14

1 Meghmani Organics Limited Corporate Presentation

1

Meghmani Organics Limited

Corporate Presentation

2

Corporate profile

3

At a glance

• Specializes in the manufacture of green & blue pigment products and a broad spectrum of commonly used generic pesticides

• Cost advantage due to India location – manufacturing base in

Gujarat

• Extensive global presence with markets in the US, Europe, Latin America and the Asia Pacific - approximately 70% from exports

• Established brand names

• 130 agrochemicals products registrations worldwide with more than 440 registrations in the pipeline

• Integrated manufacturing facilities and strong focus on R&D

• Listing:

– 2004: First Indian company to be listed on SGX Mainboard

– 2007: Obtained dual listing on Indian bourses, NSE and BSE

Established in 1986, Meghmani Organics is a leading pigments

and agrochemicals manufacturer in India

4

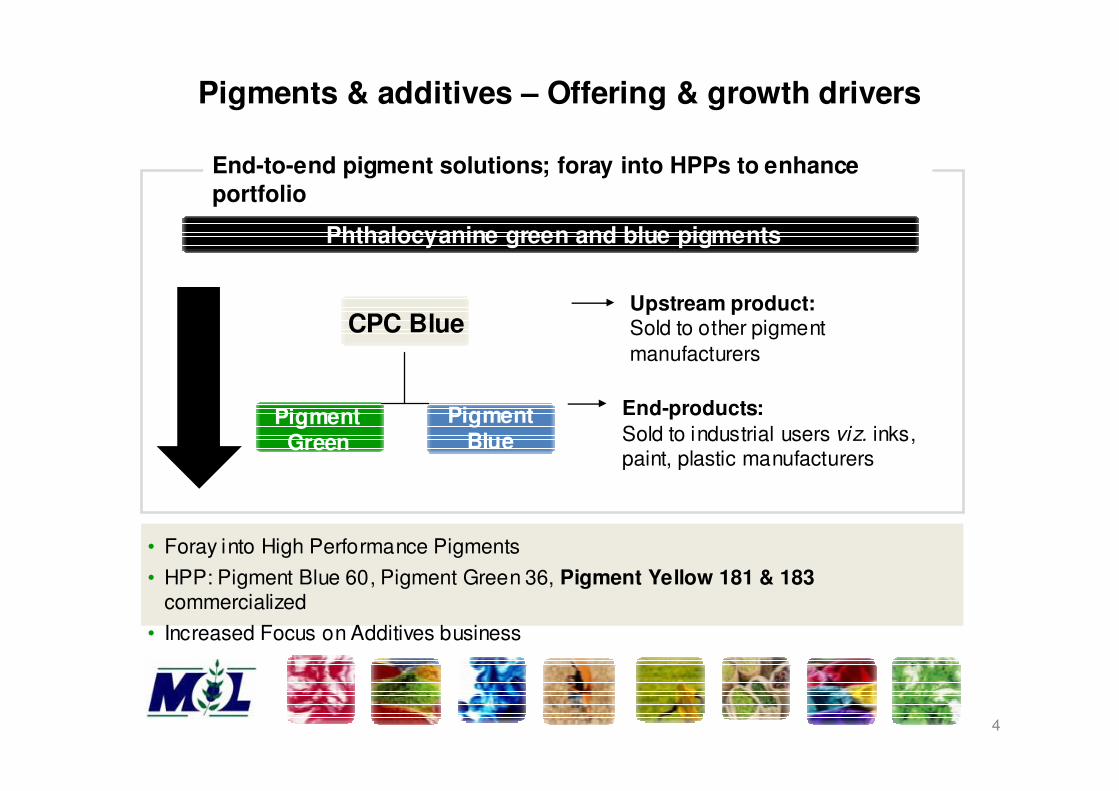

Pigments & additives – Offering & growth drivers

Phthalocyanine green and blue pigments

Upstream product:Sold to other pigment

manufacturers

End-products:

