29

ENERGY FORUM Consumers’ Perspective on Energy Issues By Philip Tan Representing FMM August 9, 2010 Sheraton Imperial Hotel, KL

ENERGY FORUM

Consumers’ Perspective on Energy Issues

By Philip TanRepresenting FMM

August 9, 2010

Sheraton Imperial Hotel, KL

2222

Industry’s Concerns

• Benchmark for energy pricing

• Efficiencies in power sector

– Is Electricity tariff COMPETITIVE?

• Disadvantage to industries to be energy efficient through co-

generation; i.e. combined heat and power CHP)

• Other Issues

– Sunday Tariff Rider tariff restricted to Sunday

– Off peak energy should apply to Sunday Tariff Rider

– Special Industrial Tariff – energy intensity vs energy

efficiency

3

ENERGY PRICING

• FMM recognizes that energy pricing should be at

market rate.

• However adjustment to market price must be gradual and

pre-announced to give sufficient time for adjustment.

• Have a transparent and consistent pricing formula for both

natural gas and electricity tariffs to allow the industry to

estimate future price increases.

• Market price of indigenous fuel such as NG should be

benchmarked against an appropriate alternative fuel.

44

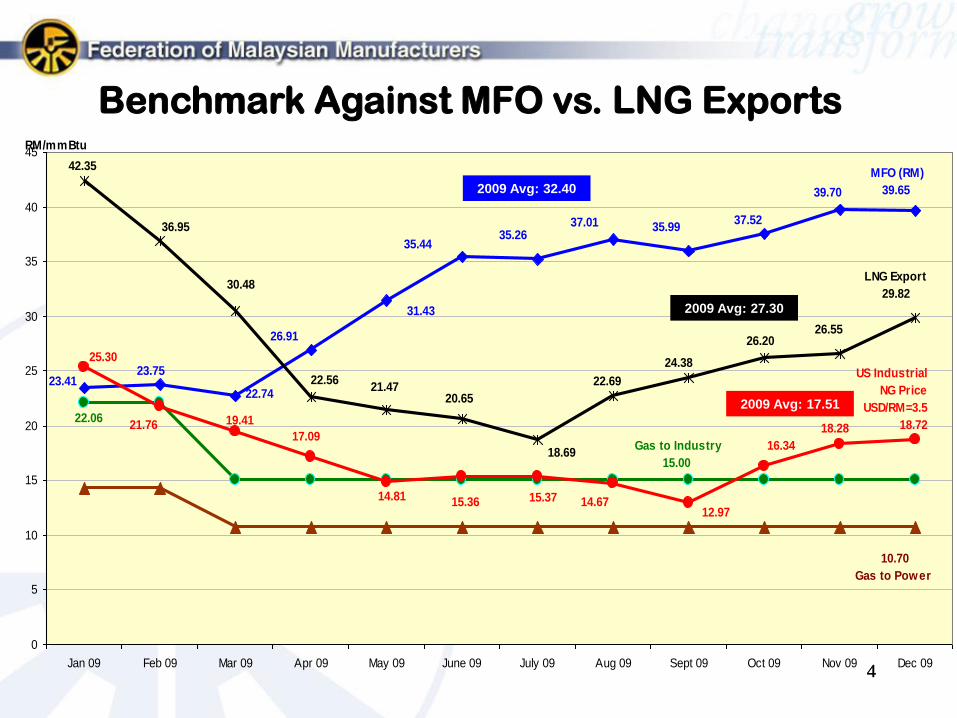

35.9937.0135.26

35.44

31.43

26.91

22.74

23.7523.41

37.52

39.70

MFO (RM)

39.65

10.70

Gas to Power

22.06

Gas to Industry

15.00

42.35

36.95

30.48

22.5621.47

20.65

18.69

22.69

24.38

26.2026.55

LNG Export

29.82

18.28

US Industrial

NG Price

USD/RM=3.5

18.72

16.34

12.9714.6715.3715.3614.81

17.09

19.4121.76

25.30

0

5

10

15

20

25

30

35

40

45

Jan 09 Feb 09 Mar 09 Apr 09 May 09 June 09 July 09 Aug 09 Sept 09 Oct 09 Nov 09 Dec 09

