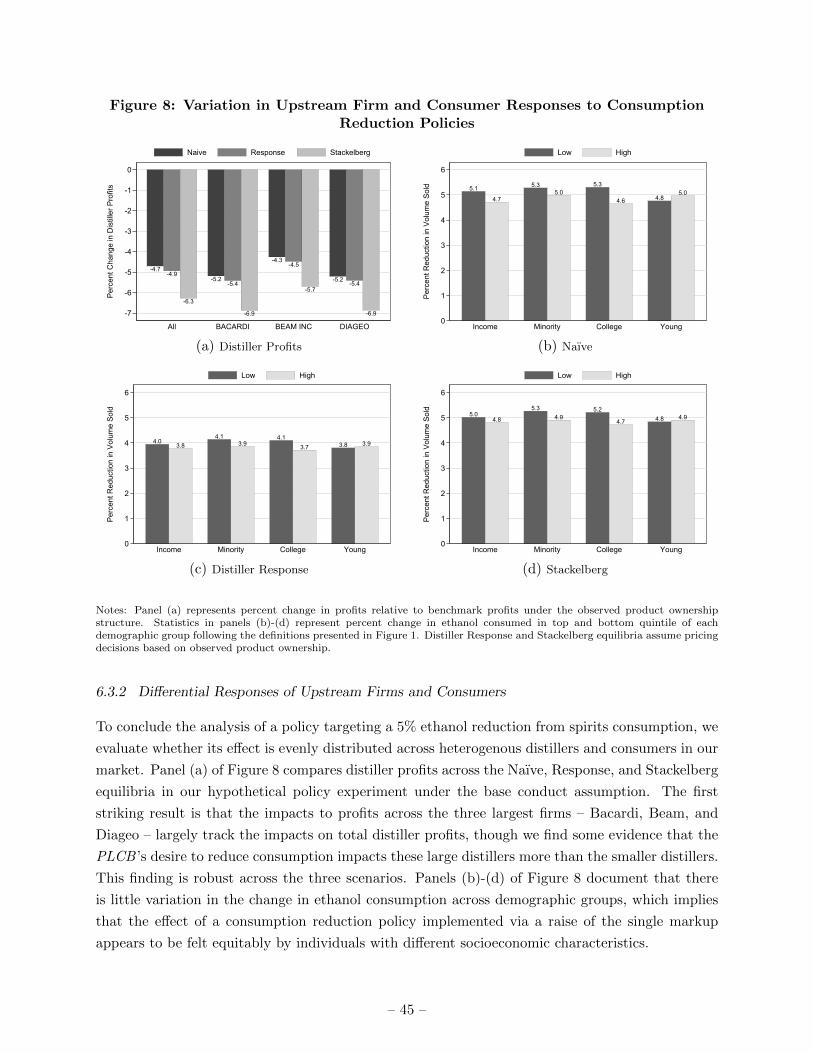

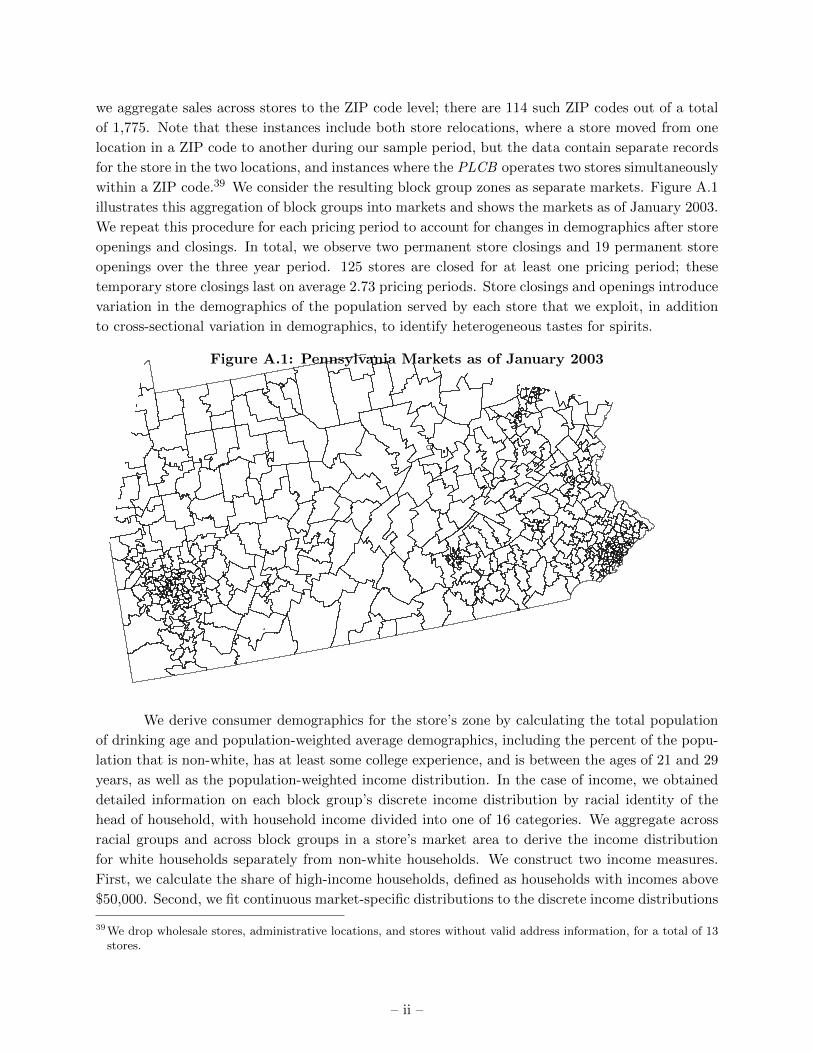

Market Power and the Laffer Curve ? Eugenio J. Miravete † Katja Seim ‡ Jeff Thurk § September 1, 2017 Abstract We characterize the trade-off between consumption tax rates and tax revenue – the Laffer curve – while allowing for re-optimization by both consumers and firms with market power. Using detailed data from Pennsylvania, a state that monopolizes retail sales of alcoholic beverages, we estimate a discrete choice demand model allowing for flexible substitution patterns between products and across demographic groups while not imposing conduct among upstream distillers. We find that current policy overprices spirits and that firms respond to reductions in the state’s ad valorem tax rate by increasing wholesale prices. The upstream response thus limits the state’s revenue gain from lower tax rates to only 14% of the incremental tax revenue predicted under the common assumption of perfect competition. The burden of such na¨ ıve policy falls disproportionately on older, poorer, uneducated, and minority consumers. Upstream collusion exacerbates these effects. Keywords: Laffer Curve, Market Power, Public Monopoly Pricing, Tax Incidence. JEL Codes: L12, L21, L32 ? This paper supersedes an earlier version titled “Complexity, Efficiency, and Fairness of Multi-Product Monopoly Pricing.” We thank the editor, Liran Einav, and three referees for their guidance and thorough reading of our manuscript. We also thank Thomas Krantz at the Pennsylvania Liquor Control Board as well as Jerome Janicki and Mike Ehtesham at the National Alcohol Beverage Control Association for helping us to get access to the data. We are also grateful for comments and suggestions received at several seminar and conference presentations, and in particular to Jeff Campbell, Kenneth Hendricks, and Joel Waldfogel. We are solely responsible for any remaining errors. † The University of Texas at Austin, Department of Economics, 2225 Speedway Stop 3100, Austin, Texas 78712-0301; Centre for Competition Policy/UEA; and CEPR, London, UK. Phone: 512-232-1718. Fax: 512-471-3510. E–mail: [email protected]; http://www.eugeniomiravete.com ‡ Wharton School, University of Pennsylvania, Philadelphia, PA 19104-6372; CEPR and NBER. E–mail: [email protected]; https://bepp.wharton.upenn.edu/profile/712/ § University of Notre Dame, Department of Economics, Notre Dame, IN 46556. E–mail: [email protected]; http://www.nd.edu/ jthurk/

Transcript

Market Power and the Laffer Curve?

Eugenio J. Miravete† Katja Seim‡ Jeff Thurk§

September 1, 2017

Abstract

We characterize the trade-off between consumption tax rates and tax revenue – the Laffer curve

– while allowing for re-optimization by both consumers and firms with market power. Using

detailed data from Pennsylvania, a state that monopolizes retail sales of alcoholic beverages,

we estimate a discrete choice demand model allowing for flexible substitution patterns between

products and across demographic groups while not imposing conduct among upstream distillers.

We find that current policy overprices spirits and that firms respond to reductions in the state’s

ad valorem tax rate by increasing wholesale prices. The upstream response thus limits the

state’s revenue gain from lower tax rates to only 14% of the incremental tax revenue predicted

under the common assumption of perfect competition. The burden of such naıve policy falls

disproportionately on older, poorer, uneducated, and minority consumers. Upstream collusion

exacerbates these effects.

Keywords: Laffer Curve, Market Power, Public Monopoly Pricing, Tax Incidence.

JEL Codes: L12, L21, L32

?

This paper supersedes an earlier version titled “Complexity, Efficiency, and Fairness of Multi-Product MonopolyPricing.” We thank the editor, Liran Einav, and three referees for their guidance and thorough reading of ourmanuscript. We also thank Thomas Krantz at the Pennsylvania Liquor Control Board as well as Jerome Janickiand Mike Ehtesham at the National Alcohol Beverage Control Association for helping us to get access to the data.We are also grateful for comments and suggestions received at several seminar and conference presentations, and inparticular to Jeff Campbell, Kenneth Hendricks, and Joel Waldfogel. We are solely responsible for any remainingerrors.

† The University of Texas at Austin, Department of Economics, 2225 Speedway Stop 3100, Austin, Texas 78712-0301;Centre for Competition Policy/UEA; and CEPR, London, UK. Phone: 512-232-1718. Fax: 512-471-3510. E–mail:[email protected]; http://www.eugeniomiravete.com

‡ Wharton School, University of Pennsylvania, Philadelphia, PA 19104-6372; CEPR and NBER. E–mail:[email protected]; https://bepp.wharton.upenn.edu/profile/712/

§ University of Notre Dame, Department of Economics, Notre Dame, IN 46556. E–mail: [email protected];http://www.nd.edu/ jthurk/

1 Introduction

Economic research rarely achieves the overnight policy influence of the Laffer curve – the famous

inverted U-shape function that relates tax rates and government revenues first scribbled on a napkin

(Wanniski, 1978). The concept proved to be a cornerstone of “Reaganomics”, inspired the 1981

Kemp-Roth tax cuts, and continues to be at the foundation of every discussion of tax reform. And

yet, there exists little quantitative evidence of its underlying economic mechanisms so the Laffer

curve remains more of an ethereal concept rather than an empirically well-understood fundamental.

Our objective is to empirically characterize the determinants of the Laffer curve in the

taxation of consumer goods – an area which accounts for 17.4% government revenues in the United

States and 32.7% of revenues in the average developed country.1 The industrial organization

literature has demonstrated that in many consumer goods categories, ranging from cereals to

icecream, soft drinks, and the alcoholic beverages we study, firms possess significant market power

in pricing, stemming in part from the differentiated nature of the products they offer and the

market segmentation these product offerings facilitate. We therefore build upon earlier work that

uses detailed data to study the Laffer curve via reduced-form estimation under the assumption of

perfect competition among firms (e.g., Auerbach, 1985; Chetty, 2009) to allow firms to respond

strategically in their choice of pre-tax prices to changes in tax policy. Foreshadowing our results,

allowing for the possibility that both consumers and imperfectly competitive firms respond to

changes in tax policy has significant impact on optimal taxation and the characterization of the

Laffer curve.

