37

Market Fundamentals Frederick University 2012

| Date post: | 30-Dec-2015 |

| Category: |

Documents |

| Upload: | leslie-jenkins |

| View: | 213 times |

| Download: | 0 times |

Market Fundamentals

Frederick University

2012

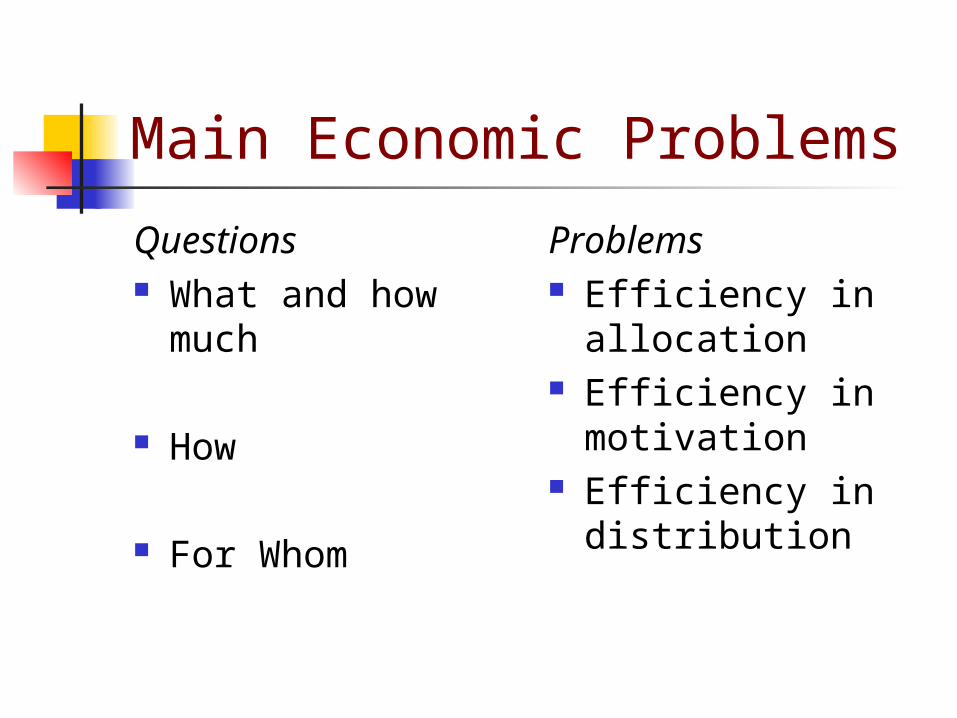

Main Economic Problems

Questions What and how

much

How

For Whom

Problems Efficiency in

allocation Efficiency in

motivation Efficiency in

distribution

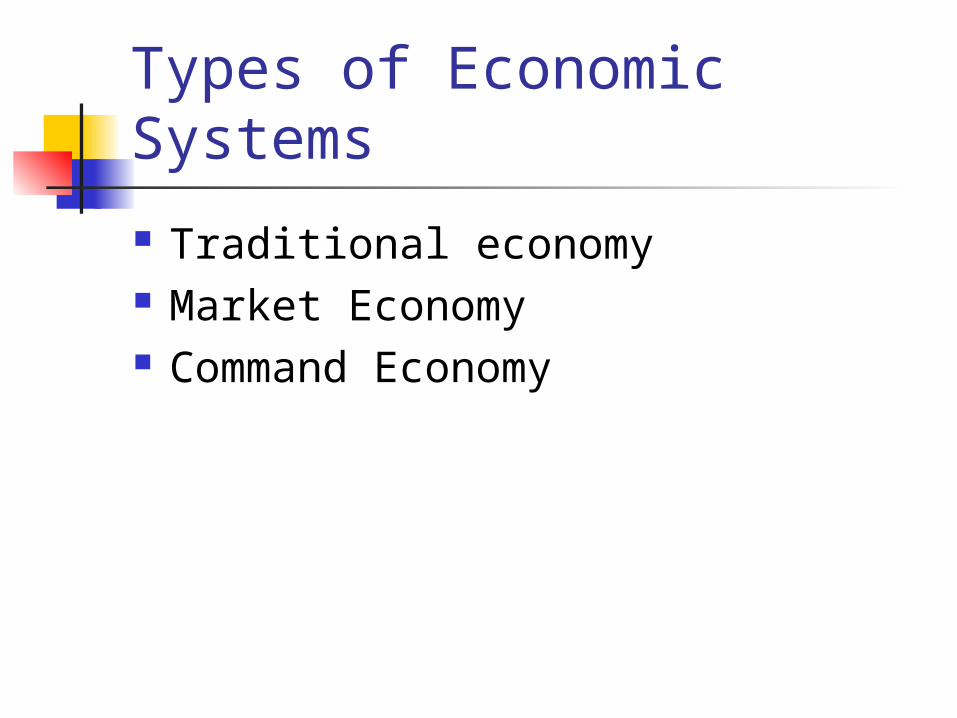

Types of Economic Systems

Traditional economy Market Economy Command Economy

Market Functions

Allocation of scarce resources Motivation for efficiency Distribution of goods and services

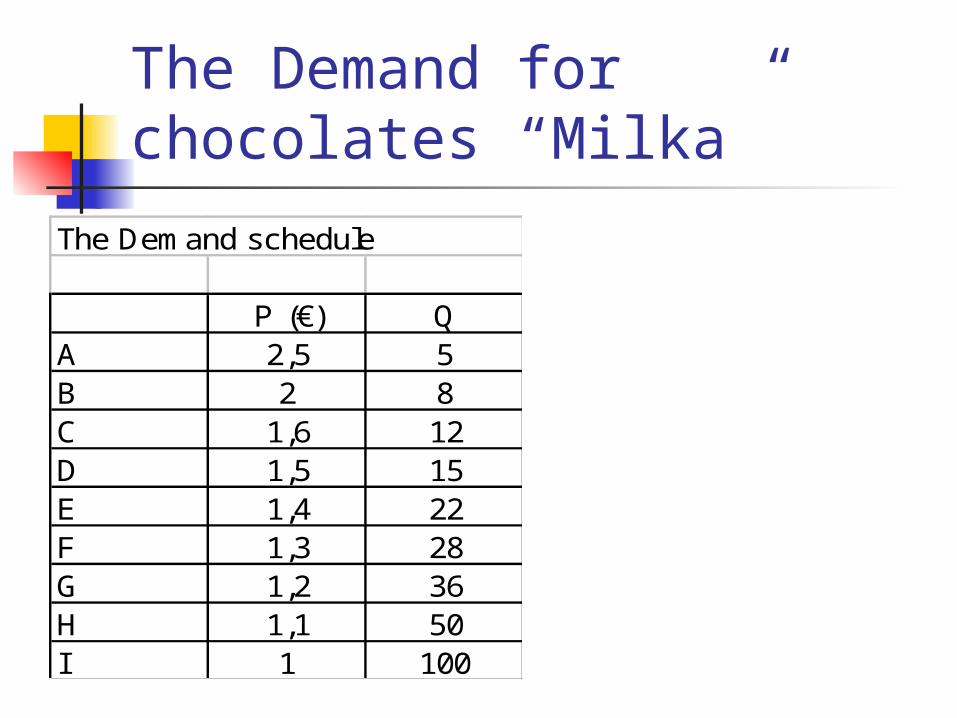

The Demand for chocolates “Milka”

