51

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. Chapter 14 Options: Puts and Calls

| Date post: | 28-May-2017 |

| Category: |

Documents |

| Upload: | ashok-chowdary-g |

| View: | 213 times |

| Download: | 0 times |

Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

Chapter 14

Options: Puts and Calls

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-2

Options: Puts, Calls, and Warrants

• Learning Goals

1. Discuss the basic nature of options in general, and puts and calls in particular, and understand how these investment vehicles work.

2. Describe the options market, and note key options provisions, including strike prices and expiration dates.

3. Explain how put and call options are valued and the forces that drive options prices in the marketplace.

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-3

Options: Puts, Calls, and Warrants

• Learning Goals (cont’d)4. Describe the profit potential of puts and calls, and note

some popular put and call investment strategies.

5. Explain the profit potential and loss exposure from writing covered call options, and discuss how writing options can be used as a strategy for enhancing investment returns.

6. Describe market index options, puts and calls on foreign currencies, and LEAPS, and discuss how investors can use these securities.

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-4

Options: Puts, Calls and Warrants

• Financial Asset: asset that represents a financial claim on an issuing organization – Stocks, bonds and convertible securities

are examples

• Option: the right to buy or sell a certain amount of an underlying financial asset at a specified price for a given period of time

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-5

Types of Options

• Types of Options– Puts– Calls– Rights– Warrants

• All of the above are types of derivative securities, which derive their value from the price behavior of an underlying real or financial asset

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-6

Options: Puts and Calls

• Puts and calls may be traded on:– Common stocks– Stock indexes– Exchange traded funds– Foreign currencies– Debt instruments– Commodities and financial futures

• Owners of put and call options have no voting rights, no privileges of ownership, and no interest or dividend income

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-7

Options: Puts and Calls (cont’d)

• Options allow buyers to use leverage; investors can buy a lot of price action with limited capital

• Options allows investors to nearly always enjoy limited exposure to risk

• Puts and calls are created by individual investors, not by the organizations that issue the underlying financial asset

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-8

Options: Puts and Calls (cont’d)

• Option Buyer:– Has the right to buy or sell an underlying asset

for a given period of time, at a price that was fixed at the time of the option contract in exchange for paying the seller a fee

• Buyer can walk away from a bad option

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-9

Options: Puts and Calls (cont’d)

• Option Seller/Maker/Writer:– Has the obligation to buy or sell the underlying

asset according to the terms of the option contract, for which the seller has been paid a certain amount of money

• Seller cannot walk away from a bad option

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-10

Options: Puts and Calls (cont’d)

• Put and call options trade in the open market much like any other security and may be bought and sold through securities brokers and dealers

• Values of puts and calls change with the values of the underlying assets

• Values of puts and calls change with the time period before they expire:– Closer to expiration date, option values go down

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-11

Advantages of Puts and Calls

• Allows use of leverage– Leverage: the ability to obtain a given equity

position at a reduced capital investment, thereby magnifying total return

• Option buyer’s exposure to risk is limited to fee paid to purchase the put or call option

• Investor can make money when value of assets go up or down

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-12

Disadvantages of Puts and Calls

• Investor does not receive any interest or dividend income

• Options expire; the investor has limited time to benefit from options before they become worthless

• Options are complex and tricky• Option seller’s exposure to risk may be unlimited• Options are risky because an investor has to be

correct on two decisions to make money:– Which direction the price of the asset will move– When the price change will occur

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-13

How Calls Work

• Call: a negotiable instrument that gives the holder (buyer) the right to buy the underlying security at a specified price over a set period of time from the seller/maker/writer in exchange for a fee paid to the seller/maker/writer– The buyer of the call option wants the price of the

underlying assets to go up– The seller/maker/writer of the call option wants the price

of the underlying assets to go down

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-14

How Calls Work (cont’d)

• If the price of the underlying assets goes up:– The buyer will buy the asset at the lower strike price

from the seller/maker/writer and sell it at the higher market price, making a profit

– The seller will sell the assets at a price lower than the market price. If the seller does not already own the assets, then the seller will have to purchase them at the higher market price

• Covered call: seller owns the asset• Naked call: seller does not own the asset

Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

How Calls Work (cont’d)

• If the price of the underlying assets go down:

– The buyer will let the call option expire worthless and lose the fee paid

– The seller will keep the fee received and make a profit

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-16

How Calls Work (cont’d)

• Example: Assume the market price for a share of common stock is $50. A call option to purchase 100 shares of the stock at a strike price of $50 per share may be purchased for $500

• If the market price of the stock goes up to $75 per share, the buyer will purchase 100 shares at the strike price from the seller/maker/writer and sell them at the higher market price.

