MARCO Research and Innovation Action (RIA) This project has received funding from the European Union's Horizon 2020 research and innovation programme under grant agreement No 730272. Start date : 2016-11-01 Duration : 24 Months Interim definition, taxonomy and report Authors : Mr. Steve HOWARD (KMatrix), Sarah Howard (kMatrix) MARCO - D2.2 - Issued on 2018-08-10 14:34:46 by KMatrix

Transcript

MARCOResearch and Innovation Action (RIA)

This project has received funding from the EuropeanUnion's Horizon 2020 research and innovation programme

under grant agreement No 730272.

Start date : 2016-11-01 Duration : 24 Months

Interim definition, taxonomy and report

Authors : Mr. Steve HOWARD (KMatrix), Sarah Howard (kMatrix)

MARCO - D2.2 - Issued on 2018-08-10 14:34:46 by KMatrix

MARCO - D2.2 - Issued on 2018-08-10 14:34:46 by KMatrix

MARCO - Contract Number: 730272MArket Research for a Climate Services Observatory

Document title Interim definition, taxonomy and report

Author(s) Mr. Steve HOWARD, Sarah Howard (kMatrix)

Number of pages 402

Document type Deliverable

Work Package WP2

Document number D2.2

Issued by KMatrix

Date of completion 2018-08-10 14:34:46

Dissemination level Public

Summary

D2.2 Interim definition, taxonomy and report. It includes 3 new industries and the "Mixed" platform. The taxonomy has beenmapped to NACE Codes allowing reporting through NACE Codes alongside industry reporting. Import and Export data hasbeen included.

Approval

Date By

2018-08-13 11:04:31 Dr. Joerg CORTEKAR (HGF/HZG)

2018-08-20 09:10:46 Dr. Gabor SZENDRO (LGI)

MARCO - D2.2 - Issued on 2018-08-10 14:34:46 by KMatrix

Interim Definition, Taxonomy and Report

This project has received funding from the European Union’s Horizon 2020 research and innovation programme under grant agreement No 730272. The content in this document reflects only the views of

the authors. The European Commission is not responsible for any use that may be made of the information it contains.

Introductory Notes to this Report This report is submitted as a deliverable for the MARCO project - to provide an update of the 2015/16 data submitted in D2.1, to focus on the Climate Services market, but with reference to Weather Services and to incorporated changes to the taxonomy and updated metrics determined through the project. As in the previous 2015/16 market report (D2.1), the data in this report is based on transactional information and only commercial services. This report provides an updated Baseline for the Climate Services market, in line with the new definitions which have been determined during the MARCO project. The CS market has been re-defined during the project in collaboration with MARCO partners. As outlined in D4.3, we have added a further 3 end-user industry sectors (Processing Industries, Civil Engineering and “Not Elsewhere Classified”), 380 applications and a “Mixed Services” data platform. In line with D4.5, we have mapped the data to NACE codes, which allows for reporting through both the taxonomy Industries and NACE codes. This is important as it enables full flexibility in the data, being accessible to governments and other users who work with NACE codes, but also to individual companies who categorise themselves differently. Ultimately the goal would be to map to a lower level of NACE code, which should be achievable as the market matures and data is more readily available at more in-depth NACE code level. At present we have mapped to 17 top line NACE codes. The new taxonomy reflects the new research into the quantifiable market for Climate Services and has been retro-fit to previous years. This new format will be used to provide an updated report for the 2017/18 financial year, to be delivered as D2.3.

Notes related to kMatrix data:

This report is a Market Assessment of the Weather & Climate Services market and the Climate Services market. It is a market data report and contains no non-market mapping or documentation. kMatrix Data Services Ltd is a private commercial company from the U.K. who specialise in providing market data (Sales figures, employment, companies, growth and other metrics) to National and Regional Governments, major research institutions, major corporates, investors and others worldwide. All sales figures relate to the private sector and not the public sector. All figures are for the Total Market and not a sample of the market. All figures are produced by the kMatrix proprietary process, which is unique in its field. The process itself will not the published, but ancillary methodology is available in the D2.1 report in section 2 and appendix J. In all kMatrix reports, “Demand and Supply” refers to commissioned projects and sales where there is a monetary transaction. Disclaimer: The content in this report reflects only the views of the authors. The European Commission is not responsible for any use that may be made of the information it contains.

Interim Definition, Taxonomy and Report

April 2018 Page 2 of 402

Industry Glossary

This Glossary relates to the 27 economic/industrial sectors that have been identified as users of Weather and Climate Services. It describes briefly what aspects of each sector have been included in the research. Agriculture

Provision of Weather and Climate Services to the farming (both

arable and livestock) and other agriculture sector activities.

Biotech

Provision of Weather and Climate Services to the manufacturing and research functions of the bio-tech sector

Built Environment

Provision of Weather and Climate Services to the construction sector, includes the civil engineering (small-scale) and engineering & project management sectors.

Business Services

Provision of Weather and Climate Services to the general business services sector i.e. advertising, marketing, consultancy etc.

Communications

Provision of Weather and Climate Services to the communications sector which includes both the equipment and service provision for all electronic communications.

Defence

Provision of Weather and Climate Services to the defence sector which includes army, air force, navy and central command and control. In addition, this covers border protection and other defence- related activities.

Education & Training

Provision of Weather and Climate Services to the education and training sector which includes schools, universities and other learning environments, as well as commercial, educational and training services to the public and private sectors.

Exploration

Refers to the provision of Weather and Climate Services to Oil & Gas exploration (not the utility for supply) and to Mining and Quarrying.

Food & Drink

Provision of Weather and Climate Services to the food and drink sector, which includes all elements from post- agriculture to retail sales

Forestry & Timber

Provision of Weather and Climate Services to the forestry and timber sector which includes timber processing.

Health Care

Provision of Weather and Climate Services to the healthcare and hospitals sector, which includes both public and the private healthcare delivery.

Interim Definition, Taxonomy and Report

April 2018 Page 3 of 402

Hospitality

Provision of Weather and Climate Services to the hospitality market which includes hotels and restaurants

Legal & Financial

Provision of Weather and Climate Services to the following sub

sectors: general business and private insurance sector; the re-

insurance sector; the financial investments sector; the legal sector

and the banking sector.

Logistics

Provision of Weather and Climate Services to the Logistics sector defined as: Air Travel - Air Travel industry which includes airport management and operations, people and goods but not storage as this is covered within “large vehicles & Storage.” Land Travel - Land Travel industry which includes highway and roadway management and operations, people and goods but not storage as this is covered within “large vehicles & Storage.” Sea Travel - Sea Travel industry which includes port management and operations, people and goods but not storage as this is covered within “large vehicles & Storage”.

Manufacturing

Provision of Weather and Climate Services to the Manufacturing sector, excluding food and drink, pharmaceuticals, bio-tech, chemicals processing and project orientated engineering- all of which are included separately.

News Publishing & Journalism

Provision of Weather and Climate Services to the news,

publishing and journalism sector.

Operational Services

Provision of Weather and Climate- related Services to the operational services sector which, in turn, provides services to industry, airports and call centres.

Pharmaceuticals

Provision of Weather and Climate Services to the research and manufacturing functions of the pharmaceuticals sector.

Public & Charitable Bodies

Public Sector

Provision of Weather and Climate Services to the public sector

which includes, central, regional, and local government and public

services.

Charitable bodies

Provision of Weather and Climate Services to the charitable bodies sector, including non- government organisations (NGOs).

Renewable Energy

Provision of Weather and Climate Services to the renewable energies market, which includes photovoltaic, geothermal and wind.

Interim Definition, Taxonomy and Report

April 2018 Page 4 of 402

Research & Development

Provision of Weather and Climate Services to the research and development sector- i.e. research into the effects of climate change on both food and non- food crops as growing conditions change.

Retailing & Wholesale

Provision of Weather and Climate Services to the retailing and wholesale sector

Tourism & Leisure

Provision of Weather and Climate Services to the tourism and leisure sector, but excludes hospitality.

Utilities Processing Industry Not Elsewhere Classified Civil Engineering Sector Not Elsewhere Classified “Not Elsewhere Classified”

Provision of Weather and Climate Services to the utilities sector,

which includes nuclear and non- nuclear power generation and

distribution, distribution of natural gas and the distribution and

recycling of water.

