39

Mapping the Israeli high tech industry Project: IFISE Work package 7 Arie Sadovski

| Date post: | 16-Dec-2015 |

| Category: |

Documents |

| Upload: | mariah-porter |

| View: | 214 times |

| Download: | 0 times |

Mapping the Israeli high tech industry

Project: IFISE

Work package 7

Arie Sadovski

Methodology

• Database from a commercially available source• Eight hundreds companies were contacted in

two cycles• Companies: estb. 1993 or later and hdqtrs in

Israel • Received 143 qualified, filled-in questionnaires• Each company was contacted at least two times; in most cases three times: 1st call to identify the

founders, then interview via fax/email and follow-up

The companies

Major industrial sectors•Communication (hardware) and electronic components•Software for internet•Software for other applications•Electronic medical instruments and devices•Software for telecommunication (ex internet)•Biotechnology (excluding pharmaceuticals)•Computer (hardware) semiconductor devices and electronic components•Optical instruments and materials (including optical communication items)

Industrial sectors

0% 5% 10% 15% 20% 25%

Communication&comp.

SW-internet

SW-Other application

Medical instruments

SW-telecom.

Biotechnology (ex.pharma)

Computers&comp.

Computers&comp.

Industrial eng. &autom.

New materials

Internet sites

Internet services

Precision instruments

Other

Pharma

Number of employees

• The average number is 36

• 80% of the firms have < 50

• 15% of the companies have < 10

• Mean employees' number having formal academic degrees is 23.4

• on the average at least 65% of the employees have academic degrees

Companies’ age

Companies

Age # %

1 year 29 20

2-3 years 54 38

4-5 years 31 22

6+ years 29 20

Total resp 143 100 Mean 3.5

Number of employees*

Employees companies %

1-5 9 7 6-9 20 1510-19 46 3420-49 33 2550-99 18 13100-249 7 5250+ 3 2Total 136 100 Mean 35.6* From data base

Product development phases

# %Research and development 21 15Technological demonstration 6 4Prototype 12 9ß site 17 12Initial sales 43 31Sales 41 29Total respondents 140 100

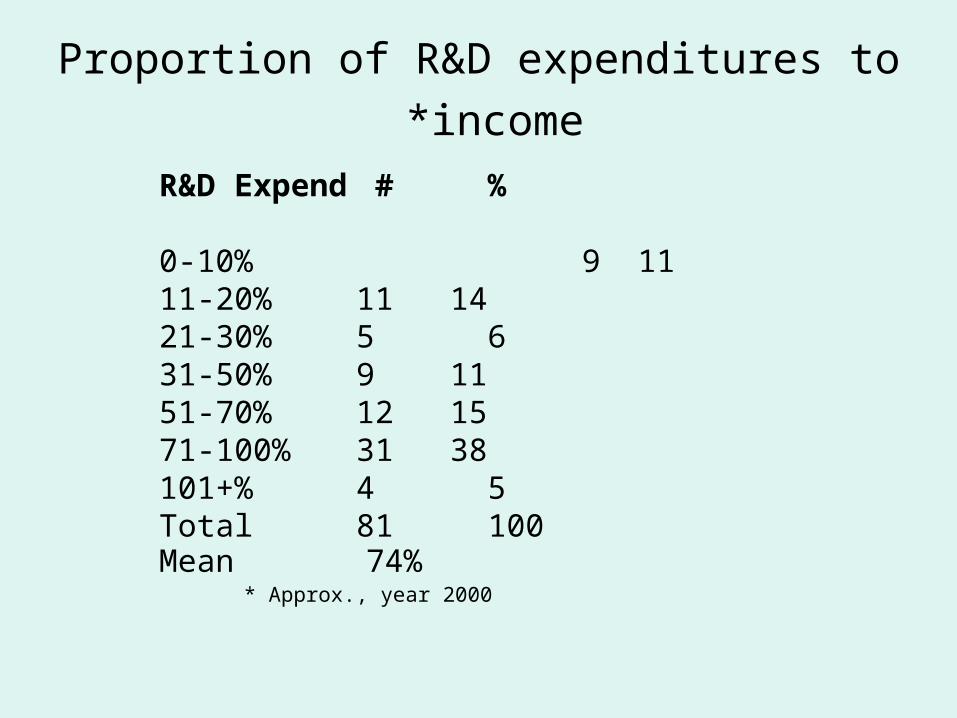

Proportion of R&D expenditures to income*

R&D Expend # % 0-10% 9 1111-20% 11 1421-30% 5 631-50% 9 1151-70% 12 1571-100% 31 38101+% 4 5Total 81 100Mean 74% * Approx., year 2000

