Multiple Choice Problems 1. a Combined equipment amounts P1,050,000 Less: gain on sale 25,000 Consolidated equipment balance P1,025,000 Combined Accumulated Depreciation P 250,000 Less: Depreciation on gain 5,000 Consolidated Accumulated Depreciation P 245,000 2. a Original cost of P1,100,000 Accumulated depreciation, 1/1/20x4 P 250,000 Add: Additional depreciation (P1,100,000 – P100,000) / 20 years ____50,000 Accumulated depreciation, 12/31/20x4 P 300,000 3. a Combined building amounts P650,000 Less: Intercompany gain __30,000 Consolidated buildings P620,000 Combined Accumulated Depreciation P195,000 Less: Piecemeal recognition of gain ___3,000 Consolidated accumulated depreciation P192,000 4. a – the amount of land that will be presented in the presented in the CFS is the original cost of P416,000 + P256,000 = P672,000. 5. a The costs incurred by BB to develop the equipment are research and development costs and must be expensed as they are incurred. Transfer to another legal entity does not cause a change in accounting treatment within the economic entity. 6. e Original cost of P 100,000 Accumulated depreciation, 1/1/20x6 (P100,000 x 50%) P 50,000 Add: Additional depreciation (P100,000 – P50,000) / 5 years ___10,000 Accumulated depreciation, 12/31/20x6 P 60,000 7. d Sales price P

Transcript

Multiple Choice Problems 1. a

Combined equipment amounts P1,050,000Less: gain on sale 25,000Consolidated equipment balance P1,025,000

Combined Accumulated Depreciation P 250,000Less: Depreciation on gain 5,000Consolidated Accumulated Depreciation P 245,000

2. aOriginal cost of P1,100,000

Accumulated depreciation, 1/1/20x4 P 250,000Add: Additional depreciation (P1,100,000 – P100,000) / 20 years ____50,000Accumulated depreciation, 12/31/20x4 P 300,000

3. aCombined building amounts P650,000Less: Intercompany gain __30,000Consolidated buildings P620,000

Combined Accumulated Depreciation P195,000Less: Piecemeal recognition of gain ___3,000Consolidated accumulated depreciation P192,000

4. a – the amount of land that will be presented in the presented in the CFS is the original cost of P416,000 + P256,000 = P672,000.

5. a The costs incurred by BB to develop the equipment are research and development costs and must be expensed as they are incurred. Transfer to another legal entity does not cause a change in accounting treatment within the economic entity.

6. e Original cost of P 100,000

Accumulated depreciation, 1/1/20x6 (P100,000 x 50%) P 50,000Add: Additional depreciation (P100,000 – P50,000) / 5 years ___10,000Accumulated depreciation, 12/31/20x6 P 60,000

7. dSales price P 80,000Less: Book value Cost P100,000 Less: Accumulated depreciation (50% x P100,000) __50,000 __50,000Unrealized gain on sale P 30,000Less: Realized gain - depreciation (P30,000 / 5 years) ___6,000Net unrealized gain, 12/31/20x6 P 24,000

8. e Eliminating entries: 12/31/20x6: subsequent to date of acquisition Realized Gain – depreciation

Accumulated depreciation 6,000 Depreciation expense 6,000 [P80,000 - (P100,000 - {P100,000 x 50%])] = P30,000 / 5 years or P15,000 – P8,000 = P7,000

“Should be in CFS” Parent – Pylux “Recorded as” Subsidiary - SyluxDepreciation expense (P50,000 /5 years) 10,000

Depreciation expense (P80,000 / 5 years) 16,000

Acc. Depreciation 8,000 Acc. depreciation 16,000

9. d20x4 20x5

Unrealized gain on sales of equipment (downstream sales) ( 90,000) -0-Realized gain on sale of equipment (downstream sales) through depreciation P90,000 / 10 years

___9,000 9,000

Net ( 81,000) 9,000

10. d20x4 20x5

Unrealized gain on sale of equipment (downstream sales) ( 150,000) -0-Realized gain on sale of equipment (downstream sales) through depreciation P150,000 / 10 years

___15,000 15,000

Net ( 135,000) 15,000

11. a20x4 20x5

Unrealized gain on sale of equipment (upstream sales) : 50,000 – 30,000 ( 20,000) -0-Realized gain on sale of equipment (upstream sales) through depreciation P20,000 / 5 years ___4,000 __4,000Net ( 16,000) __4,000

12. eOriginal cost of P

100,000

Accumulated depreciation, 1/1/20x6 P 40,000

Add: Additional depreciation (P100,000 – P40,000) / 6 years x 2 years ___20,000

Accumulated depreciation, 12/31/20x4 P 70,000

13. cSales price P 48,000Less: Book value Cost P100,000 Less: Accumulated depreciation __40,000 __60,000Unrealized loss on sale P(12,000)Add: Realized loss - depreciation (P12,000 / 6 years) x 2 years

___4,000

Net unrealized loss, 12/31/20x7 P( 8,000)

14. a Eliminating entries: 12/31/20x7: subsequent to date of acquisition Realized Gain – depreciation

[P48,000 - (P100,000 - P40,000) = P(12,000) / 6 years or P10,000 – P8,000 = P2,000

“Should be in CFS” Parent – Poxey “Recorded as” Subsidiary - SoxeyDepreciation expense (P60,000 /6 years) 10,000

Depreciation expense (P48,000 / 6 years) 8,000

Acc. Depreciation 10,000 Acc. depreciation 8,000

15. c Original cost of P

100,000

Accumulated depreciation, 1/1/20x6 (P100,000 - P20,000) P 80,000

Add: Additional depreciation (P100,000 – P80,000) / 5 years x 2 years ____8,000Accumulated depreciation, 12/31/20x7 P

88,000

16. cSales price P 45,000Less: Book value Cost P100,000 Less: Accumulated depreciation __80,000 __20,000Unrealized gain on sale P 25,000Less: Realized gain - depreciation (P25,000 / 5 years) x 2 years

__10,000

Net unrealized gain, 12/31/20x7 P 15,000

17. b Eliminating entries: 12/31/20x7: subsequent to date of acquisition Realized Gain – depreciation

22. bConsolidated Net Income for 20x5 P Company’s net income from own/separate operations…………. P 98,000 Realized gain on sale of equipment (downstream sales) through depreciation

___0

P Company’s realized net income from separate operations*…….….. P 98,000 S Company’s net income from own operations…………………………………. P 55,000 Unrealized gain on sales of equipment (upstream sales) (15,000) Realized gain on sale of equipment (upstream sales) through depreciation (P15,000 / 3 years) 5,000 S Company’s realized net income from separate operations*…….….. P 45,000 45,000 Total P143,000 Less: Amortization of allocated excess…………………… 0 Consolidated Net Income for 20x5 P143,000 Less: Non-controlling Interest in Net Income* * 18,000 Controlling Interest in Consolidated Net Income or Profit attributable to equity holders of parent – 20x5………….. P125,000

*that has been realized in transactions with third parties.

