Page 1

Maybank Asset Management Sdn Bhd

(421779-M)

Level 12 Tower C

Dataran Maybank

No.1 Jalan Maarof

59000 Kuala Lumpur

Telephone +603 2297 7888

Facsimile +603 2297 7998

www.maybank-am.com

MAYBANK GLOBAL BOND FUND

Interim reportFor the financial period ended 31 December 2017

Page 2

CONTENT PAGE

Manager's report 1 - 9

Trustee's report 10

Statement by Manager 11

Unaudited statement of comprehensive income 12 - 13

Unaudited statement of financial position 14

Unaudited statement of changes in equity 15

Unaudited statement of cash flows 16

Notes to the financial statements 17 - 44

MAYBANK GLOBAL BOND FUND

Page 3

MAYBANK GLOBAL BOND FUND

Manager’s report for the 6 months financial period ended 31 December 2017

A. Fund Information

1. Name of the Fund

Maybank Global Bond Fund (the “Fund”)

2. Type of Fund

Income

3. Category of Fund

Feeder fund

4. Duration of the Fund

The Fund is an open-ended fund

5. Fund launch date

4 November 2013

6. Fund’s investment objective

7. Fund distribution policy

8. The Fund’s performance benchmark

JP Morgan Global Government Bond Index

9. Has the Fund achieved its objective?

10. The Fund's investment policy and principal investment strategy

For the period under review ended 31 December 2017, the Fund delivered a total return of -4.23% vis-à-

vis the Target Fund's total return of -3.70% (in Ringgit Malaysia ("RM") terms), and the benchmark JP

Morgan Global Government Bond Index's total return of -1.60% (in RM terms).

The Fund invests at least 95% of the Fund’s Net Asset Value ("NAV") in the Class A (Mdis) Singapore

Dollar (“SGD”) – H1 shares of the Target Fund, a sub-fund of the Franklin Templeton Investment Funds,

managed by Franklin Advisers, Inc. (the "Target Fund Manager"). The remaining 2% to 5% of the Fund’s

NAV are invested in liquid assets. The base currency of the Target Fund is in United States Dollar

(“USD”), whereas the shares of the Target Fund in which the Fund invests in are denominated in SGD.

Note : (Mdis) is a share class which distributes income (whenever available) on a monthly basis and

SGD-H1 refers to SGD hedged share class which means the currency of the share class is hedged

against the USD.

The objective of the Fund is to maximise investment returns by investing in the Templeton Global Bond

Fund ("Target Fund").

Distribution, if any, will be made from the realised income of the Fund. Distribution will be on a quarterly

basis (subject to availability of income).

1

Page 4

MAYBANK GLOBAL BOND FUND

Manager’s report for the 6 months financial period ended 31 December 2017 (cont'd)

A. Fund Information (cont'd)

11. Net income distribution for the 6 months financial period ended 31 December 2017

12. Breakdown of unitholdings by size

Fund size

As at 31 December 2017, the size of the Fund stood at 3,605,740 units.

Breakdown of unitholdings as at 31 December 2017

No. of No. of

unitholders % units ('000) %

5,000 units and below 1 25.00 *1 0.03

5,001 to 10,000 units - - - -

10,001 to 50,000 units - - - -

50,001 to 500,000 units 1 25.00 **56 1.55

500,001 units and above 2 50.00 **3549 98.42 Total 4 100.00 3,606 100.00

* Represents 1,129 units held by Maybank Asset Management Sdn Bhd (the "Manager")

** Represent units held under an Institutional Unit Trust Agent (“IUTA”)

B. Performance Review

1. Key performance data of the Fund

Category 01.07.2017 01.07.2016 01.07.2015 01.07.2014

to to to to

31.12.2017 30.06.2017 30.06.2016 30.06.2015

% % % %

Collective investment

scheme - foreign 96.25 97.94 95.05 97.64

Cash and other net

assets (%) 3.75 2.06 4.95 2.36

Total (%) 100.00 100.00 100.00 100.00

NAV (RM’000) 3,633 4,608 6,417 8,547

Units in circulation (‘000) 3,606 4,375 6,569 8,210

NAV per unit (RM) 1.0076 1.0534 0.9768 1.0411

Highest NAV per unit (RM) 1.0722 1.1233 1.0921 1.0695

Lowest NAV per unit (RM) 1.0077 0.9553 0.9257 0.9970

Annual return (%) (1)

- Capital growth (%) (6.02) 7.84 (6.17) 1.76

- Income distribution (%) 1.90 4.51 4.42 3.34

Total return (%) (4.23) 12.70 (2.02) 5.16

Unitholdings

The Fund did not make a distribution for the 6 months financial period ended 31 December 2017.

2

Page 5

MAYBANK GLOBAL BOND FUND

Manager’s report for the 6 months financial period ended 31 December 2017 (cont'd)

B. Performance Review (cont'd)

1. Key performance data of the Fund (cont'd)

Category 01.07.2017 01.07.2016 01.07.2015 01.07.2014

to to to to

31.12.2017 30.06.2017 30.06.2016 30.06.2015

% % % %

Target fund (3.70) 16.04 (0.73) 6.15

Benchmark (1.60) 4.76 17.23 12.54

Distribution date

Quarter 1 - - 30.09.2015 30.09.2014

Quarter 2 - 31.12.2016 31.12.2015 -

Quarter 3 - 31.03.2017 - -

Quarter 4 - 30.06.2017 - 30.06.2015

Gross/net distribution per unit (sen)

Quarter 1 - - 2.50 2.00

Quarter 2 - 1.50 2.00 -

Quarter 3 - 1.25 - -

Quarter 4 - 2.00 - 1.40

Total - 4.75 4.50 3.40

Management Expense Ratio

("MER") (%) (2)

0.55 1.43 1.28 1.14

Portfolio Turnover Ratio

("PTR") (times) (3)

0.13 0.31 0.35 1.01

31.12.2017 30.06.2017 30.06.2016 30.06.2015 30.06.2014

% % % % %

Annual total return (4.23) 12.70 (2.02) 5.16 2.30

Note:(1)

(2)

(3)

The Fund’s MER decrease from 1.43% to 0.55% in the current financial period ended 31 December

2017 due to lower average expenses as compared to previous financial year.

Actual return of the Fund for the financial period is computed based on the daily average NAV per

unit, net of Manager's and Trustee's fee.

Investors are reminded that past performance of the Fund is not necessarily an indicative of its future

performance and that unit prices and investment returns may fluctuate.

The Fund’s PTR decreased from 0.31 times to 0.13 times in the current financial period which was

mainly due to lower investing activities during the financial period ended 31 December 2017.

3

Page 6

MAYBANK GLOBAL BOND FUND

Manager’s report for the 6 months financial period ended 31 December 2017 (cont'd)

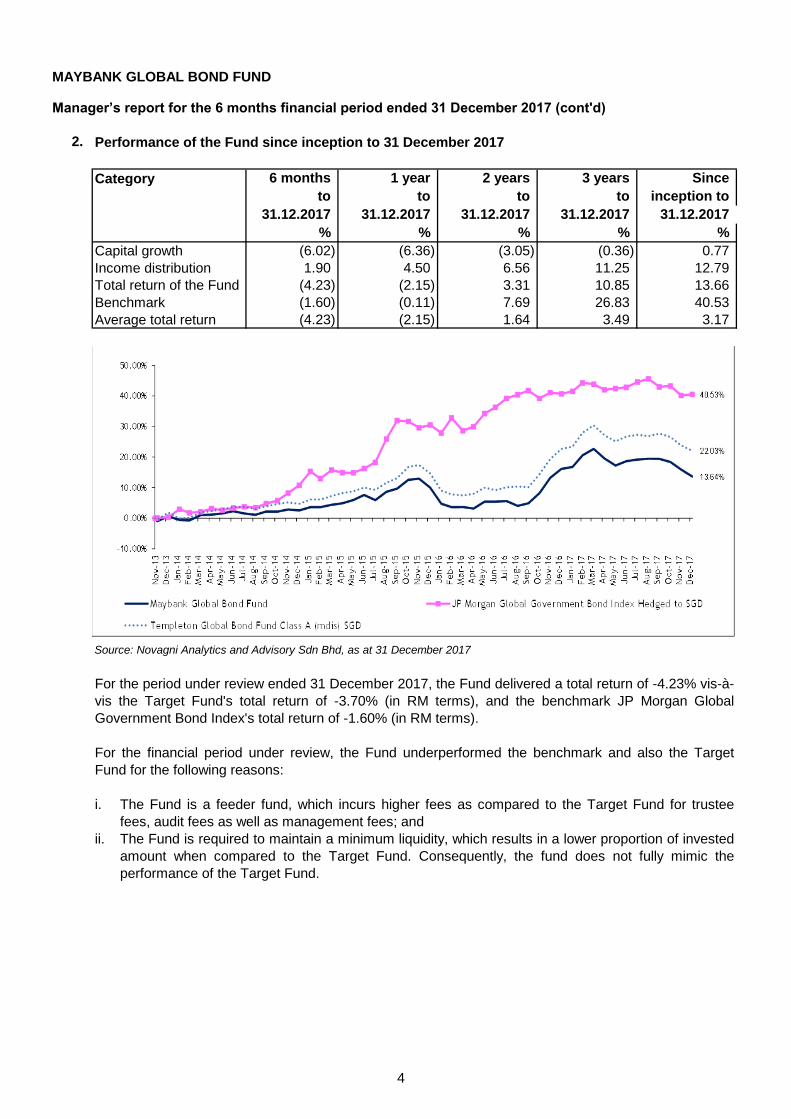

2. Performance of the Fund since inception to 31 December 2017

Category 6 months 1 year 2 years 3 years Since

to to to to inception to

31.12.2017 31.12.2017 31.12.2017 31.12.2017 31.12.2017

% % % % %

Capital growth (6.02) (6.36) (3.05) (0.36) 0.77

Income distribution 1.90 4.50 6.56 11.25 12.79

Total return of the Fund (4.23) (2.15) 3.31 10.85 13.66

Benchmark (1.60) (0.11) 7.69 26.83 40.53

Average total return (4.23) (2.15) 1.64 3.49 3.17

Source: Novagni Analytics and Advisory Sdn Bhd, as at 31 December 2017

i.

ii.

