24

Managerial Accounting UMST-MBA-BATCH 8 http://omer2t.webs. com

| Date post: | 29-Dec-2015 |

| Category: |

Documents |

| Upload: | warren-morrison |

| View: | 229 times |

| Download: | 5 times |

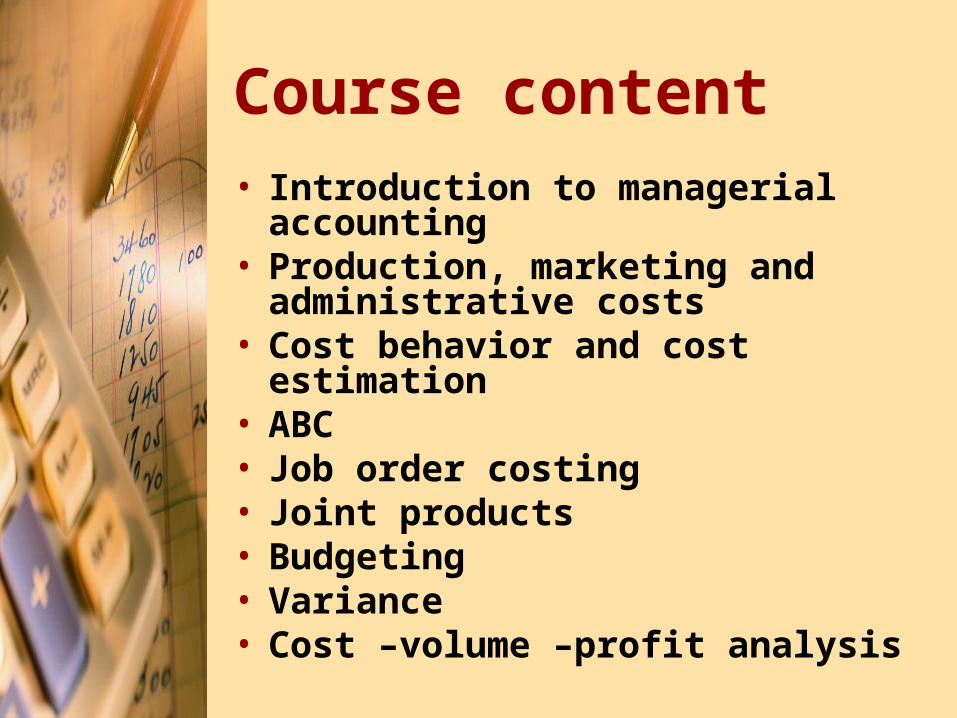

Course content• Introduction to managerial accounting• Production, marketing and

administrative costs• Cost behavior and cost estimation• ABC• Job order costing• Joint products• Budgeting• Variance • Cost –volume –profit analysis

