STATE OF MICHIGAN DEPARTMENT OF ATTORNEY GENERAL P.O. BOX 30755 LANSING, MICHIGAN 48909 DANA NESSEL ATTORNEY GENERAL May 28, 2021 Ms. Lisa Felice Executive Secretary Michigan Public Service Commission 7109 West Saginaw Highway Lansing, MI 48917 Dear Ms. Felice: Re: MPSC Case No. U-21015 Enclosed find the Attorney General's Initial Brief, and related Proof of Service. Sincerely, Joel B. King Assistant Attorney General cc: All Parties

Transcript

STATE OF MICHIGAN DEPARTMENT OF ATTORNEY GENERAL

P.O. BOX 30755 LANSING, MICHIGAN 48909

DANA NESSEL ATTORNEY GENERAL

May 28, 2021

Ms. Lisa Felice Executive Secretary Michigan Public Service Commission 7109 West Saginaw Highway Lansing, MI 48917 Dear Ms. Felice: Re: MPSC Case No. U-21015

Enclosed find the Attorney General's Initial Brief, and related Proof of Service.

Sincerely, Joel B. King Assistant Attorney General

cc: All Parties

STATE OF MICHIGAN

BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION

___________________________

In the matter of the Application of DTE ELECTRIC COMPANY MPSC Case No. U-21015 for a Financing Order Approving the Securitization of Qualified Costs. /

ATTORNEY GENERAL INITIAL BRIEF

Dana Nessel Attorney General Joel B. King (P81270) Assistant Attorney General Special Litigation Division PO Box 30755 Lansing, MI 48909 517-335-7627

STATEMENT OF FACTS ......................................................................................................... 1

I. ARGUMENT .................................................................................................................... 5

A. Qualified Costs ........................................................................................... 8

B. Amortization of Tree Trimming Costs ................................................ 16

C. Net Present Value Test ........................................................................... 20

D. Financial Advisor .................................................................................... 21

E. Retirement of Debt and Equity Capital .............................................. 23

F. Bill Credit .................................................................................................. 25

G. Deferred Taxes Surcharge..................................................................... 27

II. Conclusion and Relief Sought .................................................................................... 27

1

INTRODUCTION

On March 26, 2021, DTE Electric Company (“DTE,” “DTE Electric,” or the

“Company”) filed an application requesting authority to securitize certain qualified

costs related to tree trimming and the retirement of River Rouge Unit 3. A

prehearing conference was held on April 20, 2021 before Administrative Law Judge

(ALJ) Dennis Mack. At the prehearing, the ALJ granted the interventions of the

Michigan Department of the Attorney General (“Attorney General” or “AG”),

Michigan Environmental Council (MEC), Association of Businesses Advocating

Tariff Equity (ABATE), and Soulardarity. The MPSC Staff also participated. On

May 6, 2021, the AG, Staff, MEC, and ABATE filed direct testimony and exhibits.

DTE filed rebuttal testimony on May 13, 2021. A cross-examination hearing was

held on May 19, 2021.

STATEMENT OF FACTS

Pursuant to the schedule set at the prehearing conference by the ALJ, all

intervenors were required to file direct testimony by May 6, 2021 and initial briefs

by May 28, 2021. The Attorney General sponsored direct testimony and exhibits of

Sebastian Coppola, consisting of 36 pages of questions and answers and 11 exhibits

labeled AG-1 through AG-11. In addition, the Attorney General admitted eight

exhibits at the cross-examination hearing, labeled AG-12 through AG-19.

Attorney General Direct Testimony

The 11 exhibits the AG prefiled with Mr. Coppola’s Direct Testimony and 8

additional exhibits admitted at cross examination are as follows:

2

1. Exhibit AG-1 Capital Structure and Cost of Capital 2. Exhibit AG-2 Customer Benefit of AG Securitization Proposal 3. Exhibit AG-3 Response on Deferred Taxes Removal 4. Exhibit AG-4 DTEE Response on Securitization Legal Fees 5. Exhibit AG-5 DTEE Responses on Audit Fees and Other Securitization

Costs 6. Exhibit AG-6 DTEE Response on Verification of Customer Estimated

Billings 7. Exhibit AG-7 DTEE Responses on Underwriters and Financial Advisor 8. Exhibit AG-8 DTEE Responses on Short-Term Debt and Long-Term

Capital 9. Exhibit AG-9 DTEE Response on River Rouge Plant O&M and

Property Taxes 10. Exhibit AG-10 AG Recalculation of Power Supply Bill Credit 11. Exhibit AG-11 DTEE Response for Revised Exhibit A-2 12. Exhibit AG-12 DTEE Response on Unwind of Deferred Tax Liabilities 13. Exhibit AG-13 DTEE Response on Legal Costs of Securitization 14. Exhibit AG-14 DTEE Response on Law Firms for Securitization 15. Exhibit AG-15 DTEE Response on Rating Agency Fees 16. Exhibit AG-16 DTEE Response on Commission Costs 17. Exhibit AG-17 DTEE Response on Witness Solomon’s Experience 18. Exhibit AG-18 DTEE Response on River Rouge O&M and Property Tax

Expenses 19. Exhibit AG-19 DTEE Responses on River Rouge Plans and O&M Costs

Sebastian Coppola

In direct testimony, Mr. Coppola addressed the following issues:

1. The amount of qualified costs for the River Rouge power plant and tree trimming costs.

2. The amount of the upfront costs to issue the securitized bonds.

3. The role of Citigroup as the transaction advisor to the Company.

4. The verification of financing and debt service costs to be recovered from customers.

3

5. The amortization period for some of the qualified costs and the

related term of the bonds to be issued.

6. The appropriate proportion of debt and equity capital to be removed from the Company’s capital structure from proceeds received from the securitization bonds.

