Analysts who prepared this report are registered as research analysts in Indonesia but not in any other jurisdiction. PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES & DISCLAIMERS IN APPENDIX 1 AT THE END OF REPORT. Media Prime time to overweight We initiate our coverage on media companies MNC Nusantara Citra (MNCN/ Buy/ TP IDR2,700) and Surya Citra Media (SCMA/ Buy/ TP IDR3,870). We like SCMA on the back of its: 1) low gearing and high free cash flow (FCF), 2) robust dividend payout ratio, and 3) stellar ROE compared to peer. For MNCN, we favor the company due to 1) its strong audience share, 2) top notch power ratio, 3) the fact that it is the only TV operator that has integrated studio facilities located in one area in Kebon Jeruk, (MNC studio complex). We also believe MNCN will benefit from the strengthening of the rupiah given its USD debt exposures. Indonesian media: appealing outlook ahead We believe the media industry is well positioned to benefit from the continued expansion of private consumption. Given the large population base (4th populous country in the world) combined with stable income growth of consumers, we believe fast moving consumer goods (FMCG) companies are likely to benefit from this favorable macro backdrop. Furthermore, we expect FMCG companies to gear up their advertisement spending to maximize their position in the market. Even though Indonesia has exhibited high ad spend growth over the past couple of years (16% CAGR during 2011-2016F), we note that the average price for 30-second prime-time spot is relatively inexpensive at only USD5,400/spot compared to peer countries such as Australia, Singapore, Philippines (indicating ample room for growth). Furthermore, existing free-to- air TV operators are likely to benefit from the natural entry barrier given broadcasting license is limited by the regulators. Expecting better revenue in2Q on the back of Ramadhan We project revenue growth for both MNCN and SCTV will jump in 2Q, largely due to the sahur (“pre-dawn meal” which refers to food consumed early in the morning) base effect. As a quick reminder, Ramadhan was held during mid-June to July last year (vs. during the early part of June in 2016). MNCN and SCMA feature popular religious dramas during sahur in Ramadan. We initiate coverage on SCMA with a buy recommendation and a target price of IDR3,870, implying 34.7x 2016F P/E. We think the premium valuation on SCMA is justified, given that SCMA has a strong track record and a solid balance sheet. Our IDR3,870 target price is derived by using a blended calculation of target P/E at 35x and Discounted Cash Flow (DCF) method with 10-year time span. We initiate our coverage on MNCN with a trading buy rating and a target price of IDR2,700, implying 27.5x 2016F P/E. Our target price of IDR2,700 was derived using a blended calculation of target P/E at 28x and Discounted Cash Flow (DCF) method with 10-year time span. Media companies covered in this report Company name Ticker Rating TP (IDR) ROE (%) P/E(x) P/B(x) 2016F 2017F 2016F 2017F 2016F 2017F Media Nusantara Citra MNCN Buy 2,700 14.2 16.6 22.4 17.8 3.1 2.9 Surya Citra Media SCMA Trading Buy 3,870 47.5 47 29.6 25 12.6 10.7 Source: Daewoo Securities Research Overweight (Initiate) Initiation July 29, 2016 PT Daewoo Securities Indonesia Trade Christine Natasya +62-21-515-1140 [email protected]

Transcript

Analysts who prepared this report are registered as research analysts in Indonesia but not in any other jurisdiction. PLEASE SEE

ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES & DISCLAIMERS IN APPENDIX 1 AT THE END OF REPORT.

Media

Prime time to overweight

We initiate our coverage on media companies MNC Nusantara Citra (MNCN/ Buy/ TP

IDR2,700) and Surya Citra Media (SCMA/ Buy/ TP IDR3,870). We like SCMA on the back

of its: 1) low gearing and high free cash flow (FCF), 2) robust dividend payout ratio, and

3) stellar ROE compared to peer. For MNCN, we favor the company due to 1) its strong

audience share, 2) top notch power ratio, 3) the fact that it is the only TV operator that

has integrated studio facilities located in one area in Kebon Jeruk, (MNC studio complex).

We also believe MNCN will benefit from the strengthening of the rupiah given its USD

debt exposures.

Indonesian media: appealing outlook ahead

We believe the media industry is well positioned to benefit from the continued

expansion of private consumption. Given the large population base (4th populous

country in the world) combined with stable income growth of consumers, we believe fast

moving consumer goods (FMCG) companies are likely to benefit from this favorable

macro backdrop. Furthermore, we expect FMCG companies to gear up their

advertisement spending to maximize their position in the market. Even though Indonesia

has exhibited high ad spend growth over the past couple of years (16% CAGR during

2011-2016F), we note that the average price for 30-second prime-time spot is relatively

inexpensive at only USD5,400/spot compared to peer countries such as Australia,

Singapore, Philippines (indicating ample room for growth). Furthermore, existing free-to-

air TV operators are likely to benefit from the natural entry barrier given broadcasting

license is limited by the regulators.

