1 Why does a firm disclose its pursuit ofstrategic alternatives? Michael Dambra 1 Decembe r 15, 2010 AbstractThis paper develops an empirical model to determine what influences a firm to publicly disclose its pursuit of strate gic alternative s (referred to as a strategic disclosure ). I find that disruption costs, negative earnings, shareholder activity, and abnormally low trading volume all affect the decis ion to s trategically disclose. These results are not only statistically significant, but highly econ omically s ignificant. After a blockholder purchase (quarterly loss) there is a10.7% (18.8%) higher probability of announcing a strategic disclosure. The market finds strate gic disclosures informative. Strategic disclosures provide a positi ve abnormal return of 7.2%. Firms that strategic ally disclose solicit more bids than firms tha tdo not. I find no difference in merger premiums give n manage ments pree mptive disclosure decision. 1 William E. Simon Graduate School of Business, Universit y of Rochester. Many thanks to Matthew Gustafson, Ivan Ivanov, Edward Li, Ed Owens, and Jerry Zimmerman for helpful advice, comments, and suggestions.

Transcript

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 1/42

1

Why does a firm disclose its pursuit of

strategic alternatives?

Michael Dambra1

December 15, 2010

Abstract

This paper develops an empirical model to determine what influences a firm to publicly

disclose its pursuit of strategic alternatives (referred to as a strategic disclosure). I find

that disruption costs, negative earnings, shareholder activity, and abnormally low trading

volume all affect the decision to strategically disclose. These results are not onlystatistically significant, but highly economically significant. After a blockholder purchase

(quarterly loss) there is a 10.7% (18.8%) higher probability of announcing a strategic disclosure.

The market finds strategic disclosures informative. Strategic disclosures provide a positive

abnormal return of 7.2%. Firms that strategically disclose solicit more bids than firms that

do not. I find no difference in merger premiums given managements preemptive

disclosure decision.

1 William E. Simon Graduate School of Business, University of Rochester. Many thanks to Matthew Gustafson,Ivan Ivanov, Edward Li, Ed Owens, and Jerry Zimmerman for helpful advice, comments, and suggestions.

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 2/42

2

1.0 Introduction

Firms are usually silent in terms of strategy related disclosures prior to a merger

announcement. Announcing negotiations of intent to sell disrupts the normal operations of a

company.

The buyer and target abhor premature disclosure. If the deal does not happen, there is egg on everyones face

anddamage may have been done to employee, supplier, and customer relationships (Miller 2008).

Employees would be concerned about job security, customers may fear disruption of a suppliers

service or goods delivery, and shareholders will be upset if premature disclosure occurs and no

acquisition happens. I find that approximately 13% of acquired firms either: disclose intentions to

pursue strategic alternatives, disclose they are in negotiations with potential bidders, or announce

the retention of an investment banker prior to a public announcement of a merger (hereafter jointly

referred to as strategic disclosures). This paper first investigates the determinants of a firm's

decision to disclose managements strategy prematurely. I find evidence that labor intensity, high

demand for management strategy, and market uncertainty formulate managements decision to

strategically disclose. Next, I explore the market reaction to the disclosure and the effect the

disclosure has on the negotiation process and the final premium paid by the bidder. Consistent

with Woolridge and Snow (1990) there is a favorable stock market reaction to strategic disclosures.

The average market adjusted return of a strategic disclosure is 7.2%. When strategic alternatives

are publicly disclosed there are more bidders prior to and following the merger announcement.

However, I find no evidence that strategic disclosures affect the total premium paid for the target

firm, consistent with Schwert (1996) and Heitzman and Klasa (2010).

Target firm behavior in a corporate control contest is an often studied area in empirical

finance and accounting research (see Betton et. al [2008] for a comprehensive literature review).

There is a tradeoff between the informativeness of conversations between target firms and suitors

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 3/42

3

to stakeholders and the benefit of private negotiations that do not disrupt ongoing operations.

Tradeoffs also exist for management publicly disclosing internal strategies. These disclosures are

informative to stakeholders, but firms incur proprietary costs from competitors learning

managements private information and can also unnerve a firms supply chain and employees.

Strategic disclosure could be useful for identifying potential suitors. Hence informational

asymmetry will be reduced by revealing managements private information. Of course, to provide

proper duty of care, managers will retain an investment banker to oversee the selling process.

Relying on the investment banker alone will provide a cap to the number of potential strategic

partners the firm would contact. As a complementary effect, strategic disclosure will inform the

entire market, along with potential suitors the investment banker identifies, managements

intentions.

This study also considers the legal ramifications of pre-acquisition disclosure. Security

exchanges may force publicly traded firms to disclose the origin of the unusual trading activity, if

known. The SEC does permit non-disclosure of negotiations between target and bidder firms

before the offer announcement. This is the typical approach for firms that are acquisition targets.

The SEC allows non-disclosure of a material event because public announcement of the negotiation

between target firms and bidder firms could prevent the deal from being completed. If a firm

publicly announced its decision to solicit merger partners or pursue strategic alternatives, then it

considered the information tradeoff ex ante.

This study contributes to the literature in several ways. To my knowledge it is the first

paper to attempt to model the strategic alternative disclosure decision. The paper combines the

theoretical voluntary disclosure literature, practitioner literature, and legal literature into a testable

empirical setting. Previous studies (Gupta and Misra [1989], Schwert [1996], and Heitzman and

Klasa [2010], among others) have either grouped strategic disclosures, gossip, and Form 13D filings

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 4/42

4

into an explanatory variable and identified the timing effects of the runup or the effect news has on

the premium to the target firm without considering the determinants of the firms decision. A

firms decision to strategically disclose can be considered an empirical proxy for whether a firm

undergoes a private sale versus a public auction, rather than partitioning the number of bidders for

a target firm. This study also adds to the intersection of the merger and voluntary disclosure

research, which is detailed below.

2.0 Existing Literature

2.1 Disclosure and Merger Literature: Healy and Palepu (2001) note that two motivations

for managers disclosure decisions are capital market transactions and the market for corporate

control. In both of these areas, informational asymmetry between a target firm and the overall

market can cause severe issues. Previous theory has shown that voluntary disclosure can have a

significant beneficial impact on a stocks liquidity, which lowers cost of capital (Diamond and

Verrecchia 1991). High stock return volatility, as a proxy for informational asymmetry, is

undesirable for firms. It can increase their riskiness (Froot and Stein [1992]), stock-based

compensation can be more costly (Jorgensen [1998]), and there is an increase in the likelihood of a

lawsuit following a large stock decline (Francis et. al [1994]).

