Forrester Research, Inc., 60 Acorn Park Drive, Cambridge, MA 02140 USA Tel: +1 617.613.6000 | Fax: +1 617.613.5000 | www.forrester.com Mapping The Connected World by Christopher Mines and Michele Pelino, October 31, 2013 For: CIOs KEY TAKEAWAYS Technology Maturity Outstrips Operational And Process Maturity e technology of connected world systems -- sensors, networks, analytics soſtware -- is maturing rapidly. But incorporating the real-time data from physical assets requires processes, staffing, and skills changes that are more difficult than technology implementations. The Ripest Connected World Opportunities Are Out Of The Spotlight While smart homes and cool personal gadgets get the press, non-glamour applications get the traction. e connected world will come first to warehouses, trucks, factories, and farms. Aggregators And Integrators Have Crucial Advantages Over OEMs Product manufacturers are building connectivity into everything from appliances to autos to HVAC systems. But these our-gear-only solutions will over time be superseded by data aggregators and systems integrators that pull together heterogeneous sets of assets.

Transcript

Forrester Research, Inc., 60 Acorn Park Drive, Cambridge, MA 02140 USA

Mapping The Connected Worldby Christopher Mines and Michele Pelino, October 31, 2013

For: CIOs

Key TaKeaways

Technology Maturity Outstrips Operational and Process MaturityThe technology of connected world systems -- sensors, networks, analytics software -- is maturing rapidly. But incorporating the real-time data from physical assets requires processes, staffing, and skills changes that are more difficult than technology implementations.

The Ripest Connected world Opportunities are Out Of The spotlightWhile smart homes and cool personal gadgets get the press, non-glamour applications get the traction. The connected world will come first to warehouses, trucks, factories, and farms.

aggregators and Integrators Have Crucial advantages Over OeMsProduct manufacturers are building connectivity into everything from appliances to autos to HVAC systems. But these our-gear-only solutions will over time be superseded by data aggregators and systems integrators that pull together heterogeneous sets of assets.

A technology revolution is brewing that uses sensors, networks, and analytics software to connect physical objects and infrastructure to computing systems, providing an unprecedented view into the status, location, and activities of products, assets, and people. By understanding the landscape of the connected world, business technology leaders can prepare their firms for the implications — positive and negative — of optimizing assets, differentiating products and services, and transforming customer relationships. In this report, we separate the hype from reality by mapping the landscape of the emerging connected world and analyzing the maturity of different industry sectors and applications.

Table of Contents

welcome To The Connected world

separating Connected world Hype From Reality

Mapping The Landscape Of The Connected world

Buyers Face a Complex and shifting Vendor Menagerie

reCommendaTIons

CIOs Must Link Connected world Tech with Business Outcomes

WHaT IT means

The Connected world Foments a data economy

supplemental Material

notes & resources

Forrester interviewed 27 companies involved in developing and implementing connected world solutions.

related research documents

smart Products Will require a Hybrid CTo/CIo skill setnovember 16, 2012

Prepare Your security organization For The Internet of Thingsoctober 23, 2012

smart Computing Connects CIos With The Businessmarch 28, 2012

Mapping The Connected worldsoftware Control of The Physical World Will Change Your Businessby Christopher mines and michele Pelinowith Charles s. Golvin, Holger Kisker, Ph.d., sharyn Leaver, and Joanna Clark

A new technology revolution is brewing that uses sensors, networks, and analytics software to connect physical objects and infrastructure to computing systems, providing unprecedented visibility and control of the status, location, and activities of products, assets, and infrastructures. Connected world solutions link physical assets to analytics and control systems through the Internet, allowing firms to take action based upon comprehensive and real-time understanding of situations.

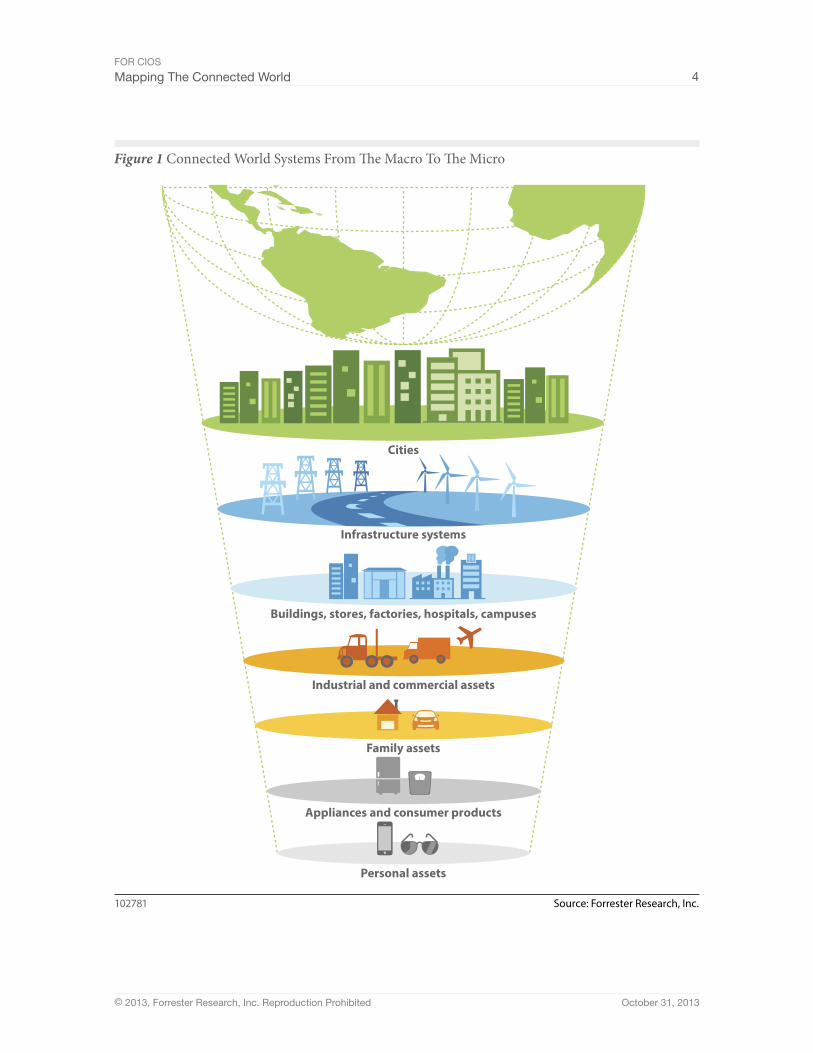

The connected world is being built in the macro — integrating sprawling infrastructure systems like electricity grids and water systems — and in the micro — with tiny, single-function sensors that count steps or send a text if they get wet (see Figure 1).

We are on the threshold of a connected world where digital-to-physical awareness, analysis, and actions will enable improved business outcomes in environments as diverse as:

■ The wired farm. Connected world solutions are used to automate the farming industry. Farmers use data from soil monitors, remote irrigation equipment, smart tractors, and micro-weather forecasts to determine what to plant, when to plant, when to irrigate, when to fertilize, and when to harvest. Tom Farms, 16,000 acres across 30 square miles and six Indiana counties, uses connected world systems like these to determine which types and density of seeds to plant according to soil composition and weather conditions. By adapting farming practices to automated data input and analysis, farmers improve short-term crop yield and their long-term utilization of cropland, workers, machines, and financial resources.