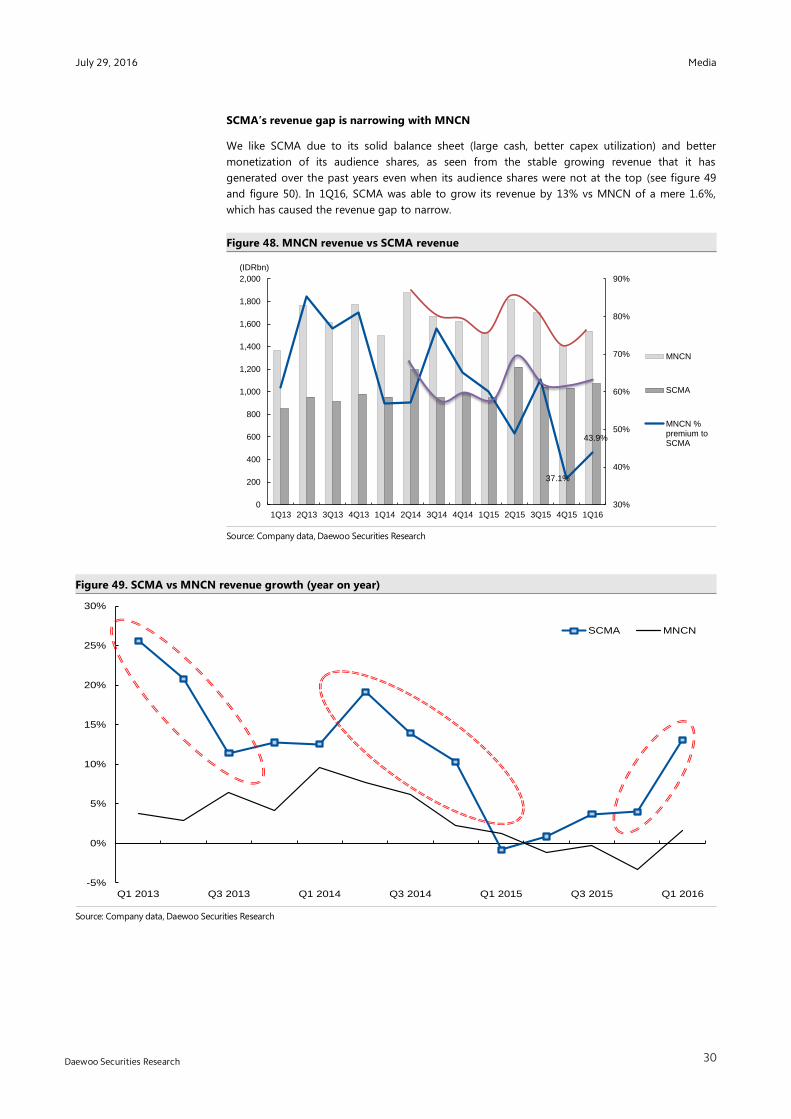

Expecting better revenue in2Q on the back of Ramadhan

We project revenue growth for both MNCN and SCTV will jump in 2Q, largely due to the

sahur (“pre-dawn meal” which refers to food consumed early in the morning) base effect.

As a quick reminder, Ramadhan was held during mid-June to July last year (vs. during the

early part of June in 2016). MNCN and SCMA feature popular religious dramas during

sahur in Ramadan.

We initiate coverage on SCMA with a buy recommendation and a target price of

IDR3,870, implying 34.7x 2016F P/E. We think the premium valuation on SCMA is

justified, given that SCMA has a strong track record and a solid balance sheet. Our

IDR3,870 target price is derived by using a blended calculation of target P/E at 35x and

Discounted Cash Flow (DCF) method with 10-year time span.