A detriment to voluntary disclosure prior to a merger is that proprietary costs are incurred

(for example, Verrecchia [1983], Wagenhoufer [1990]). In more competitive industries the outside

options of target company executives are more homogeneous, which allows for an easier transition

to competing companies. The ability to retain key employees is a critical issue post-acquisition

(Hartzell et. al [2004]), Krug [2009], Martin and McConnell [1991]). Key employees may begin

their job search earlier after public acknowledgement of the pursuit of strategic alternatives. Also,

where products are similar, skittish customers can more easily migrate to competing products.

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 5/42

5

The negotiation process between target companies and potential bidders prior to the

merger announcement has been an area of increasing empirical research interest (Boone and

Mulherin [2007], Heitzman [2010]). Boone and Mulherin (2007, 2009) provide an analysis of the

best way to sell a company, via a private or public sale. They note that common sense suggests that

all sellers should implement a wide ranging auction; however information costs can severely limit

the benefits of an auction. Hence, the negotiation choice made (public vs. private) was optimal for

each individual firm. The decision to disclose strategically is comparable to the auction versus

private negotiation choice.

Previous research has shown that rumors (Jarrell and Poulsen [1989]), toeholds (Walking

[1985]), and insider trading (Jarrell and Poulsen [1989], Heitzman and Klasa [2010]) have often

been cited as components of the runup (Schwert [1996]). Haw et. al (1990) find that market

runups occur earlier for owner controlled firms when Form 13D was filed or when rumors were

published in the financial press. Target firm disclosure can also contribute to the run-up. The

target company has the ability to preempt hostile offers or negotiation with friendly bidders with

strategic disclosures.

The firms decision to strategically disclose would take into consideration how various

stakeholders are affected. Bowen et. al (1995) argue that a firms financial image influences

stakeholders assessments of its ability to fulfill its implied commitments. If a companys ongoing

operations would be detrimentally affected by premature disclosure, such firms are more apt to

avoid strategic disclosures.

I study a particular intersection of mergers and acquisitions and voluntary disclosure. This

intersection has been studied in regards to management earnings forecasts (Bernille and Bauguess

[2010], Brennan [1999], Wandler [2007], Amel-Zadeh et. al [2008]) and conference calls around an

acquisition announcement (Kimbrough and Louis [2010]). From the bidders perspective, Ahern

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 6/42

6

and Sosyura (2010) find that bidder firms have increased media coverage concurrent with merger

negotiations. The increased media coverage was a proxy for opportunistic disclosure issued by the

bidder firm. There has also been event study analyses documenting the benefit of improved

mandatory disclosure regulation associated with merger negotiation (see Eckbo and Langohr

[1989]).

2.2 Legal Literature: A tension in this paper is whether strategic disclosure is actually

voluntary. Target managers are granted flexibility by the SEC in regards to the necessity of

strategic disclosure prior to a merger announcement. The SEC (1989) recognizes that firms have an

interest in preserving the confidentiality of negotiations and attempts to balance the informational

need of investors against the costs of premature disclosure. This is not all-inclusive. According to

Nusbuam and Young (1987) there are two types of disclosure requirements: express disclosure

reports, and current reports (i.e. material events) considered essential for investors to make

informed decisions. Express disclosure explicitly requires firms to publicly announce attempts to

acquire 51% of a firms stock via a tender offer and to disclose the merger negotiation ex post

within the proxy solicitation. In other reports, such as the 8-K or annual report, directors must not

deny that negotiations are occurring, because such denial is subject to litigation under the Williams

Act (Nusbuam and Young [1987]). Firms must either fully disclose or issue a no comment

disclosure2.

There are three situations where there is an implied duty for firms to disclose preliminary

merger or acquisition negotiations under the federal security law anti-fraud provisions: (1) to

prevent insider trading, (2) to quell merger or acquisition based rumors, or (3) to prevent then

dissemination of false and misleading corporate statements. If an insider, such as a CEO or board

2 In other words, a public announcement that the firm has no comment in regards to published rumors orunusual market activity.

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 7/42

7

member, is aware of ongoing negotiations and wanted to sell some his or her insider stock, then the

firm would be obliged to announce ongoing negotiations prior to the sale. In regards to rumors, the

company is only obligated to respond if the rumors of negotiations are attributable to the firm. The

security boards are more restrictive and these bodies hold full affirmative disclosure requirements.

The NYSE Manual (2010) states that if published rumors are false or inaccurate then they should be

promptly denied or clarified. If the rumors are true then management should issue an immediate

statement regarding the development of negotiations or corporate plans. A firm that refuses to do

so can be subject to exchange sanctions.

Disclosing that no merger negotiations are occurring when the opposite is true is

misleading. This is a deliberate denial disseminated to shareholders. In Levinson v. Basic, Inc.

directors denied that negotiations were taking place, when in fact they were, and a merger was

announced shortly thereafter. Former shareholders that sold shares prior to the merger

announcement sued and successfully won. Under rule 10b-5 shareholders can allege that directors

omitted or failed to disclose material information which caused them to suffer trading losses.

Hazen (1986) argues that due to Levinson v. Basic firms should either provide full disclosure of

ongoing negotiations or issue a no comment statement. Anything short of no comment or full

disclosure of the negotiations, no matter how preliminary, would increase uncertainty. This in turn

would be likely to mislead, add to rumors, and thus act against an informed and efficient market

(Nusbaum and Young [1987]).

A rumor can be attributed to management if unusual trading activity occurred around a

board meeting that the directors discussed exploring strategic alternatives or engaging an

investment banker. By studying the target firms information environment immediately prior to a

strategic disclosure, or upon board decisions authorizing the nonpublic pursuit of strategic

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 8/42

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 9/42

9

To develop a model for strategic disclosure disruption costs, extant information

environment, proprietary costs, legal ramifications, and preemptive strategies are considered in the

subsequent hypotheses. In the merger literature the negative stock performance puzzle post-

acquisition has been partially attributed to the brain drain, or poor retention of target employees

(Krug [2009)]. Strategic disclosures affect employees beliefs of his or her sustainability of

employment with the target firm. The practitioner literature posits that manager attention is

reduced when there is a public announcement of management intention. Managers are more

heavily involved in investor relations and a larger number of bidder meetings as compared to a

private negotiation strategy. Once a firm strategically discloses, stakeholders will demand updates

on the firms strategic alternative process, which will require additional management attention.

Given this, firms that are more sensitive to management/employee disruption are less likely

to strategically disclose (H1).

