation, and financial statement presentation. End‐of‐period inventory values are computedby using unit cost data.

Management Perspective

Many companies suffer from poor cost accounting. As a result, they sometimes make productsthey ought not to be selling at all and buy others that they could more profitably makethemselves. Also, inaccurate cost data lead companies to misallocate capital and frustrateefforts by plant managers to improve efficiency.

For example, consider the case of a diversified company in the business of rebuilding diesellocomotives. The managers thought they were making money, but a consulting firm foundthat costs had been seriously underestimated. The company bailed out of the business, andnot a moment too soon. Says the consultant who advised the company: “The more contractsit won, the more money it lost.”

Managerial AccountingChapter 2

Page 74

Before You Go On...

Review It

1. What is cost accounting?

2. What does a cost accounting system consist of?

3. How does a job order cost system differ from a process cost system?

JOB ORDER COST FLOW

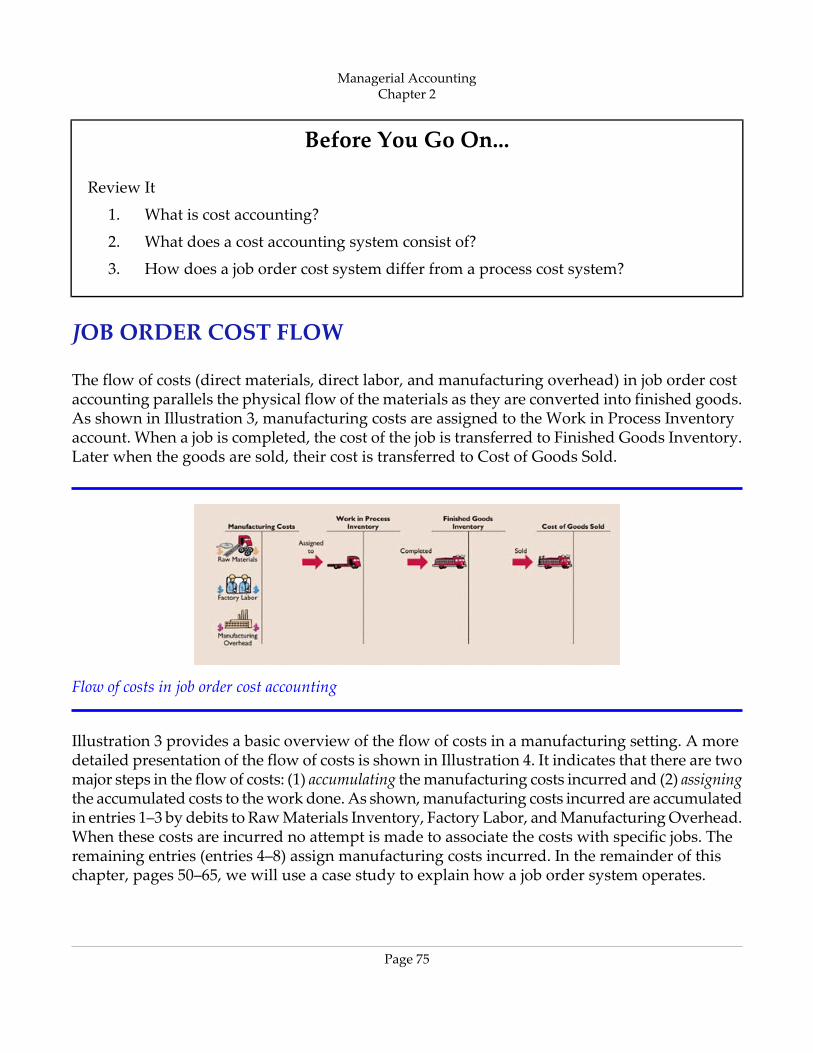

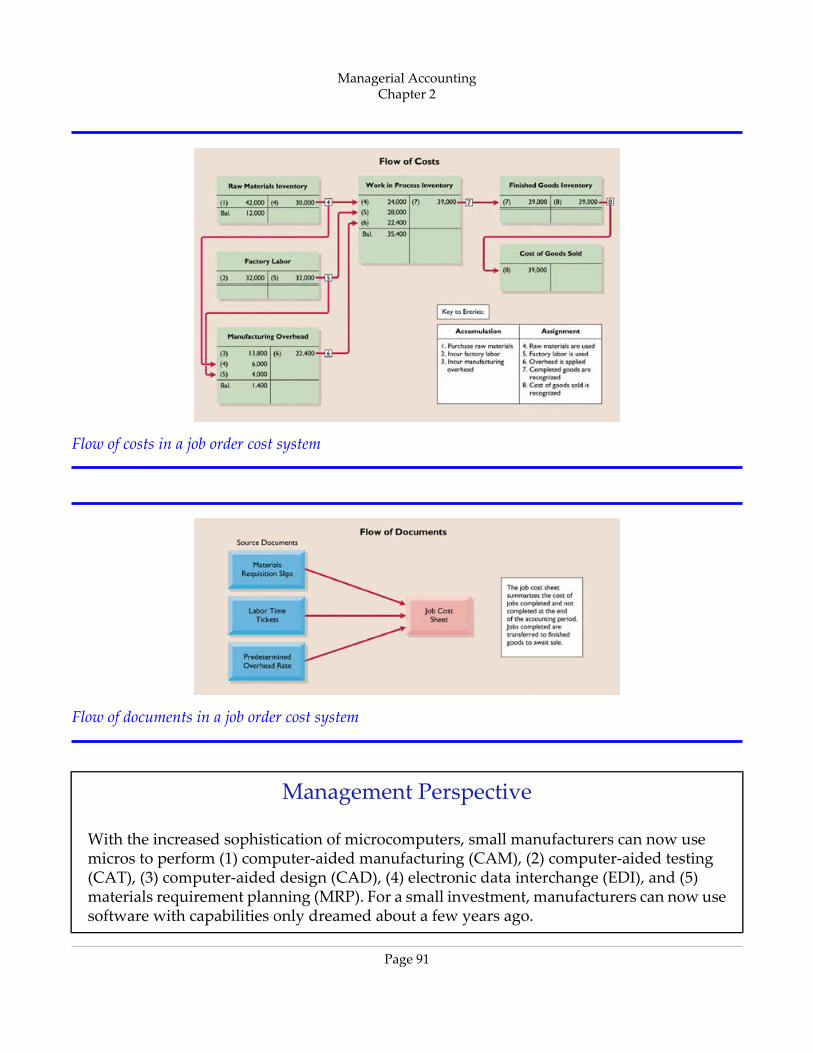

The flow of costs (direct materials, direct labor, and manufacturing overhead) in job order costaccounting parallels the physical flow of the materials as they are converted into finished goods.As shown in Illustration 3, manufacturing costs are assigned to the Work in Process Inventoryaccount. When a job is completed, the cost of the job is transferred to Finished Goods Inventory.Later when the goods are sold, their cost is transferred to Cost of Goods Sold.

Flow of costs in job order cost accounting

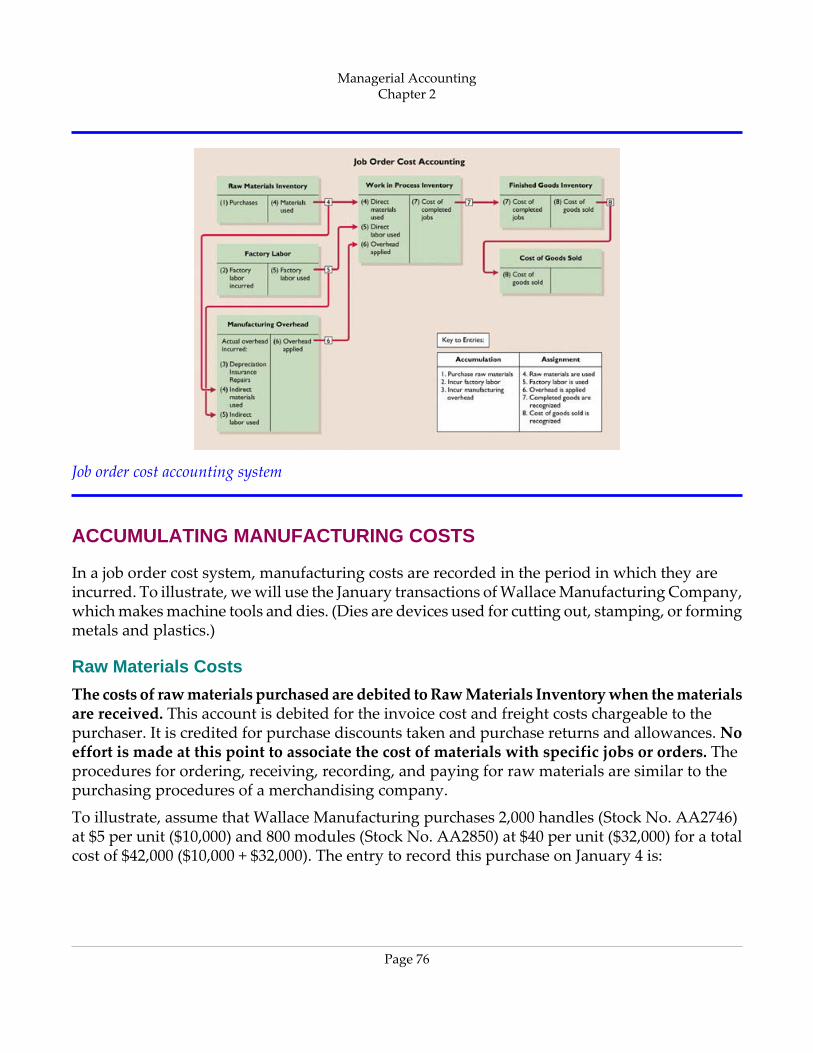

Illustration 3 provides a basic overview of the flow of costs in a manufacturing setting. A moredetailed presentation of the flow of costs is shown in Illustration 4. It indicates that there are twomajor steps in the flow of costs: (1) accumulating the manufacturing costs incurred and (2) assigningthe accumulated costs to the work done. As shown, manufacturing costs incurred are accumulatedin entries 1–3 by debits to Raw Materials Inventory, Factory Labor, and Manufacturing Overhead.When these costs are incurred no attempt is made to associate the costs with specific jobs. Theremaining entries (entries 4–8) assign manufacturing costs incurred. In the remainder of thischapter, pages 50–65, we will use a case study to explain how a job order system operates.

Managerial AccountingChapter 2

Page 75

Job order cost accounting system

ACCUMULATING MANUFACTURING COSTS

In a job order cost system, manufacturing costs are recorded in the period in which they areincurred. To illustrate, we will use the January transactions of Wallace Manufacturing Company,which makes machine tools and dies. (Dies are devices used for cutting out, stamping, or formingmetals and plastics.)

Raw Materials Costs

The costs of raw materials purchased are debited to Raw Materials Inventory when the materialsare received. This account is debited for the invoice cost and freight costs chargeable to thepurchaser. It is credited for purchase discounts taken and purchase returns and allowances. Noeffort is made at this point to associate the cost of materials with specific jobs or orders. Theprocedures for ordering, receiving, recording, and paying for raw materials are similar to thepurchasing procedures of a merchandising company.