We initiate our coverage on MNCN with a trading buy rating and a target price of

IDR2,700, implying 27.5x 2016F P/E. Our target price of IDR2,700 was derived using a

blended calculation of target P/E at 28x and Discounted Cash Flow (DCF) method with

Indonesian media: appealing outlook ahead 3 Buy rating for SCMA (TP IDR3,870) and Trading buy for MNCN (TP IDR2,700) 4

Overview of the media industry 5

Private consumption is the backbone for advertisement demand 5 FMCG companies, especially cigarettes companies dominate the TV ad spend 9 TV companies’ biggest revenue comes from PT.Wira Pamungkas Pariwara 11 Ad supply: Limited for TV, yet huge potential for online advertisement 13 Biggest media TV competitor: Online advertisement 15

Surya Citra Media 18

Company Background 18 PT Indonesia Entertainment Group 20 Management team 21 Famous TV shows/drama currently played on SCTV 23 Famous TV shows/drama that is currently playing on Indosiar 24 SCMA investment in iflix 25 Analyzing the Sports content 26 Investment thesis on SCMA 28 Surya Citra Media (Valuations) 34 Surya Citra Media (Ticker SCMA IJ/ Buy/ TP: IDR3,870) 35

Media Nusantara Citra 39

Company Background 39 MNCN’s local content 40 MNC Pictures 40 Talent management 41 MNC Channels 41 MNC’s FTA stations appeal to different audience segments 47 Famous dramas currently played on RCTI 47 Famous dramas that are currently played on GlobalTV 48 Famous dramas that are currently played on MNC TV 49 MNCN charges more premium advertising cost through its quality contents 50 Investment thesis on MNCN 51 Media Nusantara Citra (Valuations) 54 Media Nusantara Citra (Ticker MNCN IJ/ Trading buy/ TP: IDR2,700) 55

Risks to our call 58

Media

3

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Investment summary

Indonesian media: appealing outlook ahead

We believe Indonesia’s TV media industry is well poised to benefit from the continued private

consumption expansion. Given the large population base (Indonesia is the world’s 4th

largest

populous country) combined with stable income growth of consumers, we believe fast moving

consumer goods (FMCG) companies are likely to benefit from this favorable macro backdrop.

Furthermore, we expect FMCG companies to increase their advertisement expenses to maximize

their position in the market. Even though Indonesia has already exhibited high ad spend growth

over the past couple of years (16% CAGR during 2011-2016F), we note that the average price for

30-second prime-time spot is relatively inexpensive at only USD5,400/spot compared to peer

countries such as Australia, Singapore, Philippines (indicating ample room for growth).

Furthermore, existing free-to-air TV operators are likely to benefit from the natural entry barrier

given broadcasting license is limited by the regulators.

Figure 1. Indonesia ad spending has grown by 16% CAGR in 2011-2016F

Source: Media Partners Asia, Daewoo Securities Research

Figure 2. Average price for 30 seconds prime-time spot

Source: Media Partners Asia, Daewoo Securities Research

80,000

5,400

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Australia Singapore Philippines Thailand Vietnam Malaysia Indonesia

USD/spot

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Media

4

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Figure 3. Prime time all demography (Free-to-air TV market share)

Source: Nielsen, Daewoo Securities Research

Buy rating for SCMA (TP IDR3,870) and Trading buy for MNCN (TP IDR2,700)

We like Surya Citra Media (SCMA) due to 1) its ability to maintain strong revenue growth despite

lower audience share compared to Media Nusantara Citra (MNCN), 2) better monetization of its

audience shares, and 3) high dividend payout ratio and strong cash position, as well as its stellar

EBITDA margin compared to peers.

MNCN, we favor the company due to 1) its strong audience share, 2) top notch power ratio, 3) the

fact that it is the only TV operator that has integrated studio facilities located in one area in Kebon

Jeruk, (MNC studio complex). We also believe MNCN will benefit from the strengthening of the

rupiah given its USD debt exposures.

Risks to our investment call

Risks to our call include 1) growing internet penetration which should prompt higher demand for

digital advertisement growth and pose threat to the conventional TV ad market, 2) government’s

regulation on cigarettes advertisement (as a quick reminder, cigarette companies command a

large portion of TV operators’ revenue), as well as 3) macroeconomic factors such as weaker-than-

expected Indonesian GDP (Daewoo forecast: 5.1% in 2016F, 5.3% in 2017F), commodity prices,

inflation rate, as well as the rupiah value against other countries.

48%

23%

14%

11%

4%

MNC Group

SCMA

VIVA

Trans group

Others

Media

5

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Overview of the media industry

Private consumption is the backbone for advertisement demand

Private consumption is a crucial part of Indonesia’s economy

Indonesia’s 1Q16 GDP growth picked up 4.9% YoY. Although 1Q16 GDP growth is below the 2-

year average of c. 5.0% YoY growth, at the same time, we note that 1Q16 GDP print was higher

than the 4.7% YoY growth in 1Q15. Given private consumption is a key growth driver for the

broader economy (accounting for c. 55% of Indonesia’s economic output), we judge private

consumption growth to be an important economic indicator for growth.

