MM Credo •We Will Always Follow Formal Practices Of Business, Pay All Our Taxes, And Fulfill All Legal Liabilities and Our Responsibilities Towards Our Nation. The Amount Left After Fulfilling All Our National And Citizen Responsibilities Would Be The Actual Profit For Us , and Only That Is What We Deserve.

Transcript

MM Credo

• We Will Always Follow Formal Practices Of Business, Pay All

Our Taxes, And Fulfill All Legal Liabilities and Our

Responsibilities Towards Our Nation. The Amount Left After

Fulfilling All Our National And Citizen Responsibilities

Would Be The Actual Profit For Us , and Only That Is What

We Deserve.

MEDIA & ENTERTAINMENT INDUSTRY 2016

Presented by

Roshni Trivedi

Objective

• How M&E Industry is changing its strategy and grabbing the opportunities to exist their presence• Mobility has changed and become dominance access over M&E

industry

Flow of presentation

• Introduction• The Great Disruption• Media & Entertainment Industry 2016

Tomorrow Begins

Media and entertainment: Sectors TelevisionRadioDigital ConsumptionFilmsPrintOut of HomeAnimation VFX and post productionLive eventsTheme parksSportsTax and regulatoryDeal volume and value

A Decade of Mobility: Mobile media consumption today

1. 20 years of mobile but serious data use only in past 5 years2. Close to a billion mobile subscribers, over 500 million unique users3. 180 million smartphone now to reach 690 million by 2020, But low

price points key to adoption4. Non-smart ‘feature phones’ too support data, basic apps but will

get phased out5. Most media consumed by mobile users via shares on social media

and chat apps. But memory and data light models critical for success

6. Indian needs have unique challenges, opportunities. 1. E.g. video on memory card downloads rather than just streaming

Mobile will

continue to be

the primary medium

of internet access

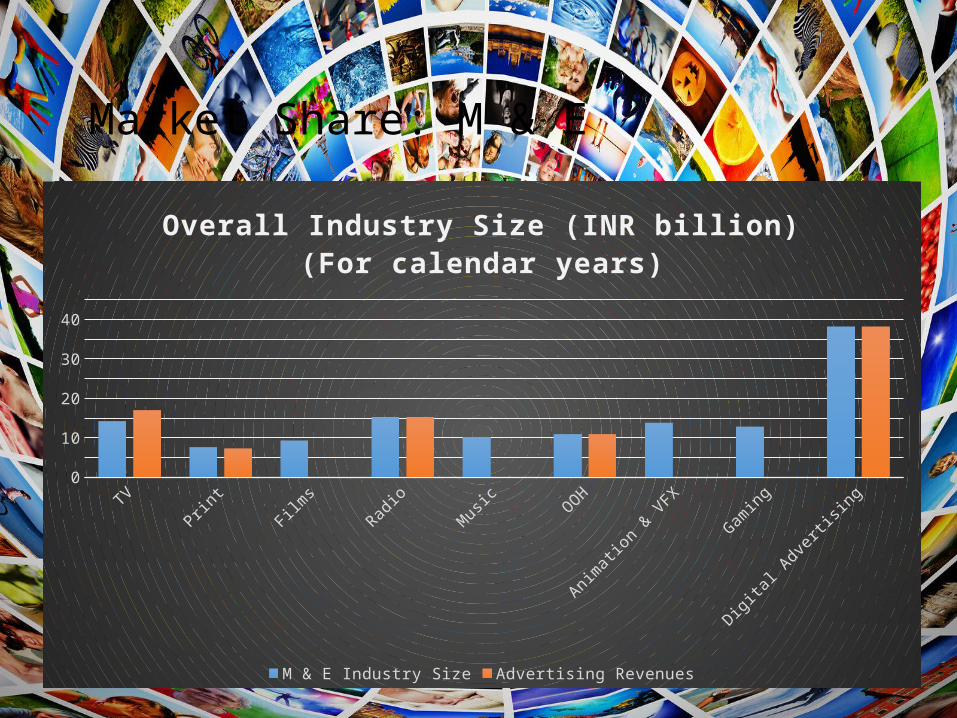

Market Share: M & E

TV Print Films Radio Music OOH Animation & VFX Gaming Digital Advertising0

5

10

15

20

25

30

35

40

45

Overall Industry Size (INR billion) (For calendar years)

M & E Industry Size Advertising Revenues

Next 5 years Projection

• M & E Industry will grow by 14.3%• Advertising revenues will grow by 15.9%• How Virtual Media has dominated this industry