We first use a simple model of monopoly taxation to explore the equilibrium interactions

between firms and consumers in response to changes in the tax rate. We show that raising excise

tax rates beyond a critical level indeed decreases government revenues under very general demand

conditions and that the shape and location of the Laffer curve depends not only on the tax rate and

consumer demand elasticity but also on the firm’s strategic response. Moreover, we show that the

tax rate and the firm price response are strategic substitutes so the latter mutes the change in retail

price induced by a change in the tax rate. The effectiveness of tax policy therefore depend on the

government’s ability to anticipate the strategic pre-tax price response of the firm to tax changes.

More generally, incorporating the equilibrium response of the firm is vital to making correct policy

recommendations and failing to do so would result in the firm’s price response unraveling, at least

partially, the government’s objective.

We evaluate these predictions empirically within the context of alcohol taxation. The

production, distribution, and sale of alcoholic beverages is the second largest beverage industry in

the United States (behind soft drinks) and an important source of government tax revenues. Using

detailed price and quantity data for 2002-2004 across all retail liquor stores in Pennsylvania, we

estimate the response elasticities of both upstream firms and consumers to the state’s choice of ad

valorem tax rate in the market for distilled spirits – a product category which generated substantial

tax revenue for the state’s general fund and represents the industry’s fastest growing segment.

Several remarkable features of the data enable us to estimate key parameters of the model

rather than impose them ex ante, thereby increasing the reliability of both our demand estimates

and the Laffer curves they generate. First, in Pennsylvania the state monopolizes both the wholesale

and retail distribution of alcoholic beverages and applies a simple pricing rule that translates

wholesale prices into retail prices via a single uniform ad-valorem tax. Thus, upstream distillers

effectively choose retail prices taking into account this tax. Second, as a product’s retail price is

common across the state at any point in time, differences in consumer preferences materialize in

differences in product purchases. This enables us to let consumer tastes vary systematically across

products and demographics leading to more flexible substitution patterns and better estimates of

both consumer demand and upstream market power. It also enables us to evaluate the effects

of tax policy on different consumer groups. Third, the fact that we observe both wholesale and

retail prices enables us to estimate consumer demand without placing any restrictions on upstream

conduct and market power ex ante. Our estimation therefore allows for the possibility that firms

are price-takers and cannot react strategically to changes in policy.

We lever these features to estimate product-level demand for 312 products produced by 37

firms across a variety of consumer types. The combination of robust demand estimates with data

on wholesale prices in a model of oligopoly pricing reveals that upstream firms in the industry enjoy

considerable market power, earning 35 cents in income for every dollar of revenue. To illustrate

the implications of not accounting for the strategic responses of these firms to changes in tax

policy, we compare market equilibria when the state can either perfectly anticipate the distillers’

response to changes in its taxation policy – a Stackelberg equilibrium – or, alternatively, assume that

firms do not respond at all to policy changes, our so-called “naıve” equilibrium. To complete this

counterfactual analysis we also evaluate how the optimal response of upstream firms to tax policy

varies with upstream firm market conduct, ranging from single-product pricing to full collusion,

and how such a wholesale pricing response translates into changes in the shape and position of the

Laffer curve.

We show that market power among firms has a significant effect on the shape of the Laffer

curve. The estimated Laffer curve for a naıve policymaker is steeper than for the policymaker who

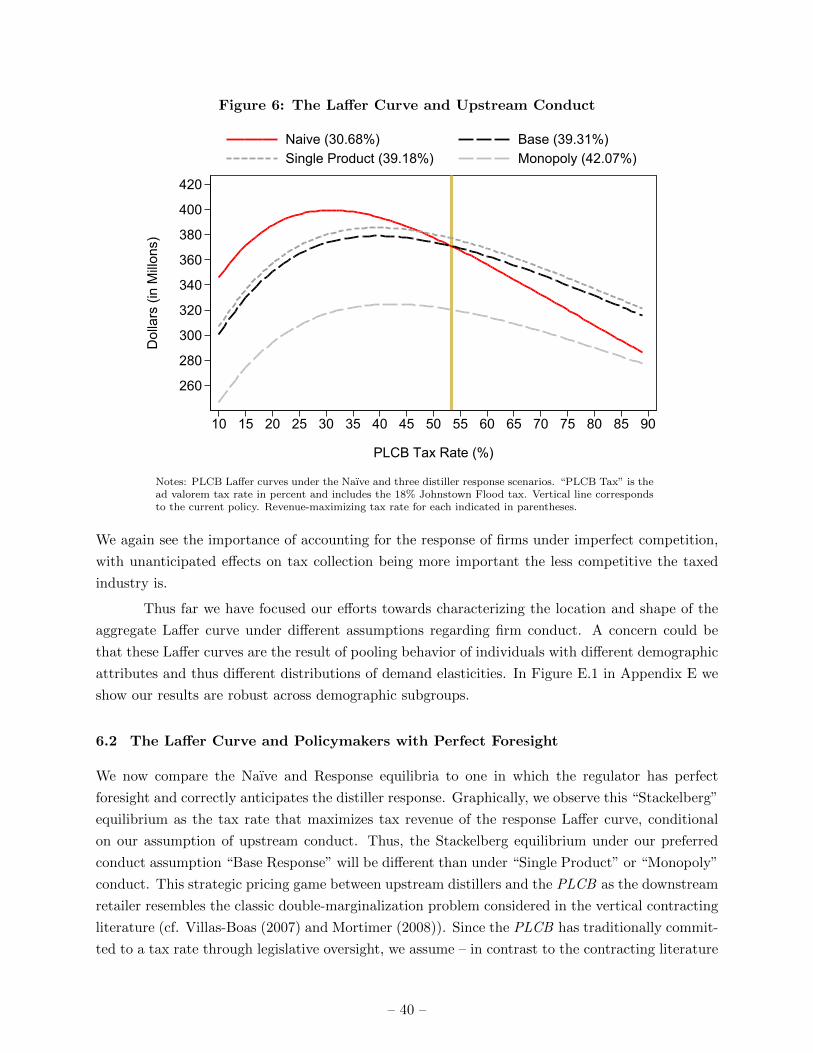

correctly anticipates pre-tax price responses. This is particularly true as conduct among upstream

becomes more collusive. Not accounting for the strategic response of upstream firms, therefore,

leads to poor policy recommendations. For instance, a naıve regulator would have concluded that

the state could increase tax revenues 7.75% (or $28.74 million) by reducing the ad valorem tax

from 53.4% to 30.68%. This reduction in the ad valorem tax would have increased profits for all

upstream firms, but we show that they could do even better by increasing their wholesale prices

by 3.79%, or 34 cents, on average. Thus, the estimated model indicates that upstream prices and

the tax rate are strategic substitutes – a prediction of the simple theoretical model.

– 2 –

While this change in upstream price may appear small, the fact that upstream distillers

price on the elastic region of demand leads to a large change in quantity demanded by consumers.

Ultimately, the firm response enables upstream firms to convert 87% of the incremental tax revenue

into firm profits, or equivalently the response limits the PLCB to attain only 13.8% of the forecasted

incremental revenues ($3.73 million). It is important to note that this substantial undoing of the

state’s revenue objective requires no coordination among firms. Were distillers to collude in setting

wholesale prices, choosing the naıve optimal tax rate leads to a net decrease in tax revenues of

14.18% of current revenue.

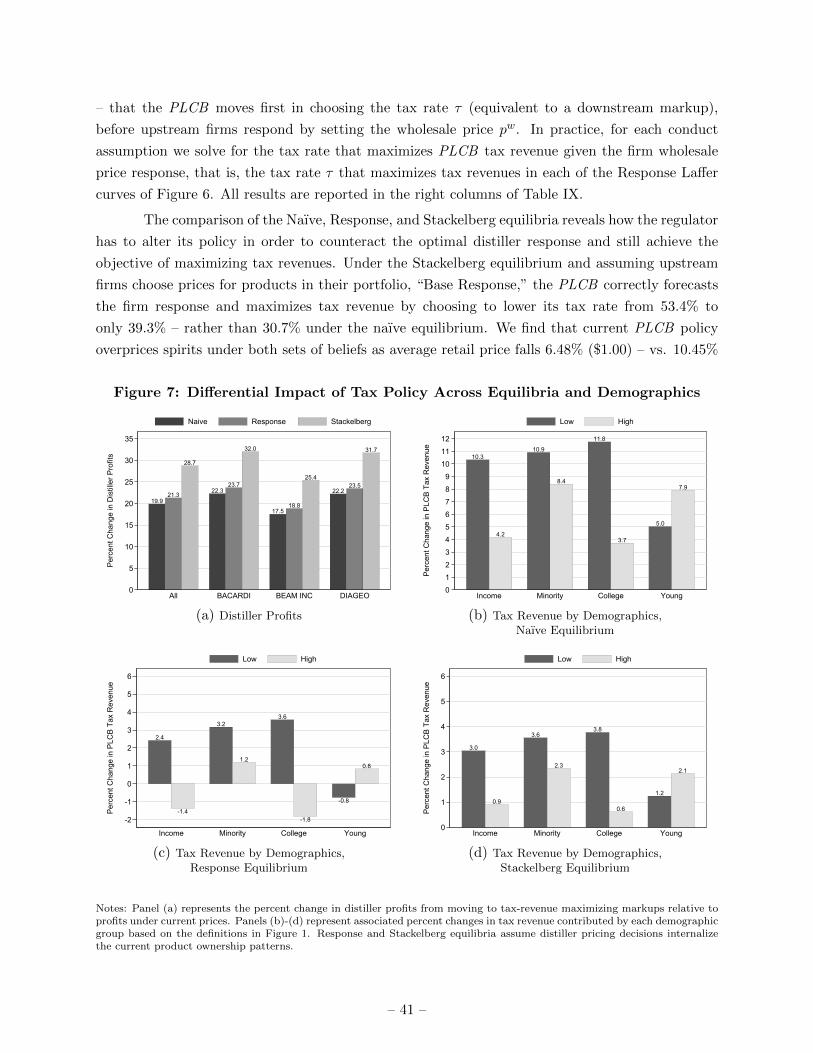

Alternatively, a regulator attempting to maximize tax revenue and endowed with perfect-

foresight would have predicted the upstream response and instead would only decrease the tax rate

to 39.31%, or 42.07% in the event of collusion among upstream firms. While the state does increase

tax revenue roughly two percent, profits among upstream distillers increase 30.8% as does their

share of integrated industry profits (from 29.5% to 34.9%).

Finally, we show that the political ramifications of naıve policy – of assuming perfect compe-

tition among firms – are significant. Not only would such policy be largely ineffective at increasing

tax revenues, but the burden of the tax falls disproportionately on older, poorer, uneducated and

minority consumers. This highlights that the ability of policymakers to account for the responses of

firms and consumers to policies is of significance both from an equity and an efficiency standpoint.

It underscores the importance of recent efforts by, for example, the Congressional Budget Office

to consider Dynamic Scoring of new proposed legislation by accounting for the response of firms,

workers, and consumers to changes in government policy, a direct – albeit delayed – response to

the Lucas Critique. The major handicap then resides in correctly predicting how agents will react

to changes in fiscal policy across different industries.2

1.1 Related Literature

The current paper contributes to several strands of literature, including the characterization of the

Laffer curve, optimal taxation, the analysis of pass-through in non-competitive markets, and the

analysis of alcohol pricing regulation.