7. The inclusion of the applicable cost savings in the calculation of the bill credit on customer bills.

8. The proposal by the Company to establish a deferred tax surcharge to customers to recover deferred taxes related to the qualified costs.

He also noted that the absence of a discussion of other matters in his

testimony should not be taken as an indication that he agrees with those aspects of

DTE’s securitization filing. The narrow focus of his testimony is, instead, a

consequence of focusing on priority issues within the available resources. 2 Tr 275

He summarized his recommendations regarding these issues as follows:

1. I recommend that the Commission reject the Company’s proposed securitization of $184 million of qualified costs for the River Rouge power plant and the deferred tree trimming costs, which are net of deferred taxes. Instead, the Commission should approve the issuance of $234 million of securitized bonds, which includes the qualified costs without the reduction of deferred tax amounts and also revised issuance costs. The larger bond issuance amount will provide an incremental benefit to customers of approximately $11.4 million as a result of a lower cost of capital.

2. I recommend that the Commission remove $2,750,000 from the forecasted bonds issuance costs of $6,500,000 and approve only the difference of $3,750,000 plus an additional $199,900 in underwriters discount and fees due [to (sic)] my proposed larger bond securitization amount. The revised issuance costs are reasonable and will provide an incentive for the Company to control and minimize issuance costs.

3. The Company stated that it engaged Citigroup as the financial advisor and lead underwriter on the bonds issuance transaction and has not yet appointed any other underwriters. The appointment of Citigroup as

4

both a financial advisor and the lead underwriter in this securitization transaction presents a conflict of interest. I recommend that the Commission direct the Company to separate the role of the financial advisor and the underwriters in future securitization bond issuances.

4. The Company proposed that the securitized tree trimming costs be amortized and recovered from customers over a 5-year period. The purpose of the Company’s proposed 7-year surge program and securitization of the costs was to spread the additional trimming costs from the surge over a longer future time period in order to reduce the impact on customer rates in the early years of the program. I recommend that the Commission deny the Company’s proposal for a 5-year amortization and cost recovery period and instead approve a 7-year period with a related longer term on the securitized bonds.

5. The Company refused to provide the calculations to support the annual amounts to be billed to customers for recovery of the bonds’ securitization costs, stating that the model used to perform the calculations is very complex and proprietary. Without access to the underlying calculations, it is not possible to validate the results of the calculated billings to customers. This validation is necessary to render an opinion on the accuracy of the calculations for both approval of the securitization application and also for the final determination of the billing amounts at time of issuance of the bonds and subsequent true-up reconciliations. Without the ability to validate the billing information, I recommend that the Commission reject the Company’s securitization application.

6. The Company plans to use the proceeds from the securitization of the River Rouge qualified costs to pay down debt and equity at a ratio of 50/50. This is in line with the debt/equity ratio approved in the permanent capital structure in Case No. U-20561. However, with regard to the proceeds received from the securitization of tree trimming costs, the Company plans to apply those proceeds entirely to the retirement of short-term debt. The Company’s claim that it financed the deferred tree trimming costs with short-term debt is unsupported. Instead, the evidence points to the fact that the qualified costs were financed with long-term debt and equity capital. I recommend that the Commission order the Company to apply the proceeds from the securitization bonds to retire equal amounts of long-term debt and common equity from the capital structure with no adjustment to the short-term debt.

7. The Company’s filed testimony and Exhibit A-19 do not include all cost savings from the retirement of the River Rouge power plant in the

5

calculation of the revenue requirement savings, which will be returned to customers through a bill credit. The Company’s calculation of a total Power Supply Bill Credit of $11,635,000 omits the O&M expense and property tax savings from the Company no longer operating the plant after securitization. I recommend that the Commission order the Company to recalculate the Power Supply Bill credit for each rate schedule based on the $41,856,000 reduction in the revenue requirement I have calculated, which is inclusive of the O&M and property tax savings.

8. As a result of my proposal to securitize the total amount of qualified costs without the reduction for deferred taxes, there is no need for the Company to recover the deferred taxes amounts through a surcharge on customer bills. Therefore, I recommend that the Commission reject the Company’s deferred tax surcharges.

2 Tr 275-79.

I. ARGUMENT

Before examining the Attorney General’s recommendations and arguments,

the Commission should consider that DTE Electric Company bears the burden of

proof to demonstrate that its securitization proposal request is reasonable and

meets the standards set forth in MCL 460.10(i). The obligation of proving any fact

lies upon the party who substantially asserts the affirmative of the issue.1 A

plaintiff always has the burden of proving its cause of action.2 In administrative

cases, a party seeking relief must prove his, her, or its claim by a preponderance of

the evidence.3 Likewise, in MPSC Cases a utility has the burden of proof by a

1 White v Campbell, 25 Mich 463, 475 (1872). 2 Caruso v Weber, 257 Mich 333; 241 NW 198 (1931). 3 Dillon v Lapeer State Home & Training School, 364 Mich 1, 8; 110 NW2d 588 (1961), and BCBSM v Governor, 422 Mich 1, 88-89; 367 NW2d 1 (1985).