To illustrate, assume that Wallace Manufacturing purchases 2,000 handles (Stock No. AA2746)at $5 per unit ($10,000) and 800 modules (Stock No. AA2850) at $40 per unit ($32,000) for a totalcost of $42,000 ($10,000 + $32,000). The entry to record this purchase on January 4 is:

Managerial AccountingChapter 2

Page 76

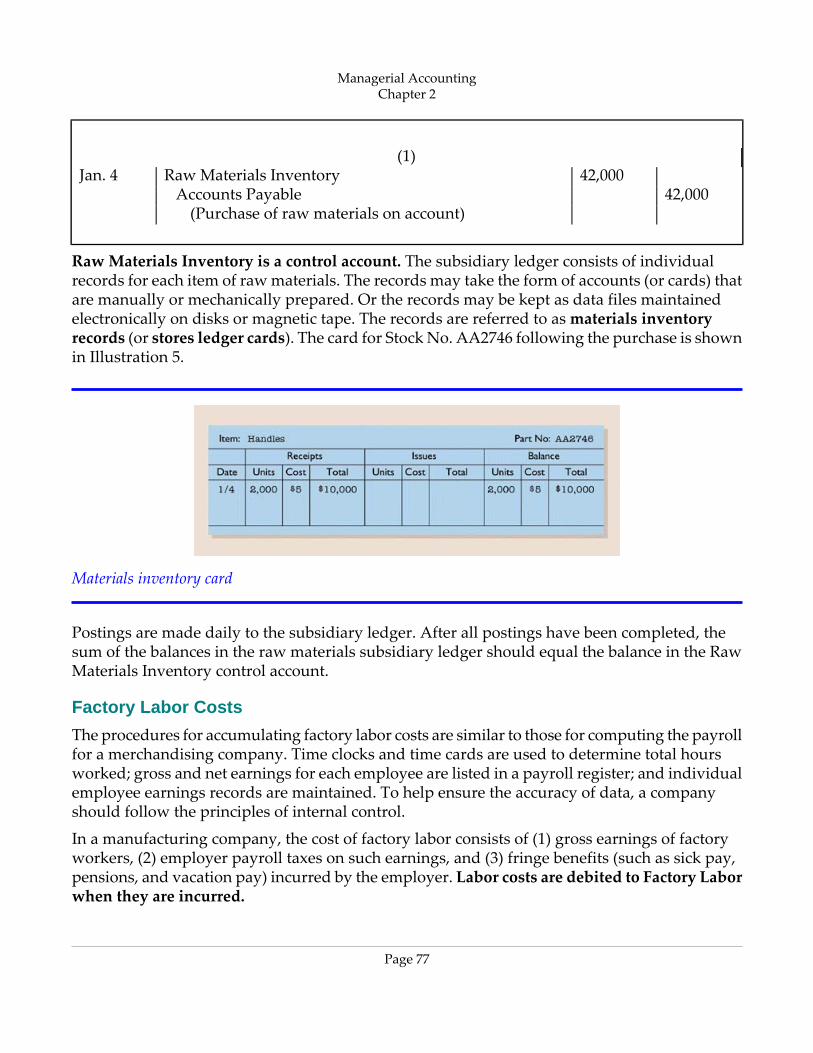

(1)42,000Raw Materials InventoryJan. 4

42,000Accounts Payable(Purchase of raw materials on account)

Raw Materials Inventory is a control account. The subsidiary ledger consists of individualrecords for each item of raw materials. The records may take the form of accounts (or cards) thatare manually or mechanically prepared. Or the records may be kept as data files maintainedelectronically on disks or magnetic tape. The records are referred to as materials inventoryrecords (or stores ledger cards). The card for Stock No. AA2746 following the purchase is shownin Illustration 5.

Materials inventory card

Postings are made daily to the subsidiary ledger. After all postings have been completed, thesum of the balances in the raw materials subsidiary ledger should equal the balance in the RawMaterials Inventory control account.

Factory Labor Costs

The procedures for accumulating factory labor costs are similar to those for computing the payrollfor a merchandising company. Time clocks and time cards are used to determine total hoursworked; gross and net earnings for each employee are listed in a payroll register; and individualemployee earnings records are maintained. To help ensure the accuracy of data, a companyshould follow the principles of internal control.

In a manufacturing company, the cost of factory labor consists of (1) gross earnings of factoryworkers, (2) employer payroll taxes on such earnings, and (3) fringe benefits (such as sick pay,pensions, and vacation pay) incurred by the employer. Labor costs are debited to Factory Laborwhen they are incurred.

Managerial AccountingChapter 2

Page 77

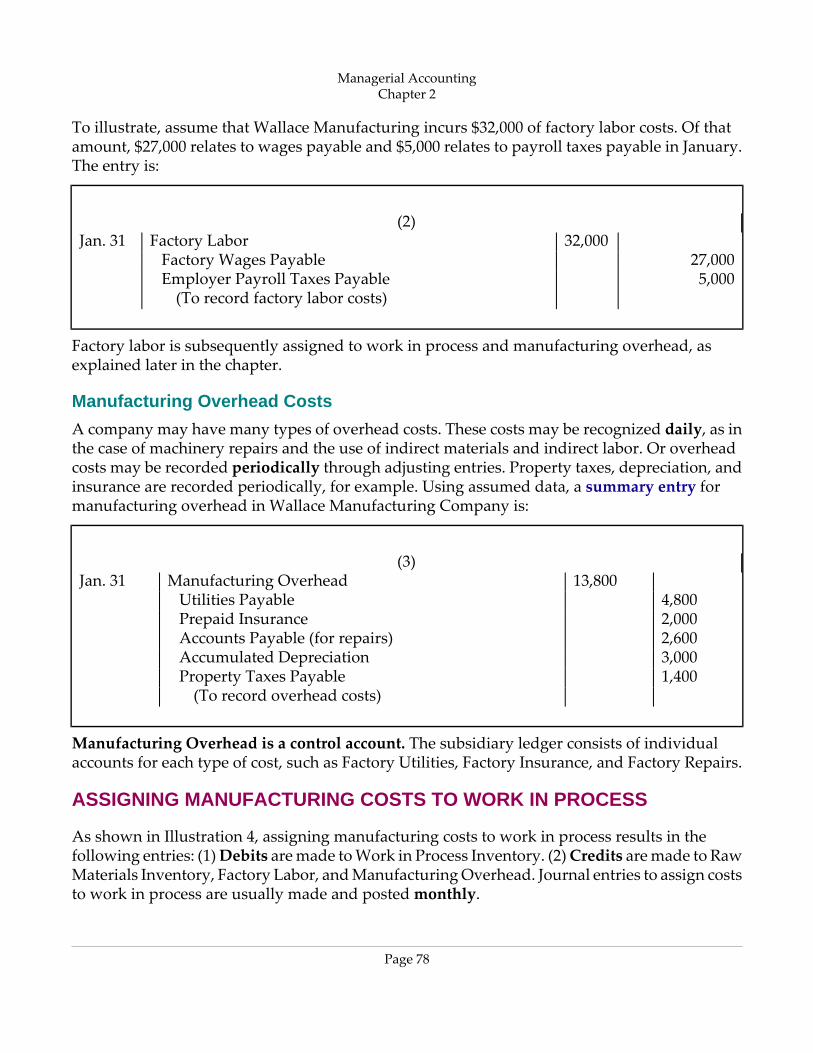

To illustrate, assume that Wallace Manufacturing incurs $32,000 of factory labor costs. Of thatamount, $27,000 relates to wages payable and $5,000 relates to payroll taxes payable in January.The entry is:

(2)32,000Factory LaborJan. 31

27,000Factory Wages Payable5,000Employer Payroll Taxes Payable

(To record factory labor costs)

Factory labor is subsequently assigned to work in process and manufacturing overhead, asexplained later in the chapter.

Manufacturing Overhead Costs

A company may have many types of overhead costs. These costs may be recognized daily, as inthe case of machinery repairs and the use of indirect materials and indirect labor. Or overheadcosts may be recorded periodically through adjusting entries. Property taxes, depreciation, andinsurance are recorded periodically, for example. Using assumed data, a summary entry formanufacturing overhead in Wallace Manufacturing Company is:

(3)13,800Manufacturing OverheadJan. 31

4,800Utilities Payable2,000Prepaid Insurance2,600Accounts Payable (for repairs)3,000Accumulated Depreciation1,400Property Taxes Payable

(To record overhead costs)

Manufacturing Overhead is a control account. The subsidiary ledger consists of individualaccounts for each type of cost, such as Factory Utilities, Factory Insurance, and Factory Repairs.

ASSIGNING MANUFACTURING COSTS TO WORK IN PROCESS

As shown in Illustration 4, assigning manufacturing costs to work in process results in thefollowing entries: (1) Debits are made to Work in Process Inventory. (2) Credits are made to RawMaterials Inventory, Factory Labor, and Manufacturing Overhead. Journal entries to assign coststo work in process are usually made and posted monthly.

Managerial AccountingChapter 2

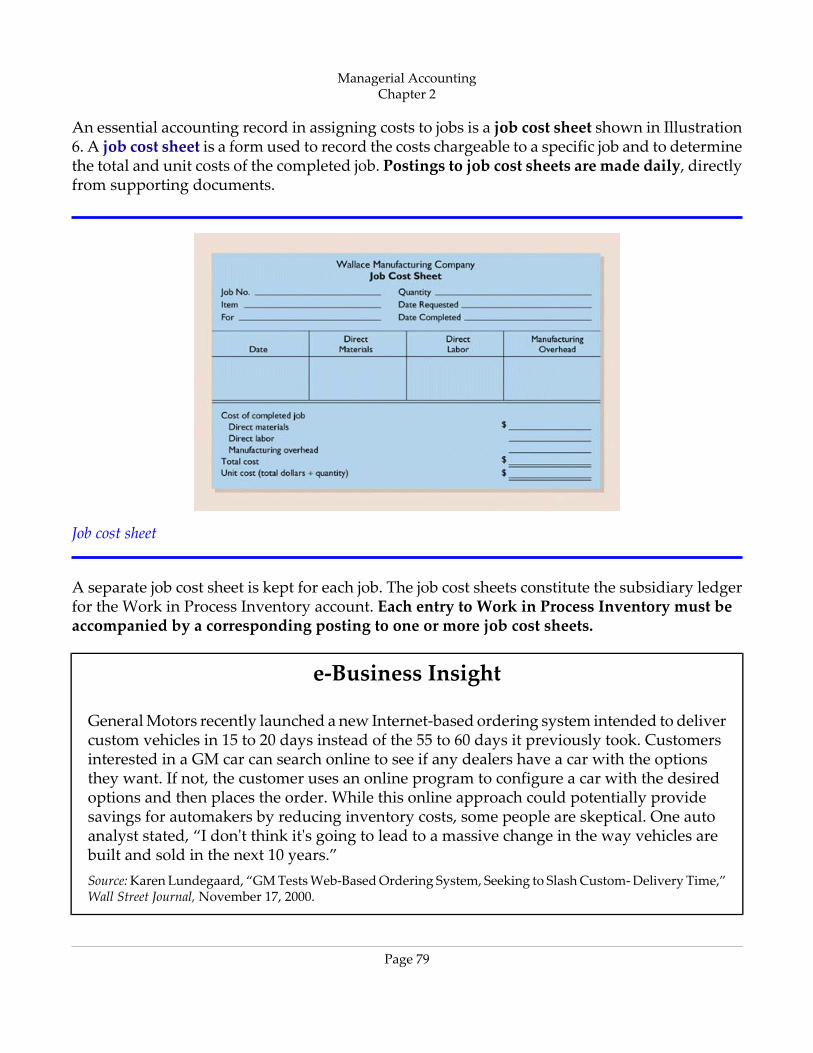

Page 78

An essential accounting record in assigning costs to jobs is a job cost sheet shown in Illustration6. A job cost sheet is a form used to record the costs chargeable to a specific job and to determinethe total and unit costs of the completed job. Postings to job cost sheets are made daily, directlyfrom supporting documents.

Job cost sheet

A separate job cost sheet is kept for each job. The job cost sheets constitute the subsidiary ledgerfor the Work in Process Inventory account. Each entry to Work in Process Inventory must beaccompanied by a corresponding posting to one or more job cost sheets.

e‐Business Insight

General Motors recently launched a new Internet‐based ordering system intended to delivercustom vehicles in 15 to 20 days instead of the 55 to 60 days it previously took. Customersinterested in a GM car can search online to see if any dealers have a car with the optionsthey want. If not, the customer uses an online program to configure a car with the desiredoptions and then places the order. While this online approach could potentially providesavings for automakers by reducing inventory costs, some people are skeptical. One autoanalyst stated, “I don't think it's going to lead to a massive change in the way vehicles arebuilt and sold in the next 10 years.”Source:Karen Lundegaard, “GM Tests Web‐Based Ordering System, Seeking to Slash Custom‐ Delivery Time,”Wall Street Journal, November 17, 2000.