“I have not been inside a tractor in years. I sit behind a desk to monitor and manage farm operations.” (Kris Tom, partner, Tom Farms)

■ The automated factory floor. Manufacturers use connected world solutions to improve the automotive production process and reduce manufacturing hours per vehicle. Keller und Knappich Augsburg (KUKA) Robotics manufactures industrial robots and factory automation solutions with 25 subsidiaries worldwide, including a plant in Toledo, Ohio, which produces more than 800 Jeep Wrangler bodies per day. Factory workers and managers, on-site and remote, get real-time inputs from sensors, cables, laser readings, and pressure switches to monitor and manage every step of the production process and ensure that each body meets its specs. Manufacturing personnel access a portal site to validate, verify, and identify voltage, amperage, and temperature from robots on the assembly line. And managers at KUKA headquarters in Germany can link to shop floor in Toledo to view real-time production data and feedback from the factory.

“Anything that reduces equipment downtime is money well spent. We ship one car body every 77 seconds. If it takes us 78 seconds, we have cost the whole enterprise lost opportunity.” (Jake Ladouceur, managing director, KUKA Toledo Production Operations)

■ The monitored healthcare delivery system. Monitoring “cold chain” delivery for suppliers of perishable goods or bio/medical samples is fast becoming a keystone connected world application. Solutions enable courier services and healthcare logistics providers like McKesson to monitor the condition of temperature-sensitive samples in real time. With regulators tightening their scrutiny of cold chain quality, alerts that help prevent ruined samples and provide end-to-end reporting of sample handling become more important to hospitals and their suppliers. Sensor-enabled cold chain monitoring is transforming the process of tracking deliveries of blood tests and other lab samples.

“Cold chain monitoring breaks down the second the sample gets off the truck. That’s where we’ve found a huge problem in the industry and a golden opportunity to deliver business value.” (Jonathon Boswell, COO, Senico Labs)

■ The software-controlled water system. Large government infrastructure systems like water and sewage are coming under the gaze of software monitoring and control systems as well. The Parker, Colorado, water and sanitation district has wired up its wells, pumping stations, and pipelines, allowing remote monitoring and optimization of mechanical, human, and natural resources. Using its network of thousands of sensors, the district monitors flow, pressure, chemical levels, and leaks throughout its system that serves 55,000 customers. It’s able to control the operation of its entire system of pumps, modulating speeds and reducing start/stops to save tens of thousands of dollars in energy costs each year. More importantly, automated operation means a more sustainable operation of the well field, longer life for the machinery, and a longer life for the water sources.

“We use a mix of human intervention and automatic response to reduce energy costs, downtime, and maintenance expense.” (Kirk Magnusson, IT manager, Parker, Colorado, Water and Sanitation District)

Forrester defines the connected world as one where:

Technologies enable objects and infrastructure to interact with monitoring, analytics, and control systems over Internet-style networks.

The connected world will dramatically broaden the reach and impact of information technology systems, impacting economic activities, applications, and use cases that IT has not touched heretofore.1 In a connected world, software and information systems monitor and control many aspects of the physical world, not just the digital one. As described in the vignettes above, this means greater efficiency and asset utilization across many industrial and commercial scenarios; similar benefits will eventually spread to consumer sectors like automobiles and homes as well.

With increased reach and control into the physical world will come increased responsibility and scrutiny of information systems. It can be inconvenient and costly if a website goes down; it’s quite another thing if a software glitch brings a power plant or transportation system to a halt. Highly reliable — and highly secure — systems are a prerequisite to the continuing spread of the connected world.2

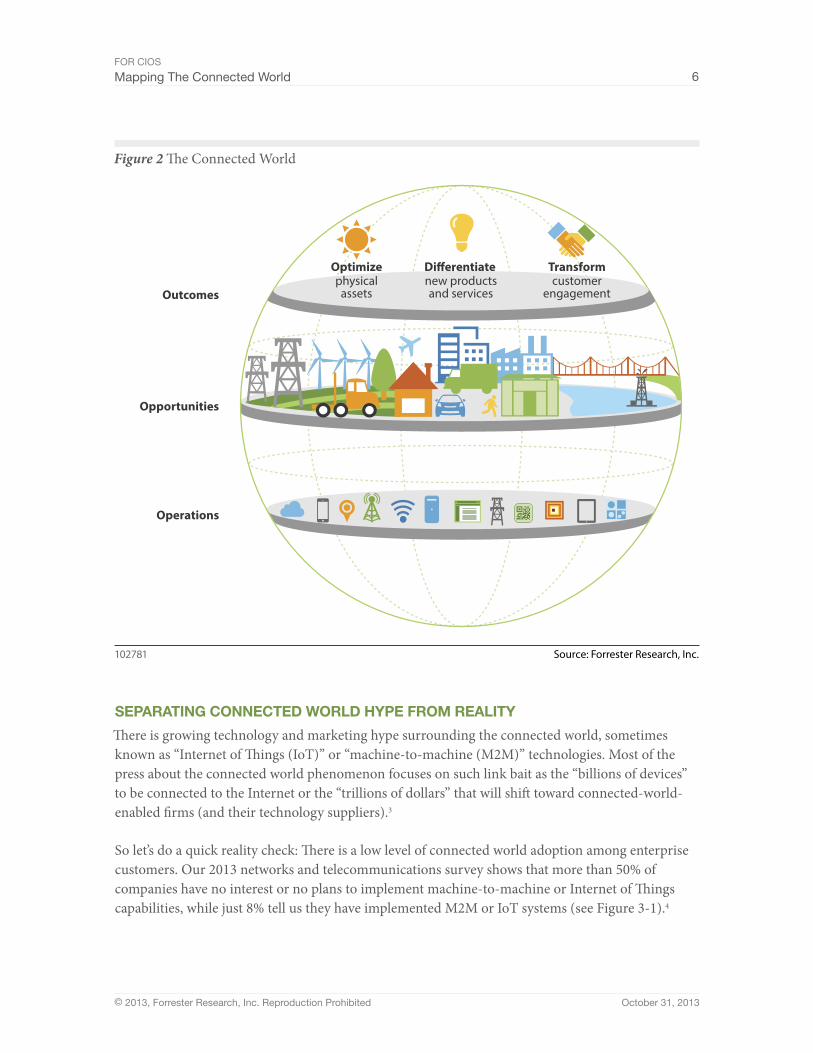

We have identified three interconnected planes that help in understanding the geography of the connected world (see Figure 2):

■ Business outcomes: the goals that organizations have in mind when evaluating connected world solutions.

■ Market opportunities: the relative ripeness of connected world solutions within specific industry contexts.

■ System operations: the (generalized) architecture and (typical) deployment sequence of connected world implementations.

We will zoom in on each of these complementary perspectives on the connected world; first, let’s do a quick reality check on the current market environment and how it’s evolving.

