31

March 2013 22

Lower potential growth for the global economy

Fewer workers mean less output, an aging world economy

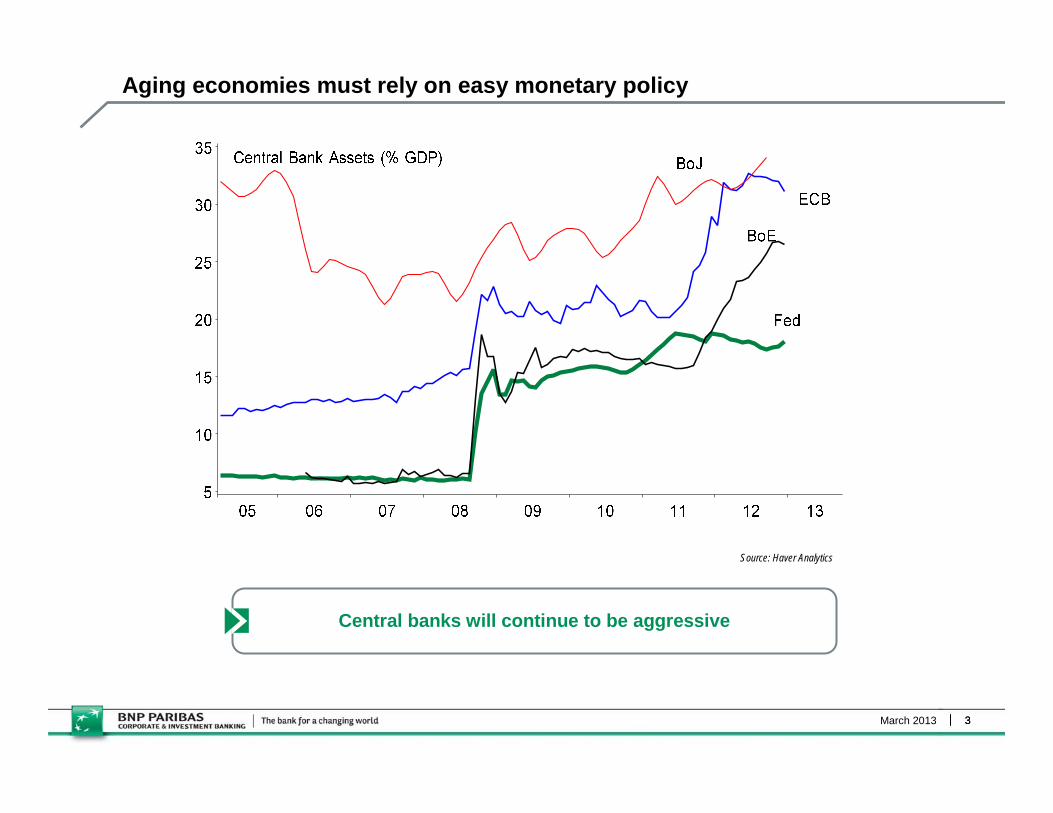

Source: Haver Analytics

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 1060.25

60.50

60.75

61.00

61.25

61.50

61.75

62.00

62.25

62.50

World employment to population ratio (%)

March 2013 33

Aging economies must rely on easy monetary policy

Central banks will continue to be aggressive

Source: Haver Analytics

4March 2013

The global manufacturing cycle is turning a corner (again)

4

The rebound is uneven and still vulnerable

Source: Reuters Ecowin Pro

5March 2013 555

Eurozone: Fiscal adjustment

The ‘peripheral’ eurozone member states are undergoing a period of concerted fiscal tightening

The change in the underlying fiscal stance is exceptionally large in 2012 in a number of countries

The adjustment is consistent with large output declines this year, even with a conservative ‘multiplier’ assumption

Concerted tightening

Source: Reuters EcoWin Pro, BNP Paribas

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Germany France Italy Spain Portugal Greece Ireland Eurozone

Change in Cyclically Adjusted Primary Budget Balance (% GDP)

2012

2011

2013

6March 2013

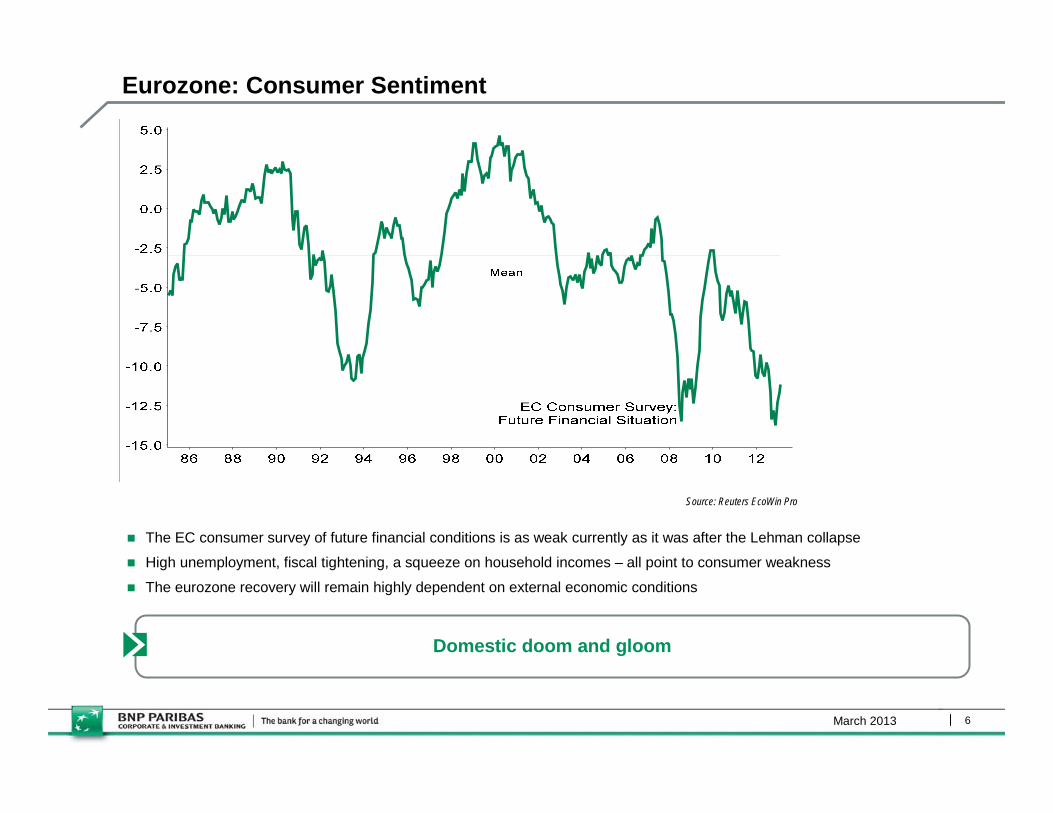

Eurozone: Consumer Sentiment

The EC consumer survey of future financial conditions is as weak currently as it was after the Lehman collapse

High unemployment, fiscal tightening, a squeeze on household incomes – all point to consumer weakness

The eurozone recovery will remain highly dependent on external economic conditions

Domestic doom and gloom

Source: Reuters EcoWin Pro

7March 2013 77

China: Money and credit key

Money growth is turning, although it remains constrained for now

Bank lending has picked up notably …

… especially when ‘other’ types of lending are included

This loosening of credit conditions is key to our belief that the economy is picking up