For the period under review ended 31 December 2017, the Fund delivered a total return of -4.23% vis-à-

vis the Target Fund's total return of -3.70% (in RM terms), and the benchmark JP Morgan Global

Government Bond Index's total return of -1.60% (in RM terms).

For the financial period under review, the Fund underperformed the benchmark and also the Target

Fund for the following reasons:

The Fund is a feeder fund, which incurs higher fees as compared to the Target Fund for trustee

fees, audit fees as well as management fees; and

The Fund is required to maintain a minimum liquidity, which results in a lower proportion of invested

amount when compared to the Target Fund. Consequently, the fund does not fully mimic the

performance of the Target Fund.

4

Page 7

MAYBANK GLOBAL BOND FUND

Manager’s report for the 6 months financial period ended 31 December 2017 (cont'd)

B. Performance Review (cont'd)

3. Basis of calculation made in calculating the returns:

An illustration of the above would be as follows:

Capital return = NAV per unit end / NAV per unit begin - 1

Income return = Income distribution per unit / NAV per unit ex-date

Total return = (1+Capital return) x (1+Income return) - 1

C. Market Review

The BOJ and ECB continued with their QE programs during the quarter as short-term yields in Japan and

the eurozone remained negative. We expect the euro and Japanese yen to weaken on widening rate

differentials with the US. Rising US Treasury yields should produce a more effective environment for the

BOJ to actively deploy additional monetary accommodation that weakens the yen. In Europe, we expect the

ECB to continue with monetary accommodation through 2017, as it has indicated. ECB President Mario

Draghi has indicated the ECB will announce a new schedule for additional QE tapering in October.

Nonetheless, Draghi continued to indicate that overall monetary accommodation is still needed for the near

term, with eventual policy normalizing still several quarters away.

A number of currencies strengthened against the US dollar during the third quarter, notably the Brazilian

real, Colombian peso, euro and Australian dollar. However, the US dollar broadly strengthened against a

number of global currencies during September, reversing the weakening trend that had persisted throughout

much of 2017. Europe largely remained in a state of optimism during the quarter, driven by the cyclical

upswing in eurozone growth as well as recent political refortifying since French President Emmanuel

Macron’s victory in May. However, Angela Merkel’s win in the German election in September came with new

uncertainties around forming a coalition.

The performance figures are a comparison of the growth/decline in NAV after taking into account all the

distributions payable (if any) during the stipulated period.

The US Federal Reserve ("Fed") kept rates unchanged during the third quarter 2017, while remaining on

track for a rate hike in December and announcing its intentions to begin unwinding its balance sheet in

October. Fed Chair Janet Yellen commented on the strength of the US economy and household spending,

while indicating that the committee expects inflation to stabilize around its 2% target over the medium term.

The comments appeared a bit more hawkish than markets had been expecting. Overall, we expect US

Treasury yields to continue rising as the Fed unwinds its balance sheet and tightens policy, while inflation

pressures build on exceptional strength in the US labor market.

The Bank of Japan ("BOJ") and European Central Bank ("ECB") continued with their quantitative easing

("QE") programs during the quarter as short-term yields in Japan and the eurozone remained negative. We

expect the euro and Japanese yen to weaken on widening rate differentials with the US. Rising US Treasury

yields should produce a more effective environment for the BOJ to actively deploy additional monetary

accommodation that weakens the yen. In Europe, we expect the ECB to continue with monetary

accommodation through 2017, as it has indicated. ECB President Mario Draghi has indicated the ECB will

announce a new schedule for additional QE tapering in October. Nonetheless, Draghi continued to indicate

that overall monetary accommodation is still needed for the near term, with eventual policy normalizing still

several quarters away.

5

Page 8

MAYBANK GLOBAL BOND FUND

Manager’s report for the 6 months financial period ended 31 December 2017 (cont'd)

C. Market Review (cont'd)

In Europe, yields generally declined but the euro strengthened against the US dollar. We expect widening

rate differentials between rising yields in the US and the low to negative yields in the eurozone to depreciate

the euro against the US dollar. Although the ECB is scheduled to reduce the pace of its bond-buying

programme in January 2018 to €30 billion per month, down from the current pace of €60 billion per month,

the overall monetary effect is still highly accommodative. ECB President Mario Draghi has continued to

indicate that rates are not likely to be hiked until QE ends, implying that rates would likely remain unchanged

in 2018.

In Japan, Prime Minister Shinzo Abe’s political mandate remains strong after his political coalition

maintained its supermajority in October elections. We expect Abenomics programmes to continue as

planned with Abe’s ongoing political strength. Japan’s economy continues to need weakness in the yen. The

BOJ continued with its QE programme as short-term yields in Japan remained negative. Rising UST yields

should produce a more effective environment for the BOJ to actively deploy additional monetary

accommodation that weakens the yen, as it continues to target a 0.0% yield on the 10-year Japanese

government bond. Overall, we expect the yen to weaken on widening rate differentials with the US.

The BOJ and ECB continued with their QE programs during the quarter as short-term yields in Japan and

the eurozone remained negative. We expect the euro and Japanese yen to weaken on widening rate

differentials with the US. Rising US Treasury yields should produce a more effective environment for the

BOJ to actively deploy additional monetary accommodation that weakens the yen. In Europe, we expect the

ECB to continue with monetary accommodation through 2017, as it has indicated. ECB President Mario

Draghi has indicated the ECB will announce a new schedule for additional QE tapering in October.

Nonetheless, Draghi continued to indicate that overall monetary accommodation is still needed for the near

term, with eventual policy normalizing still several quarters away.

Across emerging markets, rate environments were generally idiosyncratic, as Indonesia and Brazil saw

declining yields in the 10-year range of their yield curves, while India, Colombia and Mexico saw a modest

rise. Overall, we continue to see a number of local-currency markets that we believe are undervalued,

particularly in places like India, Indonesia, Mexico and Colombia. We also see attractive risk-adjusted yields

in places like Brazil and Argentina. On the whole, we continue to expect select currencies to appreciate over

the medium term, particularly in countries with economic resilience and relatively higher, maintainable rate

differentials.

The Fed kept rates unchanged at its November meeting, but market expectations for a rate hike in

December notably strengthened. Jerome Powell was nominated by US President Donald Trump to be the

next Fed chair, scheduled to replace Janet Yellen in February 2018. Markets have appeared to view Powell

as a mainstream continuation of the Yellen/Bernanke Fed, though Powell brings more private sector

experience and more support for deregulation. Market expectations for additional rate hikes in 2018

strengthened after the Powell nomination, with federal funds futures indicating expectations for another rate

hike in March 2018.

The Fed continued with its balance sheet unwinding, targeting around US$6 billion in USTs and US$4 billion

in mortgage-backed securities (“MBS”) to roll off each month as they mature. Markets appear to be

underappreciating the potential impacts of Fed unwinding, which we expect to put upward pressure on

yields. Overall, we expect UST yields to continue rising as the Fed unwinds its balance sheet and tightens

policy, while inflation pressures build on exceptional strength in the US labour market.

6

Page 9

MAYBANK GLOBAL BOND FUND

Manager’s report for the 6 months financial period ended 31 December 2017 (cont'd)

C. Market Review (cont'd)

(Source: Franklin Templeton Investments)

D. Market Outlook

The impact of Fed policy tightening on emerging markets should vary from country to country in the

upcoming year. It’s important to identify countries with idiosyncratic value that may be less correlated to

broad-based beta (market) risks. Countries that are more domestically driven and less reliant on global trade

often have those idiosyncratic qualities along with inherent resiliencies to global shocks. A select few have

already demonstrated that resilience in recent years, notably Indonesia. For others, economic risks are

related to the reforms underway within their country, rather than what happens externally, such as in Brazil

or Argentina. Higher rate differentials are also crucial in a rising-rate environment. By contrast, emerging

markets with macro imbalances or low rate environments should be impacted harder by rising rates.

Another group of potentially vulnerable countries are those with lower rates, such as South Korea or

Singapore, which despite strong macro fundamentals could also be vulnerable to currency depreciation as

the yield differential with the US flips. Thus we think the key to emerging-market allocations in 2018 will be to

avoid the broad beta risks and find those idiosyncratic sources of alpha that can withstand rising rates. In

the major developed economies, we continue to see unattractive bond markets, particularly the low to

negative yields in the eurozone and Japan

Across emerging markets, yields rose in specific areas of Latin America and Asia, with some exceptions.

Emerging-market currencies broadly appreciated against a weakened US dollar in November, with notable

appreciations in the Mexican peso and Argentine peso. A number of countries continued to see positive

yield carry, benefitting from elevated yields. We continue to have positive medium-term outlooks for both

Argentina and Brazil as their governments trend away from prior failed policies and move towards important

structural reforms. Risk-adjusted yields in Brazil and Argentina remain attractive, in our view. Additionally,

we continue to see a number of local-currency markets that we believe are undervalued, particularly in India,

Indonesia, Mexico and Colombia.

For nearly a decade, financial markets have surfed a wave of low-cost money in the US, courtesy of the US

Federal Reserve’s massive QE programs that were launched after the global financial crisis (“GFC”) of

2007–2009. The expansion of the Fed’s balance sheet from around US$900 billion in 2008 to nearly US$4.5

trillion today has arguably been the most dominant force shaping global financial markets. QE has driven

down yields and pushed up asset prices, steering many investors toward riskier assets while keeping the

costs of capital artificially suppressed. This has distorted valuations in bonds and in equities. In short, the

era of QE has created a seemingly complacent market that views persistently low yields as a permanent

condition. However, these conditions are neither normal nor permanent, in our assessment, and we expect

the reversal of QE by the Fed to meaningfully impact financial markets in 2018 and beyond.

A number of factors are poised to pressure UST yields higher, including the aforementioned reversal of QE,

but also the exceptional strength in US labor markets, rising wage and inflation pressures, ongoing resiliency

in the US economy, and a structural shift toward deregulation by both the Trump administration and

potentially a Jerome Powell Fed. At the same time, major foreign buyers of USTs from prior years have

notably stopped acquiring USTs over the last few years. China has reduced its foreign reserves by around

US$1 trillion, while oil exporting nations like Saudi Arabia have similarly become net borrowers instead of

lenders, no longer buying massive levels of USTs. Now the Fed will also be departing that market, further

driving down the supply of UST buyers. Markets could see sharp corrections to UST yields in upcoming

quarters. The challenge for investors in 2018 will be that the traditional diversifying relationship between

bonds and risk assets may not hold true in this new cycle of UST declines. It’s quite possible to see risk

assets also decline as the “risk-free” rate ratchets higher.