The Demand schedule

P (€) QA 2,5 5B 2 8C 1,6 12D 1,5 15E 1,4 22F 1,3 28G 1,2 36H 1,1 50I 1 100

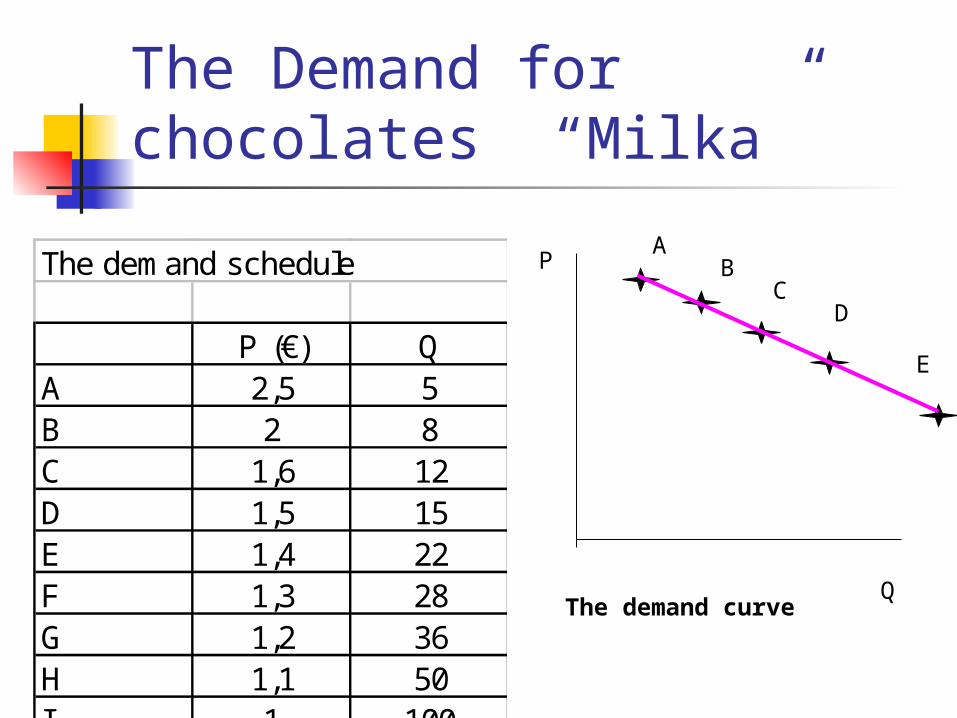

The Demand for chocolates “Milka”

The demand schedule

P (€) QA 2,5 5B 2 8C 1,6 12D 1,5 15E 1,4 22F 1,3 28G 1,2 36H 1,1 50I 1 100

P

Q

AB

CD

E

The demand curve

Demand

Demand – buyers’ behavior The Demand for a good – the

quantities buyers are willing and able to buy at every different price

The law of Demand – the decrease in the price of the good raises the quantity of the good demanded, other factors held equal

FACTORS DETERMINING DEMAND

Buyers’ income Prices of the other

goods Buyers’

expectations Buyers’ taste and preferences

Market size Institutions

P

Q

Demand rises = the demandcurve shifts rightwards

Demand falls = the demandcurve shifts leftwards

D

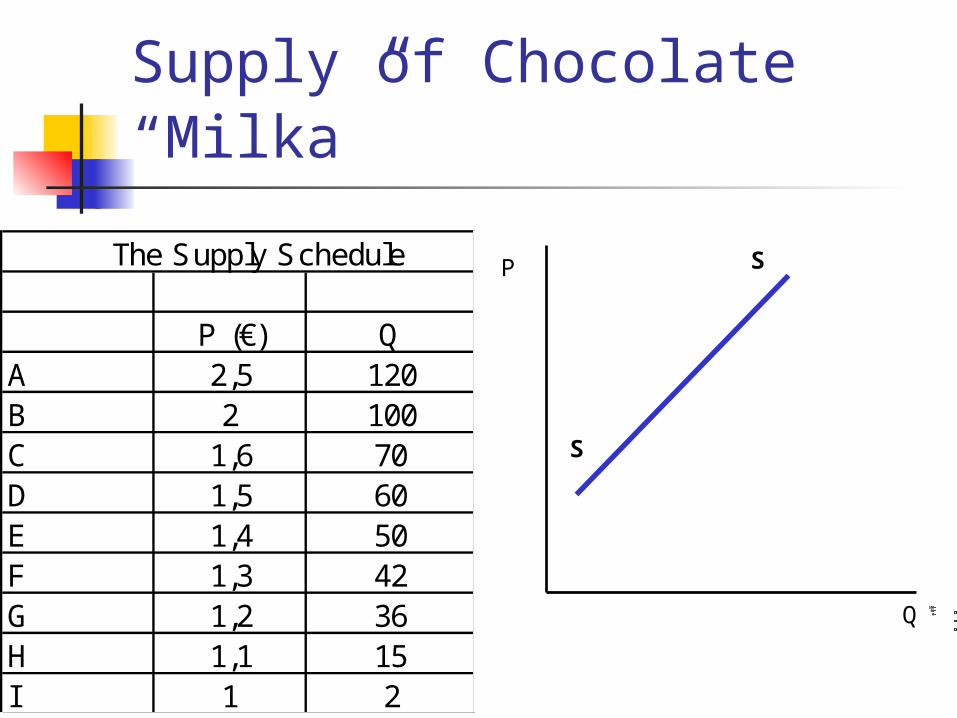

Supply of Chocolate “Milka”

050100

1st

Qt

r

East

West

North

The Supply Schedule

P (€) QA 2,5 120B 2 100C 1,6 70D 1,5 60E 1,4 50F 1,3 42G 1,2 36H 1,1 15I 1 2

P

Q

S

S

Supply

Supply – sellers’ behaviorThe Supply of a good – quantities of

the good that sellers are willing to sell at different price levels

The Law of Supply – as the price of the good rises, sellers are willing to sell greater quantities of the good, ceteris paribus.

