44

Mergers and Acquisitions: Indian Pharmaceutical Industry Naveen Kumar

| Date post: | 15-Jul-2015 |

| Category: |

Health & Medicine |

| Upload: | naveen-kumar |

| View: | 12,966 times |

| Download: | 2 times |

Mergers and

Acquisitions:

Indian

Pharmaceutical

Industry

Naveen

Kumar

Contents

O Introduction

O Reasons for M&A

O Leading M&A deals

O Case study: Abbott- Piramal deal

O Future

Introduction

O India ranks 3rd worldwide by volume of

production and 14th by value

O India accounts for 10% of world’s

production by volume and 1.5% by value

O India continues its growth trajectory

facilitated by a dynamic position and a

global trend towards consolidation

O M&A has become important tool for

inorganic growth in Indian Pharma

Contd..

O A strong and growing domestic market, a

robust pipeline of generic drugs and an

ability to service developed markets

abroad have suddenly made Indian

pharma companies most sought-after in

the M&A space

O The story started in a small way in 2006

with the $736 million Matrix-Mylan deal

What are MNCs looking for?O Presence of strong portfolio of brands which are

ranked amongst the top in their respective segments

O Strong generics portfolio with presence in high

growth/ high margin therapeutic categories like CV,

CNS, Oncology and anti diabetes

O Availability of infrastructure to cater to regulated

markets. This will enable them to act as a

manufacturing base to meet the demand for

regulated markets

O Presence in niche segments like vaccines, biotech,

nutraceuticals, OTC etc which has substantial

growth potential both in India as well as globally

Why M&A??

Reasons for M&A

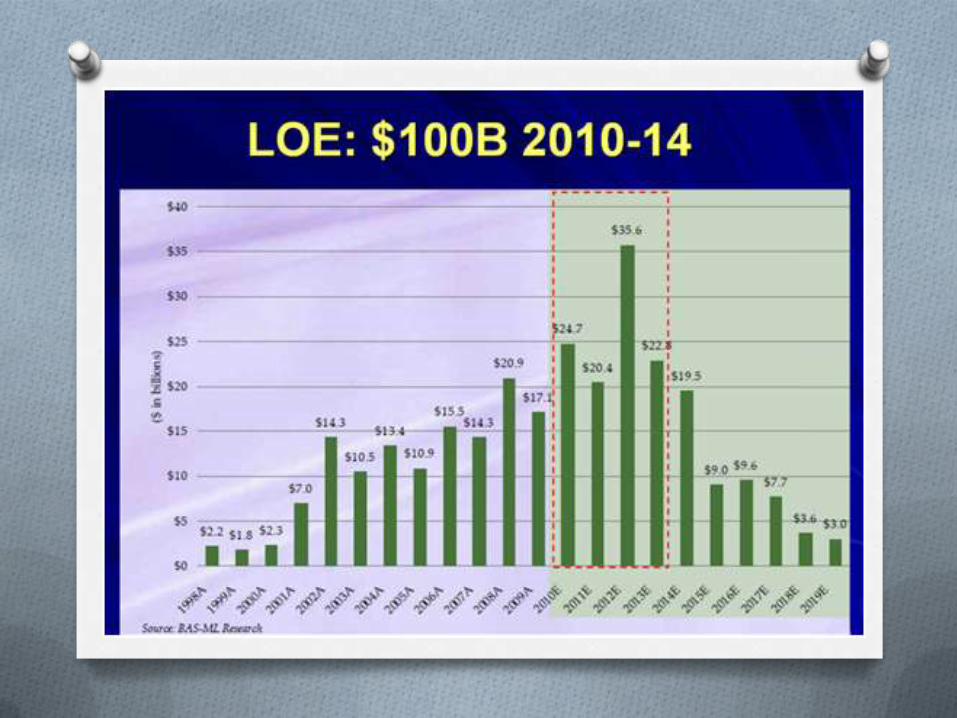

O Patent cliff: The total value of patents expiring between 2010 and 2015 is expected to reach US $100 Billion

O Expanding market is one of the strategies to maintain the flow of revenue

O India with high population and growing market, is attracting MNCs to invest in India

2010 2011

Product 2009 sales

($mn)

Product 2009 sales

($mn)

Aricept 3,991 Lipitor 12,535

Cozaar 3,561 Advair 7,794

Effexor XR 3,182 Zyprexa 4,916

Taxolere 3,034 Levaquin 2,648

Protonix 2,052 Xalatan 1,737

Flomax 1,970 Concerta 1,326

Arimidex 1,921 Femara 1,292

Gemzar 1,363 Xeloda 1,160

NovoSeven 1,320 Avelox 1020

Coreg 253 Caduet 548

Total 22,647 Total 34,976

Year of first available generics; Source: Ken Kaitin, Tufts University, R&D

Productivity conference, May 5, 2011

2012 2013

Product 2009 sales

($mn)

