PMAC FIRST ANNUAL COMPLIANCE FORUM MARKETING September 11, 2012 Christina Forster Pazienza, Vice President, Compliance MFS McLean Budden MFS McLean Budden SM is the registered business name of McLean Budden Limited.

Transcript

PMAC FIRST ANNUAL COMPLIANCE FORUM

MARKETING September 11, 2012 Christina Forster Pazienza, Vice President, Compliance MFS McLean Budden

MFS McLean BuddenSM is the registered business name of McLean Budden Limited.

Overview of presentation

• Marketing in the portfolio management environment • Regulatory history • Regulatory requirements • Current areas of focus • Key concerns and suggested practices • Key internal controls

Marketing in the portfolio management environment

• Prospective clients and ongoing client relationships • Attract and maintain clients • Provide information on firm’s services, skills and experience • Variety of mediums: presentations, brochures, websites, etc.

Regulatory history

• Area of focus and ongoing concern for the Canadian Securities Administrators • Continue to see issues in the marketing practices of portfolio managers • Investors place significant reliance on marketing materials • Two focused reviews to date:

– 2006/2007: OSC – 2011: CSA

Regulatory requirements

• Specific rules and instruments, both prescriptive and principles based • s. 122 (1) of the OSA prohibits a person or company from making statements that are untrue, or omitting

information that is necessary to prevent the statement from being false or misleading • s. 2.1 of OSC Rule 31-505 Conditions of Registration

– portfolio managers required to deal fairly, honestly and in good faith with their clients • Guidance found in two staff notices:

– OSC Staff Notice 33-729 – November 9, 2007 – CSA Staff Notice 31-325 – July 8, 2011

Current areas of focus

• Preparation and use of hypothetical performance data • Exaggerated and unsubstantiated claims • Policies, procedures and internal controls • Use of benchmarks • Performance composites • Holding out and use of names • Other performance return issues • Disclosure related issues • Use of social web sites

Preparation and use of hypothetical performance data

• Concerns – Not based on actual performance – Different forms – e.g. back-tested, model – A lot of room for manipulation – Misleading to investors

• Suggested practices – Firms should market their actual performance – Limited circumstances where hypothetical data may be used

• Sophistication of client (i.e. institutional vs private wealth) • Nature of information • How information is disseminated to clients

Exaggerated and unsubstantiated claims

• Concerns – Most common deficiency identified – Claims made re: performance, skills, education, experience or services without evidence to support

• Suggested practices – All statements/claims should be supported – Reference information supporting claims

Policies, procedures and internal controls

• Concerns – Lack of or inadequate policies and procedures to address preparation, use and approval of marketing

materials – No independent review and approval

• Suggested practices – Guidelines on:

• Preparation and review to prevent false or misleading statement and to ensure compliance with Ontario securities law

• Approval by appropriate person (e.g. Chief Compliance Officer) • Preparation of performance data • Composite construction • Benchmark selection and presentation

Use of benchmarks

• Standard against which a portfolio manager’s investment strategy is measured • Concerns

– Lack of comparability – Not widely recognized/available – Inadequate disclosure – Risk that comparison not meaningful

• Suggested practices – Benchmarks should be relevant – Guidance on use of benchmarks

• Selection • disclosure

Performance composites

• Concerns – Inadequate composite construction – Inadequate methodology – Inadequate policies and procedures – Unfair presentation/misleading to clients – Cherry picking portfolios with the best returns to present better than actual results

• Suggested practices – Composites should include all portfolios with similar investment strategies – Guidance provided on construction and presentation

Holding out and use of names

• Concerns – Unregistered individuals using business titles that implied they were registered – Inappropriate use of business or trade names – Use of names of other registered firms without prior consent

• Suggested practices

– Use full legal name or registered trade name when marketing activities – Individuals should use job titles that adequately reflect the nature of their duties or category of

registration – Ensure adequate policies and procedures in place to review and approve the use of trade names of the

firm and job titles used by individuals

Other performance return issues

• Concerns – Marketing performance returns from an individual’s previous firm (portability issue) – Marketing proprietary firm and individual PM’s performance returns as representative of a firm’s

strategy

• Suggested practices – Present performance returns of the firms’ actual performance composites or investment funds since the