Managerial AccountingChapter 2

Page 79

Raw Materials Costs

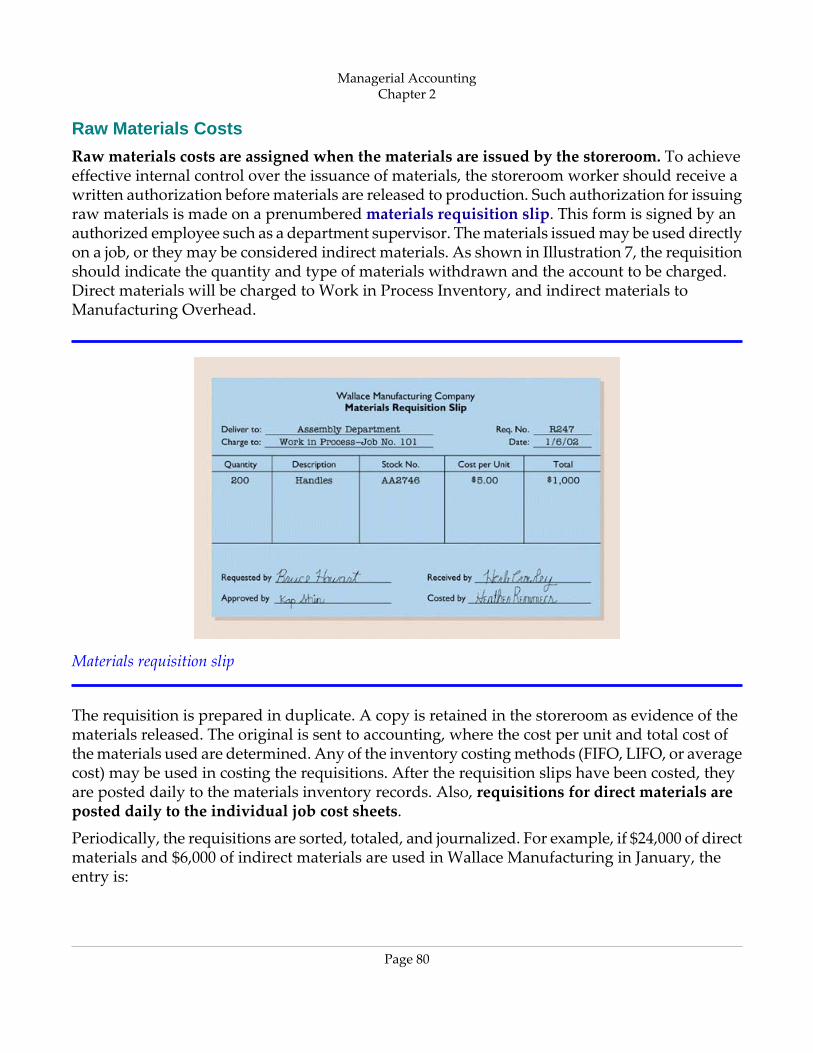

Raw materials costs are assigned when the materials are issued by the storeroom. To achieveeffective internal control over the issuance of materials, the storeroom worker should receive awritten authorization before materials are released to production. Such authorization for issuingraw materials is made on a prenumbered materials requisition slip. This form is signed by anauthorized employee such as a department supervisor. The materials issued may be used directlyon a job, or they may be considered indirect materials. As shown in Illustration 7, the requisitionshould indicate the quantity and type of materials withdrawn and the account to be charged.Direct materials will be charged to Work in Process Inventory, and indirect materials toManufacturing Overhead.

Materials requisition slip

The requisition is prepared in duplicate. A copy is retained in the storeroom as evidence of thematerials released. The original is sent to accounting, where the cost per unit and total cost ofthe materials used are determined. Any of the inventory costing methods (FIFO, LIFO, or averagecost) may be used in costing the requisitions. After the requisition slips have been costed, theyare posted daily to the materials inventory records. Also, requisitions for direct materials areposted daily to the individual job cost sheets.

Periodically, the requisitions are sorted, totaled, and journalized. For example, if $24,000 of directmaterials and $6,000 of indirect materials are used in Wallace Manufacturing in January, theentry is:

Managerial AccountingChapter 2

Page 80

(4)24,000Work in Process InventoryJan. 316,000Manufacturing Overhead

30,000Raw Materials Inventory(To assign materials to jobs and overhead)

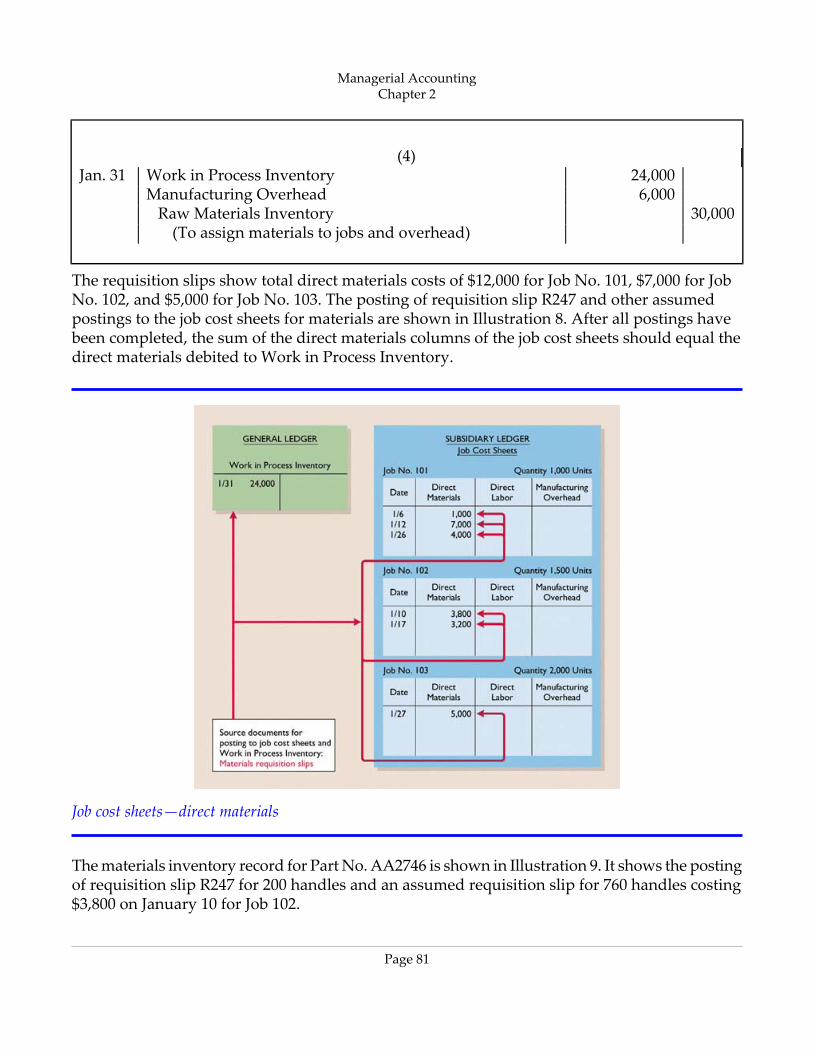

The requisition slips show total direct materials costs of $12,000 for Job No. 101, $7,000 for JobNo. 102, and $5,000 for Job No. 103. The posting of requisition slip R247 and other assumedpostings to the job cost sheets for materials are shown in Illustration 8. After all postings havebeen completed, the sum of the direct materials columns of the job cost sheets should equal thedirect materials debited to Work in Process Inventory.

Job cost sheets—direct materials

The materials inventory record for Part No. AA2746 is shown in Illustration 9. It shows the postingof requisition slip R247 for 200 handles and an assumed requisition slip for 760 handles costing$3,800 on January 10 for Job 102.

Managerial AccountingChapter 2

Page 81

Materials inventory card following issuances

Factory Labor Costs

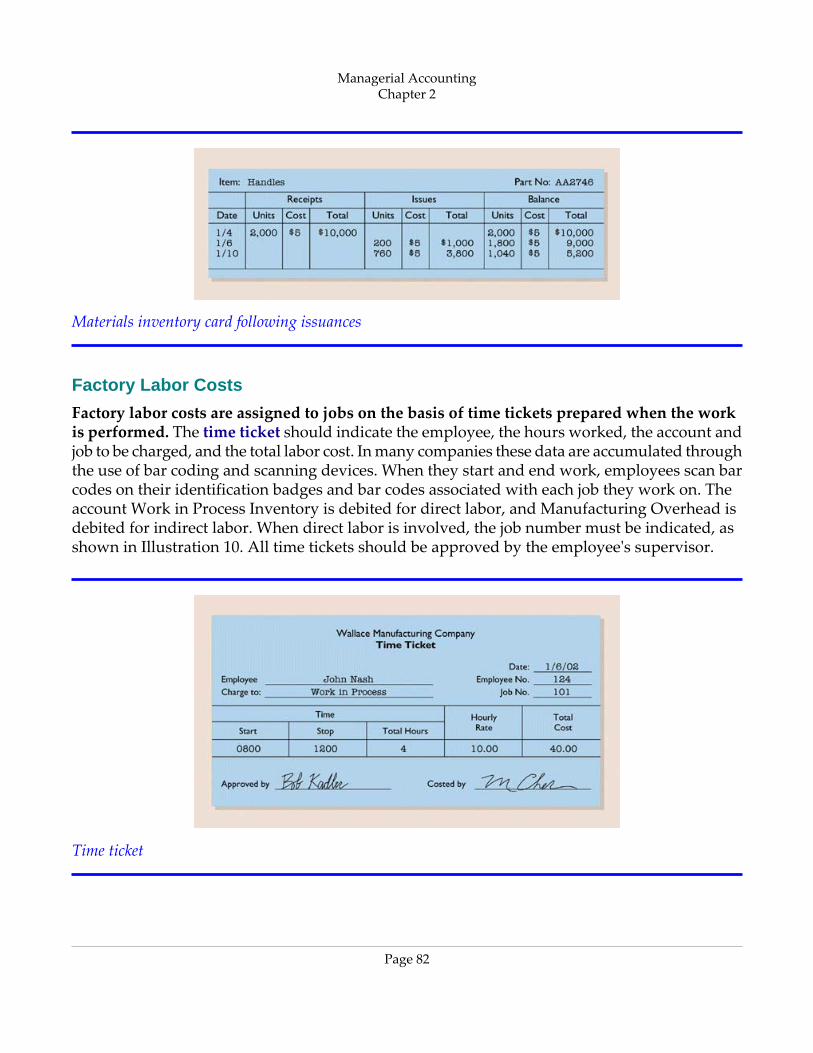

Factory labor costs are assigned to jobs on the basis of time tickets prepared when the workis performed. The time ticket should indicate the employee, the hours worked, the account andjob to be charged, and the total labor cost. In many companies these data are accumulated throughthe use of bar coding and scanning devices. When they start and end work, employees scan barcodes on their identification badges and bar codes associated with each job they work on. Theaccount Work in Process Inventory is debited for direct labor, and Manufacturing Overhead isdebited for indirect labor. When direct labor is involved, the job number must be indicated, asshown in Illustration 10. All time tickets should be approved by the employee's supervisor.

Time ticket

Managerial AccountingChapter 2

Page 82

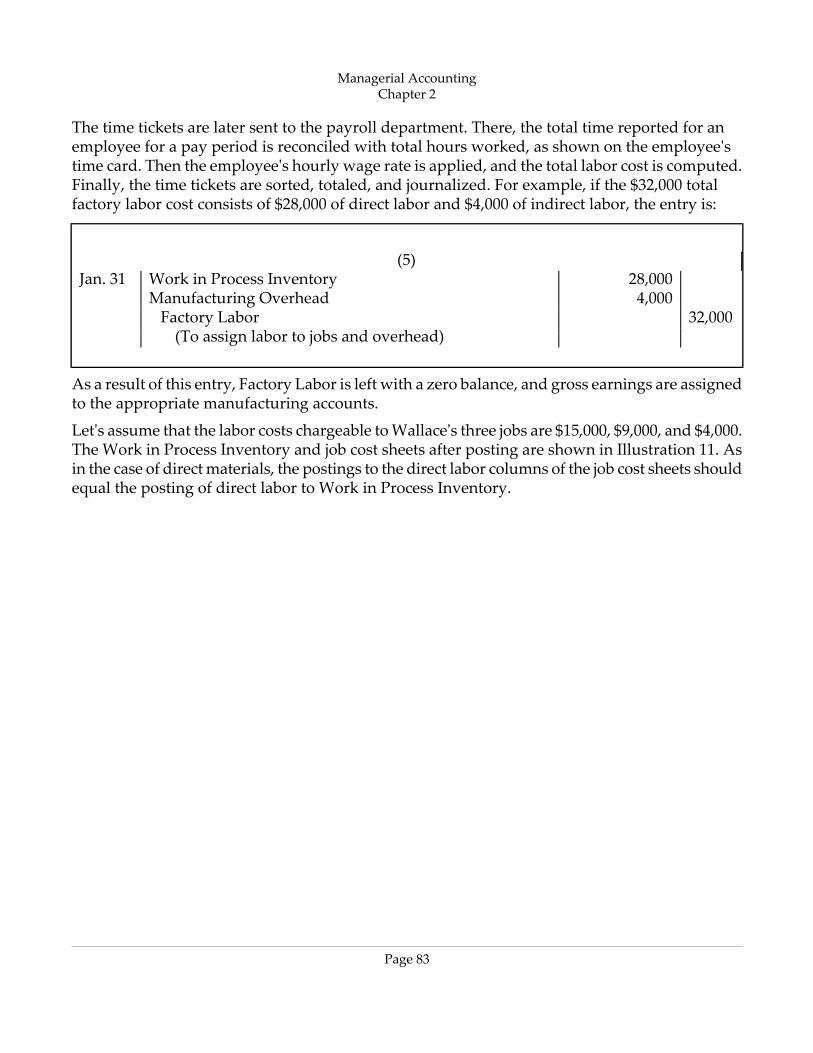

The time tickets are later sent to the payroll department. There, the total time reported for anemployee for a pay period is reconciled with total hours worked, as shown on the employee'stime card. Then the employee's hourly wage rate is applied, and the total labor cost is computed.Finally, the time tickets are sorted, totaled, and journalized. For example, if the $32,000 totalfactory labor cost consists of $28,000 of direct labor and $4,000 of indirect labor, the entry is:

(5)28,000Work in Process InventoryJan. 314,000Manufacturing Overhead

32,000Factory Labor(To assign labor to jobs and overhead)

As a result of this entry, Factory Labor is left with a zero balance, and gross earnings are assignedto the appropriate manufacturing accounts.