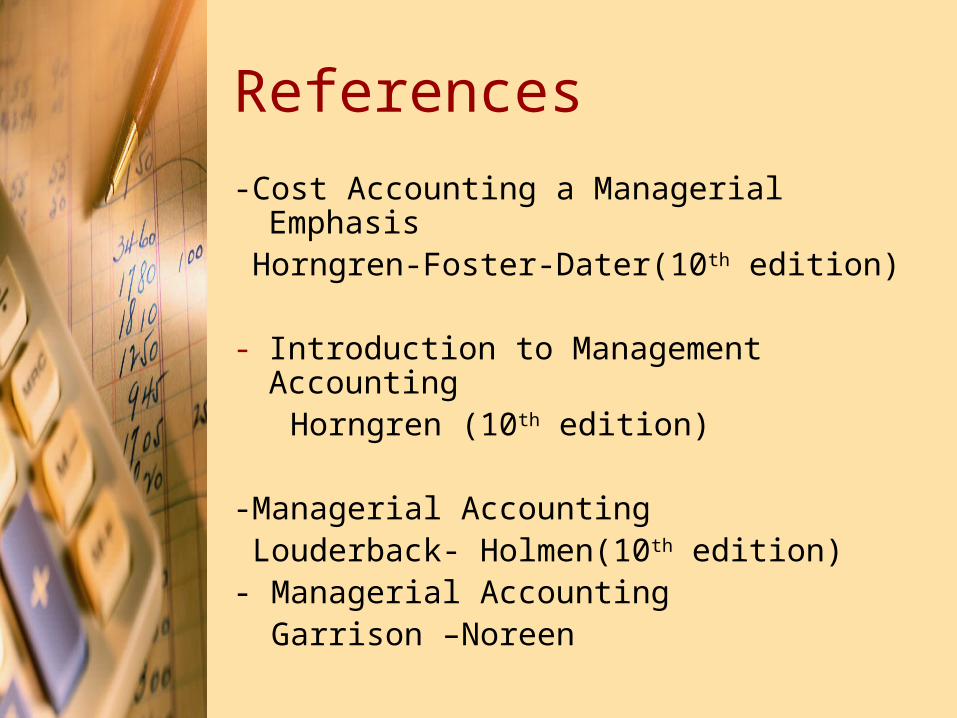

References

-Cost Accounting a Managerial Emphasis Horngren-Foster-Dater(10th edition)

- Introduction to Management Accounting Horngren (10th edition)

-Managerial Accounting Louderback- Holmen(10th edition)- Managerial Accounting Garrison –Noreen

• What is management accounting?

• It is the process of identification, measurement, accumulation, analysis, preparation, interpretation and communication of cost information that assist executive in fulfilling organization objective.

• Accordingly there are two aspects in management accounting

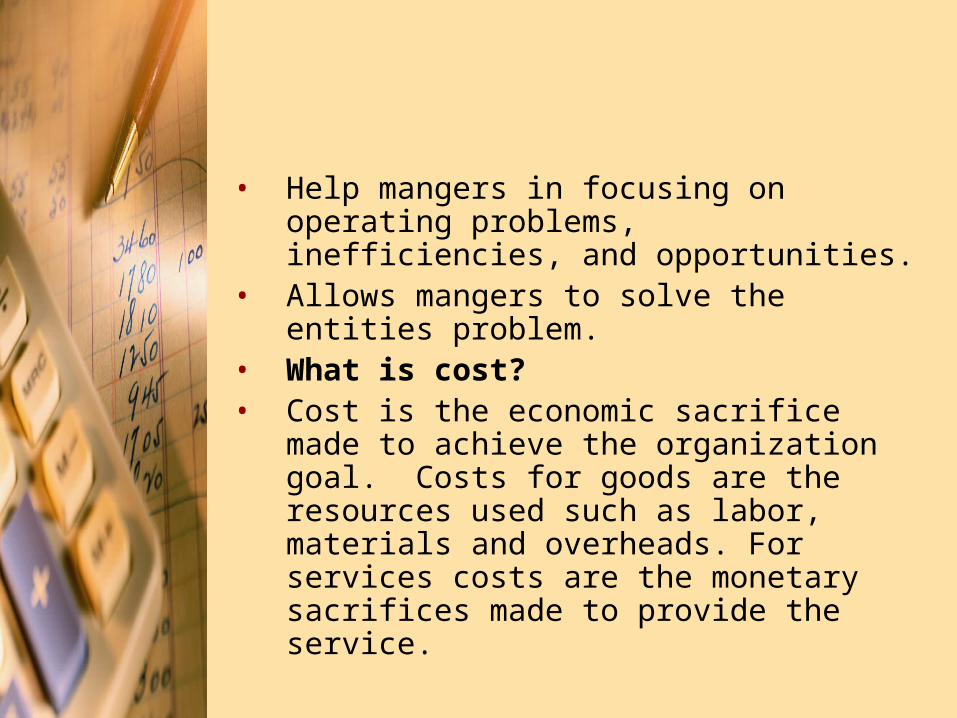

• Help mangers in focusing on operating problems, inefficiencies, and opportunities.

• Allows mangers to solve the entities problem.

• What is cost?• Cost is the economic sacrifice made to

achieve the organization goal. Costs for goods are the resources used such as labor, materials and overheads. For services costs are the monetary sacrifices made to provide the service.

• What is cost accounting?• It is the discipline that identifies, defines,

measures reports and analyzes various elements of direct and indirect costs of goods and services associated with the production and marketing of goods and services. The main objective of cost accounting is communicating financial information to management for planning, controlling and evaluating performances.

Cost and financial accounting

• Cost accounting provides us with cost information which helps in preparing financial statements. Financial accounting provides information for users on the status of assets, liabilities, owners equity and income. In order to prepare these statements cost information is required e.g. inventory and income determination.

Cost behavior

• Costs can be variable, fixed or semi variable.

• Variable costs are costs that vary in direct proportion to change in the cost drive. Direct labor is a good example only if workers are paid by piece.