Theoretical analysis of the Laffer curve has fallen mostly within the reign of macroeconomics,

which has focused on the possibility of the Laffer curve arising as a result of a general equilibrium

effect induced by taxation on the supply of labor and capital.3 Early empirical attempts such as

Stuart (1981) or Fullerton (1982) build upon static two-sector general equilibrium models where

households allocate their time between taxed labor and non-taxed leisure. Pecorino (2011) adds

a dynamic component as hours worked entail human capital accumulation. Trabandt and Uhlig

(2011) allow for household preference heterogeneity within a neoclassical growth model to generate

2 See the presentation by Wendy Edelberg, the CBO’s Assistant Director for Macroeconomic Analysis, to the FederalReserve Bank of Chicago at https://www.cbo.gov/publication/50730.

3 See Ireland (1994), Novales and Ruiz (2002), or Schmitt-Grohe and Uribe (1997) to name a few.

labor and capital Laffer curves for the U.S. and fourteen European countries assuming calibrated

country-specific Frisch elasticities of labor supply and intertemporal elasticities of substitution.

Relative to this literature we focus on excise taxation with particular attention to the

responses of not only consumers but also suppliers with market power. Consequently within this

literature, our analysis is more related to optimal capital rather than labor taxation. Our results

then indicate that modifications of the capital tax rate could be largely undone by providers of

capital if they have market power – a likely scenario. The advantage of our approach is that we

have detailed industry data that allows us not to impose any restrictions on the model such as a

predetermined objective of the state. As our model generates robust estimates of consumer demand

and upstream market power, this approach increases the reliability of our conclusions.

We show that the existence, shape, and location of the Laffer curve in our context depends

not only on the interaction of the tax rate and consumers’ downstream product demand responses

(via demand elasticities) but also on upstream market power and firms’ strategic pre-tax price

setting. This is a commonly overlooked aspect of the analysis of taxation since the empirical public

finance literature deals primarily with perfectly competitive scenarios despite the well-documented

market power of firms in the studied industries.4 Our data enables us to evaluate this assumption by

drawing a distinction between the mechanical effects of and behavioral responses to taxation (Saez,

2001, §3.2). Specifically, we allow the policymaker to be well aware of downward sloping retail

demands but potentially naıve regarding the upstream firms’ reaction to taxes/pricing regulations.

A comparison of the Laffer curve with this naıve policy design to the one generated by a policymaker

who chooses the tax rate in anticipation of the optimal firm responses (Stackelberg equilibrium)

allows us to evaluate the implications of this assumption. Our results indicate that assuming perfect

competition among firms, i.e., assuming upstream firms cannot respond to changes in policy, has

substantial equilibrium effects on firms, consumers, and overall tax revenue across a variety of

assumptions regarding upstream conduct.5,6

Finally, we are not the first to address the implications of policy in the regulation of

alcoholic beverages. Seim and Waldfogel (2013) evaluate the potential welfare effects of free entry

in Pennsylvania. Aguirregabiria, Ershov and Suzuki (2016) study the case of partial entry in the

wine segment where state-run stores sell side by side with private, yet price regulated, retailers.

Illanes and Moshary (2015) take advantage of the privatization of the alcohol distribution system in

Washington state to evaluate the effect of potential retail entry on pricing and product offering. In

a related paper (Miravete, Seim and Thurk, 2017), we show that current policy is largely consistent

4 For instance, Chetty, Looney and Kroft (2009) and Evans, Ringel and Stech (1999) both assume competitive supplyin the beer and cigarette industries, respectively.

5 Weyl and Fabinger (2013) show the impact of imperfect competition on tax pass-through under a variety of modelenvironments but do not address asymmetric firms with horizontally-differentiated products. Consequently, ourresults provide an empirical extension.

6 There are other papers that address the market conduct in the alcoholic beverage industry. Conlon and Rao (2015)document how the “post and hold” regulation in some states help wholesalers set collusive prices. Miller andWeinberg (2015) use mergers in the brewing industry to identify collusive behavior.

– 4 –

with tax-revenue maximization (versus managing ethanol consumption) and compare the current

uniform policy to a subsidy-free taxation policy with optimal product-specific ad valorem taxes. We

find that the one-size-fits-all policy employed by the state generates significant redistribution within

upstream firms and downstream consumers. Griffith, O’Connell and Smith (2017) evaluate the use

of product-specific corrective taxes to minimize health externalities related to ethanol consumption

under the assumption that all firms, including suppliers and retailers, do not respond. In this paper,

we abstract from modeling the motivation behind the state’s tax code to more clearly illustrate the

key determinants of the tax rate/revenue trade-off and to characterize the shape and location of

the Laffer curve empirically while accounting for re-optimization by both firms and consumers.

1.2 Organization of the Paper

The paper is organized as follows. In Section 2 we provide a simple model of taxation under

imperfect competition to illustrate the key mechanisms underlying our results. In Section 3 we

present the data, discuss the details of the Pennsylvania pricing rule, address the interaction with

the upstream distillers, and document heterogeneous consumption patterns across demographic

groups. In Section 4 we present an equilibrium discrete choice model of demand for horizontally

differentiated spirits. The model allows preferences to be correlated across products of similar

characteristics and incorporates the features of the current pricing regulations while allowing for

(but not imposing) imperfect competition in the upstream distillery market. In Section 5 we discuss

the estimation procedure and how the unique features of our data help identify the rich substitution

patterns across products in our econometric specification. We pay particular attention to dealing

with the potential endogeneity of prices using retail price information from other control states and

variation in input costs. We also show how we use the estimated model to infer upstream market

power among distillers. In Section 6 we show that this market power has significant implications

for the shape and location of the Laffer curve while also documenting the variation in Laffer curves

across consumer types. We conclude and discuss avenues for future research in Section 7. We

include additional data sources, descriptive statistics, robustness of demand estimates, and other

results in the Appendices.

2 A Simple Model of the Laffer Curve Under Market Power

In this section we present a simple model of monopoly excise taxation to provide an economic

framework for the interpretation of our empirical analysis in an oligopolistic environment. Our goal

is to illustrate how a regulator’s tax rate choice affects its tax revenue when allowing for optimal

price responses by taxed firms to changes in policy. We show that tax revenue is not monotonic in

the tax rate and that certain tax rates fall into what Arthur Laffer called the “Prohibitive Range,”

when an increase in the tax rate leads to a reduction in tax revenue. To this end, we investigate how

the optimal pre-tax price responds to a change in the tax rate, and show that whenever demands are

less convex than in the isoelastic case, the pre-tax price and the tax rate are strategic substitutes.

– 5 –

Consider the case of a single product sold by a monopoly supplier and produced at a constant

marginal cost. Focusing on the single-product monopoly case allows us to avoid accounting for

cross-product substitution as the excise tax and tax-inclusive prices change; instead we simply

consider the marginal consumer’s decision to switch between the inside and outside good. Our

empirical analysis in the context of multi-product oligopoly upstream suppliers agrees, nevertheless,

with all predictions of the model. The monopolist chooses the pre-tax price pw (wholesale price

in our empirical context) for a given tax rate τ ≥ 0, which impacts the tax-inclusive price the

consumer pays, pr (retail price),

pr = (1 + τ)pw . (1)

In setting its optimal pre-tax price, the monopolist chooses pw to maximize profits Π(pw) = (pw −c)D(pr), given the retail demand D(pr), constant marginal cost c, and the chosen tax rate τ , which

requires:

D(pr) + (pw − c)D′(pr)(1 + τ) = 0 , (2)

or equivalently, in terms of the Lerner index,

pw − cpw

=−D(pr)

D′(pr)(1 + τ)· 1 + τ

pr=−1

ε(pr). (3)

This inverse-elasticity pricing rule relates the pre-tax (wholesale) markup of the monopolist

to the inverse of the demand elasticity evaluated at the tax-inclusive (retail) price. The monopolist

thus sets the pre-tax price pw so that the tax-inclusive price falls in the elastic region of demand.

This result is behind the optimal pricing response of the taxed firm to changes in the tax rate

shown below. We argue that under general conditions, for any demand that is less convex than an

isoelastic demand function, a tax rate increase induces the non-competitive taxed firm to reduce

its pre-tax price in order to keep the tax-inclusive market price in a region of demand that is not

too elastic. Thus, tax rates and non-competitive firm prices move in opposite directions, i.e., they

are strategic substitutes.

To characterize the monopolist’s optimal price response to a change in tax policy we make

use of the retail price definition in equation (1) and totally differentiate the first order condition in

equation (2) with respect to pw and τ to obtain:

dpw

dτ=−1

1 + τ· (2pw − c)D′(pr) + pr(pw − c)D′′(pr)

2D′(pr) + (pw − c)(1 + τ)D′′(pr). (4)

For convenience we define η(τ) as the elasticity of the monopolist’s optimal pre-tax price to a

change in the tax rate τ . We make use of the inverse-elasticity rule (3) to express the firm’s

optimal response elasticity as

η(τ) ≡ dpw

dτ· τpw

=−1

1 + τ·

(pw − pw

ε(pr)

)D′(pr)− pw×pr

ε(pr) D′′(pr)

2D′(pr)− pr

ε(pr)D′′(pr)

· τpw

. (5)

– 6 –

Further simplification using the retail price definition (1) yields:

η(τ) =−τ

1 + τ·

(1− 1

ε(pr)

)− κ(pr)

2− κ(pr), (6)

where κ(pr) is the curvature of demand given by

κ(pr) =D′′(pr)D(pr)

[D′(pr)]2. (7)

The curvature of demand κ(pr) is the key element that determines the sign of η(τ). We are

interested in characterizing demand conditions under which the pre-tax price response elasticity

η(τ) is negative, given that the firm prices in the elastic region of demand, ε(pr) < −1. We explore

first the case of linear and concave demand followed by somewhat convex demand functions.

It is straightforward to show that η(τ) < 0 in equation (6) under profit-maximizing pricing

with ε(pr) < −1 whenever demand is linear or concave as D′′(pr) ≤ 0 ensures that κ(pr) ≤ 0. Linear

demand is commonly used for algebraic convenience but concave demand is frequently assumed in

theoretical models, see Tirole (1989, §1.1).

There is however a larger set of demand systems that entails the strategic substitutability

of pw and τ . For instance, equation (6) indicates that η(τ) is always negative when κ(pr) ∈ [0, 1)

and the monopolist prices on the elastic region of demand. The curvature condition of κ(pr) < 1

describes the class of log-concave demand functions, including both concave and somewhat con-

vex demand functions.7 Log-concavity characterizes the vast majority of demand specifications

commonly used in economic analysis, including discrete choice models of demand based on Type

I extreme value distributed errors so widely used in empirical work, including ours, e.g., Fabinger

and Weyl (2016, Appendix 3).

Even for demand systems with higher curvature, with κ(pr) ∈ [1, 2), it is possible for η(τ)

to be negative, depending on the relative magnitudes of(1− 1

ε(pr)

)and κ(pr).8 Isoelastic demand, a

popular choice in the macro literature (e.g., Dixit-Stiglitz CES preferences), amounts to a limiting

case as it is straightforward to show that for these demand functions κ(pr) =(

1− 1ε(pr)

)and

thus, η(τ) = 0 according to equation (6). Thus, firms in these models do not alter their pricing

decisions in response to changes in tax policy by assumption. But whenever demand is less convex

than this popular limiting case, we characterize a large and empirically relevant class of demand

specifications where the optimal response of the monopolist to an increase in the tax rate always

is to reduce the pre-tax price, i.e., η(τ) < 0 so that the pre-tax prices and tax rates are strategic

substitutes.

7 If κ(pr) < 1, it follows from the definition of curvature that D′′(pr)D(pr) − [D′(pr)]2 < 0, which is the conditionfor demand to be log-concave.

8 We restrict attention to demand systems with κ < 2 since κ(pr) ∈ [0, 2) ensures that the revenue function R(pr) =prD(pr) is concave in pr, or equivalently, that the marginal revenue function is decreasing, a common demandrestriction in models of imperfect competition.