The shareholder base reacts more negatively to poor performance, which increases the

pressure on CEOs (Martin and McConnell [1991]). The primary purpose of disclosure is to satisfy

the information demand from stakeholders. Rogers and Van Buskirk (2009) note information

demand is higher subsequent to a firm reporting a loss. Strategic disclosure is more likely

subsequent to the firm reporting a loss (H2). If shareholders file Form 13D, then they have an

active interest 3 in altering firm strategy whether it is to elect board members or induce

management to consider strategic alternatives. Mohan (2006) finds that monitoring by

institutional investors appears to induce better corporate disclosure. Bushee and Noe (2000) find

that firms with increases in transient ownership (i.e. aggressive traders) have associated

improvements to disclosure quality. Hence, firms with a more active shareholder base are

more likely to strategically disclose (H3).

3 If a blockholder is more interested in passive investment, according to SEC regulations, they should submit Form 14D, rather than 13D.

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 10/42

10

In highly competitive industries companies are more homogeneous. Dissatisfied

employees, customers, and suppliers would incur less switching costs in transferring their services,

demands, or products to an industry peer. Firms with higher proprietary costs are less likely to

strategically disclose (H4).

Less informed shareholders have been shown empirically to demand more information

(Kim [1993]). Via adverse selection theories, if insiders have more complete information than

outsiders than there will be disperse opinions of the true value of a subject companys expected

discounted future cash flows. This can be damaging to target shareholders given the uncertainty of

the realization of a merger premium ex ante. Firms that have higher levels of informational

asymmetry are more likely to publicly announce strategic disclosures (H5a). The extant

voluntary disclosure literature indicates that subsequent to disclosure, informational asymmetry or

uncertainty decreases (Rogers [2008] among others). In contrast, this may not hold subsequent to

a strategic disclosure. Although shareholders are more informed there may be higher dispersion

among analysts, shareholders, and traders in regards to the market value of the announcing firm.

The probability of mergers, potential bidders, synergy estimates, or other strategic options has to

be incorporated into the firms stock price.

It could also be the case that a strategic disclosure is not voluntary. An alternative

argument is security exchanges or the companys legal counsel have identified a high level of

trading volume or stock volatility in recent days and advised the firm to consider providing private

information to the market. Although the legal literature specifically stresses that this requirement

adheres to merger negotiations it can be logically extended to consider strategic alternatives. This

is especially true if market activity occurs more frequently around a firm initiated event (Heitzman

and Klasa [2010]). Hence, firms with abnormally high market activity are more likely to

publicly announce strategic disclosures (H5b).

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 11/42

11

4 .0 Data

To identify determinants of strategic disclosure, I require an environment where data is

available for both firms that publicly announced strategic disclosures and firms that kept their

strategic decision process private. This constrains the ability to conduct such a test since most

firms are not obligated to disclose their decision to pursue strategic alternatives. However, the SEC

does require firms to disclose negotiation events leading up to a merger ex post in the merger filings

by the acquirer or target firm. Applying my empirical research question in a merger setting allows

for both a subset of firms that announced their intentions and firms that have decided via a board

meeting to privately entertain strategic alternatives (either implicitly or explicitly). The alternative

approach is to employ a text based EDGAR search identifying firms that announced strategic

disclosures. These firms would then be compared to peer performance-matched companies that

are predicted to be contemplating a similar approach privately. The merger setting was

determined to provide a better comparative sample. A disadvantage is that there is no certainty

that this research environment is generalizable to all firms. In other words, firms that strategically

disclose and later announce a merger may be different from firms who pursue other non-

acquisition related strategic alternatives.

All fiscal 2007 acquisition announcements above $5 million where the target firm was

publicly traded in the U.S. and a controlling interest was sought were accessed via SDC. This

provided 383 observations. In addition, hand collection was required to identify the starting point

of the negotiation/strategic alternatives process. Data from CRSP and COMPUSTAT data was

required for the construction of independent variables in the subsequent analyses. The EDGAR

website was utilized to obtain the applicable merger forms (Form S-4, Form DEFM-14A, and Form

SC-TO).

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 12/42

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 13/42

13

used as the starting point of negotiations, respectively. This increases the noise in the non-strategic

disclosure firms, but should not bias the results in a particular direction. After hand collecting first

event dates from the background of SEC filings my initial sample size was 225 observations. Refer

to Table 1.

5 .0 Model

A maximum likelihood estimation procedure with a logistic distribution is employed to

model the probability of strategic disclosure.

Pr 1 0 1 2 3 4 5

(1)

5.1 Employee Disruption Variables: If a companys ongoing operations are more likely to be

disrupted from a public announcement of strategic alternatives, then it is less likely to strategically

disclose. The employee specific disruption costs are unobserved so three proxy variables are

implemented. The number of managers employed at each firm is unknown. Multi-segment firms

typically have a tiered structure in which each division has its own executive manager, and each

segment has its own tranche of middle management. Given the implied costs of management

disruption I utilize Seg_D as an indicator variable that equals 1 if a firm has more than one segment

and is equal to zero otherwise. Since multi-segment firms will have executives operating each

branch I hypothesize that firms with more divisions are less likely to strategically disclose.

The second disruption variable comes from Matsumoto (2002), Lab_Int . Firms that are less

capital intensive are less likely to publicly pre-announce the pursuit of strategic alternatives.

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 14/42

14

Disruption costs are lower for capital intensive firms because such firm can rely on its machines to

keep producing. A manufacturing firm that strategically disclosed will be able to produce its

product at a constant rate given its capital investment in its property, plant, and equipment. A

service firm which relies on customer service and its salesforce is hypothesized to be more

damaged with full disclosure of management plans. If the merger is not consummated there is

potential that the intangible value (customer relationships) of the target firms is irreparably

damaged. Lab_Int is a measure of labor intensity,

. Since labor intensive firms are

more dependent on its employees to conduct operations I would expect a negative coefficient. An

alternative argument would be that labor intensive firms hold more growth options. I cannot refute

this argument, but include BTM as a control variable to attempt to capture the value of firm

heterogeneity between an assets in place firm versus a firm with growth options (Smith and Watts

[1992]). Regardless, a firm with more growth options derives more of its value from intangibles

(employees, customer relationships, internally developed brand names). Disruption costs for such

firms are more severe and not inconsistent with Hypothesis 1.

The third variable, EE_Rev, is revenue per 1,000 employees. The higher the ratio of revenue

per 1,000 employees the more likely it is that disruption costs will prematurely damage the firm.

Hence I would expect a negative relationship.

5.2 Information Demand Variables: The extant literature has shown that information

demand is higher when firms report losses (Chen et al. [2002], Rogers and Van Buskirk [2009]).

When a firm reports a loss to the market, shareholders may be concerned with managements

operating plan going forward or that the concurrent operating plan is ineffective. Hence

management has an incentive to strategically disclose to inform the market of its new strategy.