7

Page 10

MAYBANK GLOBAL BOND FUND

Manager’s report for the 6 months financial period ended 31 December 2017 (cont'd)

D. Market Outlook (cont'd)

(Source: Franklin Templeton Investments)

E. Investment Strategy

As we look ahead in 2018, we expect the reversal of QE, rate hikes and rising inflation pressures in the US

to be among the most impactful factors for global financial markets in the upcoming year. When the first

rounds of QE were initially deployed by the Fed nearly a decade ago, many skeptics argued that pumping

money into the financial system would cause high inflation. But inflation never accelerated, in part because

banks and financial companies stockpiled cash while credit activity remained constrained by post-GFC

regulations, such as the Dodd-Frank Act. However, the factors that previously limited inflation and money

creation over the last decade are also now approaching their end. Deregulation efforts through executive

action are already underway, while credit activity has been accelerating. This potential acceleration in money

velocity combined with existing inflation pressures in the US economy and labor markets leads us to expect

higher inflation and higher UST yields in the upcoming year.

The core strategy for the Target Fund is to position the portfolio to navigate a rising-rate environment as the

Target Fund Manager believes that rate hikes from the Fed are needed given prevailing conditions and that

a return to appropriate monetary policy in the US can catalyst markets towards a broad fundamental

recovery. Consequently, it has continued to position defensively with regard to duration and actively seek

opportunities that can potentially offer positive real yields without taking undue interest-rate risk. Countries

that have solid underlying fundamentals and policymakers who have stayed ahead of the curve regarding

fiscal, monetary and financial policy remain the preferred sovereign investments.

8

Page 11

MAYBANK GLOBAL BOND FUND

Manager’s report for the 6 months financial period ended 31 December 2017 (cont'd)

F. Asset Allocation

RM % RM %

136,105 3.75 94,745 2.06

Total NAV 3,633,229 100.00 4,608,331 100.00

G. NAV as at 31 December 2017

31.12.2017 30.06.2017 Changes (%)

NAV (RM) 3,633,229 4,608,331 (21.16)

Units in circulation (units) 3,605,740 4,374,732 (17.58)

NAV per unit (RM) 1.0076 1.0534 (4.35)

H. Soft Commissions and Rebates

The comparison of the Fund’s asset allocation as at 31 December 2017 to the previous financial year is as

below:

Asset allocation31.12.2017 30.06.2017

During the financial period ended 31 December 2017, the Manager and its delegates (if any) did not receive

any soft commissions and rebates from brokers or dealers.

3,497,124 96.25 4,513,586 97.94

Cash, deposit with a licensed financial

institution and other net assets

During the 6-month period, the Fund’s allocation in the investment in Class A (Mdis) SGD - H1 shares of the

Target Fund has decreased from 97.94% to 96.12% in terms of RM value.

Overall, the NAV of the Fund has reduced by 21.05% from RM4.61 million to RM3.64 million. In tandem, the

units in circulation has also reduced by 17.58% to RM3.61 million as at 31 December 2017 from RM4.37

million as at 30 June 2017. NAV per unit decreased by 4.21% from RM1.0534 to RM1.0091.

The Manager and its delegates (if any) will not retain any form of soft commissions and rebates from or

otherwise share in any commission with any broker in consideration for directing dealings in the investments

of the Fund unless the commission received is retained in the form of goods and services such as financial

wire services and stock quotations system incidental to investment management of the Fund. All dealings

with brokers are executed on best available terms.

Class A (Mdis) SGD - H1

shares of the Target Fund

9

Page 12

TRUSTEE’S REPORT

TO THE UNITHOLDERS OF MAYBANK GLOBAL BOND FUND

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017

(a)

(b)

(c)

For and on behalf of

RHB TRUSTEES BERHAD

TONY CHIENG SIONG UNG

Director

Kuala Lumpur, Malaysia

28 February 2018

Valuation/pricing was carried out in accordance with the Deed and any regulatory

requirements; and

Creation and cancellation of units were carried out in accordance with the Deed and relevant

regulatory requirements;

MAYBANK GLOBAL BOND FUND

We have acted as Trustee of Maybank Global Bond Fund (the "Fund") for the six months

financial period ended 31 December 2017. In our opinion and to the best of our knowledge,

Maybank Asset Management Sdn Bhd, the Manager, has operated and managed the Fund in

accordance with the following:

Limitations imposed on the investment powers of the Manager and the Trustee under the

Deed, the Securities Commission’s Guidelines on Unit Trust Funds, the Capital Markets and

Services Act 2007 ("CMSA") and other applicable laws;

10

Page 13

STATEMENT BY MANAGER

For and on behalf of the Manager

Badrul Hisyam Abu Bakar

Kuala Lumpur, Malaysia

28 February 2018

I, Badrul Hisyam Abu Bakar, being a Director of Maybank Asset Management Sdn Bhd (the

"Manager") do hereby state that, in the opinion of the Manager, the accompanying financial

statements set out on pages 12 to 44 are drawn up in accordance with Malaysian Financial

Reporting Standards 134 Interim Financial Reporting and International Financial Reporting

Standards 34 Interim Financial Reporting so as to give a true and fair view of the financial

position of Maybank Global Bond Fund as at 31 December 2017 and of its results, changes in

equity and cash flows for the financial period then ended and comply with the requirements of the

Deed.

MAYBANK GLOBAL BOND FUND

11

Page 14

MAYBANK GLOBAL BOND FUND

UNAUDITED STATEMENT OF COMPREHENSIVE INCOME

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017

01.07.2017 01.07.2016

to to

31.12.2017 31.12.2016

Note RM RM

INVESTMENT INCOME

Interest income 2,654 2,826

Dividend income 133,591 155,454

Net loss from available-for-sale ("AFS")

financial assets (80,710) (200,497)

Net realised foreign exchange gain 132,650 238,404

Net unrealised foreign exchange loss (263,633) (36,324)

Rebate income 6,091 8,084

Redemption fee income 820 434

(68,537) 168,381

EXPENSES

Manager's fee 3 21,335 28,150

Trustee's fee 4 1,067 1,407

Auditor's remuneration 3,025 3,025

Tax agent's fee 1,765 1,765

Administrative expenses 3,520 2,991

30,712 37,338

Net (loss)/income before taxation (99,249) 131,043

Income tax credit/(expense) 5 7,384 (4,019)

Net (loss)/income after taxation (91,865) 127,024

Other comprehensive income

Items that may be reclassified to income statement

in subsequent years

Effects of changes in fair value (144,739) 172,108

Realised gain transferred to income statement

upon disposal 68,796 206,376

Net changes in fair value of AFS financial assets (75,943) 378,484

Total comprehensive (loss)/income for the financial period (167,808) 505,508

12

Page 15

MAYBANK GLOBAL BOND FUND

UNAUDITED STATEMENT OF COMPREHENSIVE INCOME

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

01.07.2017 01.07.2016

to to

31.12.2017 31.12.2016

Note RM RM

Net (loss)/income after taxation is made up

of the following:

Net realised (loss)/income 12(b) (355,498) 90,700

Net unrealised income 12(c) 263,633 36,324

(91,865) 127,024

Distribution for the financial period:

Net distribution 13 - 70,897

Gross distribution per unit (sen) 13 - 1.50

Net distribution per unit (sen) 13 - 1.50

The accompanying notes form an integral part of the unaudited financial statements.

13

Page 16

MAYBANK GLOBAL BOND FUND

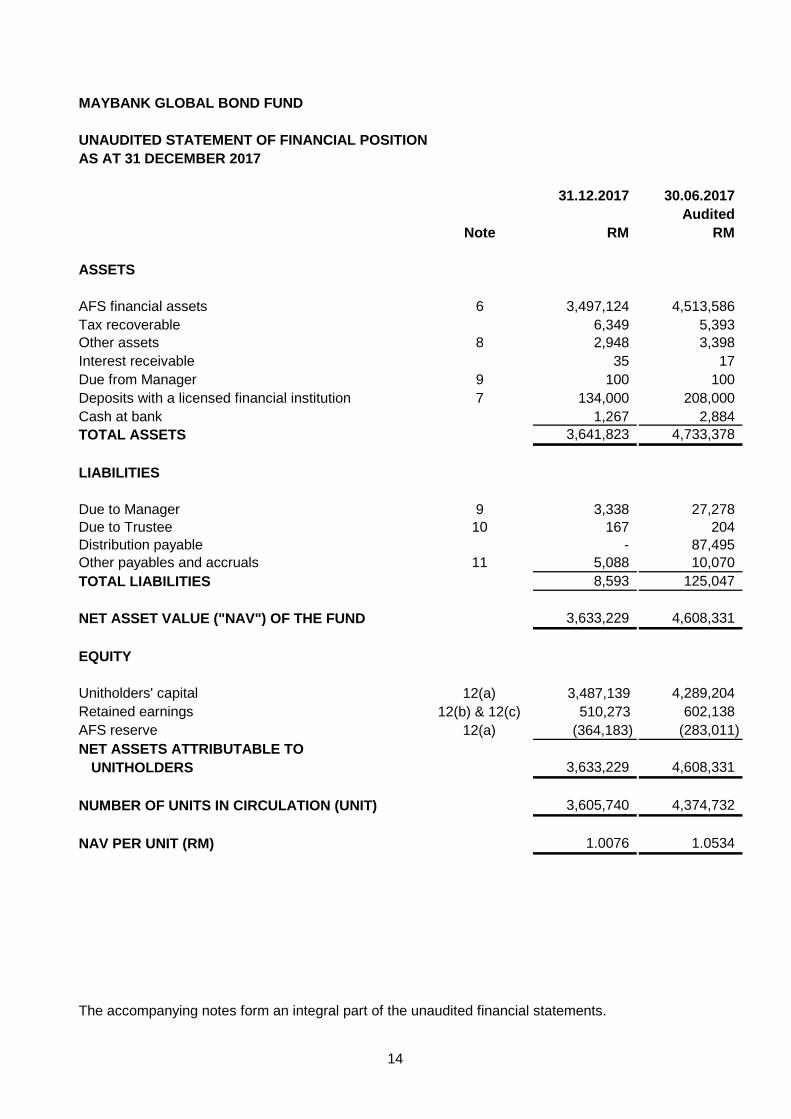

UNAUDITED STATEMENT OF FINANCIAL POSITION

AS AT 31 DECEMBER 2017

31.12.2017 30.06.2017

Audited

Note RM RM

ASSETS

AFS financial assets 6 3,497,124 4,513,586

Tax recoverable 6,349 5,393

Other assets 8 2,948 3,398

Interest receivable 35 17

Due from Manager 9 100 100

Deposits with a licensed financial institution 7 134,000 208,000

Cash at bank 1,267 2,884

TOTAL ASSETS 3,641,823 4,733,378

LIABILITIES

Due to Manager 9 3,338 27,278

Due to Trustee 10 167 204

Distribution payable - 87,495

Other payables and accruals 11 5,088 10,070

TOTAL LIABILITIES 8,593 125,047

NET ASSET VALUE ("NAV") OF THE FUND 3,633,229 4,608,331

EQUITY

Unitholders' capital 12(a) 3,487,139 4,289,204

Retained earnings 12(b) & 12(c) 510,273 602,138

AFS reserve 12(a) (364,183) (283,011)

NET ASSETS ATTRIBUTABLE TO

UNITHOLDERS 3,633,229 4,608,331

NUMBER OF UNITS IN CIRCULATION (UNIT) 3,605,740 4,374,732

NAV PER UNIT (RM) 1.0076 1.0534

The accompanying notes form an integral part of the unaudited financial statements.

