Medicare and Medicaid Audit Sampling Strategies Developing Sampling Plans and Challenging Flawed CMS Audit Samples Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10. TUESDAY, AUGUST 14, 2012 Presenting a live 90-minute webinar with interactive Q&A Anna M. Grizzle, Member, Bass Berry & Sims, Nashville, Tenn. Patricia L. Maykuth, Ph.D, President, Research Design Associates, Decatur, Ga.

Transcript

Medicare and Medicaid Audit Sampling Strategies Developing Sampling Plans and Challenging Flawed CMS Audit Samples

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

For CLE purposes, please let us know how many people are listening at your

location by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number of

attendees at your location

• Click the word balloon button to send

FOR LIVE EVENT ONLY

Medicare and Medicaid Audit Sampling Strategies

Anna M. Grizzle

Partner

Bass, Berry & Sims PLC

Patricia Maykuth, Ph.D.

President

Research Design Associates, Inc.

August 14, 2012

Agenda

• When is statistical sampling and extrapolation used?

• What is the legal basis for statistical sampling and extrapolation?

• How is statistical sampling and extrapolation performed?

• How can I defend against extrapolated overpayment results?

5

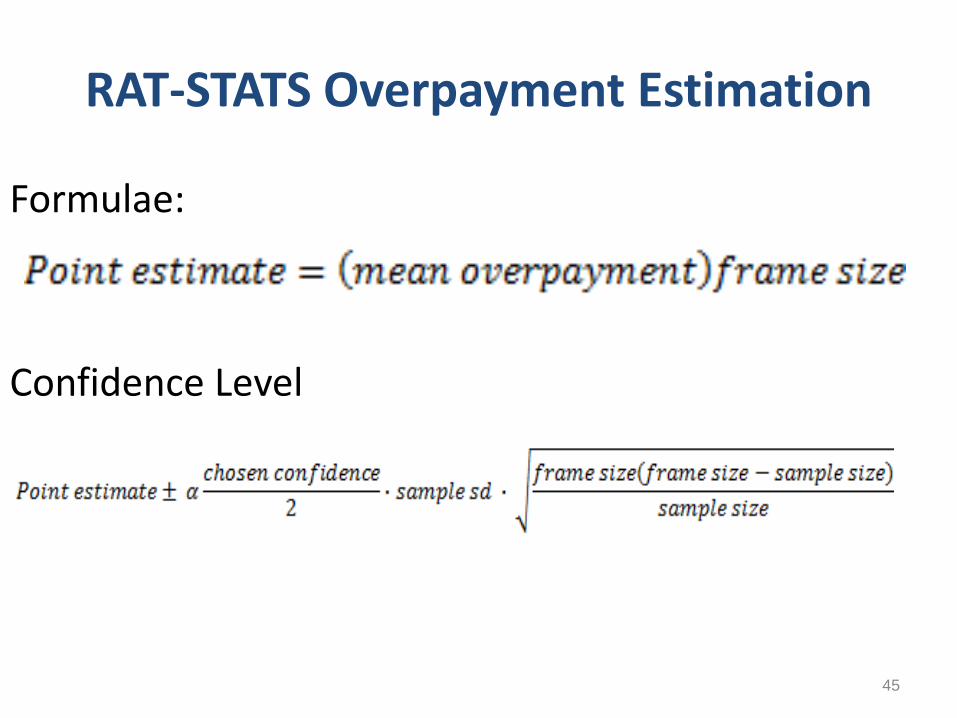

Use of Statistical Sampling for Overpayment Estimation

• Acceptable tool in different audits: Medicare, Medicaid, tax, financial statements, etc.

• Appropriate when records are too voluminous for individual review

• Used in Medicare overpayment reviews since the 1970’s

6

Use of Statistical Sampling for Overpayment Estimation

• CMS overpayment audit

• OIG self-disclosure protocol

• Internal compliance audit

7

Legal Basis for Statistical Sampling for Overpayment Estimation

“The use of statistical sampling to project an overpayment. . . does not deny a provider or supplier due process. Neither the statute nor regulations require that a case-by-case review be conducted in order to determine that a provider or supplier has been overpaid and to determine the amount of overpayment.”