There is growing technology and marketing hype surrounding the connected world, sometimes known as “Internet of Things (IoT)” or “machine-to-machine (M2M)” technologies. Most of the press about the connected world phenomenon focuses on such link bait as the “billions of devices” to be connected to the Internet or the “trillions of dollars” that will shift toward connected-world-enabled firms (and their technology suppliers).3

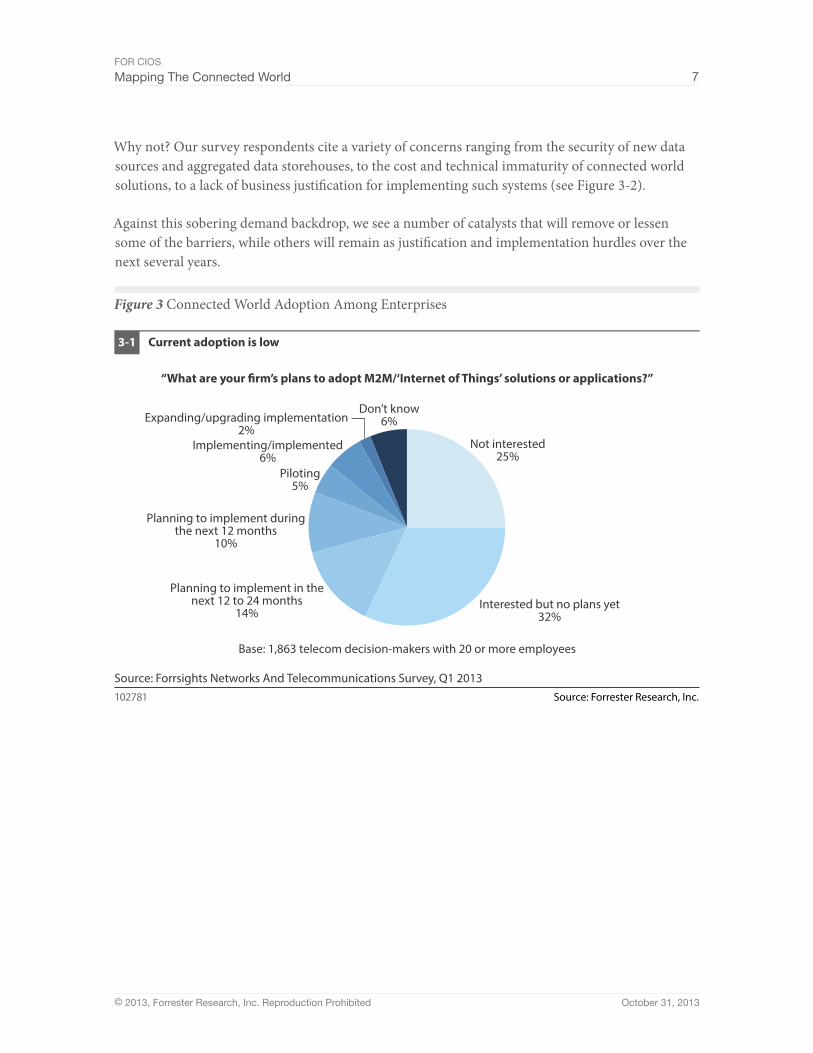

So let’s do a quick reality check: There is a low level of connected world adoption among enterprise customers. Our 2013 networks and telecommunications survey shows that more than 50% of companies have no interest or no plans to implement machine-to-machine or Internet of Things capabilities, while just 8% tell us they have implemented M2M or IoT systems (see Figure 3-1).4

Why not? Our survey respondents cite a variety of concerns ranging from the security of new data sources and aggregated data storehouses, to the cost and technical immaturity of connected world solutions, to a lack of business justification for implementing such systems (see Figure 3-2).

Against this sobering demand backdrop, we see a number of catalysts that will remove or lessen some of the barriers, while others will remain as justification and implementation hurdles over the next several years.

Figure 3 Connected World Adoption Among Enterprises

Source: Forrester Research, Inc.102781

“What are your �rm’s plans to adopt M2M/‘Internet of Things’ solutions or applications?”

Base: 1,863 telecom decision-makers with 20 or more employees

Source: Forrsights Networks And Telecommunications Survey, Q1 2013

Figure 3 Connected World Adoption Among Enterprises (Cont.)

Source: Forrester Research, Inc.102781

“What are your �rm’s concerns, if any, with deployingM2M/‘Internet of Things’ technologies?”

Base: 1,863 telecom decision-makers with 20 or more employees

Source: Forrsights Business Decision-Makers Survey, Q4 2012

Security issues are �rms’ No. 1 concern in deploying M2M/Internet of Things technologies3-2

None 10%

Don’t know 8%

Other 1%

We can’t �nd the right supplier(s) 7%

Lack of executive support 16%

Regulatory issues or concerns 18%

We don’t think we have an application orprocess that will be enhanced by M2M 20%

Di�culty and risk of migration or installation 21%

Pricing is unclear or complicated 14%

Integration challenges 24%

Lack of technology maturity 25%

Total cost concerns (total cost of ownership) 32%

Security concerns 37%

Catalysts drive Connected world adoption . . .

On both the demand/customer and supplier sides of the connected world markets, catalysts are emerging that will mitigate objections, make business cases easier to build, and generally goose the uptake of connected world solutions in the coming years. The most important of these are:

■ Lighthouse customers in a wide range of industries. Customer experience and success is becoming visible across a number of different industries and application use cases. As customers come out of piloting and testing and start to publicize their experiences and results, others in those industries will be spurred to act, whether by fear of falling behind or greed for

the same kind of results. As one big retailer reports 10% to 15% energy savings from a heating, ventilation, and air conditioning (HVAC) management system, others will want to follow. The same goes for industrial machinery manufacturers, consumer product goods (CPG) suppliers, chemical companies, etc. Similarly, tech suppliers are refining their offerings, learning from customers like the Port of Cartagena (Colombia) that did not want an all-encompassing connected port system from IBM but simply wanted to increase the utilization of the loading cranes at the port. Paradoxically, as vendors learn from their customers to narrow their connected world solutions to solve specific problems, those systems become attractive to a wider set of customers.

■ Declining prices and broader availability of component technologies. Whether its sensors at the digital-physical boundary, network connectivity, or analytic horsepower, the components of connected world systems are getting cheaper and more widely available. GPS-enabled tracking devices used in fleet management solutions, for example, have dropped from $500 to less than $60 per device over the past several years. Communications costs are experiencing a similar trend; many wireless operators are significantly cutting the monthly fees (in some cases to pennies a month for each meter) for the cellular link to support smart meters installed by electric utilities. And business intelligence (BI) or analytics software, formerly resident only on pricey high-end computing systems, is now available in the cloud with pay-per-use pricing.5

■ Transportation regulations to improve safety and resource utilization. In the US, for example, the Rail Safety Improvement Act of 2008 requires railroads to implement positive train control (PTC) systems on heavily travelled routes by 2015. PTC solutions prevent train derailments and collisions by automatically warning a locomotive engineer to act or by engaging brakes to stop the train if an engineer fails to act. CSX is deploying PTC technology covering more than 16,000 miles of track, overlaying a new signaling and management system on top of highly heterogeneous legacy systems. In Europe, the European Commission has mandated eCall standards requiring all new cars to have an automatic emergency call system installed by 2015. If there is a crash, the eCall system transfers location and accident data to the nearest emergency service center, reducing the time for emergency responders to arrive.