Provision of Weather and Climate Services to the processing

industry, defined as industrial processing of substances and

materials both solid and liquid. These products range from paints

through to road surfaces.

Provision of Weather and Climate Services to large civil

engineering projects including the assembly and construction of

bridges, roads and other major, load carrying structures.

Provision of Weather and Climate Services to any industries not

elsewhere classified.

Interim Definition, Taxonomy and Report

April 2018 Page 5 of 402

Markets Glossary The 27 economic/industry sectors identified above are divided into 138 distinctive markets. A full list of Industries and Markets are found in Appendix A. These markets are based upon the limitations and differentiations in the source materials available (i.e. we report what we find rather than what we would like to find) and, therefore, may not always correspond to how an industry would typically divide or define its activities. Most of the titles describing these markets are self-evident or self-explanatory. But some are not and so they are included below. Where an industry is defined as "Manufacturing" markets are denoted by different manufacturing processes that may have different Climate Services needs i.e. Aerospace is represented as Aerospace Batch Manufacture, Aerospace Manufacturing Assembly and Aerospace Project Orientated Production. These processes are defined below. Batch Production

Process that, for example, produces vehicle trailers in batches of twenty units to order rather than in a continuous production.

In-Line Process Manufacture

Continuous inline process manufacture, for example, continuous chemicals processing of orientated polymers for the packaging sector.

Manufacturing Assembly

Manufacturing assembly, for example, the assembly of white goods.

Project Orientated Production

Project orientated production, typically of much large products or infrastructure i.e. shipbuilding.

Other markets that may need further definition or clarification are shown below. High End Engineering

High end engineering sector includes, electronics, precision engineering and high value electrical engineering installation and maintenance.

High-Tech based Services (Emergent)

These are predominantly new high tech based services across all industrial sectors. These are new emergent technologies such as artificial photosynthesis, genetic engineering and neuro-informatics.

Industrial Services and Servicing

Industrial services and servicing sector includes large engineering maintenance providers, large industrial catering providers and large supply chain management houses.

Local Government

Where national, regional and local government combine to address issues like long term climate change, through the provision of information to local businesses and residents and by the planning and provision of services like waste management, flood abatement and town and country planning.

Interim Definition, Taxonomy and Report

April 2018 Page 6 of 402

Other Defence Services Providers

Provision of Weather and Climate Services to the other defence services providers not included in the main defence category i.e. providers of non-battle theatre products and services such as home based construction services.

Other Financial Services

Provision of Weather and Climate Services to other financial services not elsewhere covered i.e. Pension funds and private equity funds.

Other Professional Business Services

Provision of Weather and Climate Services to the other professional business services not elsewhere covered for i.e. personnel recruitment agencies.

Other Publications

Provision of Weather and Climate Services to the news, publishing and journalism functions not elsewhere covered i.e. educational publications for academia.

Public Services

Provision of Weather and Climate Services to publicly funded services like Police, Fire, Ambulance and coastal protection.

Interim Definition, Taxonomy and Report

April 2018 Page 7 of 402

Table of Contents Section

Contents

Page

1

Introduction 10-16

2

Methodology and Measures 17-21

3

Uses for Weather and Climate Services 21-23

4

Global Weather and Climate Services 24-56

5

International Weather and Climate Services 57-73

6

Discussion 74-76

Appendix A

Appendix B

Appendix C

Appendix D

Appendix E

Appendix F

Appendix G

Appendix H

Appendix I

Appendix J

Appendix K

Appendix L

Industry Markets

NACE Code Markets

Selected Sources

Confidence Levels

Global Industry Analysis for Climate Services

Global Market Values by Industry and NACE Code

Global NACE Code Analysis for Climate Services

Industries and NACE Code by Platform & Services for

Climate Services

Global Country Analysis for Climate Services

EU Country Dashboards for Climate Services

EU Country Tables for Climate Services

Methodology for Import/Export Data

77-79

80-82

83-87

88-90

91-144

145-152

153-186

187-190

191-195

196-335

336-391

392-402

Interim Definition, Taxonomy and Report

April 2018 Page 8 of 402

List of Figures Page

Figure 1: Confidence Levels for Platform by Key Measure 20 Figure 2: Confidence Levels for Service by Key Measure 20 Figure 3: Confidence Levels for Industry by Key Measure 20 Figure 4: Frequency of Climate Service Uses 22 Figure 5: Weather & Climate Services €m 24 Figure 6: Weather Services €m 24 Figure 7: Climate Services €m 24 Figure 8: Value by Data Platform €m 25 Figure 9: Transaction Volume by Data Platform 26 Figure 10: Value by Service Type Climate and Weather Services €m 26 Figure 11: Value by Service Type CS and WS Transactions 27 Figure 12: Climate Services Historical Growth Trend for Service Types €m 27 Figure 13: Climate and Weather Services by Industry End-User €m 29 Figure 14: Climate and Weather Services by Industry End-User % 30 Figure 15: Industrial split by Climate and Weather Services 32 Figure 16: Historical Climate Services Sales by Industry €m 33 Figure 17: Top 10 Industries for CS split by Market €m 2016/17 34 Figure 18: Top 10 Industries for WS split by Market €m 2016/17 36 Figure 19: Climate and Weather Services by NACE Code End-User €m 39 Figure 20: Climate and Weather Services by NACE End-User % 40 Figure 21: NACE Code split by Climate and Weather Services 42 Figure 22: Historical Climate Services Sales by NACE Code €m 43 Figure 23: Top 10 NACE Codes for CS split by Market €m 2016/17 44 Figure 24: Top 10 NACE Codes for WS split by Market €m 2016/17 46 Figure 25: Top 10 Industries by Service Type for CS 2016/17 (%) 49 Figure 26: Top 10 Industries by Service Type for WS 2015/ 16 (%) 51 Figure 27: Top 10 NACE Codes by Service Type for CS 2016/17 (%) 53 Figure 28: Top 10 NACE Codes by Service Type for WS 2015/ 16 (%) 55 Figure 29: Forecast Global Annual Growth in W&CS (%) to 2024/25 56 Figure 30: Forecast Global Annual Growth in CS and WS (%) to 2024/25 56 Figure 31: Weather & Climate Services Sales by Global Region 2016/17 57 Figure 32: CS and WS Sales Compared by Global Region 2016/17 57 Figure 33: Top 15 Countries for Climate Services 2016/17 €m 58 Figure 34: Top 15 Countries for Weather Services 2016/17 €m 59 Figure 35: Top 15 Countries for CS Imports and Exports 2016/17 €m 60 Figure 36: Top 15 Countries for WS Imports and Exports 2016/17 €m 61 Figure 37: EU 28 Countries for Climate and Weather Services 2016/17 €m 62 Figure 38: EU 28 Countries for CS and WS 2016/17 Imports and Exports €m 62 Figure 39: EU 28 Countries for CS and WS by Platform 2016/17 €m 63 Figure 40: EU 28 Countries Import/Export Data for CS by Platform 2016/17 €m 63 Figure 41: EU 28 Countries Import/Export Data for WS by Platform 2016/17 €m 64 Figure 42: EU 28 Countries for CS and WS by Service 2016/17 €m 64 Figure 43: EU 28 Countries for CS and WS by Service 2016/17 Transactions 65 Figure 44: EU 28 Countries Import/Export Data for CS by Service 2016/17 €m 66 Figure 45: EU 28 Countries Import/Export Data for WS by Service 2016/17 €m 66 Figure 46: EU 28 Countries for CS and WS by Industry 2016/17 €m 67 Figure 47: EU 28 Countries Import/Export Data for CS by Industry 2016/17 €m 68 Figure 48: EU 28 Countries Import/Export Data for CS by Industry 2016/17 €m 69 Figure 49: EU 28 Countries for CS and WS by NACE Code 2016/17 €m 70 Figure 50: EU 28 Countries Import/Export Data for CS by NACE Code 2016/17 €m 71

Interim Definition, Taxonomy and Report

April 2018 Page 9 of 402

Figure 51: EU 28 Countries Import/Export Data for WS by NACE Code 2016/17 €m 72

List of Tables Page

Table 1: Markets with the Broadest Range of Climate Services Needs 23 Table 2: Top 20 Global Climate Services Markets 2016/17 €m 35 Table 3: Top 20 Global Weather Services Markets 2016/17 €m 37 Table 4: Top 20 Global Climate Services Markets 2016/17 €m 45 Table 5: Top 20 Global Weather Services Markets 2016/17 €m 47 Table 6: Industry by Service Type for Climate Services 2016/17 €m 48 Table 7: Industry by Service Type for Weather Services 2016/17 €m 50 Table 8: NACE Code by Service Type for Climate Services 2016/17 €m 52 Table 9: NACE Code by Service Type for Weather Services 2016/17 €m 54 Table 10: Summary Table 28 EU Countries 2016/17 73

Interim Definition, Taxonomy and Report

April 2018 Page 10 of 402

1.0 Introduction Deliverable 2.2 (revised annual baseline for Climate Services 2016/17) updates the previous report D2.1 relating to Climate AND Weather Services in 2015/16. D2.2 will include:

• Updated market values due to changes in taxonomy: new end-user sectors and market applications listed in D4.3

• Filtered results that exclude inappropriate applications like Cladding and Under- Pinning

• Adoption of NACE codes for reporting purposes • Data updated to 2016/17 (also shared with D4.5 on EU NUTS 2 Analysis) • New metrics that include national imports/exports.