Source: Reuters Ecowin Pro, CEIC, BNP Paribas

Expansion underway, delicate tradeoffs for new regime

MH / DB

-4000

-3000

-2000

-1000

0

1000

2000

3000

4000

5000

6000

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Official new loans

Other lending*

Total

12-month change in year-to-date lending

* Entrusted loans, trust loans and bankers acceptances

8March 2013

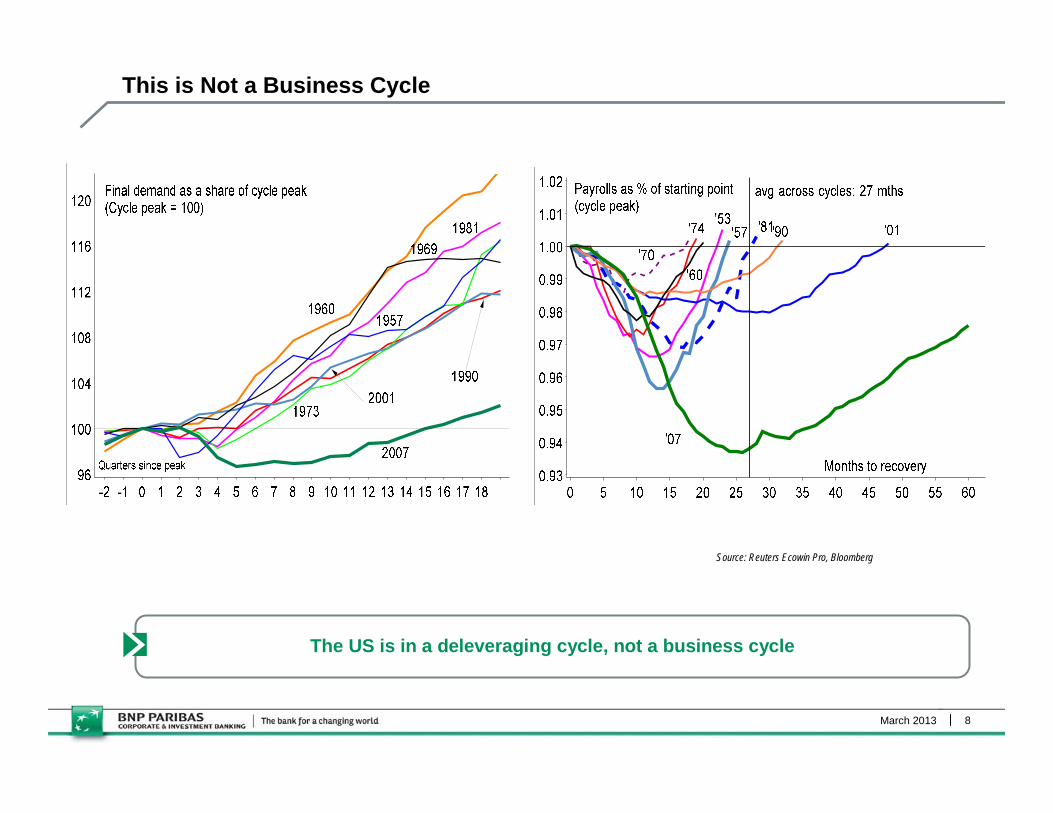

This is Not a Business Cycle

The US is in a deleveraging cycle, not a business cycle

Source: Reuters Ecowin Pro, Bloomberg

March 2013 9

A Nation of Cross-Currents

9

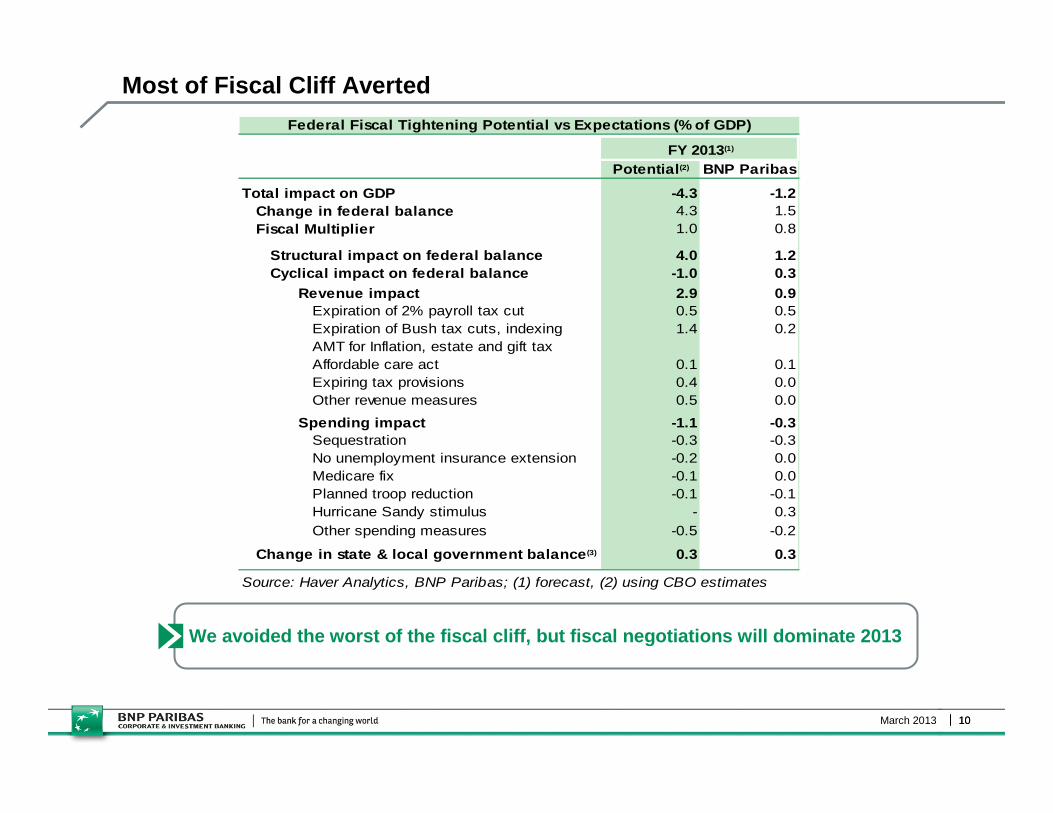

We avoided the worst of the fiscal cliff, but fiscal negotiations will dominate 2013

3.6%3.2%2.6%2.8%Underlying Pace2

-0.9%-1.3%-1.0%-0.8%Fiscal Tightening2

2.7%2.0%1.6%2.0%Real GDP

201412013120122011% Q4/Q4

Source: Haver Analytics, BNP Paribas; (1) Forecast (2) BNP Paribas estimates

March 2013 10

Most of Fiscal Cliff Averted

10

We avoided the worst of the fiscal cliff, but fiscal negotiations will dominate 2013

Potential(2) BNP Paribas

Total impact on GDP -4.3 -1.2Change in federal balance 4.3 1.5Fiscal Multiplier 1.0 0.8

Structural impact on federal balance 4.0 1.2Cyclical impact on federal balance -1.0 0.3

Revenue impact 2.9 0.9Expiration of 2% payroll tax cut 0.5 0.5Expiration of Bush tax cuts, indexing AMT for Inflation, estate and gift tax

1.4 0.2

Affordable care act 0.1 0.1Expiring tax provisions 0.4 0.0Other revenue measures 0.5 0.0

Spending impact -1.1 -0.3Sequestration -0.3 -0.3No unemployment insurance extension -0.2 0.0Medicare fix -0.1 0.0Planned troop reduction -0.1 -0.1Hurricane Sandy stimulus - 0.3Other spending measures -0.5 -0.2

Change in state & local government balance(3) 0.3 0.3

Federal Fiscal Tightening Potential vs Expectations (% of GDP)

FY 2013(1)

Source: Haver Analytics, BNP Paribas; (1) forecast, (2) using CBO estimates

March 2013 1111

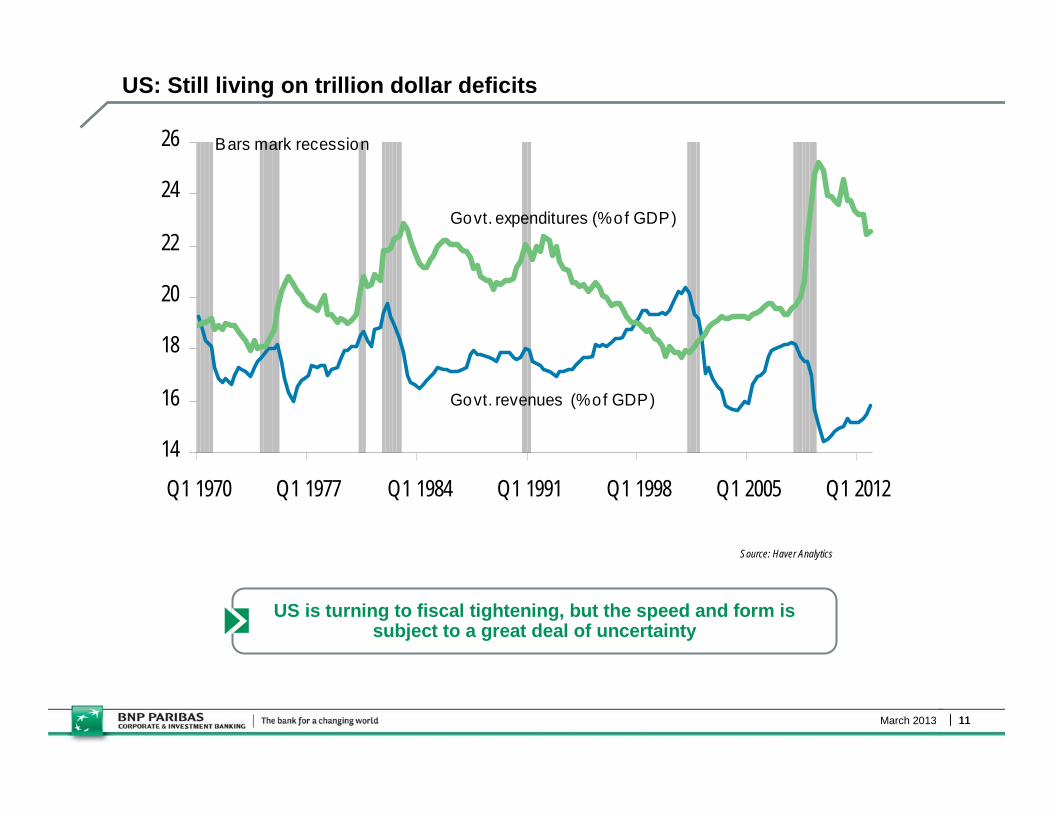

US: Still living on trillion dollar deficits

US is turning to fiscal tightening, but the speed and form is subject to a great deal of uncertainty