Sold to industrial users viz. inks, paint, plastic manufacturers

CPC Blue

• Foray into High Performance Pigments

• HPP: Pigment Blue 60, Pigment Green 36, Pigment Yellow 181 & 183commercialized

• Increased Focus on Additives business

End-to-end pigment solutions; foray into HPPs to enhance

portfolio

Pigment Green

Pigment Blue

5

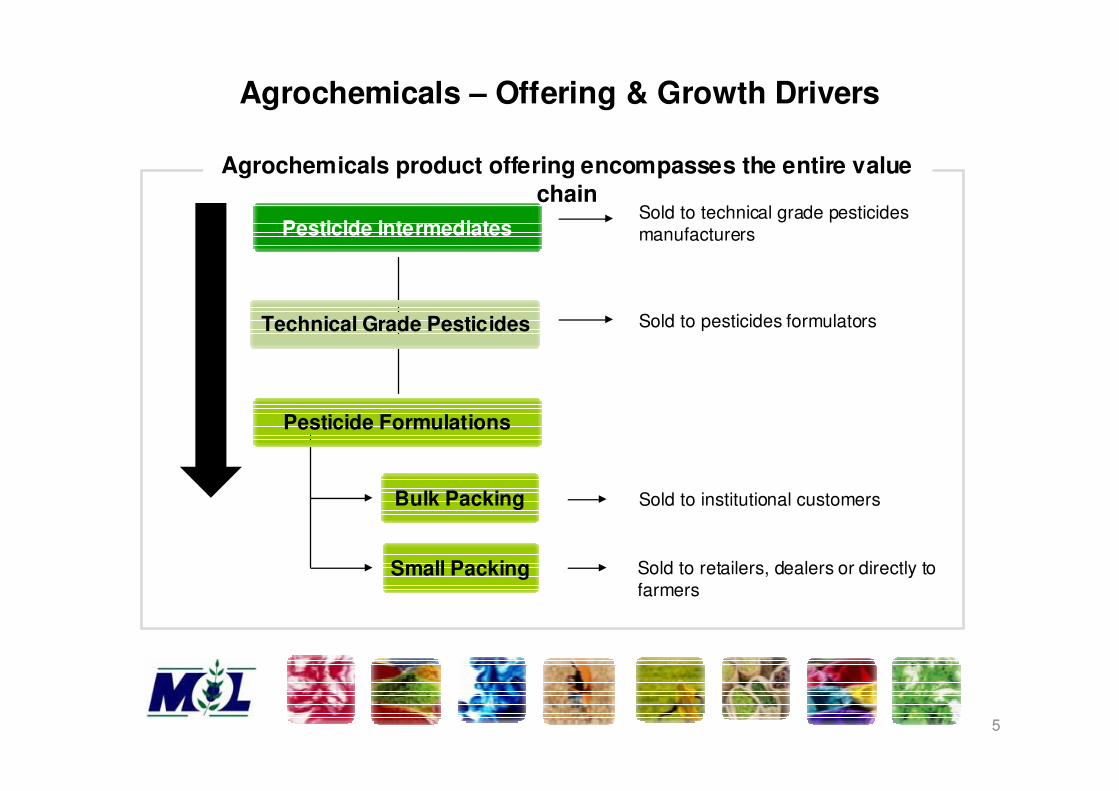

Pesticide Intermediates

Technical Grade Pesticides

Pesticide Formulations

Sold to technical grade pesticides manufacturers

Sold to pesticides formulators

Small Packing

Bulk Packing Sold to institutional customers

Sold to retailers, dealers or directly to farmers

Agrochemicals – Offering & Growth Drivers

Agrochemicals product offering encompasses the entire value