Following on from a previous debate, we will also include references to Weather Services (WS) and calculate the total Weather and Climate Services (W&CS) market (showing CS as a % of the total). But the main focus will be on Climate Services (CS).

1.1 Research Objectives This report has been prepared for the MARCO project as an update to deliverable 2.1, which was itself an update of the original research in 2011 conducted on behalf of the UK Space Agency, the Met Office, the Natural Environment Research Council (NERC) and its industrial partners. This report updates the information from D2.1, with an additional 3 industries and 24 markets. Imports and Exports (values in €m) have been calculated for all industries and markets and are presented throughout the report. Data has been updated to 2016/17 figures, with growth figures for the new taxonomy being calculated retrospectively for previous years. It provides global information on the Weather and Climate Services, Weather Services and Climate Services markets for various measures. It also looks specifically at the 28 countries of the European Union (EU) within a global marketplace. The original research objectives have been maintained for this update/upgrade and were to:

• Measure the global Weather and Climate Services market in its entirety (not just for earth observation data from Space, although this is an important component)

• Identify how market needs are currently being met in terms of data platforms and services

• Identify which industries are driving the demand for Weather and Climate Services

This study measures the global commercial markets for data, information and software services that help to mitigate or manage risks arising from existing climate conditions or from possible climate change. These services range from proactive forecasting to preventive planning to disaster response activities and can be either short term (e.g. weather forecasting), long term (e.g. population displacement due to flooding or desertification) or both (e.g. planning for renewable energy infrastructure).

Interim Definition, Taxonomy and Report

April 2018 Page 11 of 402

This study distinguishes between commercial and non-commercial Weather and Climate Services. Governments invest significantly in the infrastructure and research necessary to provide Weather and Climate Services and in return receive data and services from a range of non-commercial bodies possessing in-house, value-adding expertise. Many of these services are then freely shared with other public and private sector organisations. But this public investment in infrastructure and research also supports a commercial aftermarket for Weather and Climate Services that extends the uses of, and adds value to, the freely available data and analysis. This is where new or bespoke needs arise, where external verification rather that internal opinion is required or where the internal expertise does not exist to process and apply the available data or analysis. There is an increasing pressure on public service providers to justify public investment. There is also increasing pressure to engage users and develop and deliver new and relevant services, which include external verification. This leads to a need for better understanding of the balance between private and publicly available services and the differentiated nature of that balance within Europe and beyond. So, while the original research was motivated by an interest in the exploration of commercial after-markets for data derived from earth observation satellites, the context for the research required a comprehensive analysis of all complementary and competing sources of data for Weather and Climate Services markets. This report starts by analyzing the Weather & Climate Services sector as defined by the MARCO project and then focuses upon a deeper analysis of Climate Services and an ongoing comparison with Weather Services, with the inclusion of Import and Export data.

1.2 Defining the Weather & Climate Services Sector The original research focused on Weather and Climate Services and while the debate has progressed and Climate Services is now a focus for European Research, the context of the research still remains largely unchanged. Weather Services are the better known of the two and the difference between them is still much debated. In its simplest form, the difference between the two relates to the duration of time the data and service relates to i.e. a short-term solution (e.g. do I irrigate my crops this week?) relies on weather forecasting while a solution set further into the future (e.g. what is the likelihood of persistent crop failure leading to food shortages?) relies on longer term climate data. In reality, Weather Services and Climate Services are two points on a single continuum and many organisations require both sets of information, although (as Section 4 demonstrates) different industries use both Weather Services and Climate Services in different proportions. At different points in Sections 4 and 5 of this report the terms Weather & Climate Services sector (the totality), Weather Services and Climate Services will be used. While Climate Services is the focus of interest for MARCO, comparison with Weather Services is critical to understanding the context within which needs are defined and purchases are undertaken.

Interim Definition, Taxonomy and Report

April 2018 Page 12 of 402

From the user’s perspective weather services and climate services are a single continuum of services, with both types of service being required by many (if not most) users. The decision-making perspective makes this situation even more obvious, where there is a need to deal with the existing adaptation deficit and current climate variability and change (including extremes) through to the implications of a changing climate. The user’s perspective of a single continuum of services also reflects the implications of mainstreaming adaptation. Weather services and Climate services are being separated because market evidence shows that weather services are often procured as a separate item, if not an initial item before the procurement of climate services. This is partly due to much procurement in this sector being driven by corporate governance in major corporates for example. From a market data point of view, the two services really are separate at this time. Climate Services is a less well-known term and needs more explanation. The term "Climate Services" was actively promoted by the World Meteorological Organisation (WMO) at the World Climate Conference in 2009 as part of a "Global Framework for Climate Services." Since then various attempts have been made to define the purpose (if not the content) of Climate Services. Definitions of purpose generally include reference to "providing information or tools" to "decision makers" to help "mitigate, adapt to or manage risks" arising from "existing climatic conditions or from possible climate change". Both meteorological and hydrological data and services are included within the definition of Climate Services. The various definitions include references to proactive forecasting, preventive planning and disaster response activities and these can include both short term (weather forecasting) and long term (population displacement due to desertification) problem solving. The World Meteorological Organisation1identifies some of the many reasons why Climate Services are important to both the public and private sectors. These include:

• Anticipating changes to water quality, availability and demand

• Responding to water-related risks from extreme events

• Planning for natural disasters that may lead to crop failure and food insecurity

• Managing population displacement (migration) due to extreme events or climate change

• Supply planning for energy demand (investments in generation/distribution systems)

• Forecasting seasonal conditions for the generation of renewable energies based upon wind, solar and wave power

• Anticipating the impact of weather conditions or climate change on high-dependency resorts for tourism, hospitality and some aspects of travel

• Urban planning - what to build, where, how and to what specification based upon changing conditions

• Planning where to site transport infrastructure and hubs

• Minimizing operational disruptions to air, land and sea travel. The original market research adopted the broadest definition of purpose for Weather and Climate Services (including all of the above solutions) and translated this into a wide range of related market activities that underpin and deliver upon that purpose. Hence the segmentation within this research report into Weather Services and Climate Services, data platforms, service types, industries and markets.

1 www.wmo.int

Interim Definition, Taxonomy and Report

April 2018 Page 13 of 402

The research started with a hypothetical model of the Weather & Climate Services sector and then searched for data to either support or amend this model. The result was a pragmatic statement on Weather and Climate Services i.e. it only includes an activity and data where there is enough useful evidence to support it. The segmentation and headings used for the various activities within Weather and Climate Services are mostly derived from the data sources themselves (i.e. the user-industries) and from a need to group the evidence in a meaningful and hierarchical format. This market segmentation does deliver a quantitative baseline for the Weather & Climate Services sector (as shown by Sections 4 and 5 of this report) but it does not reflect or give a flavour of the full scope of forecasting, planning, reporting etc. activities that are conducted increasingly across many industries under the broad "umbrella" of Weather and Climate Services. To reflect the broad "needs" that Weather and Climate Services meets, the research included a brief "audit" of industry activities that, unlike the main body of the research, is unquantified. These "uses" are described in more detail in Section 32 and remain relevant enough to not require immediate updating. Once the original research was underway, it became clear that Weather Services and Climate Services should in some way be separated out for analysis. Unfortunately, most of the purchasing data sources used to compile the research data was not always clear about whether they were seeking a Weather or Climate-related solution. Therefore, the research data was split according to:

• Whether the purchaser thought that the purchase was Weather or Climate-related (i.e. it has Weather or Climate in the title), or

• Without Weather or Climate in the title, could the purchase or intent be identified as a short-term solution to a weather sensitive issue or as a longer-term challenge.