HCFA Ruling 86-1

8

Legal Basis for Statistical Sampling for Overpayment Estimation

Statistical sampling does not violate due process “so long as extrapolation is made from a representative sample and is statistically significant.”

Chaves County Home Health Service, Inc. v. Sullivan, 931 F.2d 914 (D.C. Cir. 1991), cert. denied, 402 U.S. 1091 (1992).

9

Legal Basis for Medicare Statistical Sampling and Extrapolation

A Medicare contractor may not use extrapolation to determine overpayment amounts . . . unless . . .

– There is a sustained or high level of payment error; or

– Documented educational intervention has failed to correct the payment error

42 U.S.C. §1395ddd(f)(3)

10

Legal Basis for Medicare Statistical Sampling and Extrapolation

• Sustained or high level of payment error can be determined by: – Error rate determinations by MR unit, ZPIC

– Probe samples

– Data analysis

– Provider/supplier history

– Information from law enforcement investigations

– Allegations of wrongdoing by current or former employees of provider or supplier

– Audits or evaluations conducted by the OIG

Source: Chapter 8 – Benefit Integrity; Medicare Program Integrity Manual; available at:

http://www.cms.gov/manuals/downloads/pim83c08.pdf (Previously found in Chapter 3) 11

Legal Basis for Medicaid Statistical Sampling and Extrapolation

• Dictated by state law

• If no explicit authority, look to due process requirements

13

Numbers vs. Statistics

• Numbers can readily be manipulated and outcomes understood through the use of simple math: addition, subtraction, multiplication, multiplication and division e.g., %s, differences, sums and averages.

• Statistics is branch of applied math concerned with the collection and interpretation of quantitative data and the use of probability theory to estimate universe parameters e.g. correlations, t-tests and point estimates

14

MPIM Requirements

• Key Rules

– Obtain and properly execute “probability sample”

– Keep data and records so work can be replicated

• More content and direction given in RAT-STATS Manuals and standard of care expected of statisticians under Generally Accepted Statistics Procedures and Policies (“GASPP”)

15

Validity Sample

If a particular probability sample design is properly executed, i.e., defining the universe, the frame, the sampling units, using proper randomization, accurately measuring the variables of interest, and using the correct formulas for estimation, then assertions that the sample and its resulting estimates are “not statistically valid” cannot legitimately be made. In other words, a probability sample and its results are always “valid.” MPIM § 8.4.2

16

“Always Valid” Does Not Mean Results Cannot Be Challenged

Rather the “always valid” refers to the idea that internal operation of a statistical process which, when executed, will (with respect to its mathematical assumptions) yield internally consistent results.

The concept of statistically “valid” includes the understanding that there is an expectation of error.

“Valid” results include expectation of error: wrong 10 times in 100, precision demonstrated inaccuracy, validly rejecting hypothesis.