Or, alternativelyConsolidated Net Income for 20x5 P Company’s net income from own/separate operations…………. P 98,000 Realized gain on sale of equipment (downstream sales) through depreciation

___0

P Company’s realized net income from separate operations*…….….. P 98,000 S Company’s net income from own operations…………………………………. P 55,000 Unrealized gain on sales of equipment (upstream sales) (15,000) Realized gain on sale of equipment (upstream sales) through depreciation (P15,000 / 3 years) 5,000 S Company’s realized net income from separate operations*…….….. P 45,000 45,000 Total P143,000 Less: Non-controlling Interest in Net Income* * P 18,000 Amortization of allocated excess…………………… ____0 18,000 Controlling Interest in Consolidated Net Income or Profit attributable to equity holders of parent………….. P125,000 Add: Non-controlling Interest in Net Income (NCINI) _ 18,000 Consolidated Net Income for 20x5 P143,000

*that has been realized in transactions with third parties.

**Non-controlling Interest in Net Income (NCINI) for 20x5 S Company’s net income of Subsidiary Company from its own operations (Reported net income of S Company)

P 55,000

Unrealized gain on sales of equipment (upstream sales) ( 15,000) Realized gain on sale of equipment (upstream sales) through depreciation 5,000 S Company’s realized net income from separate operations……… P 45,000 Less: Amortization of allocated excess 0

P 45,000 Multiplied by: Non-controlling interest %.......... 40% Non-controlling Interest in Net Income (NCINI) - partial goodwill P 18,000 Less: NCI on goodwill impairment loss on full-goodwill . . . . . . . . . . . . . . . . . . . . . 0 Non-controlling Interest in Net Income (NCINI) – full goodwill . . . . . . . . . . . . . P 18,000

23. a - refer to No. 22 computation24. a25. a26. b27. d – the entry under the cost model would be as follows ;

29. a30. b31. c – P50,000/5 years = P10,000 per year starting January 1, 20x6.32. b

Depreciation expense recorded by PirnP40,000

Depreciation expense recorded by Scroll 10,000 Total depreciation reported P50,000 Adjustment for excess depreciation charged by Scroll as a result of increase in carrying value of equipment due to gain on intercompany sale (P12,000 / 4 years) (3,000 )Depreciation for consolidated statements P47,000

33. eDepreciation expense: Parent P 84,000 Subsidiary 60,000Total P144,000Less: Over-depreciation due to realized gain: [P115,000 – (P125,000 – P45,000)] = P35,000/8 years __ 4,375Consolidated net income P139,625

34. c20x6

Unrealized gain on sale of equipment ( 56,000)Realized gain on sale of equipment (upstream sales) through depreciation ___7,000Net ( 49,000)

Selling price P 392,000

Less: Book value, 1/1/20x6 Cost, 1/1/20x2 P420,000 Less: Accumulated depreciation: P420,000/10 years x 2 years

84,000 336,000

Unrealized gain on sale of equipment P 56,000Realized gain – depreciation: P56,000/8 years P 7,000

35. c – (P22,500 x 4/15 = P6,000)36. a – [P50,000 – (P50,000 x 4/10) = P30,000]37.

b The P39,000 paid to GG Company will be charged to depreciation expense by TLK Corporation over the remaining 3 years of ownership. As a result, TLK Corporation will debit depreciation expense for P13,000 each year. GG Company had charged P16,000 to accumulated depreciation in 2 years, for an annual rate of P8,000. Depreciation expense therefore must be reduced by P5,000 (P13,000 - P8,000) in preparing the consolidated statements.

38.

a TLK Corporation will record the purchase at P39,000, the amount it paid. GG Company had the equipment recorded at P40,000; thus, a debit of P1,000 will raise the equipment balance back to its original cost from the viewpoint of the consolidated entity.

39.

b Reported net income of GG Company P 45,000

Reported gain on sale of equipment P15,000 Intercompany profit realized in 20x6 (5,000) (10,000 )Realized net income of GG Company P 35,000 Proportion of stock held by non-controlling interest x .40 Income assigned to non-controlling interests P 14,000

40.

c Operating income reported by TLK Corporation P 85,000

Net income reported by GG Company 45,000 P130,000

Less: Unrealized gain on sale of equipment (P15,000 - P5,000) (10,00

0)Consolidated net income P120,000

41. b Eliminating entries: 12/31/20x5: date of acquisition Restoration of BV and eliminate unrealized gain

MortarSelling price P390,000Less: Book value, 12/31/20x5 Cost, 1/1/20x2 P400,000 Less: Accumulated depreciation : P400,000/10 years x 4 years

160,000 240,000

Unrealized gain on sale of equipment P 150,000

Realized gain – depreciation: P150,000/6 years P 25,000

42. a – refer to No. 41 for computation43. b - refer to No. 41 for computation44. d Eliminating entries: 12/31/20x6: subsequent to date of acquisition Realized Gain – depreciation

Accumulated depreciation 25,000 Depreciation expense 25,000 P150,000 / 6 years or P65,000 – P40,000

“Should be in CFS” Parent Books – Mortar “Recorded as” Subsidiary Books - Granite

Depreciation expense (P400,000 / 10 years) 40,000

Depreciation expense (P390,000 / 6 years) 65,000

Acc. Depreciation 40,000 Acc. depreciation 65,000

45. c Eliminating entries: 12/31/20x6: subsequent to date of acquisition

46. aTotal gain on the sale = P1,000,000 – (P500,000 - P150,000) = P650,000Unconfirmed gain after three years = 2/5 x P650,000 = P260,000

47. dDepreciation to 1/1/x3 is P25,000Depreciation expense for 20x3 and 20x4 is (P85,000 - P25,000)/6 = P10,000 per yearTherefore accumulated depreciation at 12/31/x4 is P45,000.Net equipment balance is P85,000 - P45,000 = P40,000.

48. bAt the end of two years, the subsidiary reports the equipment at original cost of P2,500,000 and accumulated depreciation of (P2,500,000/10) x 2 = P500,000. Depreciation expense is P250,000.

The consolidated balance sheet reports the equipment at original cost of P1,000,000 and accumulated depreciation of P200,000 + ([(P1,000,000 - P200,000)/10] x 2) = P360,000.Depreciation expense is P80,000.

Eliminating entries at the end of the second year are:

Accumulated depreciation 170,000Investment in subsidiary 1,530,000

The subsidiary reports depreciation expense for the year at P500,000 (P2,500,000/5) and a gain on the sale at P1,750,000 [P2,750,000 - ((P2,500,000 - (3)(P500,000))]. The consolidated statements show depreciation expense for the year at P600,000 (P3,000,000/5) and a gain on the sale at P1,550,000 [P2,750,000 - ((P3,000,000 - (3)(P600,000))]. Therefore the eliminating entries increase depreciation expense by P100,000 and reduce the gain by P200,000, for a net effect on consolidated income of: P300,000 decrease.