firms have been registered

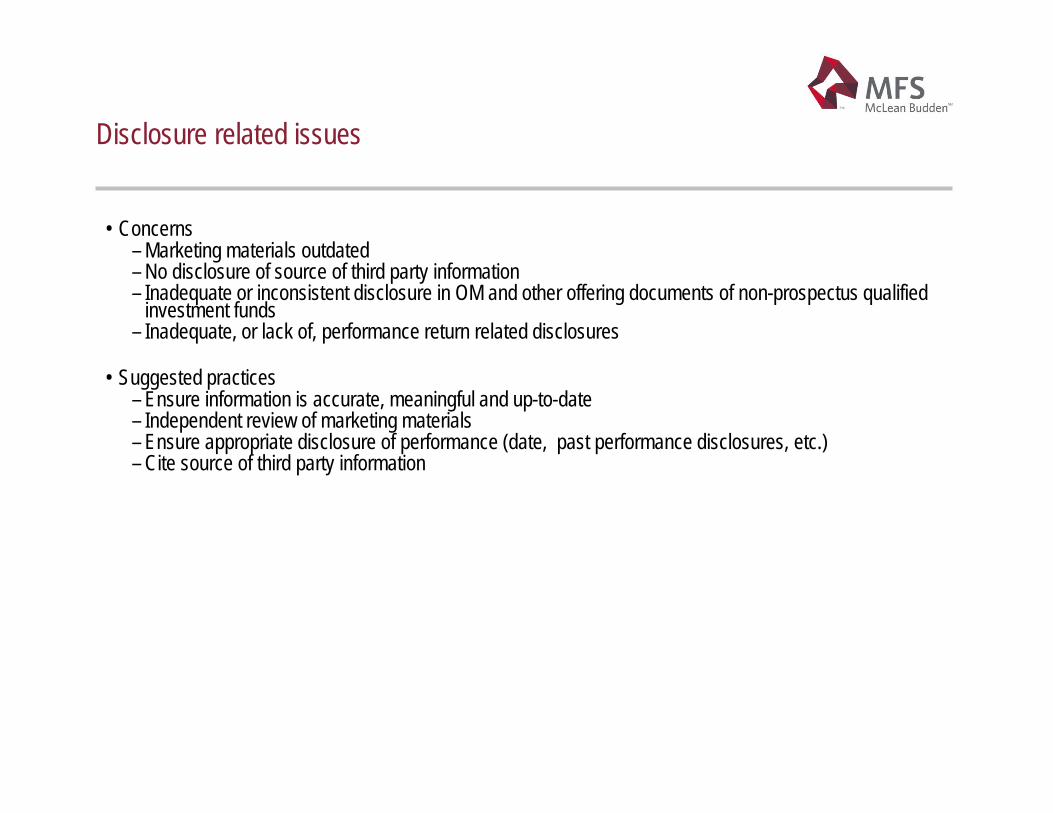

Disclosure related issues

• Concerns – Marketing materials outdated – No disclosure of source of third party information – Inadequate or inconsistent disclosure in OM and other offering documents of non-prospectus qualified

investment funds – Inadequate, or lack of, performance return related disclosures

• Suggested practices

– Ensure information is accurate, meaningful and up-to-date – Independent review of marketing materials – Ensure appropriate disclosure of performance (date, past performance disclosures, etc.) – Cite source of third party information

Use of social media web sites

• Emerging issue – recent trend • Not yet prevalent in PM environment • Concerns

– Maintenance of adequate books and records – Adequate supervision

• Suggested practices – Establishing policies and procedures for the review, supervision, retention and retrieval of materials on

social media web sites (i.e. Facebook, Twitter, Linkedin , etc.) – Designating an appropriate individual to be responsible for the supervision or approval of

communications – Reviewing the adequacy of systems and programs to ensure compliance record retention and retrieval

capability

Key internal controls

• Policies and procedures • Disclose, disclose, disclose • Train employees • Know your clients • Thoughtful and thorough preparation of marketing materials • All marketing materials approved prior to use or when changes made • Ongoing monitoring to prevent and detect issues

Questions?

