32

Melbourne Mining ClubJacynthe CôtéPresident and Chief Executive Officer, Alcan Bauxite and AluminaDecember 6, 2006

© 2 0 06 A L C A N I N C. Slide 3

Forward-Looking Statement

Statements made in the course of this presentation which describe the Company's or management’s objectives, projections, estimates, expectations or predictions may be "forward-looking statements" within the meaning of securities laws.All statements that address the Company's expectations or projections about the future including statements about the Company's growth, cost reduction goals, operations reorganization plans, expenditures and financial results are forward-looking statements.The Company cautions that, by their nature, forward-looking statements involve risk and uncertainty and actual actions or results could differ materially. Reference should be made to the most recent Form 10-Q or 10-K for a summary of factors that could cause such differences. In addition, certain non-GAAP measures are used which are reconciled to the comparable GAAP measures herein or on the Company’s website at www.alcan.com in the “Investors” section.

© 2 0 06 A L C A N I N C. Slide 4

Presentation Outline

Aluminum – the material of choice

Alcan’s Profile

Bauxite & Alumina Industry Fundamentals and Trends

Summary & conclusion

© 2 0 06 A L C A N I N C. Slide 5

Aluminum — The Material of Choice

Discovered in 1886, the Hall-Héroult electrolysis process opened its use to diverse sectors.

By 1910, the first alloys began the continuing development of its range of applications.

During World War I, aluminum played a decisive role in the development of the aeronautical industry.

After the war, the metal rapidly became part of everyday life.

© 2 0 06 A L C A N I N C. Slide 6

Myriad ApplicationsGlobal Shipments by End Use 2005Myriad ApplicationsGlobal Shipments by End Use 2005

Building & Construction

20%

Automobiles17%

Other Transportation

10%Consumer Durables

7%

Machinery and Equip.

8%

Electrical10%

Cans9%

Other Packaging7%

Other12%

© 2 0 06 A L C A N I N C. Slide 7

Benefits of Aluminum….To name a few

Lightweight – reducing GHG in transportation applications

Infinitely recyclableUse of secondary aluminum requires only 5% of power required to produce primary metal

Flexible and malleable

Excellent electrical and thermal conductivity

Corrosion resistant

© 2 0 06 A L C A N I N C. Slide 8

Presentation Outline

Aluminum – the material of choice

Alcan’s Profile

Bauxite & Alumina Industry Fundamentals and Trends

Summary and conclusion

© 2 0 06 A L C A N I N C. Slide 9

Alcan Business Groups

BAUXITE AND ALUMINA PRIMARY METAL65,000 employees in 61 countries and regions, and posted revenues of US$20.3 billion in 2005

PACKAGINGENGINEERED PRODUCTS

© 2 0 06 A L C A N I N C. Slide 10

Advantaged Platform

Many strengths to build on

Modern, Low Cost Assets

Benchmark Technology

Recognized Leader in Sustainability

Integrated Management System (AIMS)

Leading Market Positions and Strong Customer Relationships

© 2 0 06 A L C A N I N C. Slide 11

Global Asset Distribution

With 14% of the total assets, Australia is the 2nd largest capital base for Alcan

Alcan Fixed Asset Base Distribution (US$ Billion)

1.2

0.2

0.5

0.6

0.7

0.9

1.8

2.3

2.8

8.6

Rest

Brazil

Netherlands

Switzerland

Germany

UK

USA

France

Australia

Canada

Canada 44%USA 9%

South America 1%France 12%

UK 4%Netherlands 3%

Germany 3%Switzerland 3%

Australia 14%Other Asia 1%

© 2 0 06 A L C A N I N C. Slide 12

Alcan in AustraliaGOVE BAUXITE MINE100% Shareholding

NTH QUEENSLAND BAUXITE DEPOSITS100% Shareholding

GOVE ALUMINA REFINERYTotal Capacity: 2.0 Mt 100% Shareholding QAL ALUMINA REFINERY