17

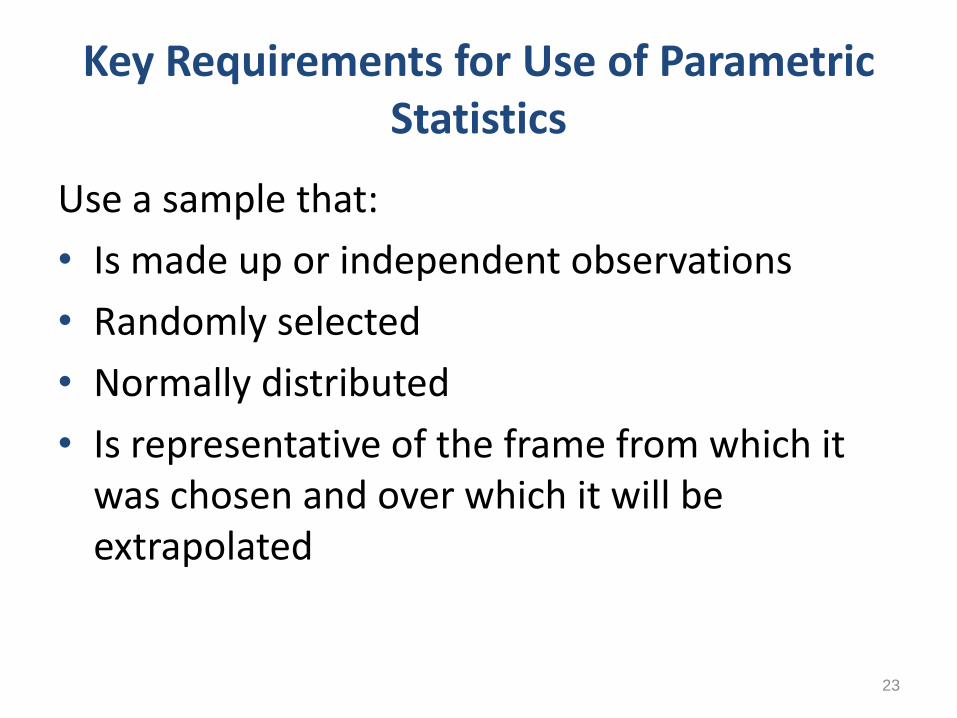

Valid Outcomes Require Properly

• defined universe

• defined the frame

• defined sampling units

• use proper randomization

• Accurate measuring the variables of interest

• using the correct formulas for estimation

• tests of key assumptions

• accurate reporting of actual findings

18

Typical Problems with Extrapolation

Sample size, not associated with precision or confidence

Incorrect use of formulas

Use of wrong formulas - choose wrong method

Use of inapplicable methodology – simple, stratified, cluster, multi-stage

Non-representative sample

Fail to meet key assumptions of statistic – math basis of statistic

Exclusion of zero paid claims

Accuracy outside of recommended range – too little precision

Reporting precision and/or confidence levels that are wrong

19

Unacceptable Departure From GASPP

• too excessive a departure from even a lenient interpretation of the MPIM

• major departures from methodology

• non-trivial mistakes in

audit definition

application of method

• non-sampling errors

• lack of statistical oversight and quality control

• Is representative of the frame from which it was chosen and over which it will be extrapolated

23

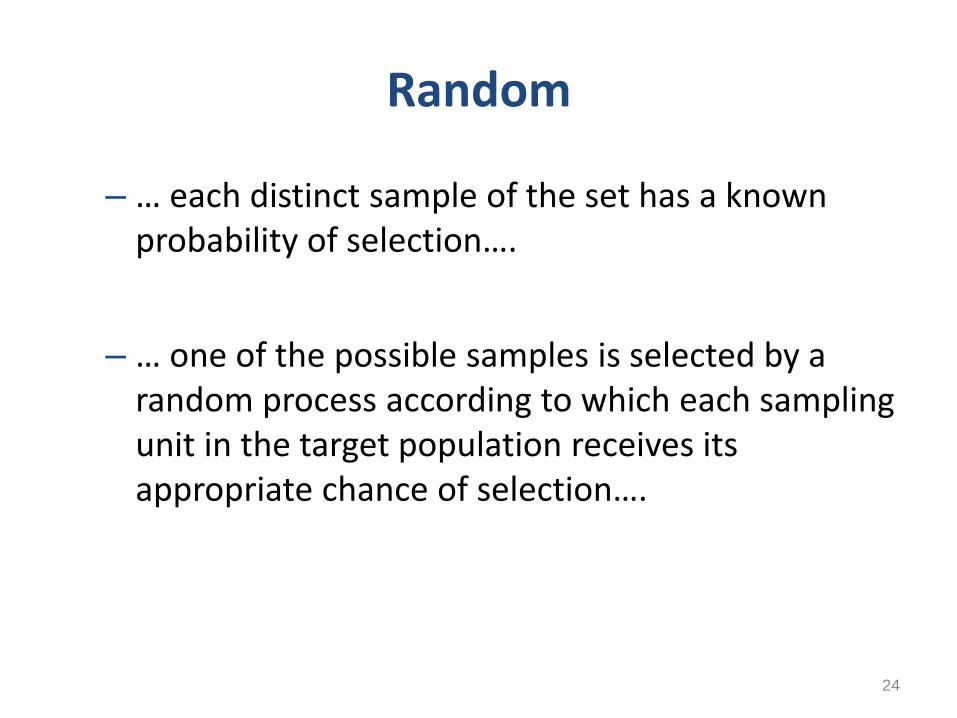

Random

– … each distinct sample of the set has a known probability of selection….