Source: Haver Analytics

14

16

18

20

22

24

26

Q1 1970 Q1 1977 Q1 1984 Q1 1991 Q1 1998 Q1 2005 Q1 2012

Govt. revenues (% of GDP)

Govt. expenditures (% of GDP)

Bars mark recession

March 2013 12

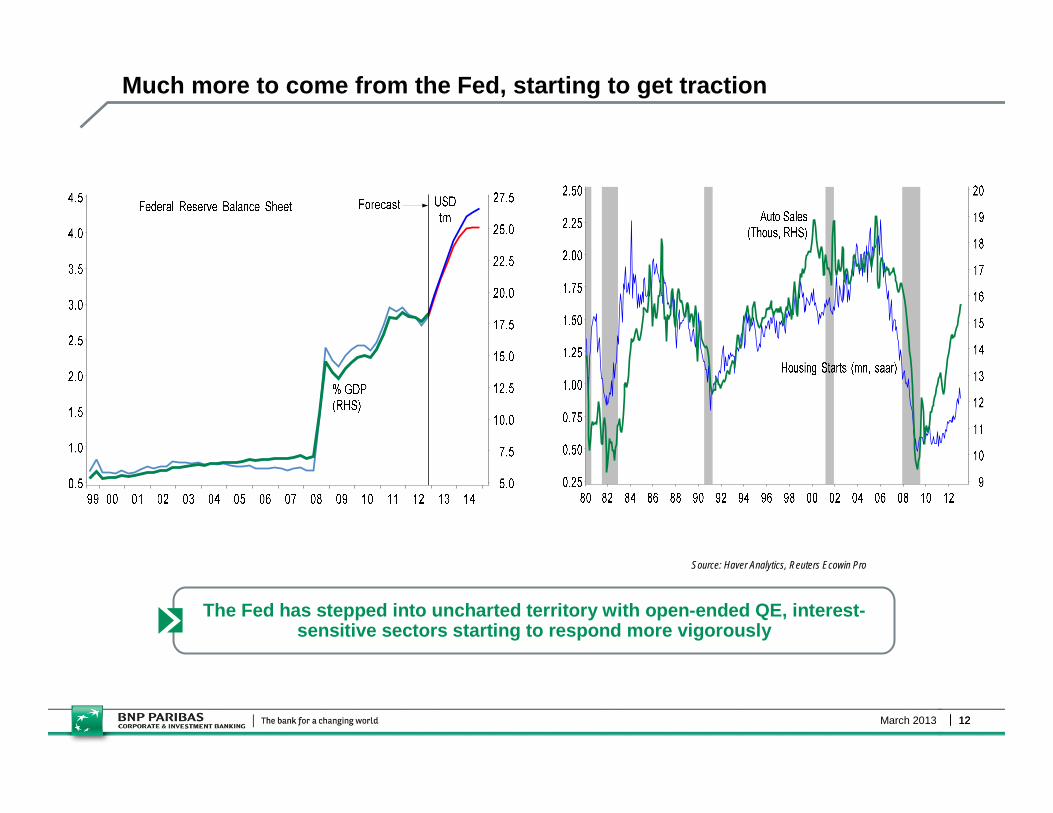

Much more to come from the Fed, starting to get traction

12

The Fed has stepped into uncharted territory with open-ended QE, interest-sensitive sectors starting to respond more vigorously

Source: Haver Analytics, Reuters Ecowin Pro

March 2013 1313

US public sector has been supporting private deleveraging

In contrast to the Eurozone approach underway, US private sector deleveraging was met with public leveraging