The founders

Number of founders per company

Founders # %

1 22 15

2 57 40

3 42 30

4 15 11

5+ 6 4

Total 142 100

Founders’ formal schooling

# %

Non academic 11 8

Vocational Engineers 8 6

B.Sc. /B.A 73 51

M.Sc. /M.A 63 44

Ph.D. 67 47

Military courses 15 10

Founders’ professional training disciplines

# %

Engineering 64 45

MBA 24 17

Exact / Computer Science 77 54

Management/Economic 21 15

Life Science 26 18

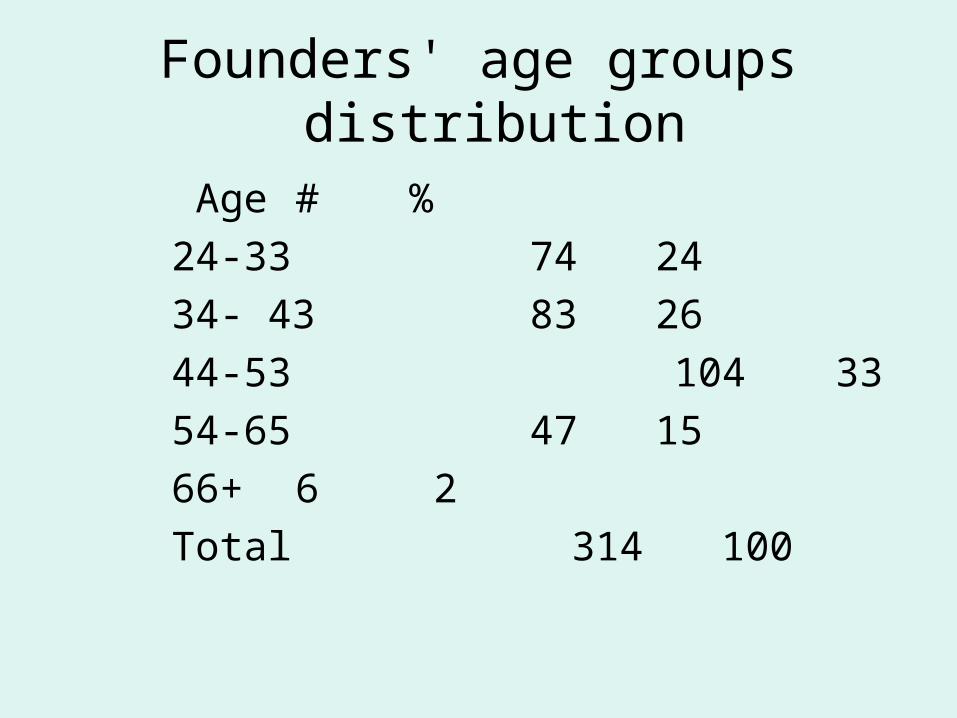

Founders' age groups distribution

Age # %

24-33 74 24

34- 43 83 26

44-53 104 33

54-65 47 15

66+ 6 2

Total 314 100

Women founders

Per company Companies

1 13

2 1

4 1

Changes in the founders' position

# %

Yes, all of them are still in the lead 94 67

No, part of them are in the lead 30 21

No, none of them are in the lead 16 11

Total respondents 140 100

The entrepreneurial

environment and background

The geographical birth place of the new technology