– 7 –

We can now explore how total tax revenue collected by the government varies as a function

of the tax rate τ when we account for the firm’s optimal price response. The government tax

revenue function is given by

T (τ) = (pr − pw)D(pr) = τpwD((1 + τ)pw

), (8)

where pr and pw are implicit functions of τ , pr(τ) and pw(τ), through the definition of the tax-

inclusive price (1) and the pre-tax price response elasticity (6). The effect of a change in the tax

rate on government tax revenue is

dT (τ)

dτ= pwD(pr) + τpwD′(pr)pw +

dpw

dτ

(τD(pr) + τpwD′(pr)(1 + τ)

)

= pw(D(pr) + τpwD′(pr)

)+ η(τ)pw

(D(pr) + ε(pr)D(pr)

)

= pwD(pr)

[(1 +

τ

1 + τε(pr)

)+ η(τ)

(1 + ε(pr)

)]. (9)

Note that the sign of dT (τ)/dτ is ambiguous and depends on the relative magnitudes of

the tax rate, demand elasticity, and the pre-tax price response elasticity. The prohibitive range of

the Laffer curve arises for a given tax rate τ when the equilibrium price elasticity of demand ε(pr)

and the equilibrium pre-tax price response elasticity η(τ) are such that:

dT (τ)

dτ< 0 ⇐⇒ 1 +

τ

1 + τε(pr) + η(τ)

(1 + ε(pr)

)< 0 . (10)

When are tax, demand, and upstream conduct conditions such that equation (10) is sat-

isfied? We consider first the case of a naıve policymaker who mistakenly believes that – akin to

the case of perfect competition – the monopolist will not modify its pre-tax (wholesale) price in

response to an increase in the ad valorem tax rate τ . When η(τ) = 0, condition (10) will not hold

for sufficiently low τ . However, this condition eventually holds as τ increases by reducing the total

value of sales receipts as higher tax rates push the price pr into a more elastic region of demand

for all demand systems other than the isoelastic limiting case. The macro literature relies on a

similar incentive mechanism to generate a Laffer curve: higher income taxation reduces workers’

labor supply to eventually reduce the labor tax base and income tax revenues. See Trabandt and

Uhlig (2011, Proposition 2).

Rewriting equation (9) when η(τ) = 0 shows that all we require to be on the prohibitive

region of the Laffer curve under a naıve policymaker is that consumer demand is sufficiently elastic

at the tax-inclusive equilibrium price,

ε(pr(τ)) < ε◦(τ) = −1 + τ

τ, (11)

– 8 –

For instance, for a tax rate of 50% (similar to the 53.4% tax charged by the PLCB) to be in the

prohibitive region of the Laffer curve of a naıve policymaker, the demand elasticity ε(pr) at the

corresponding equilibrium tax-inclusive price needs to be lower than ε◦(0.5) = −3 (a value that

many of our demand estimates exceed). The higher the tax rate and thus final retail prices, the less

elastic demand needs to be to reach the prohibitive range of the Laffer curve. Thus, tax revenue will

fall if a naıve policymaker increased taxes from a starting tax rate of 70% and the good’s demand

elasticity at the equilibrium price is at least ε(pr) < ε◦(0.7) = −2.43. Conversely, for many, more

moderate, taxation schemes, such as sales taxes, which in the U.S. across states reach only 9.45%

in 2015, demand for the affected products is unlikely to be sufficiently elastic for the observed tax

rates to be near or beyond the peak of the Laffer curve.9

To complete the analysis we compare the features of the Laffer curve for a naıve policymaker

described above with that of a policymaker with perfect foresight, capable of anticipating how the

monopolist re-optimizes its pricing decision after a change of the tax rate. Substituting (6) for η(τ)

in condition (10), the prohibitive range of the Laffer curve arises when

2− κ(pr) + 2τ

τ+ ε(pr) +

1

ε(pr)< 0 . (12)

For this inequality to hold over the elastic range of demand, ε < −1, it suffices that

ε(pr) < ε?(τ, κ) = −2− κ(pr) + τ

τ. (13)

How does the implicit relationship between the tax rate and the elasticity of demand that entails

a tax rate beyond tax revenue maximizing levels compare to the above, when η(τ) = 0? A general

comparison is dependent on the chosen demand system, which dictates a choice of κ(pr) and ε(pr).

However, when demand is log-concave and κ(pr) ∈ [0, 1), as in our empirical setting, we can show

that for any given tax rate τ :

ε?(τ, κ) = −2− κ(pr) + τ

τ< −1 + τ

τ= ε◦(τ) . (14)

When allowing for a strategic response by the monopolist to chosen tax rates, demand at tax-

inclusive retail prices thus needs to be more elastic than under the naıve scenario for any particular

tax rate to push tax revenues down the slippery slope of the Laffer curve. For example, for the above

tax rate of 50% to be in the prohibitive region for a policymaker with perfect foresight, demand

at the resulting tax-inclusive prices needs to be more elastic than −5 or −4 for κ(τ) equal to 0 or

0.5, respectively. This compares to the above critical value for the elasticity of −3 when η(τ) = 0.

For a given tax rate, the difference between the elasticity cutoff values for the perfect foresight and

naıve cases converges to zero as demand becomes more convex, reflecting that ε?(τ, κ)→ ε◦(τ) as

κ(pr)→ 1, and is highest when demand is linear and κ(pr) = 0.

9 See https://taxfoundation.org/state-and-local-sales-tax-rates-2015/. A rate of τ = 10% falls beyond thepeak of the Laffer curve if the demand elasticity at tax inclusive prices would need to be smaller than −11.

The flip side of this result is that a policymaker with perfect foresight may need to set a

higher tax rate to maximize tax revenues when compensating for the reduction in pre-tax price by

the monopolist, η(τ) < 0, than the naıve policymaker would have chosen. Expressing equation (14)

in terms of the optimal tax rate that maximizes tax revenue given the demand responsiveness at

the tax-inclusive prices, we have that

τ?(ε, κ) = −2− κ(pr)

1 + ε(pr)> − 1

1 + ε(pr)= τ◦(ε(pr)) (15)

Note that τ◦(ε) is not necessarily equal to τ◦(ε), the tax revenue maximizing tax rate for

the naıve policymaker, since the demand elasticities are evaluated at different tax-inclusive retail

prices, pr = (1 + τ?)pw in the case of the sophisticated policymaker and pr = (1 + τ◦)pw for the

naıve case. Locally, with small changes in the tax-inclusive retail price, however, and supported

by the empirical evidence we present below, the difference between τ◦(ε) and τ◦(ε) is sufficiently

small that τ?(ε, κ) > τ◦(ε(pr)).

Moving from the naıve scenario, η(τ) = 0, to one where the policymaker has perfect

foresight, η(τ) < 0, not only tends to shift the Laffer curve to the right, but also makes it flatter.

This is evident when inspecting the last term in equation (9), η(τ)(1+ε(pr)

)> 0, which equals zero

in the naıve scenario. This is the case because of the strategic substitutability of the tax rate and

wholesale prices, η(τ) < 0, under perfect foresight and the monopolist’s optimal pre-tax pricing on

the elastic region of demand, 1 + ε(pr) < 0. Thus, the stronger the firm response, the flatter the

slope of the Laffer curve becomes.

In summary, the theoretical model suggests that the downward sloping part of the Laffer

curve arises if demand is sufficiently elastic relative to the tax rate and the elasticity of the pricing

response of the taxed firm to changes in the tax policy. Even for the monopoly case, empirical

analysis is needed to determine the elasticity of demand under alternative tax-inclusive prices and

characterize the effective tax revenue function. Similarly, accounting for the firm’s price response

to excise taxation, which implies a possible shift and flattening of the Laffer curve relationship

between tax rates and revenue, requires estimates of firm market power via η(τ) and the slope of

consumer demand via ε(pr). Our analysis of PLCB pricing of spirits allows us to empirically assess

the necessary equilibrium responses of upstream firms and consumers.

This analysis could be extended to various homogeneous good oligopoly models along the

lines of the framework for analyzing tax incidence put forward by Weyl and Fabinger (2013). In our

context, however, the PLCB deals with horizontally-differentiated products for which theoretical

results do not exist, e.g., Fabinger and Weyl (2016, Appendix E). The main difficulty in evaluating

the effect of a tax rate increase in this context is that it not only induces substitution to the outside

option but also to other products that are taxed and therefore also generate tax revenues. In

consequence, addressing our research objective requires evaluating the determinants of the Laffer

curve empirically, accounting for the fact that the overall change in tax revenue after a change in the

tax rate reflects unequally induced changes in product sales due to heterogeneity in product costs

– 10 –

and characteristics. Further, firms and consumers can respond differently to a tax rate change based

on differences in market power and heterogeneous preferences, respectively. We account for these

effects empirically in characterizing the Laffer curve across not just one, but all spirits products,

both in aggregate and for different consumer types. In doing so, we are particularly interested in

comparing the tax revenue expected by a naıve regulator who mistakenly neglects the ability of

firms to re-optimize after a tax change, η(τ) = 0, to that realized by a policymaker who correctly

anticipates firm responses to its actions, η(τ) < 0.

3 PLCB Pricing and Sales Data

In this section we describe our data and institutional details that inform our theoretical modeling

and econometric specification. We first describe the data we obtained from the state of Pennsylvania

and other sources on the sales, prices, and characteristics of all products sold through the state-run

network of stores. We then summarize Pennsylvania’s current pricing regulations of alcoholic bev-

erages. We document how upstream firms’ pricing is constrained by rules regarding the frequency

and duration of temporary wholesale price adjustments. The fact that distillers need to decide far

in advance when to put their products on sale temporarily significantly reduces the endogeneity

concerns common in the estimation of models of demand for differentiated products. Next, we

explore the nature of competition in the upstream distiller market that mitigates the effectiveness of

any tax/pricing policy adopted by the PLCB . Finally, we document the heterogeneity of consumer

preferences for different types of spirits, a key source of identification in our empirical strategy.

3.1 Data: Quantities Sold, Prices, and Characteristics of Spirits

We obtained store-level panel data from the Pennsylvania Liquor Control Board (PLCB) under

the Pennsylvania Right-to-Know Law. The data contain daily information on quantities sold and

gross receipts at the UPC and store level for all spirits and wines carried by the PLCB from 2002

to 2004. We chose this sample because there were no mergers or acquisitions of relevance in the

upstream distiller industry segment resulting in a stable competitive environment. As a result,

pricing follows the “normal” pattern contemplated in the PLCB ’s rules. In addition, we received

information on the wholesale price of each product. These wholesale prices are constant across

stores, but vary over time according to well defined pricing periods.

As of January of 2003, the PLCB operated a system of 593 state-run retail stores spread

across the state.10 We combine sales of stores in the same zip code and drop several wholesale and

outlet stores, resulting in a total of 456 local markets. We then match combined store purchases with

consumer demographics by linking store locations with data on local population and demographic

characteristics using the 2000 Census. The PLCB opened and closed several stores over the time

10See Seim and Waldfogel (2013, §2) for a detailed account of the welfare losses induced by the very limited entryallowed in the wine and spirit segment of the Pennsylvania market. Pennsylvania also has a private system for thesale of beer, allowing the controlled entry of private retailers.

– 11 –

period of our sample. We take these entry/exit decisions as exogenous shifts in the demographic

composition of the potential pool of customers of each store. This feature of the data helps in

identifying the demographic interactions in our estimated model.11

Each store carries a multitude of wine and spirit products. We focus on the spirits category

as it represents a majority of PLCB off-premise sales, 60.8% of store revenue. These products

further constitute a well-defined and mature product category that can be described by few, easily

measurable product characteristics, including the type of spirit, the alcohol content, whether or not

a fruit or other flavor is added, and whether or not the product is imported.12

We further focus on sales of popular 375 ml, 750 ml, and 1.75 L bottles of products in the

spirits category, representing 80.9% of total spirit category sales by volume and 91.6% by revenue.