■ The app economy reset of customer expectations. We’re all being trained by our smartphones to expect convenient and easy-to-use applications at our fingertips, updated seamlessly and frequently. These expectations about controlling personal assets and relationships are quickly bleeding into enterprise and industrial sectors. As customer expectations rise, more companies will feel the pressure to improve the connectivity, smarts, and ease-of-use of their products and systems via software control.6

We see some barriers to connected world adoption falling rapidly; others remain to be overcome in coming years. The overarching issue is not about technology, though simplification and interoperability remain significant challenges for connected world systems; rather, the single most daunting barrier to adoption is the change required in business process, staffing, and skills that customers must make — in parallel with technology implementation — to realize the benefits of connected world solutions.

We expect these adoption dynamics to remain sticky:

■ Pushing employees out of their comfort zones. By connecting physical resources with digital systems, companies create the requirement to more tightly connect parts of their organizations. Field workers trained to deal with mechanical systems on a railroad engine, for example, now need to program, operate, and interpret software-based control systems for positive train control. Similarly, IT folks need to become familiar with how their systems extend into and operate in the field.7 Upgrades and maintenance that were performed strictly by field workers may now be done through over-the-air firmware upgrades, requiring IT and maintenance staff — white collar and blue collar — to work together in a new business process.

“Spending money on technology is the easy part relative to process change, training, and overcoming staff resistance.” (Dr. Glen Geiger, chief medical information officer, The Ottawa Hospital)

■ Addressing security and privacy concerns. Connected world solutions capture a wealth of information on the status, location, and use of assets, including people. There are at least three classes of security and privacy issues that may result: protecting the connected assets from attack; protecting the data gathered from those assets from misuse; and protecting the privacy of individuals whose assets may be supplying the data (via, e.g., electric meters or connected cars). Any connected world system implementation will have to explicitly recognize and address these issues and the processes to ensure the confidentiality of information. This will require cooperation across IT, risk management, and operations functions; too often, system and data security are “bolt ons” that land in IT’s lap.8

“Just because we can connect a device does not mean we should connect the device. We limit our security exposure by evaluating the positive impacts and potential risks associated with adding each connection.” (Kirk Magnusson, IT manager, Parker, Colorado, Water and Sanitation District)

■ Matching customer requirements with vendor solutions. Mismatches abound. Vendors have large-scale solutions while customers have narrow-gauge problems to solve. Customers have heterogeneous equipment to connect while most vendors have proprietary, our-gear-only

offerings. Customers want intuitive, lightweight software and interfaces, not likely to come from big, metal-bending suppliers making a foray into software. And customers face a huge challenge in assembling or integrating piece-parts from suppliers, while navigating an ever-shifting vendor landscape of alliances, consortia, and acquisitions.

“There is no ‘one stop shopping’ for these solutions. My IT manager has been through the wringer trying to put the pieces of the jigsaw puzzle together. It is very difficult to get all the hearts to beat as one.” (Jake Ladouceur, managing director, KUKA Toledo Production Operations)

■ Coordinating different buyer stakeholders. Marketing, operations, product development, facilities, and other functional groups drive connected world solution adoption. In many cases, these groups have different incentives and goals for a connected world system; R&D may seek product differentiation while operations expects transport-cost reduction. And IT considerations — not just security but also data management, network compatibility, and links with legacy systems — may be underappreciated and left until late in the game.

“I established a cross-functional team of physicians, IT, and operations professionals to facilitate communication, prioritize technology initiatives, and identify opportunities to improve patient care.” (Dale Potter, senior vice president of strategy and transformation, The Ottawa Hospital)

MaPPIng THe LandsCaPe OF THe COnneCTed wORLd

The landscape of the connected world is best understood from three complementary perspectives: outcomes, opportunities, and operations.

Perspective 1: Business Outcomes

Firms deploy connected world solutions to enhance their ability to recognize and achieve three types of business outcomes:

■ Optimize utilization of physical and financial assets. Asset utilization solutions apply to many industry sectors including remote management of irrigation equipment, remote machine diagnostics in manufacturing and healthcare facilities, and improvement of engine or pump life by running at the correct speed or temperature. For The Ottawa Hospital, e.g., tracking the location of patients on stretchers means better patient care, higher utilization of expensive equipment, and more efficiency for the hospital staff.

■ Differentiate products and services. Firms are fighting commoditization by integrating connectivity and smart devices into products. Among many examples, consider Nestlé’s

subsidiary Nespresso, which provides premium coffee services to restaurants, hotels, and offices. Nespresso offers its business customers proactive maintenance to ensure the machines are in proper condition, operating correctly, and are proactively receiving refill cartridges that match customer preferences. In another industry context, shipping giant Maersk monitors the condition (especially temperature) of shipping containers, creating customer visibility and peace of mind. The goal in both examples is a higher level of customer satisfaction, resulting in supplier loyalty and a premium market position.

■ Transform customer engagement. Many companies are looking to use connected world systems to change the nature of engagement with their customers, from one-time product transactions to ongoing service relationships. Rolls-Royce, for example, has shifted its revenue mix from 10% services to more than 50% services over the past six years by combining remote monitoring, analytics, and workflow management. The company has created a services business that monitors its engines in real time, analyzing the data stream to predict when an engine will need maintenance. Ground engineers know what the maintenance issue is before the plane touches down and can prepare to make the necessary repairs. This jet engine-as-a-service capability gives Rolls-Royce an ongoing engagement with its customers that the old product-sales model was lacking.

