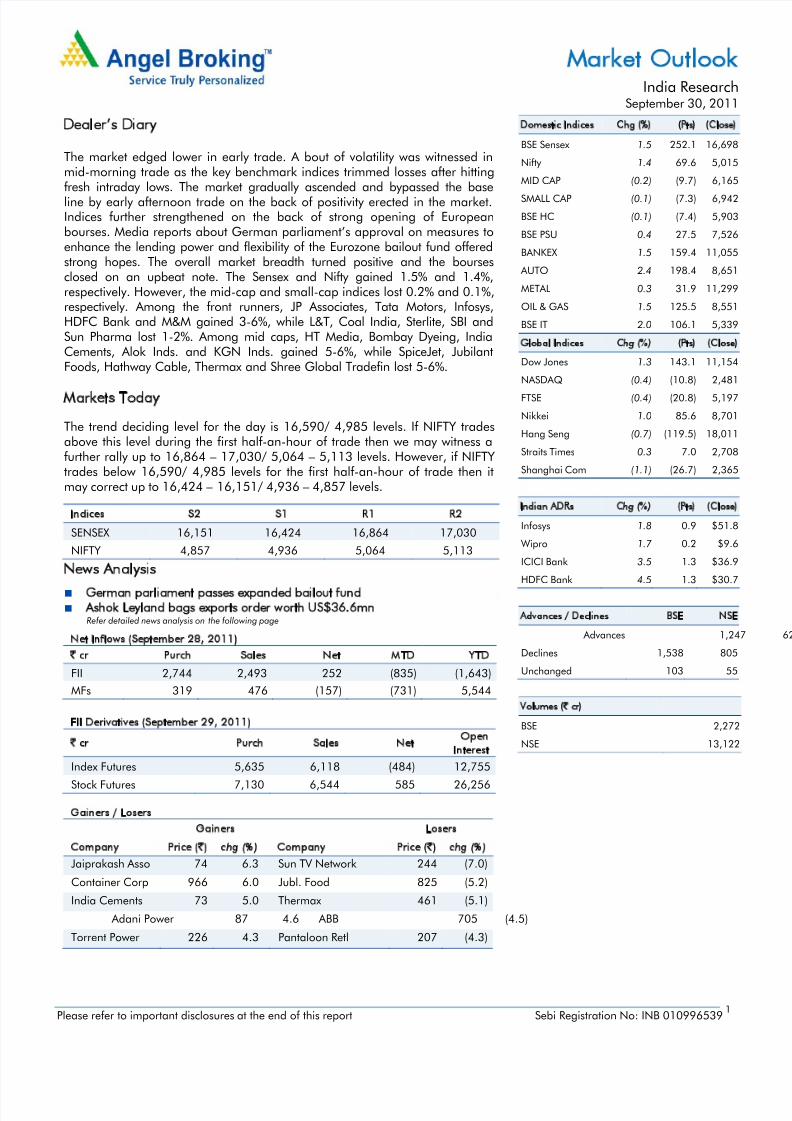

1 Market Outlook India Research September 30, 2011 Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539 Dealer’s Diary The market edged lower in early trade. A bout of volatility was witnessed in mid-morning trade as the key benchmark indices trimmed losses after hitting fresh intraday lows. The market gradually ascended and bypassed the base line by early afternoon trade on the back of positivity erected in the market. Indices further strengthened on the back of strong opening of European bourses. Media reports about German parliament’s approval on measures to enhance the lending power and flexibility of the Eurozone bailout fund offered strong hopes. The overall market breadth turned positive and the bourses closed on an upbeat note. The Sensex and Nifty gained 1.5% and 1.4%, respectively. However, the mid-cap and small-cap indices lost 0.2% and 0.1%, respectively. Among the front runners, JP Associates, Tata Motors, Infosys, HDFC Bank and M&M gained 3-6%, while L&T, Coal India, Sterlite, SBI and Sun Pharma lost 1-2%. Among mid caps, HT Media, Bombay Dyeing, India Cements, Alok Inds. and KGN Inds. gained 5-6%, while SpiceJet, Jubilant Foods, Hathway Cable, Thermax and Shree Global Tradefin lost 5-6%. Markets Today The trend deciding level for the day is 16,590/ 4,985 levels. If NIFTY trades above this level during the first half-an-hour of trade then we may witness a further rally up to 16,864 – 17,030/ 5,064 – 5,113 levels. However, if NIFTY trades below 16,590/ 4,985 levels for the first half-an-hour of trade then it may correct up to 16,424 – 16,151/ 4,936 – 4,857 levels. Indices S2 S1 R1 R2 SENSEX 16,151 16,424 16,864 17,030 NIFTY 4,857 4,936 5,064 5,113 News Analysis German parliament passes expanded bailout fund Ashok Leyland bags exports order worth US$36.6mn Refer detailed news analysis on the following page Net Inflows (September 28, 2011) ` cr Purch Sales Net MTD YTD FII 2,744 2,493 252 (835) (1,643) MFs 319 476 (157) (731) 5,544 FII Derivatives (September 29, 2011) ` crPurch Sales Net Open Interest Index Futures 5,635 6,118 (484) 12,755 Stock Futures 7,130 6,544 585 26,256 Gainers / Losers Gainers Losers