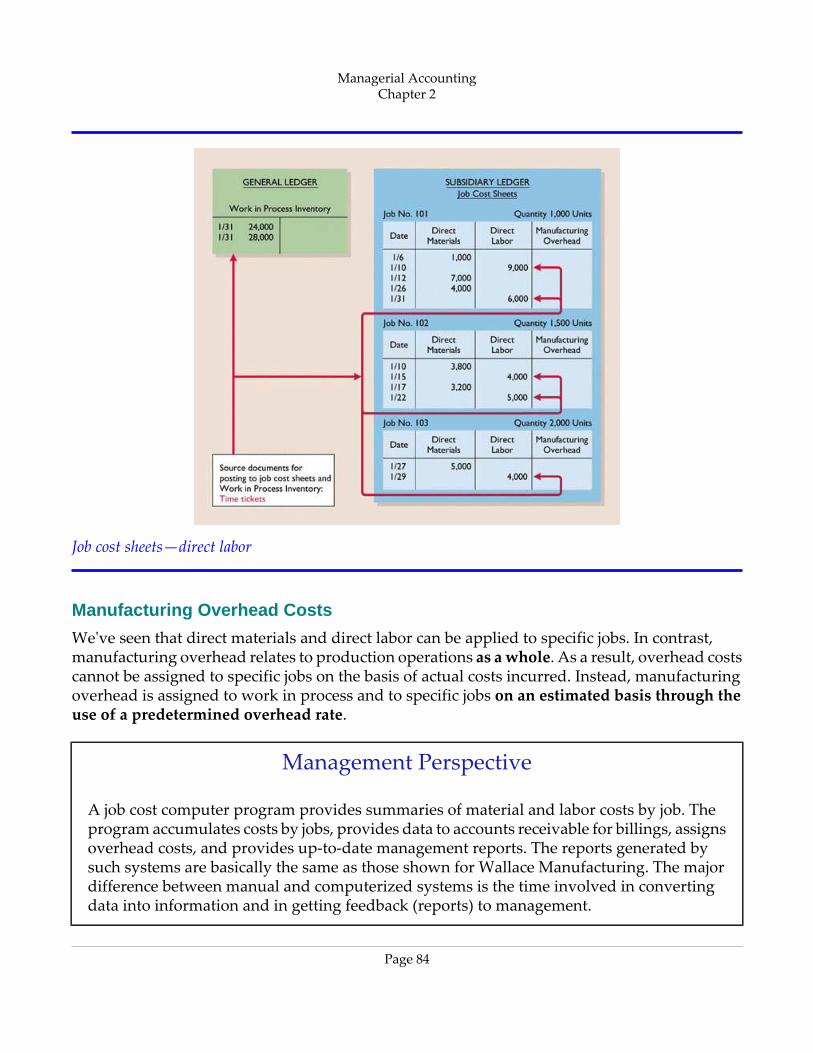

Let's assume that the labor costs chargeable to Wallace's three jobs are $15,000, $9,000, and $4,000.The Work in Process Inventory and job cost sheets after posting are shown in Illustration 11. Asin the case of direct materials, the postings to the direct labor columns of the job cost sheets shouldequal the posting of direct labor to Work in Process Inventory.

Managerial AccountingChapter 2

Page 83

Job cost sheets—direct labor

Manufacturing Overhead Costs

We've seen that direct materials and direct labor can be applied to specific jobs. In contrast,manufacturing overhead relates to production operations as a whole. As a result, overhead costscannot be assigned to specific jobs on the basis of actual costs incurred. Instead, manufacturingoverhead is assigned to work in process and to specific jobs on an estimated basis through theuse of a predetermined overhead rate.

Management Perspective

A job cost computer program provides summaries of material and labor costs by job. Theprogram accumulates costs by jobs, provides data to accounts receivable for billings, assignsoverhead costs, and provides up‐to‐date management reports. The reports generated bysuch systems are basically the same as those shown for Wallace Manufacturing. The majordifference between manual and computerized systems is the time involved in convertingdata into information and in getting feedback (reports) to management.

Managerial AccountingChapter 2

Page 84

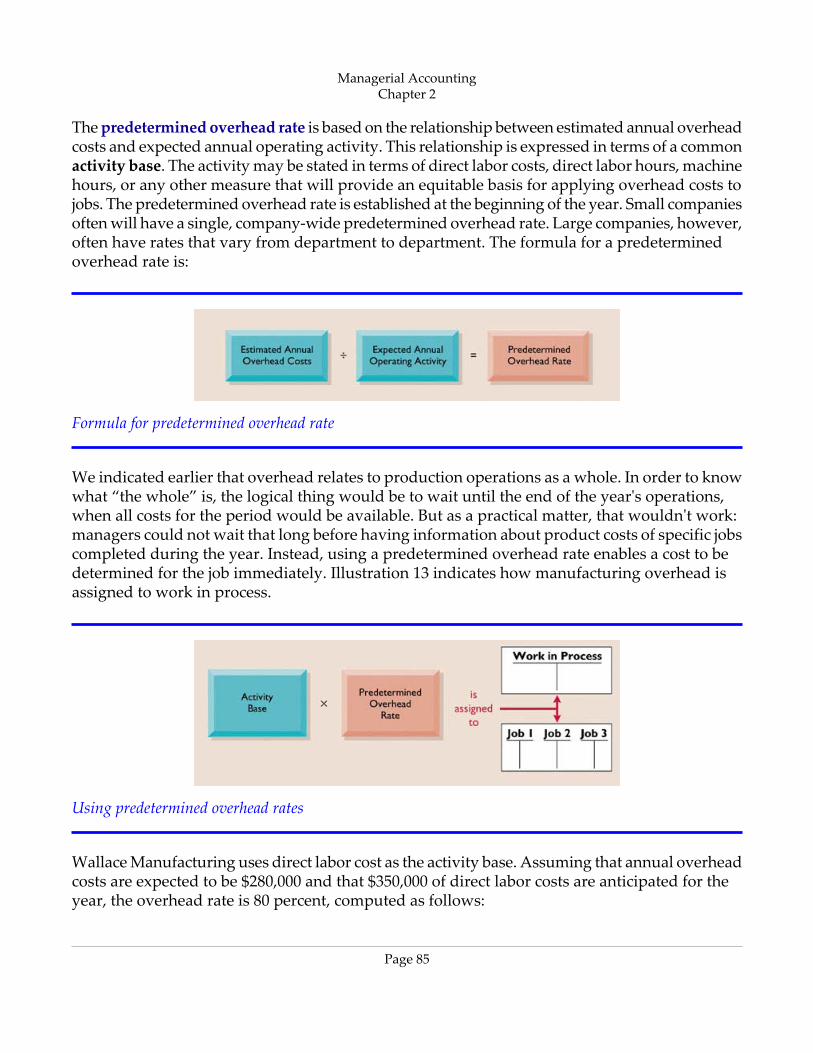

The predetermined overhead rate is based on the relationship between estimated annual overheadcosts and expected annual operating activity. This relationship is expressed in terms of a commonactivity base. The activity may be stated in terms of direct labor costs, direct labor hours, machinehours, or any other measure that will provide an equitable basis for applying overhead costs tojobs. The predetermined overhead rate is established at the beginning of the year. Small companiesoften will have a single, company‐wide predetermined overhead rate. Large companies, however,often have rates that vary from department to department. The formula for a predeterminedoverhead rate is:

Formula for predetermined overhead rate

We indicated earlier that overhead relates to production operations as a whole. In order to knowwhat “the whole” is, the logical thing would be to wait until the end of the year's operations,when all costs for the period would be available. But as a practical matter, that wouldn't work:managers could not wait that long before having information about product costs of specific jobscompleted during the year. Instead, using a predetermined overhead rate enables a cost to bedetermined for the job immediately. Illustration 13 indicates how manufacturing overhead isassigned to work in process.

Using predetermined overhead rates

Wallace Manufacturing uses direct labor cost as the activity base. Assuming that annual overheadcosts are expected to be $280,000 and that $350,000 of direct labor costs are anticipated for theyear, the overhead rate is 80 percent, computed as follows:

Managerial AccountingChapter 2

Page 85

This means that for every dollar of direct labor, 80 cents of manufacturing overhead will beassigned to a job. The use of a predetermined overhead rate enables the company to determinethe approximate total cost of each job when the job is completed.

Historically, direct labor costs or direct labor hours have often been used as the activity base.The reason was the relatively high correlation between direct labor and manufacturing overhead.In recent years, there has been a trend toward use of machine hours as the activity base, dueto increased reliance on automation in manufacturing operations. Or, as mentioned in Chapter1, activity‐based costing has resulted in more accurate allocation of overhead costs based on theactivities that give rise to the costs.

A company may use more than one activity base. For example, if a job order is manufactured inmore than one factory department, each department may have its own overhead rate. In theFeature Story about fire trucks, two bases were used in assigning overhead to jobs: direct materialsdollars for indirect materials, and direct labor hours for such costs as insurance and supervisors'salaries.

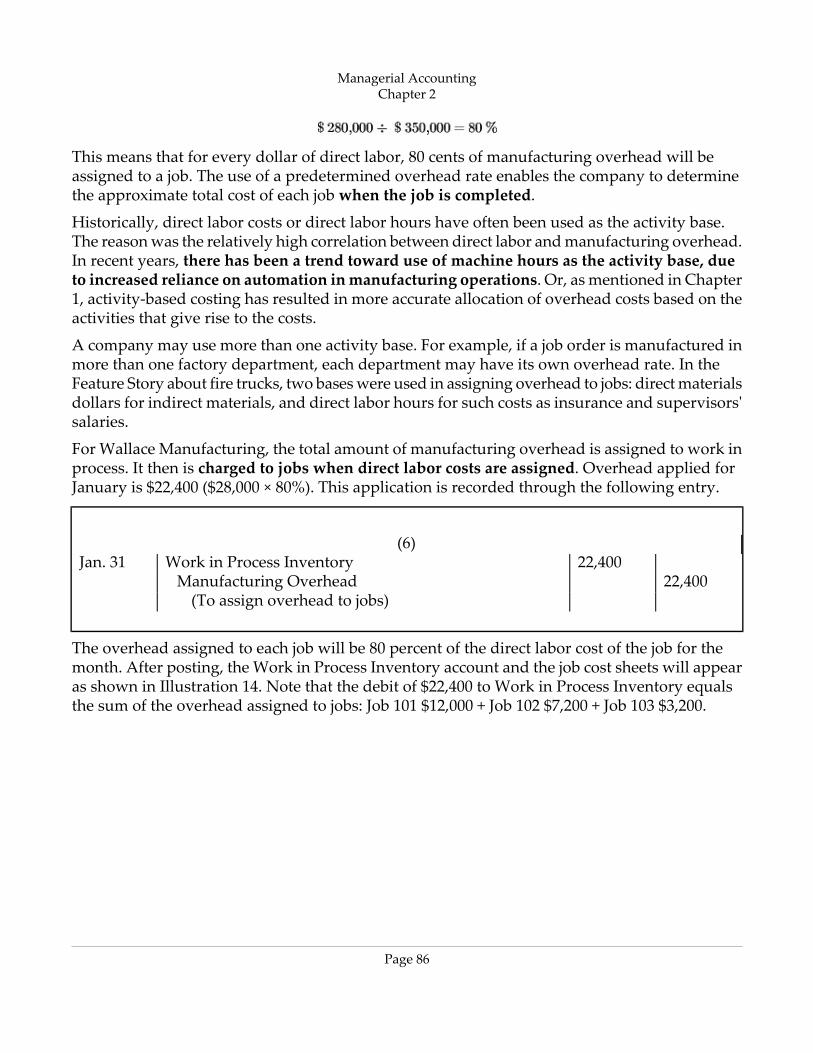

For Wallace Manufacturing, the total amount of manufacturing overhead is assigned to work inprocess. It then is charged to jobs when direct labor costs are assigned. Overhead applied forJanuary is $22,400 ($28,000 × 80%). This application is recorded through the following entry.