Product 2009 sales

($mn)

Plavix 9,801 Cymbalta 4,660

Enbrel 6,575 AcipHox 2,728

Diovan 6,013 Humalog 1,959

Seroquel 5,126 Zometa 1,469

Singulair 4,660 Niaspan 853

Lexapro 3,263 Lovaza 705

Avapro 3,088 Xopenex 357

Actos 2,532 Zomig 166

Viagra 1,892 Advicor 80

Avandia 724 Fuzeon 26

Total 43,674 Total 13,003

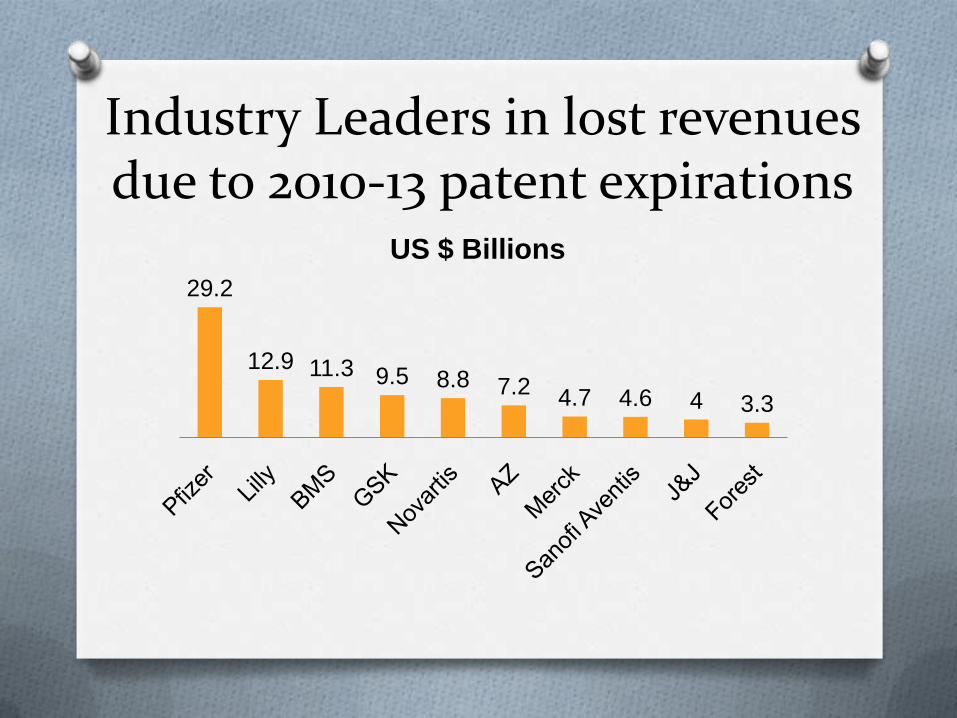

Industry Leaders in lost revenues due to 2010-13 patent expirations

29.2

12.9 11.3 9.5 8.8 7.2 4.7 4.6 4 3.3

US $ Billions

Reasons for M&A(contd..)

O High cost of R&D and decreased R&D

productivity(Poor returns)

O High valuation of Indian firms (Premium Value)