So, the original split between Weather Services and Climate Services was a pragmatic amalgam of intent and timescale. Since 2011 the data sources to support this research have increased in both quality and quantity. There is still, however, clearly uncertainty in end-user markets about the differences between the two types of services. So, separating the two sets of services in data terms is still part-science/part-art.

1.3 Defining "Commercial" Weather and Climate Services In the original research, there was also a need to distinguish between commercial and non-commercial Weather and Climate Services. Governments invest significantly in the infrastructure and research necessary to provide short and long-term Weather and Climate Service data (from air, land, sea or space), tools and analysis and in return receive (and share) data and services free of charge. So, a large proportion of the Weather and Climate Services market includes free data, tools and analysis that are "internalized" by public and private sector customers for their own purposes. This report does not attempt to quantify these services, although the money invested in them is substantial3. But this investment in infrastructure and research also supports a commercial aftermarket for Weather and Climate Services that extends the uses of, and adds value to, the freely

2 A Eurisy publication "30 Regions, Cities and SMEs Share Good Practice" Oct 2011 includes local examples where earth

observation data in used to response to challenges in the Energy, Environmental, Agricultural and Forestry sectors. 3 More information about global initiatives to leverage current levels of public investment into more effective and widely

available Climate Services (for humanitarian and economic purposes) can find this at www.wmo.int and in the WMO

publication- "Global Framework for Climate Services" 2009.

Interim Definition, Taxonomy and Report

April 2018 Page 14 of 402

available data and analysis. This is where new or bespoke needs arise, where external verification rather that internal opinion is required or where the internal expertise does not exist to process and apply the available data or analysis. So, this research is NOT intended to be an assessment of public sector investments in Weather and Climate research, but an analysis of the traceable commercial "after-market" that follows on from these investments, the resulting research and subsequent national and international policy agendas. The research is based upon a complex methodology that uses multiple sources of data to derive statistically significant market numbers in terms of value (€m), volume (transactions) and market growth (%). This is described in more detail in Section 3. This methodology has been applied to many "difficult-to-measure" industry activities including other space-related opportunities for earth observation like Carbon Markets. Following the advice given at a UK Space Conference (2011) the focus is on uncovering "markets that do not have Space in the title." Since 2011 this research methodology has been applied to equally complex sectors and markets like climate change adaptation, the green economy, geo-services, cyber security and design.

1.4 Segmenting Commercial Weather and Climate Services It was recognized that many of the Weather and Climate Service solutions identified above often required multiple services, multiple data sources and may be conducted over several years by several suppliers. These services may be purchased as a single contract or as several services combined. The previous report (D2.1) reported on the individual data platforms, however through the MARCO project, another platform called “Mixed Services” has been added. The research segments the Weather and Climate Services Aftermarket in a variety of ways. The first is by data platform, where the options are now Airborne, Land, Marine, Space and Mixed Services: Air Services

Refers to earth observation via airborne systems - Fixed & Rotary winged manned and unmanned aircraft and air ships

Land Services

Refers to earth observation via land-based systems like land-based radar, weather stations, atmospheric sampling and arctic survey.

Marine Services

Refers to earth observation via Sea-based systems i.e. marine craft both surface and underwater, buoys and sea bed systems

Space Services Mixed Services

Refers to earth observation via Space craft-based systems - Including satellites and space stations. Refers to a mixture or combination of the other four platforms.

The second level of segmentation is by service type, of which there are eight that can be fully differentiated and quantified. These are:

Interim Definition, Taxonomy and Report

April 2018 Page 15 of 402

Advisory Services

Advisory services, risk assessment and decision support tools provided to public and private sector organisations relevant to global weather, climate and climate change. For example, risk assessment for the long-term location of nuclear power stations.

Data Management

Provision of calibrated data sets, data archiving, data certification and data sales for global weather, climate and climate change applications. For example, the provision of validated data sets to consultancies for further analysis.

Measurement

Instruments and technologies for measurement and calibration for global weather, climate and climate change applications. For example, the provision of assistance and advice in the assembly of sensing arrays for ground-based weather stations.

Modelling

Modelling of data, both certified and non-certified for global weather, climate and climate change. For example, the modelling of collated data from the arctic survey in order to predict the most likely rate of degradation of the polar ice cap.

Operation

Collection and provision of raw data for global weather, climate and climate change applications i.e. the provision of raw date to media weather centres.

Other Consulting

Consulting services for global weather, climate and climate change not elsewhere covered i.e. the provision of advice on corporate statements to share-holders on corporate policy towards climate change. "Other Consulting" often includes more general consulting services about corporate responses to the challenges arising from specific weather and climate data (whether purchased separately or processed internally) and also more specialist services (incorporation of new data sets).

Processing & Re-Analysis

Provision of data analysis and retrieval services including data mining tools, for global weather, climate and climate change i.e. the provision of essential climate variable models to academia.

Publication

General publication of analysis findings for global weather, climate and climate change i.e. the assembly of publications on climate forecasts based on data and analysis for both private and public sector organisations.

The research measured each of these services individually, although it is well known that the different services complement one another and are often purchased together. Each service type was then segmented into Industries that reflected WHERE in the global economy they were being purchased. An assessment of the data sources and collaboration with MARCO partners has enabled us to identify 27 broad Industry/economic sectors that

Interim Definition, Taxonomy and Report

April 2018 Page 16 of 402

reflect the full range of current Weather and Climate Services interests. These are listed below and described in more detail in the Glossary.

• Agriculture

• Biotech

• Built Environment

• Business Services

• Communications

• Civil Engineering Sector NEC

• Defence

• Education & Training

• Exploration, Mines and Quarries

• Food & Drink

• Forestry & Timber

• Health Care & Hospitals

• Hospitality

• Legal & Financial

• Logistics

• Manufacturing

• News Publishing and Journalism

• Not Elsewhere Classified

• Processing Industry NEC

• Operational Services

• Pharmaceuticals

• Public & Charitable

• Renewable Energy

• Research & Development

• Retailing & Wholesale

• Tourism & Leisure

• Utilities

It was felt that analysis at the Industry level might be too "broad brush" so these in turn were segmented into more easily understood or more accessible markets (138 in total). These markets are listed at Appendix A and some of the less obvious ones are described in more detail in the Glossary. We also included 380 applications as new column to the dataset and sub-divided according to the previous activity heading of Advisory, Data Management, Measurement, Modelling, Operations, Consulting, Publications and Processing, Re-analysis etc. Applications are effectively solutions that draw on data/information from a range of sources (Land, Satellite, Air and Sea), which is why the “Mixed” category was added to the platform list. By combining the different segments of Weather and Climate Services (Platform, Service, Industry and Market) a data template of 6815 market options was created and then populated for 181 countries (45 countries returned no data) to create the global analysis. Since 2011, the research sources have improved to the point that now data is available on almost all countries. The global analysis of this data is the focus of Section 4 of this report, where the Weather & Climate Services sector is measured for value, transactional volume and growth and differentiated by platform, service, industry and market. In Section 5 the focus is at the international level, (28 countries of the EU) identifying the key economies for Weather and Climate Services. As this is a baseline analysis to create a context for further and deeper study of Climate Service needs and delivery, evidence outweighs commentary. But it is hoped that evidence will provoke commentary based upon experience and new market feedback. Following on from the detailed quantitative analysis in Sections 4 and 5 of the original research, Section 6 presents several findings and observations that relate both to the compilation and analysis of the Weather and Climate Services data set. This section remains relevant to the issues of quantifying a “difficult” sector like Weather & Climate Services and is essentially unchanged from D2.1.