The resulting sample exhibits a long right tail common to consumer goods, where many products

are available to consumers but are rarely purchased. We therefore restrict the sample to only include

the most popular products in each bottle size, spirit type pairing. Consequently, a 750 ml bottle of

E&J Brandy (average retail price of $9.95) is in our final sample while a 750 ml bottle Remy Martin

Louis XIII Cognac (average retail price of $1,078) is not.13 Our final sample consists of 3,377,659

observations of market and time-period level purchases of 312 products that span brandy, cordials,

gin, rum, vodka, and whiskey for three bottle sizes. The final sample represents 56.8% and 63.2%

of the total off-premise bottle sales and revenue from spirits, respectively.

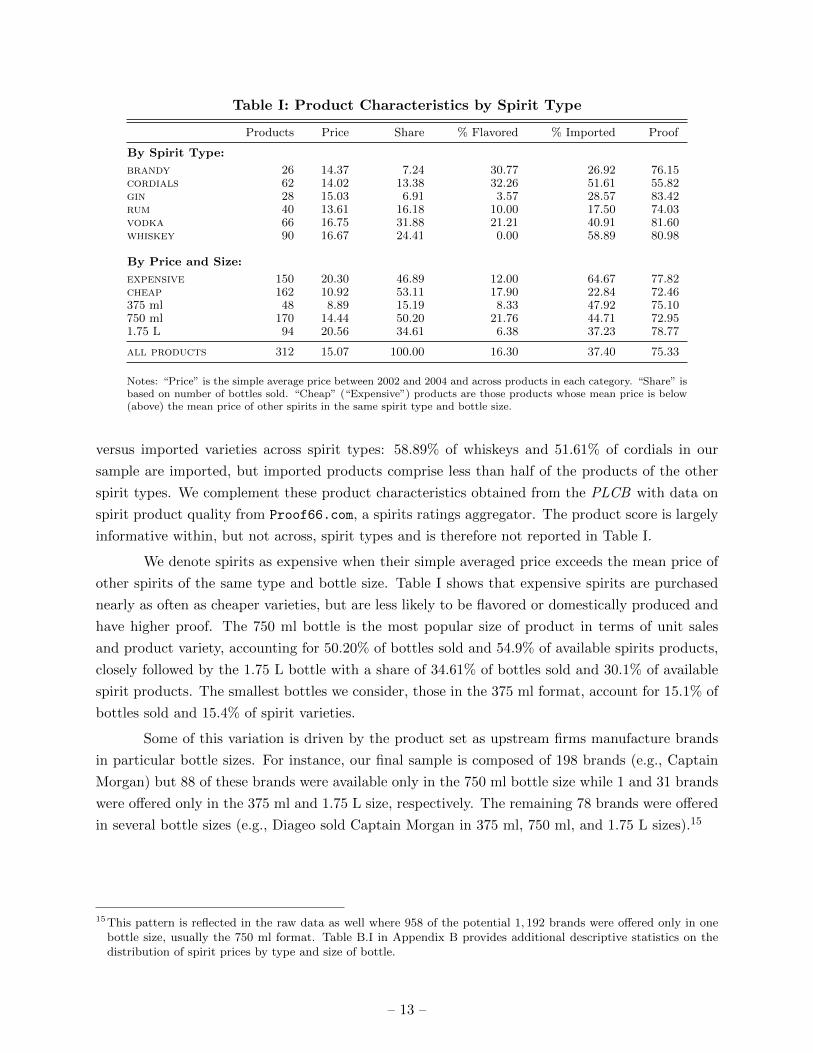

Table I reports the average characteristics of products in our sample. The average proof

is 75.33; 37.40% of products are imported; and 16.3% of products contain flavor add-ins.14 Table

I summarizes these product characteristics further by type of spirit. Vodkas and whiskeys have

significantly larger market shares (31.88% and 24.41%, respectively) than rum (16.18%), cordials

(13.38%), brandy (7.24%), or gin (6.91%). The differences in product variety within each category

mirror the differences in market shares, with only approximately one half as many brandy and

gin varieties as vodkas while 28.9% of the products are whiskeys. Flavored products are primarily

cordials and brandies and to a lesser extent vodkas and rums. We also see variation in domestic

11Appendix A describes how we assign Census block groups to their closest store and how we deal with store openingsand closings, and provides detail on the construction of the demographic variables. We also document that thelarge majority of spirits are sold at every store; this alleviates concerns about assortment differences between storesleading to potential competition for consumers between stores.

12This contrasts favorably with wines whose quality determinants are mostly unobserved, with a large number ofproducts with limited life cycles. This leads to tiny, highly volatile market shares of wines with frequent entry andexit of products of different vintages. For example, within the popular 750 ml bottle category, the top-100 sellingwines (out of 4,675) constitute 45% of total 750 ml wine revenue.

13We define popular products as the highest selling products that together account for 80% of total off-premise spiritsales of a bottle size, spirit type pair. By this definition, a 375 ml bottle of Captain Morgan could theoretically beexcluded from the sample, if it sales rank among 375 ml bottles is too low, while the 750 ml and 1.75 L versionsare included. In practice this did not occur. We also drop the Tequila segment as it accounts for few products.Together, these two restrictions allow us to drop a total of 1,240 products from our sample.

14 In 16th century England, if a pellet of gunpowder soaked in a spirit could still burn determined whether the spiritwas “proof” and thus taxed at a higher rate. Only if the alcohol by volume in rum exceeds 57.15% will gunpowderignite. To simplify, since 1848 in the U.S., a 100 proof corresponds to a spirit with 50% alcohol by volume content.See Jensen (2004).

Notes: “Price” is the simple average price between 2002 and 2004 and across products in each category. “Share” isbased on number of bottles sold. “Cheap” (“Expensive”) products are those products whose mean price is below(above) the mean price of other spirits in the same spirit type and bottle size.

versus imported varieties across spirit types: 58.89% of whiskeys and 51.61% of cordials in our

sample are imported, but imported products comprise less than half of the products of the other

spirit types. We complement these product characteristics obtained from the PLCB with data on

spirit product quality from Proof66.com, a spirits ratings aggregator. The product score is largely

informative within, but not across, spirit types and is therefore not reported in Table I.

We denote spirits as expensive when their simple averaged price exceeds the mean price of

other spirits of the same type and bottle size. Table I shows that expensive spirits are purchased

nearly as often as cheaper varieties, but are less likely to be flavored or domestically produced and

have higher proof. The 750 ml bottle is the most popular size of product in terms of unit sales

and product variety, accounting for 50.20% of bottles sold and 54.9% of available spirits products,

closely followed by the 1.75 L bottle with a share of 34.61% of bottles sold and 30.1% of available

spirit products. The smallest bottles we consider, those in the 375 ml format, account for 15.1% of

bottles sold and 15.4% of spirit varieties.

Some of this variation is driven by the product set as upstream firms manufacture brands

in particular bottle sizes. For instance, our final sample is composed of 198 brands (e.g., Captain

Morgan) but 88 of these brands were available only in the 750 ml bottle size while 1 and 31 brands

were offered only in the 375 ml and 1.75 L size, respectively. The remaining 78 brands were offered

in several bottle sizes (e.g., Diageo sold Captain Morgan in 375 ml, 750 ml, and 1.75 L sizes).15

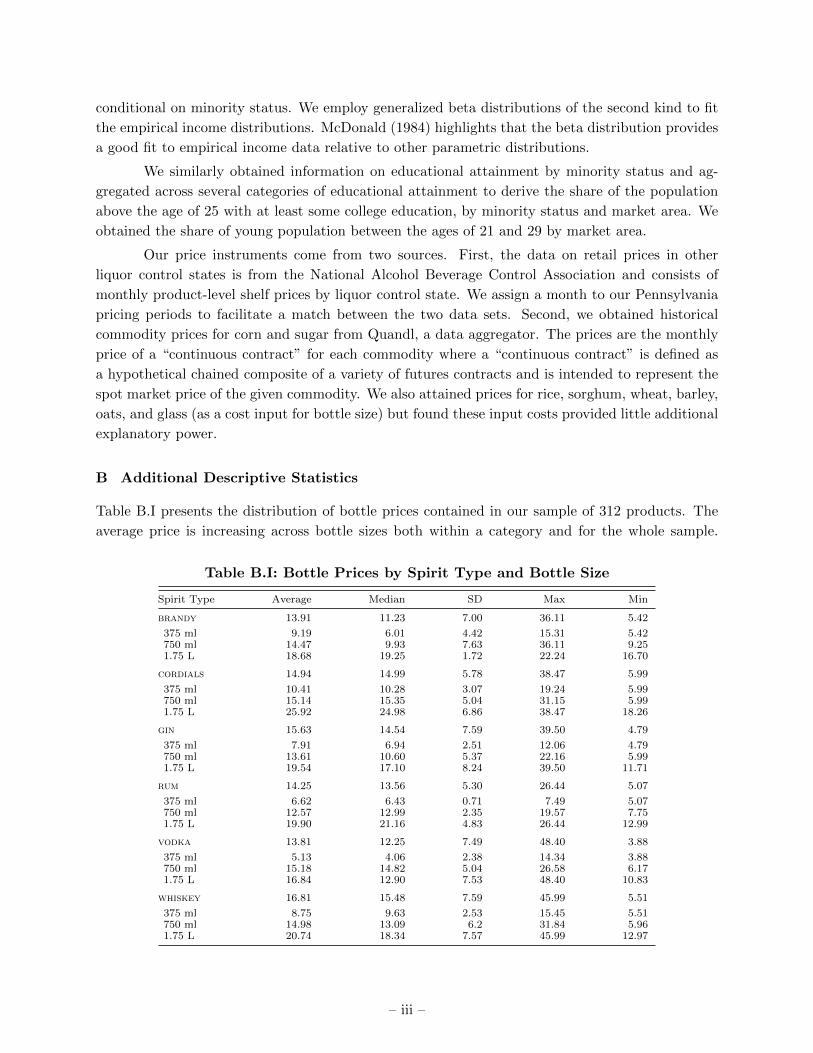

15This pattern is reflected in the raw data as well where 958 of the potential 1, 192 brands were offered only in onebottle size, usually the 750 ml format. Table B.I in Appendix B provides additional descriptive statistics on thedistribution of spirit prices by type and size of bottle.

The PLCB acts as a monopolist in the retail distribution of wine and spirits where the Pennsylvania

State Legislature exerts regulatory oversight over several aspects of the daily operations of the

stores. Most notably, as per the Pennsylvania Liquor Code (47 P.S. §1-101 et seq.) and the

Pennsylvania Code Title 40, the legislature imposes a uniform markup rule upon the retail prices

the PLCB charges both across products and across stores. Prices of spirits are thus identical across

the state at a point in time and follow a common pricing/taxation rule known to all consumers and

upstream manufacturers.

This rule has been modified only infrequently over the years. From 1937 until 1980, the

retail price for all products was based on a 55% markup over wholesale cost for all gins and whiskeys

and 60% markup for other spirits. In 1980, the markup was reduced to 25% for all products and

a per-unit handling fee, the Logistics, Transportation, and Merchandise Factor (LTMF ), of $0.81

was introduced and later increased to $0.85 in 1982. The agency instituted the current 30% markup

in 1993 when it also modified the unit fee to vary by bottle size to better reflect transportation

costs from the PLCB ’s centralized warehouses to the retail stores. The LTMF unit fee for the

375 ml, 750 ml, and 1.75 L bottles in our sample amounts to $1.05, $1.20, and $1.55, respectively.