chain

6

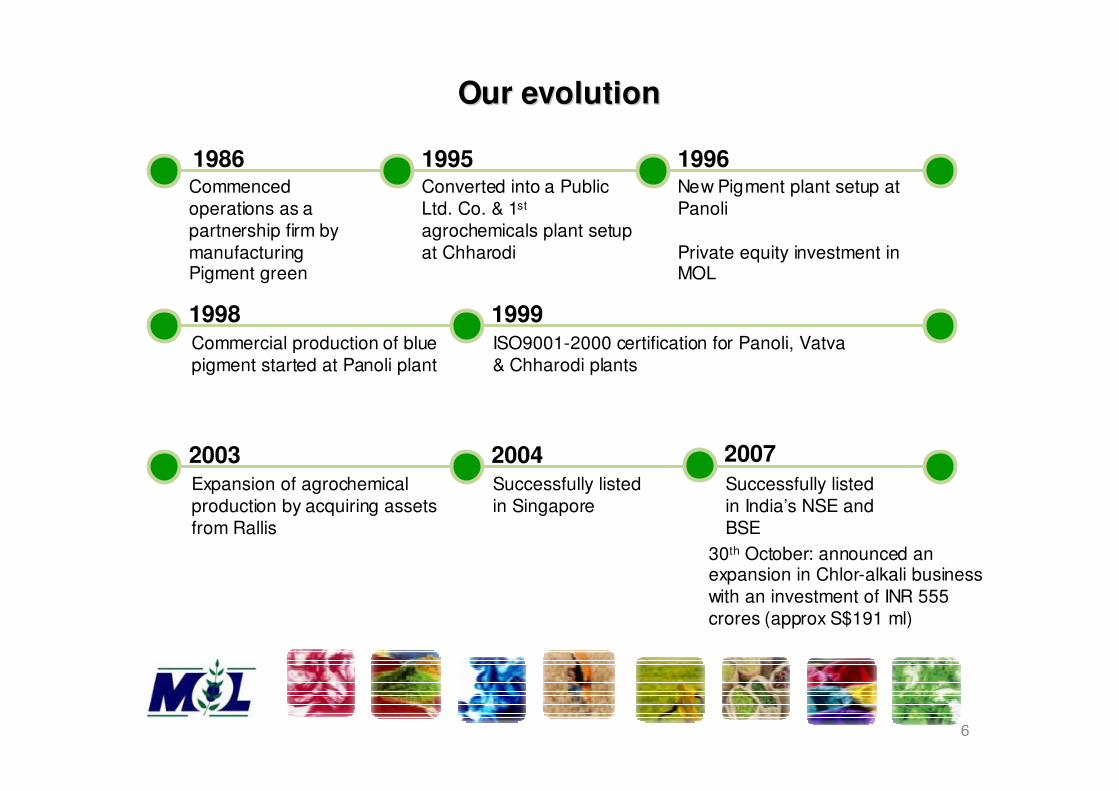

Our evolutionOur evolution

1986Commenced operations as a partnership firm by manufacturing Pigment green

1996New Pigment plant setup at Panoli

Private equity investment in MOL

1998Commercial production of blue pigment started at Panoli plant

1999ISO9001-2000 certification for Panoli, Vatva& Chharodi plants

1995Converted into a Public Ltd. Co. & 1st

agrochemicals plant setup at Chharodi

2003Expansion of agrochemical production by acquiring assets from Rallis

2004Successfully listed in Singapore

2007

Successfully listed in India’s NSE and BSE

30th October: announced an expansion in Chlor-alkali business with an investment of INR 555 crores (approx S$191 ml)