– … one of the possible samples is selected by a random process according to which each sampling unit in the target population receives its appropriate chance of selection….

Statistical sampling is used to calculate and project (i.e., extrapolate) the amount of overpayment(s) made on claims. The Medicare Prescription Drug, Improvement, and Modernization Act of 2003 (MMA), mandates that before using extrapolation to determine overpayment amounts to be recovered by recoupment, offset or otherwise, there must be a determination of sustained or high level of payment error, or documentation that educational intervention has failed to correct the payment error. By law, the determination that a sustained or high level of payment error exists is not subject to administrative or judicial review. MPIM, § 8.4.1.2

29

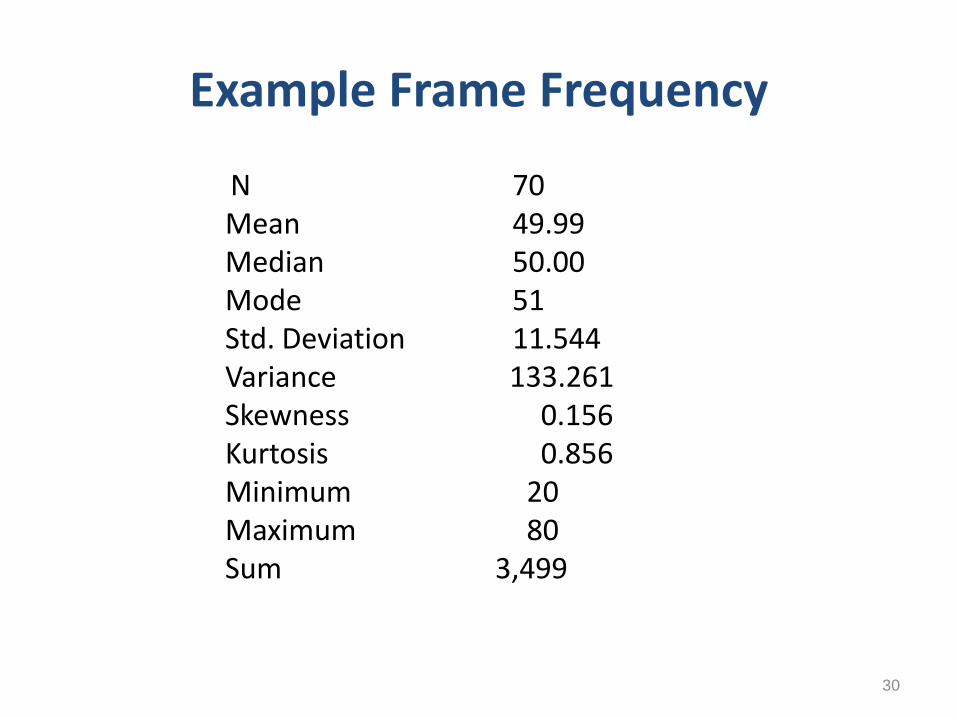

Example Frame Frequency

N 70 Mean 49.99 Median 50.00 Mode 51 Std. Deviation 11.544 Variance 133.261 Skewness 0.156 Kurtosis 0.856 Minimum 20 Maximum 80 Sum 3,499