Perspective 2: Market Opportunities

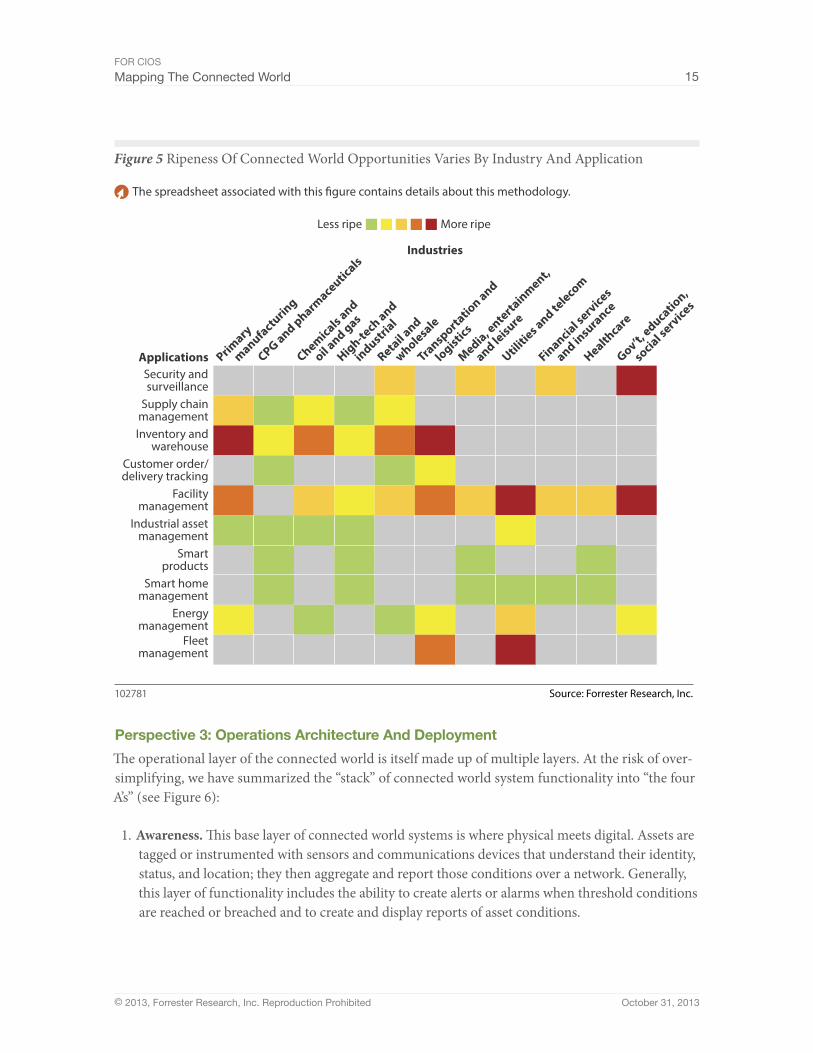

From its roots in transportation and logistics, we expect connected world solutions to spread across a wide variety of industrial, commercial, and consumer use cases. Our connected world heat map analyzes which types of connected world solutions are ripe, i.e., have a combination of attractive industry conditions and relatively strong adoption by customers in those industries.

Along the side of the map are connected world applications or use cases; this list is not comprehensive but includes most of the important types of connected world systems (see Figure 4). Across the top of the heat map are the important target industry groupings for connected world solutions. In the online spreadsheet, we have ranked each industry according to its overall asset intensiveness and its total spending on information and communications technology (ICT) products and services.9 Within the grid of the heat map are color codes that represent the ripest combinations of application and target industry, with gradations down to less ripe (but still viable) application-plus-industry combinations; a gray square means that combination of application and industry is not a prevalent connected world use case (see Figure 5).

Based on this analysis, the most fertile connected world solution markets are:

1. Fleet management in utility/telecom and transport industries. Fleet management is a time-tested connected world application, which large transportation firms such as FedEx and UPS have been using for many years. Many of today’s fleet management opportunities focus on

addressing the needs of local or regional firms with a few hundred vehicles or fewer. Companies like Jaris Transportation, a school bus company that transports special education students, uses Navman Wireless fleet tracking solutions to track fuel usage, vehicle maintenance status, routing, and driver behavior. With remote tracking systems in place, Jaris reduced fuel costs by $200 per vehicle per month and payroll by more than $400 per vehicle per month. Other benefits of fleet management solutions include faster maintenance service, reduced insurance rates, and the ability to reroute vehicles in real time.

2. Facility management in utility/telecom and government. These industries face very complex and expensive processes creating and operating facilities, especially in the handoffs between design, construction, and operation. For example, Dominion Energy is using IBM systems to track contractors building a new power plant, automating the tracking of materials, parts, and system configurations used during construction. This reduces the startup time for a new facility by reducing errors and having systems configured for operation faster.

3. Inventory and warehouse management in transportation and primary production. Tracking goods through complex global supply chains is another sweet spot for connected world systems. For example, iGPS, which rents shipping pallets, worked with Numerex and Enfora to improve management of its pallet inventory with M2M connections and radio frequency identification (RFID) tags. The global shipping line Maersk is working with AT&T and Ericsson among others to implement “remote container management,” giving it a real-time view into shipping container location and condition.

4. Surveillance in government. City governments in particular are expanding the reach of their public safety departments through networked surveillance cameras and video analysis software. These connected world implementations are sometimes part of expanding crime-fighting efforts in cities like Buenos Aires and Stavropol, Russia; they can also be part of broader “smart city” efforts that include, e.g., citywide Wi-Fi networks, software-controlled lighting systems, and smart electrical grid upgrades, as in Chattanooga, Tennessee.10

Some of the connected world sectors that get a decent amount of hype come out relatively poorly in this analysis. We expect these application areas will take some time before ripening, although there are point examples of attractive connected world implementations in each arena:

■ Home management, still too complex. While theoretically attractive to companies in insurance, telecom, and healthcare, system complexity and uncertain returns combine to hold back consumer adoption of this set of connected world applications. For example, British Gas sells Safe & Secure, a wireless system that lets consumers remotely control their homes’ heating, appliances, alarms, and remote camera monitoring. AT&T’s “Digital Life” is a similar all-encompassing security, control, and energy-management service. Consumer interest in such services is middling; actual adoption is in the single-digits for households at best.11

■ Smart products, big effort with uncertain payoff. Adding connectivity and software control to devices, products, and appliances is — at least theoretically — important to companies in the CPG, high-tech, and healthcare industries among others. For example, Ideal Life manufactures a wireless scale for congestive heart failure patients. The scale transmits patients’ weight data back to their doctor’s office, which flags weight fluctuations that may be a precursor to repeat hospitalization. Smart refrigerators, toothbrushes, and trash cans are in the offing too. But often these products are hampered by complex user interfaces (UIs) and uncertain utility, in part as a result of hardware original equipment manufacturers (OEMs) trying their hand at software, with painful results.12

■ Energy management, stymied by low prices and lack of a regulatory mandate. Controlling energy spending is a near-universal concern applicable across a variety of industries, including retail, manufacturing, and government. But energy spend remains unmanaged in most large companies, with regulatory uncertainty and cheap natural gas (at least in the US) combining to make energy management systems a tougher sell.