We suspect consumers now have greater purchasing power following the sharp decline in

inflation (average CPI: 4.3% YoY in 1Q16 vs. 6.4% YoY in FY15). However, contrary to market

expectations, private consumption growth remained sluggish in 1Q16 (4.9% YoY). Despite fatter

pockets for consumption, we judge that mid-to-higher income households are hesitant to spend.

We attribute this conservative spending to escalating uncertainties related to the macroeconomic

environment.

Nevertheless, we forecast consumption growth to pick up in 2Q16. Our view largely embeds the

Ramadan effect, school holiday and Idul Fitri festive. Furthermore, low inflationary pressures and

potential fund flows into Indonesia from the tax amnesty program should add more momentum

to private consumption, in our opinion. We retain our view that economic growth is likely to hinge

on private consumption. However, we remain positive on the broader economic growth outlook

given 1) strong willingness from the government to pace up its spending initiatives, 2)

implementation of multiple economic packages to bolster the sagging economy and 3)

elimination of bureaucratic hurdles for investments. Yet, we still think the backbone of Indonesia's

economic growth stems from private consumption, evidenced by President Jokowi’s efforts to

enhance the purchasing power.

Figure 4. Sluggish consumption growth despite low CPI Figure 5. Population is relatively young

Source: BPS, Daewoo Securities Research

Source: BPS, Daewoo Securities Research

4.4%

4.5%

4.6%

4.7%

4.8%

4.9%

5.0%

5.1%

5.2%

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16

(YoY)

26%17%

age 25-54,

42% 8%

7%

age 0-14

age 15-24

age 25-54

age 55-64

age 65+

Media

6

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Media advertisement is a proxy to consumption

We believe Indonesia’s long term growth remains intact, supported by our government’s actions

to boost public expenditure. In addition, young demographic profile (figure 5) and growing

population, higher education and improving infrastructure situation will collectively be key

catalysts for Indonesia’s long term economic outlook.

Given our positive long-term growth outlook for Indonesia, we firmly believe media companies

are likely to benefit as we expect increased demand for advertisement from various industries.

Media advertisement is an impersonal one way mass-communication related to products and/or

services which play an important role in enhancing sales and market share. Hence, we expect the

trend will continue to grow in tandem with consumption spending.

According to Media Partners Asia, Indonesia’s net advertising spending (including rate card

discounts and agency commission) will reach c. USD3,500mn in 2016F, where most of the

spending is expected to be allocated to TV and print media (figure 6). As >70% of advertising

spending is likely to be skewed towards TV, growing audiences for TV is the key determinant of TV

rate card.

Figure 6. Ad spend is focused on TV Figure 7. Free-to-air TV advertising

Source: Media Partners Asia, Daewoo Securities Research

Source: Media Partners Asia , Daewoo Securities Research

Low net Ad spend as % of GDP compared to other countries

Moreover, Indonesia’s net ad spend as a % of GDP is still relatively low compared to neighboring

countries at 0.2% in 2013 and the average price for 30 seconds prime-time spot is relatively cheap

(USD5,400/spot) compared to Australia (USD80,000/spot).

Figure 8. Net Ad spend as % of GDP (2013) Figure 9. Thirty seconds prime time spot

Source: Media Partners Asia, Daewoo Securities Research

Source: Media Partners Asia 2016, Daewoo Securities Research

80,000

5,400

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

USD/spot

0

500

1,000

1,500

2,000

2,500

3,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

USDmn

TV

Newspaper

Magazine

Online

Out-Of-Home advertising

Radio

0

500

1,000

1,500

2,000

2,500

3,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

(USDmn)

0.2%

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

0.8%

0.9%

1.0%

Media

7

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Prime time show on TV

TV operators are regulated under the Law number 32 of 2002 on Broadcasting (Law 32/2002)

dividing broadcasters into 1) public broadcasters, 2) private broadcasters, 3) community

broadcaster and 4) subscription-based broadcasters.

In the area of broadcasting, there are several provisions concerning the minimum requirement to

air local contents. For example, broadcast content of private and public TV broadcasters must

contain at least 60% of domestic programs. Therefore, Indonesian TV stations have set up in-

house production facilities to produce local contents. Popular programs which are aired on TV

stations are locally produced dramas which are aired during prime time.