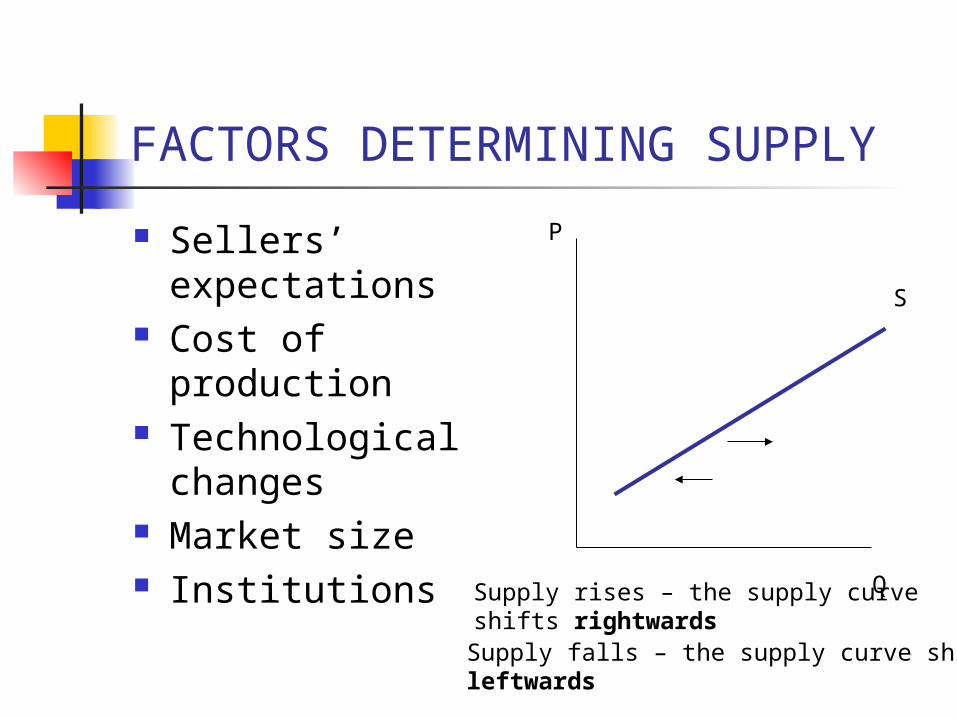

FACTORS DETERMINING SUPPLY

Sellers’ expectations

Cost of production Technological

changes Market size Institutions

P

Q

S

Supply rises – the supply curveshifts rightwardsSupply falls – the supply curve shiftsleftwards

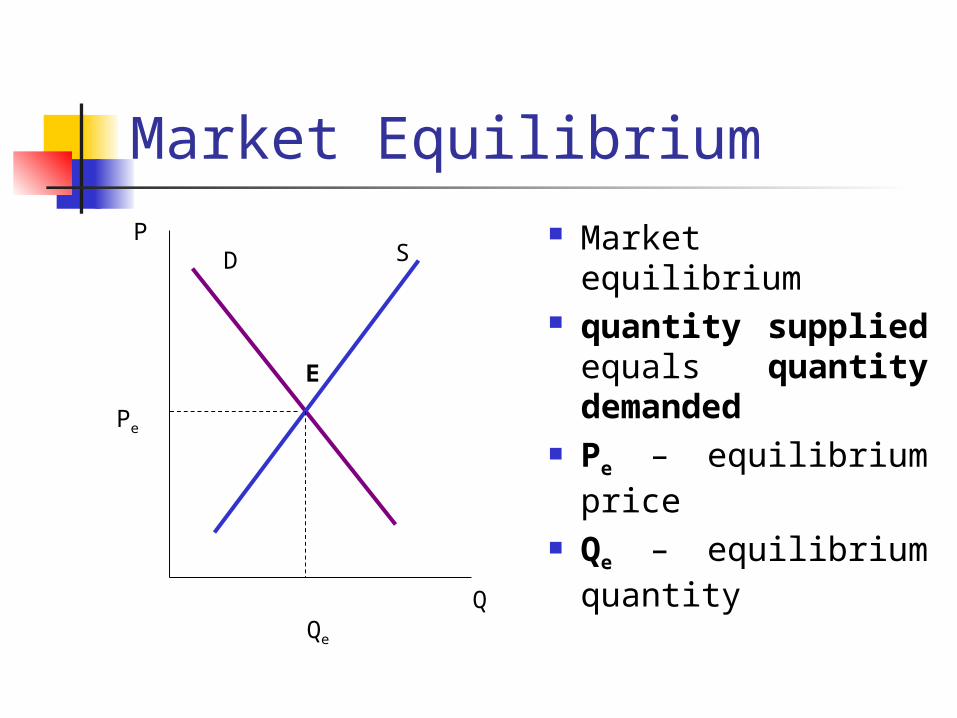

Market Equilibrium

P

Q

D S

E

The market is in equilibrium when the quantity supplied equals the quantity demanded at the same price

Pe

Qe

The Supply Schedule

P (€) QA 2,5 120B 2 100C 1,6 70D 1,5 60E 1,4 50F 1,3 42G 1,2 36H 1,1 15I 1 2

The demand schedule

P (€) QA 2,5 5B 2 8C 1,6 12D 1,5 15E 1,4 22F 1,3 28G 1,2 36H 1,1 50I 1 100

Market EquilibriumP Market equilibrium

quantity supplied equals quantity demanded

Pe – equilibrium price

Qe – equilibrium quantity

Q

D S

Pe

Qe

E

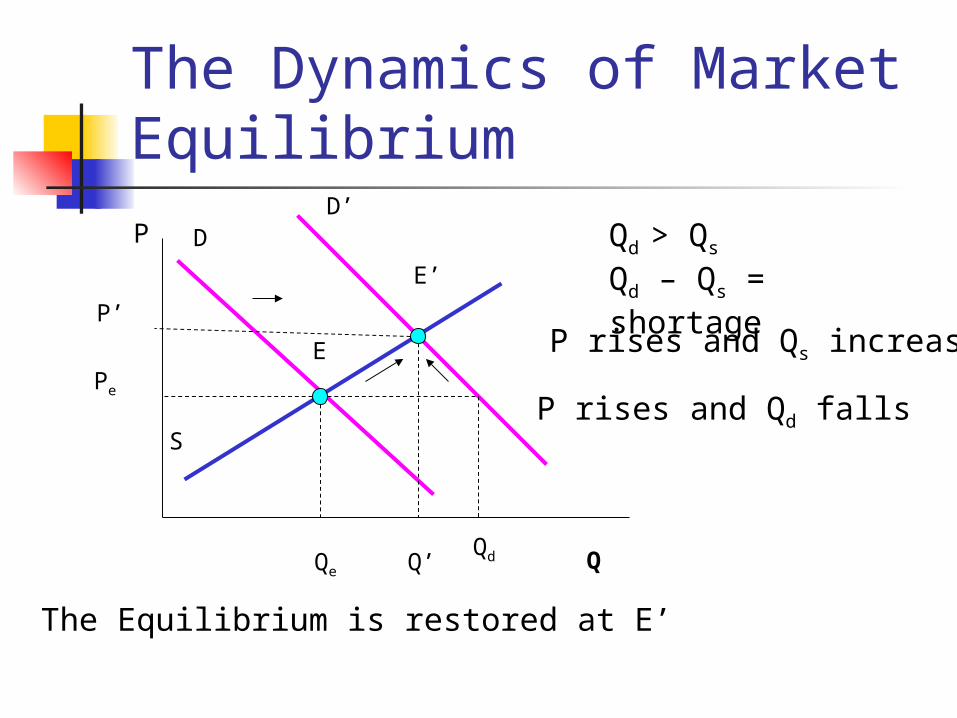

The Dynamics of Market EquilibriumP

Q

D

S

E

D’

Pe

Qe

Qd

Qd > Qs

Qd – Qs = shortage

P rises and Qs increases

P rises and Qd falls

The Equilibrium is restored at E’

P’

Q’

E’

