Investment Climate | World Bank Group Global Analysis of General Trade and Operational Licensing INVESTMENT CLIMATE MARCH 2012 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript

Investment Climate | World Bank Group

Global Analysis of General Trade and

Operational Licensing

INVESTMENT CLIMATEMARCH 2012

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

wb350881

Typewritten Text

77098

Investment Climate | World Bank Group

Global Analysis of General Trade and Operational Licensing

The information included in this work, while based on sources that the World Bank Group considers to be reli-able, is not guaranteed as to accuracy and does not purport to be complete. The World Bank Group accepts no responsibility for any consequences of the use of such data. The information in this work is not intended to serve as legal advice.

The findings, interpretations, and conclusions expressed in this work are those of the authors and do not necessarily reflect the views of the Board of Executive Directors of the World Bank or the governments of the countries which they represent.

The denominations and geographical names in this publication are used solely for the convenience of the reader and do not imply the expression of any opinion whatsoever on the part of the International Finance Corporation, the World Bank, or other affiliates concerning the legal status of any country, territory, city, area, or its authorities, or concerning the delimitation of its boundaries or national affiliation.

Rights and PermissionsThe material in this publication is copyrighted. Copying and/or transmitting portions or all of this work without permission may be a violation of applicable law. The World Bank Group encourages dissemination of its work and will normally grant permission to reproduce portions of the work promptly.

For permission to photocopy or reprint any part of this work, please send a request with complete informa-tion to the Copyright Clearance Center Inc., 222 Rosewood Drive, Danvers, MA 01923, USA; telephone: 978–750–8400; fax: 978–750–4470; online at: www.copyright.com.

All queries on rights and licenses, including subsidiary rights, should be addressed to the Office of the Publisher, the World Bank, 1818 H Street, NW, Washington, DC 20433, USA; telephone 202–522–2422; email: [email protected]

About the Investment Climate Department of the World Bank Group The Investment Climate Department of the World Bank Group helps governments implement reforms to improve their business environments and encourage and retain investment, thus fostering competitive markets, growth, and job creation. Funding is provided by the World Bank Group (IFC, MIGA, and the World Bank) and over 15 donor partners working through the multidonor FIAS platform).

CASE STUDIES ............................................................................................................................................. 33

Case 1: Tanzania — Example of Costly and Burdensome General Licensing ......................................... 33

Case 2: Bangladesh, Dhaka — Example of Partial Reform .................................................................... 35

Case 3: São Tomé and Príncipe — Example of Successful Reform ........................................................ 37

Case 4: Panama — Example of Successful Reform ............................................................................... 39

1. Examples of Unnecessary Licenses and Associated Costs ......................................................................... 24

2. Summary of Licensing Procedures............................................................................................................ 34

4 Global Analysis of General Trade and Operational Licensing

Acknowledgments

This paper has been produced by the Investment Climate Department of the World Bank Group. Mr. Andrii Palianytsia researched relevant case studies and produced an initial draft of the paper. Tshewang Tashi and Laura Celine Kaliszewski were critical to collecting the research materials from the IFC teams globally. The in-house team comprised of Marta Riveira Cazorla and Petter Lundkvist provided significant support to the data analysis. The peer reviewers included: Jacqueline Coolidge, Laurent Olivier Corthay, Hans Shrader, Peter Ladegaard, Florentin Blanc, Tarik Sahovic, Fred Zake and Serhiy Osavolyuk. Numerous other field staff of IFC have kindly pro-vided inputs and data used in the publication — to all of whom thanks are due. The research and analysis was coordinated and the content of the paper was edited by Boris Divjak. English editing was completed by Vandana Mathur with valuable support of Patricia Steele. The overall project was managed by Andrei Mikhnev.

5Managing for Impact : FIAS Strategy for FY12–16Acknowledgments 5

Executive Summary

This paper examines the general licensing regime imposed by central or local authorities, and the need to eliminate unnecessary licensing regulations imposed on businesses.

This paper provides criteria for identifying unnecessary licensing regulations, an overview of reform practices, and lessons learned from efforts to rationalize licensing. It argues in favor of eliminating unneeded licenses through a phased smart deregulation, a more radical regulatory “guillotine” approach, or, in some instances, changing licensing regulations to notifications.

The Organisation for Economic Co-operation and Development (OECD) defines licensing as the practice of requiring prior approval of a government authority for the establishment or conduct of a business or other activities. Approval is based on the provision of specific validated or certified information usually in a written form. For the purpose of this paper, general operational licenses are defined as permissions given to businesses prior to commencement of their operations by national or local authorities, business associations, chambers of commerce, or other government and non-government agencies without which business operations are deemed illegal as specified by legislation. Licenses always impose application requirements and require approval by licensing agencies. Application requirements and rules for business activities that form part of a licensing regime are called licensing conditions.

This paper argues that justified licenses typically involve all four steps specified in the World Bank Group Policy Framework Paper on Business Licensing Reform and Simplification,1 namely:

• Application process;

• Prior approval to operate, which requires regulators to assess and verify the application, ensures specified conditions have been met, and provides formal approval to a business to operate in a specified sector;

• Operating conditions, where businesses are expected to comply with standards, conditions and require-ments specified in the license; and

• Enforcement, where the regulator enforces specified license conditions, standards, and requirements through a variety of measures.

This paper further elaborates that justified licensing regimes can be applied in regard to three broad areas, namely:

• Activities with potential risks to human safety and well-being, including environmental protection;

• Activities that deal with limited resources; and

• Activities that involve undesirable, although legal, practices.

The existence of licensing conditions,2 and their clarity and effectiveness are the key to defining justified licenses. The absence of licensing conditions or deficiencies in their formulations is the main characteristic of unjustified licenses.

1 World Bank Group, Policy Framework Paper on Business Licensing Reform and Simplification.2 The term “licensing conditions” is used in this paper as any legally specified requirements that are either checked by an authorized

agency prior to issuing a license, or are monitored and enforced by this agency after the licensed company began operations. Where licensing conditions are specific to the license they accompany, they are called “unique licensing conditions.”

6 Global Analysis of General Trade and Operational Licensing

Unjustified licenses can have declared or implicit functions. Most frequently these are:

• Informational. This involves collecting data on the number of employees, assets, capital investments, types of activities and their locations, and so on, through obtaining general licenses and their regular renewing.

• Quasi-fiscal. This includes collecting license fees that form a part of local or national revenues.

• Establishing eligibility for business assistance programs or other benefits.

• Protection of competition.

• Exercising state oversight.

The paper concludes that the informational function is much more reliably and cheaply fulfilled through busi-ness registration, tax reporting, and statistical studies based on small samples of businesses. Almost all experts argue that the fiscal function is best fulfilled through a common tax collection regime. The absence of unique licensing conditions in these cases nullifies all other regulatory benefits. As for the oversight function, the absence of enforceable licensing conditions makes it prone to arbitrary decision making. Costs of such licensing regimes, however, are quite high for both the private and public sectors. Thus, elimination of such licenses is not risky and can provide immediate benefits in savings.

The key feature of the “unjustified licenses” is that they are not performing a necessary function. If a gov-ernment jurisdiction needs revenues, it should consider introducing a tax. It may also demand information from businesses. But neither the need for revenues nor information should require a license.

The outright elimination of unjustified licenses appears to be the best policy choice, unlike systemic and careful reforms of case-by-case analysis, doing regulatory impact assessments, streamlining obviously bad regulations, modeling future impacts, and trying to replace outdated regulatory tools with more efficient ones that are fully justified in other circumstances. Unjustified licenses either do not fulfill any legitimate functions, or do this in an inefficient way. What they succeed in doing is to impede business development, increase corruption opportuni-ties, and add a significant cost to both businesses and governments.