Strategic disclosures may also be the result of agency costs. After poor performance, the CEO is

concerned about job security. To maximize his payout package a CEO decides to announce strategic

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 15/42

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 16/42

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 17/42

17

Alternatively, management could use the disclosure as a preemptive defense. Management

may believe that its market price is undervalued and has received unsolicited, but friendly, private

bids. The market reacts favorably to similar disclosures (Woolridge and Snow [1990]). Subsequent

to the announcement the firms stock price rises. Then friendly (or hostile) private bidders have a

higher floor to begin negotiations with the target firm. However, this strategy seems rather

ineffective, because rational bidders would acknowledge that the increase in price is likely

influenced by the higher probability of an acquisition rather than an immediate increase to the

companys stand alone value. Heitzman and Klasa [2010] note that for news prior to a merger

announcement there is no effect on the merger premium. Nevertheless, if a preemptive argument is

true then management must be able to accurately predict when its company will be a takeover

target. Hence I utilize the control variables identified in Palepu (1986)7 and Comment and Schwert

(1995) to determine if the hypotheses derived above are robust to a preemptive defense argument.

The probability of a firm being a takeover target is notoriously difficult to predict, which was the

premise of Palepu (1986). However this seminal paper is widely cited as an empirical foundation to

determining whether takeovers can be predicted. Using extant theory Palepu (1986) tests whether

a low PE ratio, high intraindustry merger activity, poor performance, slowing growth, and a

growth/resource mismatch leads to a higher takeover probability. I include the Palepu (1986)

variables in my logistic regression. If managers want to preempt a takeover they would recognize

that the implied probability of the firms takeover is higher, hence the Palepu (1986) variables

would be statistically significant in my strategic disclosure model.

Pr

1 0

1

2

3

4

5

7 8 9 10 11 12

7 In Palepu (1986) there is a detailed two stage procedure to determine whether accounting variables can beutilized as predictors of takeovers. However I include all variables in one stage because my deterministicmodel and the Palepu (1986) model contain similar independent variables.

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 18/42

18

1 14 15 . (4)

All financial statement variables below are measured as of the most recent fiscal year ended

prior to the first event. PE is the firms price to earnings ratio. I_Dummy is an indicator variable

signifying whether or not there was an acquisition in the same industry (4-digit SIC) within two

years of the first event. Growth is the change in total sales. Pre_Abret is the sixty trading day

abnormal return prior to the strategic event. A market model is utilized to develop a firm-specific

beta. For each firm in the sample, I calculate the market model regression for the 253 trading days

ending 61 days before the strategic event.

(5)

Where Rit is the continuously compounded return to the stock of target firm i and Rmt is the

continuously compounded return to the CRSP value-weighted portfolio of NYSE, NASDAQ, and

AMEX listed stocks for day t. Firms are required to have 100 daily returns available to estimate the

parameters. Then Pre_Abret is measured by

(6)

As a caveat there are differences between the Palepu (1986) model and my model. For

several of the financial statement variables Palepu (1986) utilizes a four year average. Palepu

(1986) also includes two variables based on liquidity (current assets and current liabilities) and a

measure of profitability (ROA), which is already captured by my LOSS variable. These constraints

would have reduced my sample by 20%. If included the liquidity variables are not statistically

significant (results are untabulated). As the sample size is constrained already I did not include the

variables four year average or the liquidity variables.

6.0 Descriptive Statistics

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 19/42

19

Univariate statistics are presented in Table 2. To reduce the influence of outliers I

winsorize all non-binary variables in the sample at the 0.5% and 99.5% percentiles. Thirty out of

225 target firms issued a strategic disclosure within two years of a merger announcement, or

13.3% of the sample. The average strategic discloser has $1.9 billion in revenue and $2.6 billion in

assets versus $778 million in revenue and $1.9 billion in assets for the non-strategic discloser.

Binary variables are compared using a proportional Z-test. Non-indicator variables are compared

using a difference in means t-test. Strategic discloser firm revenue is significantly higher than non-

strategic disclosures at the 1% level. Larger companies tend to strategically disclose more often

which can be interpreted as a measure of stability and thus large firms are more confident of being

able to handle the disruptions. The average strategic disclosing firm has 7,600 employees versus

3,700 employees for the non-disclosing firms. Strategic disclosures have 4.4 segments on average

versus the 4.8 segments of non-strategic disclosers.

As measured by Lab_Int , more labor intensive firms are less likely to issue strategic

disclosures. This implies that firms which depend on their workforces tend to negotiate in private

to avoid disruption. However there is no univariate evidence of a relationship between strategic

disclosures and the number of segments a firm has or the number of employees a firm has scaled by

revenue. In fact approximately 76% of firms in both samples have multi-segment operations. One-

third of strategic discloser firms have shareholders that filed Form 13D versus 16% of non-strategic

disclosure firms. In this study, Form 13D filing proxies for shareholder activity. The difference is

statistically significant at the 1% level. Strategic disclosers reported a loss 37% of the time, versus

only 17% of the opposite group, again statistically significant at the 1% level. However, the

difference in ROA between the two subgroups is statistically indistinguishable. Although this goes

against the voluntary disclosure theory, proprietary costs of voluntary disclosure are often only

empirically identified in segment disclosure research (Heitzman et al. [2010]). On a univariate

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 20/42

20

basis there appears to be no difference in informational asymmetry in the 5 trading days prior to

the strategic decision date.

In regards to the Palepu variables, 77% of strategic disclosers witnessed recent acquisitions

in their industry versus 58% in the non-strategic disclosure category. This difference is statistically

significant and consistent with a preemptive story. Strategic disclosers are more heavily leveraged

than their peers, with long term debt as a percentage of total assets of 21% versus 14%. The

remaining Palepu (1986) variables are statistically indistinguishable from each other. Consistent

with practitioner beliefs approximately 30% of strategic disclosers bundle their news with an

earnings forecast when information is processed most readily.

The Spearman rank correlation matrix is presented in Table 3. Consistent with the

univariate comparison strategic disclosers are larger, less labor intensive, more often subject to

blockholder purchases, and more likely to record losses in its most recent quarter. In addition

strategic disclosers have a slower revenue growth rate than firms who did not issue strategic

disclosures. There are a few correlations that brought concerns up of multicollinearity. Two of the

disruption cost proxies, Seg_D and Lab_Int, have a negative correlation coefficient of -0.498. Two

other independent variable pairs had negative correlation coefficients greater than -0.40,

To assess the level of multicollinearity in the model, I

employ a variance inflation factor (VIF) test using OLS (results not tabulated, Marquardt [1970]).

VIF factors greater than five are typically seen as problematic (Longnecker 2004). In my empirical

setting, the VIF factors for the independent variables were no greater than 1.5.