51. aConsolidated Net Income for 20x9 P Company’s net income from own/separate operations…………. P 140,000 Realized gain on sale of equipment (downstream sales) through depreciation

___0

P Company’s realized net income from separate operations*…….….. P 140,000 S Company’s net income from own operations…………………………………. P 30,000

Unrealized loss on sale of equipment (upstream sales) 20,000 Realized loss on sale of equipment (upstream sales) through depreciation – none, since the date of sale is end of the year

( 0)

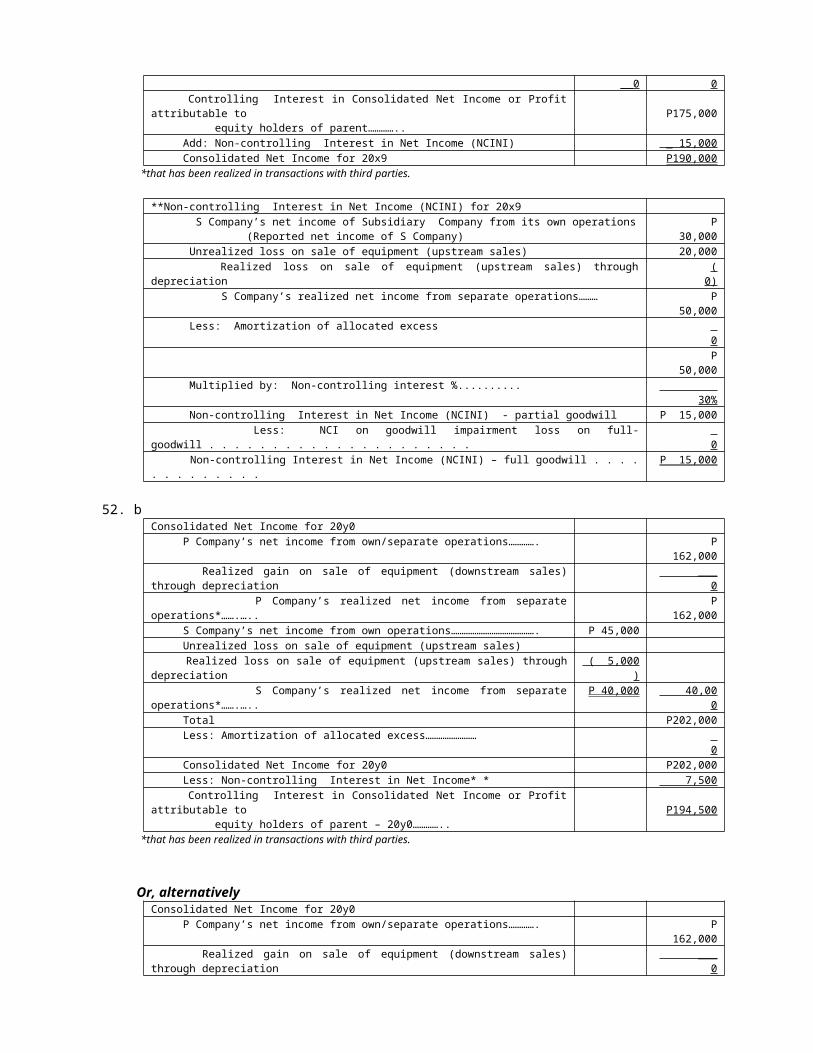

S Company’s realized net income from separate operations*…….….. P 50,000 50,000 Total P190,000 Less: Amortization of allocated excess…………………… 0 Consolidated Net Income for 20x9 P190,000 Less: Non-controlling Interest in Net Income* * 15,000 Controlling Interest in Consolidated Net Income or Profit attributable to equity holders of parent – 20x9………….. P175,000

*that has been realized in transactions with third parties.

Selling price P180,000Less: Book value, 12/31/20x9 Cost, 1/1/20x4 P500,000 Less: Accumulated depreciation : P500,000/10 years x 6 years

300,000 200,000

Unrealized loss on sale of equipment P( 20,000)

Realized loss – depreciation: P20,000/4 years P( 5,000)

Or, alternativelyConsolidated Net Income for 20x9 P Company’s net income from own/separate operations…………. P 140,000 Realized gain on sale of equipment (downstream sales) through depreciation

___0

P Company’s realized net income from separate operations*…….….. P 140,000 S Company’s net income from own operations…………………………………. P 30,000 Unrealized loss on sale of equipment (upstream sales) 20,000 Realized loss on sale of equipment (upstream sales) through depreciation ( 0) S Company’s realized net income from separate operations*…….….. P 50,000 50,000 Total P190,000 Less: Non-controlling Interest in Net Income* * P 15,000 Amortization of allocated excess…………………… ____0 15,000 Controlling Interest in Consolidated Net Income or Profit attributable to equity holders of parent………….. P175,000 Add: Non-controlling Interest in Net Income (NCINI) _ 15,000 Consolidated Net Income for 20x9 P190,000

*that has been realized in transactions with third parties.

**Non-controlling Interest in Net Income (NCINI) for 20x9 S Company’s net income of Subsidiary Company from its own operations (Reported net income of S Company)

P 30,000

Unrealized loss on sale of equipment (upstream sales) 20,000 Realized loss on sale of equipment (upstream sales) through depreciation ( 0) S Company’s realized net income from separate operations……… P 50,000 Less: Amortization of allocated excess 0

P 50,000 Multiplied by: Non-controlling interest %.......... 30% Non-controlling Interest in Net Income (NCINI) - partial goodwill P 15,000 Less: NCI on goodwill impairment loss on full-goodwill . . . . . . . . . . . . . . . . . . . . . 0 Non-controlling Interest in Net Income (NCINI) – full goodwill . . . . . . . . . . . . . P 15,000

52. bConsolidated Net Income for 20y0 P Company’s net income from own/separate operations…………. P 162,000 Realized gain on sale of equipment (downstream sales) through depreciation

___0

P Company’s realized net income from separate operations*…….….. P 162,000 S Company’s net income from own operations…………………………………. P 45,000 Unrealized loss on sale of equipment (upstream sales) Realized loss on sale of equipment (upstream sales) through depreciation ( 5,000) S Company’s realized net income from separate operations*…….….. P 40,000 40,000 Total P202,000 Less: Amortization of allocated excess…………………… 0 Consolidated Net Income for 20y0 P202,000

Less: Non-controlling Interest in Net Income* * 7,500 Controlling Interest in Consolidated Net Income or Profit attributable to equity holders of parent – 20y0………….. P194,500

*that has been realized in transactions with third parties.