14

Page 17

MAYBANK GLOBAL BOND FUND

UNAUDITED STATEMENT OF CHANGES IN EQUITY

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017

Retained

Unitholders' earnings Total

capital Note 12(b) AFS equity

Note 12(a) and 12(c) reserve

RM RM RM RM

At 1 July 2016 6,198,681 903,580 (685,523) 6,416,738

Total comprehensive income

for the financial period - 127,024 378,484 505,508

Creation of units 249,415 - - 249,415

Cancellation of units (2,085,128) - - (2,085,128)

Distributions (Note 13) 187,193 (258,090) - (70,897)

At 31 December 2016 4,550,161 772,514 (307,039) 5,015,636

At 1 July 2017 4,289,204 602,138 (283,011) 4,608,331

Total comprehensive loss

for the financial period - (91,865) (81,172) (173,037)

Creation of units 610,629 - - 610,629

Cancellation of units (1,412,694) - - (1,412,694)

At 31 December 2017 3,487,139 510,273 (364,183) 3,633,229

The accompanying notes form an integral part of the unaudited financial statements.

15

Page 18

MAYBANK GLOBAL BOND FUND

UNAUDITED STATEMENT OF CASH FLOWS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017

01.07.2017 01.07.2016

to to

31.12.2017 31.12.2016

RM RM

CASH FLOWS FROM OPERATING AND INVESTING

ACTIVITIES

Proceeds from sale of investments 1,069,011 1,855,121

Purchase of investments (340,090) (245,295)

Interest received 2,636 2,852

Dividends received 133,496 155,454

Other income received 819 9,608

Manager's and Trustee fee paid (24,516) (32,871)

Payment of other fees and expenses (4,206) (11,148)

Net cash generated from/(used in) operating and investing activities 837,151 1,733,721

CASH FLOWS FROM FINANCING ACTIVITIES

Cash received from units created 610,629 255,585

Cash paid on units cancelled (1,435,902) (2,108,071)

Distribution paid to unitholders (87,495) -

Net cash (used in)/generated from financing activities (912,768) (1,852,486)

NET INCREASE IN CASH AND CASH EQUIVALENTS

FOR THE FINANCIAL PERIOD (75,617) (118,765)

CASH AND CASH EQUIVALENTS AT THE BEGINNING

OF THE FINANCIAL PERIOD 210,884 363,046

CASH AND CASH EQUIVALENTS AT THE END

OF THE FINANCIAL PERIOD 135,267 244,281

Cash and cash equivalents comprise:

Cash at bank 1,267 244,281

Deposit with a licensed financial institution with original

maturity of less than 3 months (Note 7) 134,000 -

135,267 244,281

The accompanying notes form an integral part of the unaudited financial statements.

16

Page 19

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017

1. THE FUND, THE MANAGER AND THEIR PRINCIPAL ACTIVITIES

2.1 Basis of preparation

Maybank Global Bond Fund (“the Fund”) was constituted pursuant to the execution of a Principal

Deed dated 19 October 2012 between the Manager, Maybank Asset Management Sdn. Bhd.

("Maybank AM") and the first supplementary Deed dated 2 September 2013, second supplementary

Deed dated 20 March 2015, the Trustee, RHB Trustees Berhad and the registered holders of the

Fund.

At least 95% of the Funds NAV should be invested in the shares of the Target Fund and at least

2% to 5% of the Fund's NAV should be invested in liquid assets.

The Fund has adopted the Standards, Amendments to Standards and Interpretation Committee

Interpretations which have become effective during the financial period ended 31 December 2017.

The adoption did not result in material impact to the financial statements.

The Manager of the Fund is Maybank AM, a company incorporated in Malaysia. It is a holder of the

Capital Markets Services Licence with fund management as its regulated activity under the Capital

Markets and Services Act 2007 ("CMSA"). The principal place of business of Maybank AM is at

Level 12, Tower C Dataran Maybank, No. 1 Jalan Maarof, 59000 Kuala Lumpur, Malaysia.

Maybank AM is a wholly-owned subsidiary of Maybank Asset Management Group Berhad

("MAMG"), which in turn is a wholly-owned subsidiary of Malayan Banking Berhad ("MBB").

The financial statements of the Fund have been prepared in accordance with Malaysian Financial

Reporting Standards (“MFRS”) as issued by the Malaysian Accounting Standards Board (“MASB”)

and International Financial Reporting Standards (“IFRS”) as issued by the International Accounting

Standards Board (“IASB”).

All investments are subject to the Securities Commission Malaysia ("SC") Guidelines on Unlisted

Capital Market Products under the Lodge and Launch Framework, SC requirements and the Deed,

except where exemptions or variations have been approved by the SC, internal policies and

procedures and the Fund's objective.

The Fund aims to maximise investment return by investing in the Class A (mdis) SGD - H1 shares

of the Templeton Global Bond Fund ("Target Fund"), a sub-fund of the Franklin Templeton

Investment Funds managed by Franklin Advisers, Inc. The functional currency of the Target Fund is

in US Dollar ("USD"), whereas the Shares of the Target Fund in which the Fund invests in are

denominated in Singapore Dollar ("SGD"). The Target Fund is an open-ended collective investment

scheme domiciled in the Grand Duchy of Luxembourg and was launched on 28 February 1991. The

Target Fund is regulated by the Commission de Surveillance du Secteur Financier under Part I of

the Luxembourg law of December 20, 2002 relating to undertakings for collective investment.

17

Page 20

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

2.1 Basis of preparation (cont'd)

2.2 Standards, amendments to standards and interpretations issued but not yet effective

Effective for

for annual

periods

beginning

Description on or after

Annual Improvements to MFRSs 2014 - 2016 Cycle 1 January 2018

Transfers of Investment Property (Amendments to MFRS 140) 1 January 2018

IC Interpretation 22 Foreign Currency Transactions and Advance Consideration 1 January 2018

MFRS 2 Share-based Payment - Classification and Measurement of

Share-based Payment Transactions (Amendments to MFRS 2) 1 January 2018

MFRS 9 Financial Instruments 1 January 2018

MFRS 15 Revenue from Contracts with Customers 1 January 2018

MFRS 16 Leases 1 January 2019

IC Interpretation 23 Uncertainty over Income Tax Treatments 1 January 2019

Annual Improvements to MFRSs 2015 - 2017 Cycle 1 January 2019

MFRS 17 Insurance Contracts 1 January 2021

MFRS 10 Consolidated Financial Statements - Sale or Contribution

of Assets between an Investor and its Associate or Joint Venture To be announced

(Amendments to MFRS 10) by MASB

MFRS 10 Investment in Associates and Joint Ventures - Sale or Contribution

of Assets between an Investor and its Associate or Joint Venture To be announced

(Amendments to MFRS 128) by MASB

The financial statements have been prepared on a historical cost basis except as disclosed in the

accounting policies in Note 2.3 to Note 2.15.

The following are standards, amendments to standards and interpretations issued by the MASB,

but not yet effective, up to the date of issuance of the Fund's financial statements. The Fund

intends to adopt the relevant standards, if applicable, when they become effective.

The financial statements are presented in Ringgit Malaysia (“RM”).

18

Page 21

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D)

2.2 Standards and amendments to standards issued but not yet effective (cont'd)

(i) MFRS 9 Financial Instruments

- those to be measured subsequently at fair value (through profit or loss), and

- those to be measured at amortised cost

There will be no changes to the subsequent measurement of these financial assets.

2.3 Financial assets

The investment currently held as available-for-sale with gains and losses recorded in OCI will

be measured at fair value through profit or loss instead, which will increase volatility in

recorded profit or loss. The AFS reserve currently presented as accumulated OCI will be

reclassified to opening retained earnings.

The Fund expects that the adoption of the above standards will not have any material impact on the

financial statements in the year of initial application except as discussed below:

Financial assets are recognised in the statement of financial position when, and only when, the

Fund becomes a party to the contractual provisions of the financial instrument.

When financial assets are recognised initially, they are measured at fair value, plus directly

attributable transaction costs.

The classification depends on the purpose for which the investments were acquired. The Fund

determines the classification of its financial assets at initial recognition, and the categories

applicable to the Fund are AFS financial assets and loans and receivable.

MFRS 9 replaces MFRS 139 Financial Instruments: Recognition and Measurement ("MFRS

139"). MFRS 9 requires financial assets to be classified on the basis of the business model

within which they are held and their contractual cash flow characteristic.

The Fund will classify its financial assets in the following measurement categories:

The Manager intends to adopt MFRS 9 on the mandatory effective date.

MFRS 9 requires impairment assessments to be based on an expected loss model ("ECL"),

replacing the MFRS 139 incurred loss model. The ECL model applies to financial assets

measured at amortised cost.

19

Page 22

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D)

2.3 Financial assets (cont'd)

(a) AFS financial assets

Classification

Recognition and measurement

(b) Loans and receivables

Classification

Recognition and measurement

Non-derivative financial assets with fixed or determinable payments that are not quoted in an

active market are classified as loans and receivables. The Fund's loans and receivables

comprise cash at bank, deposit with a licensed financial institution and other assets, interest

receivable, and amount due from Manager.