30

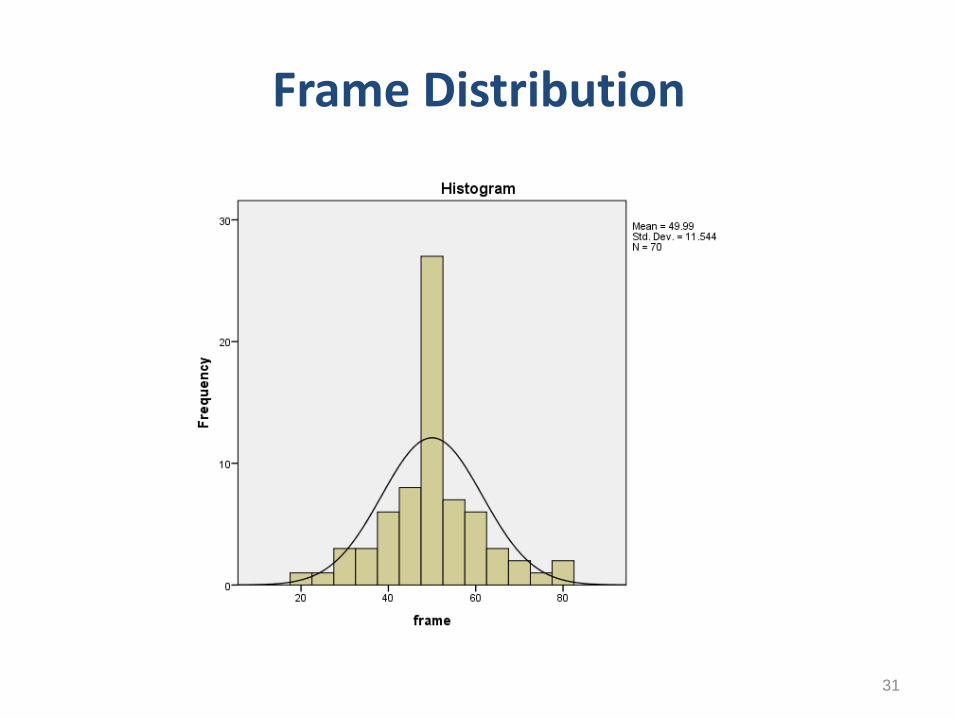

Frame Distribution

31

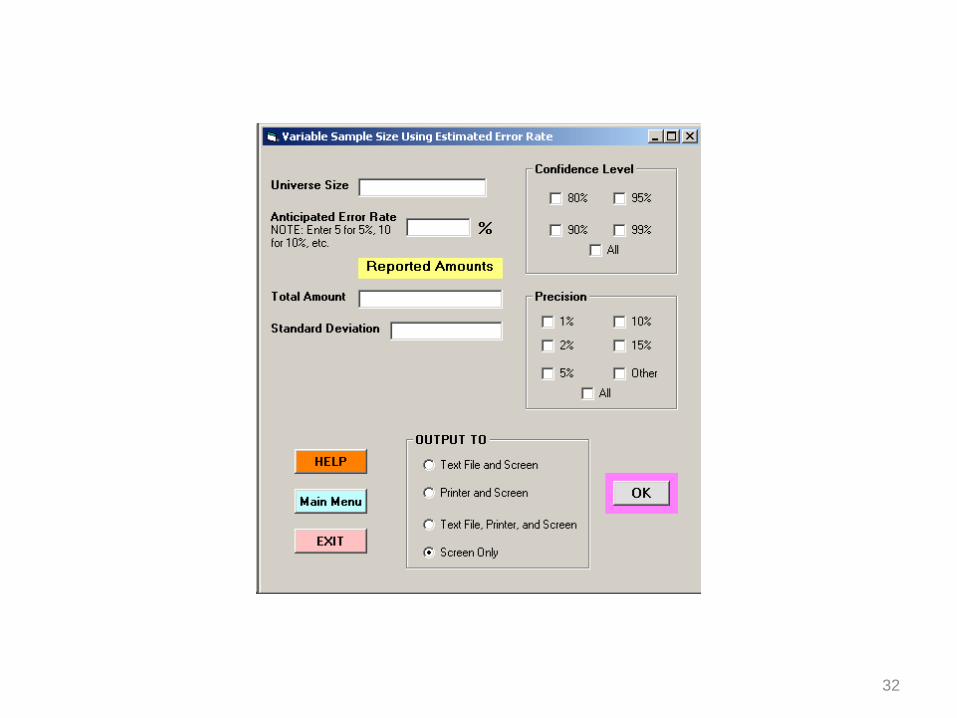

32

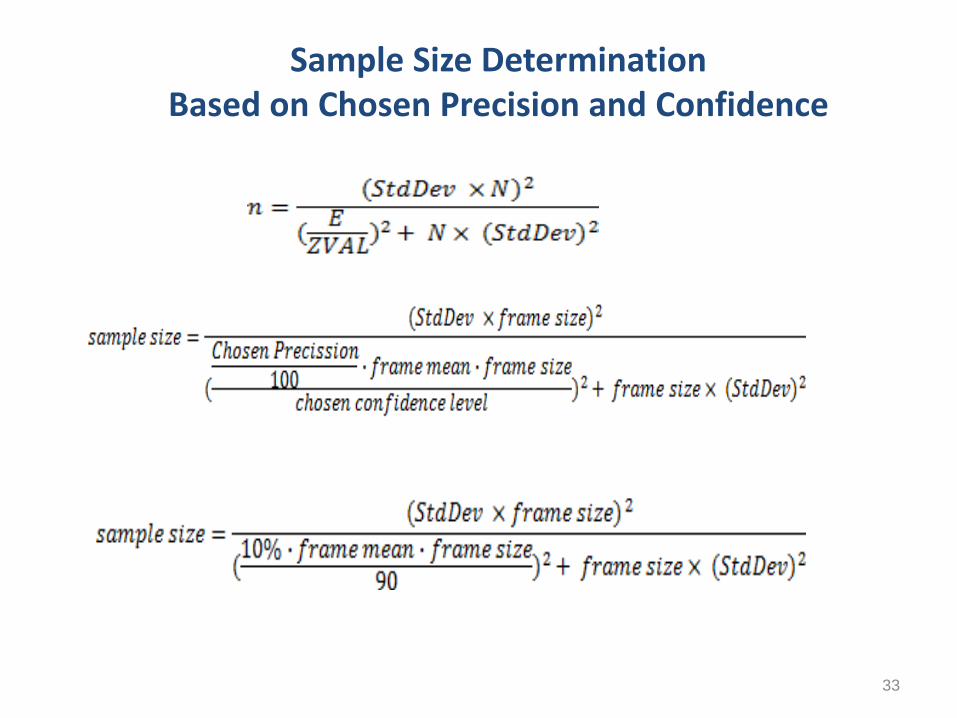

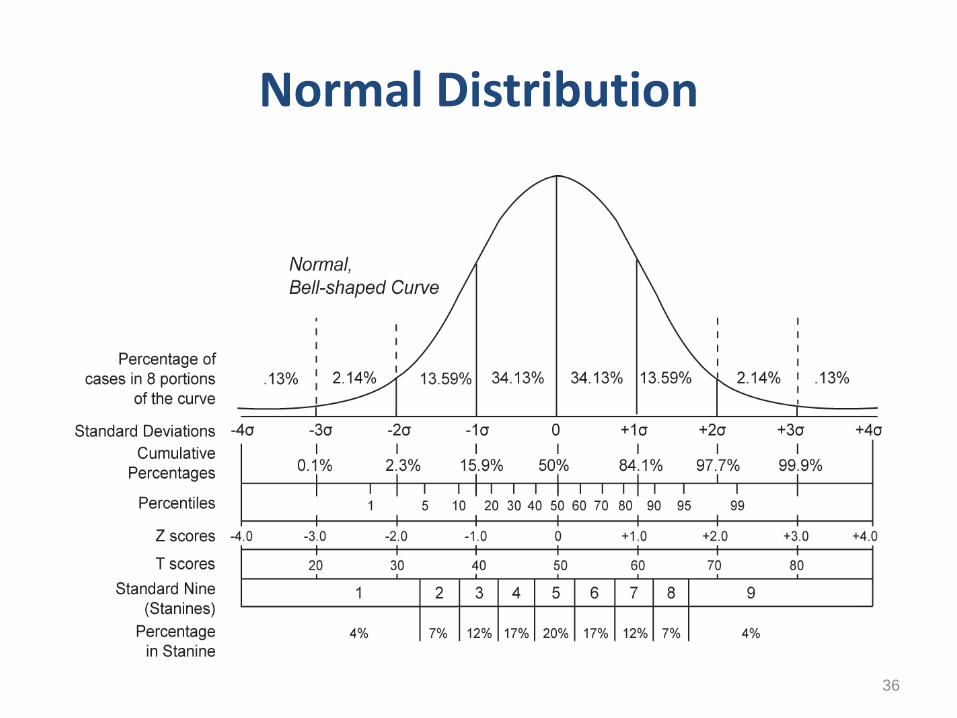

Sample Size Determination Based on Chosen Precision and Confidence

Probability theory mathematics allow the comparison of sample data to a described distribution (in this case a “normal distribution”) to describe the pattern of that data. Many inferential statistics are based on the reality that the data being analyzed were “normally distributed”

35

Normal Distribution

36

This is the standard normal distribution’s

mathematical formula.