(6)22,400Work in Process InventoryJan. 31

22,400Manufacturing Overhead(To assign overhead to jobs)

The overhead assigned to each job will be 80 percent of the direct labor cost of the job for themonth. After posting, the Work in Process Inventory account and the job cost sheets will appearas shown in Illustration 14. Note that the debit of $22,400 to Work in Process Inventory equalsthe sum of the overhead assigned to jobs: Job 101 $12,000 + Job 102 $7,200 + Job 103 $3,200.

Managerial AccountingChapter 2

Page 86

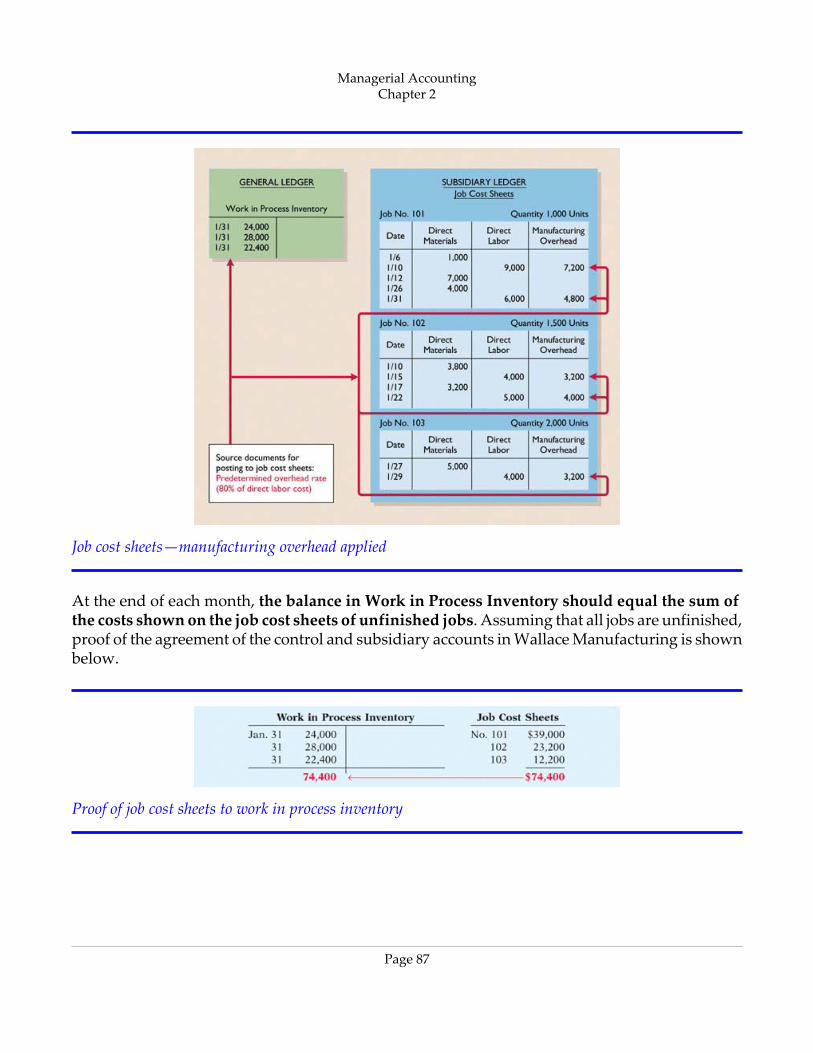

Job cost sheets—manufacturing overhead applied

At the end of each month, the balance in Work in Process Inventory should equal the sum ofthe costs shown on the job cost sheets of unfinished jobs. Assuming that all jobs are unfinished,proof of the agreement of the control and subsidiary accounts in Wallace Manufacturing is shownbelow.

Proof of job cost sheets to work in process inventory

Managerial AccountingChapter 2

Page 87

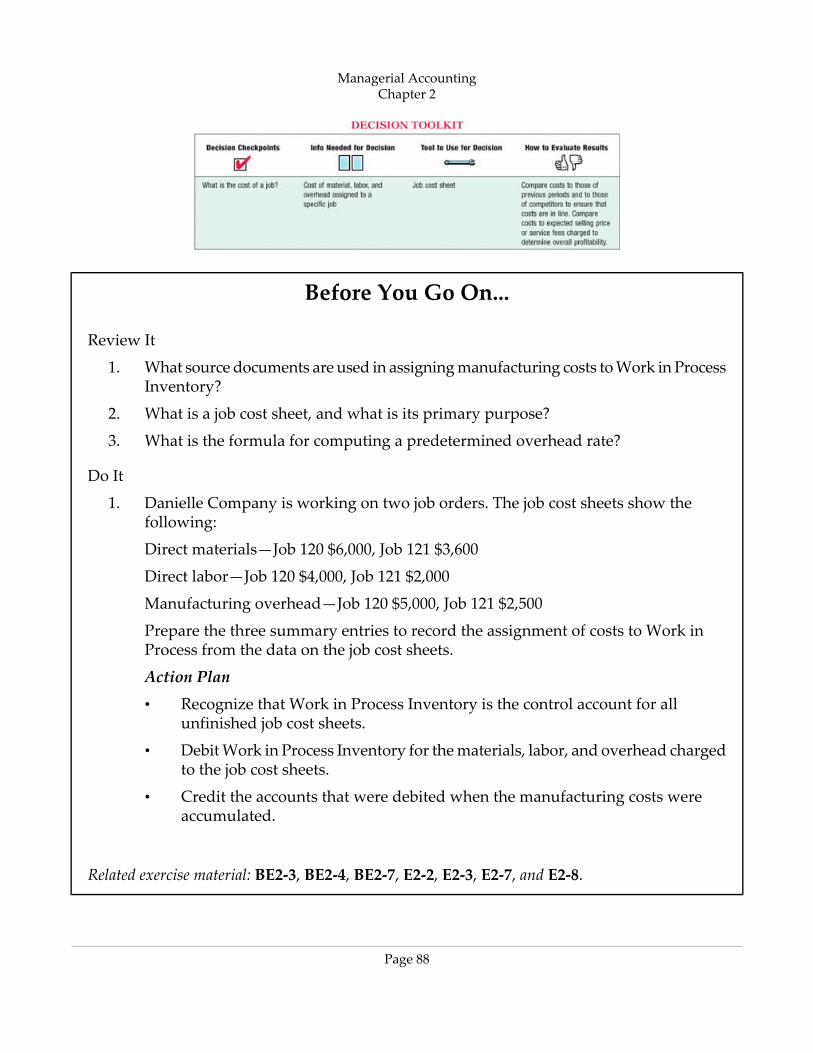

Before You Go On...

Review It

1. What source documents are used in assigning manufacturing costs to Work in ProcessInventory?

2. What is a job cost sheet, and what is its primary purpose?

3. What is the formula for computing a predetermined overhead rate?

Do It

1. Danielle Company is working on two job orders. The job cost sheets show thefollowing:

Direct materials—Job 120 $6,000, Job 121 $3,600

Direct labor—Job 120 $4,000, Job 121 $2,000

Manufacturing overhead—Job 120 $5,000, Job 121 $2,500

Prepare the three summary entries to record the assignment of costs to Work inProcess from the data on the job cost sheets.

Action Plan

• Recognize that Work in Process Inventory is the control account for allunfinished job cost sheets.

• Debit Work in Process Inventory for the materials, labor, and overhead chargedto the job cost sheets.

• Credit the accounts that were debited when the manufacturing costs wereaccumulated.

Related exercise material: BE2‐3, BE2‐4, BE2‐7, E2‐2, E2‐3, E2‐7, and E2‐8.

Managerial AccountingChapter 2

Page 88

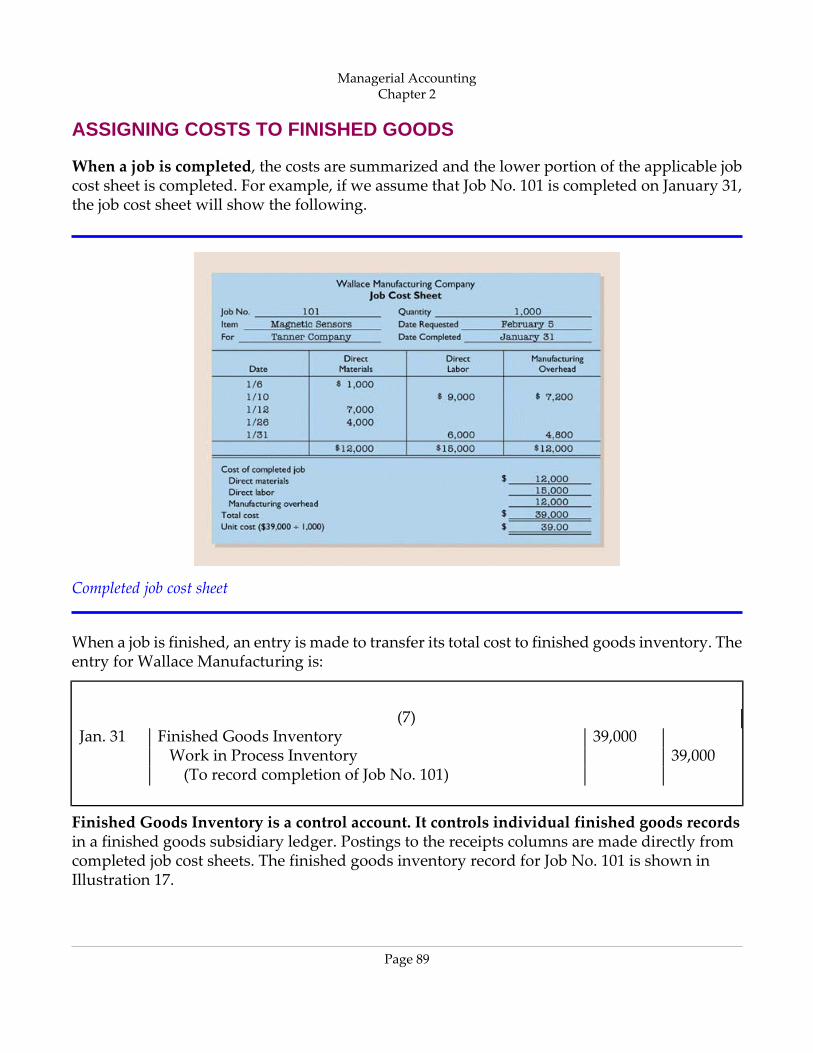

ASSIGNING COSTS TO FINISHED GOODS

When a job is completed, the costs are summarized and the lower portion of the applicable jobcost sheet is completed. For example, if we assume that Job No. 101 is completed on January 31,the job cost sheet will show the following.

Completed job cost sheet

When a job is finished, an entry is made to transfer its total cost to finished goods inventory. Theentry for Wallace Manufacturing is:

(7)39,000Finished Goods InventoryJan. 31

39,000Work in Process Inventory(To record completion of Job No. 101)

Finished Goods Inventory is a control account. It controls individual finished goods recordsin a finished goods subsidiary ledger. Postings to the receipts columns are made directly fromcompleted job cost sheets. The finished goods inventory record for Job No. 101 is shown inIllustration 17.