Interim Definition, Taxonomy and Report

April 2018 Page 17 of 402

2. Methodology and Measures

2.1 Research Methodology This report shares a methodology with a much broader research programme for the Low Carbon, Renewable Energy and Environmental sector and the Adaptation Economy that has been applied across three continents for the past ten years. The methodology is highly suited to the analysis of new and evolving markets, new-to-market technologies and “difficult to measure” industries because it works beyond standard national, industrial and market classifications and looks for multiple sources of industrial-based evidence (including the triangulation of data sources) to quantify data values. The methodology relies on a core analytical process called Profiling. This is based upon a 25-year international research programme that started in Harvard University and was subsequently developed in countries across Europe. Profiling is used to track technology and market change and uses analytical data grids, business case studies and industry research to provide probabilistic and measurable evidence about how companies and economies adapt to changing market conditions. The Profiling methodology was first tested against wide ranging corporate business portfolios and then implemented in Russia under US government initiatives to create a sustainable light industrial base. Since then it has been applied to start-ups, micros, SME’s, corporates and whole industries by government, financial and professional services sectors in the US, Europe and Australasia. The methodology has been tried and tested against both new and traditional industries on three continents and more specifically, has been applied to most priority UK economic sectors at global, national, regional and local level. Recent research targets include Environment Technologies, Low Carbon Industry, Renewable Energy, the Water Industry, Adaptation Economy, Marine Environment, Green Economy and Carbon Markets. While the requirements for each industrial sector research project vary, the methodology always follows the same five key stages:

• Define - Identify, select and group the target market activities, whilst conducting an initial check for the right volume and quality of data sources

• Assemble - Populate the data measures for each market activity, carefully filtering the core data sources to ensure that confidence levels are within bounds

• Check - Apply quality assurance checks to ensure data accuracy/ consistency across market activities and different countries and, in some cases, cross-check with different sector values

• Validate - Sense-check and spot-check market data values against specific projects/authoritative sources/expert knowledge/customers or clients

• Publish - Recalculate, update confidence levels and publish research data set. Market activities are only included within this framework when there are multiple sources of reliable data. These sources are screened to remove duplicate references to any single source and then shortlisted by removing outliers and unreliable sources. This shortlist is then

Interim Definition, Taxonomy and Report

April 2018 Page 18 of 402

screened again until some consistency in value is achieved. From the remaining sources a value is then calculated and published. Values created in this way are then “reality tested” by comparing activity values within and across economic or industrial sectors, against known national specialism, against known international trade flows, recognized industry benchmarks and ultimately, government statistics (if they are available). To reflect the wide range of industries under investigation there has to be a very wide range of sources from government, private sector, institutional, industrial, trade, Advertising, HR, financial, investor, academic and other (unpublished and “traded”) sources. These are summarised at Appendix B (approximately 600 sources) but exclude many country - specific and proprietary data sources. The exclusion of sources is based on their historic reliability, particularly in the area of forecast. Many in-country sources prove to be unreliable, particularly where they do not take into account inter-trading activities between regions and countries. This is common throughout Europe and not a characteristic of only a select number of countries. The methodology is quantitative and data intensive and, therefore, very reliant on being able to identify and evaluate multiple data sources. Much of the intellectual property resides in the process for managing and selecting reliable sources that are specific to each market activity. As a result, sources are carefully managed. They are measured and rated for their accuracy and reliability over time. Multiple references to single sources are discounted from the analysis and sources that are outdated or without a measurable track record are excluded. No less than seven qualified sources showing some consistency in results are used to derive any published values. All market intelligence produced in this way is delivered with confidence levels assigned. Confidence levels are a mathematical function of the spread of values across the range of sources that we include in our analysis. Confidence levels vary by activity, geography and by forecast year. Typically, a confidence level of above 80% is achievable, which means that corroborative sources vary around the mean value by +/- 20%. Since the original Weather & Climate Services sector research in 2011, this methodology has become much more widely documented and audited and, as a result, government work conducted using this methodology now qualifies as official statistics, having met the requisite standards. Extracts from the methodology documents, that are relevant to this research, can be provided upon request.

2.2 Defining the Key Measures In this report four key measures are used - Activity Value, Transaction Volume, Growth and Confidence Levels. Each one is explained briefly below. Transaction Volume and Activity Value Value and Volume are often (but not always) two sides of the same coin and in this research are inextricably linked. Within this report a transaction is a sale of either a product, service or product/service combination to another party. "Sale" is the operative word, because this research only considers Climate Services activities that have a financial "footprint". It does not include transactions that are provided free or are exchanged between organisations at no cost. Neither does the research include as part of its forecasts the potential value of services still under development i.e. that have not yet reached the market.

Interim Definition, Taxonomy and Report

April 2018 Page 19 of 402

So, delivery of a due diligence report on the climate risk of a project investment for a water company would be a transaction with a value (monetary) and a volume (of 1) i.e. a contract between two parties for a particular outcome. In some cases, long term multi-project contracts are placed that include multiple transactions over an extended period, in which case additional data sources are used (primarily from the industry concerned) to analyse and disaggregate the contract numbers into transactional values and volumes. In order to measure values and volumes a large number of data sources are used to maximise the accuracy of the output. Usually a source tends to state either volume or value, as their reasons for reporting are usually different. In addition, it is often the case that a source that is known to us to be reliable in reporting volume (say a data confidence rate of 80%) will be unreliable when reporting value (say a data confidence of 65% or less). This is why a large number of sources are reported for each line of data that is compiled - different sources are always used in different combinations to calculate each key measure4. A simple example of consulting multiple sources might be where we know that there were 35 investments above £1m each placed in the water purification sector in 2009/10 totaling £250m (we know this from the water sector); the fund management sector reports that £3.8m was spent on due diligence risk analysis in the water purification sector and the legal sector reports between 28 and 35 due diligence contracts for the water purification sector. Together, these sources enable an intelligent estimate of both value and volume for different but related market activities. A further example might be where for the purposes of corporate governance, major corporate organisations commission external consultants to provide ten-year risk mitigation advice to the main board on the implications of climate change. The consulting sector data shows that in 2010/11 250 major corporate organisations have commissioned this kind of work (the consulting data rarely shows work value for commercial reasons). The investor relations and fund management sector data shows that overall £8.75m was spent on this kind of work and in addition the sector-specific trade associations data reports independently that some £9.2m has been spent. By triangulating data from the different sources it is possible to arrive at highly accurate estimates of value and volume that are just not possible from consulting a single source, however authoritative that source may be within its own sector. Growth Growth is a multi-year measure that includes historical AND forecast growth. The growth measure is derived from live, rapidly changing and multi-sourced data links and is specifically based upon growth in the market value of existing Climate Service activities. Growth is generally a measure of increased market opportunity and can be used for trend analysis, comparison across different markets or as a moving indicator of market confidence (growth time series). The source data for growth forecasts varies enormously and can produce very unsettling and unreliable results if not handled carefully. This is why multiple sources are used, specific to individual activities, and then processed to exclude the outlying high and low estimates until a more consensual set of sources is selected, from which a growth estimate is then calculated. Using this method, it is possible to generate different growth forecasts (high,

4 The number of sources per line of data can vary between 230 (mature sectors/larger economies) and 24 (emergent

sectors/smaller economies). Generally speaking, the higher the number of sources the higher the confidence level that we

assign to the data.

Interim Definition, Taxonomy and Report

April 2018 Page 20 of 402

medium, low) with different risk/confidence levels. This research uses a conservative growth forecast. Confidence Levels All of the above data values are created by the intelligent use and transformation of other primary and secondary data sources. Data sources are carefully managed by measuring and rating their accuracy and reliability over time and by excluding sources that are outdated or without a measurable track record. No less than seven qualified sources are ever used and often, as is the case for this research, the final list of sources is much higher than this. A mean value is then calculated from these selected values and assigned a confidence level. What level of importance should you assign to the data within this report? The answer to that is in the confidence levels for this report, have been calculated for activity value, transaction volume and growth, by country and by industry. The detailed results are shown at Appendix C but, in summary, the global confidence level for all values, aggregated by Platform (Figure 1), Service Type (Figure 2) or Industry (Figure 3) is between 77-84%5. Figure 1: Confidence Levels for Platform by Key Measure

Figure 2: Confidence Levels for Service by Key Measure

Figure 3: Confidence Levels for Industry by Key Measure

5 Confidence levels vary at the individual country level, but these differences "net out" at the global level

Interim Definition, Taxonomy and Report

April 2018 Page 21 of 402

In each case these charts show the confidence level on the horizontal axis, the key measure on the vertical axis and each bubble represents one of the options i.e. Land, Air, Marine or Space. The size of each bubble represents the comparative value (£m) of that option. What these charts demonstrate is that while the distribution (size and positioning of options) may vary quite widely, reflecting the differences in activities and sources, the variance is within quite a narrow band. The final Confidence Level relates to the splitting of the data sources between weather Services and Climate Services. This ranges between 60% and 90% depending upon the platform, industry, market, service or country. Overall the mean figure is 75%, which means the separated values for each (within the total value) may vary within +/- 25%. This mean figure was 75% for the original research and remains at 75%. This suggests that the level of clarity around the division between Weather and Climate Services in the source literature has not substantially changed since 2011 - hence the need for projects like MARCO. Confidence Levels specific to this report can be found in Appendix D. Extended Methodology available in Deliverable D2.1 in Appendix J. Import? Export methodology available in Appendix L of this report.