7

Integrated manufacturing facilities

Key plant attributes

• Close proximity to raw materials at low costs

• Easy accessibility to road networks, railways and key ports

• Located in one of the Chemical belts of India

• ISO 9001-2000 certified

• Environment friendly

• Ability to change product mix to suit market conditions

• Average capacity utilisation of plants is 75%

Meghmani is well placed to capitalize on the outsourcing opportunity

Pigments

Agrochemical

s

•Panoli Plant •Vatva plant

•Ankleshwar plant•Chharodi plant

8

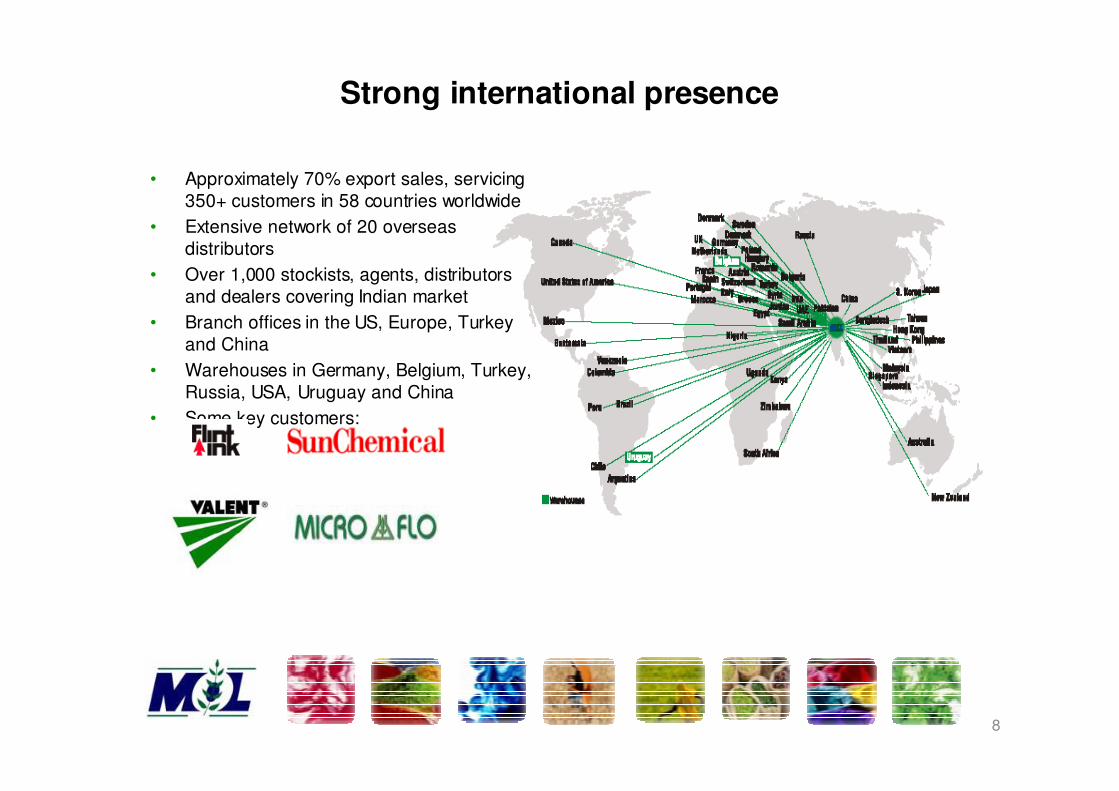

Strong international presence

• Approximately 70% export sales, servicing 350+ customers in 58 countries worldwide

• Extensive network of 20 overseas distributors

• Over 1,000 stockists, agents, distributors and dealers covering Indian market

• Branch offices in the US, Europe, Turkey and China

• Warehouses in Germany, Belgium, Turkey, Russia, USA, Uruguay and China

• Some key customers:

9

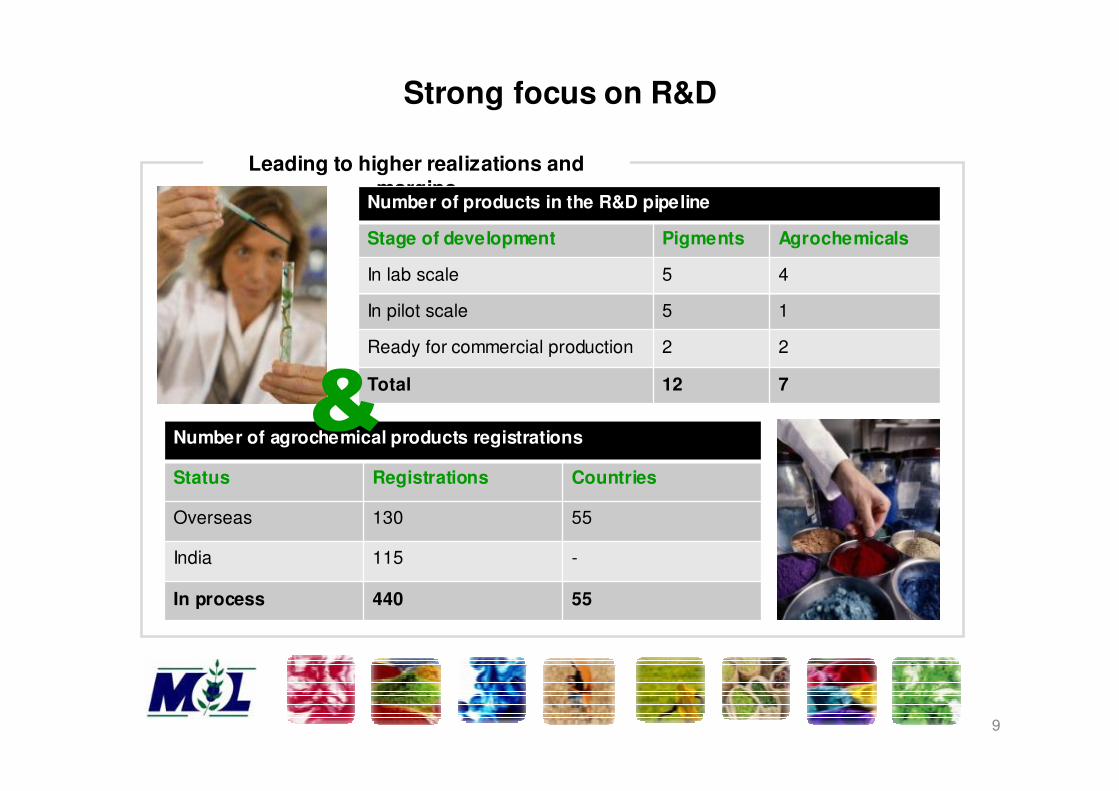

Strong focus on R&D

Leading to higher realizations and margins

Number of products in the R&D pipeline

Stage of development Pigments Agrochemicals

In lab scale 5 4

In pilot scale 5 1

Ready for commercial production 2 2

Total 12 7

Number of agrochemical products registrations

Status Registrations Countries

Overseas 130 55

India 115 -

In process 440 55

�

10

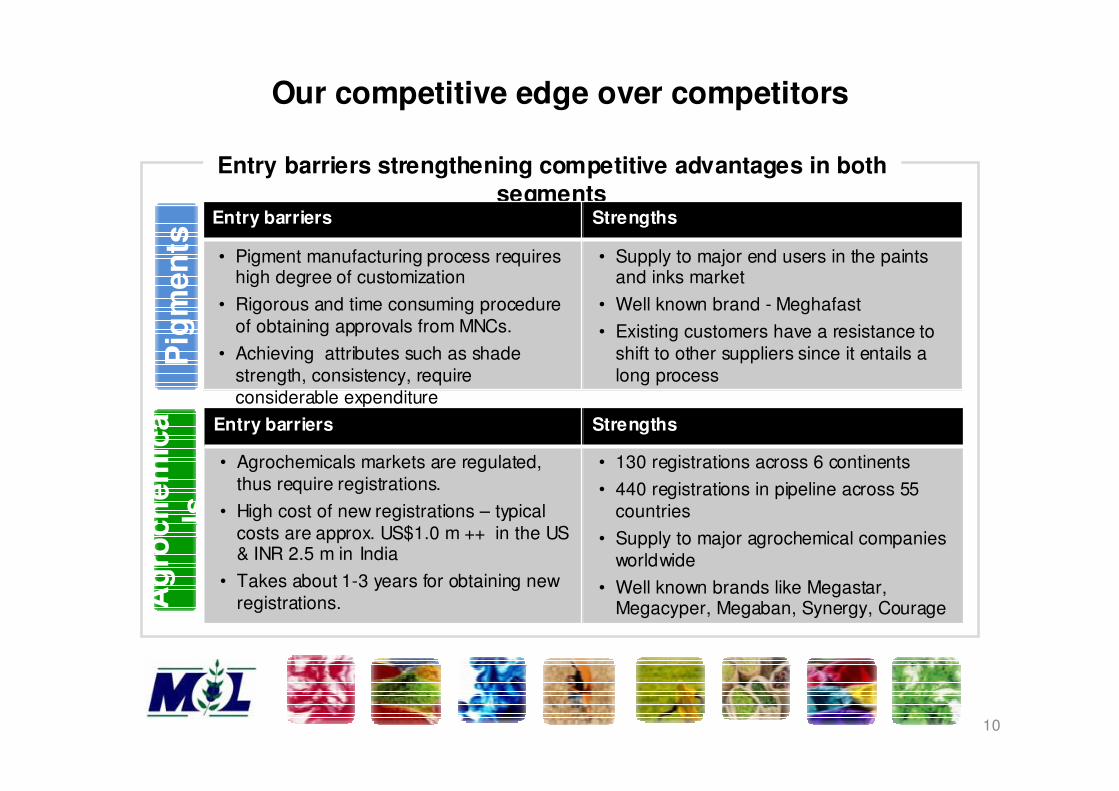

Our competitive edge over competitors

Entry barriers strengthening competitive advantages in both

segmentsP

igm

en

tsEntry barriers Strengths

• Pigment manufacturing process requires high degree of customization

• Rigorous and time consuming procedure of obtaining approvals from MNCs.

• Achieving attributes such as shade strength, consistency, require considerable expenditure

• Supply to major end users in the paints and inks market

• Well known brand - Meghafast

• Existing customers have a resistance to shift to other suppliers since it entails a long process

Ag

roch

em

ica

ls

Entry barriers Strengths

• Agrochemicals markets are regulated, thus require registrations.

• High cost of new registrations – typical costs are approx. US$1.0 m ++ in the US & INR 2.5 m in India

• Takes about 1-3 years for obtaining new registrations.

• 130 registrations across 6 continents

• 440 registrations in pipeline across 55 countries

• Supply to major agrochemical companies worldwide