RM/mmBtu

Benchmark Against MFO vs. LNG Exports

2009 Avg: 27.30

2009 Avg: 32.40

2009 Avg: 17.51

5

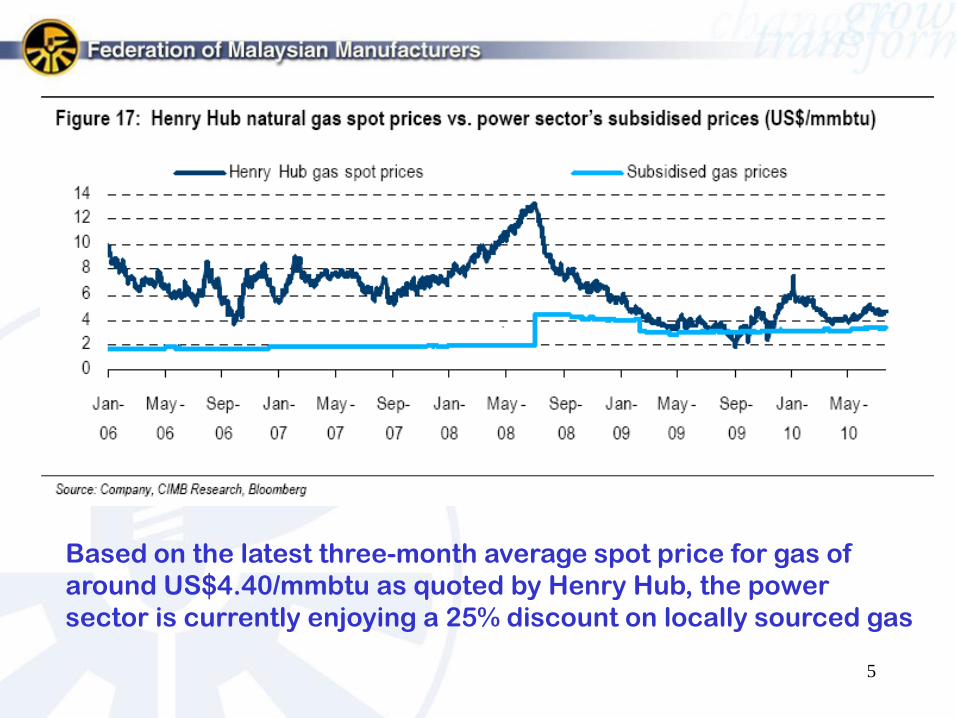

Based on the latest three-month average spot price for gas of

around US$4.40/mmbtu as quoted by Henry Hub, the power

sector is currently enjoying a 25% discount on locally sourced gas

6

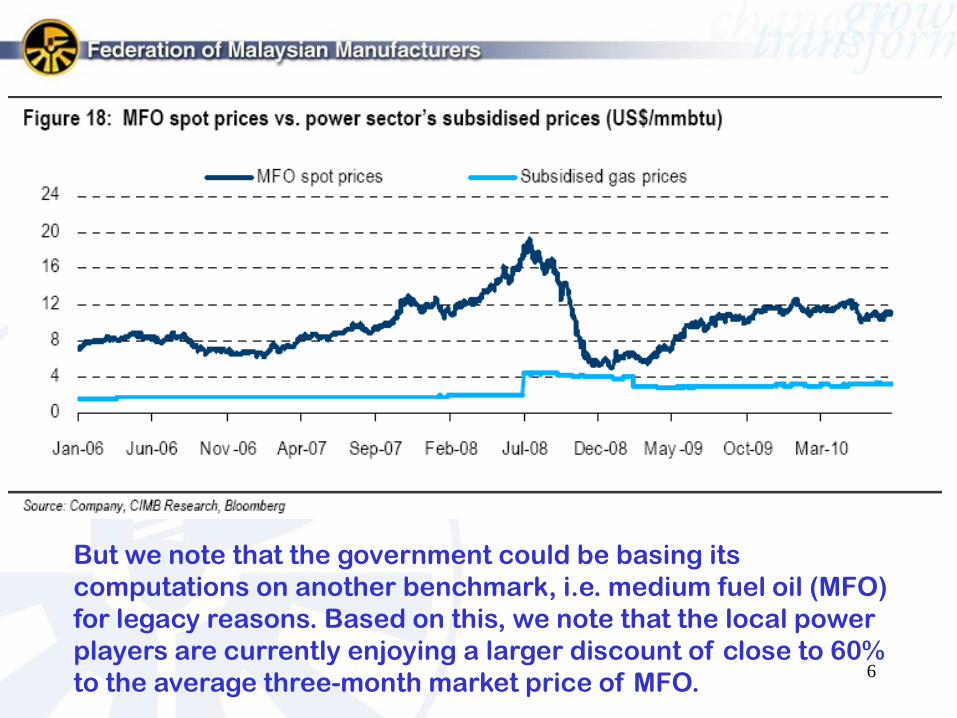

But we note that the government could be basing its

computations on another benchmark, i.e. medium fuel oil (MFO)