For the average product, the LTMF fee accounts for 26.7% of the final retail markup. In addition,

consumers also have to pay an 18% sales tax, the “Johnstown Flood Tax,” on all liquor purchases.16

Accordingly, the retail price pr of a given product with wholesale price, pw, is calculated as:17

pr = [pw × 1.30 + LTMF ]× 1.18 . (16)

Of primary concern for this paper is the uniform markup, an ad valorem tax, applied to all products,

amounting to (1.30× 1.18− 1), or 53.4%.

The PLCB has limited ability to depart from this uniform percent markup rule. It operates

seven outlet stores close to the state’s borders, in an effort to address any border bleed of consumers

who illegally import lower-priced products into Pennsylvania from neighboring states. While these

stores offer wines and spirits at discounted prices, the PLCB remains within the uniform markup

policy by selling products in the outlet stores not found in regular stores, for example multi-packs

or unusual bottle sizes for a particular product. Controlling for these stores has little qualitative

or quantitative effects on our results. Related robustness checks are reported in Appendix C.1.

The PLCB purchase bottles of spirits directly from upstream distillers at wholesale prices

pw. Because of the legislated pricing formula, retail price pr is driven by the wholesale pricing

decisions pw of the PLCB ’s suppliers and any change in the wholesale price results in a change

to the retail price passed on to consumers. A new product’s wholesale price remains fixed for

16The original 10% tax was instituted in 1936 to provide $41 million for the rebuilding of the flood-ravaged town ofJohnstown. Despite reaching the funding goal after the initial six years, the tax was never repealed, but insteadrose twice to 15% in 1963 and to 18% in 1968.

17An additional 6% sales tax is then applied to the posted price to generate the final price paid by the consumer.

– 14 –

one year after its introduction. For mature products, distillers can modify the wholesale price they

charge the PLCB at set intervals called “pricing periods” which last four or five weeks and typically

coincide with the month of year. We can therefore aggregate daily data on prices and quantity

sold to the level of these pricing intervals without concern of introducing aggregation bias into our

demand estimates – a useful aspect of our data.

The PLCB places some limitations on how often distillers can change the wholesale price for

mature products. Temporary wholesale price changes, typically price reductions or sales, amount

to 84.8% of price changes in our sample. Distillers can temporarily adjust their wholesale prices up

to four times a year, or once per quarter, but need to submit such proposed price changes to the

PLCB at least five months before the start of the promotion. A product can thus go on sale for

one month, but not for two in a row.

Upstream firms can also permanently change the wholesale price of a product, i.e., a change

in the reference price for temporary price changes. A permanent price change takes place at the

beginning of four-week long reporting periods which, for accounting purposes, occur at a slightly

different periodicity than the pricing periods. These price changes are instituted at the beginning

of the quarter’s first full reporting period, with some discretion on the part of the PLCB as to

the choice of actual reporting period. There is a time lag, however: distillers have to submit the

request for a permanent price increase by the start of the previous quarter. Permanent wholesale

price decreases may be submitted at any time and take effect at the beginning of the next period.

We discuss the periodicity of the price series further in Appendix A. The pricing periods we use

in our analysis below follow the periodicity of sales, resulting in 34 periods from 2002 to 2004.

Note that the delay between the request and effectiveness of either permanent or temporary price

adjustments limits the ability of the distillers to respond to temporary demand shocks – an issue

we revisit when discussing price endogeneity concerns in Section 5.

Table II: Percent of Products Placed on Sale Over the Year

all products 48.40 50.00 46.15 39.42 46.47 65.31 2.34

Notes: “Cheap” (“Expensive”) products are those products whose mean price is below (above) the mean price ofother spirits in the same spirit type and bottle size. We define the “Holiday” season as the two pricing periods thatencompass Thanksgiving through the end of the year. Statistics reflect the percent of products with a temporaryprice reduction during the corresponding season except for “Times,” which denotes the average number of timesthat spirits in each category are on sale during a year.

– 15 –

Table II presents descriptive statistics for changes in temporary price. First, distillers

temporarily change a product’s price 2.3 times a year on average. While not all products experience

a temporary price change, the majority do; 65.31% of spirits are on sale at least once in a given

year. This is true across spirit types, with distillers changing the price of vodkas, expensive varieties,

and all but the largest bottles more frequently than the rest. There is also a seasonal pattern of

price changes across spirit types as distillers are more likely to change a product’s price during

the Summer and less likely during the Winter. Over the holidays, defined as pricing periods that

overlap with Thanksgiving through the end of the year, distillers place 46.47% of our spirit products,

ranging from 34.62% of brandies to 53.33% of whiskeys, on sale at least once, but change the price

of 375 ml bottles rarely. The combination of variation in monthly price changes, both temporary

and permanent, and differences in the amount of the price changes is the primary source of price

variation that we exploit in the estimation of our demand model.

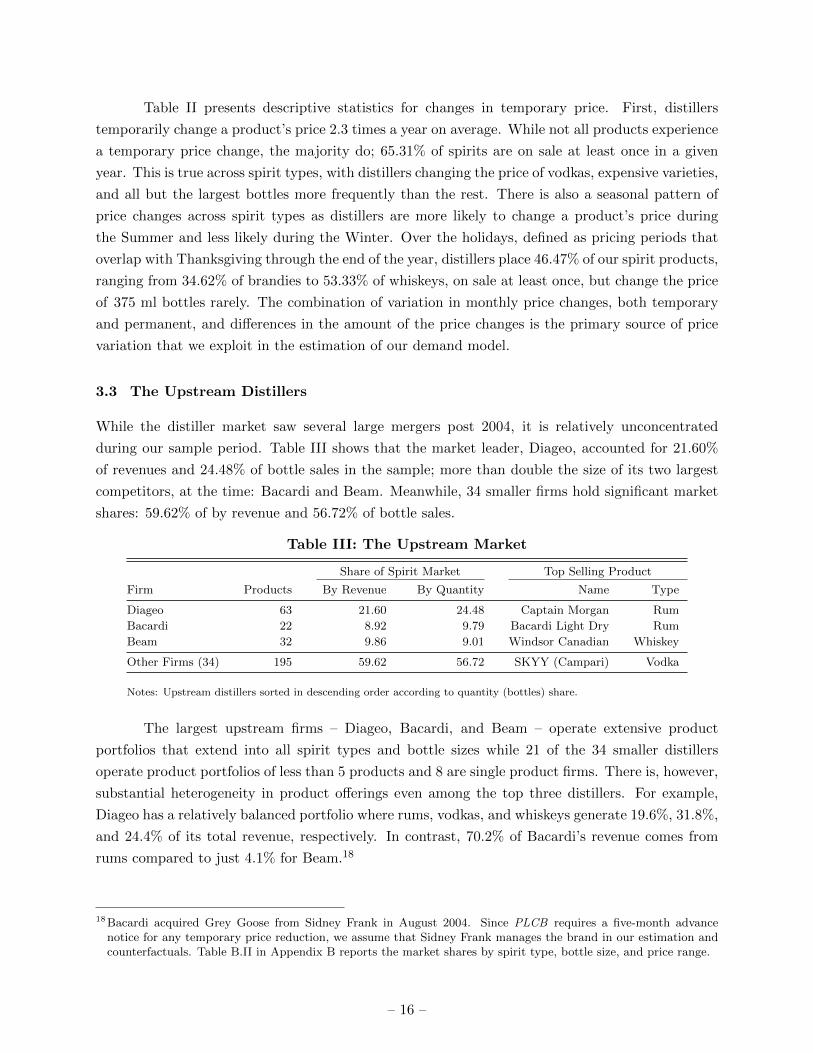

3.3 The Upstream Distillers

While the distiller market saw several large mergers post 2004, it is relatively unconcentrated

during our sample period. Table III shows that the market leader, Diageo, accounted for 21.60%

of revenues and 24.48% of bottle sales in the sample; more than double the size of its two largest

competitors, at the time: Bacardi and Beam. Meanwhile, 34 smaller firms hold significant market

shares: 59.62% of by revenue and 56.72% of bottle sales.

Table III: The Upstream Market

Share of Spirit Market Top Selling Product

Firm Products By Revenue By Quantity Name Type

Diageo 63 21.60 24.48 Captain Morgan Rum

Bacardi 22 8.92 9.79 Bacardi Light Dry Rum

Beam 32 9.86 9.01 Windsor Canadian Whiskey

Other Firms (34) 195 59.62 56.72 SKYY (Campari) Vodka

Notes: Upstream distillers sorted in descending order according to quantity (bottles) share.

The largest upstream firms – Diageo, Bacardi, and Beam – operate extensive product

portfolios that extend into all spirit types and bottle sizes while 21 of the 34 smaller distillers

operate product portfolios of less than 5 products and 8 are single product firms. There is, however,

substantial heterogeneity in product offerings even among the top three distillers. For example,

Diageo has a relatively balanced portfolio where rums, vodkas, and whiskeys generate 19.6%, 31.8%,

and 24.4% of its total revenue, respectively. In contrast, 70.2% of Bacardi’s revenue comes from

rums compared to just 4.1% for Beam.18

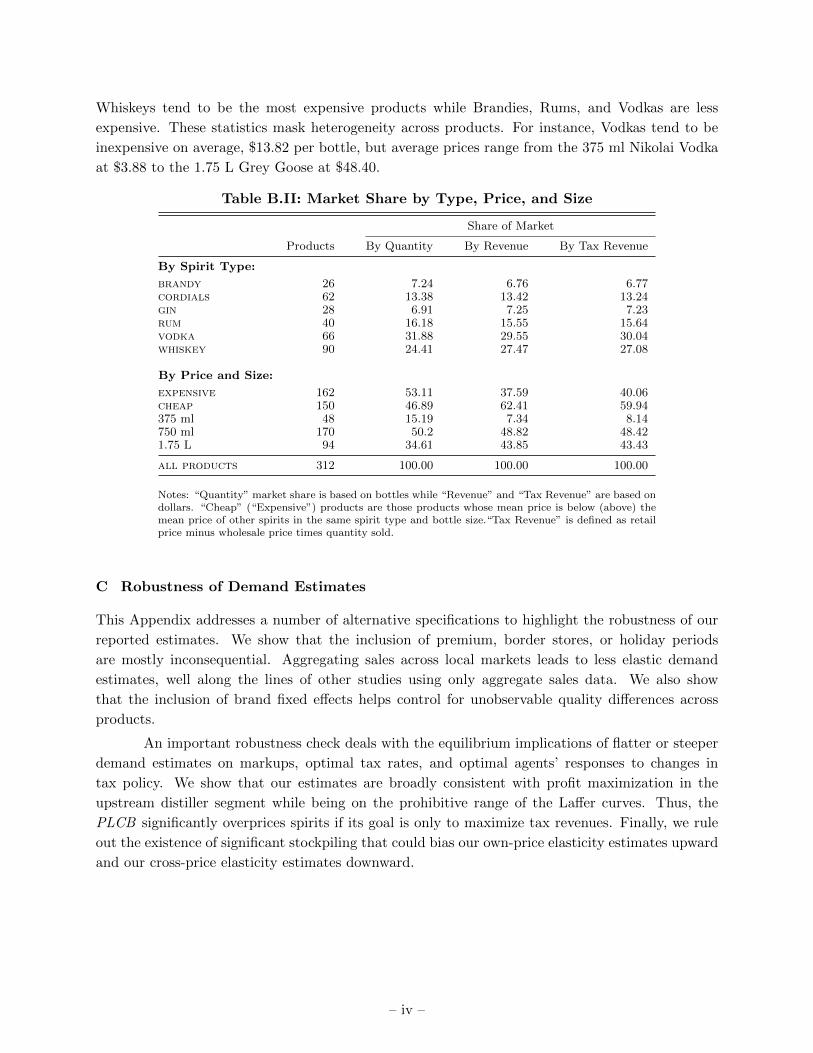

18Bacardi acquired Grey Goose from Sidney Frank in August 2004. Since PLCB requires a five-month advancenotice for any temporary price reduction, we assume that Sidney Frank manages the brand in our estimation andcounterfactuals. Table B.II in Appendix B reports the market shares by spirit type, bottle size, and price range.