Total Capacity: 3.8 Mt 41.4% Shareholding

BRISBANE1) Corporate office2) Alcan Engineering 3) R&D Centre

TOMAGO ALUMINIUM SMELTERTotal Capacity: 475 Kt 51.55% Shareholding

SYDNEYCommercial office

ALCAN STELVIN WINE CAP PRODUCTION FACILITY 100% Shareholding

© 2 0 06 A L C A N I N C. Slide 13

Bauxite and AluminaA Global Presence

May 2004

Alumina Refinery/Specialty Aluminas

Bauxite Mine/Deposit

Sales Office/Research & Development/Engineering and Other

Gladstone, Australia

Gove, Australia

Brockville, Canada

Saguenay, Canada Teutschenthal, Germany

Sangaredi, GuineaOrissa, India

Mayfield Heights,United States

Gardanne, FranceMontreal, Canada

Brisbane, Australia

Porto Trombetas, Brazil

La Bathie, FranceBeyrède,France

Caracas/Puerto Ordaz,Venezuela

Sao Paulo, Brazil

Awaso, GhanaAccra, Ghana

Takoradi, Ghana

Montroc/Paulinet, France

Sao Luis, Brazil

Paris, France

* Includes joint ventures and bauxite deposits not yet in operation.

Zurich, Switzerland

Ely, Dulhunty, Ducie-

Wenlock, Australia

Beijing, China

Spath Fluor Mine

Large Bauxite Resources

© 2 0 06 A L C A N I N C. Slide 14

Presentation Outline

Aluminum – the material of choice

Alcan’s Profile

Bauxite & Alumina Industry Fundamentals and Trends

Summary and conclusion

© 2 0 06 A L C A N I N C. Slide 15

Bauxite

10% of world bauxite production

Venezuela3%

India5%

CIS6%

China10%Guinea

10%

Australia34%

Others4%

Brazil17%

Surinam2%

Jamaica9%

Bauxite Production by Country

CVG3%

Alcoa24%

Chalco7%

Alcan10%

Comalco7%

New Rusal10%

BHP Billiton6%

Guyana3%

Nalco3%

Others27%

Bauxite Production by Company

Source: James King, B&A analysis

© 2 0 06 A L C A N I N C. Slide 16

Value Drivers in Bauxite Mining

Location

Proximity to alumina refinery

Proximity to port/power grid

Political/economic stability

Quality/Quantity

Low conversion cost rather than absolute quality

High % hydrateLow relative silica

Large reserve/mine life

© 2 0 06 A L C A N I N C. Slide 17

Alumina

9% of world alumina production

Eastern Europe

3%Other Asia6%

CIS10%

Western Europe

10%

Brazil20%

Australia27%

China12%

Africa1%

North America

11%

Source: James King, B&A analysis

Alumina Production by Region

Others27%

Hydro2%

Comalco5%

New Rusal15%

Alcan9%

Chalco11%

BHP Billiton5%

Alcoa / WMC23%

CVG3%

Alumina Production by Company

© 2 0 06 A L C A N I N C. Slide 18

Value Drivers in Alumina Refining

LocationProximity of the bauxite resourceProximity to markets (smelters)Cost of the energy sourceLocal cost of labour

Refinery OperationsTechnology/design/scale Geological characteristics of bauxite

Silica contentAlumina content

© 2 0 06 A L C A N I N C. Slide 19

Raw Material Price & Currency Volatility

The alumina industry has been affected by unprecedented price increases…Oil: SING 380 (US$/bbl)CAGR Jan 98 - Aug 06: 19%

10

20

30

40

50

1.00199

3

1995

1997

1999

2001

2003

2005

60

CAN$AUS$

1.00

1993

1995

1997

1999

2001

2003

20050.40

0.50

0.60

0.70

0.80

0.90

US$

50

100

150

200

250

300

350

400

450 Caustic: ASP North America (US$/DMT)CAGR Jan 00- Aug 06: 22%

0

1.00199

3

1995

1997

1999

2001

2003

2005

2006

2006

1,000

2,000

3,000

4,000

5,000

6,000

7,000Freight: BDI Index ($/day)