Or, alternativelyConsolidated Net Income for 20y0 P Company’s net income from own/separate operations…………. P 162,000 Realized gain on sale of equipment (downstream sales) through depreciation

___0

P Company’s realized net income from separate operations*…….….. P 162,000 S Company’s net income from own operations…………………………………. P 45,000 Unrealized loss on sale of equipment (upstream sales) Realized loss on sale of equipment (upstream sales) through depreciation ( 5,000) S Company’s realized net income from separate operations*…….….. P 40,000 40,000 Total P202,000 Less: Non-controlling Interest in Net Income* * P 7,500 Amortization of allocated excess…………………… ____0 7,500 Controlling Interest in Consolidated Net Income or Profit attributable to equity holders of parent………….. P194,500 Add: Non-controlling Interest in Net Income (NCINI) _ _ 7,500 Consolidated Net Income for 20y0 P202,000

*that has been realized in transactions with third parties.

**Non-controlling Interest in Net Income (NCINI) for 20y0 S Company’s net income of Subsidiary Company from its own operations (Reported net income of S Company)

P 30,000

Unrealized loss on sale of equipment (upstream sales) Realized loss on sale of equipment (upstream sales) through depreciation ( 5,000) S Company’s realized net income from separate operations……… P 25,000 Less: Amortization of allocated excess 0

P 25,000 Multiplied by: Non-controlling interest %.......... 30% Non-controlling Interest in Net Income (NCINI) - partial goodwill P 7,500 Less: NCI on goodwill impairment loss on full-goodwill . . . . . . . . . . . . . . . . . . . . . 0 Non-controlling Interest in Net Income (NCINI) – full goodwill . . . . . . . . . . . . . P 7,500

53. d Eliminating entries: 1/1/20x5: date of acquisition Restoration of BV and eliminate unrealized gain

Building 3,000Gain 8,250 Accumulated depreciation 11,250

Parent Books – Sky Subsidiary Books - EarthCash 33,000 Building 33,000Accumulated depreciation 11,250 Cash 33,000 Building 36,000 Gain 8,250

Sky, 7/1/20x4Selling price P33,000Less: Book value, 7/11/20x4 Cost, 1/1/20x2 P36,000 Less: Accumulated depreciation : P36,000/8years x 2.5 years

11,250 24,750

Unrealized gain on sale of equipment P 8,250Realized gain – depreciation: P8,250/5.5 years P 1,500

54. a - refer to No. 53 for computation55. b Eliminating entries: 12/31/20x4: subsequent to date of acquisition

Realized Gain – depreciation (July 1, 20x4 – December 31, 20x4)Accumulated depreciation 750 Depreciation expense 750 P8,250 / 5.5 x ½ years or P3,000 – P2,250

“Should be in CFS” Parent Books – Sky “Recorded as” Subsidiary Books - EarthDepreciation expense (P24,750 / 5.5 x ½ years) 2,250

Depreciation expense (P33,000 / 5.5 years x ½ yrs)

3,000

Acc. Depreciation 2,250 Acc. depreciation 3,000

56. c Eliminating entries: 12/31/20x5: subsequent to date of acquisition Realized Gain – depreciation

Accumulated depreciation 1,500 Depreciation expense 1,500 P8,250 / 5.5 x years or P6,000 – P4,500

“Should be in CFS” Parent Books – Sky “Recorded as” Subsidiary Books - EarthDepreciation expense (P24,750 / 5.5 years) 4,500

Depreciation expense (P33,000 / 5.5 years) 6,000

Acc. Depreciation 4,500 Acc. depreciation 6,000

57. d Eliminating entries: 1/1/20x5: subsequent to date of acquisition

d When only retained earnings is debited, and not the non-controlling interest, a gain has been recorded in a prior period on the parent's books.

65. d66. a67. b68. b – at its original cost or book value.

69. b 20x4: Any intercompany gain should be eliminated in the CFS. 20x5

Selling price – unrelated party P 100,000Less: Original Book value, 9/26/20x5 __60,000Accumulated depreciation, 9/26/20x5 P 40,000

70. d – P30,000 + P40,000 = P70,000S P Consolidated

Selling price Less: Book value

Gain P 30,000 P 40,000 P 70,000

71. d – P110,000 – P30,000 = P80,000S (Nectar) P (Lorikeet) Consolidated

Selling price P 50,000 P 110,000 P 110,000Less: Book value _30,000 __50,000 _30,000Gain P 20,000 P 60,000 P 80,000

72. dS P Consolidated

Selling price P1,980,000

P1,440,000

P1,440,000

Less: Book value: Cost P2,000,000

P1,980,000

P 1,800,000

Accumulated

___200,000

1,800,00 *1,320,000

660,000

**1,200,000

__600,000

Unrealized gain on sale of equipment P

180,000Realized Gain – depreciation (P180,000/9 x 6 yrs) 120,000Net unrealized gain, 1/1/20x9 P

60,000Gain on sale P

60,000P

780,000P 840,000

*P1,980,000/ 9 x 6 years = P1,320,000 **P1,800,000/9 x 6 years = P1,200,000

73. d –(P100,000 + P50,000 = P150,000)S P Consolidated

Selling price Less: Book valueGain P

100,000P 50,000 P 150,000

74. c S P Consolidated

Selling price P 990,000

P720,000 P 720,000

Less: Book value : Cost P1,000,000

P990,000 P 900,000

Accumulated

100,000 __900,000

*440,000 550,000

**400,000 __500,000

Unrealized gain on sale of Equipment,1/1/20x4 P

90,000Realized Gain – depreciation (P90,000/9 x 4 yrs) 40,000Net unrealized gain, 1/1/20x8 P

50,000__________ ___________

Gain on sale P 50,000

P 170,000

P 220,000

*P990,000/ 9 x 4 years = P440,000 **P900,000/9 x 4 years = P400,00075. d – (P30,000 + P15,000)76. c

Selling price – unrelated party P 14,000Less: Original Book value, 12/31/20x5 Book value, 1/1/20x4 P20,000 Less: Depreciation for 20x4 and 20x5: P20,000/4 years x 2 years 10,000 10,000Accumulated depreciation, 12/31/20x4 P 4,000

Unrealized gain on sale of Equipment, 12/30/20x3 P

10,000Realized Gain – depreciation (P10,000/6 x 3 yrs) __

5,000Net unrealized gain, 12/31/20x6

P 5,000

__________ _________

Gain on sale P 5,000 P 15,000 P 20,000 *P100,000/6 x 3 years = P48,000 ***P90,000/6 x 3 years = P45,000

78. b Depreciation expense: (P50,000 - P40,000) / 10 years = P1,000 over depreciation79. b

**Non-controlling Interest in Net Income (NCINI) for 20x4 S Company’s net income of Subsidiary Company from its own operations (Reported net income of S Company) P2,000,000 Unrealized gain on sales of equipment (upstream sales) (P700,000 – P600,000) ( 100,000) Realized gain on sale of equipment (upstream sales) through depreciation (P100,000/10)

10,000

S Company’s realized net income from separate operations……… P1,910,000 Less: Amortization of allocated excess _ 0

Non-controlling Interest in Net Income (NCINI) – full goodwill . . . . . . . . . . . . . P 764,000