3. Uses of Weather and Climate Services In Section 2.2 it was suggested that there was a danger that focusing solely upon how Weather and Climate Services are delivered may detract from the ways in which industries are using Weather and Climate Services. To overcome this an audit was conducted as part of the original research of "uses" from the core data sources for this study. The audit was conducted by checking predominantly purchasing sources of data to identify a description of the services purchased. The audit consists of a subjective assessment of uses that have been aggregated under the following 26 headings:

• Corporate Governance

• Insurance Purposes

• Corporate Planning Long Term

• Estates Locational Planning

• Content for Information- Giving Services

• Forward Crop Planning

• Investment Planning

• Infrastructure Planning

• Service Provision Planning

• Major Capital Project Planning

• Irrigation & Drainage Planning

• Research Programmes

• Disaster Recovery Planning

• Health & Safety Services

• Futures Market Data

• Humanitarian Relief planning

• Exploration Planning

• Installation Redundancy Planning

• Regulatory Services (Land Cover)

• Forensic Services

• Border Management & Planning

• Long Term Operations Planning

• Long Range Product Planning

• Educational

• Resource Planning

• Environmental Planning

These headings were then applied to the original 114 markets for Weather and Climate Services and where there was evidence that a "use" was applicable to a market a "1" was noted against the market. Unlike the original analysis of data platforms, services, industries etc. that has been updated and replicated in Sections 4 and 5 of this report, no attempt was

Interim Definition, Taxonomy and Report

April 2018 Page 22 of 402

made, then or now, to quantify either the volume of the above usages or their financial value. The audit was used only to illustrate the:

• Types of needs that Weather and Climate Services fulfill (to demonstrate that the wider research in this report has understood and captured the main uses of Weather and Climate Services), and

• Degree to which these needs are shared across different markets (to validate the industries and markets included as part of the research).

The audit showed that the most frequent usages of Weather and Climate Services were for Corporate Governance (public and shareholder accountability), Insurance, Corporate Planning and Investment Planning - functions that apply to most larger organisations and that are evident for almost all of the markets included in this study. The most specific uses of Weather and Climate Services were for:

• Forward Crop Planning (Arable, Livestock, Forestry, Timber Processing, Government, Charitable, Research and General Consulting markets)

• Exploration Planning (Water, Waste Management, Photovoltaic, Petrochemical, Oil & Gas Exploration, Mines & Quarries, Civil Engineering and General Consulting), and

• Border Management (Legal, Defence, Public Services and General Consultancy). The frequency of the listed 26 uses of Climate Services is shown at Figure 4. Figure 4: Frequency of Climate Service Uses

The audit also showed that some markets (Consultancy, Government, Public Services, Charities and Business Services) have a very broad need for Climate Services and that the needs for other markets (Financial Investments, Leisure, Tourism etc.) can be quite narrow. Table 1 shows the markets with the broadest range of needs.

112 112 110 110 108

97 9589 87 84 80 78 75

6256

18 16 14 13 13 11 11 9 9 9 6

Interim Definition, Taxonomy and Report

April 2018 Page 23 of 402

Table 1: Markets with the Broadest Range of Climate Services Needs

Frequency of use, however, should not be confused with the value of particular services or of specific markets. This information about the uses of Climate Services is really a qualitative backdrop for the quantitative analysis that follows.

What is interesting, about this early audit work and the questions that it posed is the fit with current funded projects specifically targeted at the challenges of qualifying and quantifying both met and un-met needs for Climate Services.

Industry Market Total

Business Services Consultancy (General) 26

Business Services Other Professional Business Services . 26

Public & Charitable Bodies Public Services 21

Public & Charitable Bodies Local Government 20

Renewable Energy Photovoltaic & Solar 20

Built Environment Civil Engineering 18

Education & Training Public Sector Education 18

Manufacturing Petrochemical 17

Public & Charitable Bodies Charitable Bodies 16

Util ities Energy Supply (Gas and Electricity) 16

Education & Training Large Private Educational Establishments 16

Manufacturing Aerospace and Aeronautical (Batch Production) 15

Interim Definition, Taxonomy and Report

April 2018 Page 24 of 402

4. Global Weather & Climate Services

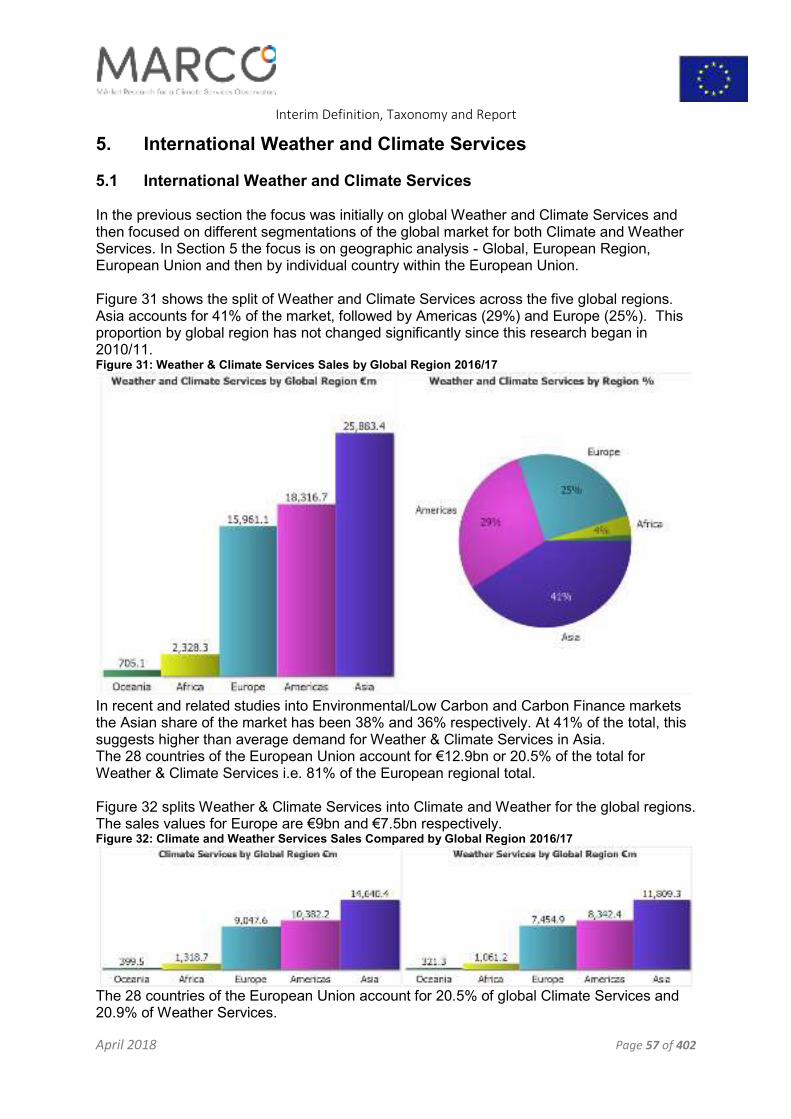

4.1 Introduction In this section of the report the global market for the Weather & Climate Services sector is quantified using the key measures of value, transaction volume and growth, with trade flows (import and export figures). The global Weather & Climate Services market is segmented by data platform, services, industry, markets and NACE codes. The main analysis is of 2016/17 data, but some historical analysis is included.