Indian film IndustryLargest in the world by films produced with over 1,400 films

produced & over 3.25bn tickets sold (~50% theatrical releases)At US$ 2.1bn, it is less than the BO of Avatar 2015 was heavily polarized wrt film performance. % of online ticketing grew by 5x from 6% to 32%Regional & Hollywood are growing domestic theatrical

Film: Revenue Split

• When you pay Rs 100 for a movie ticket, what is the split?• Gross – 100% (Rs 100) • Entertainment Tax – 30% (Rs 30) • Exhibitor – 50% of balance 70% (Rs 35) • Distributor – 50% of balance 70% (Rs 35) • Producer(s) – depends on what deal they have made with distributor

– Outright / MG / Commission / Distribution Fee • Co-producer(s) – deal-specific • P&A funding – deal specific, but usually is last-in-first-out. • Talent – actors / director – sweat equity.

Animation VFX and post -production

• Indian animation industry moving up the value chain• Today India has nearly 300 animation• 40 VFX and 85 game development studios• More than15k professionals working for them

Theme Parks in India

Emerging area

Destination entertainment

(non natural-tourism

based) yet to consolidate

in India

Evolution:

• 1980 – Appu Ghar

• 1990 – Esselworld

• 2010 – Imagica & Wonderla

• 2015 – INR 300 bn+

investment committed o

Over next 5 yrs, 19% CAGR.

Global amusement park industry performance – Resurgence in footfalls• Footfalls in 2014 130.18 million • Appu ghar to Adlabs Imagica• Top 10 amusement parks in india

Other Industry

• Sports: • Beyond cricket now industry and government is investing in other sectors• But cricket is one of the most sport seen through out all sectors

• Digital Advertisement spend:• Digital outperformed expectations in 2015, 38.2% growth.• It is expected to grow INR255 Billion in 2020.

• Print:• Telecom and e-commerce companies also preferred advertising on

television.• Business continues to grow at steady rate of around 8%

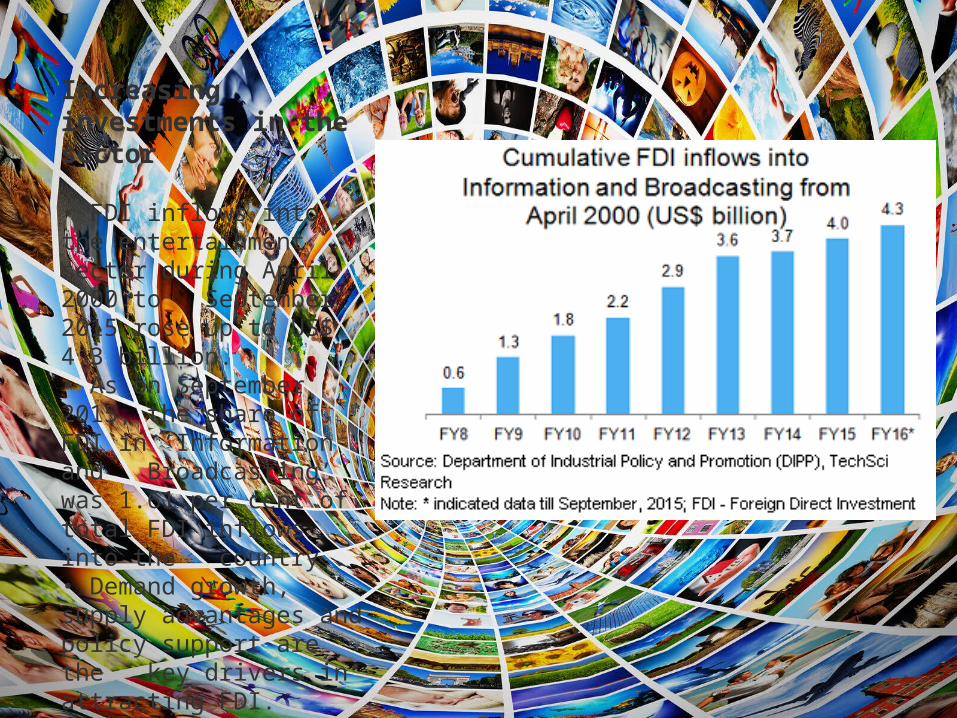

Increasing investments in the sector • FDI inflows into the entertainment sector during April 2000 to September 2015 rose up to US$ 4.3 billion.• As on September 2015, the share of FDI in ‘Information and Broadcasting’ was 1.61 per cent of total FDI inflows into the country.• Demand growth, supply advantages and policy support are the key drivers in attracting FDI.

Challenges

• Many traditional media firms don’t get tech which moves so fast that by the time they have figured out the web, its changed.• A strategic focus on technology directions will be crucial for M & E

firms to survive and thrive in the connected social digital age