14

| Date post: | 16-Jul-2015 |

| Category: |

Business |

| Upload: | tushar-warang |

| View: | 159 times |

| Download: | 5 times |

DFPCL- Timeline

1979: Incorporation Of

Company, start to

manufactures anhydrous

liquid ammonia as well as

fertilizer

1985: Start to

Manufacture

concentrated & dilute

nitric acid, low

density ammonium

nitrate

1986: Start to Manufacture

Ammonium Nitro

phosphate

1989: Start to Manufacture of various

resins based on Methanol

1990: Fertilizers sold under

brand name “Mahadhan”. Start

to manufacture dry carbon di

oxide

1994: Undertook debottlenecking

of ammonia plant to raise

capacity by 20%

1996: Add bulk fertilizers &

Specialized agro products

2000: Setting up a new nitric acid plant with

annual capacity of 1 lakh tonnes

2003: Inducts Knight Frank as real estate

consultant, setting up 6MW captive power

plant

2004: Start to manufacture of

70000 MT per annum

Isopropyl Alcohol

2011: Acquisition of 49 %

equity stake in Desai fruits &

Vegetables Pvt. Ltd.

2012: New plant of Bentonite

sulphur at Haryana, with

capacity of 32000 MTPA.

Start to manufacture Nitro

Phosphate 24:24:0

2014: Start to acquire

Mangalore chemical

fertilizers .

Source: Annual Report, Company Website

Strength• Expected to grow at significant phase• Good experienced management• Diversified Product Basket• Market leader in Indian water soluble,

Speciality fertilizers• With high end technologies increased

productivity• Healthy Balance sheet

Weakness• Company has to depend on natural

gas supply• Fertilizers use depends on monsoon &

irrigation facilities

Opportunities• Need to move from bulk fertilizers to

speciality fertilizers• To become Holistic agriculture player• Moving from domestic to global TAN

player• Moving from commodity to high value

chemicals

• Expand the market in southern region of India

Threats• Many foreign players coming in

speciality fertilizer industry, that’s why margin will get hurt in the future

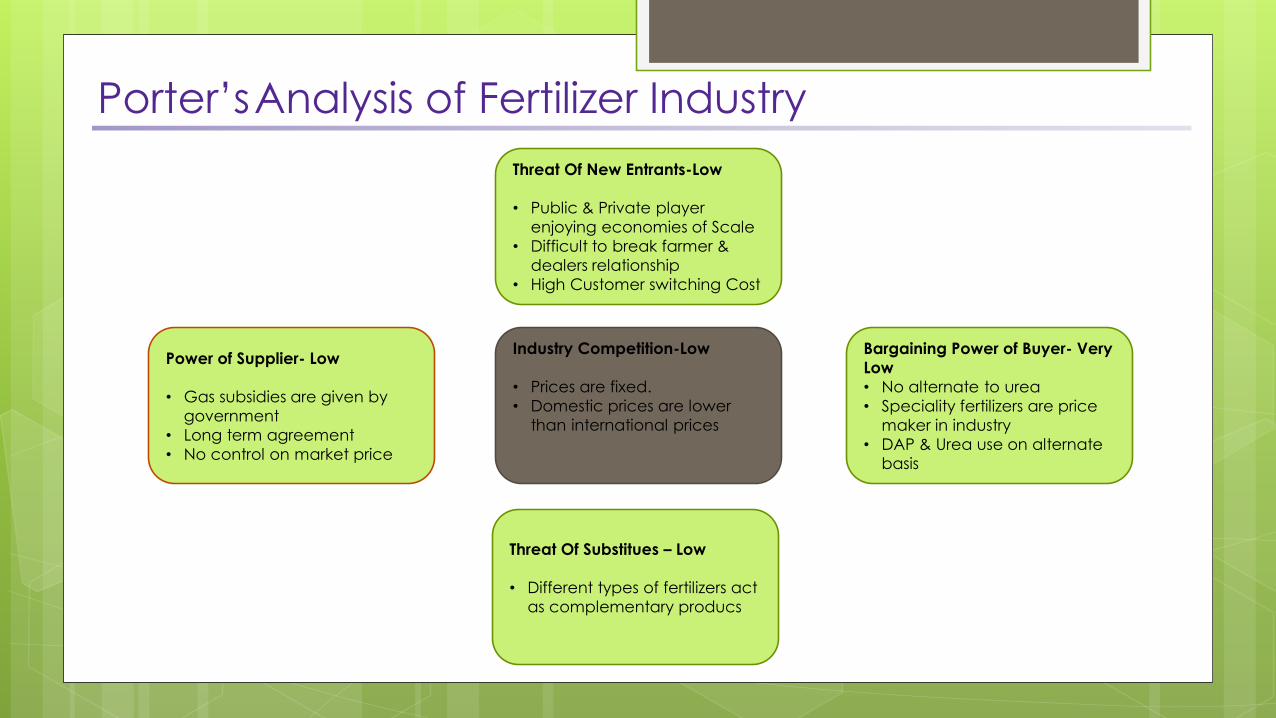

Porter’sAnalysis of Fertilizer Industry

Threat Of New Entrants-Low

• Public & Private player

enjoying economies of Scale

• Difficult to break farmer &

dealers relationship

• High Customer switching Cost

Power of Supplier- Low

• Gas subsidies are given by

government

• Long term agreement

• No control on market price

Bargaining Power of Buyer- Very

Low

• No alternate to urea

• Speciality fertilizers are price

maker in industry

• DAP & Urea use on alternate

basis

Industry Competition-Low

• Prices are fixed.