80. a**Non-controlling Interest in Net Income (NCINI) for 20y2 S Company’s net income of Subsidiary Company from its own operations (Reported net income of S Company) P 135,000 Unrealized gain on sale of equipment (downstream sales) Realized gain on sale of equipment (downstream sales) through depreciation ( 0) S Company’s realized net income from separate operations……… P 135,000 Less: Amortization of allocated excess 0

P 135,000 Multiplied by: Non-controlling interest %.......... 20% Non-controlling Interest in Net Income (NCINI) - partial goodwill P 27,000 Less: NCI on goodwill impairment loss on full-goodwill . . . . . . . . . . . . . . . . . . . . . 0 Non-controlling Interest in Net Income (NCINI) – full goodwill . . . . . . . . . . . . . P 27,000

81. aConsolidated Net Income for 20y2 P Company’s net income from own/separate operations…………. P 200,800 Realized gain on sale of equipment (downstream sales) through depreciation

_ 8,000

P Company’s realized net income from separate operations*…….….. P 208,800 S Company’s net income from own operations…………………………………. P 135,000 Unrealized gain on sale of equipment (upstream sales) Realized gain on sale of equipment (upstream sales) through depreciation ( 0) S Company’s realized net income from separate operations*…….….. P 135,000 135,000 Total P343,800 Less: Amortization of allocated excess…………………… 0 Consolidated Net Income for 20y2 P343,800 Less: Non-controlling Interest in Net Income* *(refer to No. 80) 27,000 Controlling Interest in Consolidated Net Income or Profit attributable to equity holders of parent – 20y2………….. P316,800

*that has been realized in transactions with third parties. Net income from own operations:

Prout SextonSales P1,475,00

0P1,110,000

Less: Cost of goods sold 942,000 795,000 Other expenses (including depreciation) 145,000 90,000 Income tax expense __187,200 ____90,000Net income from own operations P

200,800P 135,000

Add: Dividend income ____80,000

Net income P 280,800

P 135,000

Sexton, 1/1/20y1Selling price P360,000Less: Book value, 1/1/20y1 Cost, 1/1/20x1 P400,000 Less: Accumulated depreciation : P400,000/25 years x 10 years

160,000 240,000

Unrealized gain on sale of equipment P120,000Realized gain – depreciation: P120,000/15 years P 8,000

Or, alternativelyConsolidated Net Income for 20y2 P Company’s net income from own/separate operations…………. P 200,800 Realized gain on sale of equipment (downstream sales) through depreciation

_ 8,000

P Company’s realized net income from separate operations*…….….. P 208,800 S Company’s net income from own operations…………………………………. P 135,000 Unrealized gain on sale of equipment (upstream sales) Realized gain on sale of equipment (upstream sales) through depreciation ( 0) S Company’s realized net income from separate operations*…….….. P 135,000 135,000 Total P343,800 Less: Non-controlling Interest in Net Income* * (refer to No. 80) P 27,000 Amortization of allocated excess…………………… ____0 27,000 Controlling Interest in Consolidated Net Income or Profit attributable to equity holders of parent………….. P316,800 Add: Non-controlling Interest in Net Income (NCINI) _ _27,000 Consolidated Net Income for 20y2 P343,800

*that has been realized in transactions with third parties.

82. a – refer to No. 8183. c

Consolidated Retained Earnings, December 31, 20y2 Retained earnings - Parent Company, January 1, 20y1 (cost model) P1,300,000 Less: Downstream - net unrealized gain on sale of equipment – prior to 20y1 [P120,000 – (P8,000 x 1 year)]

112,000

Adjusted Retained Earnings – Parent 1/1/20y1 (cost model ) Son Company’s Retained earnings that have been realized in transactions with third parties..

P1,188,000

Adjustment to convert from cost model to equity method for purposes of consolidation or to establish reciprocity:/Parent’s share in adjusted net increased in subsidiary’s retained earnings: Retained earnings – Subsidiary, January 1, 20x9 P 800,000 Less: Retained earnings – Subsidiary, January 1, 20y1 1,040,000 Increase in retained earnings since date of acquisition P 240,000 Less: Amortization of allocated excess – 20x9 to – 20y0 0 Upstream - net unrealized gain on sale of equipment –prior to 20y1

0

P 240,000 Multiplied by: Controlling interests %................... 80%

P192,000

Less: Goodwill impairment loss 0 _192,000 Consolidated Retained earnings, January 1, 20x5 P1,380,000 Add: Controlling Interest in Consolidated Net Income or Profit attributable to equity holders of parent for 20x5

316,800

Total P1,696,800 Less: Dividends declared – Parent Company for 20y1 120,000 Consolidated Retained Earnings, December 31, 20y1 P1,576,800

0

Or, alternatively:Consolidated Retained Earnings, December 31, 20y2 Retained earnings - Parent Company, December 31, 20y1 (cost model) (P1,300,000 + P280,800 – P120,000) P1,460,800 Less: Downstream - net unrealized gain on sale of equipment – prior to 12/31/20y1 [P120,000 – (P8,000 x 2 years)] 104,000 Adjusted Retained Earnings – Parent 12/31/20x5 (cost model ) S Company’s Retained earnings that have been realized in transactions with third parties.. P1,356,800 Adjustment to convert from cost model to equity method for purposes of consolidation or to establish reciprocity:/Parent’s share in adjusted net increased in subsidiary’s retained earnings: Retained earnings – Subsidiary, December 31, 20y2 (P1,040,000 + P135,000 – P100,000) P

1,075,000 Less: Retained earnings – Subsidiary, January 1, 20x9 800,000 Increase in retained earnings since date of acquisition P

275,000 Less: Accumulated amortization of allocated excess 0 Upstream - net unrealized gain on sale of equipment – prior to 12/31/20y2

_______0

P 275,000 Multiplied by: Controlling interests %................... 80% P 220,000 Less: Goodwill impairment loss _____0 220,000 Consolidated Retained earnings, December 31, 20y2 P1,576,800

84. c Non-controlling interest (fulll-goodwill), December 31, 20y2 Common stock – Subsidiary Company, December 31, 20y2…… P

1,200,000 Retained earnings – Subsidiary Company, December 31, 20y2 Retained earnings – Subsidiary Company, January 1, 20y2 P1,040,0

00 Add: Net income of subsidiary for 20y2 135,00

0 Total P1,175,0

00 Less: Dividends paid – 20y2 100,00

0 1,075,00

0 Stockholders’ equity – Subsidiary Company, December 31, 20x5 P

2,275,200 Adjustments to reflect fair value - (over) undervaluation of assets and liabilities, date of acquisition (January 1, 20x4) 0 Amortization of allocated excess (refer to amortization above) : 0 Fair value of stockholders’ equity of subsidiary, December 31, 20x5…… P2,275,200 Less: Upstream - net unrealized gain on sale of equipment – prior to 12/31/20y2

_____)0

Realized stockholders’ equity of subsidiary, December 31, 20x5………. P 2,275,00 Multiplied by: Non-controlling Interest percentage…………... _ 20 Non-controlling interest (partial goodwill)………………………………….. P 455,000