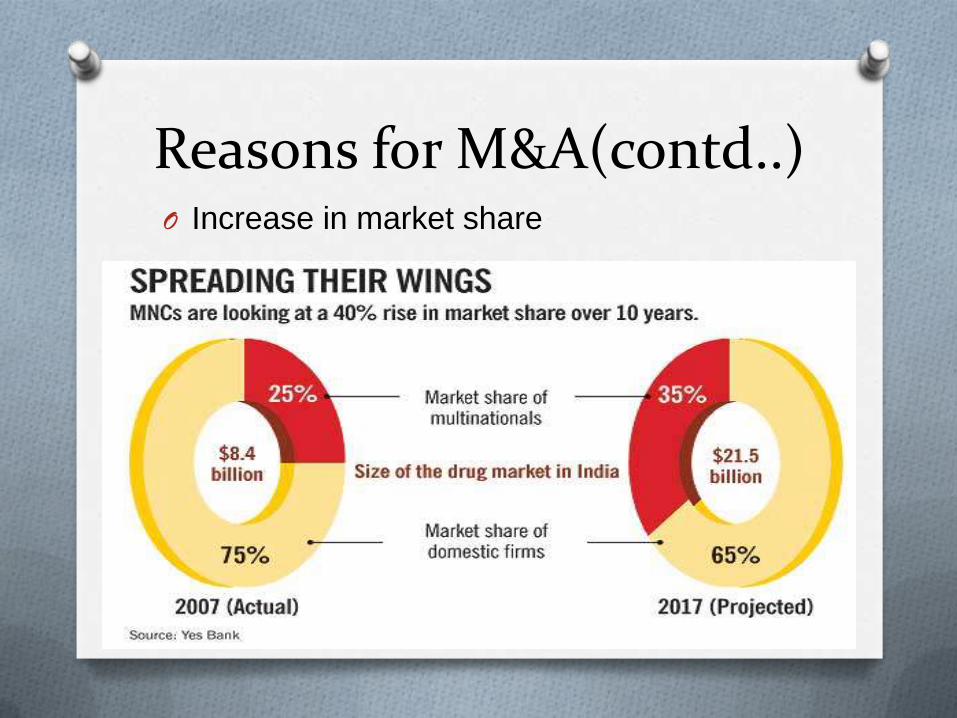

O Increase in market share

O Change in mindset of promoters

O Generic competition

O High profile product recalls

Reasons for M&A(contd..)

O Manufacturing prowess and cost

competitiveness of Indian companies

(highest no of USFDA approved plants

outside US)

O Geographical expansion

O Emerging markets- future growth driver

O Overcome barriers to entry

O Product/Brand extension

Reasons for M&A(contd..)O Growing Indian population

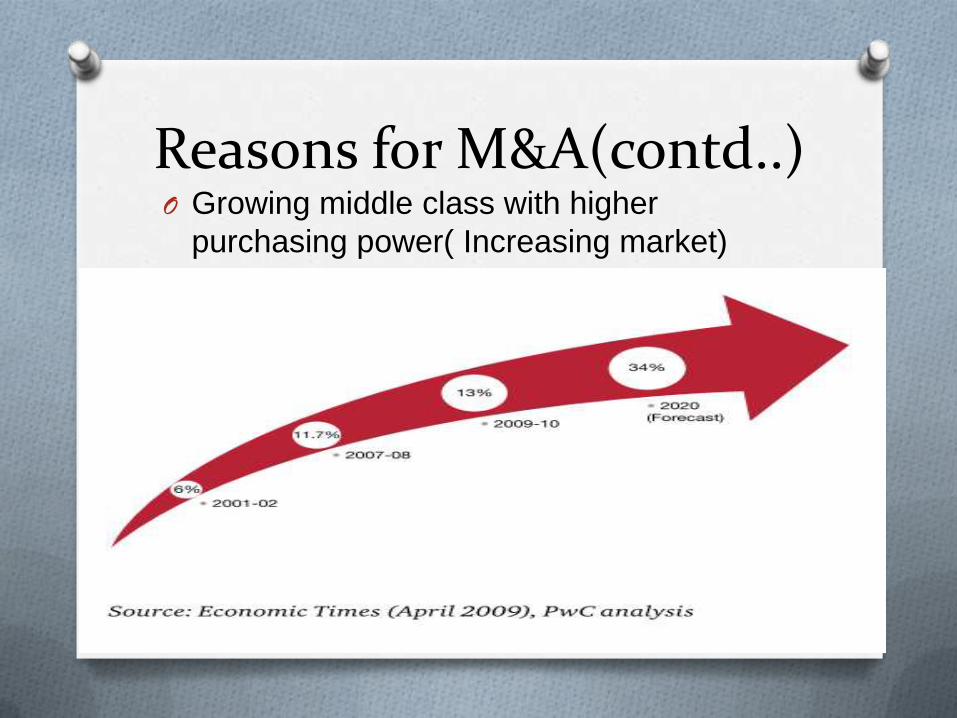

Reasons for M&A(contd..)O Growing middle class with higher

purchasing power( Increasing market)