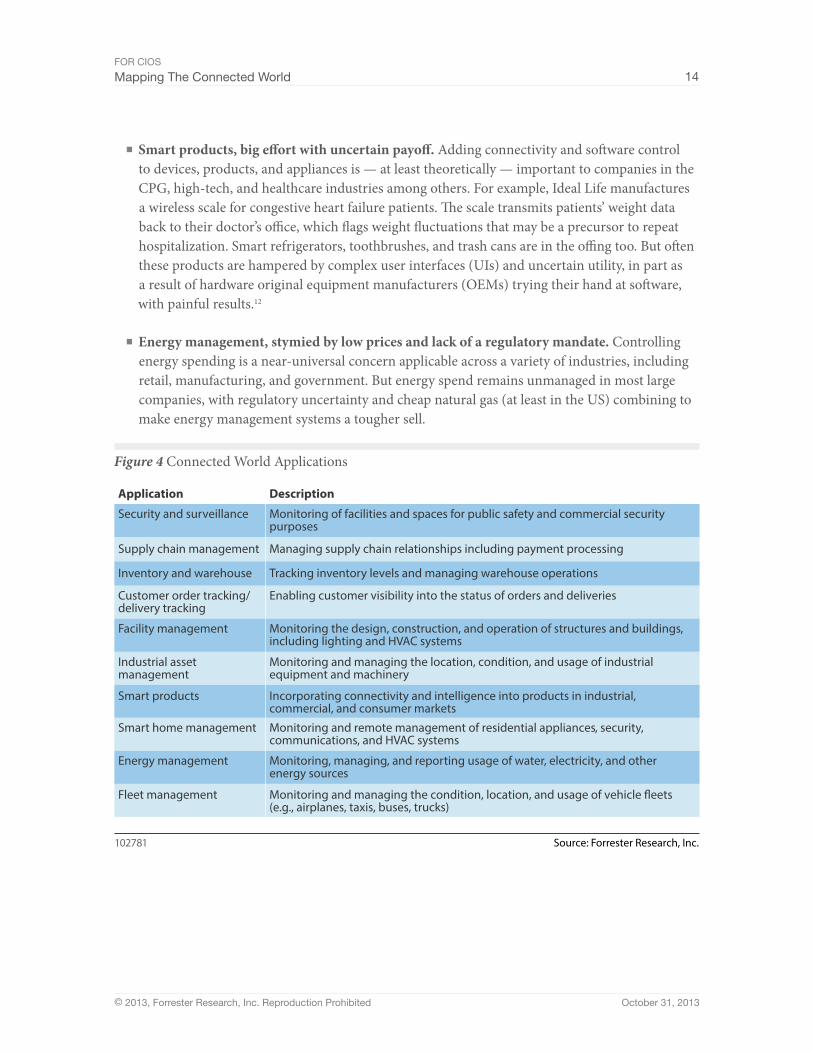

Figure 4 Connected World Applications

Source: Forrester Research, Inc.102781

Security and surveillance

Supply chain management

Inventory and warehouse

Customer order tracking/delivery tracking

Facility management

Industrial assetmanagement

Smart home management

Energy management

Monitoring of facilities and spaces for public safety and commercial securitypurposes

Application Description

Monitoring and managing the location, condition, and usage of industrialequipment and machinery

Monitoring the design, construction, and operation of structures and buildings, including lighting and HVAC systems

Managing supply chain relationships including payment processing

Monitoring, managing, and reporting usage of water, electricity, and other energy sources

Monitoring and remote management of residential appliances, security, communications, and HVAC systems

Enabling customer visibility into the status of orders and deliveries

Tracking inventory levels and managing warehouse operations

Smart products Incorporating connectivity and intelligence into products in industrial,commercial, and consumer markets

Fleet management Monitoring and managing the condition, location, and usage of vehicle �eets (e.g., airplanes, taxis, buses, trucks)

Figure 5 Ripeness Of Connected World Opportunities Varies By Industry And Application

Source: Forrester Research, Inc.102781

CPG and pharmaceutic

als

Chemicals and

oil and gas

High-tech and

industrial

Retail a

nd

wholesale

Transporta

tion and

logistics

Media, ente

rtainment,

and leisure

Financial serv

ices

and insura

nce

Healthcare

Gov’t, educatio

n,

social serv

ices

Security andsurveillance

Supply chainmanagementInventory and

warehouseCustomer order/delivery tracking

Facilitymanagement

Industrial assetmanagement

Smartproducts

Smart homemanagement

Fleetmanagement

Utiliti

es and telecom

Energymanagement

Industries

More ripeLess ripe

Applications Primary

manufacturin

g

The spreadsheet associated with this �gure contains details about this methodology.

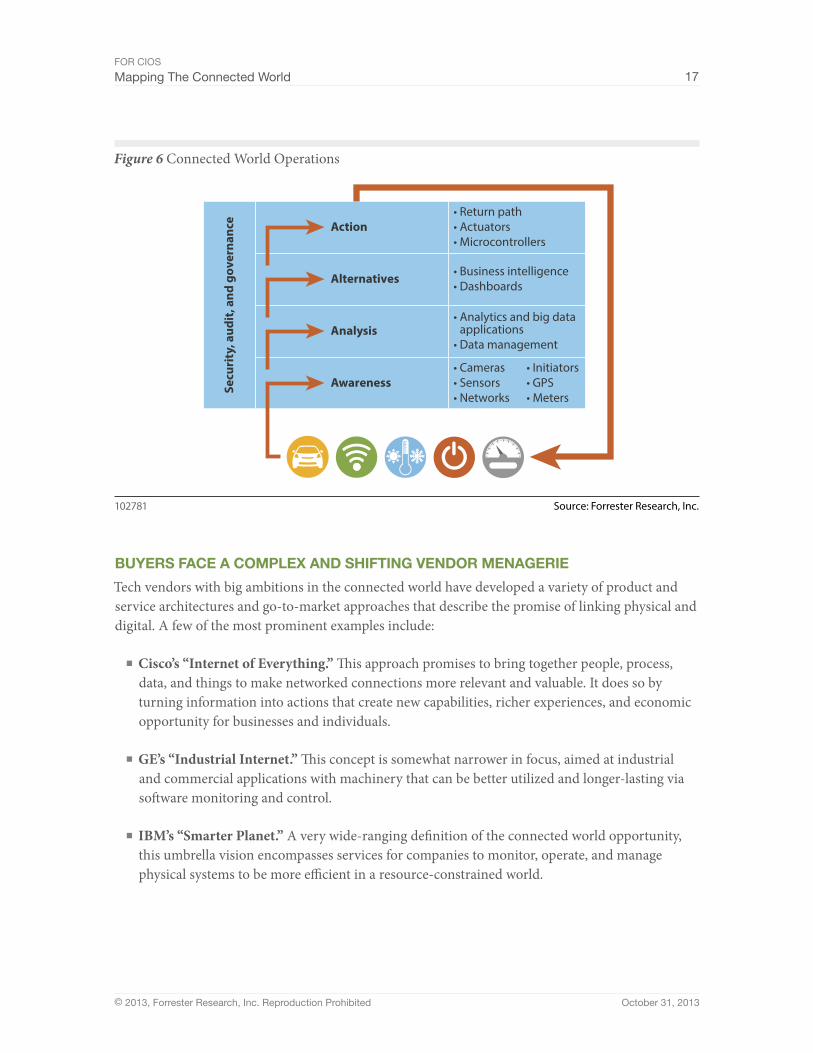

Perspective 3: Operations architecture and deployment

The operational layer of the connected world is itself made up of multiple layers. At the risk of over-simplifying, we have summarized the “stack” of connected world system functionality into “the four A’s” (see Figure 6):

1. Awareness. This base layer of connected world systems is where physical meets digital. Assets are tagged or instrumented with sensors and communications devices that understand their identity, status, and location; they then aggregate and report those conditions over a network. Generally, this layer of functionality includes the ability to create alerts or alarms when threshold conditions are reached or breached and to create and display reports of asset conditions.

2. Analysis. This layer of connected world systems actually comprises an entire technology stack on its own, ranging from databases to data management to analytics and reporting applications.13 Depending on the application arena, these tasks look at historical and real-time data inputs and may project or predict conditions into the future. Many connected world systems will also aggregate sources and feeds of data that are not directly associated with the assets being monitored or controlled, e.g., weather or social media inputs.

3. Alternatives. Advanced analytics systems will also perform hypothesis testing, scenario analysis, and predictive analysis, creating and evaluating alternatives for consideration and action.

4. Action. Connected world systems are ultimately about taking action and making decisions — better actions and decisions that are informed by real-world conditions and analysis of alternatives. This involves sending a decision — autonomic or human — to signal the monitored asset(s) through a return path, a signal that closes the valve, turns on the light, or shuts down the engine. This layer also includes a broader set of actions, including initializing, reconfiguring, customizing, or upgrading an asset or set of assets.