85. cProut Sexton Consolidated

Selling price P P300,000 P 300,000

360,000Less: Book value : Cost P

400,000P360,000 P 240,000

Accumulated

*160,000 __240,000

**48,000 312,000

***32,000 _208,000

Unrealized gain on sale of Equipment, 1/1/20y1 P

120,000Realized Gain – depreciation (P120,000/15 x 2 yrs) __16,000Net unrealized gain, 1/1/20y3 P

104,000__________ _________

Gain on sale P 104,000

P( 12,000)

P 92,000

*P400,000/25 x 10 years = P160,000 **P360,000/15 x 2 years = P48,000 ***P240,000/15 x 2years = P400,000

86. b – refer to No. 85 87. a – refer to No. 85Analysis: Workpaper entries (not required)Intercompany Sale of Equipment

Accumulated RemainingCost Depreciation Carrying Value Life Depreciation

Original Cost P400,000 P160,000 P240,000 15 yr P 16,000Intercompany Selling Price 360,000 _______ 360,000 15 yr 24,000Difference P 40,000 P160,000 P120,000 P 8,000

(1) Investment in Sexton Company 192,000

Retained Earnings - Prout 192,000To establish reciprocity/convert to equity (.80 x (P1,040,000 - P800,000))

Accumulated Depreciation 160,000To reduce beginning consolidated retained earnings by amount of unrealized profit at the beginning of the year, to restate property and equipment to its book value to Prout Company on the date of the intercompany sale.

Investment in Sexton Company (P1,600,000 + P192,000) 1,792,000Noncontrolling Interest [P400,000 + (P1,040,000 - P800,000) x .20] 448,000

To eliminate investment account and create noncontrolling interest account

Entry analysis: Journal Entry on the books of Sexton to record the sale

Cash 300,000Accumulated Depreciation - Fixed Assets (P360,000/15) x 2 years) 48,000Loss on Sale of Equipment 12,000

Plant and Equipment 360,000

Workpaper eliminating entry on December 31, 20y3 consolidated statement necessary to prepare consolidated statements:

Beginning Retained Earnings – Prout(P120,000 - P16,000) 104,000Loss on Sale of Equipment 12,000

Gain on Sale of Equipment 92,000

Cost to the Affiliated Companies P400,000Accumulated Depreciation Based on Original Cost ((12/25)x P400,000) 192,000Book Value, 1/1/y3 P 208,000Proceeds from Sale to Non-affiliate (300,000)Gain from consolidated point of view P 92,000

Note: As of Dec. 31, 20y3, the amount of profit recorded by the affiliates on their books (P120,000 - P12,000 = P108,000) is equal to the amount of profit considered realized in the consolidated financial statements (P8,000 + P8,000 + P92,000) = P108,000.

88. d - Investment in subsidiary, 12/31/20x5 (cost model) P700,000). Date of Acquisition (1/1/20x4) Partial Full Fair value of consideration given…………………….P 700,000 Less: Book value of SHE - Subsidiary): (P300,000 + P500,000) x 80%........................... 640,000 Allocated Excess.………………………………………….P 60,000 Less: Over/Undervaluation of Assets & Liabilities Increase in Bldg. (P75,000 x 80%)……………… 60,000 Goodwill ………….………………………………………….P 0 P 0 Amortization of allocated excess: building - P75,000 / 25 years = P3,000 Upstream Sale of Equipment (date of sale – 4/1/20x5):

Sales.......................................................................................................P 60,000Less: Book value of equipment……………………………………………………………….

30,000Unrealized Gain (on sale of equipment)……………………………………………………P

30,000

Realized gain on sale of equipment: 20x5: P30,000/5 years = P6,000 x 9/12 (4/1/20x5-12/31/20x5)…………………………. .P 4,500

20x6 ………………..……………………………………………………………………………P 6,000 Downstream Sale of Machinery (date of sale – 9/30/20x5):

89. d Dividend paid or declared – S…………………………………………………P 50,000x: Controlling Interest %…………………………………………………………. 80%Dividend income of Parent……………………………………………………..P 40,000

90. dConsolidated Net Income for 20x5 P Company’s net income from own/separate operations…………. P 300,000 Net unrealized gain on sale of equipment (downstream sales) through depreciation P35,000 – P875) 34,125 P Company’s realized net income from separate operations*…….….. P 265,875 S Company’s net income from own operations…………………………………. P 150,000 Unrealized gain on sales of equipment (upstream sales) (30,000) Realized gain on sale of equipment (upstream sales) through depreciation 4,500 S Company’s realized net income from separate operations*…….….. P 124,500 124,500 Total P390,375 Less: Amortization of allocated excess…………………… 3,000 Consolidated Net Income for 20x5 P387,375 Less: Non-controlling Interest in Net Income* * 24,300 Controlling Interest in Consolidated Net Income or Profit attributable to equity holders of parent – 20x5………….. P363,075

*that has been realized in transactions with third parties.

Or, alternativelyConsolidated Net Income for 20x5 P Company’s net income from own/separate operations…………. P 300,000 Net unrealized gain on sale of equipment (downstream sales) through depreciation P35,000 – P875) 34,125 P Company’s realized net income from separate operations*…….….. P 265,875 S Company’s net income from own operations…………………………………. P 150,000 Unrealized gain on sales of equipment (upstream sales) (30,000) Realized gain on sale of equipment (upstream sales) through depreciation 4,500 S Company’s realized net income from separate operations*…….….. P 124,500 124,500 Total P390,375 Less: Non-controlling Interest in Net Income* * P 24,300 Amortization of allocated excess…………………… 3,000 27,300 Controlling Interest in Consolidated Net Income or Profit attributable to equity holders of parent………….. P363,075 Add: Non-controlling Interest in Net Income (NCINI) _ 24,300 Consolidated Net Income for 20x5 P387,375

*that has been realized in transactions with third parties.