CAGR Jan 98 - Aug 06: 13%Add label

1.00199

3

1995

1997

1999

2001

2003

2005

2006

2006

© 2 0 06 A L C A N I N C. Slide 20

Alumina Industry Block Cost 2001-2006

… impacting substantially the industry cost curve

191 $/t183 $/t

28.325.8156 $/t

63.30

Industry AVG Cash Cost

136 $/t 136 $/t 137 $/t

58.82

13.6

49.71Caustic 12.1

40.63

25.50

14.77

37.35

17.7 18.1 $/t

41.9637.36Energy

19.6319.6018.78

16.7315.1228.9428.91

Labour

28.0326.8126.72

Maintenance & Materials

51.3150.3146.02Bauxite 38.9838.45

2001 2002 2003 2004 2005 2006Source: CRU

© 2 0 06 A L C A N I N C. Slide 21

Alumina World Balance

2006 - the turnaround year from supply deficit to surplus

Alumina World Market Balance Forecast

10,000

Sources : CRU, Metal Bulletin (MBR), Brook Hunt, Macquarie Bank, James F. King

Alcan

-1,121

-1,104

-1,338

-1,361

-1,486

2005

Macquarie Bank – July 06

CRU - Apr 06

MBR - Sept 06

Brook Hunt - Aug. 06

James F. King – Aug 06

8,000

[Kto

nnes

]

6,000

4,000

2,000

-

-2,000

447

1,483

2,999

2,626

1,178

2006

929

1,673

6,468

3,079

3,116

2007

1,285

2,015

4,452

5,337

2,221

2008

© 2 0 06 A L C A N I N C. Slide 22

Historical Alumina Prices

Market returns to surplus – immediate impact on spot prices

Spot, Australian Export and LME price evolution with 25-year averages

Spot

-A

us. E

xp. [

%LM

E]

5.0%

10.0%

15.0%

20.0%

San CiprianAughinish Worsley

Alumina oversupply

High metal prices

Hurricane

Eastern block sell-down

Gramercy explosion

Structural tightness (China)

Alunorte

40.0%

35.0%

30.0%

25.0% Hurricane

0.0% 0

1979

1984

1999

2004

1989

1994

Spot Aus. Export Price Source: CRU

© 2 0 06 A L C A N I N C. Slide 23

Alumina Demand Forecast

China will represent 50% of the additional alumina required between 2005 and 2010

Additionnal alumina requirements between 2005-2010 [Tons]

North America

4%

E/C Europe8%

Latin America

5% Other2%

Africa6%

Oceania1% China

54%

Asia20%

Alumina Demand by Region [2005-2010]

AfricaNorth America

Latin AmericaAsia

W. EuropeOceania

E/C EuropeOther

China

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

2005 2006 2007 2008 2009 2010

Tonn

es

© 2 0 06 A L C A N I N C. Slide 24

Evolution of Alumina Production by Region

Source : Brook Hunt

2005

WESTERN EUROPE10%

LATIN AMERICA20%

EAST / CENTRAL EUROPE

10%

ASIA9%

CHINA13%

OCEANIA27%

AFRICA1%

NORTH AMERICA10%

2010

WESTERN EUROPE

8%

LATIN AMERICA

22%

EAST / CENTRAL EUROPE

8%

ASIA9%

CHINA22%

OCEANIA22%

AFRICA1%

NORTH AMERICA

8%

Alumina Production Growth by Region [2005-2010]

0

5000

10000

15000

20000

25000

30000

2005 2006 2007 2008 2009 2010

'000

tonn

es

AFRICA NORTH AMERICA WESTERN EUROPEEAST / CENTRAL EUROPE ASIA OCEANIA LATIN AMERICA CHINA

Alumina Production Growth by Region [2005-2010]

0

5000

10000

15000

20000

25000

30000

2005 2006 2007 2008 2009 2010

'000

tonn

es

AFRICA NORTH AMERICA WESTERN EUROPEEAST / CENTRAL EUROPE ASIA OCEANIA LATIN AMERICA CHINA

By 2010, China could be one of the top three alumina producing regions

Chinese Alumina Imports

0

1000

2000

3000

4000

5000

6000

7000

2000 2001 2002 2003 2004 2005 2006F

'000

tonn

es

Source: Antaike

© 2 0 06 A L C A N I N C. Slide 25

Chinese Alumina Landscape

2727

21212222

23231818

17172020

29291010

1313

2525

15151616

2626

11

22

77

3030

33

282844

55

66

88

99

1111

1212

1414

1919

2424

Non-ChalcoChalco

MAP REFINERY1 Shandong [Chalco]2 Zhongzhou [Chalco]3 Chongqing-Nanchuan [Chalco] 4 Zunyi-Guizhou [Chalco]5 Guizhou [Chalco]6 Pingguo [Chalco]7 Zhengzhou [Chalco]8 Shanxi [Chalco]9 Mengxi (Inner Mongolia)