Company Price ( `) chg (%) Company Price ( `) chg (%) Jaiprakash Asso 74 6.3 Sun TV Network 244 (7.0) Container Corp 966 6.0 Jubl. Food 825 (5.2) India Cements 73 5.0 Thermax 461 (5.1) Adani Power 87 4.6 ABB 705 (4.5) Torrent Power 226 4.3 Pantaloon Retl 207 (4.3) Domestic Indices Chg (%) (Pts) (Close) BSE Sensex 1.5 252.1 16,698 Nifty1.4 69.6 5,015 MID CAP (0.2) (9.7) 6,165 SMALL CAP (0.1) (7.3) 6,942 BSE HC (0.1) (7.4) 5,903 BSE PSU 0.4 27.5 7,526 BANKEX 1.5 159.4 11,055 AUTO 2.4 198.4 8,651 METAL 0.3 31.9 11,299 OIL & GAS 1.5 125.5 8,551 BSE IT 2.0 106.1 5,339 Global Indices Chg (%) (Pts) (Close) Dow Jones 1.3 143.1 11,154 NASDAQ (0.4) (10.8) 2,481 FTSE (0.4) (20.8) 5,197 Nikkei 1.0 85.6 8,701 Hang Seng (0.7) (119.5) 18,011 Straits Times 0.3 7.0 2,708 Shanghai Com (1.1) (26.7) 2,365 Indian ADRs Chg (%) (Pts) (Close) Infosys 1.8 0.9 $51.8 Wipro 1.7 0.2 $9.6 ICICI Bank 3.5 1.3 $36.9 HDFC Bank 4.5 1.3 $30.7 Advances / Declines BSE NSE Advances 1,247 62 Declines 1,538 805 Unchanged 103 55 Volumes (` cr) BSE 2,272 NSE 13,122

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539

Dealer’s Diary

The market edged lower in early trade. A bout of volatility was witnessed inmid-morning trade as the key benchmark indices trimmed losses after hitting

fresh intraday lows. The market gradually ascended and bypassed the baseline by early afternoon trade on the back of positivity erected in the market.Indices further strengthened on the back of strong opening of Europeanbourses. Media reports about German parliament’s approval on measures toenhance the lending power and flexibility of the Eurozone bailout fund offeredstrong hopes. The overall market breadth turned positive and the boursesclosed on an upbeat note. The Sensex and Nifty gained 1.5% and 1.4%,respectively. However, the mid-cap and small-cap indices lost 0.2% and 0.1%,respectively. Among the front runners, JP Associates, Tata Motors, Infosys,HDFC Bank and M&M gained 3-6%, while L&T, Coal India, Sterlite, SBI andSun Pharma lost 1-2%. Among mid caps, HT Media, Bombay Dyeing, IndiaCements, Alok Inds. and KGN Inds. gained 5-6%, while SpiceJet, Jubilant

Foods, Hathway Cable, Thermax and Shree Global Tradefin lost 5-6%.