**Non-controlling Interest in Net Income (NCINI) for 20x5 S Company’s net income of Subsidiary Company from its own operations (Reported net income of S Company)

P 150,000

Unrealized gain on sales of equipment (upstream sales) ( 30,000) Realized gain on sale of equipment (upstream sales) through depreciation 4,500 S Company’s realized net income from separate operations……… P 124,500 Less: Amortization of allocated excess 3,000

P 121,500 Multiplied by: Non-controlling interest %.......... 20% Non-controlling Interest in Net Income (NCINI) - partial goodwill P 24,300 Less: NCI on goodwill impairment loss on full-goodwill . . . . . . . . . . . . . . . . . . . . . 0 Non-controlling Interest in Net Income (NCINI) – full goodwill . . . . . . . . . . . . . P 24,300

91. c – refer to No. 90 for computations 92. d – refer to No. 90 for computations 93. a

Non-controlling Interests (in net assets): 20x5 20x6 Common stock - S, 12/31..….………………………… P 300,000 P 300,000 Retained earnings - S, 12/31: RE- S, 1/1.…………………………………………….P600,000 P 700,000 +: NI-S………………………………………………… 150,000 200,000

-: Div – S…………………………………………….. 50,000 700,000 70,000 830,000 Book value of Stockholders’ equity, 12/31…….... P1,000,000 P1,130,000 Adjustments to reflect fair value of net assets

Increase in equipment, 1/1/2010..……..… 75,000 75,000 Accumulated amortization (P3,000 per year)*.…… ( 6,000) ( 9,000)

Fair Value of Net Assets/SHE, 12/31..……………… P1,069,000 P1,196,000 Unrealized gain on sale of equipment (upstream) ( 30,000) **( 25,500) Realized gain thru depreciation (upstream)……… 4,500 6,000 Realized SHE – S,12/31………………………………….. P1,043,500 P1,176,500 x: NCI %........................................................... ………… ___ 20% 20%

Non-controlling Interest (in net assets) – partial... P 208,700 P 235,300 +: NCI on full goodwill……..…………………………….. 0 0 Non-controlling Interest (in net assets) – full…….. P 208,700 P 235,300

* 20x5: P3,000 x 2 years; 2012: P3,000 x 3 years; ** P30,000 – P4,500 realized gain in 20x5 = P25,500.

Note: Preferred solution - since what is given is the RE – P, 1/1/20x5(beginning balance of the current year) -

Retained earnings – Parent, 1/1/20x5 (cost)…………………………… P 800,000 -: Downstream sale – 20x4 or prior to 20x5, Net unrealized gain 0 Adjusted Retained earnings – Parent, 1/1/20x5 (cost)……………… P 800,000 Retroactive Adjustments to convert Cost to “Equity”:

Retained earnings – Subsidiary, 1/1/20x4……………………….P 500,000 Less: Retained earnings – Subsidiary, 1/1/20x5……………….. 600,000 Increase in Retained earnings since acquisition

(cumulative net income – cumulative dividends)…………P 100,000 Accum. amortization (1/1/x4– 1/1/x5): P2,000 x 1 year…….. ( 3,000) Upstream Sale – 2010 or prior to 20x5, Net unrealized gain……………………………..……………….( 0)

P 97,000 X: Controlling Interests %..…………………………………………… 80% 77,600 RE – P, 1/1/20x5 (equity method) = CRE, 1/1/20x5………………… P 877,600 +: CI – CNI or Profit Attributable to Equity Holders of Parent……. 363,075 -: Dividends – P………………………………………………………………….. 100,000 RE – P, 12/31/20x5 (equity method) = CRE, 12/31/20x5………….. P 1,140,675

Or, if RE – P is not given on January 1, 20x5, then RE – P on December 31, 20x5 should be use.

Retained earnings – Parent, 12/31/20x5 (cost model): (P800,000 + P340,000, P’s reported NI – P100,000)……………… P1,040,000 -: Downstream sale – 20x5 or prior to 12/31/20x5, Net unrealized gain - (P35,000 – P875)……………………………. 34,125 Adjusted Retained earnings – Parent, 1/1/20x5 (cost model)..…… P1,005,875 Retroactive Adjustments to convert Cost to “Equity”:

(P600,000 + P150,000 – P50,000)..…………..……………. 700,000 Increase in Retained earnings since acquisition

(cumulative net income – cumulative dividends)……. ….P 200,000 Accumulated amortization (1/1/20x4 – 12/31/20x5): P 3,000 x 2 years……………………………………………. .( 6,000) Upstream Sale – 20x5 or prior to 12/31/20x5, Net unrealized gain – (P30,000 – P4,500)……………. ( 25,500)

P 168,500 x: Controlling Interests %..………………………………………… 80% 134,800 RE – P, 12/31/20x5 (equity method) = CRE, 12/31/20x5…………. P1,140,675

94. c – refer to No, 93 computations. 95. b – refer to No. 93 for computations 96. d – refer to No. 93 for computations

97. b Consolidated Stockholders’ Equity, 12/31/20x5:

98. d – the original cost of land99. b – no intercompany gain or loss be presented in the CFS.100. a

Consolidated Net Income for 20x4 P Company’s net income from own/separate operations…………. P 200,000 Realized gain on sale of equipment (downstream sales) through depreciation

___0

P Company’s realized net income from separate operations*…….….. P 200,000 S3 Company’s net income from own operations…………………………………. P100,000 S2 Company’s net income from own operations…………………………………. 70,000 S1 Company’s net income from own operations…………………………………. 95,000 Unrealized loss on sale of equipment (upstream sales) – S3 15,000 Unrealized gain on sale of equipment (upstream sales) – S2 ( 52,000) Unrealized gain on sale of equipment (upstream sales) - S1 ( 23,000) S Company’s realized net income from separate operations*…….….. P205,000 205,000 Total P405,000 Less: Amortization of allocated excess…………………… 0 Consolidated Net Income for 20x4 P405,000 Less: Non-controlling Interest in Net Income* * (P23,000 + P5,400 + P7,200)

35,600

Controlling Interest in Consolidated Net Income or Profit attributable to equity holders of parent – 20x4………….. P369,400

*that has been realized in transactions with third parties.

Or, alternativelyConsolidated Net Income for 20x4 P Company’s net income from own/separate operations…………. P 200,000 Realized gain on sale of equipment (downstream sales) through depreciation

___0

P Company’s realized net income from separate operations*…….….. P 200,000 S3 Company’s net income from own operations…………………………………. P100,000 S2 Company’s net income from own operations…………………………………. 70,000 S1 Company’s net income from own operations…………………………………. 95,000 Unrealized loss on sale of equipment (upstream sales) – S3 15,000 Unrealized gain on sale of equipment (upstream sales) – S2 ( 52,000) Unrealized gain on sale of equipment (upstream sales) - S1 ( 23,000) S Company’s realized net income from separate operations* P205,000 205,000 Total P405,000 Less: Non-controlling Interest in Net Income* * (P23,000 + P5,400 + P7,200)

P 35,600

Amortization of allocated excess…………………… ____0 _ 35,600 Controlling Interest in Consolidated Net Income or Profit attributable to equity holders of parent………….. P369,400 Add: Non-controlling Interest in Net Income (NCINI) _ _35,600 Consolidated Net Income for 20y0 P405,000

*that has been realized in transactions with third parties.