This paper presents four in-depth cases that illustrate different scenarios with unjustified licensing. The case of general industrial licensing in Tanzania is an illustration of unreasonable and unnecessary licensing. The case of trade licensing in Bangladesh is on one hand an example of successful reform and simplification of a licensing regime. But on the other hand, it is unnecessary and should be replaced by common taxation and declaration of beginning of operations by businesses. The case of São Tomé and Príncipe illustrates a successful reform through the elimination of requirements to obtain licenses for internal and external trade of all common goods and services. Remaining companies are subject to well justified licenses only for activities that can either endanger safety or use limited resources. Successful reform is also demonstrated by the case of Panama, where general licenses and other permits and registration are combined into one cheap and fast online procedure of obtaining Operation Notice.

7Executive Summary

8 Global Analysis of General Trade and Operational Licensing

Introduction

This report is part of a series of publications delivered by the World Bank Group’s Investment Climate Advisory Services, under the Business Regulation practice. The approach to reform highlighted in this paper is compatible with the broader Policy Framework Paper on Business Licensing Reform and Simplification3 and is comple-mentary to the Business Licensing Reform: a Toolkit for Development Practitioners,4 the handbook on How to Reform Business Licenses.5 This paper also builds upon other publications of the World Bank Group on broader regulatory topics covering reform, taxes, and administrative fees.

The Policy Framework Paper on Business Licensing Reform and Simplification provides contextual overview and framework for licensing practices, discusses potential advantages and disadvantages of licensing, and summa-rizes broad approaches to licensing reform. A more practical overview of business licensing reforms is provided in Business Licensing Reform: Toolkit for Development Practitioners with its emphasis on well-analyzed case studies. A much more project-oriented, hands-down overview of approaches to licensing reform is provided by the handbook on How to Reform Business Licensing. This handbook provides detailed guidance to practitioners on implementing fast-track, top-down licensing reform projects and takes readers step-by-step through the successive stages of reforms. Finally, sector-specific Licensing Case Studies6 provide analyses of different sec-tors, sector-specific regulations, most notably licenses, their impact on sector development, and approaches to sector-specific regulatory reforms.

This paper examines the general purpose licensing imposed by central or local authorities, and the need to elimi-nate unnecessary licensing regulations imposed on businesses. This paper does not address the issue of reform of sector-specific or professional licensing regulation, but provides criteria and tools for identifying unnecessary licensing regulations, and their elimination or, in some instances, for changing licensing regulations to free notifications.

The reason for having a closer look at general licensing lies in the fact that reform practitioners engage in prolonged and costly debates, perform complex regulatory impact assessments, review international practices, develop elaborate arguments, and draft replacement regulations in cases that warrant outright elimination of unnecessary, unjustified, and irrational licensing burdens for private and public sectors. Indeed, this paper argues that a simplified review of licensing regimes that identifies unnecessary licensing saves energy and resources for well-balanced reform of remaining licensing regulations, eventually providing better protection for the public at large and a more enabling business environment.

This paper is primarily oriented towards reform practitioners from governments that intend to reform their business environments; development agencies; donor-funded projects; practitioners of licensing reforms; and others interested in improving state and local governance.

This paper is divided into three parts: (1) overview of licensing practices that provides common definitions of licensing, analysis of justified licensing regimes with focus on criteria for their justification, and theoretical overview of unjustified and questionable licenses; (2) analysis of commonly declared functions of unjustified licenses that provides insight into the nature of these licenses and their typology; (3) four case studies that

3 World Bank Group, Policy Framework Paper on Business Licensing Reform and Simplification. 4 International Finance Corporation, Business Licensing Reform: A Toolkit for Development Practitioners. 5 World Bank Group, How to Reform Business Licenses.6 Forthcoming.

9Introduction

examine how unjustified licenses can be reformed with examples of unsuccessful, partially successful, and successful reform efforts. The analytical conclusions of this paper summarize criteria for unjustified licenses; describe lessons learned from the reform efforts; and provide a practical set of recommendations to the interested parties.

10 Global Analysis of General Trade and Operational Licensing10

Common Licensing Practices

DEFINITION OF LICENSING

In its 2006 publication, Cutting Red Tape: National Strategies for Administrative Simplifications, the OECD defined licensing as the practice of requiring prior approval of a government authority for the establishment or conduct of a business or other activities.7 Approval is based on the provision of specific validated or certified information usually in written form.

Business licensing is a commonly used form of regulation that affects specified businesses and occupations by regulating entry into markets and conduct within markets.

The World Bank Group’s Policy Framework Paper on Business Licensing Reform and Simplification specifies that business licensing is a commonly used form of regulation that affects specified busi-nesses and occupations by regulating entry into markets and conduct within markets. Licenses typically impose on businesses a range of conditions, obligations, and rights—often in the form of a specific license, permit, or concession. Breaches of specified conditions typically involve imposition of sanctions by the relevant regulatory authority, such as a fine or revocation of permission to perform an activity. Licensing does not include general registration of businesses, including for business name, taxation, and statistical purposes. Permits are usually (although not always) a subset of licenses and typically focus on providing regulatory approval for a defined activity.8

Licensing is related but distinct from procedures such as business registration, permitting, and inspections. In good business licensing regimes licensing is a means to fulfill legitimate regulatory purposes.

Business Licensing Reform: A Toolkit for Development Practitioners focuses specifically on the per-missions firms must obtain for their core business activities. Licensing is related but distinct from procedures such as business registration, permitting, and inspections. In good business licensing regimes, licensing is a means to fulfill legitimate regulatory purposes. These include protection of public health and safety, environmental protection, national security, and allocation of scarce resources. Licenses should not be used to manage competition in the economy or to generate revenue. These regulatory objectives are more efficiently addressed through competition and tax policy.9

Here are some key characteristics of business licenses:

• They regulate activities of businesses;

• They are issued prior to commencement of business activities, thus regulating entry into markets; and

• They impose obligatory rules for the ongoing conduct of business activities.

7 OECD, Cutting Red Tape: National Strategies for Administrative Simplifications.8 World Bank Group, Policy Framework Paper on Business Licensing Reform and Simplification, p. 7.9 International Finance Corporation, Business Licensing Reform: A Toolkit for Development Practitioners, pp. vii–viii.

11Common Licensing Practices

Business licenses are therefore authorizations given to businesses prior to commencement of their opera-tions by national and local authorities, business associations, chambers of commerce, and other agencies both government and non-government without which business operations are deemed illegal as specified by legislation. Licensing is the main regulation of an activity. In some countries such regulations are called permits, certification of activities, patents for activities, registration (outside of incorporation, registration of business name, and tax registration), but in essence they do not differentiate from licensing. Licensing always requires submission of an application and approval by licensing agencies. These agencies have a right to refuse issuing a license. The potential for denial is the key difference between the regimes of licensing and notification. Application requirements and rules for business activities that form part of a licensing regime are called licensing conditions.

PRINCIPLES OF JUSTIFIED LICENSES

Policy Framework Paper on Business Licensing Reform and Simplification specifies that the criteria and policies guiding the sectors and activities that should be subject to licensing vary widely among countries, and that there is no definitive list of activities that should or should not be licensed. The Framework Paper also states that licensing typically involves one or more of the following four broad features:

• It Identifies regulatory requirements (what is being licensed) and applications needed for a license;

• It requires prior approval to operate, and specific conditions to be met: the regulator receives the business application for a license, assesses and verifies the application, ensures specified conditions have been met, and provides formal approval to a business to operate in a specified sector;

• It sets operating conditions, where businesses are expected to comply with standards, conditions, and requirements specified in the license; and

• It enforces specified license conditions, standards, and requirements by the regulator through a variety of measures.10

Identifying regulatory requirements and applications are the only features universally applied in all licens-ing regimes. Without applications there would be no governmental approval and therefore no regulation enforced.