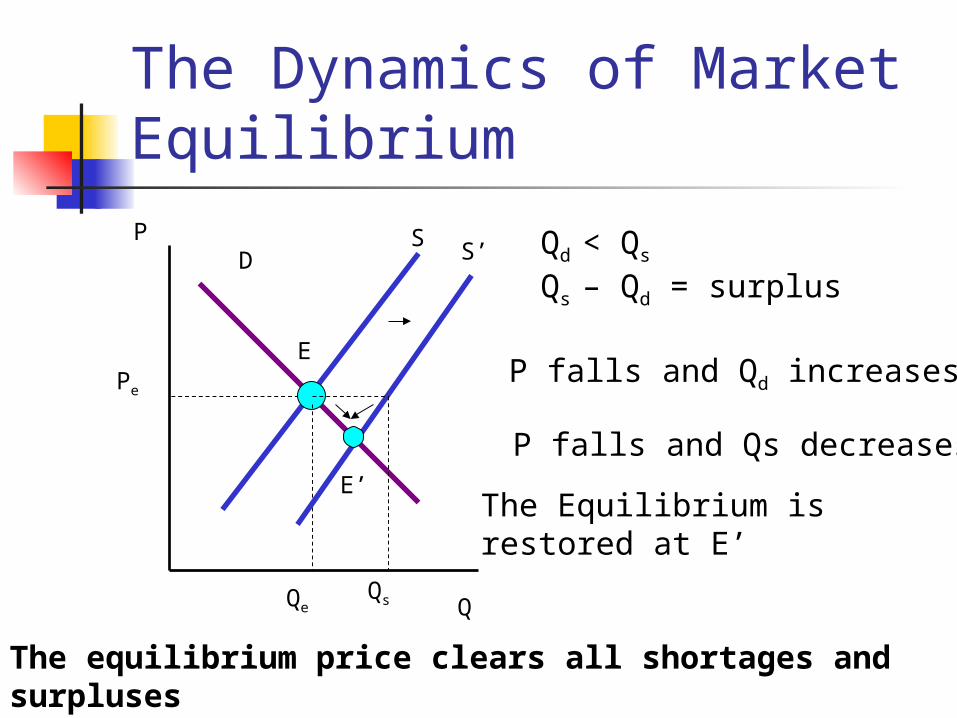

The Dynamics of Market EquilibriumP

Q

DS

EPe

Qe

S’

Qs

Qd < Qs

Qs – Qd = surplus

P falls and Qs decreases

P falls and Qd increases

E’The Equilibrium is restored at E’

The equilibrium price clears all shortages and surplusesPe = market clearing price

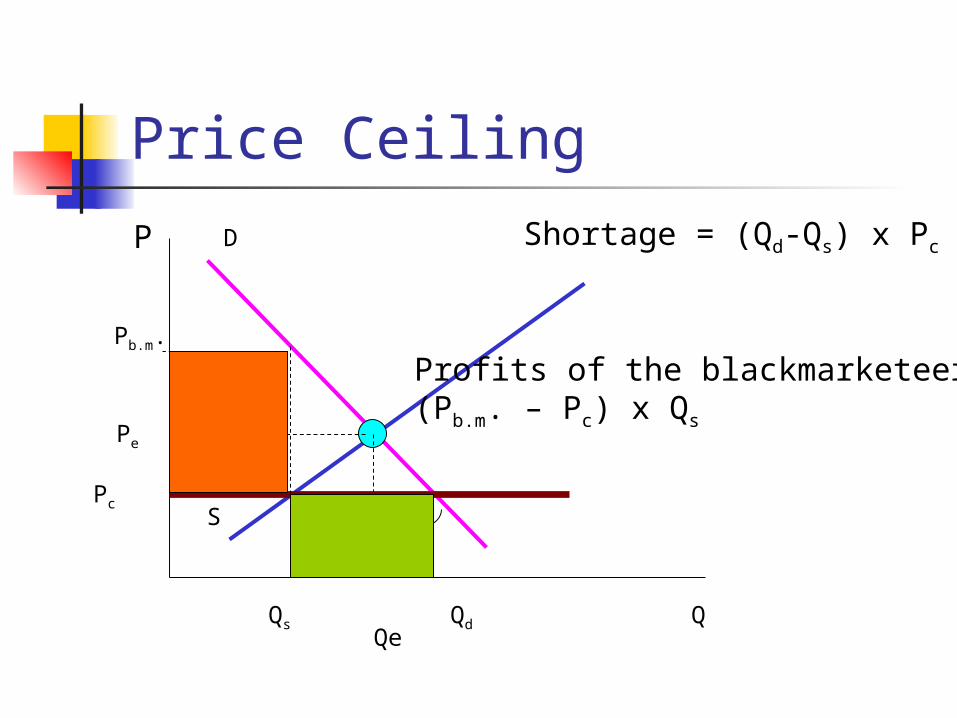

Price Ceiling

P

Q

D

S

Pe

Qe

Pc

Qs Qd

shortage

Pb.m.

Shortage = (Qd-Qs) x Pc

Profits of the blackmarketeers =(Pb.m. – Pc) x Qs

Arbitrage and speculationP

Q

Oz widget market

D

SPOz

QOz

P

Q

Zo widget market

D

S

PZo

QZo

Demand shifts to Zo marketSupply shifts to Oz market

Shifts in Supply and Demand until price differences are eliminated

exports

imports

Arbitrage and speculation

Arbitrage – the process by which individuals seek to make a profit by taking advantage of discrepancies among prices prevailing simultaneously in different markets

Speculation – a way to make a profit by taking a deliberately risky position

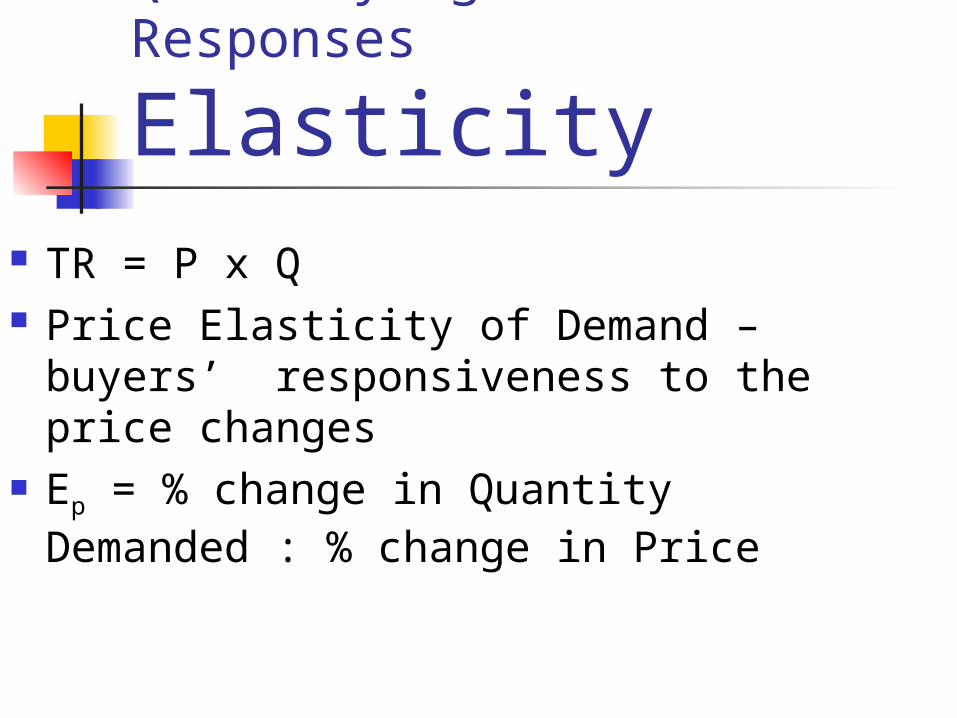

Quantifying Market Responses

Elasticity TR = P x Q Price Elasticity of Demand – buyers’