• Thank you

PMAC Compliance Forum The Client Lifecycle: New Clients

September 2012

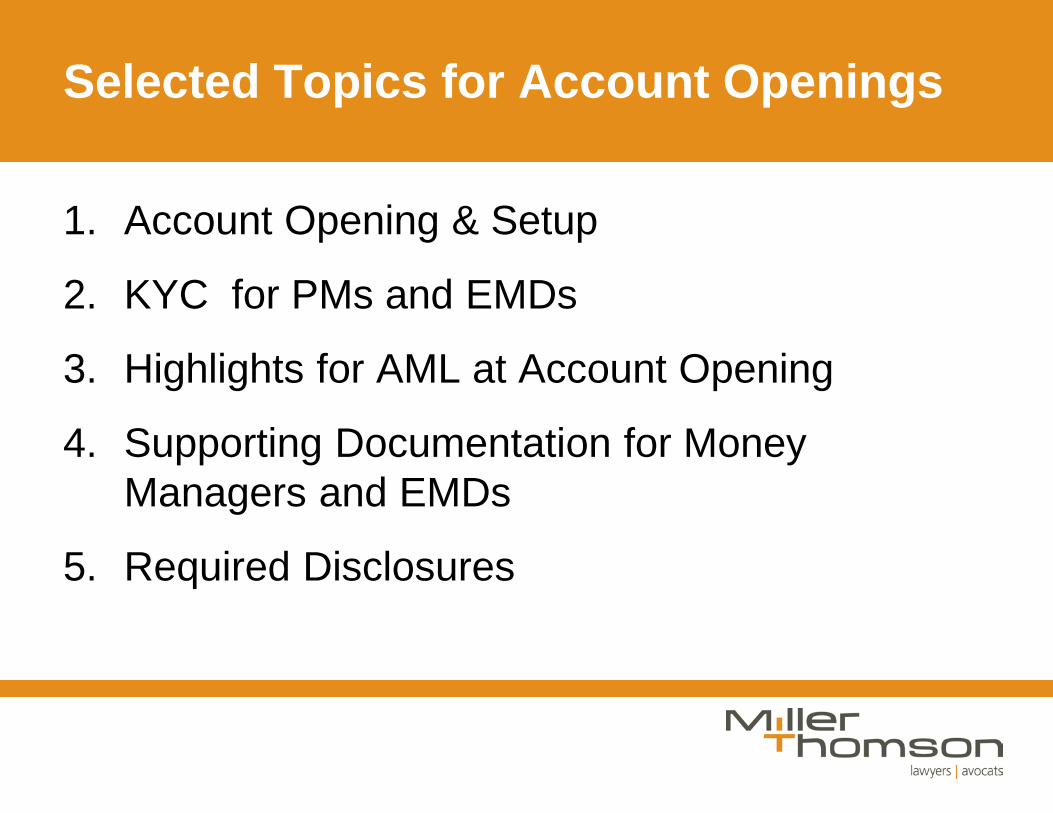

Selected Topics for Account Openings

1. Account Opening & Setup

2. KYC for PMs and EMDs

3. Highlights for AML at Account Opening

4. Supporting Documentation for Money Managers and EMDs

5. Required Disclosures

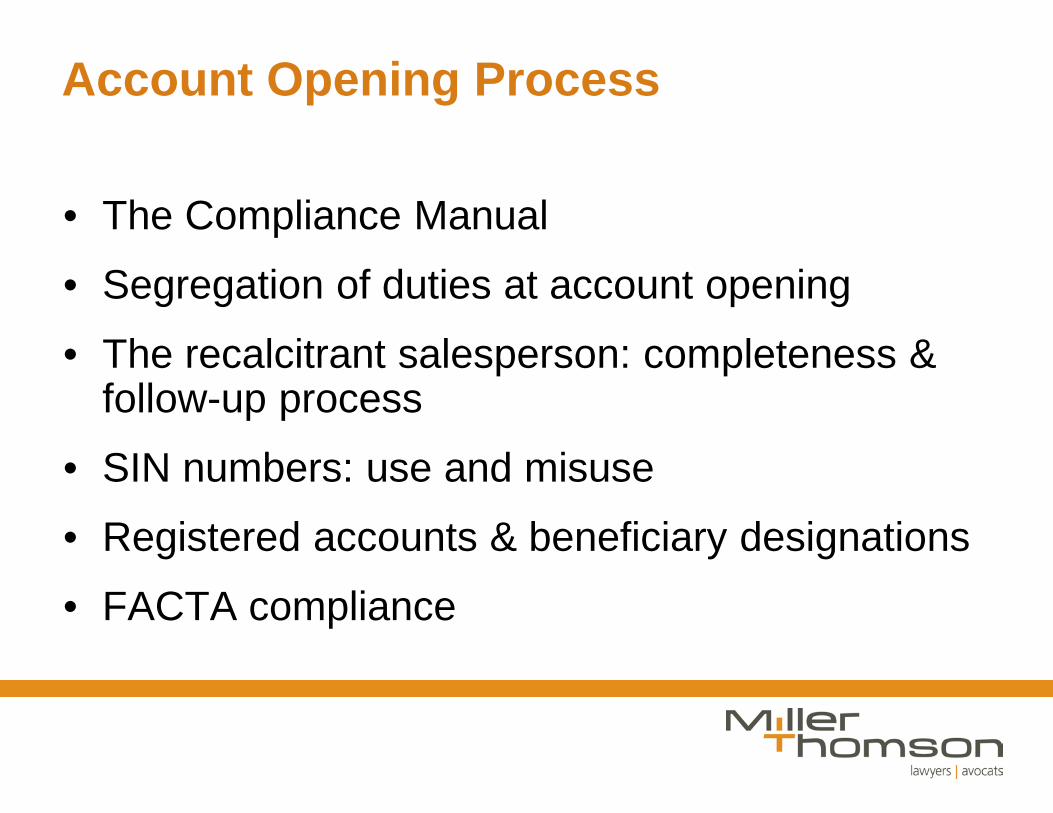

Account Opening Process

• The Compliance Manual

• Segregation of duties at account opening

• The recalcitrant salesperson: completeness & follow-up process

• SIN numbers: use and misuse

• Registered accounts & beneficiary designations

• FACTA compliance

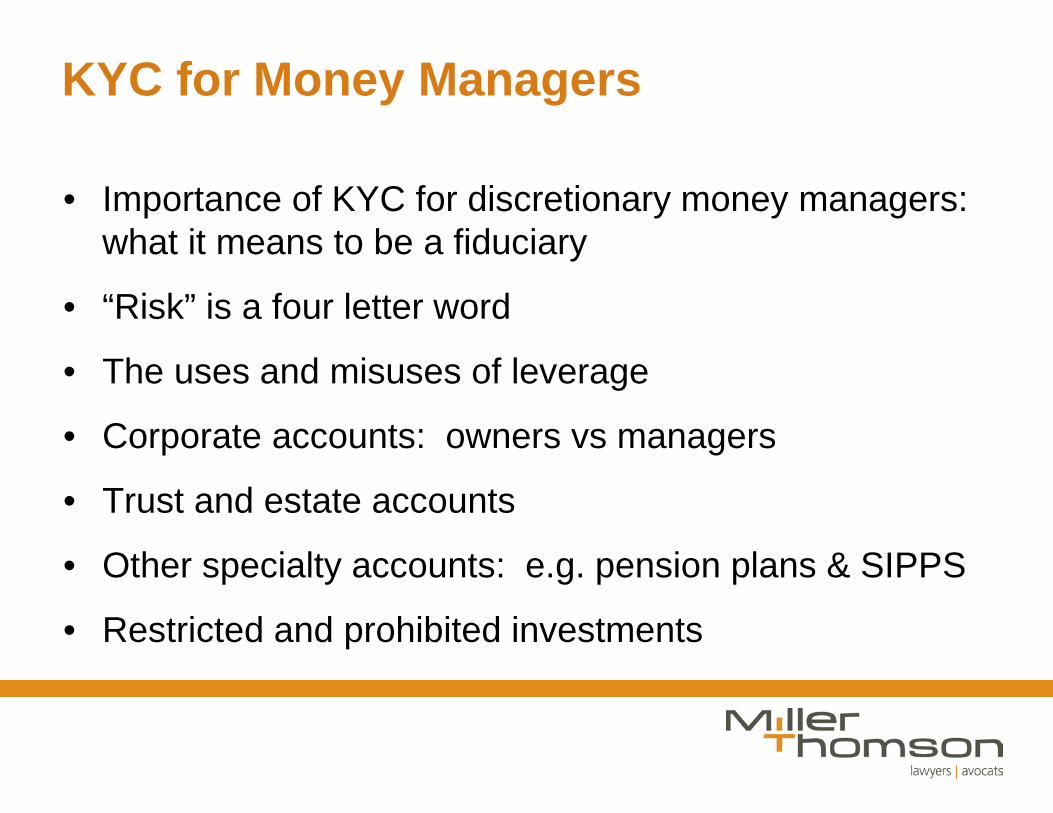

KYC for Money Managers

• Importance of KYC for discretionary money managers: what it means to be a fiduciary

• “Risk” is a four letter word

• The uses and misuses of leverage

• Corporate accounts: owners vs managers

• Trust and estate accounts

• Other specialty accounts: e.g. pension plans & SIPPS

• Restricted and prohibited investments

Accredited Investors & Permitted Investors

• Establishing that an investor is “accredited”: the test for individuals

• Prospectus exemptions are independent of one another

• Who is a “Permitted Client” and waiver of suitability

• Waiving suitability in other circumstances

Meeting AML Requirements

• Client Identification Procedures: corporations

• Client Identification Procedures: individuals

• When individual is not physically present

• Politically Exposed Foreign Persons