Source: Reuters Ecowin Pro

March 2013 14

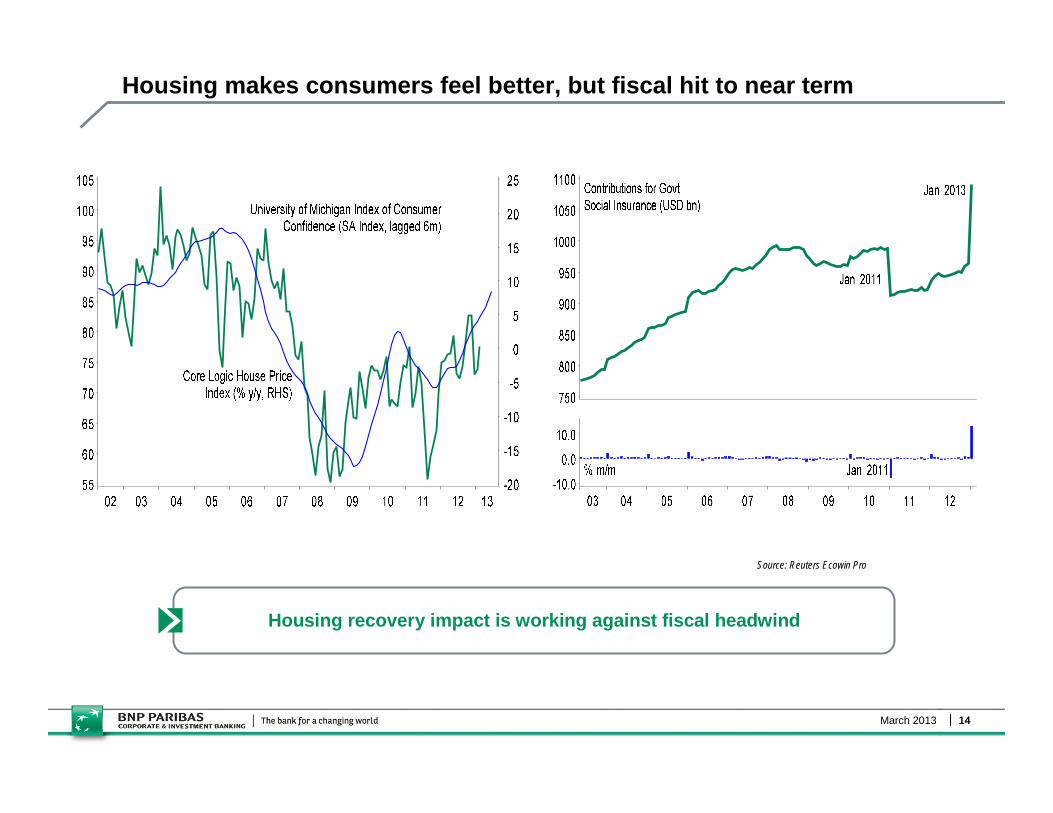

Housing makes consumers feel better, but fiscal hit to near term

14

Housing recovery impact is working against fiscal headwind

Source: Reuters Ecowin Pro

March 2013 15

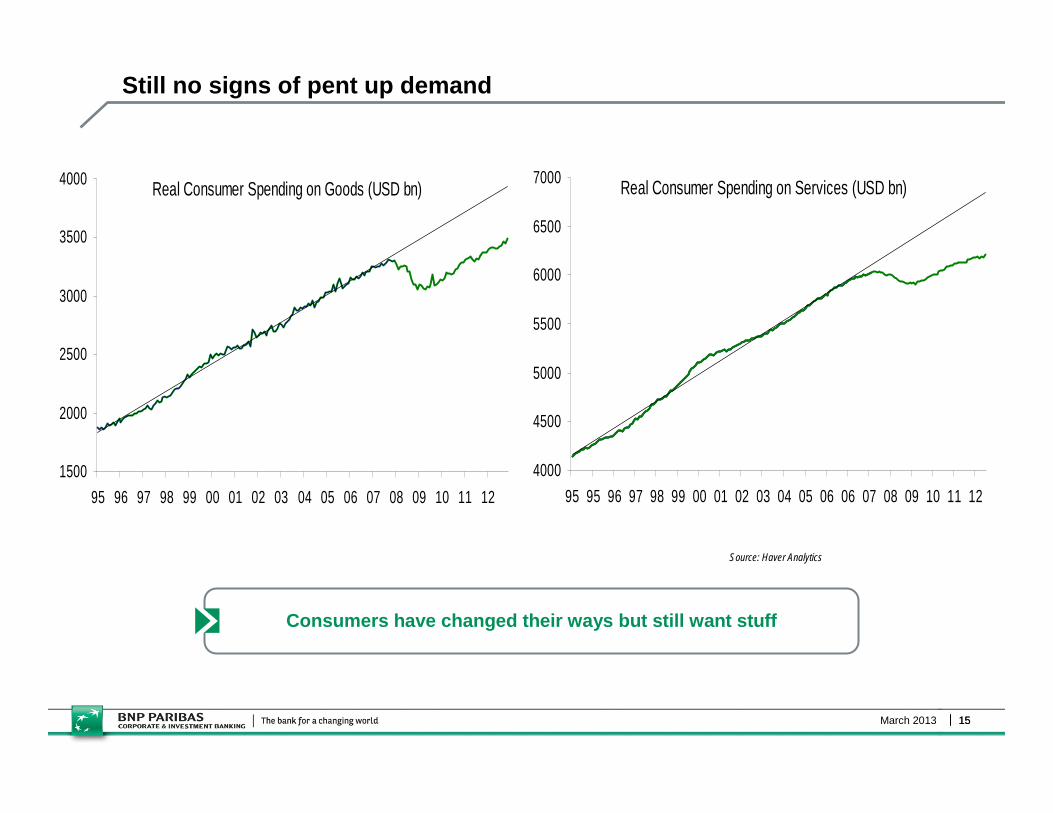

Still no signs of pent up demand

15

Real Consumer Spending on Services (USD bn)

4000

4500

5000

5500

6000

6500

7000

95 95 96 97 98 99 00 01 02 03 04 05 06 06 07 08 09 10 11 12

Consumers have changed their ways but still want stuff

Source: Haver Analytics

Real Consumer Spending on Goods (USD bn)

1500

2000

2500

3000

3500

4000

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

March 2013 16

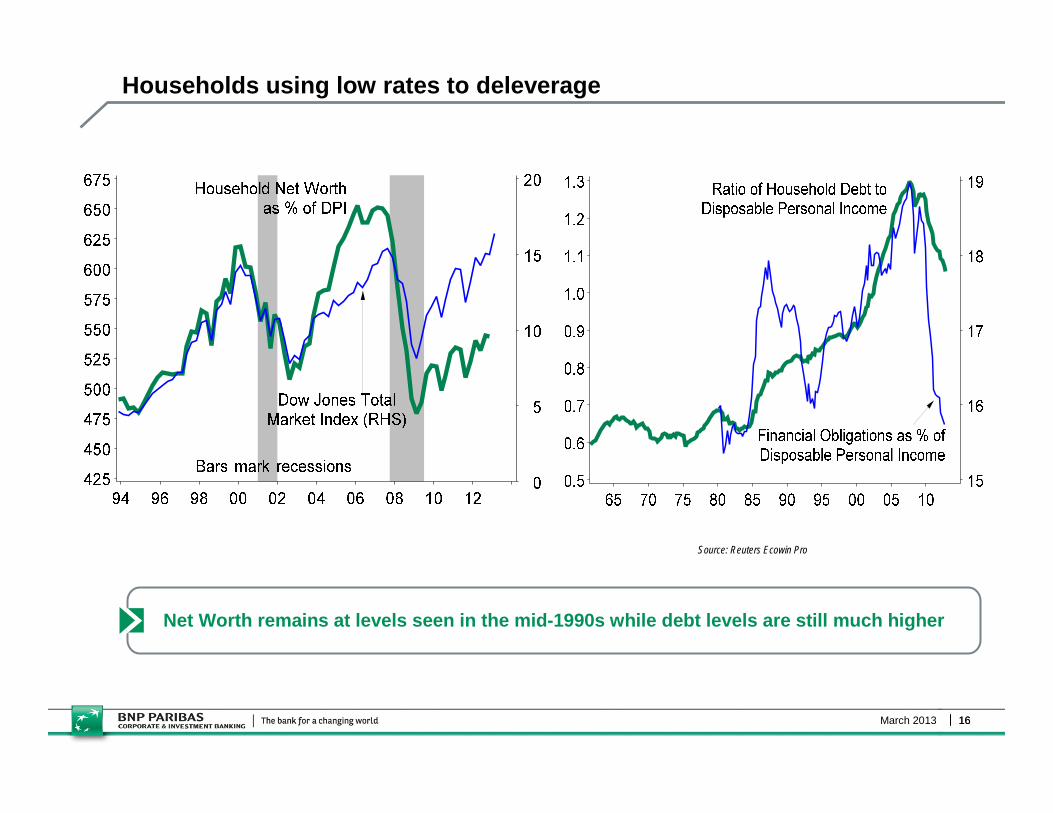

Households using low rates to deleverage

16

Net Worth remains at levels seen in the mid-1990s while debt levels are still much higher

Source: Reuters Ecowin Pro

March 2013 17

Monetary policy not reaching housing in the usual way

17

Despite record low rates, housing demand continues to be weak

Source: Reuters Ecowin Pro

March 2013 18

People increasingly want to rent not own

18

People want to preserve liquidity, mobility and new households are choosing to rent