Prime time in Indonesia is considered to be from 18:30 to 22:00. It is imperative for TV

broadcasters to air the most popular movie or the highest rated drama during prime time since it

lifts up the all-time audience shares. In addition, prime time shows are highly profitable since

clients take advantage of the prime time shows to advertise. MNCN’s top TV channel namely, RCTI,

generates around USD6,000 gross rate per episode. The price of an advertising slot is mostly

determined by the number of viewers, with upper ratings leading to higher rates.

Following the prime time hours, “adult” programs are allowed to be broadcasted. In addition,

there is also a midnight prime time during sahur (“pre-dawn meal” which refers to food consumed

early in the morning) during the month of Ramadhan. It usually takes place from 02:30 and end at

the Fajr prayer call which varies from 04:30 to 05:00 in the early morning.

Figure 10. Screen use during the day

Source: Millward Brown, Daewoo Securities Research

MNCN has recorded very strong audience share over the past couple of years (see figure 72),

which led the company to its premium rate card.

Figure 72. RCTI’s audience share has always been astonishing

Source: Nielsen, Daewoo Securities Research

RCTI has the highest power ratio

RCTI has the highest power ratio at 1.4x among all 11 nationwide FTA TV stations as of FY14.

Power ratio shows how well a media company converts ratings to revenue. Power ratio is used to

measure the companies’ revenue performance of a media company in comparison to the share of

audience that it controls. The three variables that are used to calculate include total market

revenue, the revenue of the media company itself, and % of audience share.

A higher power ratio is preferable because it indicates greater amount of revenue received from

the company's audience share. A low power ratio indicates that the company underutilizes its

capacity and there is more room for growth.

Figure 73. Power ratio of 11 nationwide FTA TV stations (as of FY 2014)

Source: Company data, Daewoo Securities Research

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

21.4

16.8

20.3

29.63

0

5

10

15

20

25

30

35

2013 average 2014 average 2015 average Average YT June 2016

SCTV

RCTI

IVM

MNCTV

GTV

Media

52

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

MNCN has integrated studio facilities

MNCN is the only TV operator that has integrated studio facilities located in one area (Kebon

Jeruk, namely MNC studio complex). The construction began in 2014 where MNCN utilized

USD250mn loans to build the four buildings. The new MNC studio complex started functioning in

July 2016, which means it is at the end of its large 3 year-capex period. MNCN is guiding its 2016F

capex for buildings and maintenance of USD60-70mn, and 2017F of USD10-20mn.

The integrated new studio complex which has four new buildings with a total of 28 new studios

and also equipped with HD rating equipment is believed to enhance the on-screen quality (better

lightning, audio sharpness, etc.) and have more production capacity. MNCN expects new studios

will help actors and actresses to with easier shooting with close proximity compared to scattered

studios.

Figure 74. MNC’s lightning equipment

Source: Daewoo Securities Research

Figure 75. MNC studio complex Figure 76. MNC studio

Source: Daewoo Securities Research

Source: Daewoo Securities Research

Media

53

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Figure 77. MNC studio Figure 78. MNC studio

Source: Daewoo Securities Research

Source: Daewoo Securities Research

Figure 79. MNC studio Figure 80. MNC studio

Source: Daewoo Securities Research

Source: Daewoo Securities Research

More clarity on PT Berkah’s dispute

The dispute over PT Berkah and Ibu Tutut has been the noise over MNCN’s stock price throughout

2014-2015. Yet, in April 2016, the Supreme Court (MA) finally issued a ruling regarding the dispute

between PT Berkah Karya Bersama (PT Berkah) and Siti Hardiyanti Rukmana. The Supreme Court

ruled that Harry Tanoesoedibyo’s Berkah Karya Bersama as the rightful owner of 75% stake in

MNC TV (previously TPI). While Ibu Tutut’s legal team states that there is no verdict on the appeal.

We believe the overhang of the dispute has faded and the ruling is finally in favor of MNC.

Media

54

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Media Nusantara Citra (Valuations)

We initiate our coverage on MNCN with a trading buy rating and a target price of IDR2,700,

implying 27.5x 2016F P/E. Our target price of IDR2,700 was derived using a blended calculation of

target P/E at 28x and Discounted Cash Flow (DCF) method with 10-year time span.

Our WACC assumption of 10.5% is derived from our estimates on risk free rate (Rf) of 7%, market

risk premium (MRP) of 5%, a terminal growth rate of 3% and equity beta of 1.0x. We believe the

reduction in cost of capital tracks the decline in Indonesian bond yields which further support our

DCF target price.