In most of our interviews across a range of industries, the implementers of connected world systems are looking to solve specific problems and realize specific benefits, with a narrow focus and a relatively short (12- to 24-month) time horizon to realize return on investment. To meet these criteria, implementations often follow the four-A model, moving up the stack from awareness to analysis through alternatives and then to action. So the initial business case is built on the basis of awareness, i.e., monitoring and reporting on asset status, and done so for a specific class of asset. Once sensor and network infrastructure is in place to support awareness, companies often add analysis and action capabilities.

BuyeRs FaCe a COMPLex and sHIFTIng VendOR MenageRIe

Tech vendors with big ambitions in the connected world have developed a variety of product and service architectures and go-to-market approaches that describe the promise of linking physical and digital. A few of the most prominent examples include:

■ Cisco’s “Internet of Everything.” This approach promises to bring together people, process, data, and things to make networked connections more relevant and valuable. It does so by turning information into actions that create new capabilities, richer experiences, and economic opportunity for businesses and individuals.

■ GE’s “Industrial Internet.” This concept is somewhat narrower in focus, aimed at industrial and commercial applications with machinery that can be better utilized and longer-lasting via software monitoring and control.

■ IBM’s “Smarter Planet.” A very wide-ranging definition of the connected world opportunity, this umbrella vision encompasses services for companies to monitor, operate, and manage physical systems to be more efficient in a resource-constrained world.

As we have discussed, most buyers are not looking for an all-encompassing solution in their hunt for more efficient operations or more differentiated products. Rather, most prospective connected world customers are looking for focused solutions to relatively narrow-gauge problems and for solutions that they can implement incrementally, moving through the awareness, analysis, and action phases.

These buyers face a multifaceted vendor landscape (see Figure 7). This picture is further complicated by an ever-evolving set of alliances and partnerships among the vendors and by serial acquisitions, typically of small/focused suppliers by larger players.

How to cope? We find that customer organizations often turn to vendors in two categories to help cut through the complexity:

■ Connected world specialists. Specialists like Axeda, Sierra Wireless, and ThingWorx bring together solution components and suppliers, including network partners, applications, provisioning, reporting, and monitoring tools, acting as platform providers or general contractors for designing and implementing connected world solutions. For example, GE turned to Axeda for a remote servicing application for its Power and Water Division’s industrial turbine and pump products. Over time, GE has expanded the relationship to gather not only real-time machine data but also customer usage data and each machine’s service history to strengthen its relationships with GE’s utility customers and to improve its product design in future releases.

■ Systems integrators. Systems integrators such as Accenture, Logica, and IBM assist firms with connected world projects leveraging their experience working on complex, multivendor systems in specific industry contexts. For example, Accenture partners with equipment providers like Siemens to provide smart metering solutions that help utility companies improve the automation, monitoring, and diagnosis of electricity grids. Wipro has created an

“eco-energy” business unit that helps retailers like Best Buy monitor and control their energy consumption, helping realize cost savings of 7% to 15%.

CIOs MusT LInK COnneCTed wORLd TeCH wITH BusIness OuTCOMes

CIOs will be a crucial catalyst for their organizations to capture emerging opportunities and harness the power of connected world solutions. Context-aware, location-based applications and services change how companies engage with and serve their customers; CIOs should straddle the line between what’s possible from a technology perspective and what’s meaningful to the business.

To do this, CIOs must:

■ Identify which business outcome(s) the connected world can deliver for your company. It’s easy to get caught up in the “gee whiz” of the connected world, and there are many examples of failed pilots going back at least a decade. Instead, CIOs should identify which of the three primary connected world business outcomes is a priority for the firm and learn about which technologies, skills, and process changes are required for success. By starting with the business outcome, CIOs are in a stronger position to help build the return on investment (ROI) business case, including the security, integration, and data analytics components necessary for implementation.

■ Partner with business leaders to ensure organizational and skill set alignment. Different business leaders will be the stakeholders for each class of business outcome: the CTO or R&D head for “differentiate products and services,” the CMO for “transform customer engagement,” and the COO or CFO for “optimize asset utilization.” The real-time data and insight captured by connected devices opens the doors to improve processes in virtually all functional areas; the CIO should help identify skills that are lacking and help fill the gaps, especially for data and analysis geeks.

■ Address security issues and data privacy concerns. The connected world heightens the importance of information security on at least three dimensions: protecting connected assets from attack, protecting captured data from misuse, and protecting the privacy of individuals whose assets are supplying the data. CIOs must proactively work with their corporate security and risk counterparts to ensure captured data will align with customer preferences as well as regulatory and compliance requirements.

■ Evaluate and expand software skills. The connected world enables businesses to capture how objects, items, and assets communicate with employees and customers; they can then use this information to improve employee activities, business processes, and customer experiences. Implementing these systems will require joint business-technology task forces, with analytics experts alongside operations, facilities, and product development. And software development skills will be in high demand too, since very few connected world systems are turnkey and they therefore require architecture, integration, and Agile development expertise.

Accelerating deployment of connected world solutions shifts the strategic priorities of CIOs and business decision-makers as well as the competitive landscape and vendor ecosystem participating in what will become a growing economic sector based on collection, aggregation, and especially analysis of connected world data.

■ Adjacent industry competition intensifies. Connected world solutions enable firms to expand beyond competing in their core competency industry and to broaden their reach into competing in adjacent, but related, industries.14 The shift from products to products-plus-services will often create new competitors and new opportunities. Furniture maker Herman Miller, for example, expanded beyond selling office furniture to offering space utilization services to help its customers design efficient office spaces and facilities. Data captured from sensors embedded in office chairs track occupancy, which translates into utilization of offices, conference rooms, and workstations. Utilization in turn shapes the size and cost of real estate, facilities, and utility charges. By wiring up products, other manufacturers will compete with firms in the adjacent services markets.

■ Product OEMs’ early lead is overtaken by integrators and aggregators. Today, OEMs such as Caterpillar, GE, and others are adding connectivity and control to their products and appliances, and they are differentiating their capabilities by establishing proprietary interfaces and application ecosystems. This proprietary approach is appropriate for today’s early stages of the connected world arena. However, in the future, siloed OEM product differentiation will give way to standards-based platforms, systems integration, and analytics solutions. Integrators and aggregators will incorporate heterogeneous products into both general-purpose and domain-specific services.

■ Data abundance drives new concerns and opportunities. Massive amounts of data captured in connected world solutions will drive new concerns regarding data access and permission. Questions about ownership of data will give way to policies governing access, permissions, sharing, and usage of data. New businesses will take aim at data aggregation and data brokerage opportunities, often clashing with product manufacturers and service providers operating connected world systems.15

■ A thousand business models bloom. Approaches to monetizing the value of connected world solutions will be as varied as the diverse array of use cases and applications and industry sectors. Progressive Insurance is pioneering usage-based insurance for its auto customers; similar product-as-service and pay-per-use transformations will spread across many industries and service offerings. Meanwhile, third-party vendors and data aggregators will create cloud services to access smart-product insights and develop analysis services.

The underlying spreadsheet detailing the data in Figure 5 is available online.

Methodology

Forrester’s Forrsights Networks And Telecommunications Survey, Q1 2013, was fielded to 2,487 IT executives and technology decision-makers located in Canada, France, Germany, the UK, and the US from SMB and enterprise companies with two or more employees. This survey is part of Forrester’s Forrsights for Business Technology and was fielded from January 2013 to March 2013. ResearchNow fielded this survey online on behalf of Forrester. Survey respondent incentives include points redeemable for gift certificates. We have provided exact sample sizes in this report on a question-by-question basis.