4.2 Weather & Climate Services Historic Growth The global Weather & Climate Services sector was first measured in 2010/11. At that time, it was estimated to be £26.6bn or €36.6bn using the initial taxonomy and definition. The previous report (D2.1) provided historical data back to 2010/11, however the integration of a Mixed Services Platform has limited the availability of data for this report to 2014/15, which allows us to see a 3-year historic growth pattern. This will be updated with the 2017/18 market figures to give a better picture in D2.3. The new taxonomy and definition has been retrofit to previous years, which is why the size of the market for previous years in this report varies from the D2.1 report. Using the MARCO definition and taxonomy, the global Weather and Climate Service market has grown from €53.9bn in 2014/15 to €63.5bn by 2016/17 as shown by Figure 5.

Figure 5: Weather & Climate Services €m

Historical growth in the Weather & Climate Services sector has been 7.9% in 2014/15 and 8.6% 2015/16.

Figure 6: Weather Services €m

Weather Services was first estimated to be €26.9bn in 2014/15. This has increased to €29bn by 2016/17.

Figure 7: Climate Services €m

Climate Services was first estimated to be €29.4bn in 2014/15. This increased to €35.8bn by 2016/17.

Interim Definition, Taxonomy and Report

April 2018 Page 25 of 402

Overall, Climate Services since 2014/15 has slightly increased its share of the market compared with Weather Services. Climate Services accounted for 54.5% of the total market in 2015/16, 55.6% in 2015/16 and 56.6% of the total market in 2016/17. This indicates that the more traditional Weather Services have been growing slightly slower over that period than the emerging Climate Services market. The previous study suggested that Weather Services and Climate Services were growing at the same rate, this new information about what is actually going on is due to the improved definition of the sector.

4.3 Climate and Weather Services by Data Platform From this point on in the analysis all figures relate to the latest data i.e. 2016/17 and compares Climate and Weather Services. The global value of Weather and Climate Services is split across the five data platforms - Airborne, Land Based, Marine in Situ and Space being the four key platforms and Mixed Services being combinations of the previous four. In Figure 8 for Climate Services, Land Based Services accounts for €12.7bn or 36%, followed by Airborne €9.1bn (26%), Space €8.1bn (23%), Mixed €3bn (8%) and Marine €2.8bn (8%). This compares with Weather Services Land €9.7bn or 33%, followed by Airborne €7.4bn (25%), Space €6.1bn (21%), Mixed Services €3.6bn (12%) and Marine €2.3bn (8%). Figure 8: Value by Data Platform €m

Interim Definition, Taxonomy and Report

April 2018 Page 26 of 402

The global volume of transactions for Weather and Climate Services is estimated at 16.8m, of which 7.0m are Climate Services and 9.7m are Weather Services. Figure 9 shows that Climate Services Land Based Services accounts for 2.6m transactions or 37%, followed by Airborne 1.9m (27%), Space 1.6m (23%), Marine 580,000 (8%) and Mixed 360,000 (5%). For Weather Services Land accounts for 3.6m transactions or 37%, followed by Airborne 2.6m (27%), Space 2.2m (23%), Marine 790,000 (8%) and Mixed 500,000 (5%). Figure 9: Transaction Volume by Data Platform

4.4 Climate and Weather Services by Service Type The second segmentation level for global Climate and Weather Services is by Service Type.

Figure 10: Value by Service Type Climate and Weather Services €m

Figure 10 shows that for Climate Services, Climate Advisory Services at €8.4bn (24%) and Other Consulting at €7.9bn (22%) are the highest values services, followed by Processing & Re-Analysis (12%), Modelling (11%), Measurement (9%), Operation (8%), Publication (7%) and Data Management (6%).

The percentages per Service Type are broadly similar for Weather Services.

Interim Definition, Taxonomy and Report

April 2018 Page 27 of 402

Figure 11: Transactions by Service Type Climate and Weather Services

Figure 11 shows that for Climate Services, Climate Advisory Services at 1.7m transactions (24%) and Other Consulting at 1.3m (21%) are the highest volume services, followed by Processing & Re-Analysis (12%), Modelling (12%), Measurement (10%), Operation (8%), Publication (8%) and Data Management (6%).

The percentages per Service Type are also broadly similar for Weather Services.

Figure 12 compares the historical values for Climate Services for each Service Type from 2014/15 to 2016/17. Figure 12: Climate Services Historical Growth Trend for Service Types €m

4.5 Weather and Climate Services by Industry The third segmentation level for global Weather and Climate Services is by Industry (see Glossary for brief Industry definitions). These Industries are, in turn, made up of different markets (varying from 1-26 for each industry) and they will be explored in more detail in sub section 4.6.

Interim Definition, Taxonomy and Report

April 2018 Page 28 of 402

Figure 13 shows the distribution of global sales of Climate and Weather Services for each of the 27 different Industries for 2016/17. The top 10 industries for Climate Services account for €23bn or 64% of the total. These are: Built Environment (€3.2bn); Renewable Energy (€3.1bn); Public & Charitable Bodies (€2.8bn); News, Publishing & Journalism (€2.7bn); Legal & Financial (€2.6bn); Exploration, Mines & Quarries (€2.2bn), Utilities (€2.1bn); Agriculture (€1.6bn); Forestry & Timber (€1.5bn) and Food and Drink (€1.3bn). The top 10 industries for Weather Services account for €19.4bn or 67% of the total. These are: Legal & Financial (€3.4bn); Public & Charitable Bodies (€3.2bn); Renewable Energy (€2.7bn); Utilities (€2.5bn); Pharmaceuticals (€1.5bn); Operational Services (€1.4bn); Built Environment (€1.3bn); Health Care and Hospitals (€1.3bn); Defence (€1.2bn) and Business Services (€1bn). Compared with the previous segmentations by Platform and by Service, industries end-users show much more significant differences between Climate and Weather Services.

Interim Definition, Taxonomy and Report

April 2018 Page 29 of 402

Figure 13: Climate and Weather Services by Industry End-User €m

Interim Definition, Taxonomy and Report

April 2018 Page 30 of 402

In Figure 14 the same data is shown, but this time as a percentage for each end-user industry for 2016/17. Figure 14: Climate and Weather Services by Industry End-User %

Interim Definition, Taxonomy and Report

April 2018 Page 31 of 402

Figure 15 explores the different industrial needs for Climate and Weather Services as a percentage of the total. Some industries like Agriculture, Hospitality, Tourism & Leisure and News, Publishing & Journalism are more focused on Climate Services as a percentage of their needs, compared with Defence, Legal & Financial, Retailing and Wholesale and Business Services who are more focused on Weather Services. Some of these results may appear surprising i.e. Agriculture and demand for Weather Services, but industry demand patterns will reflect the “commoditisation” of some weather services, as free services and new apps continue to enter and dominate the market. The full Climate Services details of each of the 27 industries included in this analysis is captured in a series of dashboards at Appendix J.

Interim Definition, Taxonomy and Report

April 2018 Page 32 of 402

Figure 15: Industrial split by Climate and Weather Services

Interim Definition, Taxonomy and Report

April 2018 Page 33 of 402

Figure 16 shows the historical sales values for Climate Services for the period 2014/15 to 2016/17. These figures suggest that global demand for Climate Services by Industry are well established and not subject to rapid or significant change. Figure 16: Historical Climate Services Sales by Industry €m

Interim Definition, Taxonomy and Report

April 2018 Page 34 of 402

4.6 Weather and Climate Services by Industry and Markets Each of the 27 industries is segmented into more distinctive markets. In Figure 17 the top ten industries (identified above) are divided into markets for global Climate Services using stacked bar charts. Table 2 Ranks the Top 20 markets for global Climate Services. Figure 17: Top 10 Industries for Climate Services split by Market €m 2016/17

Interim Definition, Taxonomy and Report

April 2018 Page 35 of 402

Table 2: Top 20 Global Climate Services Markets 2016/17 €m

The top 10 industry markets for Climate Services account for €14.4bn or 40% of the 2016/17 total. The top 20 industry markets for Climate Services account for €21.1bn or 59% of total sales in 2016/17.

The total number of industry markets is currently 129, so 16% of the industry markets account for 59% of the Climate Services value. In Figure 18 the top ten industries (identified above) are divided into markets for global Weather Services using stacked bar charts. Table 3 Ranks the Top 20 markets for global Weather Services.