responsiveness to the price changes Ep = % change in Quantity Demanded : %

change in Price

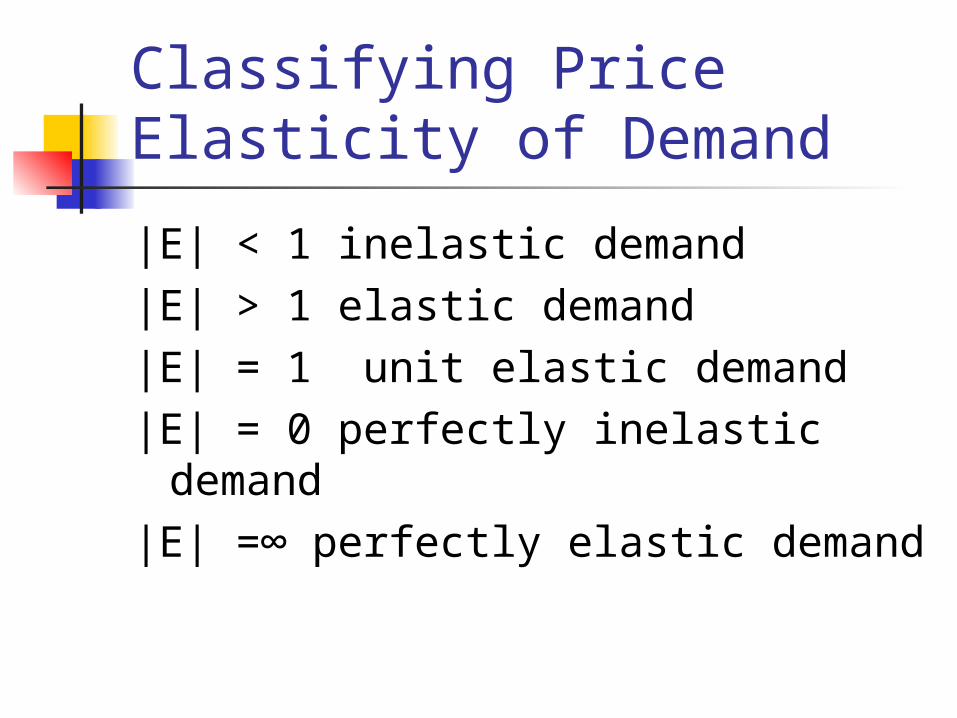

Classifying Price Elasticity of Demand

|Е| < 1 inelastic demand|E| > 1 elastic demand|E| = 1 unit elastic demand|E| = 0 perfectly inelastic demand|E| =∞ perfectly elastic demand

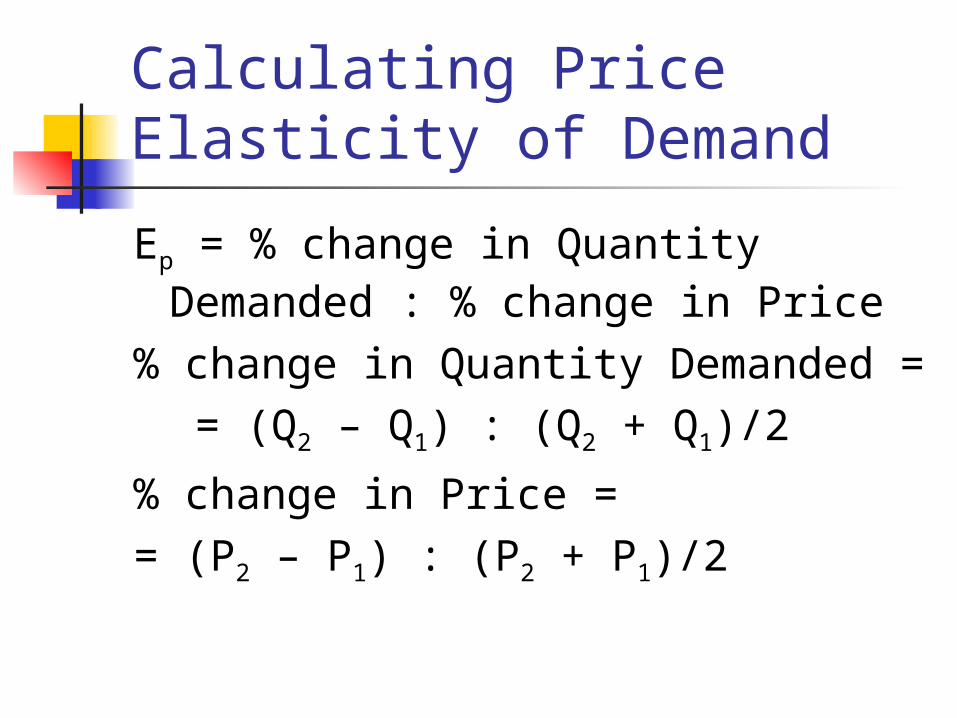

Calculating Price Elasticity of Demand

Ep = % change in Quantity Demanded : % change in Price

% change in Quantity Demanded = = (Q2 – Q1) : (Q2 + Q1)/2

% change in Price == (P2 – P1) : (P2 + P1)/2

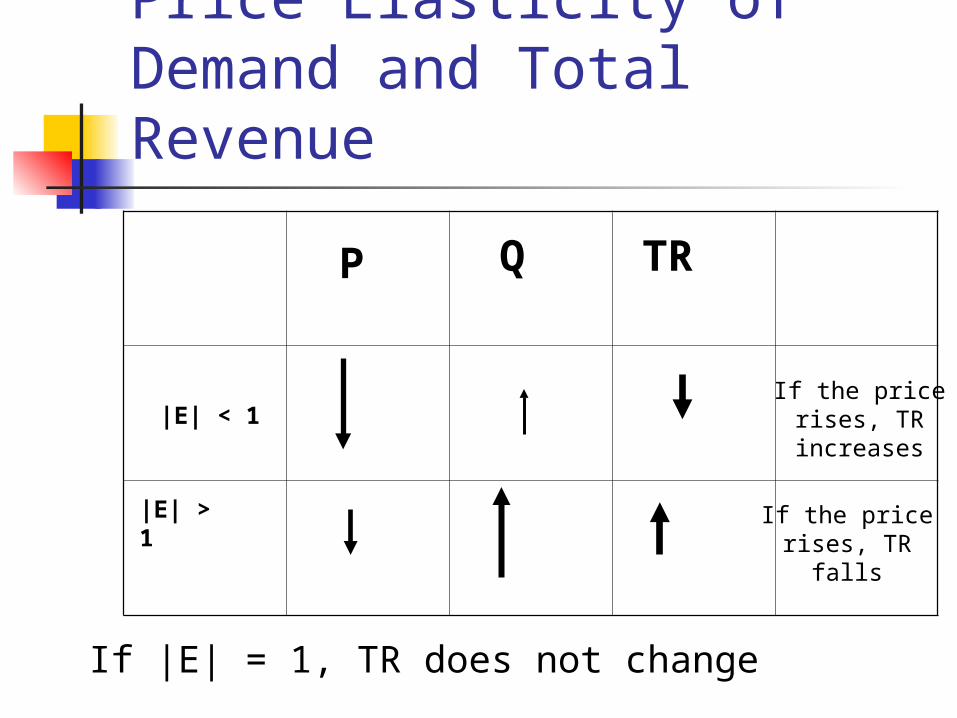

Price Elasticity of Demand and Total Revenue TR = P x Q The Law of Demand - If P rises, Q falls If the percentage change in price is

greater than the percentage change in quantity, the demand is inelastic

If the price falls, the change in quantity demanded does not compensate for the price reduction and TR falls