Managerial AccountingChapter 2

Page 89

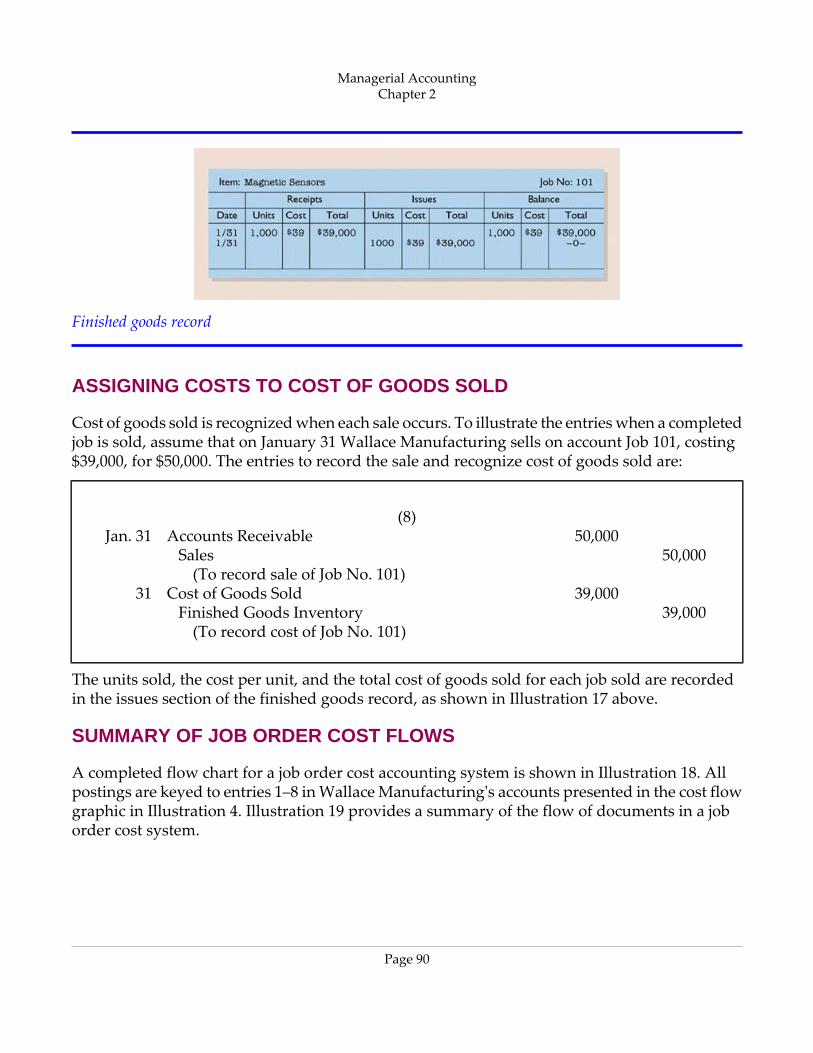

Finished goods record

ASSIGNING COSTS TO COST OF GOODS SOLD

Cost of goods sold is recognized when each sale occurs. To illustrate the entries when a completedjob is sold, assume that on January 31 Wallace Manufacturing sells on account Job 101, costing$39,000, for $50,000. The entries to record the sale and recognize cost of goods sold are:

(8)50,000Accounts ReceivableJan. 31

50,000Sales(To record sale of Job No. 101)

39,000Cost of Goods Sold3139,000Finished Goods Inventory

(To record cost of Job No. 101)

The units sold, the cost per unit, and the total cost of goods sold for each job sold are recordedin the issues section of the finished goods record, as shown in Illustration 17 above.

SUMMARY OF JOB ORDER COST FLOWS

A completed flow chart for a job order cost accounting system is shown in Illustration 18. Allpostings are keyed to entries 1–8 in Wallace Manufacturing's accounts presented in the cost flowgraphic in Illustration 4. Illustration 19 provides a summary of the flow of documents in a joborder cost system.

Managerial AccountingChapter 2

Page 90

Flow of costs in a job order cost system

Flow of documents in a job order cost system

Management Perspective

With the increased sophistication of microcomputers, small manufacturers can now usemicros to perform (1) computer‐aided manufacturing (CAM), (2) computer‐aided testing(CAT), (3) computer‐aided design (CAD), (4) electronic data interchange (EDI), and (5)materials requirement planning (MRP). For a small investment, manufacturers can now usesoftware with capabilities only dreamed about a few years ago.

Managerial AccountingChapter 2

Page 91

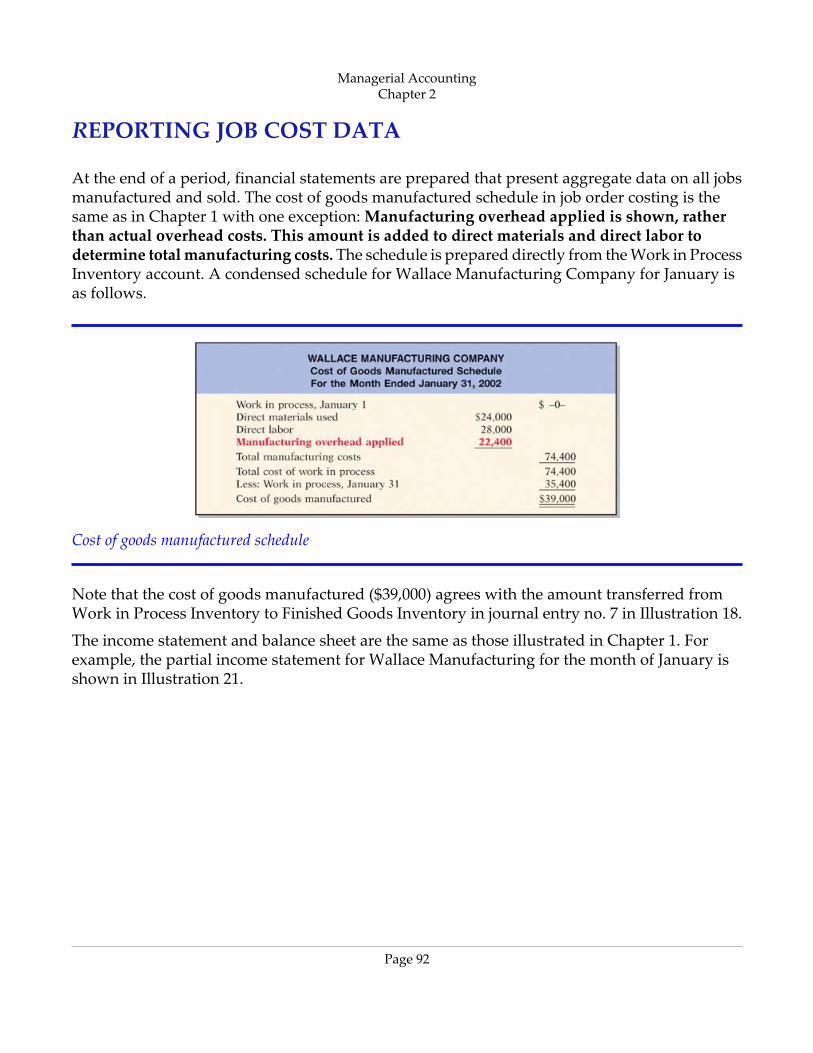

REPORTING JOB COST DATA

At the end of a period, financial statements are prepared that present aggregate data on all jobsmanufactured and sold. The cost of goods manufactured schedule in job order costing is thesame as in Chapter 1 with one exception: Manufacturing overhead applied is shown, ratherthan actual overhead costs. This amount is added to direct materials and direct labor todetermine total manufacturing costs. The schedule is prepared directly from the Work in ProcessInventory account. A condensed schedule for Wallace Manufacturing Company for January isas follows.

Cost of goods manufactured schedule

Note that the cost of goods manufactured ($39,000) agrees with the amount transferred fromWork in Process Inventory to Finished Goods Inventory in journal entry no. 7 in Illustration 18.

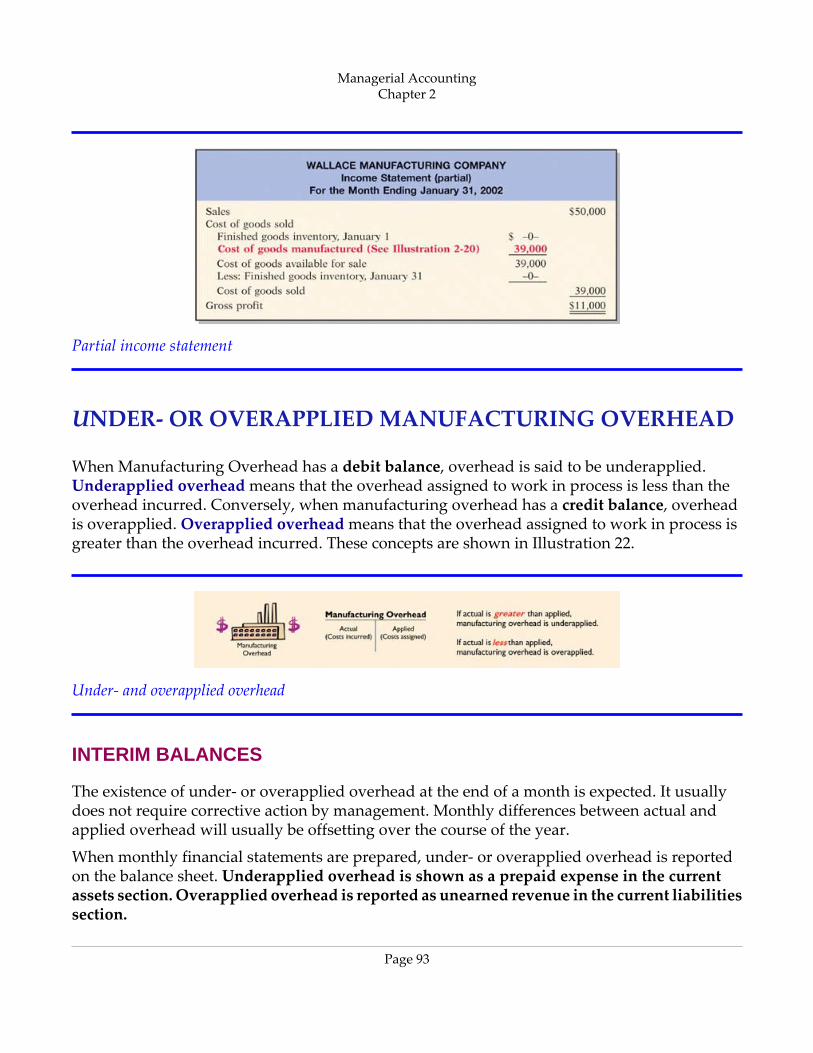

The income statement and balance sheet are the same as those illustrated in Chapter 1. Forexample, the partial income statement for Wallace Manufacturing for the month of January isshown in Illustration 21.

Managerial AccountingChapter 2

Page 92

Partial income statement

UNDER‐ OR OVERAPPLIED MANUFACTURING OVERHEAD

When Manufacturing Overhead has a debit balance, overhead is said to be underapplied.Underapplied overheadmeans that the overhead assigned to work in process is less than theoverhead incurred. Conversely, when manufacturing overhead has a credit balance, overheadis overapplied. Overapplied overheadmeans that the overhead assigned to work in process isgreater than the overhead incurred. These concepts are shown in Illustration 22.

Under‐ and overapplied overhead

INTERIM BALANCES

The existence of under‐ or overapplied overhead at the end of a month is expected. It usuallydoes not require corrective action by management. Monthly differences between actual andapplied overhead will usually be offsetting over the course of the year.

When monthly financial statements are prepared, under‐ or overapplied overhead is reportedon the balance sheet. Underapplied overhead is shown as a prepaid expense in the currentassets section. Overapplied overhead is reported as unearned revenue in the current liabilitiessection.

Managerial AccountingChapter 2

Page 93

YEAR-END BALANCE

At the end of the year, all manufacturing overhead transactions are complete. There is no furtheropportunity for offsetting events to occur. Accordingly, any balance in Manufacturing Overheadis eliminated by an adjusting entry. Usually, under‐ or overapplied overhead is considered to bean adjustment to cost of goods sold. Thus, underapplied overhead is debited to Cost of GoodsSold. Overapplied overhead is credited to Cost of Goods Sold.To illustrate, assume that WallaceManufacturing has a $2,500 credit balance in Manufacturing Overhead at December 31. Theadjusting entry for the overapplied overhead is:

2,500Manufacturing OverheadDec. 312,500Cost of Goods Sold

(To transfer overapplied overhead to cost of goods sold)

After this entry is posted, Manufacturing Overhead will have a zero balance. In preparing anincome statement for the year, the amount reported for cost of goods sold will be the accountbalance after the adjustment for either underor overapplied overhead.