# %

Israel 128 90

Abroad 12 8.5

Both 2 1.4

Total respondents 142 100

The working environment in which the new technology was borne

# %

Academic institution 23 20

High Tech industry 73 62

Academic + High Tech 4 3

Low Tech industry 18 15

Total respondents 118 100

Previous occupation of the founders

# %

Unemployed 2 1

Students 9 6

Academia, Research Institute 24 17

Industry 108 76

Total respondents 143 100

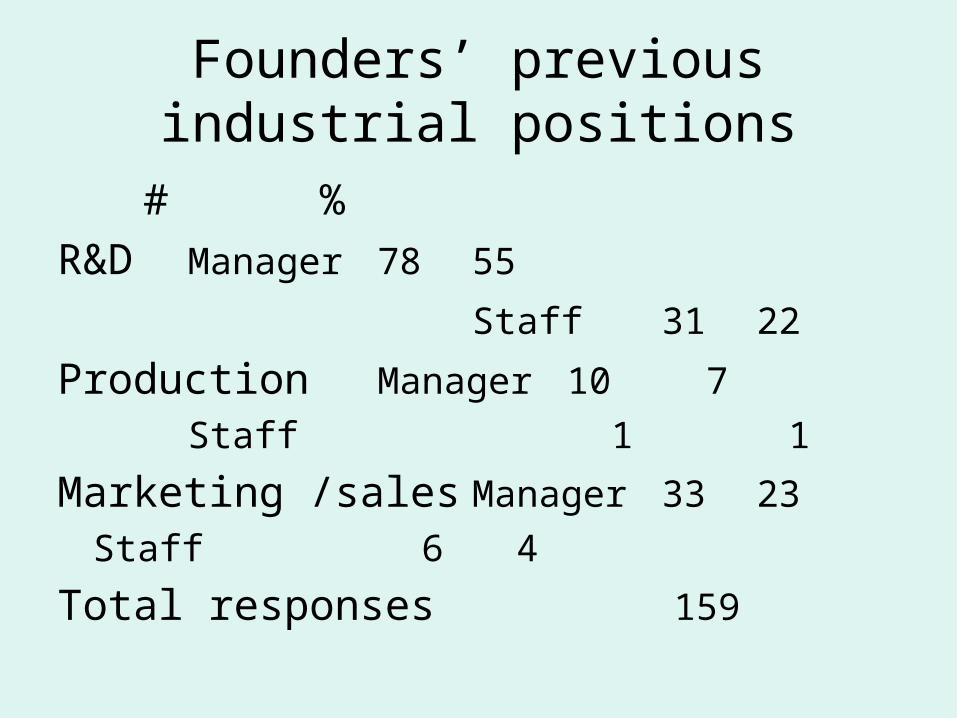

Founders’ previous industrial positions

# %

R&D Manager 78 55

Staff 31 22

Production Manager 10 7

Staff 1 1

Marketing /sales Manager 33 23

Staff 6 4

Total responses 159

Fund raising patterns

Number of rounds used for fund raising

Rounds Companies %

1 48 39

2 29 24

3 24 20

4 15 12

5 6 5

Respondents 122 100

Sums raised in the different rounds

Sums raised Seed 1st 2nd<150K 26 8 6151-600K 37 14 82-3M 30 48 403+ 8 29 46Total 100 100 100