10 Luneng Jinbei (Shanxi)11 Yangquan (Shanxi)12 Weilai Aluminum (Henan)13 Tongde (Datong- Shanxi)14 Feicheng (Shanxi)15 Xin-fa Chipping (Shandong)16 Weiqiao (Shandong)17 Pingdingshan Huiyuan Chemical(Henan)18 Yimei (Henan)19 Guangxi project (Guangxi)20 Zhongmei (Henan-Dengfeng)21 East Hope (Henan)22 Cayman (Henan)23 Wanji(Henan)24 Chongquing -Dingtai (Sichuan)25 Bosai (Chongquing-Nanchuan)26 Yunnan Aluminum (Yunnan)27 Guangxi Huayin (Guangxi)28 Kaili (Guizhou)29 Nanshan (Shandong)30 Shandong Lubei Group

MAP REFINERY1 Shandong [Chalco]2 Zhongzhou [Chalco]3 Chongqing-Nanchuan [Chalco] 4 Zunyi-Guizhou [Chalco]5 Guizhou [Chalco]6 Pingguo [Chalco]7 Zhengzhou [Chalco]8 Shanxi [Chalco]9 Mengxi (Inner Mongolia)

10 Luneng Jinbei (Shanxi)11 Yangquan (Shanxi)12 Weilai Aluminum (Henan)13 Tongde (Datong- Shanxi)14 Feicheng (Shanxi)15 Xin-fa Chipping (Shandong)16 Weiqiao (Shandong)17 Pingdingshan Huiyuan Chemical(Henan)18 Yimei (Henan)19 Guangxi project (Guangxi)20 Zhongmei (Henan-Dengfeng)21 East Hope (Henan)22 Cayman (Henan)23 Wanji(Henan)24 Chongquing -Dingtai (Sichuan)25 Bosai (Chongquing-Nanchuan)26 Yunnan Aluminum (Yunnan)27 Guangxi Huayin (Guangxi)28 Kaili (Guizhou)29 Nanshan (Shandong)30 Shandong Lubei Group