Management Perspective

Overhead also applies in nonmanufacturing companies. The State of Michigan found thatauto dealers were charging documentary and service fees ranging from $18 to $445 perautomobile and inspection fees from $88 to $360. These fees often were charged auto buyersafter a base sales price for the car had been negotiated. The Attorney General of the State ofMichigan ruled that auto dealers cannot charge customers additional fees for routine overheadcosts. The attorney general said: “Overhead is part of the sales price of a motor vehicle.Processing paper work, dealer incurred costs, and inspection fees to qualify cars for extendedwarranty plans are ordinary overhead expenses.”

Conceptually, it can be argued that under‐ or overapplied overhead at the end of the year shouldbe allocated among ending work in process, finished goods, and cost of goods sold. However,most management accountants do not believe allocation is worth the cost and effort. The bulkof the under‐ or overapplied amount will be allocated to cost of goods sold anyway, becausemost of the jobs will be sold during the year.

Managerial AccountingChapter 2

Page 94

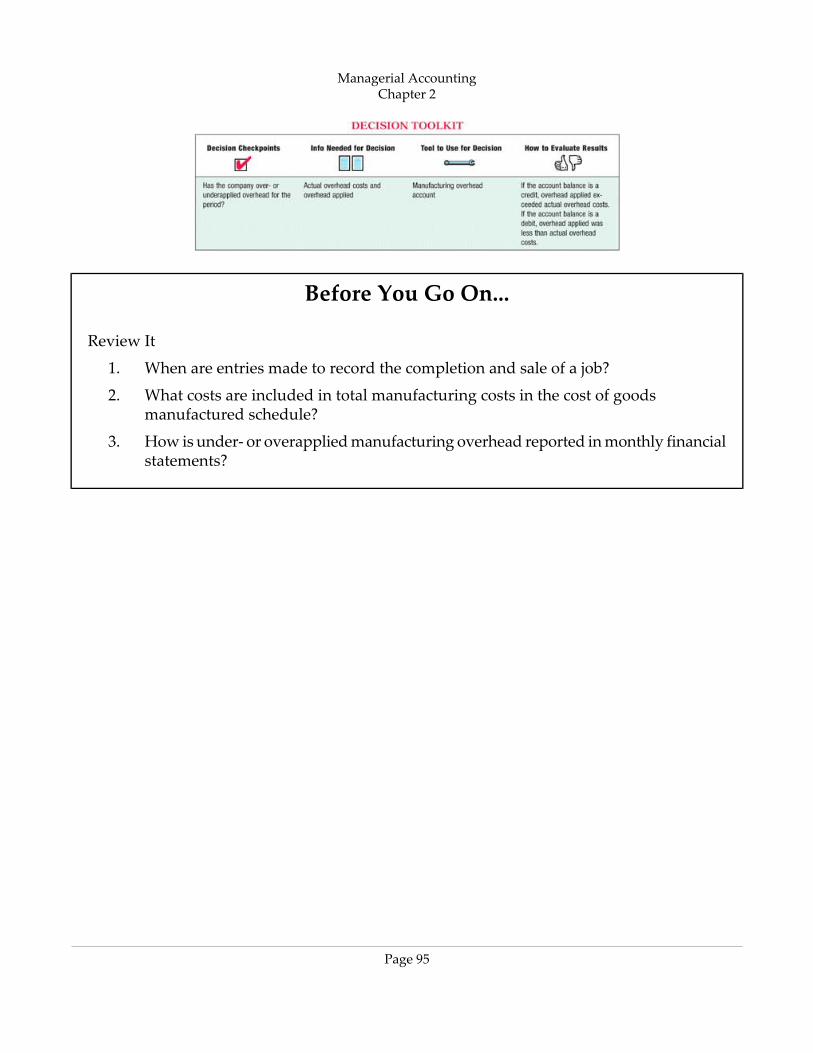

Before You Go On...

Review It

1. When are entries made to record the completion and sale of a job?

2. What costs are included in total manufacturing costs in the cost of goodsmanufactured schedule?

3. How is under‐ or overapplied manufacturing overhead reported in monthly financialstatements?

Managerial AccountingChapter 2

Page 95

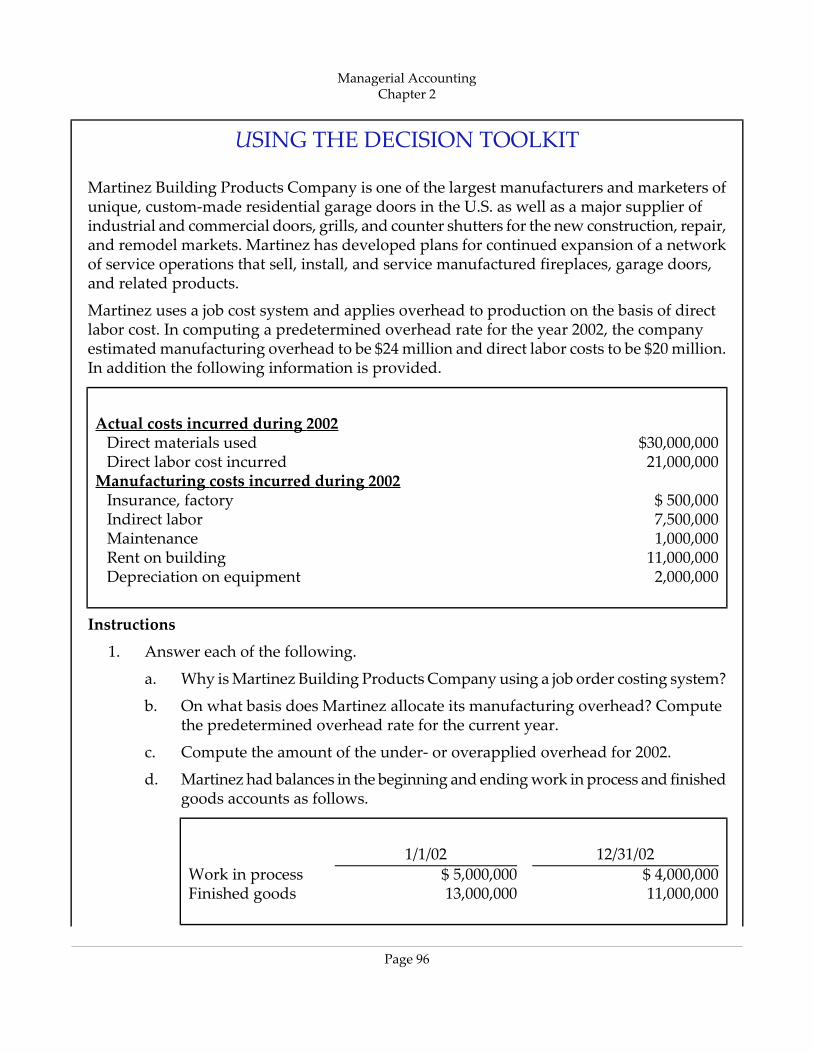

USING THE DECISION TOOLKIT

Martinez Building Products Company is one of the largest manufacturers and marketers ofunique, custom‐made residential garage doors in the U.S. as well as a major supplier ofindustrial and commercial doors, grills, and counter shutters for the new construction, repair,and remodel markets. Martinez has developed plans for continued expansion of a networkof service operations that sell, install, and service manufactured fireplaces, garage doors,and related products.

Martinez uses a job cost system and applies overhead to production on the basis of directlabor cost. In computing a predetermined overhead rate for the year 2002, the companyestimated manufacturing overhead to be $24 million and direct labor costs to be $20 million.In addition the following information is provided.

Actual costs incurred during 2002$30,000,000Direct materials used21,000,000Direct labor cost incurred

Manufacturing costs incurred during 2002$ 500,000Insurance, factory7,500,000Indirect labor1,000,000Maintenance11,000,000Rent on building2,000,000Depreciation on equipment

Instructions

1. Answer each of the following.

a. Why is Martinez Building Products Company using a job order costing system?

b. On what basis does Martinez allocate its manufacturing overhead? Computethe predetermined overhead rate for the current year.

c. Compute the amount of the under‐ or overapplied overhead for 2002.

d. Martinez had balances in the beginning and ending work in process and finishedgoods accounts as follows.

12/31/021/1/02$ 4,000,000$ 5,000,000Work in process11,000,00013,000,000Finished goods

Managerial AccountingChapter 2

Page 96

Determine the (1) cost of goods manufactured and (2) cost of goods sold forMartinez during 2002. Assume that any under‐ or overapplied overhead shouldbe included in the cost of goods sold.

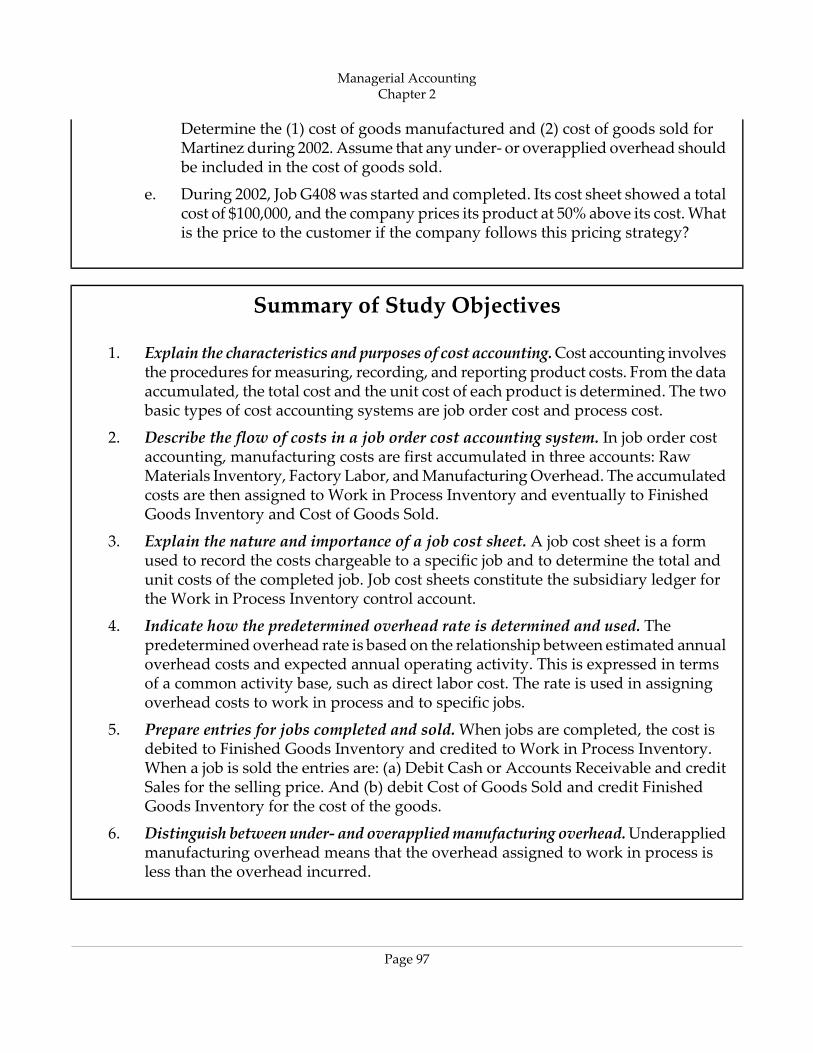

e. During 2002, Job G408 was started and completed. Its cost sheet showed a totalcost of $100,000, and the company prices its product at 50% above its cost. Whatis the price to the customer if the company follows this pricing strategy?

Summary of Study Objectives

1. Explain the characteristics and purposes of cost accounting.Cost accounting involvesthe procedures for measuring, recording, and reporting product costs. From the dataaccumulated, the total cost and the unit cost of each product is determined. The twobasic types of cost accounting systems are job order cost and process cost.

2. Describe the flow of costs in a job order cost accounting system. In job order costaccounting, manufacturing costs are first accumulated in three accounts: RawMaterials Inventory, Factory Labor, and Manufacturing Overhead. The accumulatedcosts are then assigned to Work in Process Inventory and eventually to FinishedGoods Inventory and Cost of Goods Sold.

3. Explain the nature and importance of a job cost sheet. A job cost sheet is a formused to record the costs chargeable to a specific job and to determine the total andunit costs of the completed job. Job cost sheets constitute the subsidiary ledger forthe Work in Process Inventory control account.