– 16 –

While the overall market appears competitive with a Herfindahl-Hirschman Index (HHI)

based on bottle sales of only 930.3, distillers may have more market power within some regions

of the product space than others. For example, the HHI is approximately 3,000 for rums, while

the brandy and gin segments are moderately concentrated with HHIs of approximately 2,000.

The cordial, vodka, and whiskey segments have low concentration measures (all less than 1,400)

suggesting these segments are the most competitive. Horizontal differentiation of products within

a spirit class would provide further market power. An accurate characterization of the response

of distillers to changes in government tax policy therefore requires estimation of rich substitution

patterns underlying demand that motivates the observed extent of differentiation across and within

these different product segments.

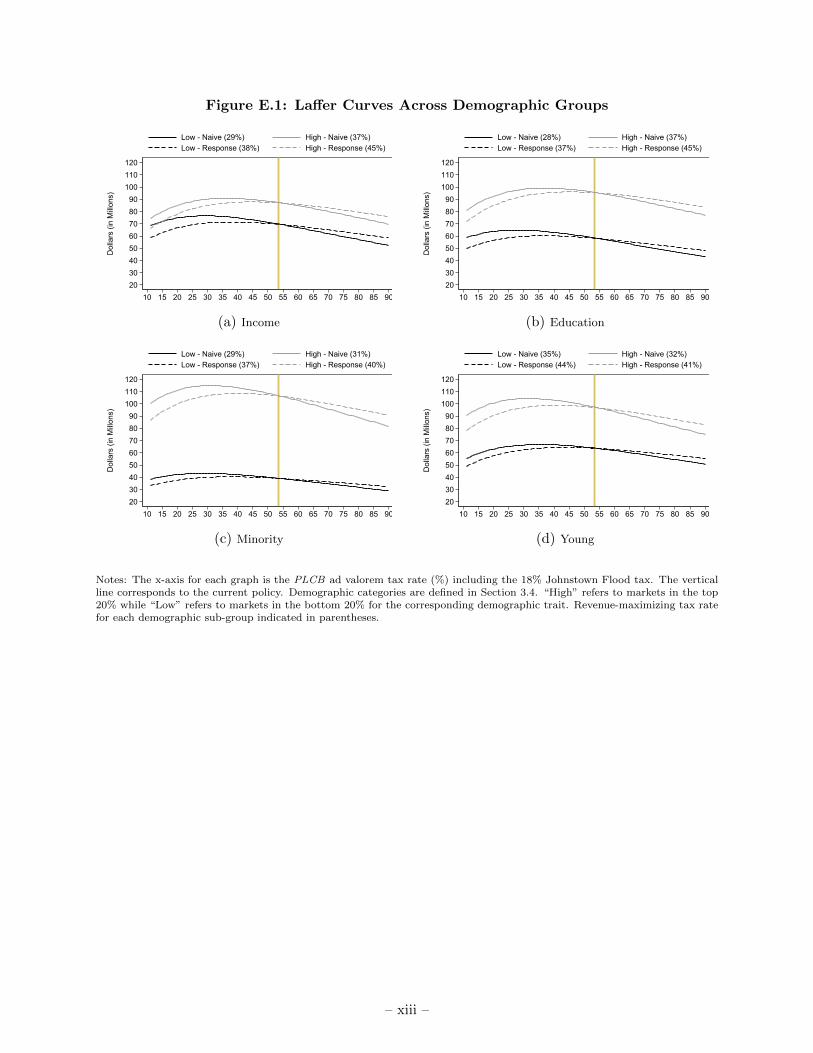

3.4 Evidence of Heterogeneity of Preferences for Liquor

To conclude the description of the primary data features, we now document systematic variation

in consumer preferences along different demographic profiles. Throughout the analyses, we rely on

four primary demographic attributes of stores’ market areas: income, educational attainment, and

the prevalence of minority and young consumers. We used categorical data on income by minority

status to fit generalized beta distributions, which allow us to draw random samples of income for

our estimation from market-specific continuous distributions that vary by demographic trait and to

estimate the share of high-income households with incomes above $50,000. We similarly obtained

information on educational attainment by minority status to derive the share of the minority

and white population with at least some college education in each area. Lastly, we employ the

unconditional share of each market’s population between the ages of 21 and 29.

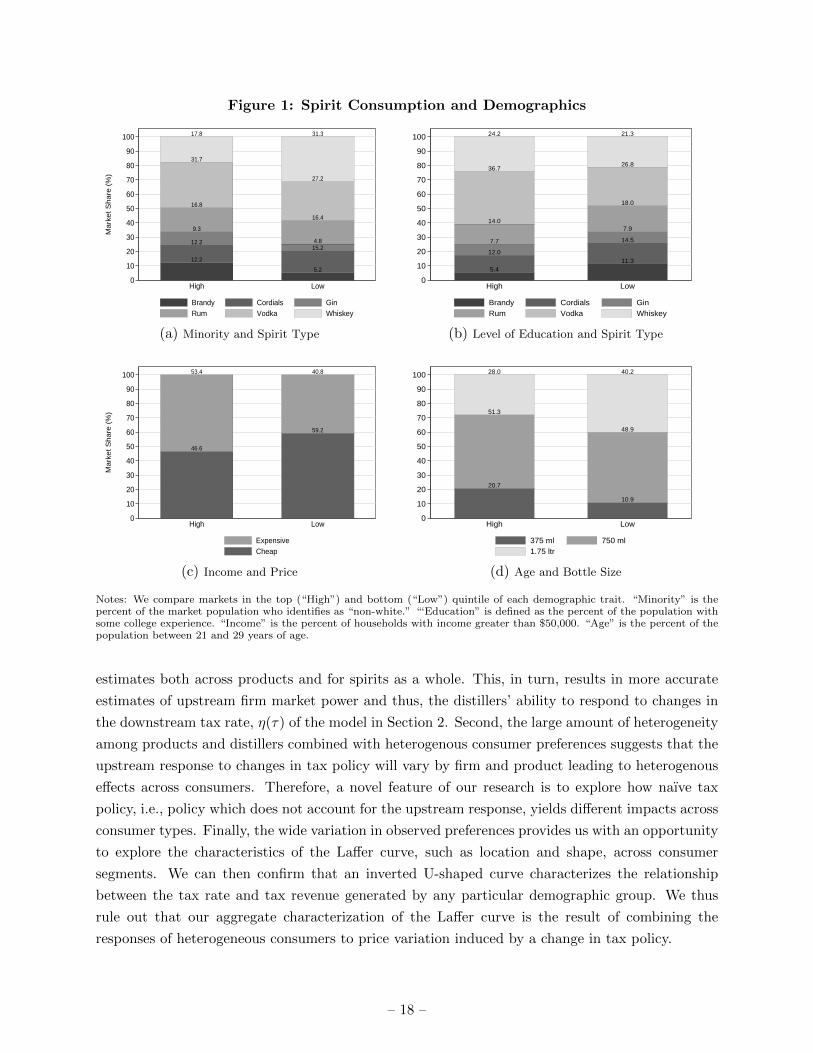

We show differences in preferences by assigning the store markets into quintiles based on

each demographic trait – the share of high-income households, the share of non-white or minority

households, the share of residents with some college education, and the share of residents in their

twenties. Figure 1 compares the purchase patterns of the top and bottom quintiles. Markets

with a greater share of minorities have substantially higher sales of vodka, gin, and brandy but

lower sales of whiskey. In areas where the population has more residents with college experience,

however, not only vodka but also whiskey is more popular, while rum and brandy have lower sales.

In markets with a larger share of high income residents, we observe larger purchases of expensive

spirits indicating that high income consumers are more willing to buy expensive spirits, presumably

because these spirits tend to be of higher quality.19 Finally, as the share of young residents increases,

so do sales of smaller bottles.

In our analysis, we exploit this wide variation in observable preferences across demographic

groups in three ways. First, this preference heterogeneity allows us to capture rich substitution

patterns to best reflect the purchase decisions of consumers, leading to more robust elasticity

19Our Proof66.com indicators confirm that price and quality are positively correlated, particularly for cordials, gins,and whiskeys.

Notes: We compare markets in the top (“High”) and bottom (“Low”) quintile of each demographic trait. “Minority” is thepercent of the market population who identifies as “non-white.” “‘Education” is defined as the percent of the population withsome college experience. “Income” is the percent of households with income greater than $50,000. “Age” is the percent of thepopulation between 21 and 29 years of age.

estimates both across products and for spirits as a whole. This, in turn, results in more accurate

estimates of upstream firm market power and thus, the distillers’ ability to respond to changes in

the downstream tax rate, η(τ) of the model in Section 2. Second, the large amount of heterogeneity

among products and distillers combined with heterogenous consumer preferences suggests that the

upstream response to changes in tax policy will vary by firm and product leading to heterogenous

effects across consumers. Therefore, a novel feature of our research is to explore how naıve tax

policy, i.e., policy which does not account for the upstream response, yields different impacts across

consumer types. Finally, the wide variation in observed preferences provides us with an opportunity

to explore the characteristics of the Laffer curve, such as location and shape, across consumer

segments. We can then confirm that an inverted U-shaped curve characterizes the relationship

between the tax rate and tax revenue generated by any particular demographic group. We thus

rule out that our aggregate characterization of the Laffer curve is the result of combining the

responses of heterogeneous consumers to price variation induced by a change in tax policy.

– 18 –

4 Empirical Model

In this section we describe a static model of oligopoly price competition with differentiated goods.

We assume that each period upstream spirit manufacturers simultaneously choose wholesale prices

{pw} to maximize profits. The downstream firm, the PLCB , takes these prices as given and gener-

ates the final retail price by applying a 30% markup, a per-unit handling fee that varies by bottle

size, and an 18% liquor tax. Finally, consumers in each market choose the product that maximizes

their utility. We solve the model backwards, first presenting downstream consumer demand and

then progressing to the profit-maximization problem of the upstream spirit manufacturers.

4.1 Downstream Market - A Discrete Choice Model of Demand for Spirits

In modeling demand for spirits as a function of product characteristics and prices, we follow the

large literature on discrete-choice demand system estimation using aggregate market share data

(cf. Berry (1994), Berry, Levinsohn and Pakes (1995) (BLP), and Nevo (2001)). This facilitates

the estimation of robust own and cross-price elasticities for a large set of products while accounting

for systematic differences in consumer preferences across demographics.

In pricing period t, consumer i in market l obtains the indirect utility from consuming a

bottle of spirit j ∈ Jlt given by

uijlt = xjβ∗i + α∗i p

rjt + [ht q3t]γ + ξjlt + εijlt ,

where i = 1, . . . ,Mlt; j = 1, . . . , Jlt; l = 1, . . . , L; t = 1, . . . , T .(17)

The n× 1 vector of observed product characteristics xj is identical in all markets l where product

j is available and fixed over time, though the availability of different spirits may change over

time due to product introductions/removals or store closings/openings. We also include a holiday

dummy variable ht that indicates whether period t coincides with the end-of-year holiday season

from Thanksgiving to the New Year and a summer dummy variable q3t for the July, August, and

September periods. We denote the retail price of product j at time t by prjt where, in accordance

with the PLCB ’s pricing mandate, the retail price does not vary across markets l within period t.