Subsequent to initial recognition, loans and receivables are measured at amortised cost using

the effective interest method. Gains and losses are recognised in the statement of profit and

loss when the loans and receivables are derecognised or impaired, and through the

amortisation process.

AFS financial assets are those intended to be held for an indefinite period of time, which may

be sold in response to needs for liquidity or investment prices, or that are not classified as

financial assets at fair value through profit or loss. The Fund designates its investments in

collective investment scheme in this category at inception.

Regular purchases and sales of financial assets are recognised on the trade date, the date on

which the Fund commits to purchase or sell the asset. Investments are initially recognised at

fair value, plus directly attributable transaction costs.

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an

orderly transaction between market participants at the measurement date. The fair value for

financial instruments traded in active markets at the reporting date is based on their quoted

price or binding dealer price quotations, without any deduction for transaction costs.

Gains and losses arising from changes in fair value of AFS financial assets are recognised

directly in other comprehensive income until the securities are derecognised or impaired at

which time the cumulative gains or losses previously recognised in equity are recognised

directly in the statement of income. Foreign exchange gains or losses of AFS financial assets

are recognised in the statement of income in the period it arises.

20

Page 23

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D)

2.4 Derecognition on financial assets

A financial asset is derecognised when:

(1) The rights to receive cash flows from the asset have expired; or

(2)

- the Fund has transferred substantially all the risks and rewards of the asset; or

-

2.5 Impairment of financial assets

Loans and receivables

On derecognition of a financial asset in its entirety, the difference between the carrying amount and

the sum of the consideration received and any cumulative gain or loss that had been recognised in

other comprehensive income is recognised in profit or loss.

The Fund has transferred its rights to receive cash flows from the financial asset or have

assumed an obligation to pay the received cash flows in full without material delay to a third

party under a "pass through" arrangement; and either:

To determine whether there is objective evidence that an impairment loss on financial assets has

been incurred, the Fund considers factors such as the probability of insolvency or significant

financial difficulties of the debtor and default or significant delay in payments.

If any such evidence exists, the amount of impairment loss is measured as the difference between

the asset’s carrying amount and the present value of estimated future cash flows discounted at the

financial asset’s original effective interest rate. The impairment loss is recognised in statement of

comprehensive income.

The carrying amount of the financial asset is reduced by the impairment loss directly for all financial

assets.

If in a subsequent period, the amount of the impairment loss decreases and the decrease can be

related objectively to an event occurring after the impairment was recognised, the previously

recognised impairment loss is reversed to the extent that the carrying amount of the asset does not

exceed its amortised cost at the reversal date. The amount of reversal is recognised in statement of

comprehensive income.

The Manager assesses at each reporting date whether there is any objective evidence that a

financial asset of the Fund is impaired.

the Fund has neither transferred nor retained substantially all the risks and rewards of

the asset, but has transferred control of the financial asset.

21

Page 24

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D)

2.5 Impairment of financial assets (cont'd)

AFS financial assets

2.6 Financial liabilities

Classification

Recognition and measurement

2.7 Fair value measurement

(i)

(ii)

The principal or the most advantageous market must be accessible by the Fund.

For debt securities, the Fund use criteria and measurement of impairment loss applicable for

“assets carried at amortised cost” above. If in a subsequent period, the fair value of a debt

instrument classified as AFS financial assets increases and the increase can be objectively related

to an event occurring after the impairment loss was recognised in statement of income, the

impairment loss is reversed through statement of income.

Financial liabilities are classified according to the substance of the contractual arrangements

entered into and the definitions of a financial liability. The Fund classifies amount due to Manager,

amount due to Trustee, distribution payable, and other payables and accruals as financial liabilities.

Financial liabilities, within the scope of MFRS 139, are recognised in the statement of financial

position when, and only when, the Fund becomes a party to the contractual provisions of the

financial instrument.

The Fund’s financial liabilities are recognised initially at fair value plus directly attributable

transaction costs and subsequently measured at amortised cost using the effective interest rate

method.

A financial liability is derecognised when the obligation under the liability is extinguished. Gains and

losses are recognised in statement of comprehensive income when the liabilities are derecognised,

and through the amortisation process.

In the absence of a principal market, in the most advantageous market for the asset or liability.

The Manager measures the Fund's financial instruments at fair value, at each reporting date of the

Fund. Fair value is the price that would be received to sell an asset or paid to transfer a liability in

an orderly transaction between market participants at the measurement date. The fair value

measurement is based on the presumption that the transaction to sell the asset or transfer the

liability takes place either:

In the principal market for the asset or liability; or

22

Page 25

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

2.

2.7 Fair value measurement (cont'd)

(i) Level 1 -

(ii) Level 2 -

(iii) Level 3 -

2.8 Functional and foreign currency

(a) Functional and presentation currency

All assets and liabilities for which fair value is measured or disclosed in the financial statements are

categorised within the fair value hierarchy, described as follows, based on the lowest level input

that is significant to the fair value measurement as a whole:

Valuation techniques for which the lowest level input that is significant to the fair

value measurement is unobservable.

Quoted (unadjusted) market prices in active markets for identical assets or

liabilities.

For assets and liabilities that are recognised in the financial statements on a recurring basis, the

Fund determines whether transfers have occurred between levels in the hierarchy by re-assessing

categorisation (based on the lowest level input that is significant to the fair value measurement as a

whole) at the end of each reporting date.

For the purpose of fair value disclosures, the Fund has determined classes of assets and liabilities

on the basis of the nature, characteristics and risks of the asset or liability and the level of the fair

value hierarchy as explained above.

Valuation techniques for which the lowest level input that is significant to the fair

value measurement is directly or indirectly observable.

The financial statements of the Fund are measured using the currency of the primary

economic environment in which the Fund operates (the "functional currency”). The financial

statements are presented in RM, which is also the Fund’s functional currency.

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D)

The fair value of an asset or a liability is measured using the assumptions that market participants

would use when pricing the asset or liability, assuming that market participants act in their

economic best interest.

A fair value measurement of a non-financial asset takes into account a market participant’s ability

to generate economic benefits by using the asset in its highest and best use or by selling it to

another market participant that would use the asset in its highest and best use.

23

Page 26

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

2.

2.8 Functional and foreign currency (cont'd)

(b) Transactions and balances

2.9 Unitholders' capital

(i)

(ii)

(iii)

(iv)

2.10 Distributions

The Fund's NAV per unit is calculated by dividing the net assets attributable to unitholders with the

total number of outstanding units.

Foreign currency transactions are translated into the functional currency using the exchange

rates prevailing at the dates of transactions or valuations where items are remeasured.

Foreign exchange gains and losses resulting from the settlement of such transactions and

from the translation at financial period-end exchange rates of monetary assets and liabilities

denominated in foreign currencies are recognised in the statement of comprehensive income,

except when deferred in other comprehensive income as qualifying cash flow hedges.

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D)

The unitholders’ contributions to the Fund meet the criteria to be presented as equity instruments

under MFRS 132 “Financial Instruments: Presentation”. Those criteria include:

the units entitle the holder to a proportionate share of the Fund’s NAV;

the units are the most subordinated class and class features are identical;

there is no contractual obligations to deliver cash or another financial asset other than the

obligation on the Fund to repurchase; and

the total expected cash flows from the units over its life are based substantially on the

statement of comprehensive income of the Fund.

The outstanding units are carried at the redemption amount that is payable at each financial period

if unit holder exercises the right to put the unit back to the Fund. Units are created and cancelled at

prices based on the Fund's NAV per unit at the time of creation or cancellation.

Distribution equalisation represents the average distributable amount included in the creation and

cancellation prices of units. This amount is either refunded to unitholders by way of distribution

and/or adjusted accordingly when units are cancelled.

Any distribution to the Fund’s unitholders is accounted for as a deduction from realised reserves

except where distribution is sourced out of distribution equalisation which is accounted for as a

deduction from unitholders’ capital. A proposed distribution is recognised as a liability in the period

in which it is approved.

24

Page 27

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

2.

2.11 Cash and cash equivalents

2.12 Income

2.13 Income tax

No deferred tax is recognised as no temporary differences have been identified.

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D)

Current tax assets and liabilities are measured at the amount expected to be recovered from or

paid to the tax authorities. The tax rates and tax laws used to compute the amount are those that

are enacted or substantively enacted by the reporting date.

Current taxes are recognised in profit or loss, except to the extent that the tax relates to items

recognised outside profit or loss, either in other comprehensive income or directly in equity.

Current tax expense is determined according to Malaysian tax laws at the current tax rate based

upon the taxable profit earned during the financial year.

Income is recognised to the extent that it is probable that the economic benefits will flow to the

Fund and the income can be reliably measured. Income is measured at the fair value of

consideration received or receivable.

Cash and cash equivalents comprise cash at bank and deposit with a licensed financial institution

with original maturity of three months or less which have an insignificant risk of changes in value.

Interest income from short-term deposits is recognised on the accruals basis using the effective

interest rate method.

Dividends are recognised as revenue when the right to receive payment is established.

Realised gain or loss on disposal of investment in collective investment scheme is accounted for as

the difference between the net disposal proceeds and the carrying amount of the investments.

Redemption fee income is charged to unitholders on cancellation of units before the maturity date

and is recognised upon cancellation of units.

25

Page 28

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

2.

2.14 Segment reporting

2.15 Critical accounting estimates and judgments

3. MANAGER'S FEE

4. TRUSTEE'S FEE

Manager's fee is computed daily based on 1.00% (30.06.2017: 1.00%) per annum ("p.a.") of the

NAV of the Fund before deducting the Manager's fee and Trustee's fees for that particular day.

The Fund makes estimates and assumptions concerning the future. The resulting accounting

estimates will, by definition, rarely equal the related actual results. To enhance the information

content of the estimates, certain key variables that are anticipated to have material impact to the

Fund’s results and financial position are tested for sensitivity to changes in the underlying

parameters.

Estimates and judgments are continually evaluated by the Manager and are based on historical

experience and other factors, including expectations of future events that are believed to be

reasonable under the circumstances.

The Manager has requested for and received the approval from the Trustee for the waiver of the

minimum fee for the current and previous financial period.

Trustee's fee is computed daily based on 0.05% (30.06.2017: 0.05%) p.a. of the NAV of the Fund

before deducting the Manager's fee and Trustee's fee for that particular day, subject to a minimum

fee of RM12,000 (30.06.2017: RM12,000) per annum.