for legacy reasons. Based on this, we note that the local power

players are currently enjoying a larger discount of close to 60%

to the average three-month market price of MFO.

7

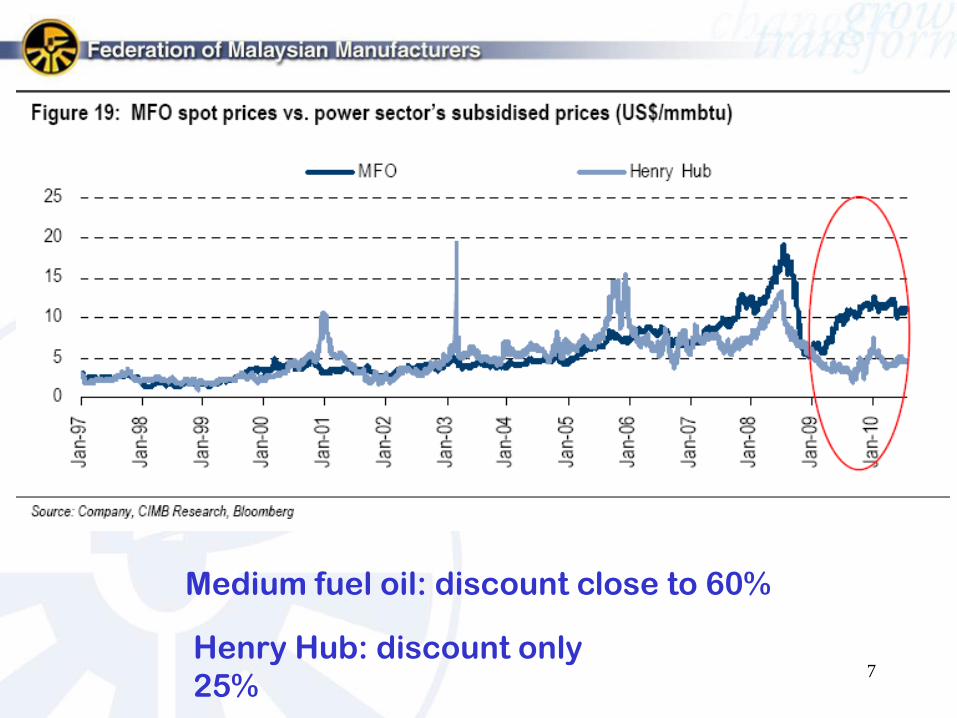

Medium fuel oil: discount close to 60%

Henry Hub: discount only

25%

8

Why MFO?

“We gather that the MFO benchmark has been in place since the 1990s. Back then, MFO prices were used because most of the power plants were running on MFO. Also, looking back at historical prices, MFO and gas prices were generally in sync (Figure 19). But since Jan 09, there has been a clear decoupling of the two benchmarks as MFO prices generally moved in tandem with crude oil prices.”