• Third Party Determination

Supporting Documentation

And Required Disclosures

Supporting Documentation

• IMA (Investment Management Agreement) • Fee Schedule • Permitted Client Waiver • Subscription Agreements and Accredited Investor

Certificates • Completed DRIP form • Disclosure re: Collection of Personal Information for

OSC Reporting purposes • Certificates of Incumbency / Authorized Signing

Authorities

More and Other Client Documentation

• Account transfer authorization / instructions • Instructions re delivery of physical certs • Banking information, instructions re EFTs, PACs, SWIPS • Language preference • Duplicate account information sent to? • Documents from trust company if SDRRSP/RRIF • LOIs, LOAs, POAs, trading authorizations • Spousal consent/ waiver forms (locked-in plans) • Hold mail / hold cheque instructions • Loan documentation • Etc. etc.

Ongoing Clients: Reporting, Fees, Updating KYC and

Suitability

Don Campbell

KYC and Suitability

• Existing Obligations – Sections 13.2 and 13.3 of NI 31-103 – Fiduciary obligations to client – CFA Code of Ethics and Standards of Professional

Conduct – Written investment management agreement with

clients

KYC and Suitability

• OSC 2011 Annual Summary Report for Dealers, Advisers and IFMs (pps. 43 to 44)

• Keep each client’s KYC information up-to-date by: – immediately contacting the client when they

know that their circumstances have changed, and – periodically contacting the client (at least

annually) to assess if their circumstances have changed.