Sums raised in the different rounds

Fund raising patterns

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

<50K <150K <300K <600K <1M 1-2M 2-3M 3-5M 5+M

Co

mp

anie

s

Seed capital

Round 1

Round 2

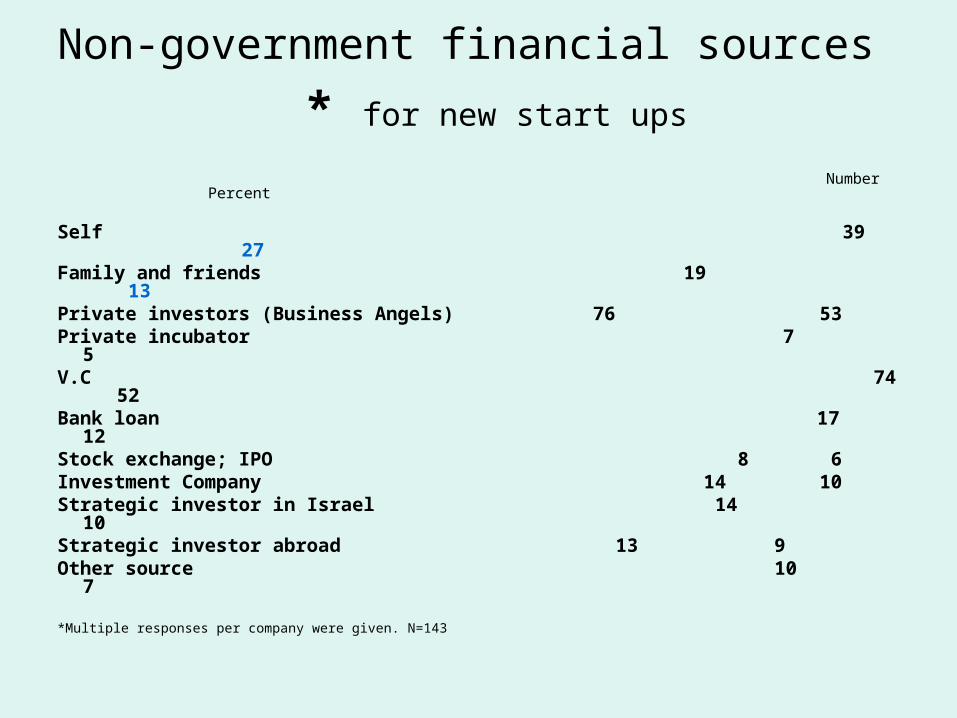

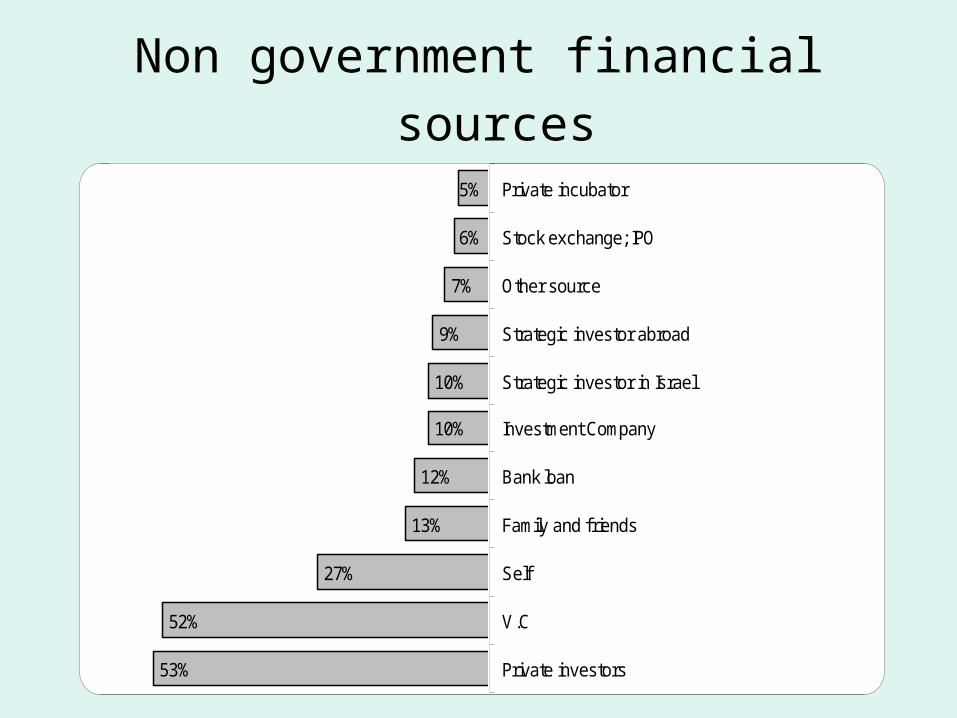

Non-government financial sources

for new start ups * Number Percent

Self 39 27Family and friends 19 13Private investors (Business Angels) 76

53Private incubator 7 5V.C 74 52Bank loan 17 12Stock exchange; IPO 8 6Investment Company 14 10Strategic investor in Israel 14 10Strategic investor abroad 13 9Other source 10 7