• Domestic prices are lower

than international prices

Threat Of Substitues – Low

• Different types of fertilizers act

as complementary producs

Urea , 53%

DAP & Complex

Fertilizers, 15%

Ammonium Bi-

carbonate, 2%

Sulphonated

Naphthalene

Formaldehyde,

1%

Plant Protection

Chemicals, 4%

Plant Nutrition

Products, 3%

Trading of

complex

fertilizer, 20%

Revenue Contribution-FY2014

Products MT (As on 2014)

Urea 3.8 Lac

DAP & Complex Fertilizers 2.8 Lac

Ammonium Bi-carbonate 24750

Sulphonated NaphthaleneFormaldehyde 21450

Plant Protection Chemicals 22000

Plant Nutrition Products 200

Trading of complex fertilizer NA

* MCFL was the ideal acquisition target preliminarily in terms of size (market share) and ease

since DPFCL already had a stake in MCFL.

0

5000

10000

15000

20000

FY12 FY13 FY14

(Rs mn)

Subsidy -% of debt

Total Debt Subsidy Pending

0

20000

40000

60000

FY12 FY13 FY14

5350 5350 5350

32850 37069 40665

Urea subsidy & farm

price breakup

Urea Price Subsidy

MCFL’s urea plant faces plant closure:• GOI issues plant closure notice to high

cost naphtha plant.• Company's sales & profit will hit by big

margin as Urea contributes approx. 50% of sales

Stress on working capital & interest cost• MCFL has witnessed significant delays in

fertilizer subsidy payment from GOI.• Due to high cost of Naphtha, subsidy

account 90% of urea cost• MCFL as strong balance sheet as most

of debt is working capital• On time subsidy payment will decrease

interest payment

Gas connectivity to its urea plant is still far away:• MCFL converted its

naphtha based plant to gas based plant.

• Expected gas connectivity to plant is in 2016-17

Source: Annual Report MCFL, www.faidelhi.org

Enhancement in Product basket:

• MCFL has diversified product basket which

includes urea, DAP and other complex fertiliser

• DFPCL’s product basket primarily includes

Ammonium Nitrate Phosphate (ANP) with

capacity of 2.3 lac MT

• DPFCL get access to the commodity product-

Urea

• Increase competitiveness in import pricing for

traded fertilizer

• DPFCL get access to the non fertilizers

speciality agriculture inputs such as soil

conditioners, Micro Nutrients, water soluble

fertilizers. (Higher margins & growth potential)

DAP, 18%

NPK, 9%

MOP,

12%

Urea,

61%

MCFL Product Portfolio

DAP, 29%

ANP, 25%

MOP,

46%

DFPCL Product Portfolio

(Fertilizer)

Source: Annual report of MCFL & DPFCL

Geographical diversification helps to

increase market share:

• MCFL enjoys strong presence in

southern region primarily Karnataka

which contributes ~75% to its fertiliser

sales.

• Other key markets include Tamilnadu

(10%) and Andhra Pradesh (8%)

• DFPCL on other hand enjoys strong

presence in western region.

• We can expect significant synergies

as DFPCL will be able to enter into

southern region

• These two companies can cross sale

their products to achieve maximum

market share

• Presently, Market shares of MCFL &

DPFCL are 4.5% and 4.9% respectively

in fertilizers.

Source: Annual report of MCFL & DPFCL

75%

10%

8%6% 1%

MCFL: Geographical Distribution

Karnataka Tamilnadu Andhra Pradesh Kerala Maharashtra

87%

6%5% 2%

DPFCL (Fertilizers): Geographical

Distribution

Maharashtra Karnataka Gujarat UP

Strong brand and farmers connect

Both the companies enjoy strong farmers connect and distribution strength in their respective

markets

MCFL’s Mangala brand & DFPCL’s Mahadhan brand has strong presence in their respective zones

Both the companies connects directly with the farmers by educating them right use of various

crop

Proximity with ports offers significant advantage

MCFL offers significant opportunity for fertiliser trading primarily DAP and MOP due to its close

proximity to the Mangalore port

MCFL’s plant is well connected, both by rail and road

It will also facilitate import of raw material / intermediates like ammonia and phosphoric acid

which will facilitate production of complex fertiliser.

Future opportunity for brownfield expansion

MCFL has surplus land of 50 acres which is sufficient to build plant with 1 MT capacity in the future

The New Mangalore Port is an all-weather port capable of handling ships up to 30 feet draft.

Other agricultural synergies

Maharsahtra & Karnataka produce similar kind of crops. Hence cross- selling of fertilizers becomes

a possibility.

Karnataka is the largest producer of coarse cereals, for which DFPCL has speciality products.