7.0 Results

8 In future versions of this paper I will use factor analysis on the disruption variables to further reducemulticollinearity concerns.

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 21/42

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 22/42

22

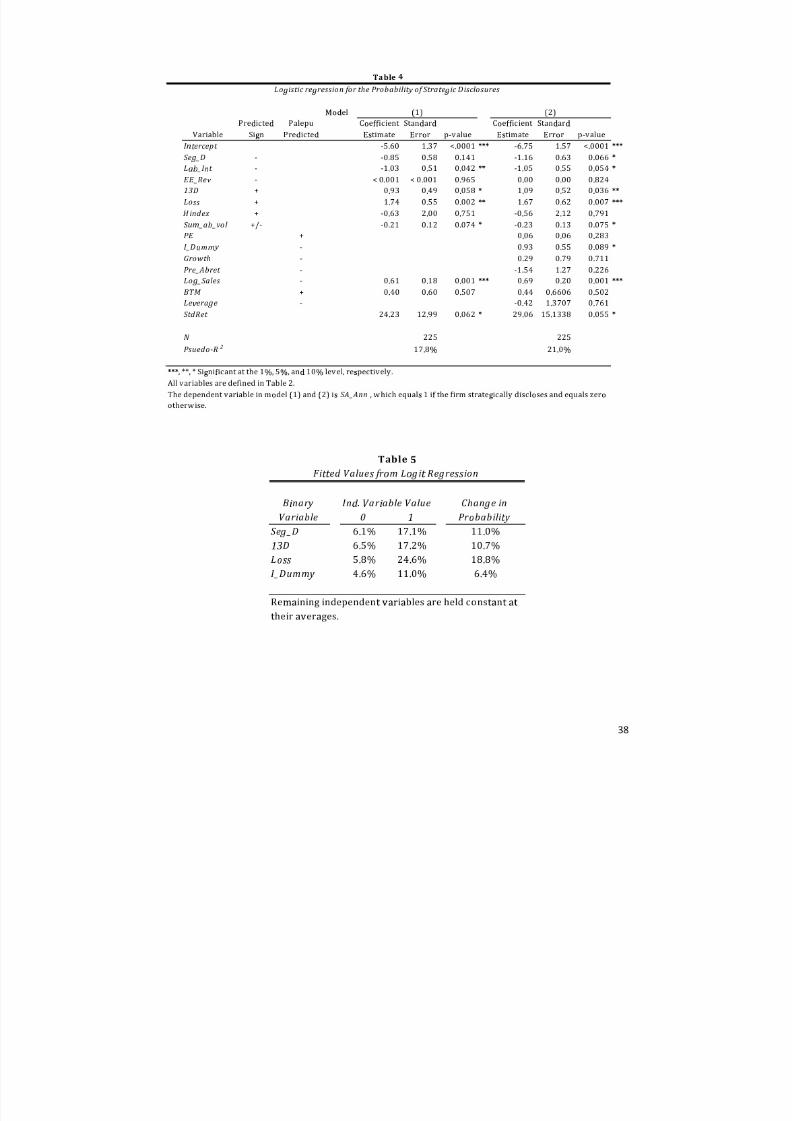

The relationship between strategic disclosures and trading volume could run in either

direction. If a firms volume is abnormally high prior to a strategic disclosure this could imply that

there was legal pressure from the SEC, firm lawyers, or its security exchange to disclose the

probable cause of the higher volume. If volume is abnormally low, informational asymmetry is

higher ex ante and such disclosure can signal to market participants that the firm is up for sale to

the highest bidder. Again, uncertainty may not decrease ex post . The market will impound the

probability of the firm being sold and the estimates of synergies from unobserved bidders. In both

models Sum_Ab_Vol is positive and marginally significant, which is interpreted as an improvement

in the firms information environment rather than a mandatory disclosure requirement. In terms of

economic significance, Figure 2 shows that a standard deviation decrease from the mean in

abnormal volume results in a 5% increase in the probability of disclosing. The slope also

accelerates as volume deficiencies become more severe.

The Palepu (1986) variables do not strongly support a preemptive defense story. Larger

companies instead of smaller companies appear to be more likely to strategically disclose,

consistent with firm stability being an important factor of preemptive disclosure. Poor

performance as measured by Pre_Abret has no affect on the disclosure decision. The Loss variable is

consistent with the poor performance story. However, if we include ROE in model (2) the

coefficient on ROE is positive and statistically significant, which again is opposite of the predicted

sign. The only consistent variable is I_Dummy. A firm is more likely to strategically disclose when

there is merger activity within its industry. If there is recent merger activity within an industry the

likelihood of a strategic disclosure increases by 5%. The remaining preemptive variables are

insignificant.

7 .2 Market Reaction to Strategic Disclosures: The previous section models the firm-specific

determinants of strategic disclosure. This section investigates the market reaction to strategic

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 23/42

23

disclosures and further investigates their impact on the runup. A negative strategic announcement

effect would infer that shareholders are surprised by the poor future prospects of a firm continuing

as a going concern. A positive strategic announcement effect implies that shareholders are

optimistic about the strategic alternative approach taken by management or that the probability of

a merger occurring is higher than expected. After such disclosure, shareholders are now aware (or

more aware than previously) that the firm is up for sale and firms shares have potential to earn a

merger premium if acquired. I calculated the strategic disclosure/event announcement return as

the two day window [0,1] using the market model beta from Pre_Abret (equations [5] and [6]).

Table 6 shows that, on average, strategic disclosures provide a positive abnormal return of

7.2%9. Compared with peer firms that did not publicly acknowledge strategic alternative

discussions or the receipt of a private bid the difference in abnormal returns is statistically

significant at the 1% level with a t-statistic of 7.6. Shareholders react favorably to the news that

management is considering strategic alternatives to maximize shareholder returns. The results

here are similar to Woolridge and Snow (1990) in that shareholders reacted favorably (0.6%), but

the cumulative abnormal returns are much higher in this study. This is due to the different

announcement effect that Woolridge and Snow (1990) capture. They focus on announcements of

strategic investments (R&D, capacity expansion, new productsetc.) rather than the public

announcement to pursue strategic alternatives.

A firm explicitly notifies the market of its intention to pursue strategic alternatives. In

Schwert (1996), the markup pricing hypothesis states that the acquisition price is effectively a

markup on the current targets stock price. As a result a $1 increase in the runup leads to a $1

higher price paid to target shareholders. I was interested to see if the management provided

9 Since approximately 30% of firms bundle their strategic disclosure to earnings announcements there is a

possibility that this window is also capturing the earnings news contemporaneously. If I excludecontemporaneous earnings announcement observations the results remain unchanged.