• The buyer’s profit will be:

• The seller/maker/writer’s loss will be:

Profit [(Market price – Strike price) 100 Shares] Cost of call$2,000 [($75 $50) 100 Shares] $500

Loss [(Strike price Market price) 100 Shares] Fee for call$(2,000) [($50 $75) 100 Shares] $500

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-17

How Calls Work:The Value of Leverage

• Example: Assume the market price for a share of common stock is $50. A call option to purchase 100 shares of the stock at a strike price of $50 per share may be purchased for $500

• If the market price of the stock goes up to $75 per share, the buyer will purchase 100 shares at the strike price from the seller/maker/writer and sell them at the higher market price. The buyer’s profit will be $2,000.

• The buyer’s total return using the call option will be:

• The buyer’s total return directly owning the stock would be:

Total Return Profit

Amount invested

$2,000$500

400%

Total Return Profit

Amount invested

$2,000$5,000

40%

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-18

How Calls Work (cont’d)

• Example: Assume the market price for a share of common stock is $50. A call option to purchase 100 shares of the stock at a strike price of $50 per share may be purchased for $500

• If the market price of the stock goes down to $25 per share, the buyer will allow the call option to expire worthless.

• The buyer’s loss will be:

• The seller/maker/writer’s profit will be:

Loss Cost of callLoss $(500)

Profit Fee of callProfit $(500)

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-19

How Puts Work

• Put: a negotiable instrument that enables the holder (buyer) to sell the underlying security at a specified price over a set period of time to the seller/maker/writer in exchange for a fee paid to the seller/maker/writer– The buyer of the put option wants the price of the

underlying assets to go down

– The seller/maker/writer of the put option wants the price of the underlying assets to go up

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-20

How Puts Work (cont’d)

• If the price of the underlying assets goes down:– The buyer will buy the asset on the market at the lower

price and force the seller/maker/writer to buy the asset at the higher option price, making a profit

– The seller will pay a price higher than the market price and will own expensive assets or will have to sell them at a loss

• If the price of the underlying assets go up:– The buyer will let the put option expire worthless and lose

the fee paid– The seller will keep the fee received and make a profit

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-21

How Puts Work (cont’d)

• Example: Assume the market price for a share of common stock is $50. A put option to sell 100 shares of the stock at a strike price of $50 per share may be purchased for $500.

• If the market price of the stock goes down to $25 per share, the buyer will purchase 100 shares at the market price and force the seller/maker/writer to buy them at the option strike price.

• The buyer’s profit will be:

• The seller/maker/writer’s loss will be:

Profit [(Strike price Market price) 100 shares] Cost of put$2,000 [($50 $25) 100 Shares] $500

Loss [(Market price Strike price) 100 shares] Fee for put($2,000) [($25 $50) 100 Shares] $500

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-22

How Puts Work (cont’d)

• Example: Assume the market price for a share of common stock is $50. A put option to sell 100 shares of the stock at a strike price of $50 per share may be purchased for $500.

• If the market price of the stock goes up to $75 per share, the buyer will allow the put option to expire worthless.

• The buyer’s loss will be:

• The seller/maker/writer’s profit will be:

Loss Cost of putLoss $(500)

Profit Fee for putProfit $500

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-23

Put and Call Options Markets

• Conventional (OTC) Options– Sold over the counter– Primarily used by institutional investors

• Listed Options– Created in 1973 by the Chicago Board Option Exchange (CBOE)– Puts and calls traded through CBOE exchange, as well as

International Securities Exchange, AMEX, Philadelphia exchange, NYSE Arca and Boston Options Exchange.