CIMB Research Report 27 July 2010

9

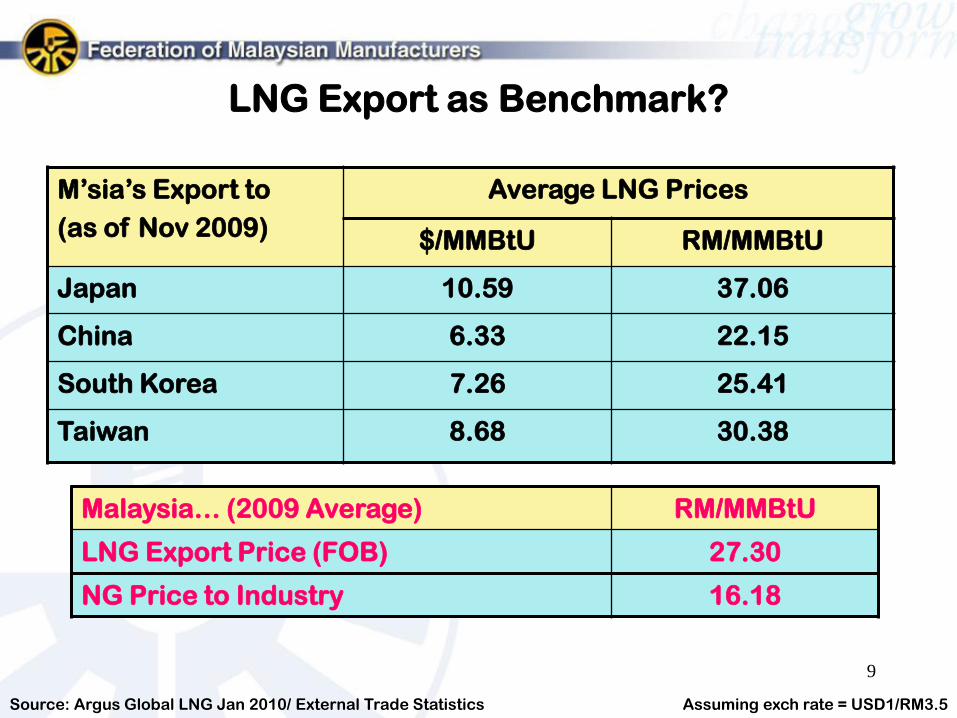

LNG Export as Benchmark?

M’sia’s Export to

(as of Nov 2009)