KYC and Suitability

• 2010 BCSC Report Card – Many firms indicated they ‘know their clients

well’, but common to find that they do not have this documented

– If clients investment objectives or risk tolerance changes, you must update in file or system

– In firms with effective compliance systems, it is common to see client information updated annually after an in-person meeting (note: OSC comments on ‘meaningful discussion’)

KYC and Suitability

• Documentation (this is the key issue) – Determine first how your firm operates to collect

information – Is your firm:

• Paper-based • CRM-based • Random note taker-based • None of the above (yikes!!)

KYC and Suitability

• Documentation – Then Determine your client review process – Is your firm

• Regular quarterly/semi-annual/annual meeting process • Note: you should be able to answer ‘yes’ to one of those

three choices • Who owns the process? • How is it tracked? • Can you produce a matrix of ‘last seen/next to be

seen/next request to be sent out’? • Definitely on a per client basis; ideally have a master firm

client list (Compliance Nirvana)

KYC and Suitability

• Documentation – How to document

• This goes to tie in your existing processes so will be unique to your firm

• Issues of documenting ‘no change’ • Issues of ‘what is material’ • Issues of ‘when does a change trigger an IPS change’

KYC and Suitability

• Other Really Important Issues – But the client does NOT respond, will NOT book a

meeting • Progressive correspondence

– Would like to meet with you – Need to meet with you – Not responsible if we don’t meet with you – You’re fired!!

KYC and Suitability

• Other Really Important Issues – Where is the client at in their life cycle

• The accumulation years are the easiest • As the client moves closer to retirement with a

declining time horizon the real work begins • Are you really a financial planner – a very difficult line

to toe

Reporting

• Existing Obligations – Sections 14.14 and 14.15 of NI 31-103

• Transactions and Account Statements • 2011 OSC Annual Summary commented on PMs not

including transactions on Account Statements • 2011 OSC Annual Summary also commented concerns

not on a per account basis • No prescribed form of account statement, just make

sure that you have the required information

Reporting

• Common Practices – Statements will include the following:

• Positions • Portfolio Composition • Activity • Performance • Performance versus benchmarks • Some form of consolidation to a family group

Reporting

• What is coming? – CRM II published June 14, 2012 on Cost

Disclosure, Performance Reporting and Client Statements

– Performance Reporting Mandated • There is a lot of devil in the detail

– Dollar weighted returns being prescribed (versus time weighted)

– Serious lack of comment letters in

Fees

• Existing Obligations – Disclosure Requirement in section 14.2 of NI 31-

103 – Reporting Requirement in section 14.4 (4) of NI

31-103 under the transaction reporting requirement (see Companion Policy)

– Past concerns regarding disclosure of ‘all costs associated with the operation of an account’ (Relationship Disclosure Sweep)

Fees

• Common Practices – Disclosure of fees charged

• Separate summary of fees charged on a quarterly basis

– versus • Just having within transaction summary • Providing an annual summary of fees charged to non-

registered accounts Note: if part of firm activity is paying any third party bills, triggers ‘custody’ for FIB purposes