Markets Today

The trend deciding level for the day is 16,590/ 4,985 levels. If NIFTY tradesabove this level during the first half-an-hour of trade then we may witness afurther rally up to 16,864 – 17,030/ 5,064 – 5,113 levels. However, if NIFTYtrades below 16,590/ 4,985 levels for the first half-an-hour of trade then itmay correct up to 16,424 – 16,151/ 4,936 – 4,857 levels.

Indices S2 S1 R1 R2

SENSEX 16,151 16,424 16,864 17,030

NIFTY 4,857 4,936 5,064 5,113

News Analysis

German parliament passes expanded bailout fund Ashok Leyland bags exports order worth US$36.6mn

Refer detailed news analysis on the following page

Net Inflows (September 28, 2011)

` cr Purch Sales Net MTD YTD

FII 2,744 2,493 252 (835) (1,643)

MFs 319 476 (157) (731) 5,544

FII Derivatives (September 29, 2011)

` cr Purch Sales NetOpen

Interest

Index Futures 5,635 6,118 (484) 12,755

Stock Futures 7,130 6,544 585 26,256

Gainers / Losers

Gainers Losers

Company Price (`) chg (%) Company Price (`) chg (%)

German lawmakers on Thursday approved an expansion of the euro-area rescue fund’sfirepower, freeing the way for European officials to focus on what next steps may beneeded to stem the debt crisis. Consequently, the size of the European Financial Stability

Fund (EFSF) stands enhanced to €440bn (US$593bn) from €250bn earlier. The lowerhouse of the German parliament passed the measure with 523 votes in favour and 85against, granting the fund powers to buy bonds in secondary markets, enabling bankrecapitalisations and offering precautionary credit lines. It raises Germany’s guarantees to €211bn (US$287bn) from €123bn. The measure will be put to the upper house of theparliament on Friday, where it is expected to be passed.

Ashok Leyland bags exports order worth US$36.6mn

Ashok Leyland (ALL) has bagged an order worth US$36.6mn from the Government ofTanzania to supply 723 trucks, buses and special application vehicles to be executed in thecurrent fiscal year. With the new order, ALL has increased its global footprint and isaggressively expanding its network in the African market. The company has network officesin Nigeria and Ghana in the West; Malawi and Mozambique in the South; and Kenya andTanzania in the East, apart from offices in South Africa and Egypt. ALL’s exportsperformance, which is witnessing strong growth traction, will be further boosted by the neworder. ALL is targeting volume growth of over 20% yoy or ~12,000 units in the exportsmarket for FY2012E and has already achieved volumes of 4,649 units YTD in FY2012. Wemaintain our Buy rating on the stock with a target price of `31.

Economic and Political News

Government to borrow ` 53kcr more, shocks debt markets

New mining law to give ` 10,000cr to 60 tribal districts

2-3% interest relief for exporters likely

Corporate News

Power Grid commissions transmission lines for Mundra UMPP

Reliance Broadcast Network raises ` 1,000cr from QIBs

Coal Ministry asks Neyveli Lignite Corp. to seek board nod for further disinvestment

CNG prices to rise by ` 2/kg this week Source: Economic Times, Business Standard, Business Line, Financial Express, Mint

Research Team Tel: 022-3935 7800 E-mail: [email protected] Website: www.angelbroking.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should makesuch investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment

decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are

those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for

general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or

damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has

not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation

or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited

endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other

reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other

advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to thelatest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may haveinvestment positions in the stocks recommended in this report.

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546