Each calendar year, Forrester’s Forrsights for Business Technology fields business-to-business technology studies in more than 17 countries spanning North America, Latin America, Europe, and developed and emerging Asia. For quality control, we carefully screen respondents according to job title and function. Forrester’s Forrsights for Business Technology ensures that the final survey population contains only those with significant involvement in the planning, funding, and purchasing of IT products and services. Additionally, we set quotas for company size (number of employees) and industry as a means of controlling the data distribution and establishing alignment with IT spend calculated by Forrester analysts. Forrsights uses only superior data sources and advanced data-cleaning techniques to ensure the highest data quality.

endnOTes1 Many CIOs are missing an opportunity to address existing and newly identified business needs through

projects focused on the smart computing technologies of sensors and other awareness devices, machine-to-machine (M2M) networks, mobile computing, real-time analytics, collaborative applications for project, case, and services management, and related technologies. These technologies help make business assets — physical, human, and financial — not just efficient, but also intelligent and more effective. In fact, CIOs and their firms are sinking billions of dollars into these technologies, but often in a piecemeal fashion. The real opportunity is to apply specific sets of smart technologies in a coordinated fashion to address key business challenges. For more on smart computing, see the March 28, 2012, “Smart Computing Connects CIOs With The Business” report.

2 As billions of devices connect via the Internet, exchanging information and taking autonomous actions based on continuous input, we will face a paradigm change that will transform our personal lives and revolutionize business. These radical transformations will pose unprecedented data privacy and security challenges to security and risk (S&R) professionals. For more information, see the October 23, 2012,

“Prepare Your Security Organization For The Internet Of Things” report.

3 Source: Michael Mandel, “Can the Internet of Everything Bring Back the High-Growth Economy?” Progressive Policy Institute, September 2013 (http://www.progressivepolicy.org/wp-content/uploads/2013/09/09.2013-Mandel_Can-the-Internet-of-Everything-Bring-Back-the-High-Growth-Economy-1.pdf) and the sources cited therein from McKinsey Global Institute, Cisco, and GE.

4 Source: Forrsights Networks And Telecommunications Survey, Q1 2013.

5 How does an enterprise — especially a large, global one with multiple product lines and multiple enterprise resource planning (ERP) applications — make sense of operations, logistics, and finances? There’s just too much information for any one person to process. This is where business intelligence (BI) comes into play. For more on BI, see the May 14, 2013, “Drive Business Insight With Effective BI Strategy” report.

6 The era of the standalone product is over. More and more offerings are becoming intelligent, connected, and thus able to provide more engaging experiences for customers in business or consumer settings. For more on smart products, see the November 16, 2012, “Smart Products Will Require A Hybrid CTO/CIO Skill Set” report.

7 IT leaders must prepare to address the technology and service implications of deploying machine-to-machine (M2M)-enabled Internet-of-Things (IoT) solutions, including new opportunities to leverage data

mining and business intelligence insight, privacy concerns, and service and support issues. For insight into the implications of M2M/IoT solutions, see the April 11, 2013, “Prepare I&O For The ‘Internet Of Things’” report.

8 As billions of devices connect via the Internet, exchanging information and taking action based on continuous input, enterprises will face a paradigm change that will transform their personal lives and revolutionize business. These transformations will pose unprecedented data privacy and security challenges to security and risk professionals. For insight into the security implications of Internet of Things solutions, see the October 23, 2012, “Prepare Your Security Organization For The Internet Of Things” report.

9 See the underlying spreadsheet for more information on the methodology behind our rankings. For details on how these industry categories are constructed and how they relate to the US Department of Commerce’s North American Industry Classification System (NAICS), see the August 2, 2010, “A Market Taxonomy For ICT” report. For information on industry asset-intensity, see the September 22, 2010, “Which Verticals Are Most Attractive For ICT Vendors?” report.

10 Source: Jennifer Belissent, Ph.D., “Redefining Your Greenfield: Existing Cities Find Greenfield Opportunities,” Jennifer Belissent, Ph.D.’s Blog, May 31, 2012.

For more information on smart cities, see the July 30, 2013, “Service Providers Accelerate Smart City Projects” report.

11 We will be highlighting if, how, and when the adoption logjam will be broken in an upcoming report on how the connected world comes home.

12 For analysis on how companies create the hybrid skill sets they need to create smart products that are useful and usable, see the November 16, 2012, “Smart Products Will Require A Hybrid CTO/CIO Skill Set” report.

13 Whether it’s optimizing the customer experience via social media or improving logistics by embedding sensors in vehicles, data analysis is simply critical, and analytics technologies are a key part firms’ BI investments. Such technologies help explore and interpret a company’s data to guide crucial decisions — but deciding which analytics technologies to implement is complicated by the wide range of existing and newer technologies. This diversity of options creates challenges in distinguishing what is possible, available, and appropriate for specific business scenarios. For more on BI, see the July 11, 2013, “TechRadar™: BI Analytics, Q3 2013” report.

14 For more details into the evolution of “adjacent possible” industry evolution and case studies, see the August 4, 2011, “Innovating The Adjacent Possible” report.

15 Enterprise execs who seek to understand their customers, market, and competitive landscape can’t afford to limit their insights to the data they generate. Nor can they hope to gain sufficient insight by purchasing data or target audiences from third parties. To meet the needs of perpetually connected customers, firms must become collaborative, both sharing their data and insight outward and absorbing it from suppliers and partners. For more on what Forrester calls “adaptive intelligence” (AI), see the August 16, 2013, “Improve Business Outcomes With Adaptive Intelligence” report.

Forrester Research, Inc. (Nasdaq: FORR) is an independent research company that provides pragmatic and forward-thinking advice to global leaders in business and technology. Forrester works with professionals in 13 key roles at major companies providing proprietary research, customer insight, consulting, events, and peer-to-peer executive programs. For more than 29 years, Forrester has been making IT, marketing, and technology industry leaders successful every day. For more information, visit www.forrester.com. 102781

«

Forrester Focuses On CIOs as a leader, you are responsible for managing today’s competing

demands on IT while setting strategy with business peers and

transforming your organizations to drive business innovation.

Forrester’s subject-matter expertise and deep understanding of your

role will help you create forward-thinking strategies; weigh opportunity

against risk; justify decisions; and optimize your individual, team, and

corporate performance.

caRol ito, client persona representing CIOs

About Forrestera global research and advisory firm, Forrester inspires leaders,

informs better decisions, and helps the world’s top companies turn

the complexity of change into business advantage. our research-

based insight and objective advice enable IT professionals to

lead more successfully within IT and extend their impact beyond

the traditional IT organization. Tailored to your individual role, our

resources allow you to focus on important business issues —

margin, speed, growth — first, technology second.

foR moRe infoRmation

To find out how Forrester Research can help you be successful every day, please contact the office nearest you, or visit us at www.forrester.com. For a complete list of worldwide locations, visit www.forrester.com/about.

client suppoRt

For information on hard-copy or electronic reprints, please contact Client Support at +1 866.367.7378, +1 617.613.5730, or [email protected]. We offer quantity discounts and special pricing for academic and nonprofit institutions.