Known Bauxite Reserves

Source : B&A Analysis, Brook Hunt

1 Shanxi2 Guizhou3 Henan4 Guangxi5 Sichuan

Top 5 Provinces in Bauxite Reserves1 Shanxi2 Guizhou3 Henan4 Guangxi5 Sichuan

Top 5 Provinces in Bauxite Reserves

China could have up to 30 alumina refineries up and running by 2010

© 2 0 06 A L C A N I N C. Slide 26

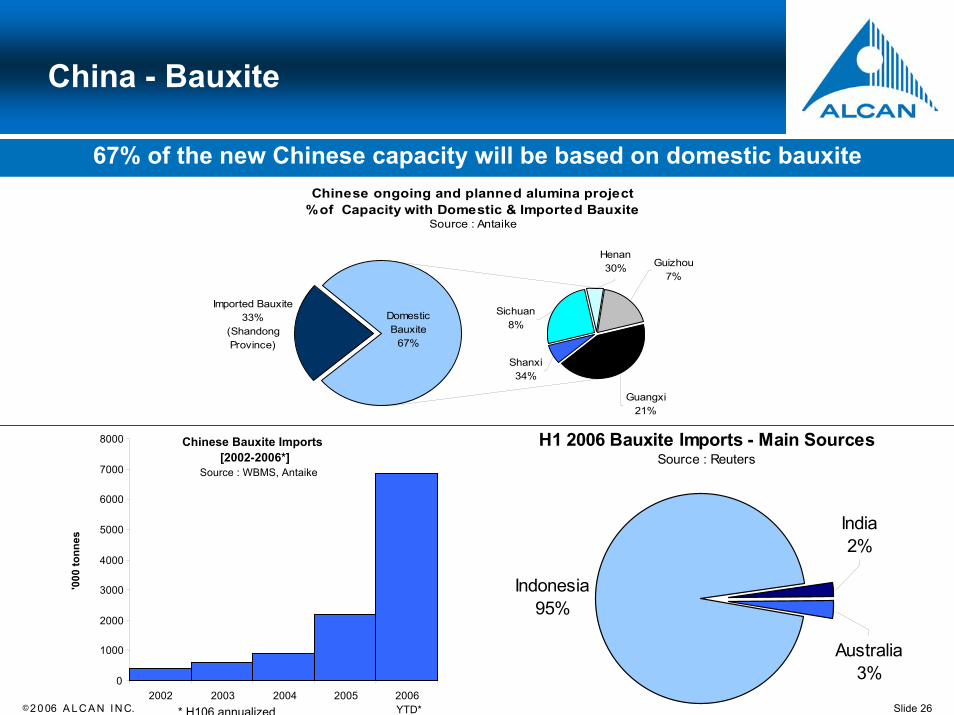

China - Bauxite

H1 2006 Bauxite Imports - Main SourcesSource : Reuters

Indonesia95%

Australia3%

India2%

Chinese ongoing and planned alumina project % of Capacity with Domestic & Imported Bauxite

Source : Antaike

Sichuan8%

Henan30% Guizhou

7%

Guangxi 21%

Domestic Bauxite

67%

Imported Bauxite33%

(Shandong Province)

Shanxi 34%

Chinese Bauxite Imports[2002-2006*]

Source : WBMS, Antaike

67% of the new Chinese capacity will be based on domestic bauxite

8000

7000

6000

* H106 annualized

0

1000

2000

3000

4000

'000

tonn

es

5000

2002 2003 2004 2005 2006 YTD*

© 2 0 06 A L C A N I N C. Slide 27

2007 Alumina Cash Cost Curve

USD/t

0

50

100

150

200

250

300

350

400

0 10000 20000 30000 40000 50000 60000 70000 80000

tpy of production

Chinese capacity

Price zone

Alumina Demand

© 2 0 06 A L C A N I N C. Slide 28

Presentation Outline

Aluminum – the material of choice

Alcan’s Profile

Bauxite & Alumina Industry Fundamentals and Trends

Summary and conclusion

© 2 0 06 A L C A N I N C. Slide 29

Summary

Aluminum industry – strong fundamentals

Alumina market in surplus for the next 2-3 years

China will represent at least 50% of the alumina demand/supply growth over the next 5 years

Operating costs of new Chinese refineries expected to be in 3rd and 4th

quartiles of industry cost curve

Chinese alumina imports expected to decrease

Industry self-regulating price of alumina should be around 250-300$/mt given forecasted cost structure

© 2 0 06 A L C A N I N C. Slide 30

ALCAN – Bauxite & AluminaKey Priorities

Leverage AIMS – Operational Excellence

Bring 50% of alumina production in lowest cost quartile and 75% in lowest half by 2009 by:

Completing Gove and Alumar expansionsConverting Gove to GasCompleting conversion of Gardanne to specialty aluminasExecuting cost reduction program at Vaudreuil and adjust production level to market conditions

Leverage our sustainability & technology/engineering know-how to pursue growth opportunities of large-scale lowest-quartile costadvantaged assets

© 2 0 06 A L C A N I N C. Slide 31

Additional Value Growth Opportunities

Opportunities in lowest cost quartile

Utkal • Greenfield project of 1.5 Mt in the province of Orissa, India• Alcan owns 45% with Hindalco holding the other 55%• Investment decision expected by H1-2007

Guinea • Greenfield project of 1.5Mt in Guinea• Alcan to own 40% with Alcoa holding another 40%• Basic Agreement with the Government of Guinea now effective• Expect to make a decision on DFS by the end of 2006

Project Description and Benefits

Ghana • MoU signed for the analysis of a mine and an alumina refinery project in joint venture with the State

• Conceptual and pre-feasibility studies underway

• Potential development of a large-scale integrated aluminium facility (bauxite mine + alumina refinery + aluminium smelter)

• Large high-quality bauxite resources

Cameroon

Madagascar• Potential development of bauxite mine and alumina refinery with Access Madagascar Sarl,

• Concept study underway

© 2 0 06 A L C A N I N C. Slide 32