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 24/42

24

information had any effect on the total premium paid to shareholders. Gupta and Misra (1989)

noted if news10 was released prematurely then the runup is higher over a 30 day window prior to a

merger announcement. Heitzman and Klasa (2010) show similar evidence of higher 63-day runups

for news, but the effect on the total market premium is indistinguishable from zero. Schwert

(1996) shows that the total 42 day merger runup with news is higher than his average merger

runup. The premiums for his total sample versus the premiums for his news sample are statistically

indistinguishable from each other. In contrast Ahern and Sosyura (2010) find that media coverage

increases for acquirer firms and this leads to higher short-term runups for acquirers prior to the

merger. According to this story media coverage is controlled by the acquiring firm and is

opportunistic in that it helps the acquiring firm set a higher exchange ratio. So in Ahern and

Sosyura (2010) the disclosure by the participant in the corporate control contest does impact the

transaction price of the acquisition.

My study differs in that I employ a longer return window and a type of news that is directly

controlled by the potential target firm. Most other merger related studies jointly measure gossip,

Form 13D filings, target disclosure, and bidder disclosure as news.

To calculate abnormal returns, a market level beta is estimated using the same approach as

Pre_Abret over the period t = -508, , -254 trading days, where t is the merger announcement date.

I calculate runup abnormal returns as the summation of the market model residuals (see equations

(5) and (6)) using two windows [-255, -1] and [-42,-1]. The longer window return is employed to

incorporate the first event, which on average occurred 162 days prior to the merger announcement.

The second window is consistent with Schwert (1996). Table 6 provides a summary of the

firms seeking approval to merger, (5) firms looking for a buyer, (6) firms rebuffing unwanted advances, and(7) other stories suggesting that the name firm is a takeover target.

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 25/42

25

For the [-255,-1] window there is no statistical difference in abnormal returns between the

strategic disclosers (-1.4%) and the non-strategic disclosures (-1.1%). In the smaller [-42,-1]

window the strategic disclosure abnormal returns are -4.2% versus 0.2% for non-strategic

disclosures and the non-disclosers run-up is relatively more positive at the 10% level with a t-

statistic of 1.81. This is likely due to the run-up benefit already being exhausted for the strategic

disclosers prior to the 42 day run-up window. These runups are markedly different from what was

found in Schwert (1996) where the average runup was 13.3%. The difference between the two

runups based on sample period differences. The year 2007 contained the beginning of the liquidity

crisis and it is possible that more distressed firms were acquired in this time period. When I apply

my model over a longer time period (1994 -2009) the average runup was 9.4% which is consistent

with Heitzman and Klasa (2010), 9.6%.

The merger markup is measured from t= 1, , 110. Again, the total markup is

indistinguishable whether the firm is a strategic or non-strategic discloser. The markup for the

non-strategic disclosers is 24.3% and the markup for the strategic disclosers is 21%. Figures 3 and

4 show the merger premium graphically over the two separate windows. In Figure 4 there is a

relatively more positive runup and a higher merger announcement return for non-disclosers. The

non-strategic disclosure merger announcement abnormal return is 25.1% versus the strategic

disclosure abnormal return of 18.1%. The difference of 7% is likely due to the probability of

acquisition already being impounded in the stock price for strategic disclosers. However, these two

returns are not statistically different from one another. Strategic disclosing firms have more

volatile returns consistent with the logistic regression in Table 4.

Although informative the simple premium analysis cannot quantify the effect of the

disclosure. Without introducing counterfactual evidence, it is not observable what the total

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 26/42

26

premium would have been without a firm strategically disclosing11. The negotiation process can be

studied to see how, if at all, the preemptive disclosure affected the merger. Table 6 shows that the

number of trading days from the first event to the merger announcement, M_Lag, is shorter for

strategic disclosers with an average of 108 days versus the 170 trading day average for the non-

strategic disclosers. M_Lag should be interpreted cautiously because this relationship may be due

to construction of the SA_Ann date. When firms are classified as strategic disclosers the SA_Ann

date could come after the firm began considering strategic alternatives. For example say a firm

internally discussed strategic alternatives on January 1, 2007 but did not disclose their intentions

until March 31, 2007 and announced the merger on June 30, 200. M_Lag would only represent the

trading days between March 31 and June 30, even though they began internal discussions on

January 1.

Publicly disclosing intentions should attract all possible bidders (Gole and Hilger [2008]). I

find evidence supporting this claim as there were more than double non-binding indications of

interest, Pre-Bidders, in the pre-merger announcement period for the strategic disclosers (4.8)

versus the non-strategic disclosures (2.2). I also find that disclosing firms are less likely to be

purchased with stock than non-strategic disclosers. To see if the potential suitors for a target firm

(strategic versus non-strategic) affects the disclosure decision I determine whether the eventual

winning bidder is classified in the same Fama and French (1997) industry. Strat is equal to 1 if the

target and bidder firms are in the same industry and is equal to zero otherwise. If disclosing firms

are using disclosure to attract potentially unknown bidders I posit that more out-of-industry

purchases occur for the strategic disclosers. Based on the results in Table 6, this does not appear to

be the case.

8.0 Summary and Future Work

11 See forthcoming analysis.

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 27/42

27

This study provides an understanding of the determinants of firms disclosure decisions

prior to an official merger announcement. Based on the empirical evidence I find that firms with

higher demand for information or firms that experience increased shareholder activity are more

likely to strategically disclose, as proxied by a loss in the most recent quarter or a recently filed

Form 13D. I also find some evidence that disruption costs are important to the managers decision

of whether or not to strategically disclose. Trading volume is abnormally low prior to a strategic

disclosure. Shareholders react favorably to strategic disclosures and such disclosures are

associated with more competition in the market for corporate control. My findings appear robust

to an alternative explanation of preemptive defense tactics. However, similar to Heitzman and

Klasa (2010) there appears to be no significant difference in the total premium paid for a target

firms stock for strategic disclosers and non-strategic disclosers.

In future work I would like to expand my sample and collect strategic disclosures beyond

the merger and acquisition realm to see if my findings are consistent for non-acquired firms. It

would be interesting to determine how often strategic disclosing firms are acquired. Do

shareholders punish managers for not following through on a promise to pursue strategic

alternatives? Although there are no findings on the impact of a strategic disclosure premium I need

to develop a more complex econometric model where counterfactuals can be developed to measure

the cost of not disclosing. In addition I would like to better understand how strategic disclosure

alters the relationship between the target firm and the investment bank (in terms of fees,

investment bank responsibilityetc.).

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 28/42

28

9.0 References

Ahern, K. and Sosyura, D. (2010). Who Writes the News? Corporate Press Releases During Merger

Negotiations. U niversity of Michigan: Working Paper.