Licensing pre-conditions and licensing operating conditionsPrior approvals to operate, which require specified conditions to be met, and operating conditions are the key in a licensing regime. These represent the licensing conditions and can be subdivided into licensing pre-conditions and licensing operating conditions as they respectively apply prior to the approval and after the approval has been granted by the regulator.

The volume and depth of licensing pre-condition requirements and licensing operating conditions differ greatly from one country to another and among types of licensed activities. The key assumption is that in the absence of explicit or implicit licensing pre-conditions, the regulators have nothing to verify or approve. Therefore, this type of regulation can be applied prior to commencement of business activity without permission from the regulator through a simple declaration or notification. Indeed, many countries that reformed licensing regimes changed their licenses into notifications, which are friendlier to businesses and cheaper for government regulation. Therefore, justified licenses rather than the simple notifications must have clearly defined licensing pre-conditions.

Clearly defined licensing operating conditions therefore must be a part of all licenses to be considered as justified.

10 World Bank Group, Policy Framework Paper on Business Licensing Reform and Simplification, pp. 8–10.

12 Global Analysis of General Trade and Operational Licensing

If clearly defined specific operating conditions do not exist, the activity is regulated exactly as de facto any other business activity. It means that the licensing regime in these cases does not provide an additional regulatory benefit. Clearly defined licensing operating conditions therefore must be a part of all licenses to be considered as justified.

To further elaborate on the importance of licensing pre-conditions and licensing operating conditions for such justified licenses, it is necessary to re-visit areas in which licensing is most commonly applied. Overall, the justi-fied licensing regime can be applied in three broad areas, namely:

• Activities with potential risks to human safety and well-being, including environmental protection;

• Activities that deal with limited resources; and

• Activities that involve undesirable, although legal practices.

Activities with potential risks to human safety include activities that can directly or indirectly endanger human life, health, and well-being. This broad category therefore includes national security concerns, activities related to weapons, processing of foodstuffs, health care, elements of environment protection (for example, clean water and air), anti-monopoly regulations, energy, transportation, and the financial sector.

Activities that deal with limited resources relate foremost to radio frequencies (for example, communications), extraction of natural resources (mining, oil industry), use of some elements of infrastructure (rail transportation, wired communications), and any business that deals with activities subject to state quotas either for input or for output.

Activities that involve undesirable practices most commonly refer to production and sales of alcohol, tobacco, gambling, recreational drugs, and prostitution where these are regulated.

Box 1. Definitions of Licensing Pre-conditions and Operating Conditions (example of pharmacies)

Licenses required for retail pharmacies illustrate the difference between licensing pre-conditions and licensing

operating conditions. Generically, the licensing pre-conditions for retail pharmacies include:

• document of rent or ownership of premises;

• conformity of the premise with specified codes for pharmacies;

• proof of availability of secured and climate-controlled storage capacities;

• proof of employment of certified pharmacy specialists; and

• availability of proper record-keeping systems.

These pre-conditions are verifiable and must be met before a pharmacy becomes operational. A license is issued

only if these pre-conditions are met.

Operating conditions, in turn, can be monitored through inspections. These generically include:

• ongoing record keeping on medicines sold;

• clean premises; and appropriate storage and dispensing of medicines.

If operating conditions are found to be violated, the license can be suspended or eliminated.

Source: Iowa Board of Pharmacy, http://www.state.ia.us/ibpe/pharmacy/index.html

13Common Licensing Practices

Licensing pre-conditions for the first broad area of activities with potential risks to human safety should, as the definition of this area suggests, minimize potential risks. Licensing pre-conditions applied in this area are a set of rules that target minimization of risk factors for potentially dangerous activity prior to commencement of this business activity. In order to operate a clinic or pharmacy, a business must have certified premises and proper certified equipment. It should also hire licensed medical or pharmaceutical practitioners prior to opening a practice. These requirements indeed minimize potential risk factors associated with medical or pharmaceutical activities. Yet this is sometimes confused with the practice of licensing of professional qualifications. Licensing of medical practitioners almost in all countries requires proof of specialized medical education, whereby the medical diplomas serve as de facto licenses.

Licensing pre-conditions for the second broad area of activities that deal with limited resources are quite differ-ent in nature. Limited resources suggest that the regulations most frequently limit the increase in the number of operators and access to the limited resources through quotas and exclusive rights of exploration. The best example of such licensing pre-conditions can be found in licensing of cell phone communication providers, TV, and radio stations. Ideally, licensing preconditions for these activities consist of necessity to purchase radio frequencies through an open bidding process. Other examples include license for oil or minerals extraction. Here, the main license pre-condition is linked to the ownership (lease) of the extraction area and sometimes the concessional production quota.

Licensing pre-conditions for the third broad area of activities that involve undesirable, although regulated, practices are different from the first two cases. They most frequently deal with the location of intended activity. For example, in many countries where gambling is legal, location of gambling facilities is highly regulated. Sometimes businesses must purchase quotas on gambling tables or machines. Locations of alcohol retail outlets are also regulated in relation to proximity to schools, playgrounds, churches, etc. For example, in Washington, D.C., potential operators of liquor stores or bars must obtain “no objection” from neighbors. However, unlike the two previous areas, licensing pre-conditions are not as clearly defined. Countries and communities have different objectives in regulating these activities. These objectives are reflected in licensing pre-conditions.

Quasi-fiscal function of licensingA significant number of business activities falls simultaneously into more than one broad area defined above. Most frequently they fall into the first and second areas. In such cases licensing pre-conditions are more complex and use general rules for the first and second areas. Good examples here are mining operations or rail transpor-tation. In addition to these business activities being potentially dangerous, they use limited resources. Indeed, most activities from the second broad area—limited resources—to some extent also belong to the first area, that is, activities with potential risks to human safety.

Numerous publications stress that the licensing regime should not have a fiscal function other than the direct cost recovery. Indeed revenues are most effectively collected by taxes. However, the second broad area of licens-ing that deals with limited resources has in its nature elements of justified revenue collection through purchases of quotas, or through public offering of concessions.11 Elements of the justified revenue collection are also present in some aspects of the third area if quotas are sold.12

Enforcement of licensing regimeFinally, enforcement of licensing regimes is very important. Even where properly specified licensing conditions exist, yet enforcement of these conditions is absent or ineffective, businesses will be motivated to operate out-side the regulated zone. This can make the licensing regime completely obscure and unapplied. Most frequently, however, enforcement is absent if licensing conditions are not specified. In both cases such a licensing regime is ineffective or fails to render benefits. Thus, enforcement of licensing regimes is essential for any justified licenses.

11 In some cases direct purchasing of quotas can be changed into payments of royalties. 12 These are most commonly used in gambling industries.

14 Global Analysis of General Trade and Operational Licensing

What licensing should not regulateLicensing is considered to be one of the most invasive and expansive regulatory tools. Indeed, there are sectors and business activities that need to be regulated to protect people and the environment, or to otherwise maxi-mize public good. However, there are numerous regulations beyond licensing that are effective in addressing any market shortcomings. These are:

• Obligatory and voluntary certifications of goods;

• Voluntary certifications of services;

• Notifications of regulatory compliance;

• Process inspections; and

• Trade associations or other non-governmental associations’ accreditations.

Licensing should be reserved for the most potentially hazardous activities. In his paper, Occupational Licensing, Morris M. Kleiner addressed the issue of how legally obligatory state licensing of various professions in the United States can distort employment, wages, level of services, and overall economic outlook of communities.13 Licensing should be approached as regulation of last resort only in areas where other regulations cannot achieve well-justified goals.

UNJUSTIFIED LICENSES

For the licenses to be justified, all four broad features of licensing specified in the Framework paper must be present (from application to enforcement). However, the existence of licensing conditions, their clarity and effectiveness are the key in defining the justified licenses. Thus, problems with licensing conditions or their absence are the main features of unjustified licenses.