We further allow utility to vary across products, markets, and time via the time and location-specific

product valuations ξjlt, which are common knowledge to consumers, upstream firms, and the PLCB

but unobserved by the econometrician.

We characterize consumer i in market l by a d-vector of observed demographic attributes

including education, race, youth, and income, that we denote by Dil. To allow for individual hetero-

geneity in purchase behavior, we model the distribution of consumer preferences over characteristics

and prices as multivariate normal with a mean νil that shifts with these consumer attributes,(α∗iβ∗i

)=

(α

β

)+ ΠDil + Σνil , νil ∼ N(0, In+1) , (18)

– 19 –

where Π is a (n + 1) × d matrix of coefficients that measures the effect of observable individual

attributes on the consumer valuation of spirit characteristics, while Σ measures the covariance in

unobserved preferences across characteristics. We restrict Σjk = 0 ∀k 6= j, and estimate only the

variance in unobserved preferences for characteristics. Introducing unobserved preferences for a

given characteristic j allows higher cross-price elasticities among products with similar characteris-

tics, e.g., flavored or imported, thereby relaxing the restrictive substitution patterns generated by

the Independence of Irrelevant Alternatives (IIA) property of the multinomial logit model. Simi-

larly, matrix Π captures the contribution of demographic and product characteristic interactions

that allows cross-price elasticities to vary differentially in markets with observed differences in

demographics. For instance, we expect expensive vodkas to have higher cross-price elasticities in

markets with a large fraction of high-income consumers.

Next, we follow Grigolon and Verboven (2014) in modeling the unobserved individual pref-

erences and assume that they are correlated across spirits of the same type, resulting in the random

coefficient nested logit model or RCNL. The term εijlt follows the distributional assumptions of

the nested logit model, thereby increasing the valuations of products within the same group (nest),

here given by spirit type. There are g = 0, 1, ..., G distinct groups to whom we assign each product;

we define group zero to be the outside good. We can therefore write the idiosyncratic valuation by

consumer i for product j in market l and period t as

εijlt = ζigt + (1− ρ)εijlt , (19)

where ρ ∈ [0, 1] and we assume that the distribution of ε is i.i.d. multivariate type I extreme value

and the distribution of ζigt is such that εijlt is also distributed extreme value. We define groups

according to spirit type (brandy, cordials, gin, rum, vodka, and whiskey), and call ρ the “nesting

parameter” as its value modulates the importance of spirit type in explaining consumer purchases.

As ρ goes to one, consumers view products within each spirit type as perfect substitutes while ρ

converging to zero reduces within-type correlation to zero. Plugging (19) into (17) yields

uijlt = xjβ∗i + α∗i p

rjt + [ht q3t]γ + ξjlt +

G∑g=1

1(j ∈ g)ζigt + (1− ρ)εijlt , (20)

where 1(j ∈ g) is a group indicator variable equal to one when product j belongs to spirit type

g. Together, equations (18) and (20) encompass several demand specifications allowing for a wide

arrange of substitution patterns. When Σ = 0 and ρ > 0 the model collapses to the nested logit.

Alternatively, when ρ = 0 but Σ > 0 the model collapses to the random coefficients model of BLP .

When both Σ = 0 and ρ = 0 the model returns the simple multinomial logit choice probabilities.

We assume that during a particular time period, each consumer selects either one bottle of

the Jlt spirits available in her market l or opts to purchase the outside option denoted by j = 0. We

– 20 –

define the potential market, Mlt, as all off-premise purchases, i.e., those purchases not consumed

in a restaurant or bar, of alcoholic beverages, including spirits, beer, and wine.20

The annual potential market for location l then is the number of drinking-age residents

scaled by per-capita off-premise consumption, which we calculate as follows. According to Haugh-

wout, Lavallee and Castle (2015) the average drinking-age Pennsylvanian consumed 124.2, 120.5,

and 121.0 liters of alcoholic beverages in 2002, 2003, and 2004, respectively. Of this consumption,

79.8% on average was purchased off-premise, resulting in per-capita off-premise consumption of

132.1, 128.3, and 128.7 bottle-equivalents of 750 ml, respectively.21 To put these figures in

perspective, beer accounts for approximately 90% of total consumption by volume so the average

drinking-age Pennsylvanian consumes the equivalent of nearly five 375 ml bottles of beer per week

vs. approximately four 750 ml bottles of both wine and liquor during the year.

The potential market Mlt for location l in period t is simply the prorated potential con-

sumption according to the number of days included in pricing period t. A consumer opting for

the outside option then consumes a 750 ml “bottle” of beer (i.e., two 375 ml bottles) or a 750

ml bottle of wine. Note that this definition of the potential market accounts for the total volume

of alcoholic beverages but not for the different ethanol contents of beer (4.5% on average), wine

(12.9% on average), and spirits (37.9% on average in our sample). Thus, policy can reduce total

ethanol consumption by increasing retail prices of spirits leading consumers to substitute towards

beer and wine.

Next, we address consumers’ choice decisions. The set of individual-specific characteristics

leading to the optimal choice of spirit j is given by

where we summarize all model parameters by θ. We follow the literature in decomposing the

deterministic portion of the consumer’s indirect utility into a common part shared across consumers,

δjlt, and an idiosyncratic component, µijlt. These mean utilities of choosing product j and the

idiosyncratic deviations around them are written as follows:

δjlt = xjβ + αprjt + [ht q3t]γ + ξjlt , (22a)

µijlt =(xj prjt

)(ΠDil + Σνil) . (22b)

In estimating the model, we take advantage of the additive specification of normally-

distributed deviations from mean utility and extreme-value random shocks to integrate over the

20The present static discrete choice approach has limitations when instead, individuals purchase several productsor multiple bottles of the same product at the same time. See Nevo (2000, p.401) and Hendel (1999). Hendeland Nevo (2006a) further show that static demand estimates overestimate own-price elasticities and underestimatecross-price elasticities when consumers make dynamic purchase decisions. We discuss potential issues and biasesassociated with stockpiling in Appendix C.4 as well as provide evidence that stockpiling is not an issue in our data.

21Authors’ calculations based on data from the National Alcohol Beverage Control Association.

– 21 –

distribution of εit giving rise to Ajt analytically. The probability that consumer i purchases product

j in market l in period t is then

sijlt =

exp

(δjlt + µijlt

1− ρ

)exp

(Iiglt

1− ρ

) ×exp(Iiglt)

exp(Iilt), (23)

where

Iiglt = (1− ρ) ln

Jg∑m=1

exp

(δmlt + µimlt

1− ρ

), (24a)

Iilt = ln

1 +G∑g=1

exp(Iiglt)

. (24b)

Deriving product j’s aggregate market share in each location requires integrating over the

distributions of observable and unobservable consumer attributes Dil and νil, which we denote by

PD(Di) and Pν(νi), respectively. Thus, the model predicts a market share for product j in market

l at time t of

sjlt =

∫νl

∫Dl

sijltdPD(Di)dPν(νi) , (25)

which we evaluate by Monte Carlo simulation. For each market l we simulate the consumption

choices of 200 randomly drawn heterogeneous consumers who vary in their demographics and

income. We construct the sample for each market using the previously discussed census data

on race, age, educational attainment, and income. We simulate whether each randomly drawn

consumer is a minority or in their twenties based on the prevalence of these demographic groups

in each market. Conditional on the consumer’s realized minority status, we then take a random

draw from the corresponding estimated continuous distribution of income and discrete distribution

of educational attainment. See Appendix A for further details. Since the ambient population

of stores changes with store openings and closings over the course of the sample, we allow the

simulated set of agents to also change. Lastly, we account for the unobserved preferences (ν) via

Halton draws in order to reduce simulation bias as recommended by Judd and Skrainka (2011).

4.2 An Oligopoly Model for Upstream Distillers

Wholesale prices pw are the outcome of an upstream market equilibrium given the PLCB ’s pricing

rule. We now present a flexible model of upstream behavior that places few restrictions on firm

conduct while allowing for robust estimates of upstream market power. Each firm f ∈ F produces

a subset Jft of the j = 1, . . . , Jt products and faces several competitors from the set F of upstream

distillers. In each period t the upstream firms simultaneously choose the vector of wholesale prices

{pwjt}j∈Jft to maximize period t profit

– 22 –

max{pwjt}

∑j∈Jft

(pwjt − cjt)×L∑l=1

Mltsjlt(pr(pw), x, ξ; θ

)︸ ︷︷ ︸

statewide demand forproduct j in period t

, (26)

where Mlt is the size of market l and cjt denotes the marginal cost of producing spirit j in period t.

Given the static nature of the firms’ pricing decisions, we omit the period t subscripts for the sake

of clarity going forward.22 Define as sj(pr, x, ξ; θ) =

∑Ll=1Mlsjl(p

r, x, ξ; θ) the state-wide demand

for product j. Assuming a pure strategy Bertrand-Nash equilibrium in wholesale prices, profit

maximization in the upstream market implies that upstream firm f chooses prices pwj ∀j ∈ Jf to

solve the set of first-order conditions

sj(pr(pw), x, ξ; θ

)+∑m∈Jf

(pwm − cm)sm(pr(pw), x, ξ; θ

)× ∂sm∂pwj

= 0 . (27)

The term ∂sm∂pwj

is the change in quantity sold for product m in response to a change in the wholesale

price and, through the pricing rule, the retail price of product j.23 Converting (27) into vector

where Owt denotes the ownership matrix for the upstream firms with element (j,m) equal to one

if goods j and m are in Jf . We define ∆w as a matrix that captures changes in demand due to

changes in wholesale price as follows

∆w=∆d∆p′=

∂s1∂pr1

. . . ∂s1∂prJ

.... . .

...∂sJ∂pr1

. . . ∂sJ∂prJ

dpr1dpw1

. . .dpr1dpwJ

.... . .

...dprJdpw1

. . .dprJdpwJ

′

=

∂s1∂pr1

. . . ∂s1∂prJ

.... . .

...∂sJ∂pr1

. . . ∂sJ∂prJ

1.534 . . . 0...

. . ....

0 . . . 1.534

, (29)

where ∆d is the matrix of changes in quantity sold in period t due to changes in retail price with

element (r,m) equal to ∂sr∂prm

and ∆p is the matrix of changes in retail price due to changes in

wholesale price with element (m, j) equal to dprmdpwj

.

22Table II documents that the PLCB limits the number of times distillers can temporarily reduce a product’s price.In the data, the average product goes on sale only 2.3 times per year and 76.6% of products go on sale three timesor less in a year, indicating that this regulation does not constrain upstream pricing for the majority of products.We thus do not address any dynamic considerations to the timing of pricing decisions over the course of the year,but employ a simpler and more tractable static pricing model instead.

23For simplicity, we assume that firms observe the distribution of consumer preferences. We thus abstract fromsecond-degree price discrimination across bottle sizes as in in McManus (2007) and instead focus on horizontaldifferentiation between products.

– 23 –

Villas-Boas (2007) shows that in vertical retail pricing markets, ∆p can be a complicated

object. In our context, however, the state’s regulation of alcohol sales simplifies this matrix

significantly by committing downstream stores to a uniform pricing policy and by eliminating

off-diagonal terms. For example, under the current pricing rule,dprjdpwj

is simply 1.30×1.18, reflecting

the 30% uniform tax and the 18% liquor tax that translate a change in the wholesale price for

product j to a change in the product’s retail price. Further, the retail price for product m does

not respond to a change in the wholesale price for product j: dprmdpwj

= 0 ∀m 6= j. The uniform tax

rule from equation (16) thus limits the PLCB ’s ability to respond to changes in wholesale prices