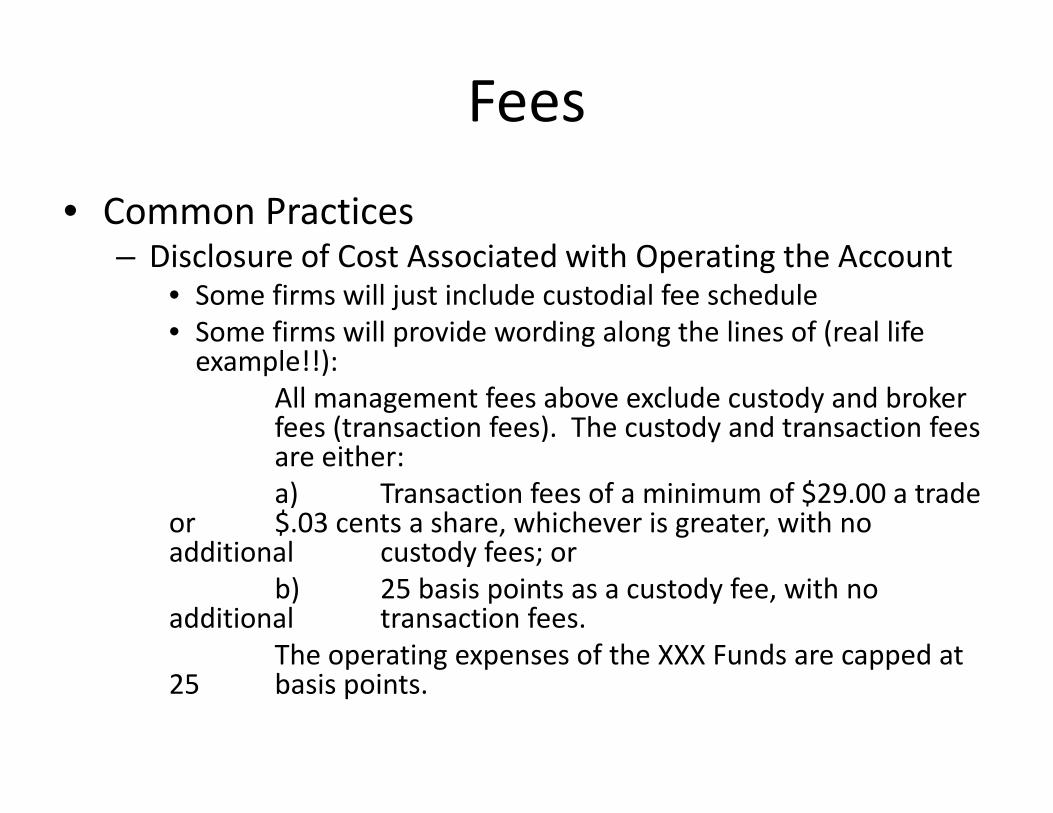

Fees • Common Practices

– Disclosure of Cost Associated with Operating the Account • Some firms will just include custodial fee schedule • Some firms will provide wording along the lines of (real life

example!!): All management fees above exclude custody and broker fees (transaction fees). The custody and transaction fees are either: a) Transaction fees of a minimum of $29.00 a trade or $.03 cents a share, whichever is greater, with no additional custody fees; or b) 25 basis points as a custody fee, with no additional transaction fees. The operating expenses of the XXX Funds are capped at 25 basis points.

Fees

• What is Coming? – CRM II

• RD information regarding operating charges, transaction charges and benchmarks

• Annual Charges and Compensation Report – Disclosure of trailing commissions on mutual funds (may be an

issue for legacy accounts and new accounts transferred in prior to liquidation)

– Potential for fixed income compensation paid to dealers (have fun with that)

– Any fees paid by third parties in relation to the account

The End

Any Questions?

Don Campbell

Tetrem Capital Management/dc.law

COMPLIANCE MANAGEMENT…FOR DEPARTING CLIENTS

“There is no departing from the words

of the law” (Latin Proverb)

WHY DO CLIENTS LEAVE?

Move to a competitor firm Move to another province or country

Death

YOUR OBLIGATIONS WHEN A CLIENT LEAVES

Maintain historical books and records

Ensure client confidentiality

Facilitate timely transfer of client assets

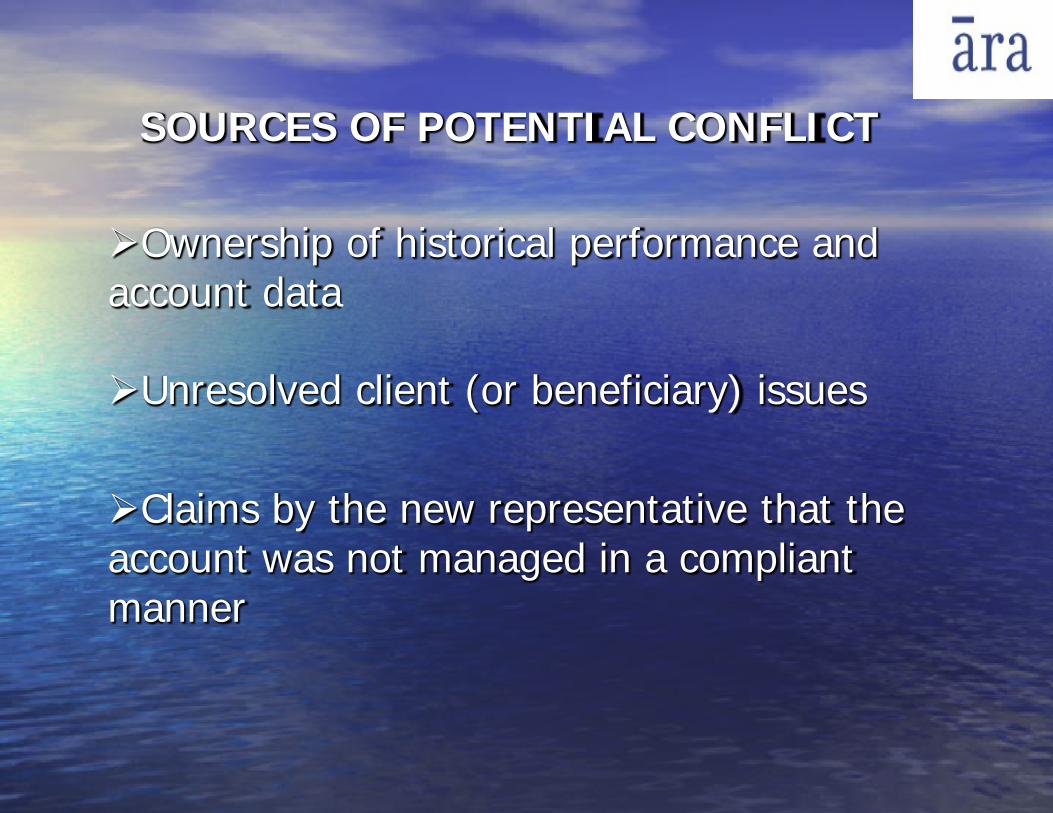

SOURCES OF POTENTIAL CONFLICT

Ownership of historical performance and account data

Unresolved client (or beneficiary) issues Claims by the new representative that the account was not managed in a compliant manner