There are several variants where licensing conditions are either absent or do not have a defined utility. Most prominently these are:

• General licenses

• Sector licenses

• Location licenses

• “Benefits” licenses

With general licensing, pre-conditions and operating conditions either do not exist as separate requirements, or they are fully repeating general requirements for all businesses to begin operations or general rules of con-duct. This case is indeed widespread and in such instances has a form of general business or trade license. These licenses can be applied both at national and local levels. An example of this type of unnecessary license applied at the local level is presented in Box 2. Examples of countries that either issue such licenses at the national level or explicitly authorize subnational authorities to issue them are presented in Box 3. Some main characteristics of these licenses:

• They require universal coverage (all businesses that are in operation in a particular location or country must have such licenses);

• Licensing pre-conditions either do not exist in addition to the proof of registration, or they are of general nature and relate to the proofs of bank accounts, addresses, and registrations with various state and local offices;

• These licenses do not have operating conditions that are activity specific;

• They do not provide additional benefits except the opportunity to operate legally; and

• One general license enables business to operate in multiple locations either nationally or in a municipality if such a license was issued locally.

13 Kleiner, Journal of Economic Perspectives, pp. 189–202.

15Common Licensing Practices

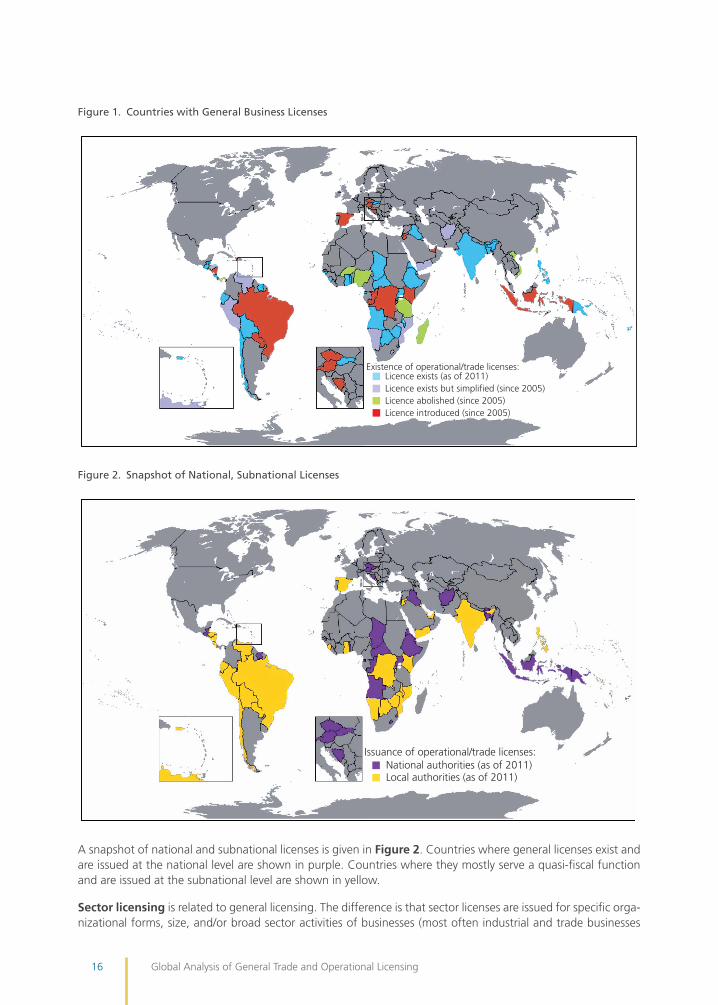

Figure 1 outlines the countries where such general licenses still exist (blue); the countries that have undertaken reforms, which resulted in their significant simplification but not extinction (purple); the countries where such licenses have been removed altogether (green); and finally the batch of countries where the reforms slid back and reintroduced the general licenses (red). The majority of countries nevertheless remain uncolored, that is, not running the practice of operational licenses. The map is based on the table in Annex 1 of this report and illustrates the snapshot of information as per the Doing Business 2012 report.

Box 2. Basic Business License in Washington, D.C.

Starting from 2009, the District of Columbia began requiring all businesses that pay business taxes to have a

valid District of Columbia Basic Business License (BBL). Under the Business Licensing Processing Adjustment Act of

2008 passed by the D.C. Council, an estimated 10,000 previously unlicensed businesses were required to obtain a

General Business License.

The introduction of the new license allowed the District government to identify businesses now subject to licensure

and take enforcement action against businesses operating without a license in the District. This supposedly

prevented illegal business from negatively influencing legitimate commerce and protected consumers in the District

from poor business practices.

The General Business License costs $110 per year and is being charged biannually. An application fee of $77 and a

$27.50 activity fee are due with the application. The total cost was $324.50 for a General Business License.

Box 3. Examples of General Business Licenses in Existence or Recently Reformed

Bosnia and Herzegovina: issued at subnational level; operating licenses cover all sectors.

Comoros: issued at the national level; operating licenses (patente) cover all sectors.

Kenya: issued at the subnational level; Single Business Licenses, cover all sectors.

Papua New Guinea: issued at the subnational level; trade licenses cover all sectors.

Peru: issued at the national level; operating licenses cover all sectors.

Philippines: issued at the subnational level; mayor’s licenses cover all sectors.

Qatar: issued at the national level; commercial licenses cover all sectors.

Tanzania: issued at the subnational level; business licenses cover all sectors as well as general industrial licenses

issued at the national level (see Case No.1).

Tonga: issued at the national level; general business licenses cover all sectors.

Vanuatu: issued at the subnational level; business licenses cover all sectors.

Vietnam: issued at the subnational level; business licenses cover all sectors.

Source: Investment Climate Advisory Services, World Bank Group

16 Global Analysis of General Trade and Operational Licensing

A snapshot of national and subnational licenses is given in Figure 2. Countries where general licenses exist and are issued at the national level are shown in purple. Countries where they mostly serve a quasi-fiscal function and are issued at the subnational level are shown in yellow.

Sector licensing is related to general licensing. The difference is that sector licenses are issued for specific orga-nizational forms, size, and/or broad sector activities of businesses (most often industrial and trade businesses

Existence of operational/trade licenses:Licence exists (as of 2011)Licence exists but simplified (since 2005)Licence abolished (since 2005)Licence introduced (since 2005)

Figure 1. Countries with General Business Licenses

Issuance of operational/trade licenses:National authorities (as of 2011)Local authorities (as of 2011)

Figure 2. Snapshot of National, Subnational Licenses

17Common Licensing Practices

Box 4. Examples of Countries with Sector Licenses

Afghanistan

National government in Afghanistan issues 1-year duration licenses for:

• Domestic individual traders

• Domestic corporations

• Foreign or foreign-domestic joint venture companies

Bhutan

National government in Bhutan issues 1-year duration licenses for:

• Retail trade

• Wholesale trade

• Services

• Production and manufacturing

Botswana

National government in Botswana issues or authorizes local governments to issue 1-year duration licenses for:

• Industry, which includes all sectors except trade

• Trade

Cambodia

National government in Cambodia issues 1-year duration licenses for:

• Small and Medium production companies (industry)

• Large industrial enterprises

• Trade

Indonesia

Subnational governments in Indonesia issue 1-year duration licenses for:

• Industry, which includes all sectors except trade

• Trade

(continued next page)

need licenses that are different from each other). These licenses are mostly issued by national authorities and may still be accompanied by additional licenses. Examples of sector licenses are presented in Box 4. Sector licenses have the following characteristics:

• They tend to cover all businesses in a given country because of their multiplicity;

• In most cases these licenses have clearly specified duration limits;

• Licensing pre-conditions either do not exist other than the proof of registration, or they are of a general nature and relate to the proof of bank account, address, registration with various state and local offices, and any other proofs for applied specifications (organizational form, size, broad activity area);

• Operating conditions are not specified in addition to other codes of business conduct.