If the price rises, TR will increase

Price Elasticity of Demand and Total Revenue

P Q TR

|E| > 1

If the pricerises, TRincreases

If the pricerises, TR

falls

If |E| = 1, TR does not change

|E| < 1

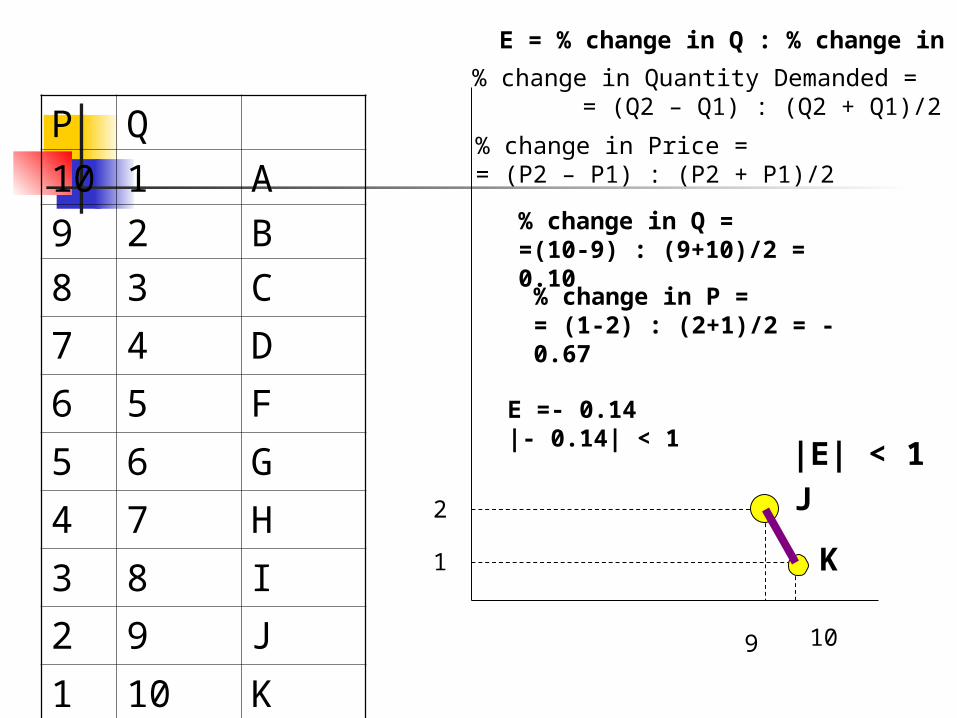

P Q

10 1 A

9 2 B

8 3 C

7 4 D

6 5 F

5 6 G

4 7 H

3 8 I

2 9 J

1 10 K

|E| < 1

2

9

1

10

E = % change in Q : % change in P

% change in Quantity Demanded = = (Q2 – Q1) : (Q2 + Q1)/2

% change in Price == (P2 – P1) : (P2 + P1)/2

% change in Q = =(10-9) : (9+10)/2 = 0.10% change in P = = (1-2) : (2+1)/2 = - 0.67