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D)

Operating segments are reported in a manner consistent with the internal reporting used by the

chief operating decision-maker. The chief operating decision-maker is responsible for the allocating

resources and assessing performance of the operating segments.

26

Page 29

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

5. INCOME TAX EXPENSE

01.07.2017 01.07.2016

to to

31.12.2017 31.12.2016

RM RM

Net (loss)/income before taxation (99,249) 131,043

Tax at Malaysian statutory rate of 24% (30.06.2017: 24%) (23,820) 31,450

Effects of income not subject to tax (64,535) (95,204)

Effect of expenses not deductible for tax purposes 95,739 59,735

Income tax expense/(credit) for the year 7,384 (4,019)

The tax charge for the financial period is in relation to the taxable income earned by the Fund after

deducting the permitted expenses. A reconciliation of income tax (credit)/expense applicable to net

(loss)/income before taxation at the statutory income tax rate to income tax (credit)/expense at the

effective income tax rate is as follows:

27

Page 30

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

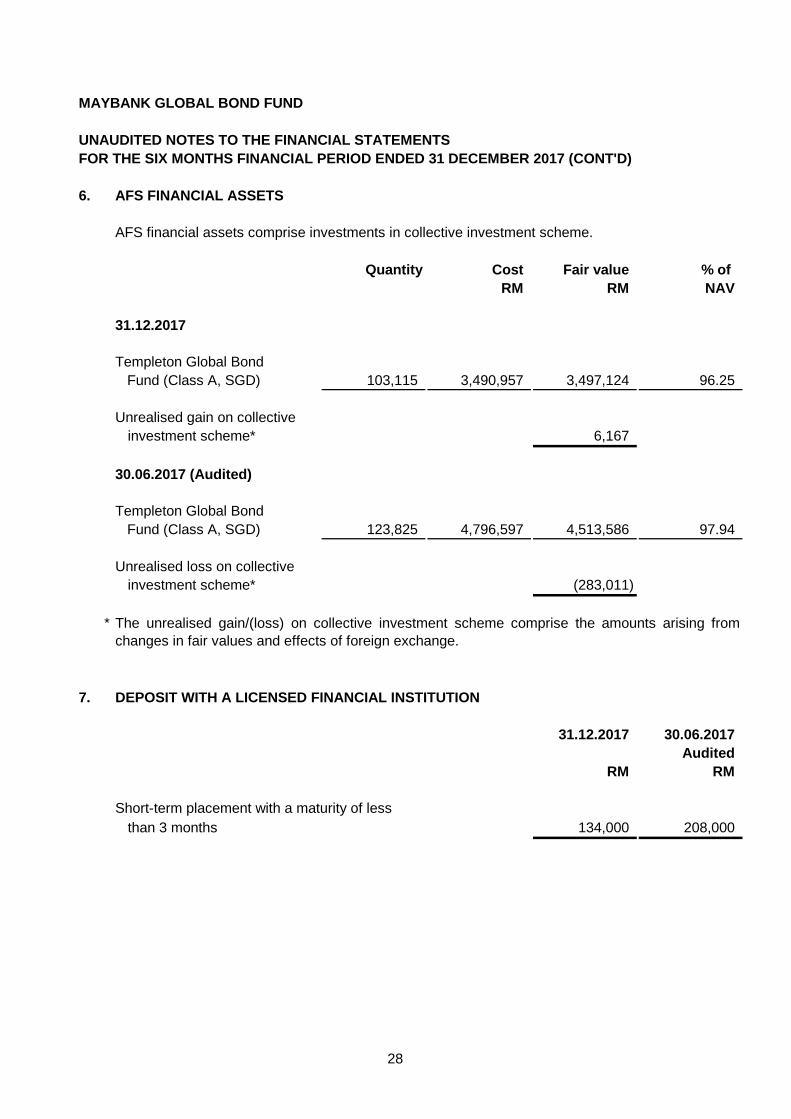

6. AFS FINANCIAL ASSETS

Quantity Cost Fair value % of

RM RM NAV

31.12.2017

Templeton Global Bond

Fund (Class A, SGD) 103,115 3,490,957 3,497,124 96.25

Unrealised gain on collective

investment scheme* 6,167

30.06.2017 (Audited)

Templeton Global Bond

Fund (Class A, SGD) 123,825 4,796,597 4,513,586 97.94

Unrealised loss on collective

investment scheme* (283,011)

*

7. DEPOSIT WITH A LICENSED FINANCIAL INSTITUTION

31.12.2017 30.06.2017

Audited

RM RM

Short-term placement with a maturity of less

than 3 months 134,000 208,000

The unrealised gain/(loss) on collective investment scheme comprise the amounts arising from

changes in fair values and effects of foreign exchange.

AFS financial assets comprise investments in collective investment scheme.

28

Page 31

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

7. DEPOSIT WITH A LICENSED FINANCIAL INSTITUTION (CONT'D)

Average Average

WAEIR Maturity WAEIR Maturity

% p.a. Days % p.a. Days

Deposit with a licensed

financial institution 3.18 2 3.05 3

8. OTHER ASSETS

31.12.2017 30.06.2017

Audited

RM RM

Rebate income receivable 2,948 3,398

9. DUE FROM/TO MANAGER

31.12.2017 30.06.2017

Audited

Note RM RM

Due from Manager

Subscription of units (a) 100 100

Due to Manager

Manager's fee (b) 3,338 4,070

Redemption of units (c) - 23,208

3,338 27,278

(a) The amount represents amount receivable from the Manager for units created.

(b)

(c) The amount represents amount payable to the Manager for units redeemed/cancelled.

31.12.2017

The weighted average effective interest rates (“WAEIR”) per annum and average maturity of

deposit with a licensed financial institution as at the reporting date were as follows:

30.06.2017

Audited

The amount relates to the amount payable to the Manager arising from the accruals for

Manager's fee at the end of the financial year. The normal credit term for Manager's fee is 15

days (30.06.2017: 15 days).

29

Page 32

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

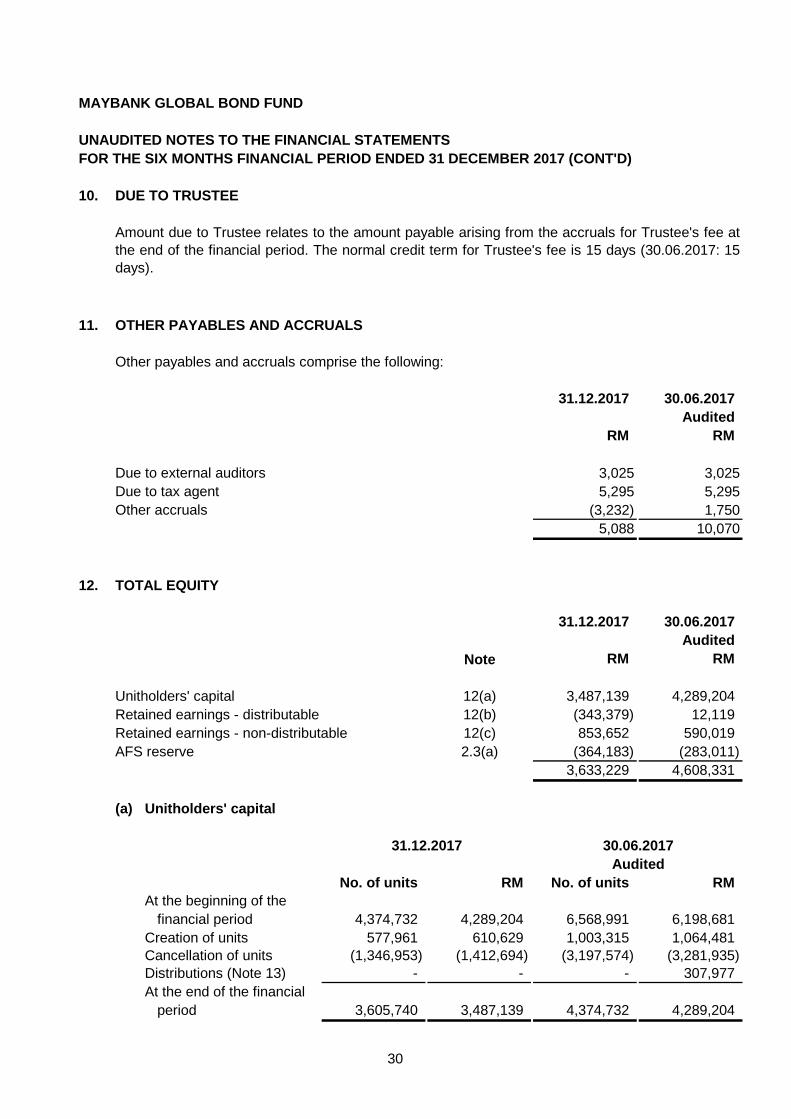

10. DUE TO TRUSTEE

11. OTHER PAYABLES AND ACCRUALS

Other payables and accruals comprise the following:

31.12.2017 30.06.2017

Audited

RM RM

Due to external auditors 3,025 3,025

Due to tax agent 5,295 5,295

Other accruals (3,232) 1,750

5,088 10,070

12. TOTAL EQUITY

31.12.2017 30.06.2017

Audited

Note RM RM

Unitholders' capital 12(a) 3,487,139 4,289,204

Retained earnings - distributable 12(b) (343,379) 12,119

Retained earnings - non-distributable 12(c) 853,652 590,019

AFS reserve 2.3(a) (364,183) (283,011)

3,633,229 4,608,331

(a) Unitholders' capital

No. of units RM No. of units RM

At the beginning of the

financial period 4,374,732 4,289,204 6,568,991 6,198,681

Creation of units 577,961 610,629 1,003,315 1,064,481

Cancellation of units (1,346,953) (1,412,694) (3,197,574) (3,281,935)

Distributions (Note 13) - - - 307,977

At the end of the financial

period 3,605,740 3,487,139 4,374,732 4,289,204

Amount due to Trustee relates to the amount payable arising from the accruals for Trustee's fee at

the end of the financial period. The normal credit term for Trustee's fee is 15 days (30.06.2017: 15

days).