**Non-controlling Interest in Net Income (NCINI) S3 S2 S1 S Company’s net income of Subsidiary Company from its own operations (Reported net income of S Company) P 100,000 P 70,000 P 95,000 Unrealized (gain) loss on sale of land (upstream sales) 15,000 ( 52,000) ( 23,000)

S Company’s realized net income from separate operations P 115,000 P 18,000 P 72,000 Less: Amortization of allocated excess 0 0 0

P 115000 P 18,000

P 72,000

Multiplied by: Non-controlling interest %.......... 20% 30% 10% Non-controlling Interest in Net Income (NCINI) - partial goodwill

P 23,000 P 5,400 P 7,200

Less: NCI on goodwill impairment loss on full-goodwill 0 0 0 Non-controlling Interest in Net Income (NCINI) – full goodwill P 23,000 P 5,400 P 7,200

101. b Non-controlling Interest in Net Income (NCINI) for 20y2 S Company’s net income of Subsidiary Company from its own operations (Reported net income of S Company) P 40,000 Unrealized gain on sales of equipment (upstream sales) – year of sale - Realized gain on sale of equipment (upstream sales) through depreciation (P14,500 – P9,000) / 5 years 1,100 S Company’s realized net income from separate operations……… P 41,100 Less: Amortization of allocated excess 0

P 41,100 Multiplied by: Non-controlling interest %.......... 20% Non-controlling Interest in Net Income (NCINI) - partial goodwill P 8,220 Less: NCI on goodwill impairment loss on full-goodwill . . . . . . . . . . . . . . . . . . . . . 0 Non-controlling Interest in Net Income (NCINI) – full goodwill . . . . . . . . . . . . . P 8,220

102. d – the unrealized gain amounted to P15,000 (P60,000 – P45,000). It should be noted that PAS 27 allow the use of cost model in accounting for

investment in subsidiary in the books of parent company but not the equity method. Since, the cost model is presumed to be the method used, the unrealized gain of P15,000 (P60,000 – P45,000) will not be recorded in the books of parent company, which give rise to no equity-adjustments at year-end.

103. c Cliff reported income P225,000Less: Intercompany gain on truck 45,000Plus: Piecemeal recognition of gain = P45,000/10 years ___4,500Cliff’s adjusted income P184,500Majority percentage 90%Income from Cliff P166,050

104. c

Pied Imperial-Pigeon’s share of Roger’s income = (P320,000 x 90%) =

P288,000

Less: Profit on intercompany sale (P130,000 - P80,000) x 90% = 45,000Add: Piecemeal recognition of deferred profit ($50,000/4 years)90% =

11,250

Income from Offshore P254,250

105 c P30,000 - (1/4 x P30,000) = P

22,500

106. d - P60,000 – P48,000)/4 years = P3,000 107. a Simon, 4/1/20x4

Selling price P68,250Less: Book value, 4/1/20x4 Cost, 1/1/20x4 P50,000 Less: Accumulated depreciation : P50,000/10 years x 3/12 __1,250 48,750

Unrealized gain on sale of equipment P19,500Realized gain – depreciation: P19,500/9.75 years P 2,000

108. c – P2,000 x 9/12 (April 1, 20x4 – December 31, 20x4) = P1,500109. c – P19,500 / 9.75 years = P2,000110. c – P19,500 / 9.75 years = P2,000111. d

20x4Share in subsidiary net income (100,000 x 90%) 90,000Unrealized gain on sale of equipment (downstream sales) ( 19,500)Realized gain on sale of equipment (downstream sales) through depreciation P2,000 x 9/12 (April 1, 20x4 – December 31, 20x4) = P1,500 _ 1,500Net 72,000

112. b 20x5

Share in subsidiary net income (120,000 x 90%) 108,000Realized gain on sale of equipment (downstream sales) through depreciation _ 2,000Net 110,000

113. d 20x6Share in subsidiary net income (130,000 x 90%) 117,000Realized gain on sale of equipment (downstream sales) through depreciation _ 2,000Net 119,000

114. c Smeder, 1/1/20x4

Selling price P84,000Less: Book value, 1/1/20x4 Cost, 1/1/20x4 P120,000 Less: Accumulated depreciation __48,000 72,000Unrealized gain on sale of equipment P12,000Realized gain – depreciation: P12,000/6 years P 2,000

115. b 20x4

Share in subsidiary net income (28,000 x 80%) 22,400Unrealized gain on sale of equipment (upstream sales); 12,000 x 80% ( 9,600)Realized gain on sale of equipment (upstream sales) through depreciation P2,000 x 80% _ 1,600Net 14,400

116. c 20x5

Share in subsidiary net income (32,000 x 80%) 25,600Realized gain on sale of equipment (upstream sales) through depreciation P2,000 x 80% _ 1,600Net 27,200

117. d Eliminating entries: 1/1/20x4: date of acquisition Restoration of BV and eliminate unrealized gain

Smeder, 1/1/20x4Selling price P84,000Less: Book value, 1/1/20x4 Cost, 1/1/20x4 P120,000 Less: Accumulated depreciation __48,000 72,000Unrealized gain on sale of equipment P12,000Realized gain – depreciation: P12,000/6 years P 2,000

Eliminating entries: 12/31/20x4: subsequent to date of acquisition Realized Gain – depreciation

Accumulated depreciation 2,000 Depreciation expense 2,000 P12,000 / 6 years or P14,000 – P12,000

“Should be in CFS” Parent – Smeder “Recorded as” Subsidiary - CollinsDepreciation expense (P72,000 /6 years) 12,000

Depreciation expense (P84,000 / 6 years) 14,000

Acc. Depreciation 12,000 Acc. depreciation 14,000

Combining the eliminating entries for 1/1/20x4 and 12/31/200x4, the net effect of accumulated depreciation would be a net credit of P46,000 (P48,000 – P2,000).

118. c20x4

Unrealized gain on sale of equipment ( 12,000)

Realized gain on sale of equipment through depreciation ___2,000Net ( 10,000)

119. d Eliminating entries: 5/1/20x4: date of acquisition Restoration of BV and eliminate unrealized gain

Cash 5,000 Loss 5,000

Parent – Stark Subsidiary - ParkerCash 80,000 Land 85,000Loss 5,000 Cash 85,000 Land 85,000

Stark Parker ConsolidatedSelling price P 80,000 P 92,000 P 92,000Less: Book value, 5/1/20x4 _85,000 __80,000 _85,000Unrealized gain on sale of equipment P ( 5,000) P 12,000 P 7,000

120. b – refer to No. 119 for eliminating entry

121. bCash 5,000

Retained earnings 5,000

122. e 20x4

Share in subsidiary net income (200,000 x 90%) 180,000Unrealized loss on sale of land (upstream sales): P5,000 x 90% _ 4,500Net 184,500

123. d 20x4

Share in subsidiary net income (200,000 x 90%) 180,000Unrealized loss on sale of land (upstream sales): P5,000 x 90% _ 4,500Net 184,500

124. bStark Parker Consolidated

Selling price P 80,000 P 92,000 P 92,000Less: Book value, 5/1/20x4 _85,000 __80,000 _85,000Unrealized gain on sale of equipment P ( 5,000) P

12,000P 7,000

125. a – refer to No. 124 for computation126. e – None, the loss was already recognized in the books of Stark in the year of sale -

20x4 but not in the subsequent years.127. c

20x6Share in subsidiary net income (220,000 x 90%) 198,000Intercompany realized loss on sale of land (upstream sales): P5,000 x 90% _ ( 4,500)Net 193,500