– Provided convenient market that made options trading more popular and help create a secondary market

– Helped standardize expiration dates and exercise/strike prices– Reduced trading costs

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-24

Stock Options

• Common Stock Options– Over 1.5 billion option contracts are traded

each year– Options on common stocks is the most popular

form of option– Over 90% of all option contracts are

stock options

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-25

Key Provisions of Stock Options

• Strike Price– Stated price at which you can buy a security with a call or

sell a security with a put– Conventional (OTC) options may have any strike price– Listed options have standardized prices with price

increments determined by the price of the stock• Expiration Date

– Stated date when the option expires and becomes worthless if not exercised

– Conventional (OTC) options may have any working day as expiration date

– Listed options have standardized expiration dates

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-26

Figure 14.1 Quotations for Listed Stock Options

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-27

Expiration Date of Listed Stock Options

• Three Expiration Cycles– The January/April/July/October cycle– The February/May/August/November cycle– The March/June/September/December cycle

• The longest-term expiration dates are normally no longer than nine months

• The options that are longer than nine months are called LEAPS, and they are only available on some of the stocks

• Listed options always expire on the third Friday of the month of expiration

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-28

Valuation of Stock Options

• Option Premium (Price): the quoted price the investor pays to buy a listed put or call option

• Option premiums (prices) are affected by:– Fundamental (intrinsic) value: based upon

current market price of underlying assets– Time Premium: amount that option price

exceeds the fundamental value

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-29

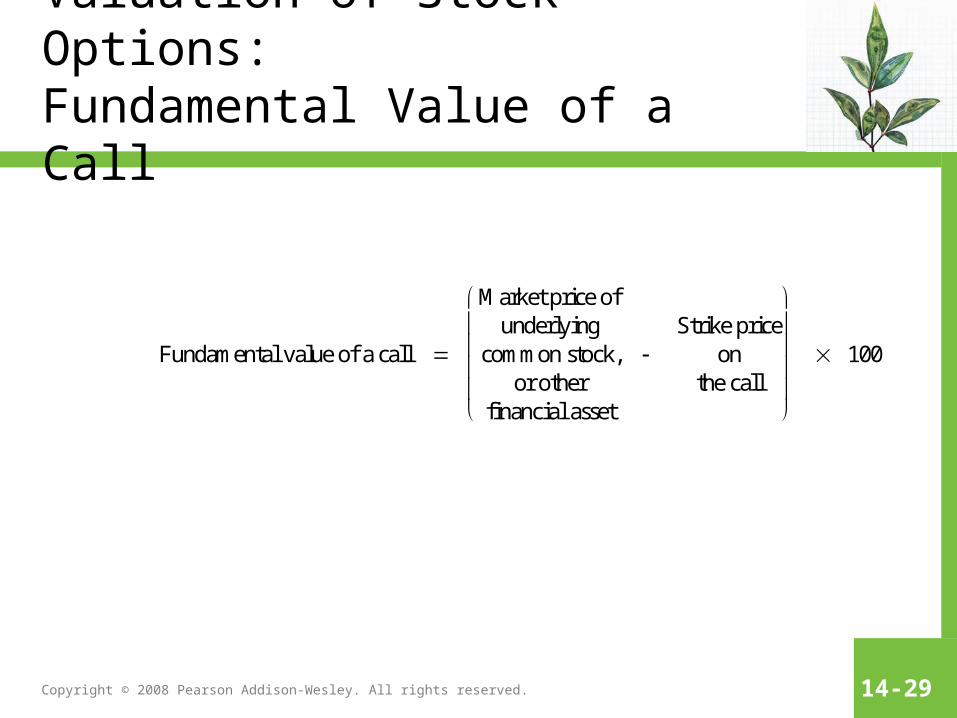

Valuation of Stock Options:Fundamental Value of a Call

Fundamental value of a call

Market price ofunderlying

common stock,or other

financial asset

Strike price

onthe call

100

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-30

Valuation of Stock Options:Fundamental Value of a Put

Fundamental value of a put Strike price

onthe put

Market price ofunderlying

common stock,or other

financial asset

100

V SPP MP 100

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-31

Figure 14.2 The Valuation Properties of Put and Call Options

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-32

Valuation of Stock Options

• In-the-Money– Call option: when the strike price is less than the market

price of the underlying security– Put option: when the strike price is greater than the

market price of the underlying security

• Out-of-the-Money– Call option: when the strike price is greater than the

market price of the underlying security– Put option: when the strike price is less than the market

price of the underlying security

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-33

Table 14.1 Option Price Components for an Actively Traded Call Option

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-34

Option Trading Strategies

• Buying for Speculation• Hedging to modify risks• Writing Options to enhance returns• Spreading Options to enhance returns