Amel-Zadeh, A., Evans, O., and Meeks, G. (2008). Forecasts of Earnings by Takeover Bidders.

U niversity of Cambridge: Working Paper.

Ball, R. and Brown, P. (1968). An Empirica0l Evaluation of Accounting Income Numbers. Journal of

Accounting Research 6: 159 178.

Berger, P. and Hann, R. (2007). Segment Disclosures, Proprietary Costs, and the Market for

Corporate Control. The Accounting Review 82: 869 906.

Bernile, G., and Bauguess, S. (2010). Do Merger Synergies Exists? U niversity of Miami: Working

Paper.

Betton, S., Eckbo, E., and Thorburn, K. (2008). Chapter 15: Corporate Takeovers. Handbook of Corporate Finance, Vol.2, 289 427.

Boone, A. and Mulherin, J. (2007). How are Firms Sold? The Journal of Finance 42: 847 875.

Boone, A., and Mulherin, J. (2009). Is There One Best Way to Sell a Company? Journal of Applied

Corporate Finance 21: 28 37.

Bowen, R., DuCharme, L., and Shores, D. (1995). Stakeholders Implicit Claims and Accounting

Method Choice. Journal of Accounting and Economics 20: 255 295.

Brennan, N. (1999). Voluntary Disclosure of Profit Forecasts by Target Companies in Takeover

Bids. Journal of Business, Finance, and Accounting 26: 883 917.

Bushee, B. and Noe, C. (2000). Corporate Disclosure Practices, Institutional Investors, and Stock

Return Volatility. Journal of Accounting Research 38 Supplement: 171 202.

Campbell, C. and Wasley, C. (1996). Measuring Abnormal Daily Volume for Samples of NYSE/ASE

and NASDAQ Securities Using Parametric and Nonparametric Test Statistics. Review of Quantitative

Finance and Accounting 6: 309 326.

Chen, S., DeFond, M., and Park, C. (2002). Voluntary Disclosure of Balance Sheet Information in

Quarterly Earnings Announcements. Journal of Accounting and Economics 33: 229 251.

Comment, R. and Schwert, G.W. (1995). Poison or Placebo? Evidence on the Deterrence and Wealth

Effects of Modern Antitakeover. Journal of Financial Economics 39: 1 43.

Diamond, D. and Verrecchia, R. (1991). Disclosure, Liquidity, and the Cost of Capital. The Journal of

Finance 66: 1325 1355.

Eckbo, E., and Langohr, H. (1989). Information Disclosure, Method of Payment, and Takeover

Premiums. Journal of Financial Economics 24: 363 403.

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 29/42

29

Eritmur, Y. (2004). Accounting Numbers and Information Asymmetry: Evidence from Loss Firms.

Duke U niversity: Working Paper.

Fama, E. and French, K. (1997). Industry Costs of Equity. Journal of Financial Economics 43: 153

193.

Francis, J., Philbrick, D., and Schipper, K. (1994). Shareholder Litigation and Corporate Disclosures.

Journal of Accounting Research 32: 137 164.

Froot, K. and Stein, J. (1992). Shareholder Trading Practices and Corporate Investment Horizons.

Journal of Applied Corporate Finance September/October: 42 58.

Gole, W. and Hilger, P. (2008). Corporate Divestitures: A Mergers and Acquisitions Best Practices

Guide. Hoboken: Wiley.

Gupta, A. and Misra, L. (1989). Public Information and Pre-Announcement Trading in Takeover

Stocks. Journal of Economics and Business 41: 225 233.

Hartzell, J., Ofek, E., and Yermack, D. (2004). Whats in it for me? CEOs Whose Firms Are Acquired?

The Review of Financial Studies 17: 37 61.

Haw, I., Pastena, V., and Lilien, S. (1990). Market Manifestation of Nonpublic Information Prior to

Mergers: The Effect of Ownership Structure. The Accounting Review 65: 432 451.

Hazen, T. (1986). Rumor Control and Disclosure of Merger Negotiations or other Control-Related

Transactions: Full Disclosure or No Comment the Only Safe Harbors. Maryland Law Review 46:

954 973.

Healy, P. and Palepu, K. (2001). Information Asymmetry, Corporate Disclosure, and the Capital

Markets: A Review of the Empirical Disclosure Literature. Journal of Accounting and Economics 31:

405 - 440.

Heitzman, S. (2010). Equity Grants to Target CEOs During Deal Negotiations. U niversity of Oregon

Working Paper.

Herz, J. and Baller, C. (1971). Business Acquisitions: Planning and Practice. N ew York: Practicing

Law Institute.

Heitzman, S. and Klasa, S. (2010). Causes and Consequences of Stock Price Runups in Acquisition

Targets: Evidence from Deal Negotiations. U niversity of Oregon: Working Paper.

Jarrell, G. and Poulsen, A. (1989). Stock Trading Before the Announcement of Tender Offers:

Insider Trading of Market Anticipation. Journal of Law, Economics, and Organization 2: 225 248.

Jorgensen, B. (1998). Hedging and Performance Evaluation. Harvard Business School Working

Paper.

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 30/42

30

Kim, O. (1993). Disagreements among Shareholders over a Firms Disclosure Policy. The Journal

of Finance 48: 747 760.

Kimbrough, M. and Louis, H. (2010). Voluntary Disclosure to Influence Investor Reactions to Merger

Announcements: An Examination of Conference Calls. Pennsylvania State U niversity: Working

Paper.

Krug, J. A. (2009). An analysis of long-term leadership continuity in target firms. Journal of Business

Strategy 30: 4 -14.

Longnecker, M.T. (2004). A First Course in Statistical Methods. Belmont: Thomson-Books/Cole.

All variables are defined in Table 2. Bolded co rrelation coeff icients imply statistical significance of 0.05 or greater.

Spearman Correlation Matrix

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 38/42

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 39/42

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 40/42

40

Appendix A ± Background Example

The following is excerpted from Factor Card & Party Outlets Form SC TO-T (tender offer proxy statement)issued on October 1, 2007:

On December 12, 2006, Factory Card publicly announced that it had initiated an external process to explore

strategic alternatives to enhance stockholder value. On January 23, 2007, Factory Card publicly announced itsselection of Goldsmith Agio Helms (Goldsmith) as its financial advisor. Goldsmith contacted Berkshire in oraround April 2007 to solicit interest in a possible transaction with Factory Card.

AAH Holdings executed a confidentiality agreement with Goldsmith on April 24, 2007 and subsequentlyreceived a confidential information memorandum (CIM) concerning Factory Card. Berkshire and WestonPresidio assisted AAH Holdings in (i) analyzing the opportunities for Factory Card as a part of the AAHHoldings organization; (ii) evaluating the fair market value of Factory Card and its attractiveness as aninvestment for AAH Holdings; and (iii) assessing AAH Holdings ability to fund the acquisition.