Average LNG Prices

$/MMBtU RM/MMBtU

Japan 10.59 37.06

China 6.33 22.15

South Korea 7.26 25.41

Taiwan 8.68 30.38

Assuming exch rate = USD1/RM3.5

Malaysia… (2009 Average) RM/MMBtU

LNG Export Price (FOB) 27.30

NG Price to Industry 16.18

Source: Argus Global LNG Jan 2010/ External Trade Statistics

10

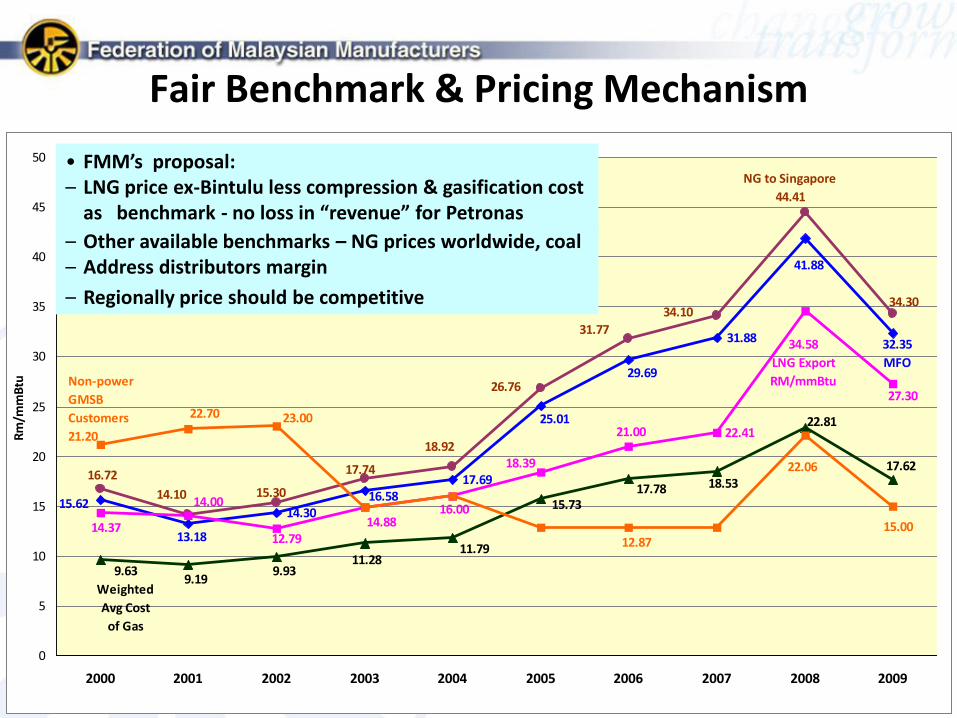

Fair Benchmark & Pricing Mechanism

14.30

17.69

31.88

22.41

41.88

15.62

13.18

16.58

25.01

29.69

32.35

MFO

34.30

16.72

15.30

17.74

18.92

26.76

31.77

34.10

14.10

NG to Singapore

44.41

22.81

18.53

9.63

Weighted

Avg Cost

of Gas

9.199.93

11.2811.79

15.7317.78

17.62

27.30

14.00

14.37

21.00

18.39

12.7914.88

16.00

34.58

LNG Export

RM/mmBtu

15.00

22.06

23.0022.70

Non-power

GMSB

Customers

21.20

12.87

0

5

10

15

20

25

30

35

40

45

50

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Rm

/mm

Btu

• FMM’s proposal: – LNG price ex-Bintulu less compression & gasification cost

as benchmark - no loss in “revenue” for Petronas

– Other available benchmarks – NG prices worldwide, coal– Address distributors margin

– Regionally price should be competitive

11

Efficiencies in Power Sector

12121212

Current Malaysian NG price LOWEST –but HIGH electricity tariff

10.70

20.00

33.56

19.40

29.45

34.40 33.03

20.76

34.6033.59

44.17

0

5

10

15

20

25

30

35

40

45

50

Gas to Power (RM/mmBtu) Electricity HT(sen/kWh) Electricity LT(sen/kWh)

Ma

lays

ia

Ma

lays

ia

Ma

lays

ia

Th

ail

an

d

Th

ail

an

d

Th

ail

an

d

Sin

ga

po

re

Ind

on

esia

Sin

ga

po

re

Sin

ga

po

re

Ind

on

esia

M’sian NG price• 1/3 Singapore• 1/2 Thailand

M’sian electricity (High Tension)• 90% Singapore• 86% Thailand

M’sian electricity(Low Tension) • 78% Singapore• 103% Thailand

Note: As of 2009

13

SAHA’s Study Review of Future Tariff

Proposal

• SAHA met with FMM during their study to design a future tariff

structure in Peninsular Malaysia and Sabah

• FMM understands that future tariff structure could be based on

incentive based regulation as against cost of service regulation.

• Towards this end the tariff rates associated for the regulated assets

for distribution and for transmission would be separately

identified.

• Understand only the regulated assets for transmission and

distribution would be considered. Tariffs justification would be

made known and subjected to consultation, review and written

comments/arguments by all stakeholders including FMM.

14

Transparency in Cost and Price

• FMM recognizes that companies (including utilities and IPPs) need to

earn reasonable return for their investment. As utilities' tariffs are not

subjected to competition but are of general public interest (including to

members of FMM) the costs and prices for various parts of the supply

chain be must transparent so that any inefficiencies could be identified

and hopefully corrected.

• Towards transparency FMM believes that the cost and prices for the

following should be available and published:

a. Non fuel IPPs’ unit cost and utility margin;

b. Power utilities own non fuel generation cost and price per unit,

c. Transmission cost and price per unit,

d. Distribution cost and price per unit,

e. Gas utilities’ cost and price of transmission.

15

Transparency in IPPs’ Costs

• FMM believes that each IPP’s costs for non-fuel and non fuel, generation amount sold to utilities should be made available to the public.

• With incentive based regulation, FMM believe that the following monetary values should be treated as follow:

a. Deduction of payments for not meeting guarantees not be to the sole benefit of the utilities but to the consumers as well,

b. Fuel advantages should shared on a win-win-win arrangement without setback to IPPs when gas was at RM6.40/MMBTU as follow:

- Allow offline water washing without imposition of UOR,

- Share fuel advantage in proportion 1:1:2 among IPP, TNB and consumers.

16

Historical Baggage Still in Place

that Discourages Co-generation

17

Support for CO-GENERATION• Co-generation or Combined Heat and Power (“CHP”) - most effective

way with regards to energy efficiency

• Because we produce electricity and capture waste heat from power generation to steam simultaneously rather than wasting it.