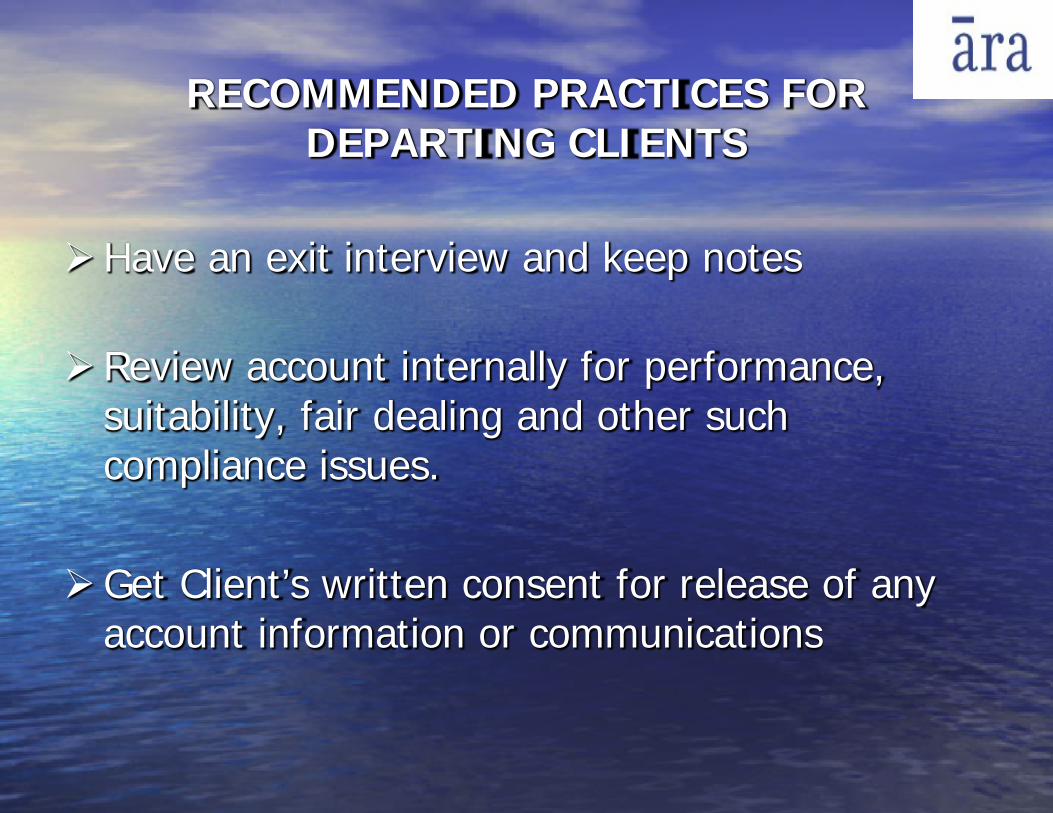

RECOMMENDED PRACTICES FOR DEPARTING CLIENTS

Have an exit interview and keep notes

Review account internally for performance, suitability, fair dealing and other such compliance issues.

Get Client’s written consent for release of any account information or communications