Public and Charitable Bodies Local Government 1,623.6

News Publishing and Journalism Multi Media and Broadcasting Sector 1,412.1

Exploration, Mines and Quarries Oil and Gas Exploration 1,395.8

Multi-Industry Location Planning for Large Establishments 1,330.5

Agriculture Arable 1,323.4

Utilities Water Supply 1,180.2

Forestry and Timber Forestry Corporates 1,127.3

Built Environment Construction 1,091.7

Hospitality Hotels and Catering 893.9

News Publishing and Journalism News Papers and Periodicals 847.5

Public and Charitable Bodies Public Services 722.9

Exploration, Mines and Quarries Mines and Quarries 716.2

Utilities Energy Supply (Gas Electricity) 649.7

Health Care and Hospitals Hospitals 620.9

Food and Drink Food Production (In-Line Process Manufacture) 606.4

Legal and financial Re Insurance 581.8

Tourism and Leisure Operation of Leisure Facilities 537.2

Renewable Energy Geothermal 503.0

Interim Definition, Taxonomy and Report

April 2018 Page 36 of 402

Figure 18: Top 10 Industries for Weather Services split by Market €m 2016/17

Interim Definition, Taxonomy and Report

April 2018 Page 37 of 402

Table 3: Top 20 Global Weather Services Markets 2016/17 €m The top 10 industry markets for Weather Services account for €11bn or 38% of the 2016/17 total. The top 20 industry markets for Weather Services account for €16bn or 56% of total sales in 2016/17.

The full listing for all 129 markets is included at Appendix F.

Industry Market

Weather

Services €mPublic and Charitable Bodies Local Government 1,858.6

Renewable Energy Wind 1,639.1

Multi-Industry Location Planning for Large Establishments 1,584.1

Utilities Water Supply 1,415.0

Public and Charitable Bodies Public Services 820.7

Built Environment Civil Engineering 763.8

Legal and financial Re Insurance 746.9

Utilities Energy Supply (Gas Electricity) 742.1

Business Services Consultancy (General) 722.9

Defence Contractors for Defence Projects 693.1

Healthcare and Hospitals Hospitals 607.9

Exploration, Mines and Quarries Oil and Gas Exploration 588.0

Pharmaceuticals Pharmaceuticals (In-Line Process Manufacture) 567.8

Legal and financial Future Analysts 554.6

Operational Services Airport Servicing and Operations 535.4

4.7 Weather and Climate Services by NACE Codes The kMatrix taxonomy of data is built from the “bottom up” rather than the “top down”, this means that the data is not fixed and allows reporting in different formats. The previous sections have looked at the data in terms of Industry, however in D4.5 the taxonomy was mapped to NACE codes. We can now explore the Climate Services and Weather Services at this level of reporting. Figure 19 shows the distribution of global sales of Climate and Weather Services for each of the 17 different NACE codes for 2016/17. The top 10 NACE Codes for Climate Services account for €29.2bn or 82% of the total. These are: Electricity, Gas, Steam & Air Conditioning (€3.9bn); Information & Communication (€3.6bn); Public Administration & Defence (€3.5bn); Construction (€3.4bn); Agriculture, Forestry & Fishing (€3.1bn); Manufacturing (€2.9bn); Financial & Insurance (€2.6bn); Accommodation & Food (€2.5bn); Mining and Quarrying (€2.2bn) and Transport & Storage (€1.7bn). The top 10 NACE Codes for Weather Services account for €23.4bn or 80% of the total. These are: Public Administration & Defence (€4.4bn); Electricity, Gas, Steam & Air Conditioning (€3.6bn); Financial & Insurance (€3.4bn); Manufacturing (€3.3bn); Professional, Scientific & Technical (€1.6bn); Water Supply, Sewerage & Waste Management (€1.6bn); Construction (€1.5bn); Information & Communication (€1.4bn): Human Health (€1.3bn) and Agriculture, Forestry and Fishing (€1.2bn). NACE end-users show significant differences between Climate and Weather Services, for example although the top 5 NACE Codes make up 56% of the Weather Services market, the top 4 NACE Codes account for 51%. Those 4 NACE Codes dominate the market, such dominance is not present in the Climate Services market.

Interim Definition, Taxonomy and Report

April 2018 Page 39 of 402

Figure 19: Climate and Weather Services by NACE Code End-User €m

Interim Definition, Taxonomy and Report

April 2018 Page 40 of 402

In Figure 20 the same data is shown, but this time as a percentage for each end-user NACE code for 2016/17. Figure 20: Climate and Weather Services by NACE End-User %

Interim Definition, Taxonomy and Report

April 2018 Page 41 of 402

Figure 21 explores the different NACE needs for Climate and Weather Services as a percentage of the total. Some NACE Codes, like Agriculture, Forestry & Fishing; Accommodation & Food; Arts, Entertainment & Recreation and Information & Communication are more focused on Climate Services as a percentage of their needs, compared with Professional, Scientific & Technical; Wholesale & Retail; Financial & Insurance and Public Administration & Defence who are more focused on Weather Services. As for the Industry split, some of these results may appear surprising i.e. Agriculture and demand for Weather Services, but NACE demand patterns will reflect the “commoditisation” of some weather services, as free services and new apps continue to enter and dominate the market. The full Climate Services details of each of the 17 NACE Codes included in this analysis is captured in a series of dashboards at Appendix J.

Interim Definition, Taxonomy and Report

April 2018 Page 42 of 402

Figure 21: NACE Code split by Climate and Weather Services

Interim Definition, Taxonomy and Report

April 2018 Page 43 of 402

Figure 22 shows the historical sales values for Climate Services for the period 2014/15 to 2016/17. These figures suggest that global demand for Climate Services by NACE Code are well established and not subject to rapid or significant change. Figure 22: Historical Climate Services Sales by NACE Code €m

Interim Definition, Taxonomy and Report

April 2018 Page 44 of 402

4.8 Weather and Climate Services by NACE Codes and Markets Each of the 17 NACE Codes is segmented into more distinctive markets. In Figure 23 the top ten NACE Codes (identified above) are divided into markets for global Climate Services using stacked bar charts. Table 4 Ranks the Top 20 markets for global Climate Services. Figure 23: Top 10 NACE Codes for Climate Services split by Market €m 2016/17

Interim Definition, Taxonomy and Report

April 2018 Page 45 of 402

Table 4: Top 20 Global Climate Services Markets 2016/17 €m

The top 10 NACE Code markets for Climate Services account for €14.4bn or 40% of the 2016/17 total. The top 20 NACE Code markets for Climate Services account for €21.1bn or 59% of total sales in 2016/17.

NACE Code Market

Climate

Services €mConstruction Civil Engineering 1,978.2

Electricity, Gas, Steam & Air Conditioning Wind 1,912.3

Public Administration & Defence Local Government 1,623.6

Information & Communication Multi Media and Broadcasting Sector 1,412.1

Mining and Quarrying Oil and Gas Exploration 1,395.8

Multi-Code Location Planning for Large Establishments 1,330.5

Multi-Code Arable 1,323.4

Water Supply, Sewerage & Waste Management Water Supply 1,180.2

Information & Communication News Papers and Periodicals 847.5

Public Administration & Defence Public Services 722.9

Mining and Quarrying Mines and Quarries 716.2

Electricity, Gas, Steam & Air Conditioning Energy Supply (Gas Electricity) 649.7

Human Health Hospitals 620.9

Accommodation & Food Food Production (In-Line Process Manufacture) 606.4

Financial & Insurance Re Insurance 581.8

Arts, Entertainment and Recreation Operation of Leisure Facilities 537.2

Electricity, Gas, Steam & Air Conditioning Geothermal 503.0

Interim Definition, Taxonomy and Report

April 2018 Page 46 of 402

In Figure 24 the top ten NACE Codes (identified above) are divided into markets for global Climate Services using stacked bar charts. Table 5 Ranks the Top 20 markets for global Climate Services. Figure 24: Top 10 NACE Codes for Weather Services split by Market €m 2016/17

Interim Definition, Taxonomy and Report

April 2018 Page 47 of 402

Table 5: Top 20 Global Weather Services Markets 2016/17 €m

The top 10 NACE Code markets for Weather Services account for €11bn or 38% of the 2016/17 total. The top 20 NACE Code markets for Weather Services account for €16bn or 56% of total sales in 2016/17.

NACE Code Market

Weather