E =- 0.14|- 0.14| < 1

J

K

|E|>1

|E| < 1

|E|= 1

% change in Q = (6-5) : (6+5)/2 == 1.18

% change in P = (5-6) : (5+6)/2 = - 1.18

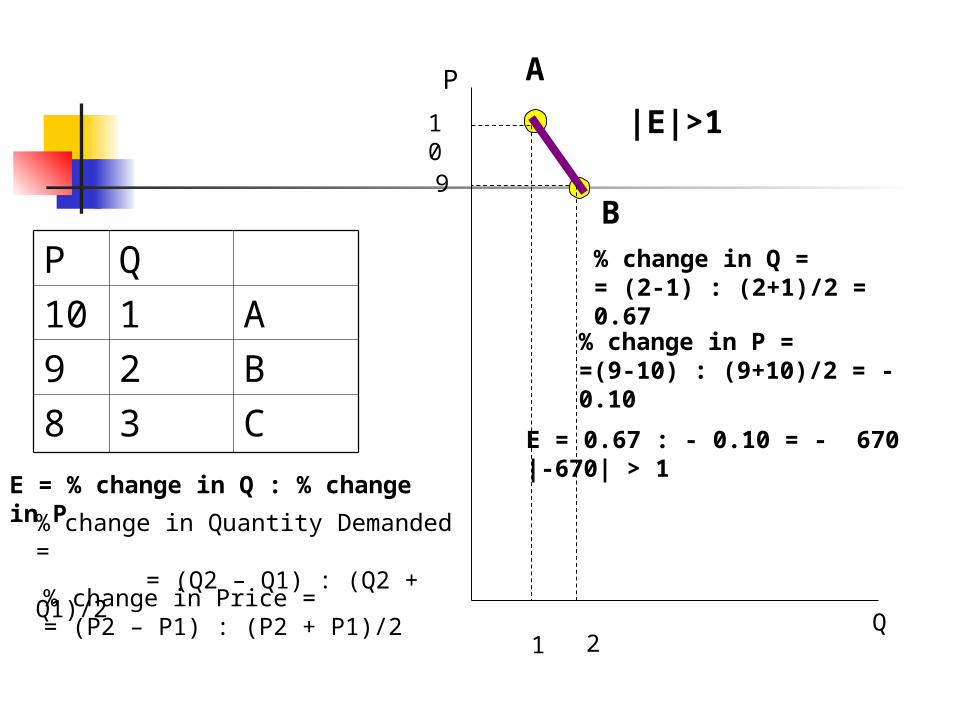

P Q

10 1 A

9 2 B

8 3 C

7 4 D

6 5 F

5 6 G

4 7 H

3 8 I

2 9 J

1 10 K

6

5

5

6

F

G

E = 1.18 : - 1.18 = -1|- 1| = 1

P Q

10 1 A

9 2 B

8 3 C

|E|>1

% change in Q = = (2-1) : (2+1)/2 = 0.67

% change in P = =(9-10) : (9+10)/2 = - 0.10

A

B

P

Q

10

1

9

2

E = % change in Q : % change in P

E = 0.67 : - 0.10 = - 670|-670| > 1

% change in Quantity Demanded = = (Q2 – Q1) : (Q2 + Q1)/2

% change in Price == (P2 – P1) : (P2 + P1)/2

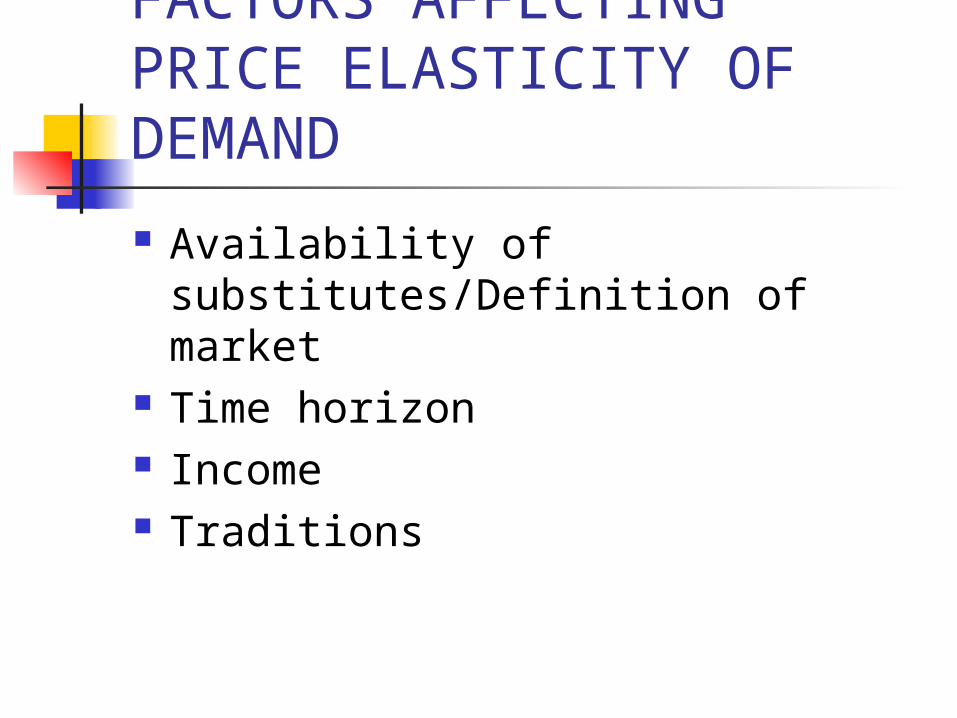

FACTORS AFFECTING PRICE ELASTICITY OF DEMAND

Availability of substitutes/Definition of market

Time horizon Income Traditions

Price Elasticity of Supply

Price elasticity of supply – sellers’ responsiveness to the price changes

Ep = % change in Quantity Supplied : % change in Price

Price Elasticity of Supply

P

Q

E < 1

E > 1

E = 1

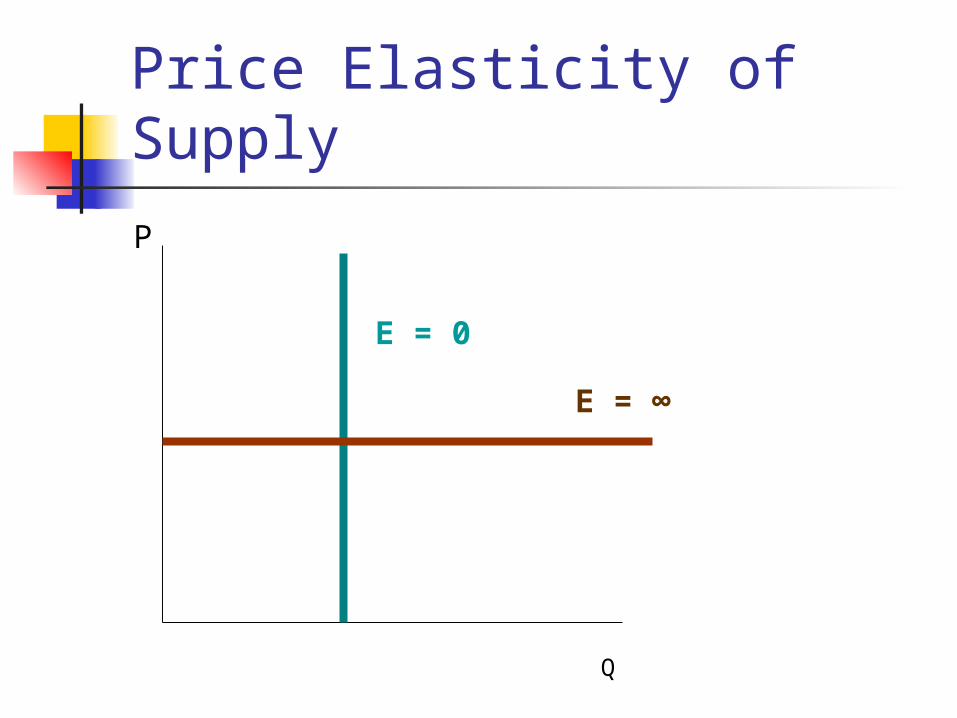

Price Elasticity of Supply

P

Q

E = 0

E = ∞

FACTORS AFFECTING PRICE ELASTICITY OF SUPPLY

Time horizon Availability of production factors Mobility of production factors Inventory levels Competitiveness of the market

structure Institutions

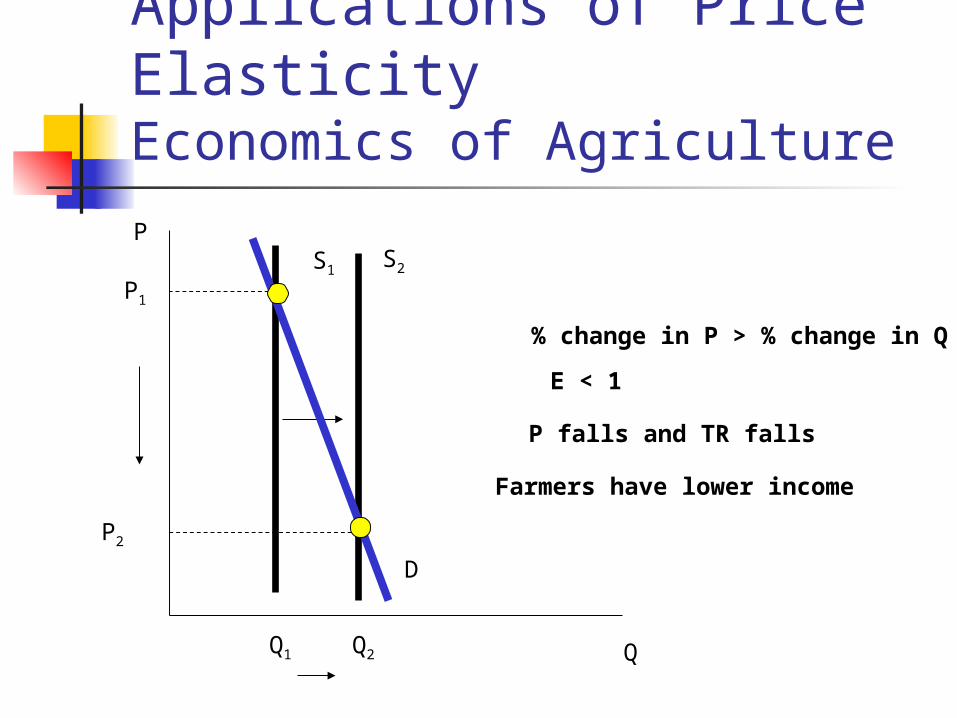

Applications of Price ElasticityEconomics of Agriculture

P

Q

S1 S2

D

Q1

P1

P2

Q2

% change in P > % change in Q

E < 1

P falls and TR falls

Farmers have lower income

Applications of Price ElasticityEconomics of Agriculture

P

Q

S

D

P1

P0

Q

Solution 1: government pays the difference P1 – P0 to the farmers

Government will lose (P1 – P0) x Q

Applications of Price ElasticityEconomics of Agriculture

P

Q

S

D

Q1

P1

P0

Q

Solution 2: government buys allQ from farmers at P1 and sells it.However, buyers will buy less at P1

Government cannot sell Q – Q1 and willlose (Q – Q1) x P1

Solution 2 is preferable because the loss is smaller.