We like MNCN on the back of its: 1) Strong audience viewers’ performance, 2) lower capex as

MNCN has completed the construction of its integrated studio facilities 3) premium rate card

charged on the back of its high audience share.

Table 7. DCF Assumption Table

Item Details

Cost of Equity 12%

Risk free rate 7.0%

Beta 1.00

Equity risk premium 5%

WACC 10.5%

Terminal growth rate 3%

After tax Cost of Debt 6.84%

Total PV of FCF 16,348

PV of TV 22,160

Total PV of FCF and TV 38,508

Cash 2013 1,967

Debt 2013 3,866

Equity value (in IDRbn) 37,770

Equity value/share 2,646

Source: Daewoo Securities Research

Figure 81. MNCN PE Band

Source: Daewoo Securities Research

-1 Std Dev

Avg PER

+1 Std Dev

-2 Std Dev

+2 Std Dev

10

12

14

16

18

20

22

24

26

28

30

Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

( x )

Media

55

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Media Nusantara Citra (Ticker MNCN IJ/ Buy/ TP: IDR2,700)

Table 8. Forecast and valuations

2014 2015 2016F 2017F

Revenue (IDRbn) 6,666 6,445 7,015 7,925

EBITDA (IDRbn) 2,772 2,447 2,739 3,087

Net profit (IDRbn) 1,761 1,186 1,401 1,760

EPS (IDR/share) 123 83 98 123

DPS (IDR/share) 35 62 42 49

ROE (%) 19.7% 13.2% 14.2% 16.6%

Dividend yield (%) 1.6% 2.8% 1.9% 2.2%

P/E ratio (x) 17.8 26.5 22.4 17.8

P/BV ratio (x) 3.5 3.5 3.1 2.9

EV/EBITDA (x) 11.3 12.7 11.4 10.1

Source: Daewoo Securities Research

Table 9. Income statement projection

2014 2015 2016F 2017F

Revenue 6,666 6,445 7,015 7,925

COGS (2,813) (2,861) (3,037) (3,431)

Gross Profit 3,853 3,584 3,978 4,494

Opex (1,251) (1,390) (1,513) (1,709)

Operating Profit 2,602 2,194 2,465 2,785

Other income/(expenses) (54) (506) (492) (340)

Profit before income tax 2,542 1,681 1,965 2,437

Income tax expenses (660) (404) (472) (585)

Minority interest (121) (91) (91) (91)

Net profit 1,761 1,186 1,401 1,760

EBITDA 2,772 2,447 2,739 3,087

Source: Daewoo Securities Research

Media

56

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Table 10. Balance sheet projection

IDR bn 2014 2015 2016F 2017F

Assets

Cash and equivalents 3,019 1,525 3,128 3,184

Receivables 2,994 3,020 2,907 3,330

Inventories 1,635 1,593 1,447 1,721

Others 1,022 1,588 995 1,263

Total current assets 8,670 7,727 8,476 9,498

Fixed assets - net 2,659 4,145 4,799 4,762

Long term investments 1,165 1,144 1,144 1,144

Others 701 1,017 816 839

Total non-current assets 4,940 6,748 7,200 7,186

Total assets 13,610 14,475 15,676 16,684

Liabilities and equity

Short-term bank loans and

current maturities

55 117 117 117

Trade payables 403 511 570 629

Others current liabilities 434 412 514 568

Total current liabilities 892 1,040 1,201 1,313

Long term debt 3,135 3,649 3,749 3,949

Others 182 219 229 225

Total non-current liabilities 3,318 3,868 3,978 4,174

Total liabilities 4,210 4,908 5,178 5,487

Minority interests 485 601 601 601

Shareholders' equity 8,916 8,966 9,897 10,596

Source: Daewoo Securities Research

Media

57

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Table 11. Cash flow statement projection

IDRbn 2014 2015 2016F 2017F

CF from operation

Net profit 1,761 1,186 1,401 1,760

Depreciation/amortization 170 253 274 302

Change in working capitals (812) 123 319 (639)

Others (376) (588) 695 (214)

CF from operation 743 974 2,690 1,209

CF from Investments

Net capex (1,743) (979) (961) (300)

Others (1,018) (321) 201 (23)

CF from investments (2,761) (1,300) (760) (322)

CF from financing activity

Increase/(decrease) in debt 2,667 575 100 200

Increase/(decrease) in equity 368 (3) - -

Dividend payments (497) (888) (593) (701)

Others 30 (109) 132 (364)

CF from financing activity 2,568 (425) (361) (865)