Location licenses are issued for specific locations, although they do not deal with limited resources. These licenses are mostly issued by local authorities. An example of a typical location license is presented in Box 5. The main characteristics of these licenses are:

18 Global Analysis of General Trade and Operational Licensing

Box 4. (continued)

Lesotho

National government in Lesotho issues 1-year duration licenses for:

• Manufacturing, which includes all sectors except trade

• Trade

Zambia

Subnational governments in Zambia issue 1-year duration licenses for:

• Retail trade

• Wholesale trade

• Manufacturing

Source: Investment Climate Advisory Services, World Bank Group

Box 5. The Case of Barber Chair Licenses in Washington, D.C.

If someone in Washington, D.C., intends to independently lease, rent, or become authorized to occupy a barber

chair from the owner of a barber shop to perform barbering services such as shaving, beard trimming, cutting, and

boding the hair as well as giving shampoos, facial, and scalp massages, he or she needs to apply for a business

license, according to D.C. Code 47-2847, DCMR Title 17, Chapter 37 §3720.

The duration of this license will be two years and it will cost applicant:

• $78 for the category license fee;

• $70 for the application fee;

• $25 for the endorsement fee; and

• 10 percent of total for the technology fee

In order to obtain this license, applicant must fulfill the following requirements:

• Obtain a Certificate of Occupancy for Compliance for Zoning Regulations for the one planned location;

• Obtain corporate registration and tax registration. This is not required for sole proprietors, although if they are

not D.C residents, they must complete the Certified Resident Agent Appointment Form;

• Certify that they do not owe more than $100 to the D.C. government as a result of fees, penalties, interest, or

taxes through completion of a Clean Hands form provided in the application package. A signed form from the

Office of Tax and Revenue may also be required;

• Submit a properly completed Basic Business License application; and

• Verify that they have a valid barber’s license approved by the D.C. Barber and Cosmetology Board.

• They are issued for business activities at a specified address or location for business activity.

• They always have clearly specified duration limits (related to time and/or operations at the location).

• Licensing pre-conditions either do not exist other than the proof of registration, or they are of a general nature and relate to the proof of bank account, address, and registration with various state and local offices. Their issuance can also be subject to holding other licenses.

19Common Licensing Practices

Licensing:Business operations (as of 2011)Office space (as of 2011)

Figure 3. Countries Where General Licenses are Linked to Premises

• Operating conditions are not specified other than the general codes of business conduct, such as keeping proper fiscal records, providing product information disclosures, providing information on operating hours, and fulfilling legal requirements on labor, sanitary, and fire protections.

• Unlike the general license, one original location license enables businesses to operate only in one location. Additional locations in one municipality require either additional location licenses or amendments to original location licenses.

Figure 3 shows the countries where general licensing is linked to premises (red) and where licenses are more of a sector nature or related to occupation.

A “beneficial” license in the form of a permit, registration, or certificate gives holders certain benefits. These benefits come either in the form of lower taxation or any form of services provided to companies (such as training, marketing, and so on). Beneficial licenses are mostly issued by chambers of commerce, investment promotion agencies, free economic zone administrations, business associations, and Micro Small and Medium Enterprise (MSME) support agencies. Examples of beneficial licenses are presented in Box 6. The main charac-teristics of these licenses are:

• They are obligatory, despite the declared promotional or service-oriented nature of these licenses.

• They cover businesses depending on certain company characteristics (for example, companies created with foreign investments, or micro, small, and medium enterprises) as well as on overall area of business activities (these are licenses issued by trade or business associations if they are obligatory).

• Their licensing pre-conditions are related only to the licensed category qualifiers. For example, if ”benefits” are intended for SMEs, a company should submit evidence that it falls under this category in terms of the number of its employees or financial turnover, whichever is applicable.

20 Global Analysis of General Trade and Operational Licensing

Box 6. Examples of Countries with Beneficial Licenses

The most common benefit from obtaining these licenses from the specific para-state sector authority is membership

with the associations, most often with the chambers of commerce. These institutions offer discounted services

and certain free features to their members, but the license, that is, membership, is compulsory with the national

association, even where voluntary business associations exist in the same country.

Bolivia: obligatory registration at the appropriate Chamber of Commerce or Industry.

Bosnia and Herzegovina: obligatory registration of exporters with the national Chamber of Commerce.

The Republic of Congo: obligatory registration with the Chamber of Commerce.

Fiji: obligatory registration with Training and Productivity Authority.

Honduras: obligatory registration with Hand Labor Training Institute.

Jordan: obligatory registration with the Chamber of Industry or Chamber of Commerce.

Kuwait: obligatory registration with the Chamber of Commerce and Industry.

Qatar: obligatory registration with the Chamber of Industry and Commerce.

Republica Bolivariana de Venezuela: obligatory registration with the National Institute of Socialist Cooperation

and Education.

Source: Investment Climate Advisory Services, World Bank Group

21Demystifying Formal Justification for Existence of Unnecessary Licenses

Demystifying Formal Justification for Existence of Unnecessary Licenses

General licenses, sector licenses, location licenses, and beneficial licenses, while having no unique licensing conditions attached to them, can have declared or implicit functions. These functions are most frequently spelled out in preambles to the legislation that establishes them, in justification to such legislation, or can be deduced from other legislation or policies. Depending on countries and localities, these licenses have either one or more functions:

• They are used to collect information.

• They are used to raise revenue.

• They establish eligibility.

• They protect markets or consumers.

• They exercise state oversight.

The two most common are informational and fiscal functions. Both national and local governments try to collect as much information about businesses as possible. This information is used for policy planning and budget allocations. One of the easiest methods for the public sector to collect such information is through obligatory reporting requirements. Obligatory reporting is most frequently tied to tax reporting, although in some countries and locations it has its own means through obtain-ing general licenses and their regular renewals. Information collected through this method varies from country to country but most frequently includes data on number of employees, assets, capital investments, types of activities, and their locations.

The use of licensing for information collection purposes is very expensive for the public sector, which has to establish and fund licensing authorities, and cover the costs of issuing licenses, their ex-post verification, and inspection procedures. More importantly, these costs are almost always in part or fully shifted to the private sector. It is very expensive, time consuming, and somewhat uncertain for businesses to fulfill information requirements. Less intrusive ways for information collection used in countries with no general licensing are presented in Box 7.

Quasi fiscal functions of licensing are widespread, especially at the local levels of government. License fees frequently form a significant portion of the local authorities’ revenues. Fiscal functions of licensing are described in significant detail in OECD and World Bank Group publications, most notably in the Policy Framework Paper on Business Licensing Reform and Simplification and in Avoiding the Fiscal Pitfalls of Subnational Regulation. For all types of licenses, including justified, this paper stipulates that the transparent imposition of fees and charges by the licensing regulator can be appropriate to recover only the administrative costs to government of delivering that license service. The imposition of what are quasi taxes “disguised” as license fees and charges create costs and a high level of uncertainty among businesses. Moreover, the use of licensing to raise revenue for local (and national) authorities is generally recognized as an inefficient way to raise revenue compared with broader tax regimes. Good and recommendable practice when it comes to licensing

22 Global Analysis of General Trade and Operational Licensing

Box 7. Alternative and Less Obtrusive Methods of Information Collection

Annual reporting to business registry

• Evidence shows that regular requirements to report to the single business registry add value to businesses by

maintaining accurate records and eliminating all long-idle or non-existent businesses. this is sometimes linked to

tax reporting, where the registry is shared.

• The cost of reporting is minor and it can often be completed online. when no changes to the records have

occurred over a year, the notification is most simplified.