*Multiple responses per company were given. N=143

Non government financial sources

53%

52%

13%

12%

10%

10%

9%

7%

6%

5%

27%

Private investors

V.C

Self

Family and friends

Bank loan

Investment Company

Strategic investor in Israel

Strategic investor abroad

Other source

Stock exchange; IPO

Private incubator

Yozma VC funds as a funding source Companies*

Yozma VC funds Number Percent

Eurofund 4 15Medica 1 4Walden 4 15Gemini 3 11Nitzanim 1 4Apex 3 11Inventech 4 15Polaris 9 33Vertex 2 7Jerusalem Pacific Ventures 0 0Star 4 15

*Multiple responses per company were given. N=27

Government financial sources

Companies* Number Percent

Government Incubators 21 15R&D grant – Regular 49 34R&D grant - For start-up 5 3R&D grant - “Magnet” 7 5Bi-National programme – BIRDF 11 8Bi-National programme – Other 1 1Investment Center – Grant/capital equipment 11 8Investment Center – Income tax benefits 21 15

*Multiple responses per company were given. N=143

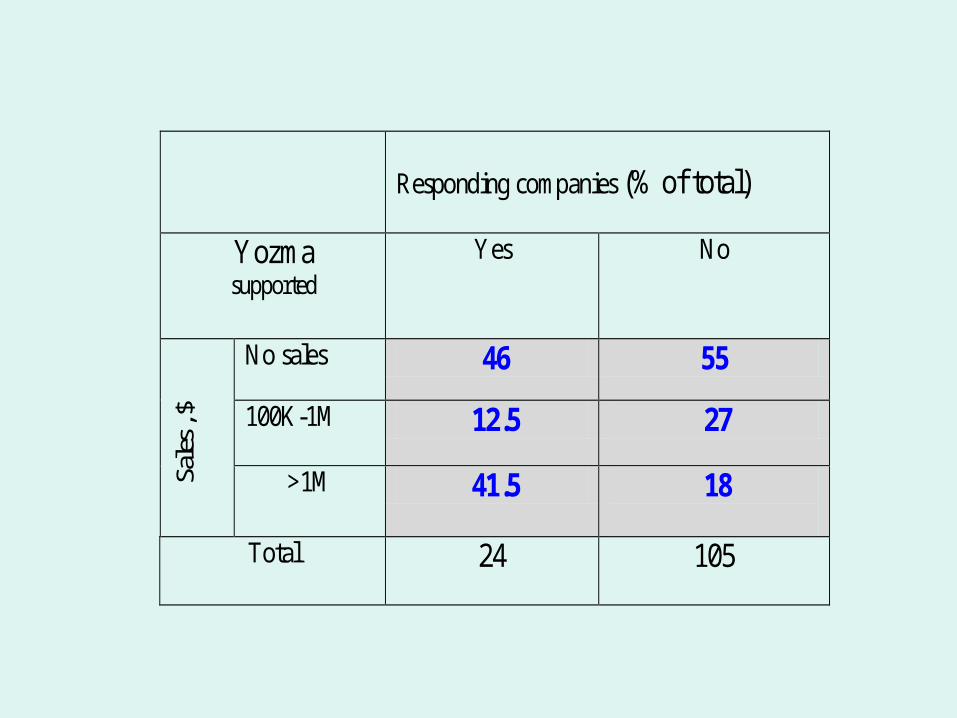

Incubators and Yozma programs affiliated companies-

comparison of sales and growth- rates to the otherrespondents companies

Respondents (% of total)

No

Yes

Incubators graduate

52 63 No sales

22 37 100k-1M

26 0 >1M

Sale

s , $

110 19

Total respondents

Responding companies (% of total)

No Yes Yozma supported

55 46 No sales

27 12.5 100K-1M

18

41.5 >1M Sale

s , $

105

24

Total

2000 1999 1998

No

Yes

No

Yes

No

Yes

Yozma supported

41 24 51 47 64 46 No

33 35 29 13 15 8 21-40

26 41 20 40 21 46 >41

G

row

th %

63

17

55

15

48

13

Total respond.