31.12.2017

Audited

30.06.2017

30

Page 33

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

12. TOTAL EQUITY (CONT'D)

(a) Unitholders' capital (cont'd)

No. of units RM No. of units RM

The Manager 1,129 1,138 1,108 1,167

(b) Retained earnings - distributable

31.12.2017 30.06.2017

Audited

RM RM

At the beginning of the financial period 12,119 190,352

Net realised (expense)/income for the financial period (355,498) 342,403

Distributions out of retained earnings (Note 13)* - (520,636)

At the end of the financial period (343,379) 12,119

*

(c) Retained earnings - non-distributable

31.12.2017 30.06.2017

Audited

RM RM

At the beginning of the financial period 590,019 713,228

Net unrealised gain/(loss) for the financial period 263,633 (123,209)

At the end of the financial period 853,652 590,019

30.06.2017

Part of the distributions in the current financial period were made from previous financial

period's net realised income.

31.12.2017

As at the end of the financial period, the total number and value of units held legally or

beneficially by the Manager are as follows:

In the opinion of the Manager, the above units were transacted at the prevailing market price.

Other than the above, there were no other units held by the Manager or parties related to the

Manager.

Audited-

31

Page 34

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

13. DISTRIBUTIONS

Details of distributions declared to unitholders in the last financial year are as follows:

30.06.2017

Audited

RM

Investment income 361,092

Less: Expenses (103,002)

Distributions out of retained earnings 258,090

Effects of distribution equalisation (Note 12(a)) (187,193)

Distributions for the financial period 70,897

The gross and net distribution declared in the previous financial period is as follows:

Gross/net

distribution

per unit

Distribution date (Sen)

31 December 2016 1.50

The Fund did not declare a distribution for the six months financial period ended 31 December 2017.

14.

Details of transactions, primarily deposit with a licensed financial institution are as follows:

Percentage Percentage

Value of of total Value of of total

placements placements placements placements

RM % RM %

Financial institution

MBB 21,614,000 100.00 43,822,000 100.00

TRANSACTIONS WITH LICENSED FINANCIAL INSTITUTIONS

31.12.2017

Audited

30.06.2017

32

Page 35

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

15.

(a) Significant related party transactions

01.07.2017 01.07.2016

to to

31.12.2017 31.12.2016

RM RM

Maybank Asset Management Sdn Bhd:

Interest on deposit 2,671 5,192

Distribution to the Manager - 22

(b) Significant related party balances

31.12.2017 30.06.2017

Audited

Malayan Banking Berhad: RM RM

Deposits with a licensed financial institution 134,000 208,000

16. MANAGEMENT EXPENSE RATIO ("MER")

The MER of the Fund is the ratio of the sum of total expenses incurred by the Fund to the daily

average NAV of the Fund. For the financial period ended 31 December 2017, the MER of the Fund

stood at 0.55% (30.06.2017: 1.43%).

The Manager is of the opinion that the transactions with the related parties have been entered into

in the normal course of business and have been established on terms and conditions that are not

materially different from that obtainable in transactions with unrelated parties.

In addition to the related party information disclosed elsewhere in the financial statements, there

are no other related party transactions and balances of the Fund.

SIGNIFICANT RELATED PARTY TRANSACTIONS AND BALANCES

In addition to the related party information disclosed elsewhere in the financial statements, the

following is the significant related party transaction and balances of the Fund during the year.

For the purpose of the financial statements, parties are considered to be related to the Fund or the

Manager if the Fund or the Manager has the ability directly or indirectly, to control the party or

exercise significant influence over the party in making financial and operating decision, or vice

versa, or where the Fund or the Manager and the party are subject to common control or common

significant influence. Related parties may be individuals or other entities.

33

Page 36

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

17. PORTFOLIO TURNOVER RATIO ("PTR")

18. SEGMENT INFORMATION

There were no changes in the reportable operating segments during the financial period.

19. FINANCIAL INSTRUMENTS

(a) Classification of financial instruments

The PMC of the Manager is responsible for the Fund's performance by investing at least 95% of the

Fund's NAV in the shares of the Target Fund and the remaining 2% to 5% of the Fund's NAV in

liquid assets.

The internal reporting for the Fund’s assets, liabilities and performance is prepared on a consistent

basis with the measurement and recognition principles of MFRS and IFRS.

As the Fund is a feeder fund, the Target Fund Manager is the ultimate decision-maker on the

investment strategy to ensure the Target Fund achieves its targeted return with an acceptable level

of risk within the portfolio.

The Fund’s financial assets and financial liabilities are measured on an ongoing basis at either

fair value or at amortised cost based on their respective classification. The significant

accounting policies in Note 2.3 to Note 2.15 describe how the classes of financial instruments

are measured, and how income and expenses are recognised.

The Portfolio Management Committee (the "PMC") of the Manager, being the chief operating

decision-maker, makes the strategic decisions on the resources allocation of the Fund. The

decisions are based on an integrated investment strategy to ensure the Fund achieve its targeted

return with an acceptable level of risk within the portfolio.

The PTR of the Fund is the ratio of average acquisitions and disposals of the Fund for the financial

period to the daily average NAV of the Fund. For the financial period ended 31 December 2017, the

PTR of the Fund stood at 0.13 times (30.06.2017: 0.31 times).

34

Page 37

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

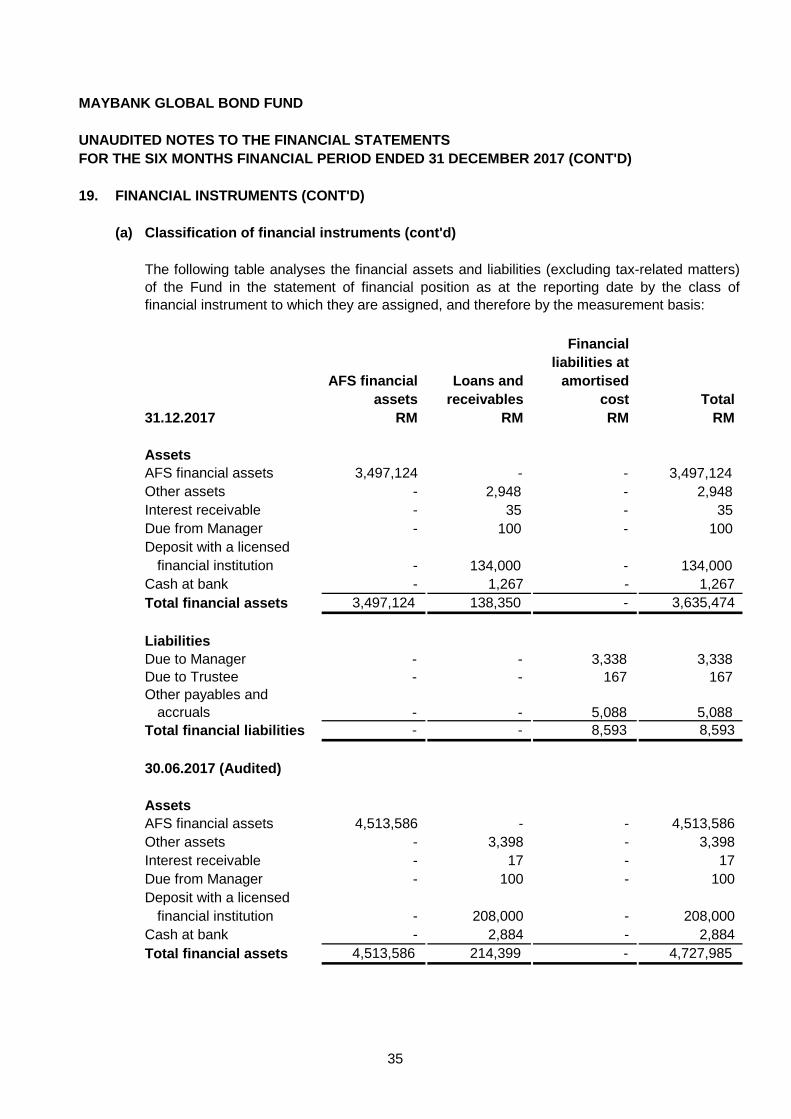

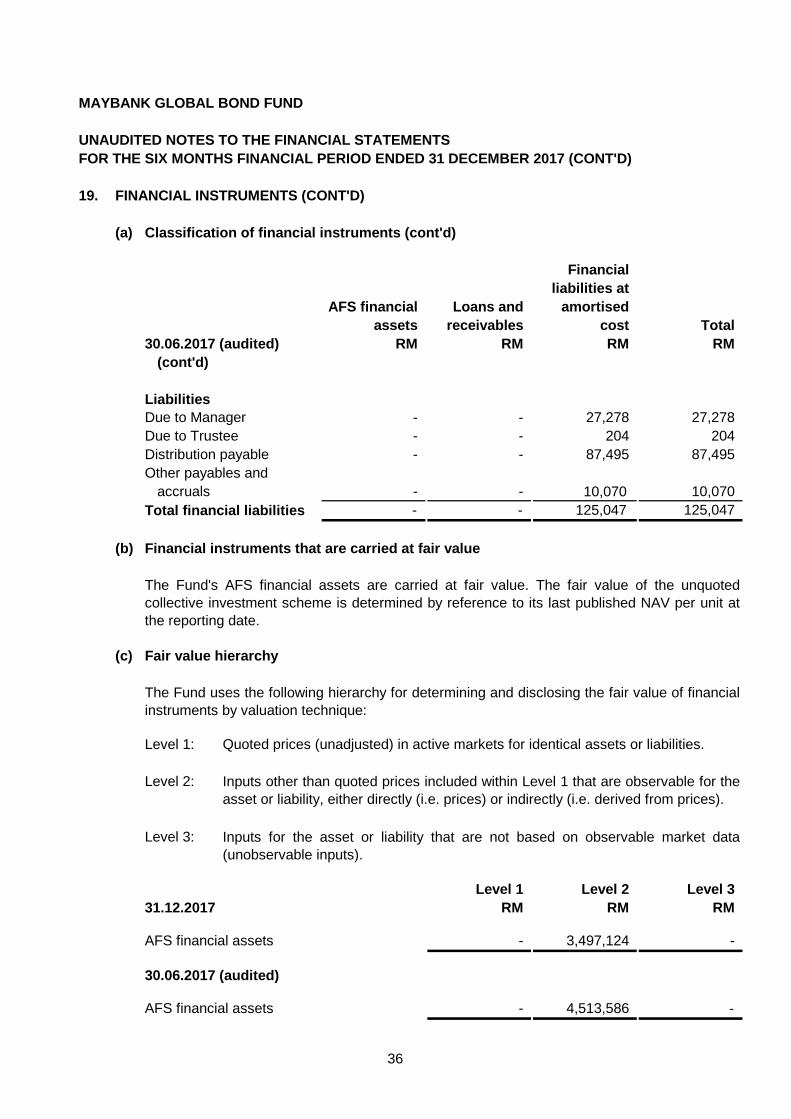

19. FINANCIAL INSTRUMENTS (CONT'D)

(a) Classification of financial instruments (cont'd)