• Fixed costs are costs that that remain the same despite change in the cost drive e.g. Depreciation, rent and insurance.

• Fixed costs are committed, i.e. they result from previous actions (depreciation). Or they can be discretionary because mgt uses its professional judgment to decide on the amount of cost.

• Semi-variable costs are costs that behave partly as fixed and partly as variable. e.g. indirect labor costs and indirect material.

Role of a cost accountant

• He/ she are responsible for collecting product cost and preparing accurate and timely reports to evaluate and control company operations. This is done by classifying and summarizing economic and financial data and pricing of goods and services. The cost accountant plans and control activities by

• 1. Obtain cost information from different sources.

2. Identify alternatives (what are the different techniques)

3. Make professional judgment to interpret the results.

• The cost accountants perform:

1. Manufacturing function: work closely with the production personnel to measure manufacturing costs.

2. Engineering function: cost accountants translate specifications for new products into estimated costs.

3. Treasurer functions: develop budgets to forecast cash and working capital .This will help in knowing whether there will be excess funds to invest.

4. Financial accounting function: provides the accountant with cost information and this assist in income determination and preparing financial statements.

5. Personnel functions: cost accountants help in administering wages rates.

Why do mangers need cost information?

1. To prepare budget: It is the coordinating the combined intelligence of an entire organization into a plan of action. Budgets include operating budget and financing budget.

• Operating budget is the budget that focuses on the acquisition and use of scarce resources on the other hand financing budget is the budget that focuses on acquiring funds to obtain resources.

2. Cost-volume- profit analysis: mangers of profit seeking organizations usually study the relationship between revenue (sales), expenses (costs) and net income (net profit). The study is commonly called cost-volume-profit analysis. (Break-even analysis)3. Take manufacturing decisions: Mangers by knowing cost information will decide on whether to manufacture or not as cost accountants by working closely with the production personnel measure manufacturing costs.

• 4. Financial accounting function: provides the accountant with cost information and this assist in income determination and preparing financial statements.

• 5. Mangers initially need accounting information to decide on their cost function with the help of a cost accountant. This known as Cost Estimation.

6.Mangers use accounting information to trace costs within departments

• Direct costs arise within the department and are easily traced.

• Indirect costs (common costs) serve two or more departments or cost centers. Therefore they are difficult to trace.

7. Mangers use cost information to decide on the factory application rates of overhead costs

• A cost driver is a factor that that causes the activity to occur. In order to apply overhead costs to product volume related application bases are used.

8. Mangers use accounting data to reduce the spending variance in marketing costs and make proper budgeting and perform segment profitability analysis.

9.Mangers use cost information in pricing decisions Mangers need cost information in order to set prices for their customers. They also have to consider certain determinants such as external determinants of pricing (environment, product characteristics, buying habits) in addition to demand and supply of product.

10.Mangers need cost information to decide on investments

• Investment decisions are basically purchase or disposal of a fixed asset. Mangers also decide on capital expenditure and revenue expenditure. The former is an expenditure that provides a benefit for one or more than accounting period. Capital expenditures are added to the balance of assets. The latter is an expenditure that provides a benefit during a current financial period and it is added to the balance of expenses.

11.Mangers need financial information to decide on operating activities.

• Operating activities: this includes operation that determines operating income. Eg. Receipts include sale of goods. Cash payment includes purchases, purchase of trading securities and interest and tax and finally paying out for expenses. That means these are the transactions relating to items in the income statement.

12.Mangers need financial information to engage in financing activities this includes transactions whereby cash is obtained and repaid to owners and creditors. this include receipts from issuance of stocks and borrowing, payments are in the form of dividends , repay principal amounts borrowed and repurchase of the entity own stock (treasury stocks). This relates to non-current liabilities and equity section of the balance sheet

13. Mangers use cost information as a measure for product quality (from a cost point of view)

• This is done by managing waste products and knowing the number of defective goods. Moreover mangers need to know the number of defective units (they require extra work before being transferred to first quality product.) Treatment of spoilage goods. ( significant imperfection and never first quality after treatment) mangers consider regular spoilage as a cost of goods in that particular job)

• Conclusion

• Costs are crucial in business entities.

• Managers need to know cost information to take various decisions; investing, operating and financing.

• The basic concern of mangers is the bottom-line figure.( gets bigger with smaller costs)