4. Indicate how the predetermined overhead rate is determined and used. Thepredetermined overhead rate is based on the relationship between estimated annualoverhead costs and expected annual operating activity. This is expressed in termsof a common activity base, such as direct labor cost. The rate is used in assigningoverhead costs to work in process and to specific jobs.

5. Prepare entries for jobs completed and sold. When jobs are completed, the cost isdebited to Finished Goods Inventory and credited to Work in Process Inventory.When a job is sold the entries are: (a) Debit Cash or Accounts Receivable and creditSales for the selling price. And (b) debit Cost of Goods Sold and credit FinishedGoods Inventory for the cost of the goods.

6. Distinguish between under- and overapplied manufacturing overhead.Underappliedmanufacturing overhead means that the overhead assigned to work in process isless than the overhead incurred.

Managerial AccountingChapter 2

Page 97

Managerial AccountingChapter 2

Page 98

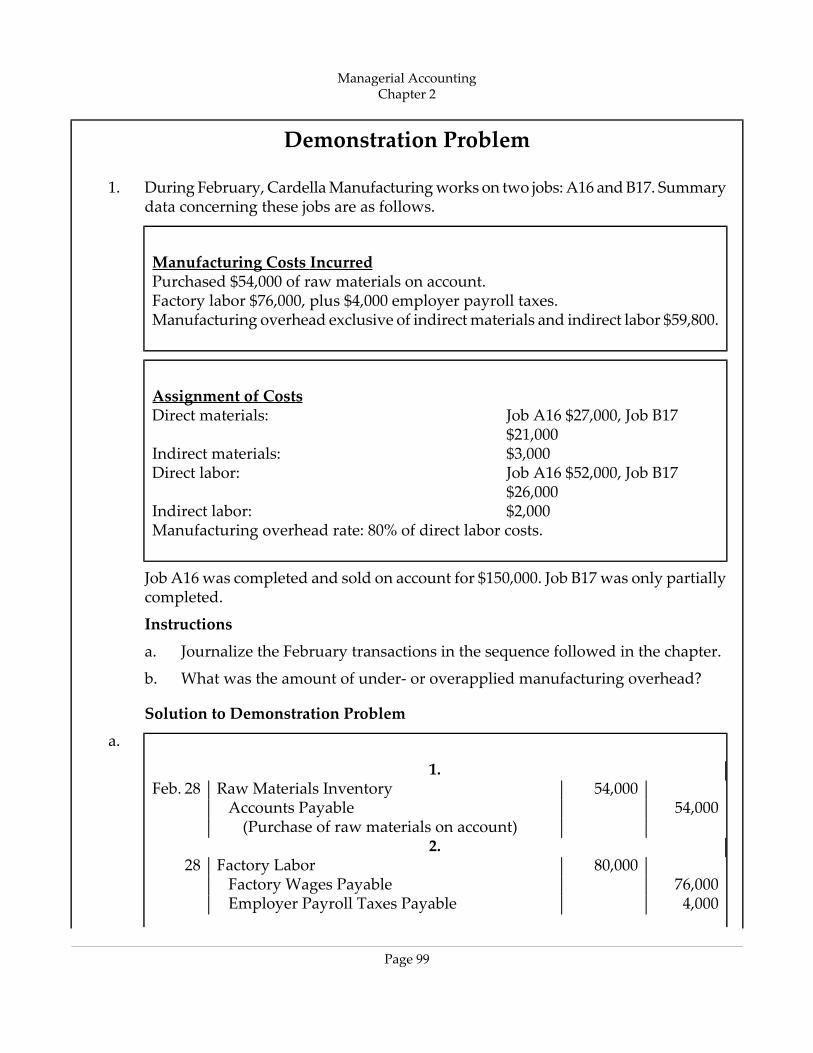

Demonstration Problem

1. During February, Cardella Manufacturing works on two jobs: A16 and B17. Summarydata concerning these jobs are as follows.

Manufacturing Costs IncurredPurchased $54,000 of raw materials on account.Factory labor $76,000, plus $4,000 employer payroll taxes.Manufacturing overhead exclusive of indirect materials and indirect labor $59,800.

Assignment of CostsJob A16 $27,000, Job B17$21,000

Direct materials:

$3,000Indirect materials:Job A16 $52,000, Job B17$26,000

Direct labor:

$2,000Indirect labor:Manufacturing overhead rate: 80% of direct labor costs.

Job A16 was completed and sold on account for $150,000. Job B17 was only partiallycompleted.

Instructions

a. Journalize the February transactions in the sequence followed in the chapter.

b. What was the amount of under‐ or overapplied manufacturing overhead?

Solution to Demonstration Problem

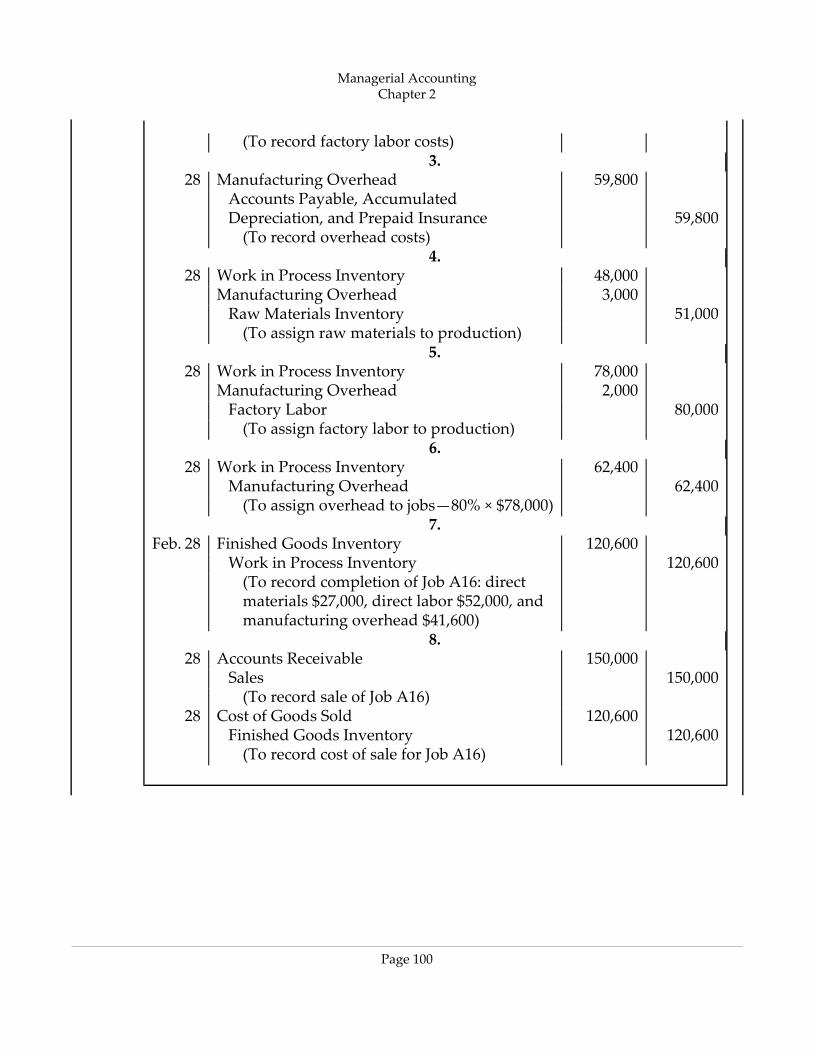

a.

1.54,000Raw Materials InventoryFeb. 28

54,000Accounts Payable(Purchase of raw materials on account)

2.80,000Factory Labor28

76,000Factory Wages Payable4,000Employer Payroll Taxes Payable

Managerial AccountingChapter 2

Page 99

(To record factory labor costs)3.

59,800Manufacturing Overhead28Accounts Payable, Accumulated

59,800Depreciation, and Prepaid Insurance(To record overhead costs)

4.48,000Work in Process Inventory283,000Manufacturing Overhead

51,000Raw Materials Inventory(To assign raw materials to production)

5.78,000Work in Process Inventory282,000Manufacturing Overhead

80,000Factory Labor(To assign factory labor to production)

6.62,400Work in Process Inventory28

62,400Manufacturing Overhead(To assign overhead to jobs—80% × $78,000)

7.120,600Finished Goods InventoryFeb. 28

120,600Work in Process Inventory(To record completion of Job A16: directmaterials $27,000, direct labor $52,000, andmanufacturing overhead $41,600)

8.150,000Accounts Receivable28

150,000Sales(To record sale of Job A16)

120,600Cost of Goods Sold28120,600Finished Goods Inventory

(To record cost of sale for Job A16)

Managerial AccountingChapter 2

Page 100

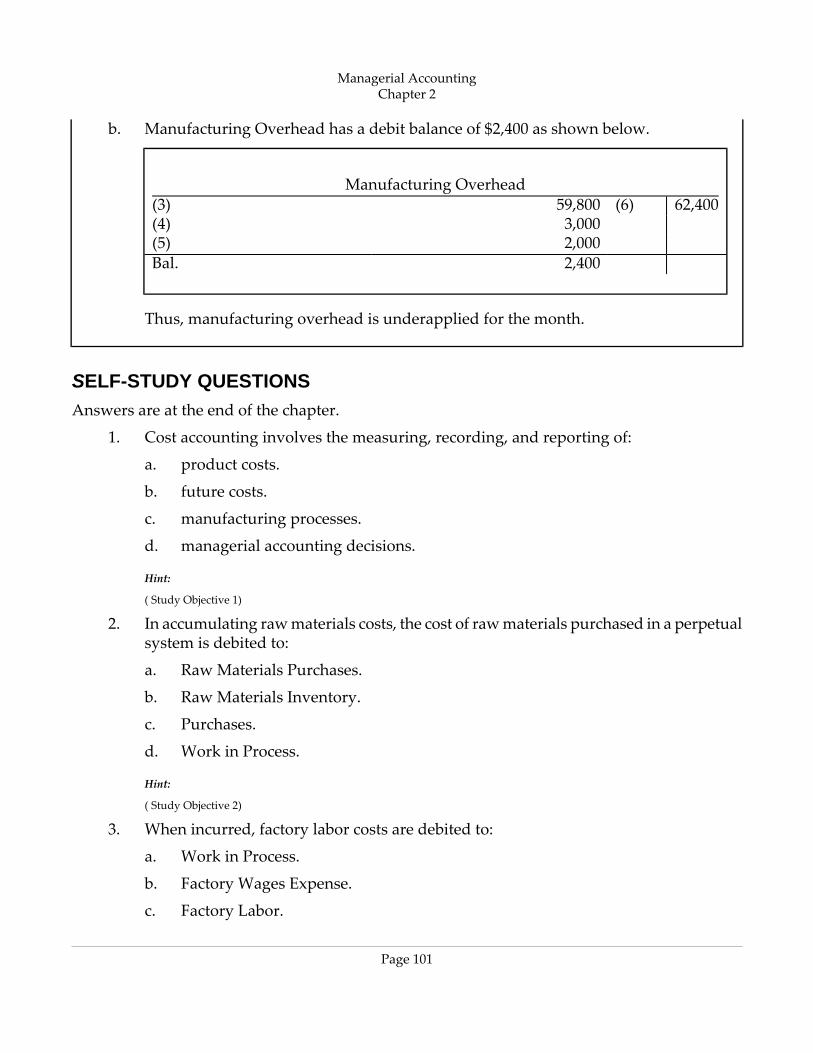

b. Manufacturing Overhead has a debit balance of $2,400 as shown below.

Manufacturing Overhead62,400(6)59,800(3)

3,000(4)2,000(5)2,400Bal.

Thus, manufacturing overhead is underapplied for the month.

SELF-STUDY QUESTIONSAnswers are at the end of the chapter.

1. Cost accounting involves the measuring, recording, and reporting of:

a. product costs.

b. future costs.

c. manufacturing processes.

d. managerial accounting decisions.

Hint:

( Study Objective 1)

2. In accumulating raw materials costs, the cost of raw materials purchased in a perpetualsystem is debited to:

a. Raw Materials Purchases.

b. Raw Materials Inventory.

c. Purchases.

d. Work in Process.

Hint:

( Study Objective 2)

3. When incurred, factory labor costs are debited to:

a. Work in Process.

b. Factory Wages Expense.

c. Factory Labor.

Managerial AccountingChapter 2

Page 101

d. Factory Wages Payable.

Hint:

( Study Objective 2)