Financial

liabilities at

AFS financial Loans and amortised

assets receivables cost Total

31.12.2017 RM RM RM RM

Assets

AFS financial assets 3,497,124 - - 3,497,124

Other assets - 2,948 - 2,948

Interest receivable - 35 - 35

Due from Manager - 100 - 100

Deposit with a licensed

financial institution - 134,000 - 134,000

Cash at bank - 1,267 - 1,267

Total financial assets 3,497,124 138,350 - 3,635,474

Liabilities

Due to Manager - - 3,338 3,338

Due to Trustee - - 167 167

Other payables and

accruals - - 5,088 5,088

Total financial liabilities - - 8,593 8,593

30.06.2017 (Audited)

Assets

AFS financial assets 4,513,586 - - 4,513,586

Other assets - 3,398 - 3,398

Interest receivable - 17 - 17

Due from Manager - 100 - 100

Deposit with a licensed

financial institution - 208,000 - 208,000

Cash at bank - 2,884 - 2,884

Total financial assets 4,513,586 214,399 - 4,727,985

The following table analyses the financial assets and liabilities (excluding tax-related matters)

of the Fund in the statement of financial position as at the reporting date by the class of

financial instrument to which they are assigned, and therefore by the measurement basis:

35

Page 38

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

19. FINANCIAL INSTRUMENTS (CONT'D)

(a) Classification of financial instruments (cont'd)

Financial

liabilities at

AFS financial Loans and amortised

assets receivables cost Total

30.06.2017 (audited) RM RM RM RM

(cont'd)

Liabilities

Due to Manager - - 27,278 27,278

Due to Trustee - - 204 204

Distribution payable - - 87,495 87,495

Other payables and

accruals - - 10,070 10,070

Total financial liabilities - - 125,047 125,047

(b) Financial instruments that are carried at fair value

(c) Fair value hierarchy

Level 1: Quoted prices (unadjusted) in active markets for identical assets or liabilities.

Level 2:

Level 3:

Level 1 Level 2 Level 3

31.12.2017 RM RM RM

AFS financial assets - 3,497,124 -

30.06.2017 (audited)

AFS financial assets - 4,513,586 -

The Fund uses the following hierarchy for determining and disclosing the fair value of financial

instruments by valuation technique:

Inputs other than quoted prices included within Level 1 that are observable for the

asset or liability, either directly (i.e. prices) or indirectly (i.e. derived from prices).

Inputs for the asset or liability that are not based on observable market data

(unobservable inputs).

The Fund's AFS financial assets are carried at fair value. The fair value of the unquoted

collective investment scheme is determined by reference to its last published NAV per unit at

the reporting date.

36

Page 39

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

19. FINANCIAL INSTRUMENTS (CONT'D)

(d)

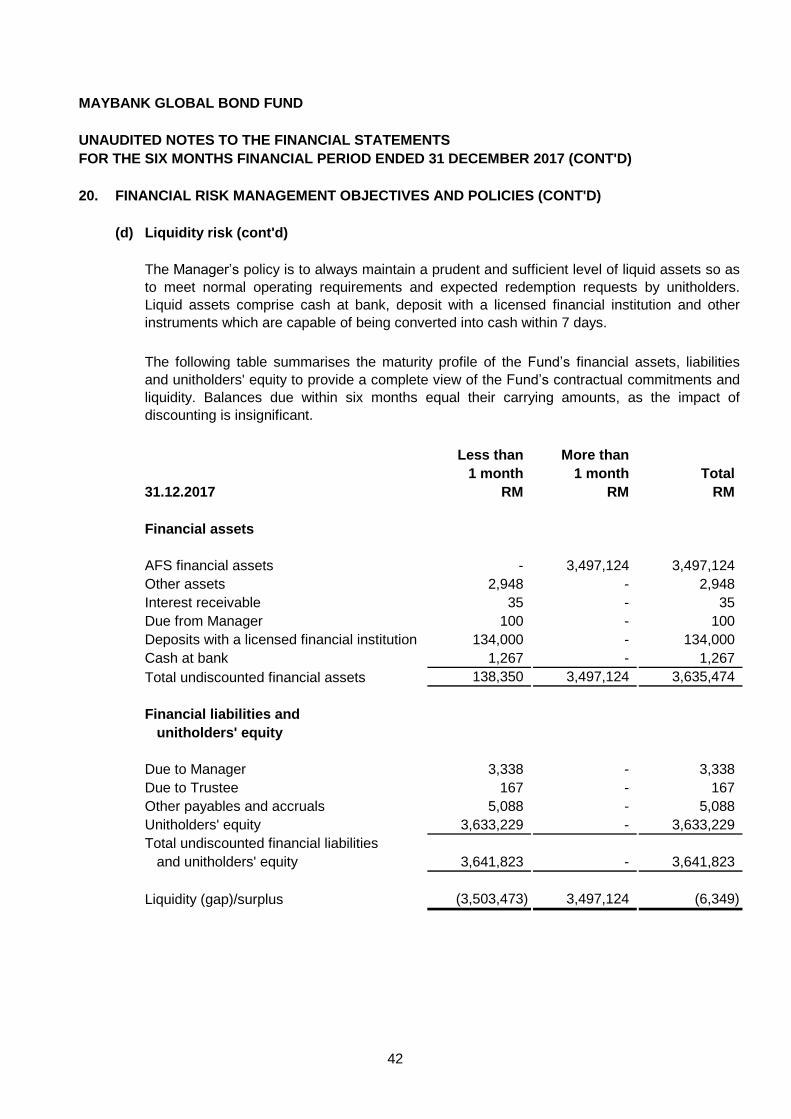

20. FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES

(a) Introduction

(b) Market risk

(i) Foreign exchange risk

The table below analyses the net positions of the Fund's financial assets and financial

liabilities which are exposed to foreign exchange risks as at 31 December 2017. As the

Fund's functional currency is RM, the financial assets and financial liabilities in other

currencies are exposed to the movement of foreign exchange rates. The exposure might

lead to the appreciation or depreciation of the financial assets and financial liabilities of the

Fund that may affect the value of the NAV attributable to unitholders.

Foreign exchange risk is the risk that the fair value or future cash flows of a financial

instrument will fluctuate because of changes in foreign exchange rates.

Market risk is the risk that the fair value or future cash flows of financial instruments will

fluctuate due to changes in market variables such as foreign exchange rates, interest rates,

and equity prices. The Fund is exposed to foreign currency risk arising from the Fund's

investment in collective investment scheme denominated in foreign currency, and other

financial assets and/or liabilities denominated in foreign currencies. The Fund is also exposed

to interest rate risk arising from its deposit placed with a licensed financial institution. The Fund

is not exposed to equity price risk as it does not hold any equity investments as at the reporting

date.

The Fund’s objective in managing risk is the creation and protection of unitholders’ value. Risk

is inherent in the Fund’s activities, but it is managed through a process of ongoing

identification, measurement and monitoring of risks. Financial risk management is also carried

out through sound internal control systems and adherence to the investment restrictions as

stipulated in the Deed, SC's Guidelines on Unit Trust Funds and CMSA.

Financial instruments that are not carried at fair value and whose carrying amounts are

reasonable approximations of fair value

There were no financial instruments which were not carried at fair value and whose carrying

amounts were not reasonable approximations of their respective fair values.

The Fund's financial instruments are not carried at fair value but their carrying amounts are

reasonable approximations of fair value due to their short term maturity.

37

Page 40

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

20. FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES (CONT'D)

(b) Market risk (cont'd)

(i) Foreign exchange risk (cont'd)

SGD TOTAL

31.12.2017 RM RM

Assets

AFS financial assets 3,497,124 3,497,124

Other assets 2,948 2,948

Total assets, and net open position 3,500,072 3,500,072

30.06.2017 (Audited)

Assets

AFS financial assets 4,513,586 4,513,586

Other assets 3,398 3,398

Total assets, and net open position 4,516,984 4,516,984

38

Page 41

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

20. FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES (CONT'D)

(b) Market risk (cont'd)

(i) Foreign exchange risk (cont'd)

Changes in Changes in

exchange Effects exchange Effects

rate on NAV rate on NAV

% RM % RM

SGD +5 175,004 +5 225,849

-5 (175,004) -5 (225,849)

(ii) Interest rate risk

(iii) Price risk

Price risk sensitivity

31.12.2017 30.06.2017

Price risk is the risk of unfavourable changes in the fair values of investments as the result

of changes in market prices (other than those arising from interest rate risk and currency

risk). The price risk exposure arises primary from the Fund’s investments in shares of the

Target Fund.

Management’s best estimate of the effect on the other comprehensive income for the

current financial year due to a reasonably possible change in price, with all other variables

held constant is indicated in the table below:

Fixed income securities are particularly sensitive to movements in market interest rates.

When interest rates rise, the value of fixed income securities will fall and vice versa, thus

affecting the NAV of the Fund. The sensitivity to market interest rate changes are normally

greater for longer tenured securities when compared to shorter tenured securities.

The table below summarises the sensitivity of the Fund's NAV to movements in exchange

rates. The analysis is based on the assumptions that the exchange rates will increase or

decrease by 5% with all other variables held constant.

The Fund's deposit with a licensed financial institution carries fixed rate and is short-term

in nature, and therefore is not affected by movements in market interest rate.

Audited

39

Page 42

MAYBANK GLOBAL BOND FUND

UNAUDITED NOTES TO THE FINANCIAL STATEMENTS

FOR THE SIX MONTHS FINANCIAL PERIOD ENDED 31 DECEMBER 2017 (CONT'D)

20. FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES (CONT'D)

(c) Credit risk

(i) Credit quality of financial assets

(ii) Credit risk concentration

The following table analyses the Fund’s investments in unquoted fixed income securities,

cash at bank, deposit with a licensed financial institution, and interest receivable by rating