• The data captures all incorporated entities (not microbusinesses), is accurate, and most up-to-date, and can cross

feed a number of other public services and databases, thus synergizing efforts.

Enhanced tax reporting

• This method relies on already existent tax reporting with small adjustments to collect data otherwise absent from

tax reporting, but needed by governments.

• It adds only a fraction of the cost to the private sector in comparison with licensing, and is spread equally through

the entire sector.

• Data collected through this method is more reliable than data collected through licensing due to higher

probability of verification through tax inspections.

• It significantly reduces public sector costs.

Business surveys

• This method is significantly cheaper than obligatory licensing for the private sector.

• Data collected through this method can be broader and include indicators on trends and attitudes.

• It is easier to add or eliminate certain data requirements, and this tool is more flexible.

• The cost of data input is lower due to the use of sampling, while the cost of analysis is comparable.

• This tool requires a procurement budget, although it provides savings for operational budgets.

• The method requires a non-government capacity to conduct surveys, although in some cases this can be done by

government institutions or organizations.

and revenue increases is typically very precise.14 In other words, licenses should generally not be used as a vehicle to raise revenue above cost recovery because it is a highly inefficient revenue collection mechanism, and because it imposes great uncertainty on licensed businesses.

When the key declared purpose of unjustified licenses is revenue collection, the argument of cost recovery is even more striking. There is one exception, however, mentioned in the chapter on justified licenses. If such a license has a function of preemptive simplified tax for certain types of businesses, and eliminates future tax liability and reporting requirements, the fiscal nature of such a license as well as the license itself is justifiable. Examples of these are the optional fixed taxes introduced on small businesses in Ukraine in 2000. Businesses that choose such taxation pay a monthly fixed preemptive tax that covers all their tax liabilities and releases them from having to report taxes.

Establishing the eligibility function of licensing refers only to “beneficial” licensing. Indeed, many countries have special regimes that benefit certain types of businesses to promote investments, growth of SMEs, innovations,

14 World Bank Group, Policy Framework Paper on Business Licensing Reform and Simplification.

23Demystifying Formal Justification for Existence of Unnecessary Licenses

manufacturing, and so on. In order to apply beneficial regimes only to eligible businesses, governments use licenses with proof of eligibility function. Unfortunately, if it is in the form of a license it becomes obligatory. Due to that obligatory nature, this type of regulation imposes administrative burdens on all businesses that may be eligible for established benefits regardless of their wish to use these benefits. Thus, making such licensing voluntary, in the form of an application to establish eligibility for benefits, will fully remove this administrative burden and effectively eliminate such common licensing.

The next two functions, namely protection of competition or consumers and exercising state oversight have one thing in common. Indeed, state institutions can exercise “control” through discretionary issuing of licenses and revoking them, although these actions do not have an objective basis because of the absence of licensing conditions that can be violated. In other words, exercised “control” in such instances amounts to nothing more than a case-by-case abuse of power. These practices of discretionary enforcement of licenses with no licensing conditions are plagued by corruption, significantly increase unpredictability of the business environment, and represent one of the most damaging licensing regimes. Thus, such licenses can be eliminated without any regulatory replacement.

Finally, there are cases when the licensing functions do not exist in an explicit form. The reasons for these instances can be numerous. In some cases these are remnants of otherwise reformed licensing regimes. In other cases these are products of reforms when licenses became consolidated and governments did not spell out the reasons for the existence of unified licenses. The main cause for this is the risk-aversion of government institutions. Centrally planned countries find it complex to outsource the previously traditional government activities or deregulate what used to be heavily regulated. Absence of licensing conditions as well as explicit reasons or functions of these regulations make these licenses one of the easiest cases for full removal with no replacement.

Yet, matching these formal grounds for issuing the license with their costs portrays a very different picture. In the table below, which summarizes data collection on selected IFC projects, the costs greatly outweigh the benefits. The calculation in Table 1 shows the total costs in official fees for the licenses, the duration of which is only one year (therefore the same costs re-emerge every year), for all the economic entities that are required to possess one. In addition, the time lost while waiting for the license approval is de facto the time during which the enterprise could not legally operate (yet it was ready to be inspected and licensed, therefore prepared to work) and therefore represents the total private sector’s time lost due to that specific bureaucratic procedure. This simple calculation does not go into the details of all direct and indirect costs imposed by the inability to legally operate while waiting for the license to be issued.15 All licenses represented in the table below apply to a majority of enterprises in its total population (commercial registry) and the number of licenses issued per year is also given.

Among these figures, there are some that are a significant source of revenue, particularly for the local govern-ment that issue them, where the license performs a quasi-fiscal function, as discussed above. The following chapter looks into a possible transformation of such fiscal requirements into a MSME tax policy, thus reducing some costs, but also the associated time loss.

15 The exception to this are license renewals, where their portion of time is only the time of the relevant staff and proportion of the management staff time lost in dealing with the regulatory requirements.

24 Global Analysis of General Trade and Operational Licensing

Table 1. Examples of Unnecessary Licenses and Associated Costs

COUNTRY NAME OF LICENSENO. OF LICENSES ISSUED IN 2009

FEES IN USD FOR PRIVATE SECTOR

NUMBER OF DAYS LOST FOR PRIVATE SECTOR

AFGHANISTAN Domestic Individual Trader Business License

new : 2,869 renewed: 2,701

186,647 16,710

Domestic Corporation License new : 3,598 renewed: 8,762

Source: IFC projects in the respective countries, license data as of end-2009.

25Reforming Unjustified Licenses

Reforming Unjustified Licenses

In countries with extensive licensing regimes, government officials may face a dilemma. Some of these licenses serve fully justified regulatory functions while others assist the government in obtaining information on businesses, collect revenue, and serve as an oversight tool for particu-lar businesses. Moreover, the governments aspire to care about protecting consumers and do not allow entrepreneurs to run amok and defraud their clients. In such controlled economies, generations got used to a heavily regulated business environment. Nevertheless, investors remain unhappy doing business in these countries. Some think-tanks and international organizations rank these business climates quite low, and economies are not developing as fast as wanted. The first approach in this dilemma is to do nothing, or simply invest resources in a public relations campaign to attract investors. Indeed, the embedded risk aversion of most governments leads to this choice.

The second choice is to undertake systemic, well-designed, and gradual reform. Again, risk aversion of the public sector plays a role here. For any adopted and practiced policy there are few incentives to change it. Even if the beneficiaries and perhaps also regulators agree that a licensing regime is ineffective, expensive, and provides only ephemeral benefits, there is no information on what a new regime will do. A solution is a systemic analysis, undertaking of regulatory impact assessments, rewriting and streamlining of poor regulations, modeling future impacts, and trying to replace outdated regulatory tools with more efficient ones, as indicated in the next paragraph. The focus is always on ensuring that the declared functions are not left unimplemented. This approach is almost always fully justified and produces positive reform results.

The World Bank Group publication How to Reform Business Licenses provides detailed advice to practitioners on standard stages and steps to implement business licensing reform. There are 33 clearly defined steps needed for a comprehensive reform of a licensing regime. They include desk review of existing diagnostics, stakeholder and political economy analysis, legal implementations of decisions, establishing reviewing regulatory management capacity, and exploring the need for a business regulations bill.”16

It is safe to assume that the entire range of tools, although highly important and recommended, is never fully used. The main reasons for this include a lack of government capacity or long-term dedication, prior partial reform efforts, and others. Even in the successful cases where countries followed most of these recommendations, some post-reform backsliding is possible.

Absence of unique licensing conditions in these cases nullifies the declared regulatory benefits.