Net changes in cash 551 (752) 1,568 22

Source: Daewoo Securities Research

Table 12. Key Ratios

2014 2015 2016F 2017F

Growth (%)

Revenue 2.2% -3.3% 8.8% 13.0%

EBITDA 2.3% -11.7% 11.9% 12.7%

Net profit 4.1% -32.7% 18.2% 25.6%

Profitability (%)

Gross margin 57.8% 55.6% 56.7% 56.7%

Operating margin 39.0% 34.0% 35.1% 35.1%

EBITDA margin 41.6% 38.0% 39.0% 39.0%

Net margin 26.4% 18.4% 20.0% 22.2%

ROE 19.7% 13.2% 14.2% 16.6%

ROA 12.9% 8.2% 8.9% 10.5%

Leverage (X)

Current ratio 9.7 7.4 7.1 7.2

Quick ratio 6.7 4.4 5.0 5.0

Debt to equity 0.4 0.4 0.4 0.4

Net debt to equity 0.0 0.2 0.1 0.1

Interest coverage 44.7 11.2 8.3 9.0 Source: Daewoo Securities Research

Media

58

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Risks to our call

The emergence of online advertisement. We believe growing internet penetration trend will

determine the growth of digital advertisement, which would be the main competitor for FTA TV.

However, we think the digital advertising trend will not be an immediate risk for TV operators

given that Indonesia is still lack of the broadband infrastructure.

Unexpected regulatory risks. Investors may have to anticipate unexpected risks such as

restrictions on broadcasting operations, licenses, transition to digital TV, etc.

Government’s stance on tobacco control. We think that government’s regulation on cigarettes

advertisement is quite a huge risk for TV companies as they contribute sizeable portion of TV

companies’ revenue. For example, broadcasting tobacco advertising on television is only allowed

from 9:30pm until 5:00am, and smoking warnings are also shown at the end of the advertisement,

such as "Smoking can cause mouth cancer, heart attack, impotency and pregnancy and fetal

disorders". Since 2014, the Indonesian government halted the branding of cigarettes as "light" or

"mild" on smoking packages and decided to place graphic images of the adverse long-term

effects of excessive smoking. Currently, tobacco advertising is still allowed, but showing the

cigarette packaging is forbidden.

Global and macroeconomic factors. As TV companies generate revenue from FMCG companies,

there are several factors that would determine how they spend their A&P expense. Economic

growth, commodity prices, inflation rate, Federal Reserve’s policy rate as well as the rupiah

exchange rate are key determinants to the FMCG’s S&P spending. We believe any significant

changes to the macroeconomic backdrop may significantly alter the strategies of FMCG

companies A&P spending.

Media

59

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

APPENDIX 1

Important Disclosures & Disclaimers

Analyst Certification

The research analysts who prepared this report (the “Analysts”) are registered with and are subject to Indonesian securities regulations. They are neither

registered as research analysts in any other jurisdiction nor subject to the laws and regulations thereof. Opinions expressed in this publication about the

subject securities and companies accurately reflect the personal views of the Analysts primarily responsible for this report. PT Daewoo Securities Indonesia

policy prohibits its Analysts and members of their households from owning securities of any company in the Analyst’s area of coverage, and the Analysts do

not serve as an officer, director or advisory board member of the subject companies. Except as otherwise specified herein, the Analysts have not received

any compensation or any other benefits from the subject companies in the past 12 months and have not been promised the same in connection with this

report. No part of the compensation of the Analysts was, is, or will be directly or indirectly related to the specific recommendations or views contained in

this report but, like all employees of PT Daewoo Securities Indonesia, the Analysts receive compensation that is impacted by overall firm profitability, which

includes revenues from, among other business units, the institutional equities, investment banking, proprietary trading and private client division. At the

time of publication of this report, the Analysts do not know or have reason to know of any actual, material conflict of interest of the Analyst or PT Daewoo

Securities Indonesia except as otherwise stated herein.

Disclaimers

This report is published by PT Daewoo Securities Indonesia (“Daewoo”), a broker-dealer registered in the Republic of Indonesia and a member of the