6

preponderance of the evidence.4 Moreover, the MPSC may disbelieve even

uncontradicted evidence.5 When the burden of proving a fact falls on one party, the

other party does not have the burden of proving the opposite fact.6

MCL 460.10i provides as follows:

(1) Upon the application of an electric utility, if the commission finds that the net present value of the revenues to be collected under the financing order is less than the amount that would be recovered over the remaining life of the qualified costs using conventional financing methods and that the financing order is consistent with the standards in subsection (2), the commission shall issue a financing order to allow the utility to recover qualified costs. (2) In a financing order, the commission shall ensure all of the following: (a) That the proceeds of the securitization bonds are used solely for the purposes of the refinancing or retirement of debt or equity. (b) That securitization provides tangible and quantifiable benefits to customers of the electric utility. (c) That the expected structuring and expected pricing of the securitization bonds will result in the lowest securitization charges consistent with market conditions and the terms of the financing order. (d) That the amount securitized does not exceed the net present value of the revenue requirement over the life of the proposed securitization bonds associated with the qualified costs sought to be securitized. (3) The financing order shall detail the amount of qualified costs to be recovered and the period over which the securitization charges are to be recovered, not to exceed 15 years. (4) A financing order is effective in accordance with its terms, and the financing order, together with the securitization charges authorized in the order, shall be irrevocable and not subject to reduction, impairment, or adjustment by further action of the commission, except as provided under section 10k(3). (5) Stocks, bonds, notes, or other evidence of indebtedness issued under a financing order of the commission shall be binding in

4 In re Michigan Gas Utilities Co, MPSC Case No. U-7484, Opinion & Order dated 8-30-83, p. 10, and In re Detroit Edison Co, MPSC Case No. U-8030-R, Opinion & Order dated 7-9-87, pp. 16-17. 5 Woodin v Durfee, 46 Mich 424, 427; 9 NW 457 (1881). Accord, Yonkus v McKay, 186 Mich 203, 211; 152 NW 1031 (1915), and Cuttle v Concordia Mut Fire Ins Co, 295 Mich 514,519; 295 NW 246 (1940). 6 S C Gary, Inc v Ford Motor Co, 92 Mich App 789, 803-804; 286 NW 2d 34 (1979).

7

accordance with their terms notwithstanding that the order of the commission is later vacated, modified, or otherwise held to be invalid in whole or in part. (6) The commission shall after an expedited contested case proceeding issue a financing order or an order rejecting the application for a financing order no later than 90 days after the electric utility files its application. (7) A financing order is only subject to rehearing by the commission on the motion of the applicant for securitization. (8) Notwithstanding any other provision of law, a financing order may be reviewed by the court of appeals upon a filing by a party to the commission proceeding within 30 days after the financing order is issued. All appeals of a financing order shall be heard and determined as expeditiously as possible with lawful precedence over other matters. Review on appeal shall be based solely on the record before the commission and briefs to the court and shall be limited to whether the financing order conforms to the constitution and laws of this state and the United States and is within the authority of the commission under this act. (9) At the request of an electric utility, the commission may adopt a financing order providing for retiring and refunding securitization bonds if the commission finds that the future securitization charges required to service the new securitization bonds, including transaction costs, will be less than the future securitization charges required to service the securitization bonds being refunded. On the retirement of the refunded securitization bonds, the commission shall adjust the related securitization charges accordingly. (10) The commission shall have the authority to retain financial or legal services to assist in issuance of a financing order and to require the electric utility to pay the cost of the services. The payments shall be included as qualified costs defined in section 10h(g).

As noted above, MCL 460.10i requires the Commission to find that the expected

structuring and expected pricing of the securitization bonds will result in the lowest

securitization charges consistent with market conditions and the terms of the

financing order. It also requires the Commission to find that customers will

receive tangible and quantifiable benefits from securitization using a net

present value analysis.

8

The testimony and exhibits of AG witness Mr. Coppola, including an

appendix of his qualifications, cover 87 pages and the AG’s eight hearing room

exhibits are comprised of 11 pages. Rather than reiterating the testimony and

exhibits in this brief, it is incorporated in its entirety and will be referenced when

applicable. Failure to reference a certain portion of testimony or exhibit does not

indicate abandonment of that issue. In determining the qualified costs and

reasonableness, the Attorney General’s direct witness and this brief provide the

necessary testimony to satisfy MCL 460.10i.

A. Qualified Costs In total, DTE proposes to issue approximately $184 million in securitized

bonds. Ex. A-8. This includes financing the retirement of the River Rouge plant

and tree trimming costs for $177.5 million, plus forecasted securitization and bonds

issuance costs of $6.5 million, which add to the $184 million. In his testimony, Mr.

Coppola described how DTE arrived at these amounts and then proposed specific

changes and alternatives to maximize the benefit to customers from the

securitization of qualified costs and the resulting reduction in rate base, as well as

the reduction in the cost of capital and the return on rate base. 2 Tr 279-92. All of

Mr. Coppola’s discussion and argument is incorporated here by reference. The AG

believes that the securitization process can be valuable where it adequately

considers the ratepayers who pay the utilities’ bills and where the decisions made

incorporate all possible customer benefits.

9

Mr. Coppola broke the the Qualified Costs section of his testimony into three

parts: A. River Rouge & Tree Trimming Costs, B. Bonds Issuance Costs, and C.

Securitized Qualified Costs.

1. A. River Rouge & Tree Trimming Costs

Mr. Coppola addressed DTE’s request to securitize $184.0 million of River

Rouge, tree trimming, and other qualified costs. 2 Tr 280-86. After discussion and

analysis he concluded, and the AG argues, that the Company has not made a

compelling case that reducing the total qualified costs of $234,000,000 for related

deferred taxes is in the best interest of its customers. Instead, the securitization of

a lower amount net of the deferred taxes is a more costly alternative to customers

and the proposal to recover the portion of qualified costs pertaining to the deferred

taxes through an additional and separate surcharge is neither advantageous to

customers nor necessary. It should be noted that Staff, MEC, and the AG are

aligned on this issue and presented similar arguments in their witnesses’ direct

testimony.

In rebuttal testimony, Company witness Uzenski disagreed with Mr.