• Non recovered losses of generation: Gas Turbine: 62% at exhaust Conventional Power Plant : 49.5% at condenser Combined Cycle : 33% at condenser GT/HRSG as Cogeneration : 11% of input

• Remove impediments to co-generation activities High standby charges – barrier to entry (RM25/kW/month) Penalty for exceeding demand

No support for buying firm excess supply TNB buys excess electricity at uneconomical price set at lowest avoided cost

Co-generation can achieve efficiency greater than 80%

1818

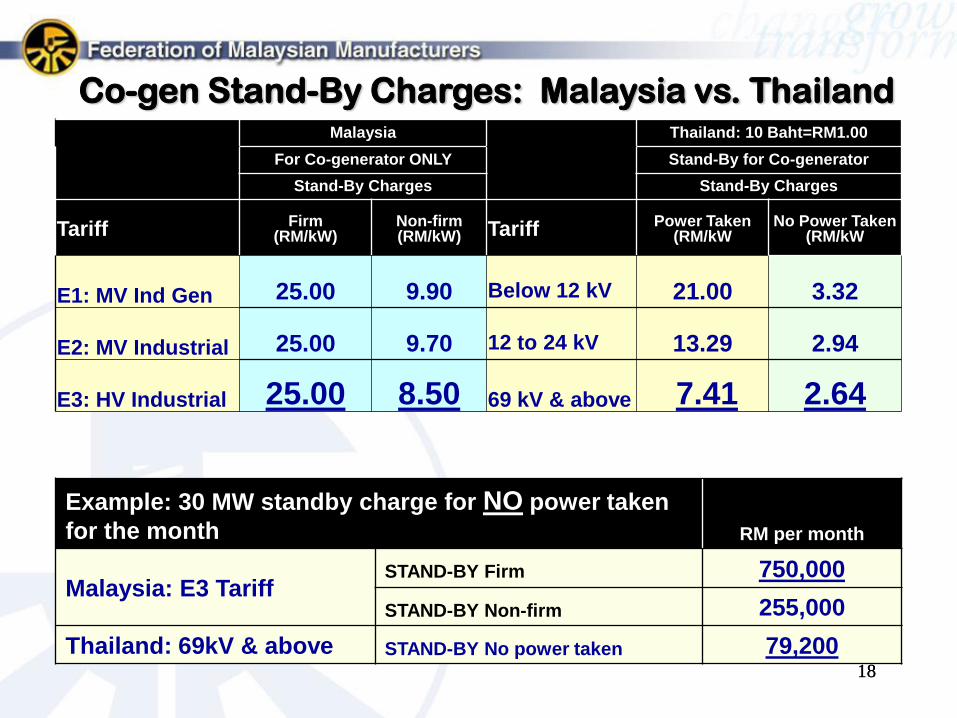

Co-gen Stand-By Charges: Malaysia vs. ThailandMalaysia Thailand: 10 Baht=RM1.00

For Co-generator ONLY Stand-By for Co-generator

Stand-By Charges Stand-By Charges

Tariff Firm(RM/kW)

Non-firm(RM/kW) Tariff Power Taken

(RM/kWNo Power Taken

(RM/kW

E1: MV Ind Gen 25.00 9.90 Below 12 kV 21.00 3.32

E2: MV Industrial 25.00 9.70 12 to 24 kV 13.29 2.94

E3: HV Industrial 25.00 8.50 69 kV & above 7.41 2.64

Example: 30 MW standby charge for NO power taken

for the month RM per month

Malaysia: E3 TariffSTAND-BY Firm 750,000

STAND-BY Non-firm 255,000

Thailand: 69kV & above STAND-BY No power taken 79,200

19

Rules for Charging Standby

• Firm Standby Rates should not be more than 20% of TNB’s actual

price of capacity charge rate for each Tariff Category.

• No Non-Firm Standby Rates to be charged for Non-Firm Standby.

If electricity is used within any month, the tariff for use is to

follow the respective Tariff Category.

• Top-up consumers to follow the electricity tariff as for normal

consumers for each Tariff Category.

• No additional penalty charge for standby and top-up consumers

that take electricity higher than the Average Load Factor of

Respective Tariff Category.

• Equitable measures to be drawn up to protect TNB from gaming

by customers and for standby customers not able to maintain at

reference plant availability (90%).

20

Rules for Charging Standby

• Appropriate incentive for co-generators able to operate at

availability greater than power section average for thermal

power plants.

• Qualifying Factor for allowing co-generation to be set at that of

the power plant with the highest efficiency in the grid system

prevailing at the time of issuing the license (TNB saves 12% in

transmission and distribution losses). Alternatively follow

Qualifying Factor of Thailand and USA.