37

Basic statistical terminology

Mean (average) the arithmetic sum of all scores divided by the number of cases

Median – the middle most real score

Mode the score that occurs most frequently in the data set (does not have to be unique – sometimes more than 1 value is equally likely)

Measures of variability (variance, standard deviation, precision and confidence interval)

38

Lower Confidence Level Upper Confidence Level

Point Estimate

39

40

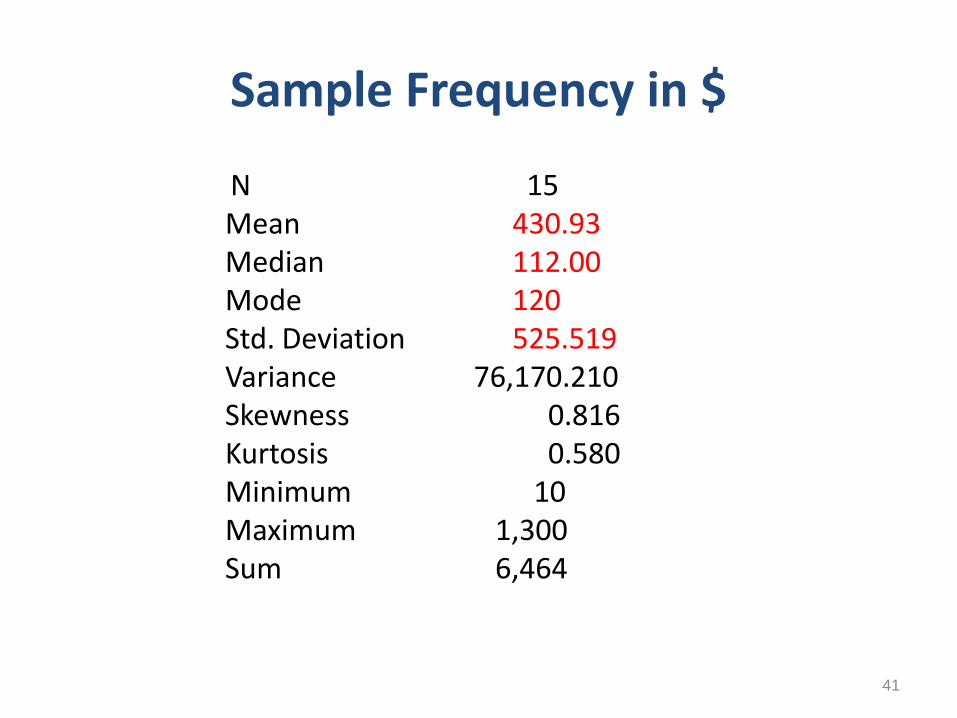

Sample Frequency in $

N 15 Mean 430.93 Median 112.00 Mode 120 Std. Deviation 525.519 Variance 76,170.210 Skewness 0.816 Kurtosis 0.580 Minimum 10 Maximum 1,300 Sum 6,464