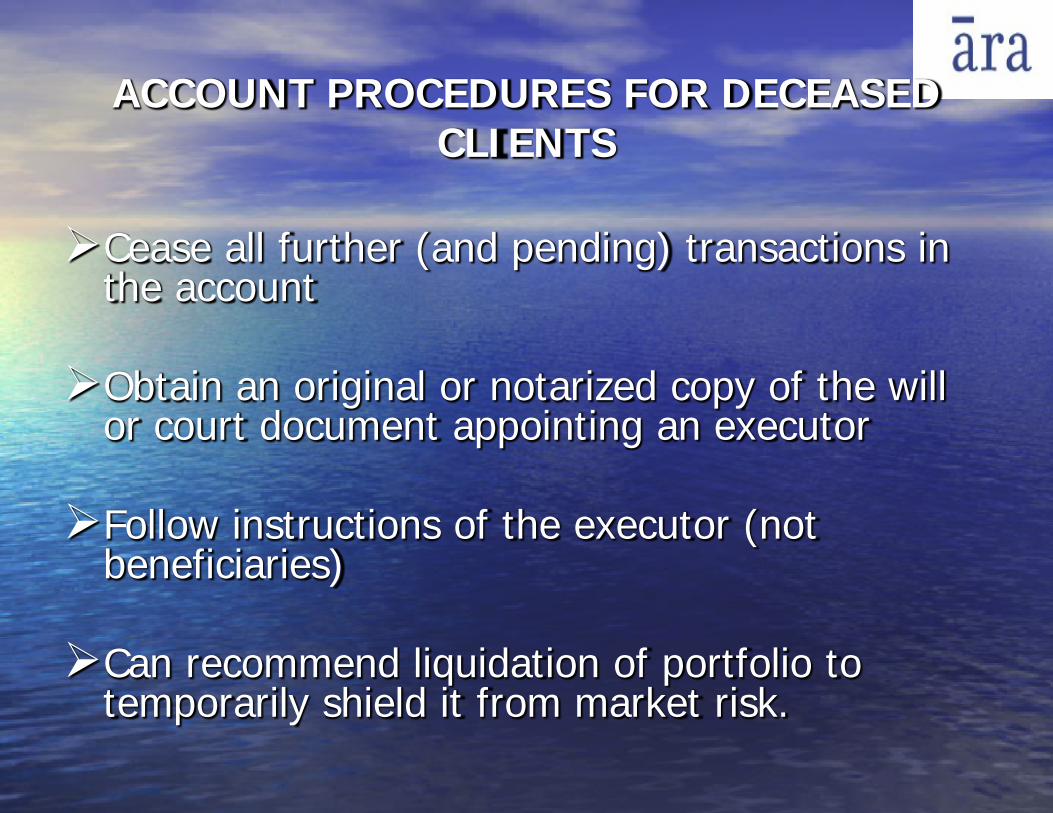

ACCOUNT PROCEDURES FOR DECEASED CLIENTS

Cease all further (and pending) transactions in the account Obtain an original or notarized copy of the will

or court document appointing an executor Follow instructions of the executor (not

beneficiaries) Can recommend liquidation of portfolio to

temporarily shield it from market risk.

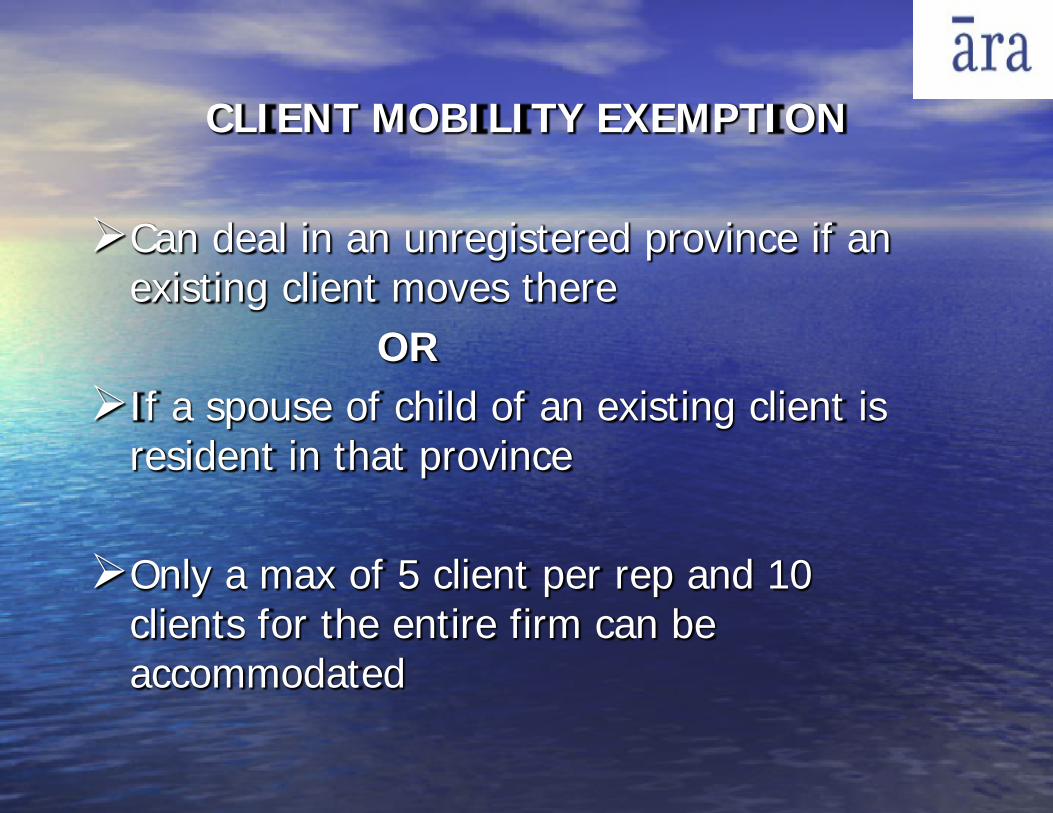

CLIENT MOBILITY EXEMPTION

Can deal in an unregistered province if an existing client moves there OR

If a spouse of child of an existing client is resident in that province Only a max of 5 client per rep and 10