• Co-generators with surplus firm capacity be paid at 5% discount

of capacity rate (capacity rate financial plus fixed O&M) for the

most recently signed financeable IPP with TNB in Malaysia (not

majority owned by TNB). The energy charge is to be the

average avoided cost of variable energy to TNB.

• Co-generators with only non-firm capacity to be paid only on

energy charge which is to be average avoided cost on variable

energy to TNB.

21

Sunday Tariff Rider

• When the Sunday Tariff Rider was offered, FMM initially thought

that Sunday usage would be considered as off-peak rates.

• When then, when FMM ask at MITI dialogue with presence of

utility, that the Rider be applied to Saturday. FMM was told

Saturday demand pattern is similar to weekday.

• When FMM met with the previous Chairman on the matter, FMM

was told otherwise. FMM was supplied the demand patterns in

the next couple of slides.

• Subsequently, on closer examination, FMM realized that only

Maximum Demand recorded is not counted under the Sunday

Tariff Rider. Peak energy charge still applies. Where is the

benefit?

2222

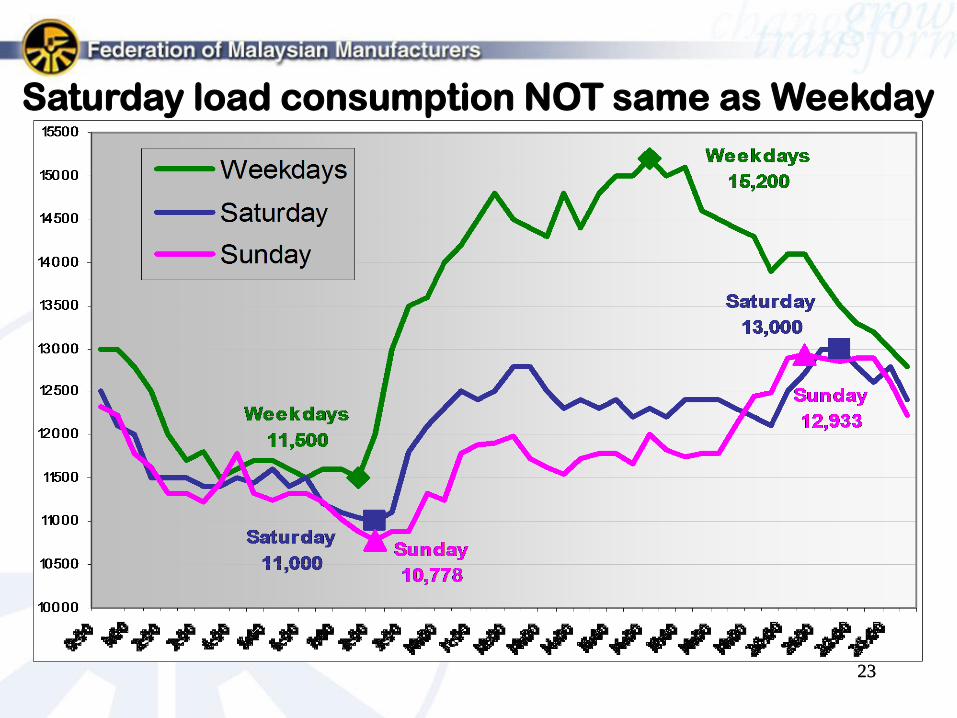

Saturday & Sunday load consumption similar pattern

but Sunday Tariff Rider only for Sunday

2323

Saturday load consumption NOT same as Weekday

24

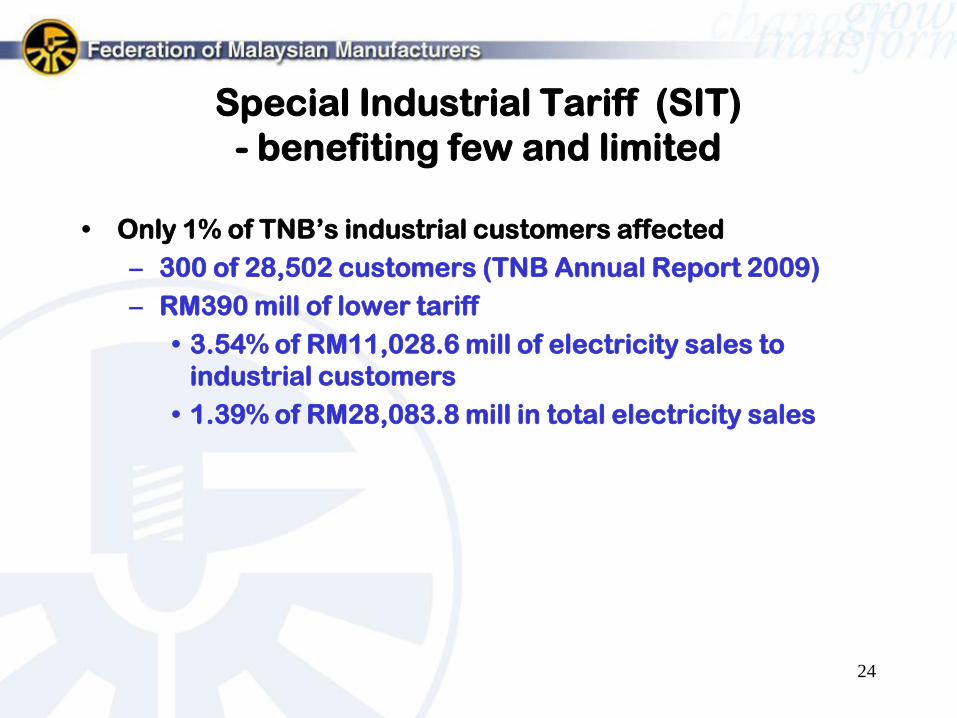

Special Industrial Tariff (SIT)

- benefiting few and limited

• Only 1% of TNB’s industrial customers affected

– 300 of 28,502 customers (TNB Annual Report 2009)

– RM390 mill of lower tariff

• 3.54% of RM11,028.6 mill of electricity sales to

industrial customers

• 1.39% of RM28,083.8 mill in total electricity sales

25

PRESS RELEASE BY FMM

on March 3, 2010

FMM recognizes that energy pricing should be at market rate. However, as with all changes to policies that have an impact on operating costs, FMM had requested the Government to ensure that the move to market price should:

• Be gradual and pre-announced to give sufficient time for adjustment;

• Have a transparent and consistent pricing formula for both natural gas and electricity tariffs to allow the industry to estimate future price increases;