The gradual reform described above is almost always justified. The cases of unjustified licensing described in this paper make the reform imperative for the set of business licensing, where the simplification approach can and should be undertaken. At the beginning of this paper it was argued that the reason for examining unjustified licensing is because, in practice, there are numerous examples when reform practitioners engage in prolonged and costly reforms drafting replacement regulations in cases that warrant outright elimination of unnecessary and unjustified licenses. Absence of unique licensing conditions in these cases nullifies the declared regulatory benefits. It was argued earlier that the information function is much more reliably

16 World Bank Group, How to Reform Business Licenses, pp. 53–57.

26 Global Analysis of General Trade and Operational Licensing

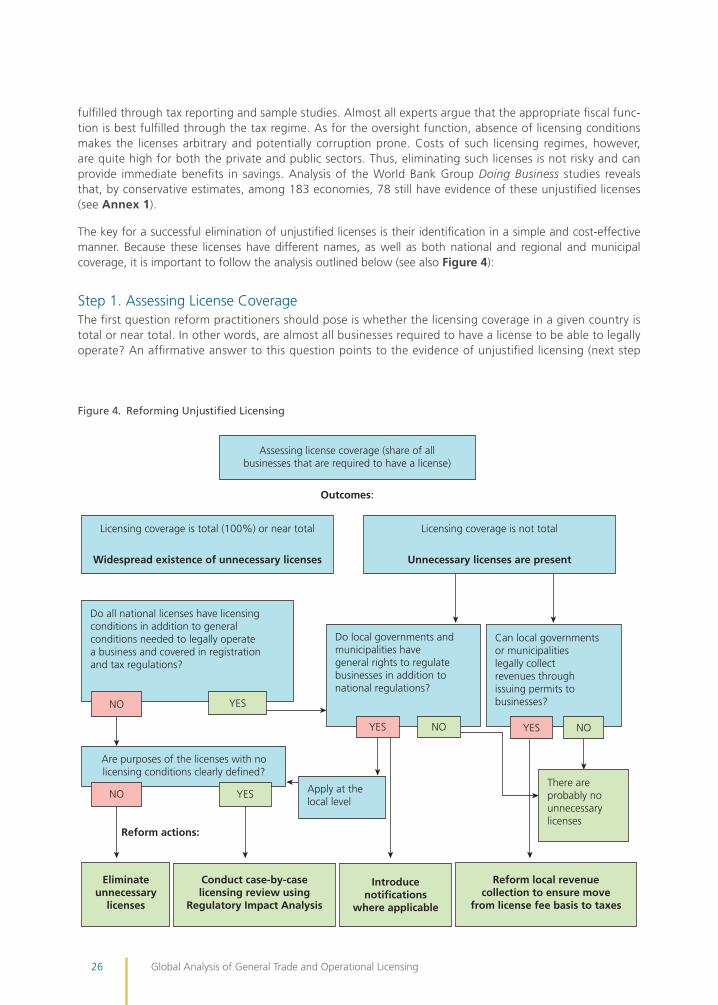

fulfilled through tax reporting and sample studies. Almost all experts argue that the appropriate fiscal func-tion is best fulfilled through the tax regime. As for the oversight function, absence of licensing conditions makes the licenses arbitrary and potentially corruption prone. Costs of such licensing regimes, however, are quite high for both the private and public sectors. Thus, eliminating such licenses is not risky and can provide immediate benefits in savings. Analysis of the World Bank Group Doing Business studies reveals that, by conservative estimates, among 183 economies, 78 still have evidence of these unjustified licenses (see Annex 1).

The key for a successful elimination of unjustified licenses is their identification in a simple and cost-effective manner. Because these licenses have different names, as well as both national and regional and municipal coverage, it is important to follow the analysis outlined below (see also Figure 4):

Step 1. Assessing License CoverageThe first question reform practitioners should pose is whether the licensing coverage in a given country is total or near total. In other words, are almost all businesses required to have a license to be able to legally operate? An affirmative answer to this question points to the evidence of unjustified licensing (next step

Outcomes:

Reform actions:

Licensing coverage is total (100%) or near total

Widespread existence of unnecessary licenses

Licensing coverage is not total

Unnecessary licenses are present

Assessing license coverage (share of allbusinesses that are required to have a license)

Do local governments andmunicipalities havegeneral rights to regulatebusinesses in addition tonational regulations?

Can local governmentsor municipalitieslegally collectrevenues throughissuing permits tobusinesses?

Do all national licenses have licensingconditions in addition to generalconditions needed to legally operatea business and covered in registrationand tax regulations?

NOYESNOYES

YESNO

Are purposes of the licenses with nolicensing conditions clearly defined?

Apply at thelocal level

NO YES

Reform local revenuecollection to ensure move

from license fee basis to taxes

Conduct case-by-caselicensing review using

Regulatory Impact Analysis

Eliminateunnecessary

licenses

Introducenotifications

where applicable

There areprobably nounnecessarylicenses

Figure 4. Reforming Unjustified Licensing

27Reforming Unjustified Licenses

is Step 2). A negative answer does not deny the existence of these licenses. They still can have a local or otherwise limited application (next step is Step 5). Methods of assessing license coverage can be the following:

• Business survey data;

• Legal analysis and an inventory of licenses (with emphasis on commercial codes; licensing laws; laws on functions of ministries, other national agencies, local governments, and municipalities; laws on local taxes and fees); and

• Focus groups with representatives of business associations and lawyers.

Step 2. Identifying General Licenses and Sector Licenses Issued at the National LevelIf licensing coverage is total or near total, it is necessary to look for general licenses that are issued immediately after business registration to all businesses regardless of their size, legal form, or main activities. In some cases, issuing of such licenses can be incorporated into business registration procedures, especially through registra-tion of one-stop shops where they exist. If such a license is identified, it is a general license that fits the definition of unjustified licensing.

Similarly, if licenses are issued to broad categories of businesses, such as for industrial production, trade, and services, or if different licenses are issued to businesses based on their size, these are likely to be sector licenses that also fit the definition of unjustified licensing.

Step 3. Reviewing Other Licenses at the National LevelIn this step, the reform practitioners should ask the question whether the mapped licenses have licensing conditions in addition to the general conditions needed to legally operate a business and covered in the registration and tax regulations. It is important at this stage only to look at the existence of such licensing conditions, not their analysis. If licensing conditions do not exist, these licenses are either unjustified or questionable.

To separate unjustified licensing from questionable licenses, one should look at the declared purposes of such licensing. If these purposes are not defined, these licenses are unjustified. In other instances, more in-depth case-by-case analyses are necessary to separate unjustified licenses from questionable licenses.

A very simple calculation of costs can also be undertaken by multiplying the number of such licenses issued with the official fees as well as the waiting time, in order to arrive to the direct costs for the private sector. These figures present potential private sector savings and increase productivity – a policy argument for technical level staff to justify the reforms to policymakers.

Step 4. Eliminating Unjustified Licenses at the National LevelAfter unjustified licensing is identified, a further reform effort should target their full elimination. Indeed, general and sector licenses at the national level do not fulfill any functions except an informative one. As seen above, the information collection is more reliable and cheaper using other, already existing methods, mostly tax reporting. Thus, these licenses can be eliminated outright. “Beneficial” licenses should become voluntary. This will eliminate them as regulation. Thus, national-level unjustified licenses can and should be eliminated without replacements.

Licenses can be eliminated by preparing amendments to the specific laws or bylaws that introduce each one, or as a lex specialis that overrules several previous legal acts in one go.

Step 5. Assessing Opportunities for Unjustified Licenses at the Local Level Existence of unjustified licensing at the local level is more difficult to identify. At the beginning one should look if, according to laws, the subnational governments and municipalities can collect revenues by issuing licenses

28 Global Analysis of General Trade and Operational Licensing

to businesses. An affirmative answer leads to a high probability of unjustified licensing at the local level. The next question is whether the subnational governments and municipalities have general rights to regulate busi-nesses in addition to the national regulations (not specifically established for different areas of possible impact or business operations). An affirmative answer further increases the likelihood the licenses are unjustified. In such cases, selective mapping of local regulations should be undertaken to identify licenses without licensing conditions, licenses that require regular (mostly annual) renewals, and conform to other tests performed at the national level and presented above. Also, national laws sometimes can directly point to unjustified licensing at the local levels.