Coppola’s testimony, as well as that of Staff and MEC, regarding how deferred taxes

should be handled. 2 Tr 43-52. Specifically, her opinion is that deferred taxes

should be deducted from the net book asset amount of the River Rouge plant and

the tree trimming regulatory asset costs to arrive at a net securitization amount to

be financed. 2 Tr 43. She argued that doing so would avoid “inappropriately and

inequitably reducing equity by a larger amount than the actual equity supporting

10

the River Rouge asset,” “is the lowest cost option for customers, and is consistent

with prior Commission orders and treatment approved by the Commission.” 2 Tr

43.

Conversely, Mr. Coppola, along with witnesses for both Staff and MEC,

propose that deferred taxes should not be deducted from the River Rouge plant and

tree trimming regulatory asset amounts and that the gross amount should be

securitized and financed. See e.g., 2 Tr 283-86. In part, this is because the “net of

tax” method increases costs on customers. In rebuttal, Ms. Uzenski characterizes

this assertion from Mr. Coppola and MEC witness Jester as “mathematically

accurate” but “unsound.” 2 Tr 44. She argues that their analyses are flawed

because of an assumption that deferred taxes are not a current source of financing

for River Rouge and tree trimming and should be excluded from cost comparisons.

2 Tr 44. She then attempts to draw a distinction between Staff’s position, stating

that Staff includes deferred taxes in the level of equity supporting River Rouge but

then asserts that DTE failed to provide evidence that River Rouge debt and equity

levels are lower because of cash flows provided by deferred income taxes. 2 Tr 45.

Ms. Uzenski abandons discussion of the tree trim surge in this part of her rebuttal,

only to bring it back in later.

The problem, as Mr. Coppola, MEC, and Mr. Nichols for Staff point out, is

that DTE can draw no link between specific financing using the deferred taxes and

a reduction of debt and equity levels at River Rouge or in the tree trimming asset.

On page 4 of her rebuttal, Q9, Ms. Uzenski herself admits that deferred taxes are

11

not tied to specific assets. 2 Tr 46. Later, however, she states that a specific

deferred tax amount should reduce plant and regulatory asset balances in

determining the amount to be securitized. 2 Tr. 47-48. With no ability to quantify

any level of deferred taxes tied to specific assets, DTE’s argument fails.

In response to AGDE-3.59, which is included as Ex. AG-12, Ms. Uzenski

stated that the River Rouge deferred tax balance will fully unwind in 2036, or 15

years from now. She also stated that the deferred tax liability will unwind over the

life of the amortization period, meaning either five or seven years, depending on

which proposal the Commission accepts. Ex. AG-12. If those deferred taxes are not

being paid off at the time of the securitization transactions, as Ms. Uzenski states,

then the AG argues that DTE should simply let those deferred taxes unwind

naturally, in the normal course of business. DTE can then include the declining

deferred tax liabilities in DTE’s capital structure in future rate cases, so there is no

need for DTE to impose a surcharge on customers to collect deferred taxes that

remain on the books of the Company and will unwind normally.

As to Ms. Uzenski’s conclusion on page 6 of her rebuttal, that the net of tax

approach is the lowest cost option for customers, that is only true if one disregards

the benefits of reducing the debt and equity capital in the capital structure for the

higher amount of securitized bonds that would be raised by not deducting deferred

taxes. Ex. AG-2. As already noted, DTE is unable to demonstrate what specific

portion of deferred taxes, if any, is related to River Rouge and the tree trim surge.

12

Exhibit AG-2 lays out the $11.4 million customer benefit of the AG’s securitization

proposal.

Importantly, in the Commission’s most recent securitization case, U-20889,

the Commission saw fit to securitize the full net book value of specific Consumers

Energy assets, without a reduction for deferred taxes. Ms. Uzenski argues that the

Commission should ignore its most recent order and look to U-12478 for a case

where the Commission “approved the net of tax approach.” 2 Tr 49-50. However, U-

12478 is a case from more than two decades ago, which Ms. Uzenski was not

involved in. 2 Tr 67-73. The Commission should adhere to the approach it endorsed

only five months ago.