Difficulties encountered

The six most difficult areas and expectations for government assistance

Areas of activity - Difficulty index (mean) * Gov. assistance

Companies responding

“YES”

Fund raising - 4.2 58%Marketing - 3.8 45% Networking with strategic partners - 3.5 37% Connection with international collaborators - 3.3 49% Recruiting - 3.2 19% Connection to funding sources - 2.9 44% Protection of IPR – 2.8 32%

* The respondents were asked to rank each difficulty on a scale of 1-5.

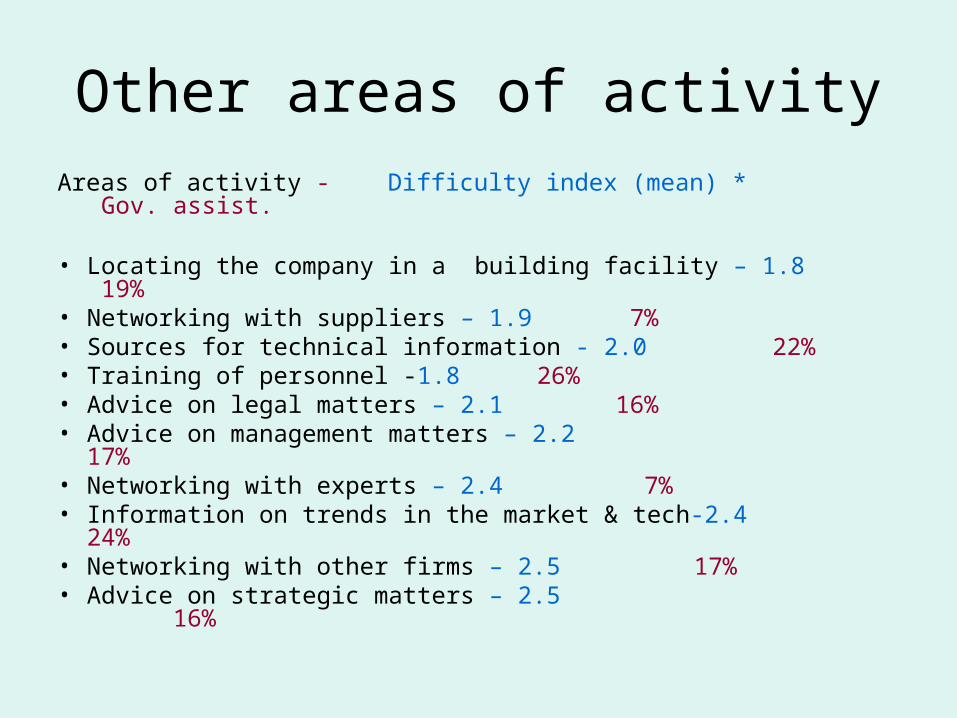

Other areas of activity

Areas of activity - Difficulty index (mean) * Gov. assist.

• Locating the company in a building facility – 1.8 19%• Networking with suppliers – 1.9 7%• Sources for technical information - 2.0 22% • Training of personnel -1.8 26%• Advice on legal matters – 2.1 16%• Advice on management matters – 2.2 17%• Networking with experts – 2.4 7%• Information on trends in the market & tech-2.4 24%• Networking with other firms – 2.5 17%• Advice on strategic matters – 2.5 16%

The areas of higher difficulty Activities of high difficulty index

4.2

3.8

3.5

3.3

3.2

2.9

2.8

2.5

2.5

2.4

2.4

00.511.522.533.544.5

Financial support

Marketing

Networking with strategic partners

Connection with international collaborators

Accessibility to labor pool and recruitment

Connection to funding sources

Protection of IPR

Professional networking with other firms

Advice on strategic matters

Networking with professional experts individuals

Information - markets trends and tech dev

Difficulty index

End