Step 6. Reforming Unjustified Licenses at the Subnational LevelAt the subnational level, the most common functions of unjustified licenses are fiscal and informative. An Information function at the local level is more difficult to replace than at the national level. There are countries where business registration and enforcement of revenue collection are done at the national level. With no effective system of information sharing between national and regional or municipal levels, it is evident that local governments impose licensing to map businesses in their jurisdiction. However, this legitimate function can be fulfilled with much less intrusive form of regulation, namely notification. This approach also relates to the “location” licenses issued at the municipal level. Proper zoning rules and notification systems replace such licenses, but may be more costly and complex to establish. The regional or municipal level unjustified licenses should be replaced by new elements of revenue collection consistent with the overall regime of taxation and notifications if necessary (see Box 8).

In all questionable cases a review based on a regulatory impact assessment approach, as specified in the World Bank Group publication How to Reform Business Licenses, is necessary.

Step 7. Ensuring Effective Functioning of Justified Licensing Regime After unjustified licenses are removed or replaced with notifications or new elements of taxation, it is essential to ensure:

• Enforcement of unjustified licenses indeed ended;

• Re-introduction of these licenses in another format is prohibited;

Box 8. Potential Revenue Implications of Business Licensing Reforms in Zambia

The study finds that the proposed reclassification of all business permits issued by local authorities into a levy to be

paid over the counter, as already envisaged by the government for the fiscal year 2011, will have minimal impact on

local government revenues over the short term. From the regulatory efficiency standpoint, success of this reform,

in the short term, is contingent upon constraining the capacity of City Councils to introduce new business permits

since they retain such powers under the Local Government Act.

The proposed repeal of the Trade Licensing Act that will eliminate all trading licenses is unlikely to constrain

Councils’ ability to efficiently regulate business activity since this objective can be achieved under primary regulating

laws such as the Health Act, the Town & Country Planning Act, and others. However some negative revenue impact

will be experienced depending on the level of dependence by local councils on revenues derived from this source.

For example, in both Mazabuka Municipal Council and Chibombo District Council, the elimination of trading

licenses will result in a loss of about 85 percent of business licensing revenue. However, the overall impact on total

Council revenues will be minimal, because trading licenses contribute a small percentage (between 3.5 percent and

12 percent) to overall council revenues. Nonetheless, there is a need to put in place mitigating measures to ensure

successful achievement of reform objectives.

Source: Republic of Zambia, Report on Revenue Impact of Business Licensing Reforms, p. 117.

29Reforming Unjustified Licenses

• Remaining licenses are fully justified and properly enforced; and

• Costs and benefits of this reform are properly calculated and communicated.

Ensuring that the enforcement of unjustified licenses has ended is best done either through feedback surveys of compliance of businesses17 with the licensing regime, or in engaging in a structured dialogue with the busi-ness community.18 Similar methods are used to detect any reverse trends in the licensing regime. It is essential, however, to implement an institutional system that will minimize opportunities for such backsliding. The World Bank Group publication How to Reform Business Licenses provides guidance on creating and maintaining such a system. This publication also advises how to ensure that remaining licenses are fully justified and properly enforced.19 In cases when unjustified licenses are replaced by notifications or changes to the tax regime, it is necessary to conduct a follow-up assessment on efficiency of new methods of revenue and information collec-tion in comparison with the old regime. Measurable benefits of reforms that will follow from such comparisons should be communicated to the business community and public at large to ensure political support for reformed governance. Lessons from the introduction of the Single Business Permit (SBP) in Kenya serve as excellent reminder of why these elements of reforms are indeed necessary (see Box 9).

Examples of the calculated savings of the recent reforms that IFC projects engaged in, supporting licensing simplification, demonstrate positive effects (Table 1 of the previous chapter), which led to significant savings to the private sector. Some of the examples include removal of the operating permit in Bosnia and Herzegovina, leading to the total elimination of the costs indicated in the table. In Kenya, the reforms led to 2 percent savings in cost and 97 percent savings in time. The simplification in Lima, Peru, resulted in an increase of 263 percent in the number of firms that decided to start operating formally (only in the first 6 months after implementation), and a reduction in the cost of getting the license of about 60 percent. IFC estimated savings in direct and indirect costs in the Philippines were as high as US$ 2.2 million as a result of 70 percent reduction in time and 10 percent cut in costs. Qatar’s license simplification reduced the issuance time by 1 day (50 percent) and QR 5,000 or approx. US$ 1,370 (50 percent) in fees. In São Paolo, a 1-day reduction in waiting time resulted in an estimated US$ 1.2 million in savings.

17 Surveys done on a sample of businesses to assess perception of regulatory compliance steps, time, and costs. 18 Examples include instituting a period for public commenting on the draft legislation, round tables with business associations, and open

hearings.19 World Bank Group, How to Reform Business Licenses, pp. 53–57.

Box 9. Lessons Learned from Introduction of the Single Business Permit in Kenya

The Single Business Permit was introduced in Kenya in 1999 to address proliferation of licenses at the local level.

The principles of SBP included:

• simplification (removing multiple and overlapping licenses, self-declaration by applicants, and uniform standards

across local authorities);

• local accountability (the Minister for Local Government “pre-approved” the fee schedule but each local authority

chose appropriate rates);

• local control and planning (to generate information needed by the local authority for planning, regulation, and

improved service);

• transparency (in order to reduce rent-seeking opportunities. Local authorities were allowed to revoke the SBP only

upon written request by the regulatory agent (for example, health officer, etc.) that the business had violated a

regulatory condition); and

• revenue generation by each local authority. It is important to note that already by design, the SBP was envisaged

as both a regulatory as well as a revenue instrument.

(continued next page)

30 Global Analysis of General Trade and Operational Licensing

Box 9. (continued)

When local governments introduced the SBP in 1999/2000, the SBP became the third most important source of

revenue after the Local Authority Transfer Fund (from the national government) and property-based collections.

Main Problems of SBP

With the introduction of the SBP, the administrative burden on businesses increased. It is now cited by businesses as

one of the main regulatory deterrents to business activity at the local level.

The government of Kenya’s Working Committee on Regulatory Reforms for Business Activity in Kenya (2007) noted

that the single business permit is the most troublesome of all local government licenses; the system of implementation

of the Single Business Permit by local authorities is not procedural; and the enforcement system adopted by the local

authorities is crude. Fundamentally, the single business permit has not been de-linked from other licenses.”

Summary of problems:

• While business in the formal sector faced higher administrative and financial costs under the Single Business

Permit, they continued to be exposed and subjected to other licenses, charges and fees, which should have been

consolidated into the Single Business Permit in 1999/2000.

• High number of “bands” for different sizes and types of businesses created ample opportunities for corruption

through negotiation of the terms.

• The SBP was not always used for its intended purpose—some local authorities impose the SBP merely for

transporting goods through the local authority’s territory for distribution elsewhere.

• Increase in a business’s economic activity could lead to an increase in the fee category (“band”) during annual

renewal of the SBP. At the same time, reduced economic activity did not lead to a reduction in the SBP fee.

• Coercive enforcement and rent-seeking by local officials, which further fostered resistance to payment and encour-

aged evasion. A well-known, if somewhat anecdotal, situation is the alleged propensity by some local authorities

to seek out regulatory infractions on business premises on a Friday afternoon, thereby necessitating bribes if the

business owner does not want to risk spending the weekend in prison before a court hearing on Monday.

• Local services have not improved with the introduction of the SBP. This was a main policy consideration about

justifying the initial purpose of a reform.