Source: Haver Analytics

March 2013 19

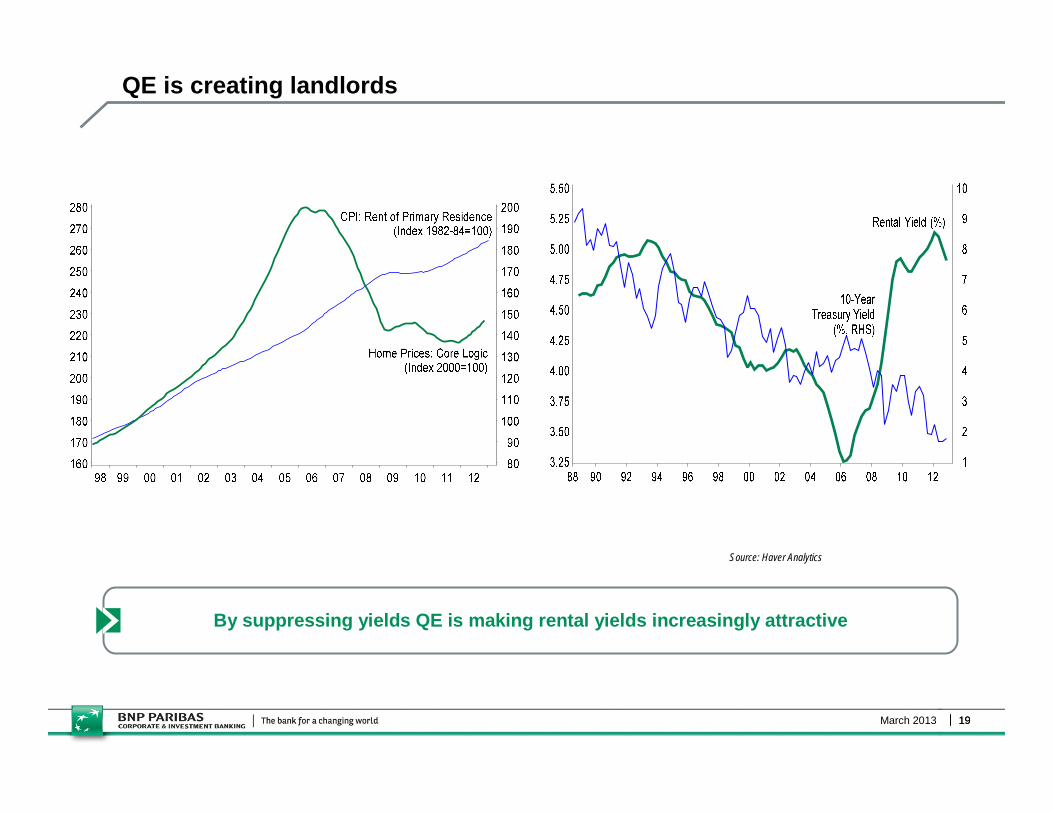

QE is creating landlords

19

By suppressing yields QE is making rental yields increasingly attractive

Source: Haver Analytics

March 2013 20

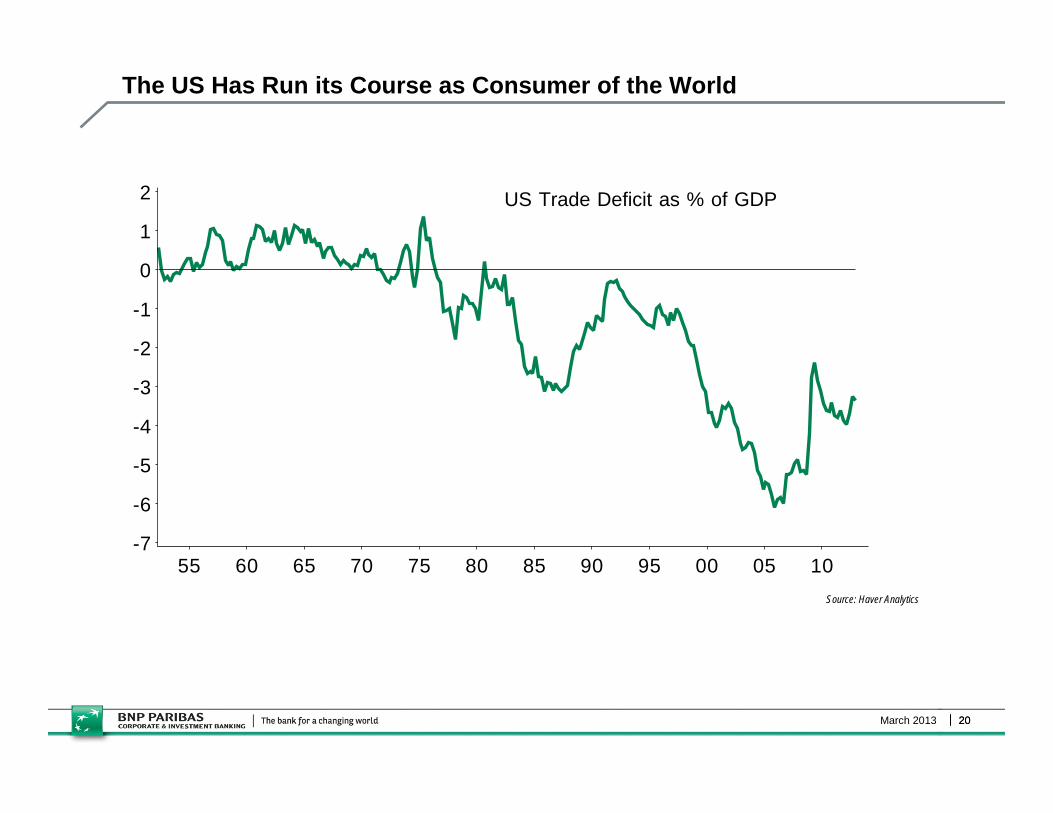

The US Has Run its Course as Consumer of the World

55 60 65 70 75 80 85 90 95 00 05 10-7

-6

-5

-4

-3

-2

-1

0

1

2 US Trade Deficit as % of GDP

20

Source: Haver Analytics

March 2013 21

The degree of corporate caution is at historic levels…

21

Businesses are not playing their traditional role as borrowers. The government is now the main borrower.

Source: Haver Analytics

-6

-4

-2

0

2

4

6

8

1960 1967 1974 1981 1988 1995 2002 2009

Domestic Business

Households

Bars mark recession

Net Saving (% of GDP)

Net lending or borrowing as % of GDP

March 2013 22

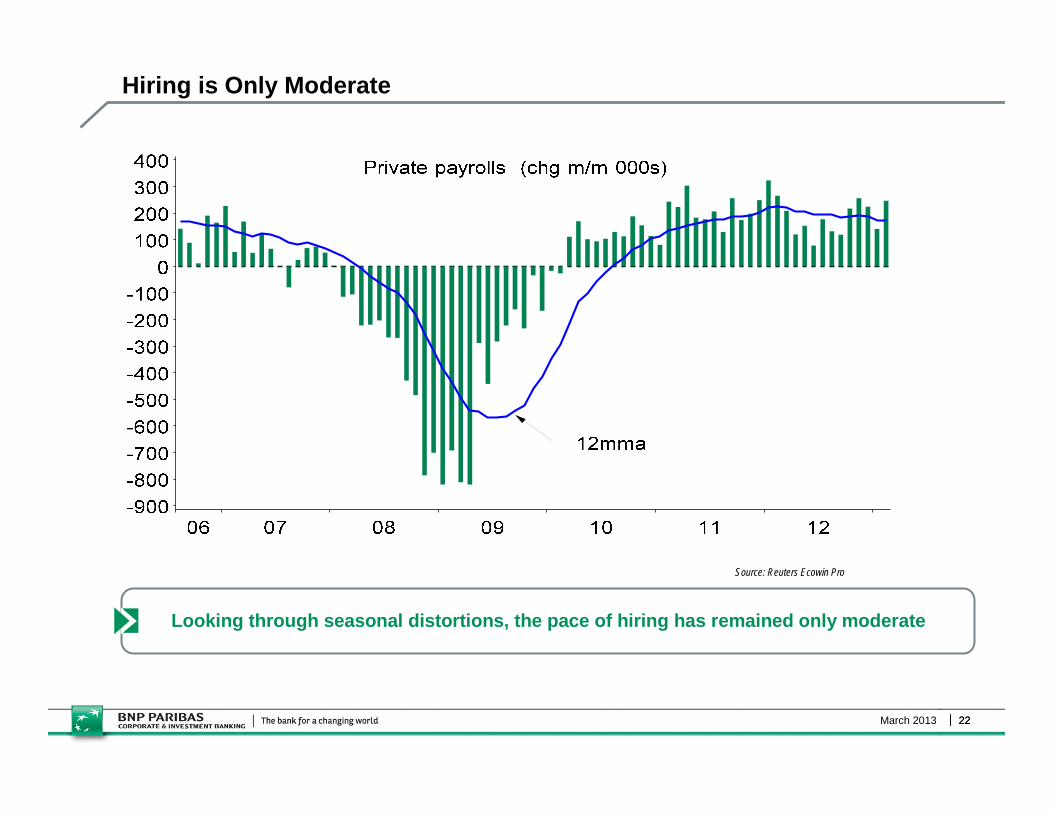

Hiring is Only Moderate

22

Looking through seasonal distortions, the pace of hiring has remained only moderate

Source: Reuters Ecowin Pro

March 2013 23

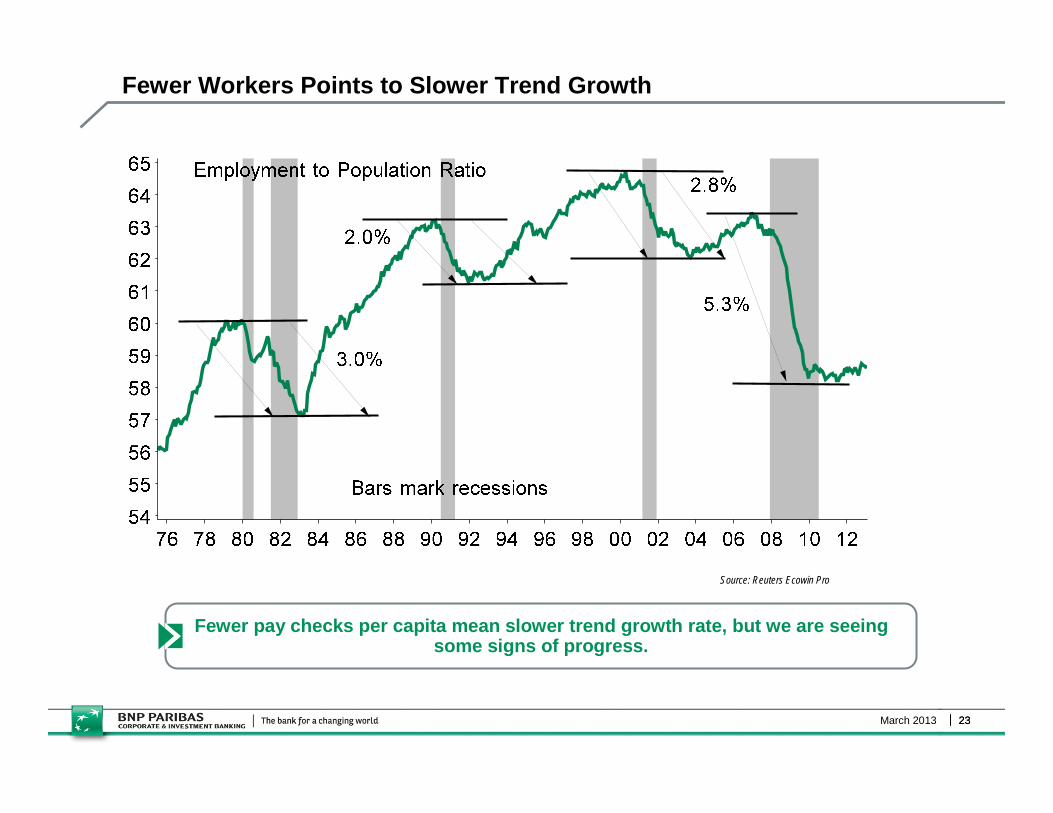

Fewer Workers Points to Slower Trend Growth

23

Fewer pay checks per capita mean slower trend growth rate, but we are seeing some signs of progress.