Indonesian Stock Exchange. Information and opinions contained herein have been compiled from sources believed to be reliable and in good faith, but such

information has not been independently verified and Daewoo makes no guarantee, representation or warranty, express or implied, as to the fairness,

accuracy, completeness or correctness of the information and opinions contained herein or of any translation into English from the Indonesian language. If

this report is an English translation of a report prepared in the Indonesian language, the original Indonesian language report may have been made available

to investors in advance of this report. Daewoo, its affiliates and their directors, officers, employees and agents do not accept any liability for any loss arising

from the use hereof. This report is for general information purposes only and it is not and should not be construed as an offer or a solicitation of an offer to

effect transactions in any securities or other financial instruments. The intended recipients of this report are sophisticated institutional investors who have

substantial knowledge of the local business environment, its common practices, laws and accounting principles and no person whose receipt or use of this

report would violate any laws and regulations or subject Daewoo and its affiliates to registration or licensing requirements in any jurisdiction should receive

or make any use hereof. Information and opinions contained herein are subject to change without notice and no part of this document may be copied or

reproduced in any manner or form or redistributed or published, in whole or in part, without the prior written consent of Daewoo. Daewoo, its affiliates and

their directors, officers, employees and agents may have long or short positions in any of the subject securities at any time and may make a purchase or

sale, or offer to make a purchase or sale, of any such securities or other financial instruments from time to time in the open market or otherwise, in each

case either as principals or agents. Daewoo and its affiliates may have had, or may be expecting to enter into, business relationships with the subject

companies to provide investment banking, market-making or other financial services as are permitted under applicable laws and regulations. The price and

value of the investments referred to in this report and the income from them may go down as well as up, and investors may realize losses on any

investments. Past performance is not a guide to future performance. Future returns are not guaranteed, and a loss of original capital may occur

Distribution

United Kingdom: This report is being distributed by Daewoo Securities (Europe) Ltd. in the United Kingdom only to (i) investment professionals falling within

Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”), and (ii) high net worth companies and other

persons to whom it may lawfully be communicated, falling within Article 49(2)(A) to (E) of the Order (all such persons together being referred to as “Relevant

Persons”). This report is directed only at Relevant Persons. Any person who is not a Relevant Person should not act or rely on this report or any of its

contents.

United States: This report is distributed in the U.S. by Daewoo Securities (America) Inc., a member of FINRA/SIPC, and is only intended for major institutional

investors as defined in Rule 15a-6(b)(4) under the U.S. Securities Exchange Act of 1934. All U.S. persons that receive this document by their acceptance

thereof represent and warrant that they are a major institutional investor and have not received this report under any express or implied understanding that

they will direct commission income to Daewoo or its affiliates. Any U.S. recipient of this document wishing to effect a transaction in any securities discussed

herein should contact and place orders with Daewoo Securities (America) Inc., which accepts responsibility for the contents of this report in the U.S. The

securities described in this report may not have been registered under the U.S. Securities Act of 1933, as amended, and, in such case, may not be offered or

sold in the U.S. or to U.S. persons absent registration or an applicable exemption from the registration requirements.

Hong Kong: This document has been approved for distribution in Hong Kong by Daewoo Securities (Hong Kong) Ltd., which is regulated by the Hong Kong

Securities and Futures Commission. The contents of this report have not been reviewed by any regulatory authority in Hong Kong. This report is for

distribution only to professional investors within the meaning of Part I of Schedule 1 to the Securities and Futures Ordinance of Hong Kong (Cap. 571, Laws

of Hong Kong) and any rules made thereunder and may not be redistributed in whole or in part in Hong Kong to any person.

All Other Jurisdictions: Customers in all other countries who wish to effect a transaction in any securities referenced in this report should contact Daewoo or

its affiliates only if distribution to or use by such customer of this report would not violate applicable laws and regulations and not subject Daewoo and its

affiliates to any registration or licensing requirement within such jurisdiction.

Stock Ratings Industry Ratings

Buy : Relative performance of 20% or greater Overweight : Fundamentals are favorable or improving

Trading Buy : Relative performance of 10% or greater, but with volatility Neutral : Fundamentals are steady without any material changes

Hold : Relative performance of -10% and 10% Underweight : Fundamentals are unfavorable or worsening

Sell : Relative performance of -10%

* Our investment rating is a guide to the relative return of the stock versus the market over the next 12 months.

* Although it is not part of the official ratings at Daewoo Securities, we may call a trading opportunity in case there is a technical or short-term material

development.

* The target price was determined by the research analyst through valuation methods discussed in this report, in part based on the analyst’s estimate of

future earnings.

* The achievement of the target price may be impeded by risks related to the subject securities and companies, as well as general market and economic

conditions.

Disclosures

As of the publication date, PT Daewoo Securities Indonesia and/or its affiliates do not have any special interest with the subject company and do not own

1% or more of the subject company's shares outstanding.

Media

60

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Daewoo Securities International Network

PT. Daewoo Securities Indonesia Daewoo Securities (Hong Kong) Ltd. Daewoo Securities (America) Inc.