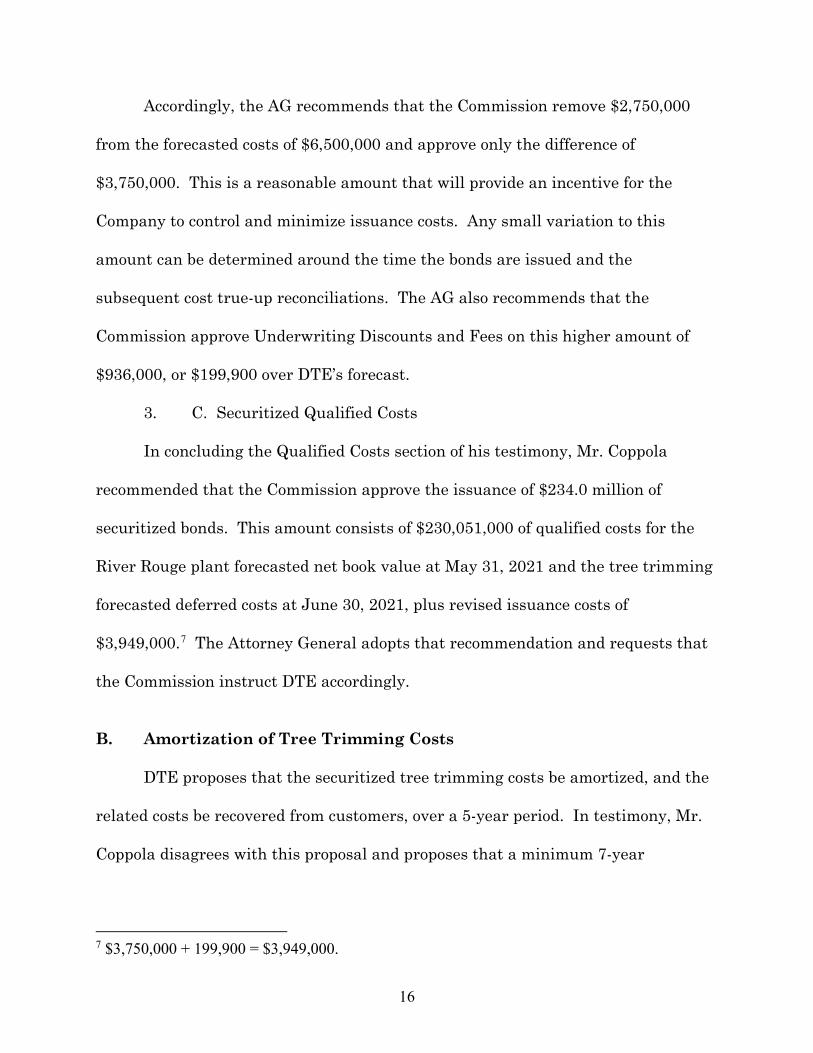

Accordingly, the AG recommends that the Commission order the Company to

securitize $230,051,000 of qualified costs plus issuance costs as this will provide the

biggest benefit to ratepayers.

2. B. Bonds Issuance Costs

Mr. Coppola addressed DTE’s forecasted issuance costs of $6.5 million,

recommending that the Commission remove $2,750,000 from the forecasted costs of

$6,500,000 and approve only the difference of $3,750,000. He also recommended a

corresponding adjustment to the Underwriting Discounts and Fees, increasing them

by $199,900 over the Company’s forecast to account for the higher qualified costs

proposed in his testimony. 2 Tr 286-91. The AG adopts both recommendations.

In rebuttal, Company witness Mr. Solomon discusses and disagrees with each

of Mr. Coppola’s recommendations that the Commission approve lower amounts for

13

certain upfront costs for the securitization. 2 Tr 110-12. First, he disagrees with

Mr. Coppola’s testimony that legal costs should be set at $2 million, rather than the

Company’s $4 million proposal. 2 Tr 110-11. He compares the legal work to be

done in this case to the legal work done in the Company’s prior securitization case,

U-12478, and draws the conclusion that the amount of work is similar. 2 Tr 111.

U-12478 involved the securitization of $1.8 billion of stranded generation costs

pertaining to the Fermi 2 nuclear plant, which is a much larger scale than the

amounts DTE is seeking to securitize in this case. Ex. A-8. Mr. Solomon also

provided no evidence that he was involved in U-12478, what the effect of inflation

over 20 years, which he refers to, has been, or evidence that the Company

attempted to shop around to lower the legal costs it is asking customers to pay for.

In discovery, DTE was asked to provide the detailed components by law firm

comprising the $4 million of legal costs it estimated for the securitization

transaction. Ex. AG-13. In response, the Company identified some of the law firms

and provided a total amount of $3.3 million, with no detailed components as

requested. Ex. AG-13. Accordingly, DTE failed to provide any detailed support for

the $4 million. DTE was also asked to explain how many law firms were

interviewed and how many proposals were received for the legal services needed for

this transaction. Ex. AG-14. The Company refused to provide the information and

referenced DR AGDE-1.18c, which is included in Ex. AG-4. Ex. AG-14. In DR

AGDE-1.18c, DTE refused to provide similar information and or stated that the

Company failed to retain pertinent records. Ex. AG-4. The conclusion to be drawn

14

from these responses is that the Company did not shop around for legal services and

instead engaged law firms without comparison of services and fees. DTE provided

no information in this case to adequately explain why legal costs for a case with an

amount of securitized bonds less than 15% of the prior securitization case, U-12478,

would necessitate close to twice the legal costs.

Regarding rating agency fees, Mr. Solomon disagreed with Mr. Coppola’s

proposed removal of $400,000 from the Company’s proposal. 2 Tr 111. He stated

that the estimated fees of $600,000 reflect the minimum fees charged by the Rating

Agencies. 2 Tr 111. In discovery, the AG asked the Company to provide the

calculations and other support for the $600,000. Ex. AG-15. In its response DTE

refused to provide the information, instead stating that based on its own witness’

experience, the rating agency cost “appears reasonable.” Ex. AG-15. The

Commission should not accept such proof as reasonable, without a more objective

source of verification. Accordingly, the Company failed to provide adequate support

for the $600,000 or to rebut Mr. Coppola’s proposal.

Mr. Solomon also disagreed with Mr. Coppola’s recommendation to remove

the estimated $150,000 in SPE Organization costs. 2 Tr 111-12. As the basis for

his estimate, Mr. Solomon referenced the amount provided by Consumers Energy in

Case Nos. U-17473 and U-20889 and attached Ex. A-33. 2 Tr 111-12. Pertinently,

those were forecasted costs and not actual costs. In testimony filed by Mr. Coppola

in U-20889, he determined that Consumers actually spent only $7,000 on SPE

Organization costs in U-17473. U-20889 Direct Testimony of Sebastian Coppola, p.

15

24. Therefore, Mr. Solomon’s rebuttal in this case is based on costs that were later

shown to be objectively inflated. There is no reason to continue to inflate such costs

in this and future cases.

Mr. Solomon then disagreed with Mr. Coppola’s proposed adjustment to the

estimated costs to be incurred by the Commission in conjunction with the

securitization proceedings. 2 Tr 112. He stated that his estimate of $200,000 was

based on communication received from the Commission’s external counsel. 2 Tr

112. In discovery, the AG asked for documentation of that communication with the

Commission’s external counsel to support the $200,000 estimated cost. Ex. AG-16.

In response, DTE failed to provide the requested information and instead provided

a circular reference to previous testimony and Ex. A-33, which both contained the

same estimate without any support. Accordingly, DTE has failed to provide

adequate support for the $200,000 estimated Commission cost.