The loss under solution 1 is (P1 – P0) x QThe loss under solution 2 is (Q – Q1) x P1

Since demand is inelastic, (P1 – P0) x Q > (Q – Q1) x P1

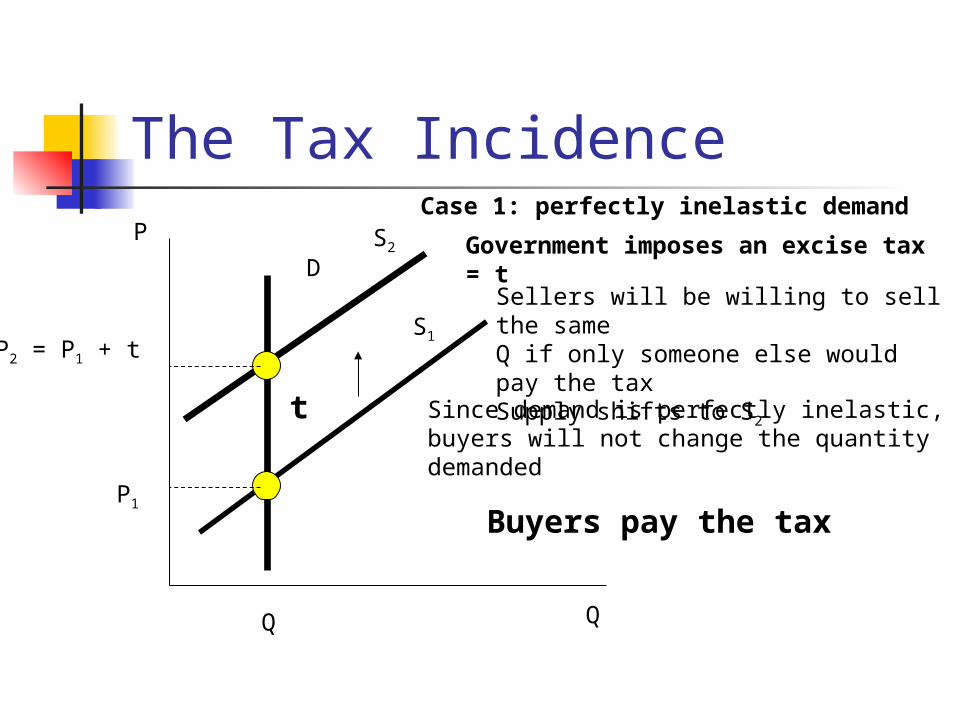

The Tax IncidenceP

Q

D

S1

Case 1: perfectly inelastic demand

Government imposes an excise tax = t

Sellers will be willing to sell the sameQ if only someone else would pay the taxSupply shifts to S2

Q

P1

Since demand is perfectly inelastic,buyers will not change the quantity demanded

t

S2

P2 = P1 + t

Buyers pay the tax

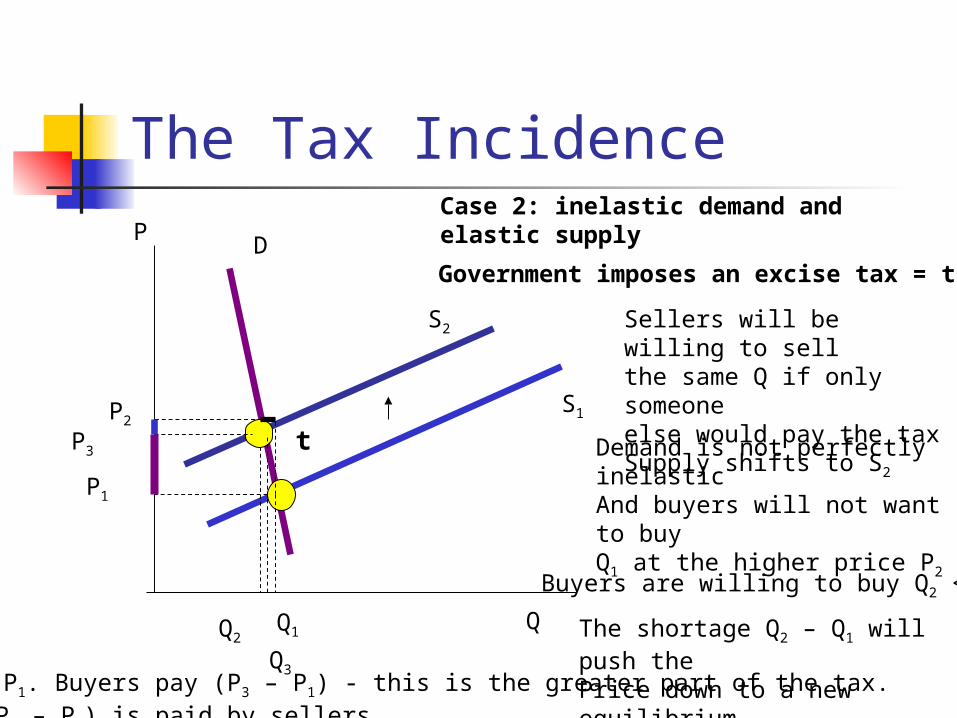

The Tax IncidenceP

Case 2: inelastic demand andelastic supply

Q

D

S1

Government imposes an excise tax = t

Sellers will be willing to sell the same Q if only someoneelse would pay the taxSupply shifts to S2

Demand is not perfectly inelastic And buyers will not want to buyQ1 at the higher price P2

Q1

P1

S2

P2

Buyers are willing to buy Q2 < Q1

Q2 The shortage Q2 – Q1 will push the Price down to a new equilibrium

P3 t

Q3Tax = P2 – P1. Buyers pay (P3 – P1) - this is the greater part of the tax. The rest (P2 – P3) is paid by sellers

The Tax Incidence

PCase 2: elastic demand andinelastic supply

Q

D

S1

Government imposes an excise tax = t

Sellers will be willing to sell the same Q if only someoneelse would pay the taxSupply shifts to S2

Demand is elastic And buyers will not want to buyQ1 at the higher price P2

Q1

P1

S2

P2

Buyers are willing to buy Q2 < Q1

Q2

The shortage Q2 – Q1 will push the Price down to a new equilibrium

P3

t

Q3

Tax = P2 – P1. Buyers pay (P3 – P1) - this is the smaller part of the tax. The rest (P2 – P3) is paid by sellers