41

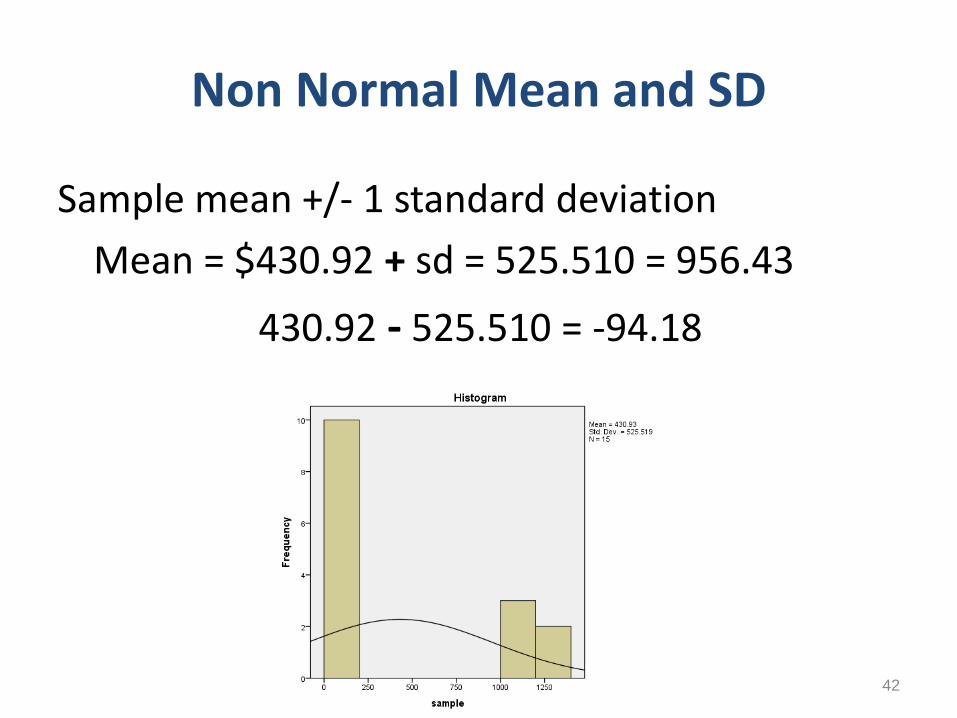

Non Normal Mean and SD

Sample mean +/- 1 standard deviation

Mean = $430.92 + sd = 525.510 = 956.43

430.92 - 525.510 = -94.18

42

Posterior Distribution

• Sample selected from amount paid to provider

• Sample analyzed using overpayment data

• Never know up front what the overpayment amount is going to be unless – There is a known history of overpayment dollar

amount

– Conduct a probe

• Overpayment amounts must meet criteria for using parametric statistic or the confidence levels are destroyed.

43

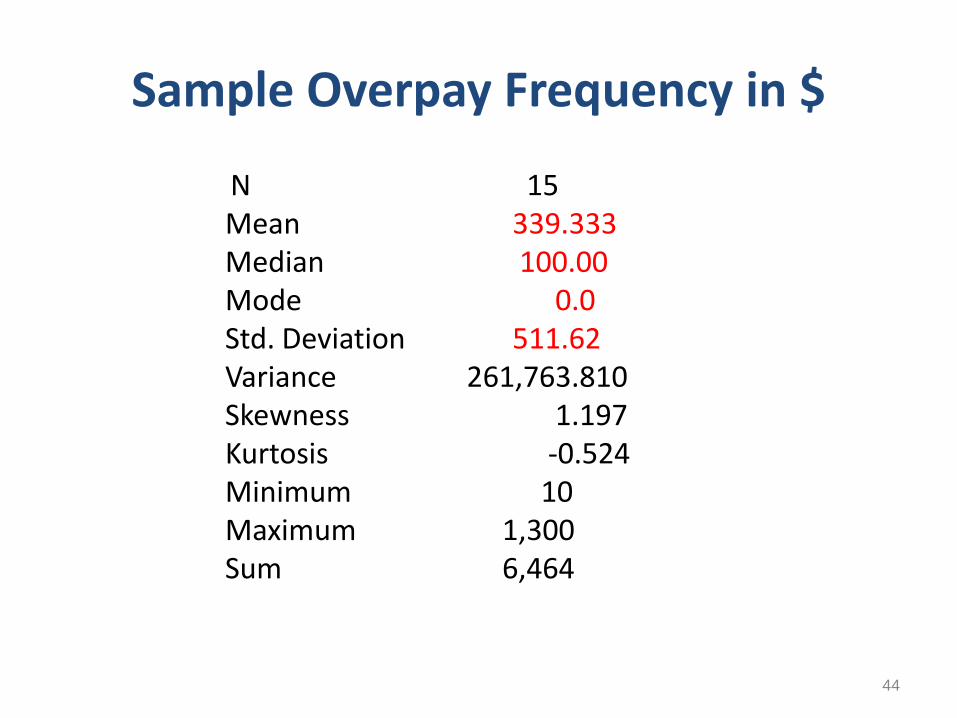

Sample Overpay Frequency in $

N 15 Mean 339.333 Median 100.00 Mode 0.0 Std. Deviation 511.62 Variance 261,763.810 Skewness 1.197 Kurtosis -0.524 Minimum 10 Maximum 1,300 Sum 6,464