26

Continued

• Be fair: i.e. to benchmark against an appropriate

alternative fuel and to ensure that supply chain

inefficiencies are not passed through to users.

FMM’s view is that an appropriate benchmark should be

the free-on-board price of liquefied natural gas that

Malaysia itself exports to other countries from Bintulu,

which is lower than the current domestic market price after

deducting transportation and gasification/degasification

costs!

FMM is also strongly of the view that the power sector

should ONLY be allowed to pass through increase in fuel

prices to consumers – not their other operating

inefficiencies.

27

Continued

• Practice domestic market obligation (DMO): i.e. to

ensure sufficient supply of the country’s natural fuel

resources for use by industries in Malaysia to increase

value-add and higher economic returns. In this respect,

FMM has also been calling on the Government to review

the export quantum to address the shortfall of fuel

resources in Peninsula Malaysia as well as to conserve the

national stockpile.

28

Recommendations• Improve efficient use of natural resources

• Establish effective subsidy transition programme

• Pre-announced review of prices, consistent & transparent formula

• Reference to a fair benchmark

– LNG price ex-Bintulu net back to price of natural gas cost supplied to LNG plant

• Maintain minimum of WACC for regulated assets because:

–NG is national resource – competitive advantage

–Spin-off and multiplier effects from industry

–Power sector provides basic energy – electricity

• Priority of supply - domestic market obligation

• Support co-gen among users of NG, reward efficient users

• Reform energy sector – market liberalization

• Address LEAKAGES – utilities efficiency, distributors margins

Thank You

![FMM / RCWA [S-Matrix] - LightTrans · 2020. 6. 8. · FMM / RCWA [S-Matrix] For the Grating Component VirtualLab Fusion Technology – Solvers and Functions. 2 Abstract The FMM/RCWA](https://static.documents.pub/doc/80x56/5fde654591cfa4041813fdb7/fmm-rcwa-s-matrix-lighttrans-2020-6-8-fmm-rcwa-s-matrix-for-the-grating.jpg)