In Exhibit A-33, which was filed with rebuttal, Mr. Solomon calculated the

upfront securitization costs as a percentage of the transaction amount. Pertinently,

the $6.5 million upfront costs represent about 3.5% of the total bonds securitization

amount to be issued, which is nearly double the percentages from the costs of other

securitization transactions to which Mr. Solomon compares them. The AG argues

that this, and in fact the numerous discrepancies between this case and the others

listed, which are apparent across the exhibit, reinforce Mr. Coppola’s testimony and

the AG’s contention that the $6.5 million estimate is excessive.

16

Accordingly, the AG recommends that the Commission remove $2,750,000

from the forecasted costs of $6,500,000 and approve only the difference of

$3,750,000. This is a reasonable amount that will provide an incentive for the

Company to control and minimize issuance costs. Any small variation to this

amount can be determined around the time the bonds are issued and the

subsequent cost true-up reconciliations. The AG also recommends that the

Commission approve Underwriting Discounts and Fees on this higher amount of

$936,000, or $199,900 over DTE’s forecast.

3. C. Securitized Qualified Costs

In concluding the Qualified Costs section of his testimony, Mr. Coppola

recommended that the Commission approve the issuance of $234.0 million of

securitized bonds. This amount consists of $230,051,000 of qualified costs for the

River Rouge plant forecasted net book value at May 31, 2021 and the tree trimming

forecasted deferred costs at June 30, 2021, plus revised issuance costs of

$3,949,000.7 The Attorney General adopts that recommendation and requests that

the Commission instruct DTE accordingly.

B. Amortization of Tree Trimming Costs DTE proposes that the securitized tree trimming costs be amortized, and the

related costs be recovered from customers, over a 5-year period. In testimony, Mr.

Coppola disagrees with this proposal and proposes that a minimum 7-year

7 $3,750,000 + 199,900 = $3,949,000.

17

amortization, financing, and cost recovery period for the securitized tree trimming

qualified costs is more appropriate. 2 Tr 292-94.

In rebuttal, Mr. Serna disagrees with Mr. Coppola’s proposal. 2 Tr 243-47.

Specifically, he continues to advocate for a 5-year amortization period, rather than a

7-year period. In Case No. U-20162, Company witness Heather Rivard made the

proposal for a 7-year surge program, which involved increased spending for tree

clearing in order to get to a 5-year routine clearing cycle. U-20162 Direct Testimony

of Heather Rivard, 3 Tr 210-11. In that case, Ms. Rivard proposed that the cost of

the 7-year surge be deferred and securitized at a later date. U-20162 3 Tr 235-36.

Specifically, she wrote,

Q. How does the Company expect to recover the program costs above base rates? A. The Company proposes to defer the incremental cost above base rates of $410 million and amortize it over 14 years as described by Company Witness Uzenski. Q. Why is the Company proposing to defer and amortize the costs?

A. As previously discussed, the surge investment is intended to lower future reactive costs that would be incurred given the current state of vegetation near or on the distribution system. The deferral recognizes the long-term nature of the program. As the costs are incurred up front and the full savings will not be realized until after the program has matured, the deferral of the incremental costs and subsequent amortization provide a better matching of costs with the anticipated savings, minimizing the cost impact to customers by aligning the increased cost with the realization of savings. Assuming securitization of the regulatory asset, amortization of the deferred costs over 14 years provides a larger net present value benefit to customers than shorter amortization periods and is consistent with the recommendation supported by Witness Solomon. [emphasis added]

U-20162 Direct Testimony of Heather Rivard, 3 Tr 235-36.

18

Company witnesses Solomon, Uzenski, and Stanczak all repeated the same

14-year securitization and amortization proposal in their testimony in U-20162.

And in U-20162, the Commission approved the 7-year surge program, the cost

deferral, the 14-year amortization period, and the securitization proposal made by

the Company. U-20162 Order pp. 79-81. However, in this securitization case Mr.

Serna now proposes a 5-year securitization and amortization period for the Tree

Trimming cost spent to date, but makes no attempt to reconcile this different

position with that presented by the Company in U-20162. The AG argues that it

would be unreasonable for the Commission to accept DTE’s position in this case as

it diverges widely from a position recently espoused by the Company and would

clearly, as argued by the Company in U-20162, create a significantly larger cost

burden on customers up front.

Beginning on the first page of his rebuttal and continuing onto the next, Mr.

Serna states that “[t]he Company believes that” the securitization amortization

period should match the underlying life of the asset. 2 Tr 243-44. He defines the

life of the asset as the ultimate 5-year ongoing tree trimming cycle, which would be

after the 7-year surge program is completed. 2 Tr 243-44. This is directly at odds

with the Company’s “belief” in U-20162 in a securitization amortization period of

14-years. There is no attempt to reconcile this discrepancy, or mention of Ms.

Rivard’s U-20162 testimony, which discussed the long-term nature of the program

and that a longer deferral and amortization period (14 years) will better align costs

with the realization of savings.

19

Also in rebuttal in this case, Mr. Serna states that a 5-year amortization

period would lessen the impact on customer bills, because the Company plans to do

two more securitization rounds. 2 Tr 244. The Commission should not make

decision based on what a utility may do. Utilities in Michigan are consistently

involved in cases that have impacts on ratepayer bills, the result of which is often to

stack another surcharge on an existing bill or raise the rates of an existing bill.

Assuming the same total amount to be amortized, it is undisputed that stretching

the securitization and amortization period over a longer period of time, such as the

Company argued in U-20162, will lessen the up-front impact on customers in this

case. If DTE applies a longer amortization period to future securitizations it will

similarly lessen the monthly impact to customers of each of those transactions. Mr.