Source: Reuters Ecowin Pro

March 2013 24

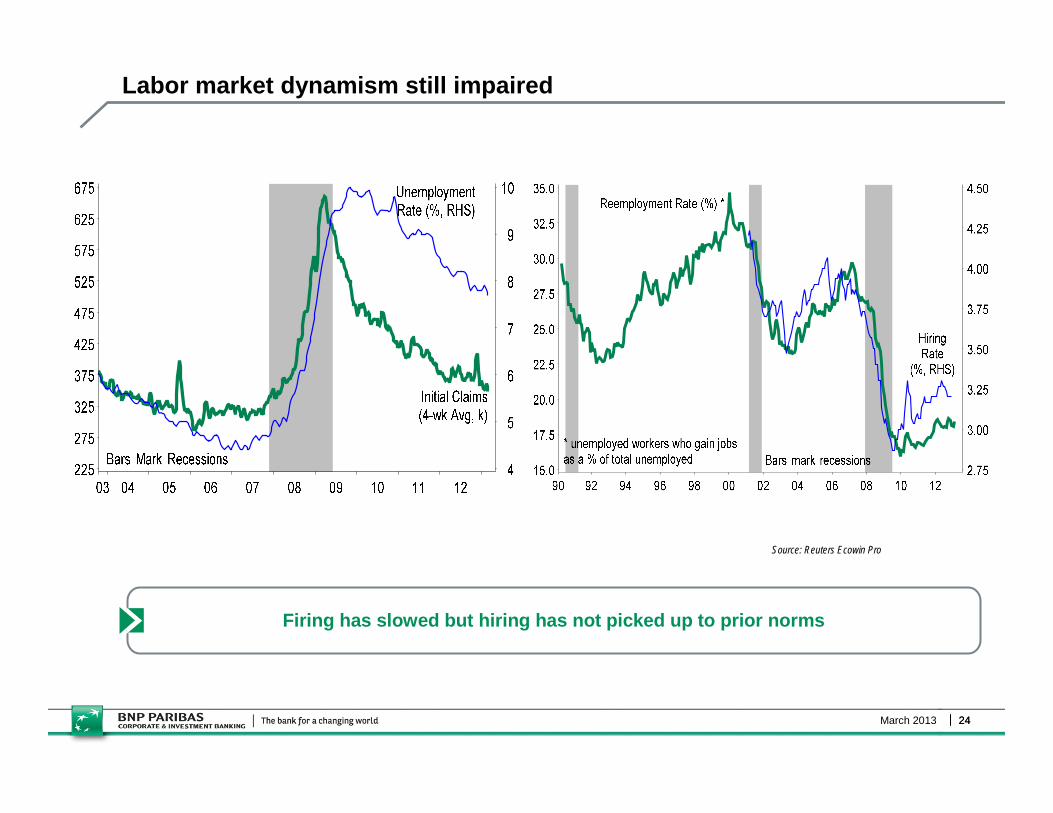

Labor market dynamism still impaired

24

Firing has slowed but hiring has not picked up to prior norms

Source: Reuters Ecowin Pro

March 2013 25

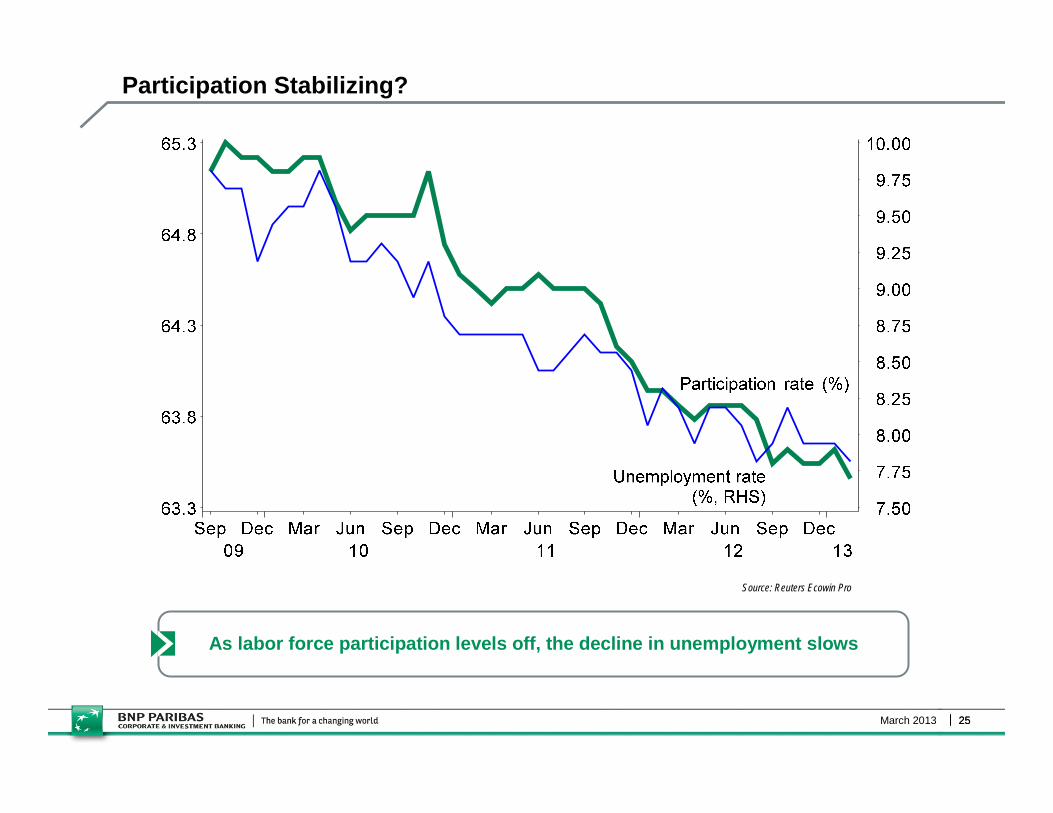

Participation Stabilizing?

25

As labor force participation levels off, the decline in unemployment slows

Source: Reuters Ecowin Pro

March 2013 26

How Much Slack is There?

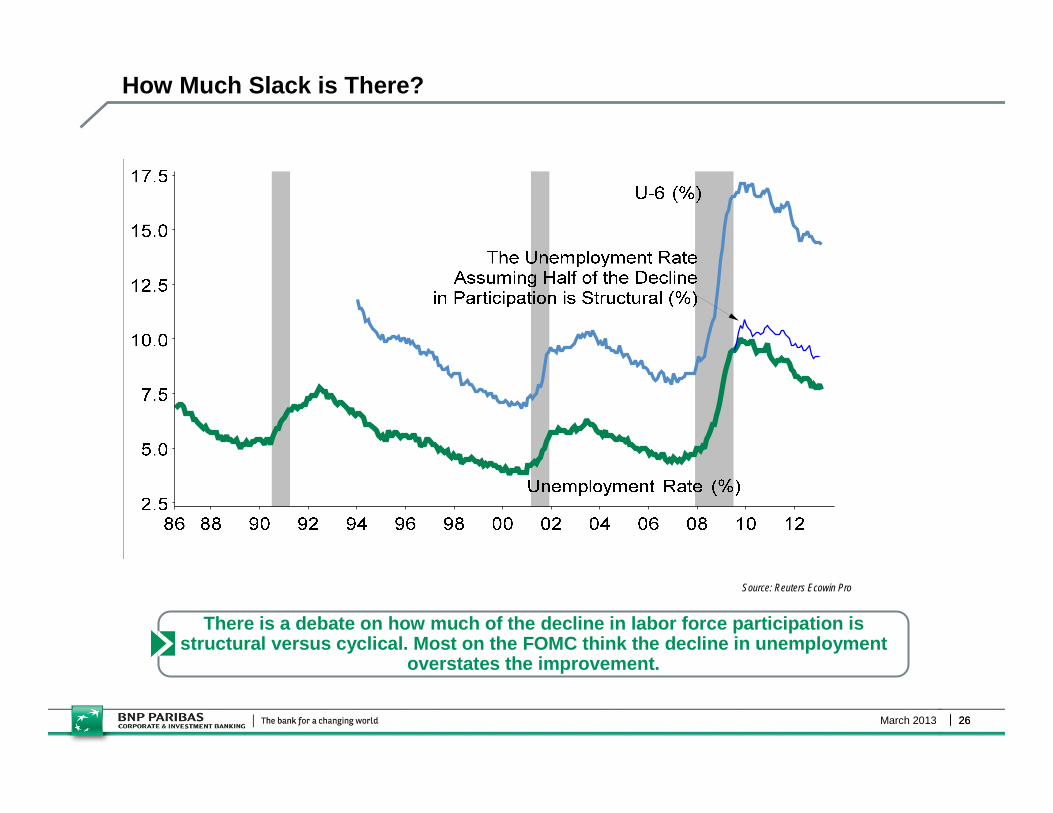

26

There is a debate on how much of the decline in labor force participation is structural versus cyclical. Most on the FOMC think the decline in unemployment

overstates the improvement.