On May 25, 2007, AAH Holdings submitted a preliminary indication of interest for between $12.50 and $16.00per share, in cash. The range was based on Factory Cards earnings potential as a subsidiary of AAH Holdingsand an analysis of relative market valuations of Factory Cards peers. Factory Cards earnings potential was

estimated using the CIM and preliminary diligence conducted by AAH Holdings and its representatives.

Based on its preliminary indication of interest, AAH Holdings was invited to attend a management presentation regarding Factory Card. On June 6, 2007, representatives of Factory Card and Goldsmith met with representatives of AAH Holdings. Gary W. Rada, Factory Cards President and Chief Executive Officer,gave a presentation regarding Factory Cards historical financial performance, strategic growth plan andprojections, and merchandising and marketing strategy.

Beginning on June 21, 2007, Factory Card provided AAH Holdings and its representatives with access tofinancial and legal diligence materials in an online data room. In the course of conducting their due diligence.

On July 18, 2007, representatives from AAH Holdings and Ernst & Young, financial consultant to AAHHoldings, met with certain members of Factory Cards finance team. AAH Holdings reviewed Factory Cards

financial systems and reporting processes, balance sheet reserves and key accounting policies, gross marginsand other operating costs, managements view of extraordinary expenses, and other general accountingmatters. Generally from June 21 through July 25, 2007, Factory Card management and Goldsmith helpedanswer outstanding diligence questions when information was not readily available in the data room.

Goldsmith instructed interested parties to submit final bids for Factory Card on July 25, 2007. On July 25,2007, AAH Holdings submitted a bid for $15.00 per share and submitted comments to Factory Cardsproposed form of merger agreement.

On July 27, 2007, representatives from Goldsmith met telephonically with representatives from AAH Holdingsto discuss AAH Holdings bid. The representatives from Goldsmith informed AAH Holdings that Goldsmithwas authorized to make a counter-proposal to selected parties that had submitted bids. Goldsmith alsodescribed the Boards concern regarding AAH Holdings ability to close the transaction. Goldsmith proposed

that AAH Holdings increase its bid to $17.50 per share.

On July 31, 2007, AAH Holdings submitted a revised proposal for $16.00 per share, which included a$4 million reverse breakup fee to address the Boards concern regarding the certainty of AAH Holdingsability to close the transaction. At $16.00 per share, AAH Holdings still viewed Factory Card as an attractiveasset within AAH Holdings. AAH Holdings requested a two-week exclusivity period to complete its duediligence and finalize the merger agreement.

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 41/42

41

On August 2, 2007, representatives from Goldsmith met telephonically with representatives from AAHHoldings to discuss AAH Holdings revised bid. Goldsmith informed AAH Holdings that Factory Card wouldenter into a two-week exclusivity agreement with AAH Holdings if AAH Holdings increased its bid to $17.50per Share.

On August 4, 2007, AAH Holdings submitted a revised proposal for $16.50 per share. Goldsmith subsequently

informed AAH Holdings that based on the revised proposal and the parties discussions to date, Factory Cardwas prepared to grant AAH Holdings the requested limited exclusivity period.

On August 8, 2007, AAH Holdings executed an exclusivity agreement with Factory Card whereby AAHHoldings was granted an exclusive period, expiring on August 22, 2007, to conduct additional due diligence inorder to confirm its $16.50 per share offer price and negotiate definitive documentation of the proposedtransaction.

From August 8 to August 22, representatives of AAH Holdings, and its financial and legal advisors, workedwith Factory Cards management and financial and legal advisors to complete AAH Holdings due diligence.Representatives from both parties legal counsel worked with AAH Holdings and Factory Card to negotiatethe merger agreement.

On August 22, 2007, the initial exclusivity period expired and AAH Holdings requested an extension of theexclusivity period until August 31, 2007 to complete its due diligence and finalize the merger agreement. AAHHoldings also indicated for the first time that it wanted the executive officers of Factory Card who hademployment agreements with Factory Card to agree to certain amendments to those agreements prior to theexecution of the Merger Agreement. On August 23, 2007, the exclusivity period was extended until August 29,2007.

Over the next several days, the parties respective legal advisors continued to negotiate the terms of theMerger Agreement. During the last week of August, AAH Holdings commenced negotiations between AAHHoldings and certain of Factory Cards executive officers, who were represented by counsel in thesenegotiations separate from Factory Cards counsel, regarding amendments to their employment agreementsto be put in place at the closing of the Merger. Parent, as the sole stockholder of Purchaser, reviewed andapproved the form of the merger agreement, and the transactions contemplated thereby, on August 27, 2007.

The board of directors of each of Parent and Purchaser approved the form of the merger agreement, and thetransactions contemplated thereby, on August 28, 2007 and August 29, 2007, respectively.

The executive officers and AAH Holdings continued to negotiate the executive agreements during the first twoweeks of September. AAH Holdings and Factory Card also continued to negotiate and exchange drafts of themerger agreement during this time.

Once the executive agreements and the merger agreement were finalized, the Factory Card board of directorsapproved the agreement, and the transactions contemplated thereby, on September 17, 2007. The MergerAgreement was executed by Factory Card, Purchaser and Parent the evening of September 17, 2007. Thefollowing day, AAH Holdings and Factory Card issued a press release announcing the execution of the MergerAgreement.

8/7/2019 MD 12-15-10

http://slidepdf.com/reader/full/md-12-15-10 42/42

Appendix B Press Release Example

The following is excerpted sections from Factory Card & Party Outlet Corps 8-K issued on December 12,2006:

Item 2.02. Results of Operations and Financial Condition

On December 12, 2006, Factory Card & Party Outlet Corp. issued a press release announcing fiscal 2006 thirdquarter financial results and that it had begun an external process to explore strategic alternatives to enhancestockholder value. A copy of Factory Card & Party Outlet Corp's press release is attached hereto as Exhibit 99.1.

Item 8.01. Other Events

The Company also announced that the board of directors of the Company has initiated an external process toexplore strategic alternatives to enhance stockholder value. Such strategies may include, but are not limitedto, acquisitions, the potential sale of the Company, strategic joint ventures, mergers and/or stock repurchases. The board of directors intends to engage an investment banking firm to assist management andthe board in exploring strategic alternatives. The Company will evaluate the alternatives and pursue those it

believes are in the best interest of the Company and its stockholders. At this time, there can be no assurancethat this strategic analysis will result in any transaction(s). The Company may not make any furtherannouncements regarding its exploration of strategic alternatives unless and until the process is terminatedor it executes a definitive agreement relating to a transaction.