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-35

Speculating with Stock Options

• Similar to investing in common stocks– Goal is to “buy low, sell high”– Buyer does not need as much capital since can

use leverage– Buyer cannot lose more than cost of the option

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-36

Table 14.2 Speculating with Call Options

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-37

Hedging with Stock Options

• Purpose is to reduce or eliminate risk• Combines two or more securities into a single investment

position• Hedging a “Long” Position

– Buying a put and holding appreciated stock in the same company– Buying a put would provide “insurance” in case the stock price went

down before you sold the stock

• Hedging a “Short” Position– Selling stock short and buying a call– Buying a call would allow you to buy stock to cover the short sale if

the stock price went up instead of down

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-38

Table 14.3 Limiting Capital Loss with a Put Hedge

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-39

Table 14.4 Protecting Profits with a Put Hedge

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-40

Writing Stock Options

• The seller/maker/writer is betting that the option buyer will be wrong about the direction of the stock price or the time period the price change will occur– Statistically, the odds favor the writer over the buyer– Easy money if the option expires worthless. The writer cannot

make more than the fee received– High risk if the option is “in-the-money”

• Naked options: writer does not own the optioned securities and has to buy them. No limit on loss exposure

• Covered options: writer owns the optioned securities. Loss exposure is limited to the price originally paid for the securities

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-41

Table 14.5 Covered Call Writing

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-42

Spreading Options

• Purpose is to take advantage of differences in prevailing option prices and premiums

• Combines two or more options into a single transaction• “Vertical” Spread

– Buying a call at one strike price and writing a call (on same stock for same expiration date) at a higher strike price

• “Option” Straddle– Simultaneous purchase (or sale) of both a put and a call on the

same underlying common stock

• Spreading options is extremely tricky and should be used only by knowledgeable investors

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-43

Stock-Index Options

• Stock-Index Option: a put or call option written on a specific stock market index

• Major stock indexes for options:– The S&P 500 Index– The S&P 100 Index– The Dow Jones Industrial Average– The Nasdaq 100 Index

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-44

Stock-Index Options (cont’d)

• Market price is function of strike price of option and latest published stock market index value

• Valuation techniques are similar to valuing options for individual securities

• Price behavior and investment risk are similar to options for individual securities

• May be used to hedge a whole portfolio of stocks rather than individual stocks

• May be used to speculate on the stock market as a whole

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-45

Other Types of Options

• Exchange traded funds: put and call options written on exchange traded funds (EFT’s)– Very similar to market index options

• Interest rate options: put and call options written on fixed-income (debt) securities– Small market involving only U.S. Treasury securities– Option prices change with yield behavior of

debt securities

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-46

Other Types of Options (cont’d)

• Currency options: put and call options written on foreign currencies– Available on most major world currencies – Option prices change as exchange rates between

currencies fluctuate

• LEAPS: long-term options that may extend out to 3 years– Available on several hundred stocks and over two

dozen stock indexes and ETF’s

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-47

Chapter 14 Review

• Learning Goals1. Discuss the basic nature of options in general, and puts

and calls in particular, and understand how these investment vehicles work.

2. Describe the options market, and note key options provisions, including strike prices and expiration dates.

3. Explain how put and call options are valued and the forces that drive options prices in the marketplace.

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-48

Chapter 14 Review (cont’d)

• Learning Goals (cont’d)4. Describe the profit potential of puts and calls, and note

some popular put and call investment strategies.

5. Explain the profit potential and loss exposure from writing covered call options, and discuss how writing options can be used as a strategy for enhancing investment returns.

6. Describe market index options, puts and calls on foreign currencies, and LEAPS, and discuss how investors can use these securities.

Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

Chapter 14

Additional Chapter Art

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-50

Figure 14.3 Quotations on Index Options

Copyright © 2008 Pearson Addison-Wesley. All rights reserved. 14-51

Table 14.6 Foreign Currency Option Contracts on the Philadelphia Exchange