Similarly DFPCL’s product portfolio includes mining and industrial chemicals.

Valuation (INR Crore) Except per share price

EBIT 223.454

NOPAT 169.447

add: dep 31.636

less: inc wkg cap 27

Capex 87.9

86.2

Agg. DCF 77.1

FCFF 87.9

Terminal Value 893.0

PV of Terminal Value 798.3981103

Total Enterprise value 875.45

Shares 11.86

Price/share 73.82

By our estimates, intrinsic value of MCF is Rs 73.82 per share.However, considering the probable synergies, we offer a premium of 26% to Rs 93 per share.

Balance Sheet (INR Crore) FY 2015e On Cash Deal

Source of Fund

Share Capital 88.20

Reserve 1432.06

Shareholder's Funds 1520.26

Secured Loans 1594.71

Unsecured Loans 182.01

Total Debts 1776.72

Current Liabilities 2759.52

Provisions 104.11

Total Current Liabilities 2840.82

Total Liabilities 6137.79

Good Will 107.55

Gross Block 3706.72

Less: Accumulated Depreciation 1560.92

Net Block 2145.81

Capital Work in Progress 236.69

Investments 561.66

Current Assets, Loans & Advances 0.00

Inventories 688.45

Sundry Debtors (Debotrs) 835.26

Cash and Bank 139.01

Other Current Assets 1406.01

Loans and Advances 176.57

Total Current Assets 3245.30

Deferred Tax Assets / Liabilities -159.73

Total Assets 6137.27

P&L (INR Crore) FY 2015 On Cash Deal

Gross Sales 8315.36

Less: Excise 281.72

Net Sales 8033.65

EXPENDITURE :

Increase/Decrease in Stock 17.99

Raw Materials Consumed 5556.39

Power & Fuel Cost 540.36

Employee Cost 3075.37

Other Manufacturing Expenses 210.74

General and Administration

Expenses 245.25

Selling and Distribution Expenses 151.02

Miscellaneous Expenses 115.96

Total Expenditure 7200.88

PBIDT (Excl OI) 832.76

Other Income 53.57

Operating Profit 788.27

Interest 286.15

PBDT 502.12

Depreciation 159.63

Profit Before Taxation &

Exceptional Items 342.49

Profit Before Tax 342.49

Provision for Tax 119.87

PAT 222.62

Assumptions:

• DPFCL is

buying

MCFL on

26% ao the

intrinsic

value .

• Deal has

been taken

place on

the basis of

all cash

DPFCL will

raise long term

debt of 738

Crore at an

average of

10% interest

rate

CASE 1 : ALL CASH DEAL

Balance Sheet (INR Cr) FY 2015 Shares offered 1:1

Source of Fund

Share Capital 177.15

Reserve 1432.06

Shareholder's Funds 1609.21

Share Premium 738.29

Secured Loans 767.47

Unsecured Loans 182.01

Total Debts 949.48

Current Liabilities 2759.52

Provisions 104.11

Total Current Liabilities 2840.82

Total Liabilities 6137.79

Good Will 107.55

Gross Block 3706.72

Less: Accumulated Depreciation 1560.92

Net Block 2145.81

Capital Work in Progress 236.69

Investments 561.66

Current Assets, Loans & Advances 0.00

Inventories 688.45

Sundry Debtors (Debotrs) 835.26

Cash and Bank 139.01

Other Current Assets 1406.01

Loans and Advances 176.57

Total Current Assets 3245.30

Deferred Tax Assets / Liabilities -159.73

Total Assets 6137.27

P&L (INR Cr) FY 2015 As share offered 1:1

Gross Sales 8315.36

Less: Excise 281.72

Net Sales 8033.65

EXPENDITURE :

Increase/Decrease in Stock 17.99

Raw Materials Consumed 5556.39

Power & Fuel Cost 540.36

Employee Cost 3075.37

Other Manufacturing

Expenses 210.74

General and Administration

Expenses 245.25

Selling and Distribution

Expenses 151.02

Miscellaneous Expenses 115.96

Total Expenditure 7200.88

PBIDT (Excl OI) 832.76

Other Income 53.57

Operating Profit 788.27

Interest 203.43

PBDT 584.84

Depreciation 159.63

Profit Before Taxation &

Exceptional Items 425.21

Profit Before Tax 425.21

Provision for Tax 148.82

PAT 276.39

Assumptions:

• DPFCL is

buying

MCFL on

26%

premium

of the

intrinsic

value .

• Deal has

been

taken

place on

the basis

of 1:1

exchange

ratio

CASE 2 : SHARES 1:1

Ratios DPFCL Post Merger DPFCL - All cash Post Merger DPFCL - Shares 1:1

D/E 6.71 10.08 4.33

Interest Coverage 3.96 2.35 3.31

ROE 16.55% 14.64% 17.18%

In the near term, improvement in key ratios is observed in the post merger scenario.

Post Merger DPFCL - All cash Post Merger DPFCL - Shares 1:1

No of Shares

(Crore) 8.82 17.72

Total Earnings

(Crore) 264.39 276.39

EPS 29.98 15.60

Market Value (Crore) 2289.73

PE 8.66 8.28

Thank You