Serna’s hypothetical, which the Commission should ignore, also states that

customers may “face three tree trimming securitization surcharges over a period of

three years.” 2 Tr 244. If the Company plans to file securitizations that quickly,

the pancaking Mr. Serna claims to be concerned about will occur whether a 5-year

or a 7-year amortization period is applied. Under Mr. Serna’s proposal, unless DTE

waits another 5 years before filing its next securitization case, some concurrent

surcharges will occur.

Accordingly, the AG recommends that the Commission deny the Company’s

proposal for a 5-year amortization and cost recovery period and instead approve a 7-

year period. This is consistent with the position DTE has taken in past cases and

more appropriately spreads out known costs on customers.

20

C. Net Present Value Test As laid out in his testimony, Mr. Coppola was unable to perform an updated

Net Present Value (NPV) test in conjunction with his higher proposed securitization

amount and longer amortization period for tree trimming costs. 2 Tr 294-96.

Without the ability to properly validate billing information, Mr. Coppola proposed

that the Commission reject DTE’s securitization application. 2 Tr 296.

In rebuttal, DTE witness Mr. Lunde argued against Mr. Coppola’s

conclusions. Specifically, he responded to Mr. Coppola’s concerns about Citigroup’s

unwillingness to share its model and its involvement in this case as both financial

advisor and lead underwriter. 2 Tr 170.

As an employee of Citigroup, Mr. Lunde was hired as an advisor to assist

DTE in structuring this securitization. 2 Tr 117-19. In rebuttal he discussed

Citigroup’s model, stating that Citigroup has developed a very detailed and complex

cash flow model to calculate the case requirements and customer billings from the

securitization transaction, the information for which is displayed in Ex. A-6. 2 Tr

170-71. Exhibit A-6 is a 6-page exhibit showing both the River Rouge and Tree

Trimming securitization transactions with both expected and breakeven cases. The

AG’s issue comes on page one, in column G, where the AG’s expert requested a copy

of the model to validate the specific calculations Mr. Lunde performed to arrive at

the amounts DTE Electric customers will ultimately pay for the securitization.

Unfortunately for customers, Citigroup refused to provide a copy of the model

for the AG to perform any sort of validation of customer billings, and as the AG

21

understands, not even DTE was able to audit the model or validate calculations in

any detail, despite payment of a significant fee to Citigroup. 2 Tr 171-72. The fact

that Citigroup does not typically give the model to others does not mean that it

should not be provided in this case to allow calculations to be validated. The AG

argues that it is neither reasonable nor responsible for all parties to this case to

accept the calculations performed by Citigroup without detailed verification or any

chance to otherwise understand them.

The AG wants to strike an appropriate balance regarding these issues. While

she is generally supportive of the securitization process, the inability to properly

validate information in DTE’s filing is a serious concern. DTE could not even

provide assurance that the Company itself was able to thoroughly review the

relevant model for reasonableness. The Company’s discussion in rebuttal did little

to assuage these concerns. The AG recommends that the Commission carefully

consider the lack of available information and respond accordingly. That may

include instructing DTE to conduct future securitization proceedings in a different

manner or rejecting certain portions of this securitization application as

unsupported.

D. Financial Advisor Mr. Coppola’s testimony raised issues regarding Citigroup’s involvement in

this transaction as both financial advisor and underwriter. 2 Tr 297-98. He

22

recommended that in future securitization transactions DTE should separate the

role of the financial advisor from the underwriters. 2 Tr 297.

In rebuttal, Mr. Lunde and Mr. Solomon argue that the Commission should

ignore Mr. Coppola’s concerns. 2 Tr 113, 172. However, as lead underwriter,

Citigroup stands to take the largest portion of the bonds to be sold and earn the

largest portion of the underwriting fees. In this transaction, the total underwriting

fees are about $736,000. 2 Tr 291. That means that Citigroup receives the majority

of this amount, plus an additional amount as the financial advisor. On page 4 of his

rebuttal, Mr. Lunde states that a competitive bidding process would not deliver the

desired outcome, because securitization is a specialized activity and that being both

a financial advisor and lead underwriter is beneficial, as there are few

knowledgeable market players. 2 Tr 173.

Having the same party play two separate roles on the same major project

leads to concerns of conflicts of interest and self-dealing. Pages 3 and 4 of Ex. A-7

show a list of financial institutions that specialize in securitization transactions.

Many of those financial institutions could have taken on the role of financial advisor

in this case. Therefore, the role of financial advisor and underwriter could be

separated to avoid the situation where conflicts of interest may arise.

The AG argues that transparency and accountability are two indispensable

tenets of cases involving ratepayer money, which the Commission oversees. There

are serious, common-sense concerns about conflicts of interest when one party acts

as both a financial advisor and underwriter on one project. As noted, other

23

financial institutions exist that can provide a second party to these transactions.

Accordingly, the AG recommends that the Commission direct the Company that in

future securitization transactions it should separate the role of the financial advisor

from the underwriters. Such separation will protect customers by utilizing the

competitive process and arm’s length dealing between parties.

E. Retirement of Debt and Equity Capital

In testimony, Mr. Coppola provides a summary of DTEs position on the

proportion of debt and equity capital that should be removed from DTE’s capital

structure. 2 Tr 298. After an analysis of the Company’s proposal, Mr. Coppola

recommends that the Commission order the Company to apply the proceeds from

the securitization bonds to retire equal amounts of long-term debt and common

equity from the capital structure, with no adjustment to the short-term debt. 2 Tr

298-302.

In rebuttal, Mr. Solomon disagrees with Mr. Coppola’s analysis. 2 Tr 108-09.

Specifically, he argues that the Company should only have to retire short-term debt

with proceeds from the Tree Trim Surge qualified costs, rather than retiring long-

term debt and equity. 2 Tr 109.