• Well known brands like Megastar, Megacyper, Megaban, Synergy, Courage

11

Experienced management team with a proven track

record

Name /Title Pigments /dyes

experience

Agrochemicals

experience

Qualification

Mr. Jayanti Patel,

Executive Chairman and co-founder of Meghmani

> 29 years > 10 years Bachelors of Chemical Engineering degree

Mr. Ashish Soparkar,

Managing Director and co-founder of Meghmani

> 29 years > 10 years Bachelors of Chemical Engineering degree

Mr. Natwarlal Patel,

Managing Director and co-founder of Meghmani

> 27 years > 13 years Masters of Science degree

Mr. Ramesh Patel,

Executive Director and co-founder of Meghmani

> 27 years > 13 years Bachelor of Arts degree

Mr. Anand Patel,Executive Director and co-founder of Meghmani

> 20 years - Bachelor of Science degree

12

Industry overview

13

Pigments

Printing Ink

Paint

Plastics

Growth drivers and market outlook

• Organic pigments market size is approximately US$8.2b globally and growing at around 2-3% p.a.

• Steady demand for India’s pigments

– Increasing direct supplies requirements from the US, Europe, Central and South America, and Japan

– Growing Indian ink market > Pigment requirement approx. Rs. 10bn

– Growing Indian Paint and Plastic market > Pigment requirement approx. Rs. 10bn ++

• Select set of large corporates control the world market of Paints and Inks – such as Sun-DIC, Flint Group, Akzo Nobel, DuPont, PPG Industries, etc.