Source: Reuters Ecowin Pro

March 2013 27

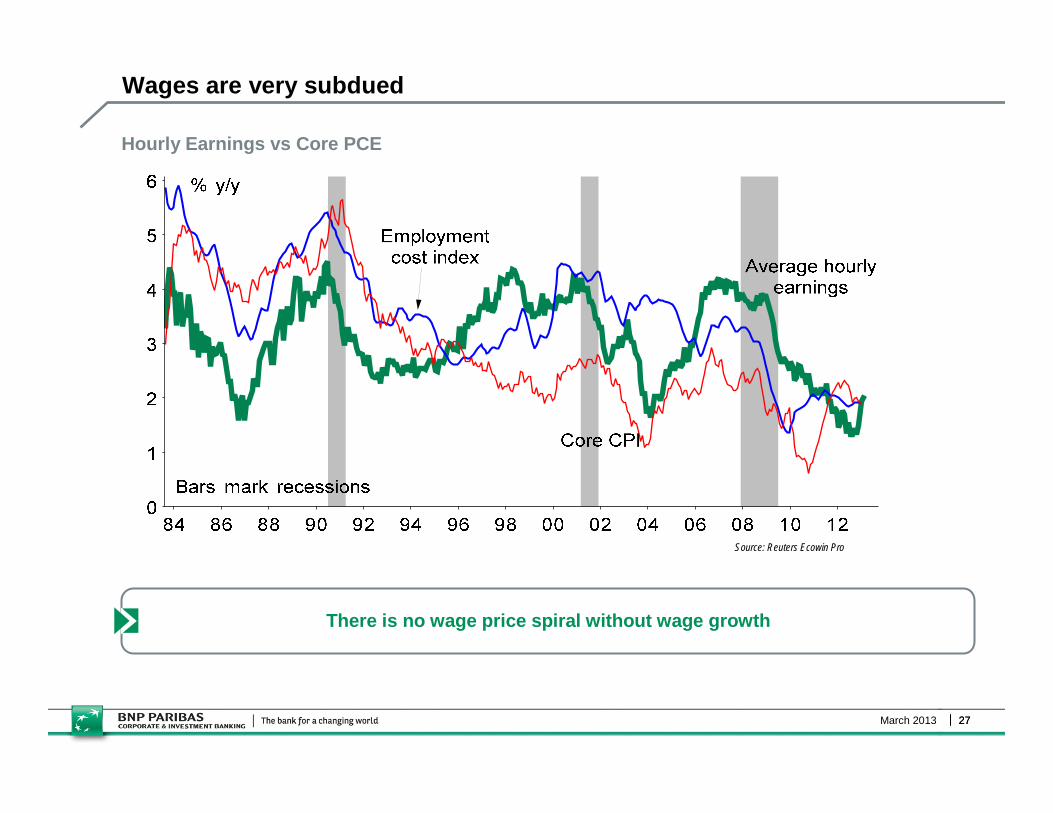

Wages are very subdued

27

There is no wage price spiral without wage growth

Hourly Earnings vs Core PCE

Source: Reuters Ecowin Pro

March 2013 28

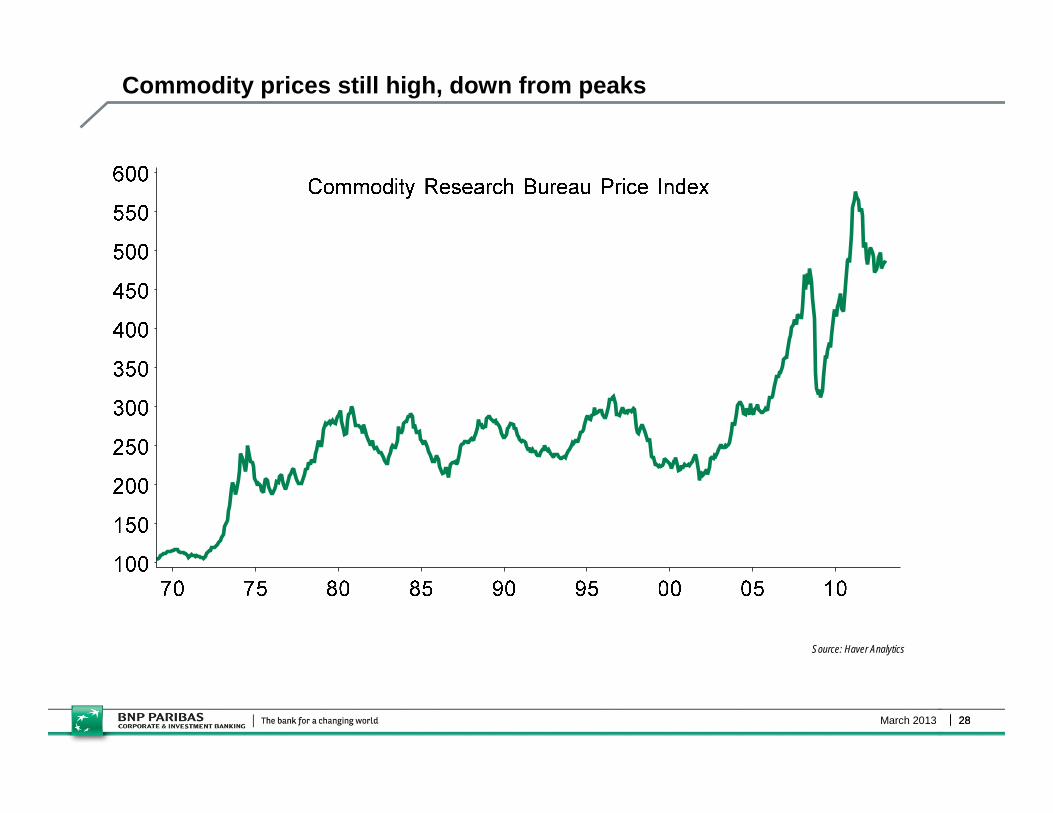

Commodity prices still high, down from peaks

28

Source: Haver Analytics

March 2013 29

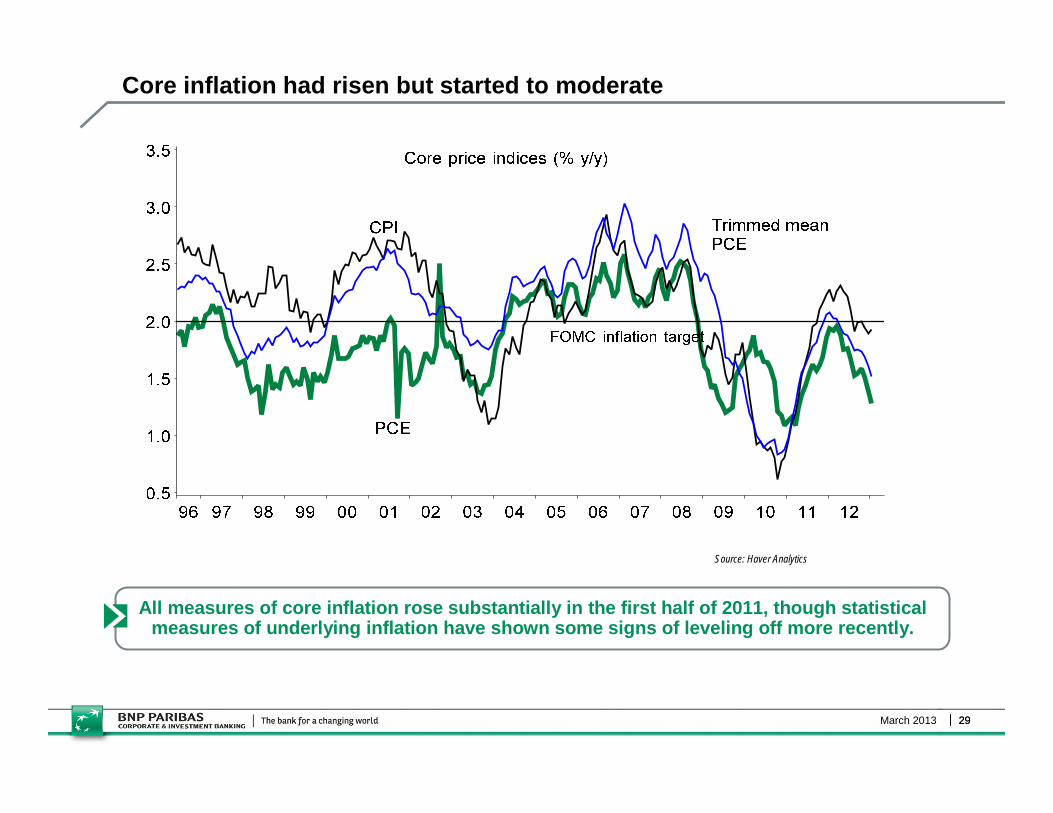

Core inflation had risen but started to moderate

29

All measures of core inflation rose substantially in the first half of 2011, though statistical measures of underlying inflation have shown some signs of leveling off more recently.