Mr. Solomon states that the Company does not identify specific assets to be

financed with short-term debt or long-term debt, and instead the Company manages

its balance sheet in total. 2 Tr 113. However, on page 6 of his direct testimony, he

states that the proceeds from the securitization of the tree trimming costs should be

24

applied to reduce short-term debt because those costs were financed with short-term

debt. 2 Tr 88. These statements contradict each other. On the one hand, Mr.

Solomon is saying that the Company does not finance specific assets with short-

term debt, and on the other, he is implying that it did just that by retiring only

short-term debt with the securitization proceeds. The AG argues that the Company

cannot have it both ways. This undercuts Mr. Solomon’s arguments in this area.

On lines 24 and 25 of page 6 of Mr. Solomon’s rebuttal then, and into the next

page, he states that the short-term debt will grow to be in excess of the $116.2

million later in the year. 2 Tr 113-14. He also states that this higher short-term

debt will finance other working capital needs such as pension funding costs and

capital expenditures. 2 Tr 114. However, he did not provide what the short-term

debt will grow to later in the year and what it will be comprised of. He did provide

a balance for short-term debt of $78 million at of the end of March 31, 2021 in

response to DR AGDE-1.15b. Ex. AG-8. Assumedly, this amount also includes the

funding of the same and perhaps other working capital needs, in addition to any

amounts that may pertain to tree trimming costs. Therefore, there is no direct

evidence that tree trimming costs were financed with short-term debt. The

Commission’s approval of a short-term debt rate to compensate the Company for the

differed costs is not evidence that the Company actually financed those costs with

short-term debt. 2 Tr 109.

Accordingly, the AG adopts Mr. Coppola’s argument and recommendation

and recommends that the Commission order the Company to apply the proceeds

25

from the securitization bonds to retire equal amounts of long-term debt and

common equity from the capital structure, with no adjustment to the short-term

debt. This is shown in Ex. AG-1 and will provide the maximum benefit to

ratepayers.

F. Bill Credit In testimony, Mr. Coppola discusses what should be included in the

calculation of the revenue requirement savings from the retirement of River Rouge.

2 Tr. 302-03. He recommends that the Commission order the Company to

recalculate the Power Supply Bill credit for each rate schedule, based on the

$41,856,000 reduction in the revenue requirement as shown in Exhibit AG-10.

In rebuttal, Mr. Serna states that Mr. Coppola is incorrect. 2 Tr 244-47. He

states that the intent of the interim bill credit is to only reflect the removal of the

net book value from rate base after the securitization of those costs. 2 Tr 244-45.

He argues that changes in the level of O&M expense or property tax expense should

be addressed in a general rate case. 2 Tr 246. The AG takes issue with this

approach to ratepayer monies. Once River Rouge ceases to operate, O&M costs will

necessarily be less than when it was operating. While those costs are unlikely to go

all the way to zero, there will no longer be a need for the same amount of personnel,

and maintenance costs should be greatly reduced as there will no longer be

operating generation equipment to be monitored and fixed. However, Mr. Serna’s

rebuttal takes the position that the Company should not refund to customers those

lower operating costs through the bill credit along with the net book value. His

26

position is that the Company should retain the revenue requirement set in the last

rate case that pertains to operating costs at River Rouge that it is no longer

incurring after shutting down the power plant in May 2021, and that the revenue

requirement need not be reset until the next rate case.

Mr. Serna also supported this view in discovery. In response to AGDE-3.52,

Mr. Serna noted that the forecasted O&M costs for the River Rouge plant included

in base rates were $7.6 million. Ex. AG-18. And in response to AGDG 3.53 a and b

he confirmed that River Rouge will cease operations in May 2021. Ex. AG-19. In

response to AGDE-3.53ciii he stated that, except for a few months past May 2021,

once decommissioning and dismantling of the plant begins later in 2021, any costs

incurred at the site will be charged to the depreciation reserve and not to O&M

expense. Ex. AG-19. So, sometime during the summer or fall of 2021, the Company

will stop incurring most O&M costs at the site, but DTE wants to continue

recovering those expenses in rates until rates from the next rate case go into effect.

Under this setup the Company stands to realize a potential windfall of

millions of dollars. It is unclear when DTE Electric’s next rate case will be, and it is

doubtful that that filing will include an adjustment retroactive to May 2021 to

capture the costs that the Company did not incur from that time to the beginning of

the next projected test year. This is neither a fair nor reasonable outcome for

customers and would simply work to charge them for O&M that is not taking place.

27

The AG continues to recommend that the Commission order the Company to

recalculate the Power Supply Bill credit for each rate schedule, based on the

$41,856,000 reduction in the revenue requirement as shown in Exhibit AG-10.

G. Deferred Taxes Surcharge

In the final section of his testimony, Mr. Coppola summarized his conclusion

and recommendation, which the AG adopts here, regarding DTE’s proposed

surcharge to recover deferred taxes related to River Rouge and tree trimming

deferred costs. 2 Tr 304. The AG proposes that those deferred taxes remain on the

books of the Company until they unwind and are removed in the normal course of

business, once the book to tax timing differences are resolved. Accordingly, there is

no need for DTE to recover the deferred tax amounts through a surcharge on

customer bills. The AG recommends that the Commission reject the Company’s

deferred tax surcharges shown in Exhibits A-22 and A-25.

II. Conclusion and Relief Sought

For the reasons stated above and in her expert witness’s direct testimony and

all of her exhibits, the Attorney General recommends that the Commission adopt

her adjustments and recommendations.

28

Respectfully submitted, Dana Nessel Attorney General Joel B. King (P81270) Assistant Attorney General Special Litigation Division PO Box 30755 Lansing, MI 48909 517-335-7627