• India capitalizing on the outsourcing play

Major markets for pigment use

Leather, Textiles etc

The pigments industry

Outsourcing trend to India providing impetus to Indian pigment

manufacturers

Printing ink and coatings account for approx.

80% of

consumption

14

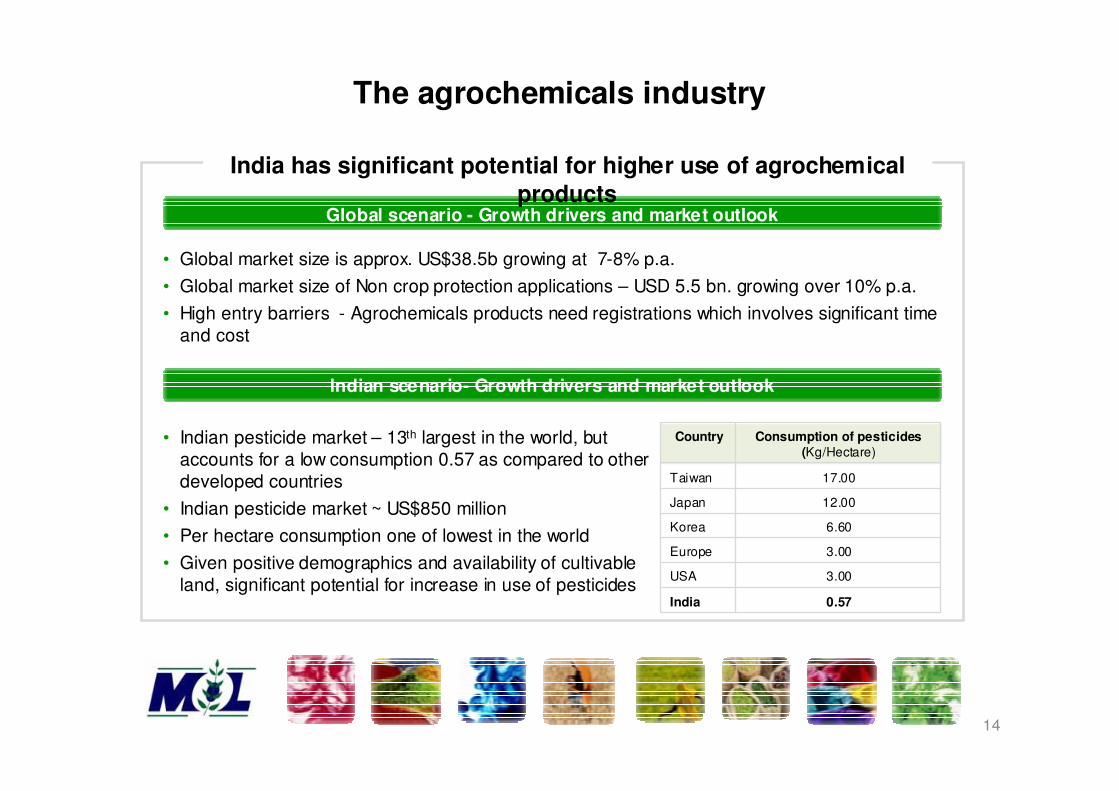

Indian scenario- Growth drivers and market outlook

Country Consumption of pesticides (Kg/Hectare)

Taiwan 17.00

Japan 12.00

Korea 6.60

Europe 3.00

USA 3.00

India 0.57

• Indian pesticide market – 13th largest in the world, but accounts for a low consumption 0.57 as compared to other developed countries

• Indian pesticide market ~ US$850 million

• Per hectare consumption one of lowest in the world

• Given positive demographics and availability of cultivable land, significant potential for increase in use of pesticides

Global scenario - Growth drivers and market outlook

• Global market size is approx. US$38.5b growing at 7-8% p.a.

• Global market size of Non crop protection applications – USD 5.5 bn. growing over 10% p.a.

• High entry barriers - Agrochemicals products need registrations which involves significant time and cost

The agrochemicals industry

India has significant potential for higher use of agrochemical

products