Source: Haver Analytics

March 2013 30

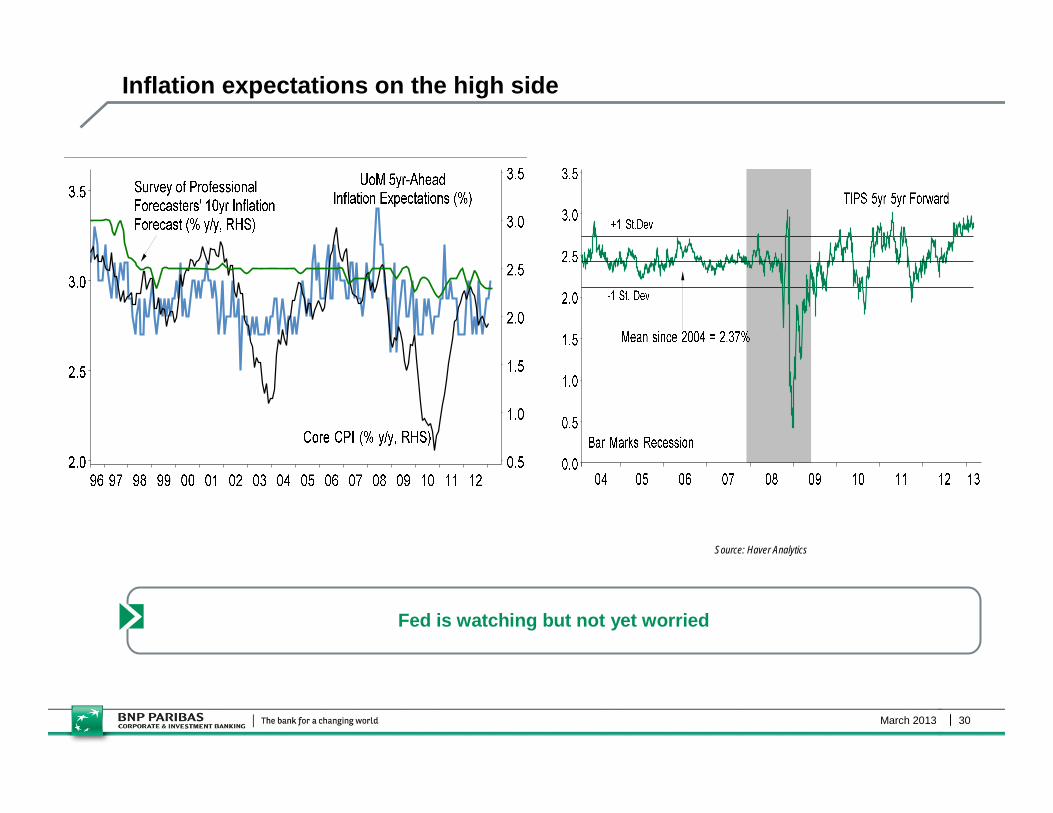

Inflation expectations on the high side

Fed is watching but not yet worried

Source: Haver Analytics

March 2013 31

Disclaimer

31

Please see important disclosures in the text of this report.The information and opinions contained in this report have been obtained from, or are based on, public sources believed to be reliable, but no representation or warranty, express or implied, is made that such information is accurate, complete or up to date and it should not be relied upon as such. This report does not constitute an offer or solicitation to buy or sell any securities or other investment. Information and opinions contained in the report are published for the assistance of recipients, but are not to be relied upon as authoritative or taken in substitution for the exercise of judgement by any recipient, are subject to change without notice and not intended to provide the sole basis of any evaluation of the instruments discussed herein. Any reference to past performance should not be taken as an indication of future performance. To the fullest extent permitted by law, no BNP Paribas group company accepts any liability whatsoever (including in negligence) for any direct or consequential loss arising from any use of or reliance on material contained in this report. All estimates and opinions included in this report are made as of the date of this report. Unless otherwise indicated in this report there is no intention to update this report. BNP Paribas SA and its affiliates (collectively “BNP Paribas”) may make a market in, or may, as principal or agent, buy or sell securities of any issuer or person mentioned in this report or derivatives thereon. BNP Paribas may have a financial interest in any issuer or person mentioned in this report, including a long or short position in their securities and/or options, futures or other derivative instruments based thereon, or vice versa. BNP Paribas, including its officers and employees may serve or have served as an officer, director or in an advisory capacity for any person mentioned in this report. BNP Paribas may, from time to time, solicit, perform or have performed investment banking, underwriting or other services (including acting as adviser, manager, underwriter or lender) within the last 12 months for any person referred to in this report. BNP Paribas may be a party to an agreement with any person relating to the production of this report. BNP Paribas, may to the extent permitted by law, have acted upon or used the information contained herein, or the research or analysis on which it was based, before its publication. BNP Paribas may receive or intend to seek compensation for investment banking services in the next three months from or in relation to any person mentioned in this report. Any person mentioned in this report may have been provided with sections of this report prior to its publication in order to verify its factual accuracy. BNP Paribas is incorporated in France with limited liability. Registered Office 16 Boulevard des Italiens, 75009 Paris. This report was produced by a BNP Paribas group company. This report is for the use of intended recipients and may not be reproduced (in whole or in part) or delivered or transmitted to any other person without the prior written consent of BNP Paribas. By accepting this document you agree to be bound by the foregoing limitations. Certain countries within the European Economic Area: This report is solely prepared for professional clients. It is not intended for retail clients and should not be passed on to any such persons.

This report has been approved for publication in the United Kingdom by BNP Paribas London Branch. BNP Paribas London Branch is authorised and supervised by the Autorité de Contrôle Prudentiel and authorisedand subject to limited regulation by the Financial Services Authority. Details of the extent of our authorisation and regulation by the Financial Services Authority are available from us on request.This report has been approved for publication in France by BNP Paribas, a credit institution licensed as an investment services provider by the Autorité de Contrôle Prudentiel whose head office is 16, Boulevard des Italiens 75009 Paris, France. This report is being distributed in Germany either by BNP Paribas London Branch or by BNP Paribas Niederlassung Frankfurt am Main, regulated by the Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin).United States: This report is being distributed to US persons by BNP Paribas Securities Corp., or by a subsidiary or affiliate of BNP Paribas that is not registered as a US broker-dealer to US major institutional investors only. BNP Paribas Securities Corp., a subsidiary of BNP Paribas, is a broker-dealer registered with the U.S. Securities and Exchange Commission and a member of the Financial Industry Regulatory Authority and other principal exchanges. For the purposes of, and to the extent subject to, §§ 1.71 and 23.605 of the U.S. Commodity Exchange Act, this report is a general solicitation of derivatives business. BNP Paribas Securities Corp. accepts responsibility for the content of a report prepared by another non-U.S. affiliate only when distributed to U.S. persons by BNP Paribas Securities Corp. Japan: This report is being distributed to Japanese based firms by BNP Paribas Securities (Japan) Limited or by a subsidiary or affiliate of BNP Paribas not registered as a financial instruments firm in Japan, to certain financial institutions defined by article 17-3, item 1 of the Financial Instruments and Exchange Law Enforcement Order. BNP Paribas Securities (Japan) Limited is a financial instruments firm registered according to the Financial Instruments and Exchange Law of Japan and a member of the Japan Securities Dealers Association and the Financial Futures Association of Japan. BNP Paribas Securities (Japan) Limited accepts responsibility for the content of a report prepared by another non-Japan affiliate only when distributed to Japanese based firms by BNP Paribas Securities (Japan) Limited. Some of the foreign securities stated on this report are not disclosed according to the Financial Instruments and Exchange Law of Japan.Hong Kong: This report is being distributed in Hong Kong by BNP Paribas Hong Kong Branch, a branch of BNP Paribas whose head office is in Paris, France. BNP Paribas Hong Kong Branch is regulated as a Registered Institution by Hong Kong Monetary Authority for the conduct of Advising on Securities [Regulated Activity Type 4] under the Securities and Futures Ordinance.Some or all the information reported in this document may already have been published on https://globalmarkets.bnpparibas.com© BNP Paribas (2013). All rights reserved.

IMPORTANT DISCLOSURES:

![Global and US Outlook MABE Outlook 2011[1]](https://static.documents.pub/doc/80x56/577d34871a28ab3a6b8e3de1/global-and-us-outlook-mabe-outlook-20111.jpg)