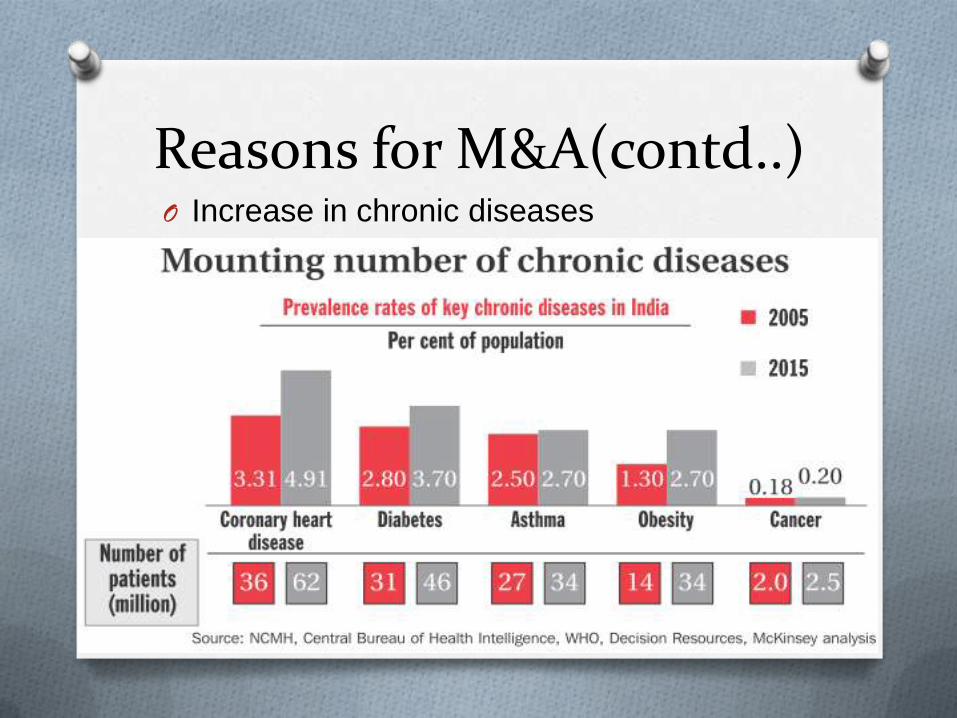

Reasons for M&A(contd..)O Increase in chronic diseases

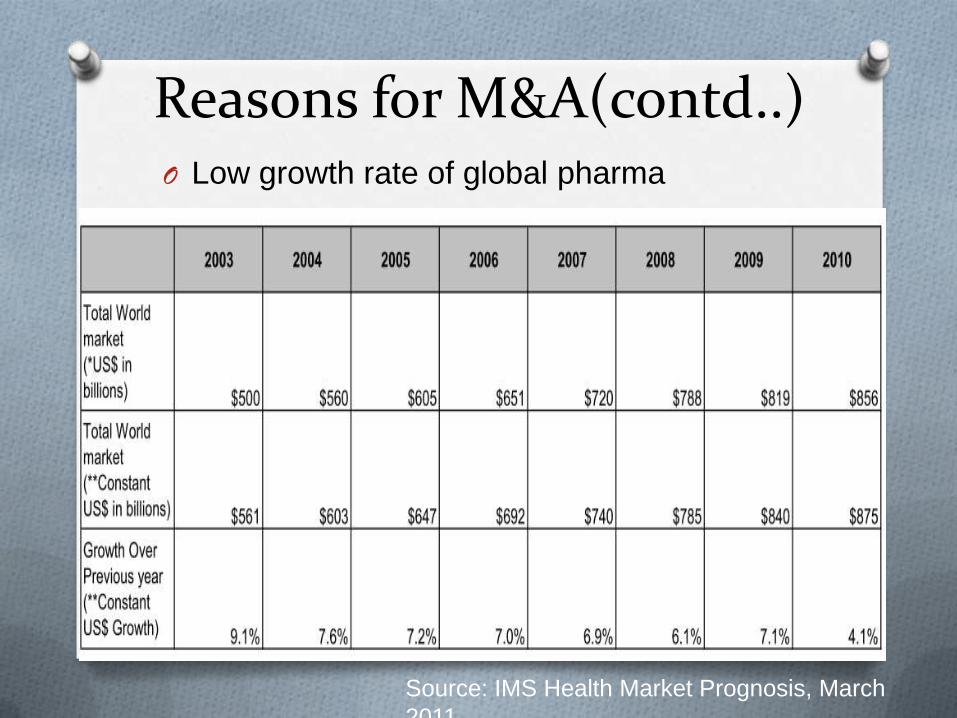

Reasons for M&A(contd..)O Low growth rate of global pharma

Source: IMS Health Market Prognosis, March

2011

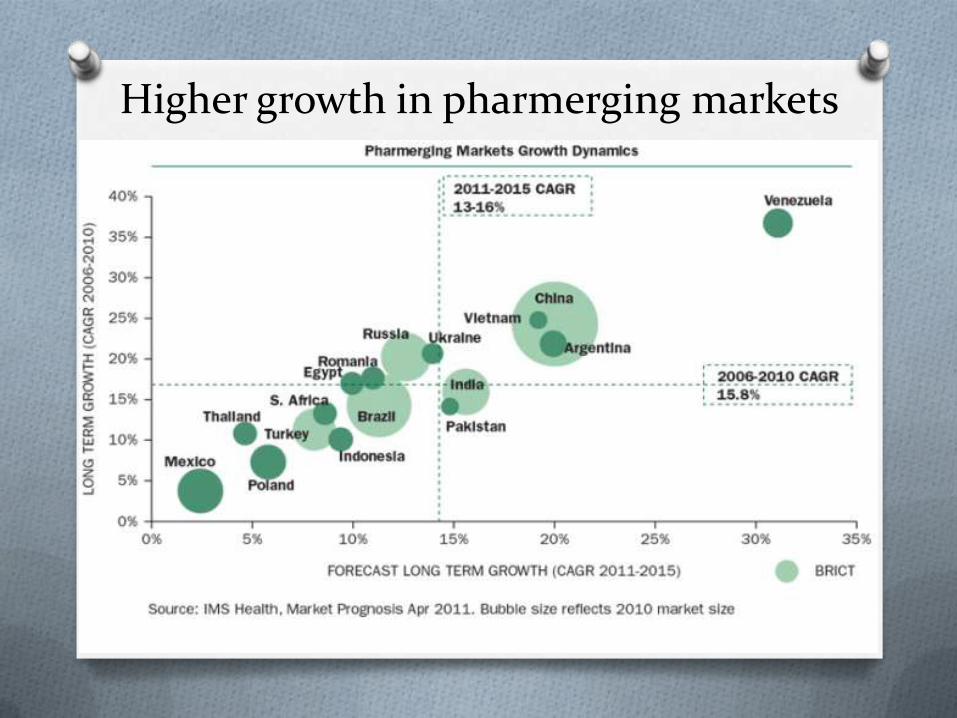

Higher growth in pharmerging markets

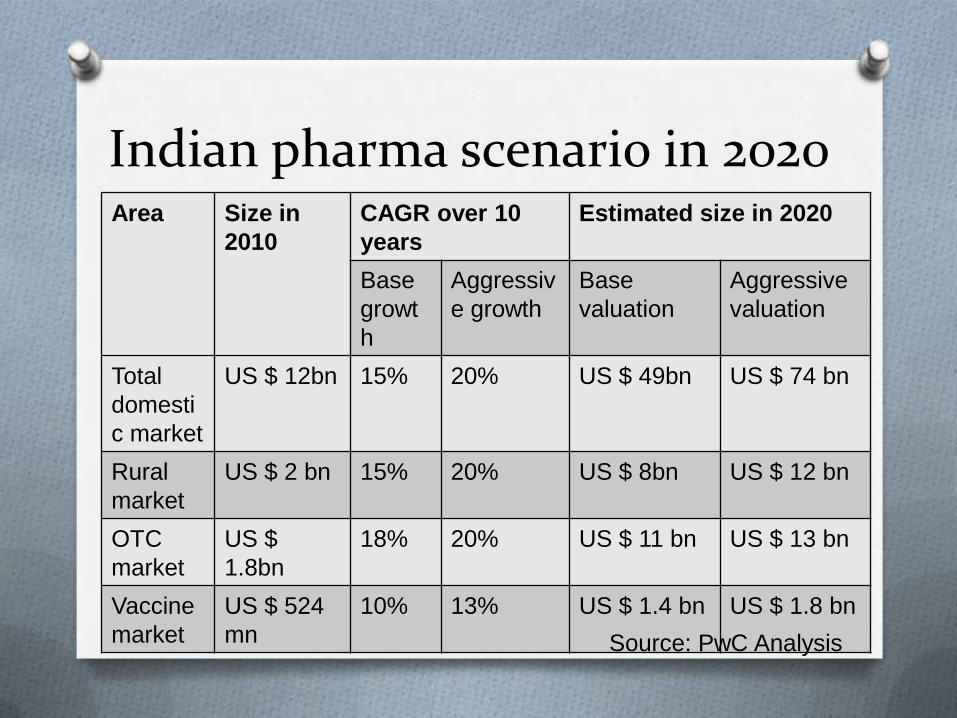

Indian pharma scenario in 2020Area Size in

2010

CAGR over 10

years

Estimated size in 2020

Base

growt

h

Aggressiv

e growth

Base

valuation

Aggressive

valuation

Total

domesti

c market

US $ 12bn 15% 20% US $ 49bn US $ 74 bn

Rural

market

US $ 2 bn 15% 20% US $ 8bn US $ 12 bn

OTC

market

US $

1.8bn

18% 20% US $ 11 bn US $ 13 bn

Vaccine

market

US $ 524

mn

10% 13% US $ 1.4 bn US $ 1.8 bn

Source: PwC Analysis

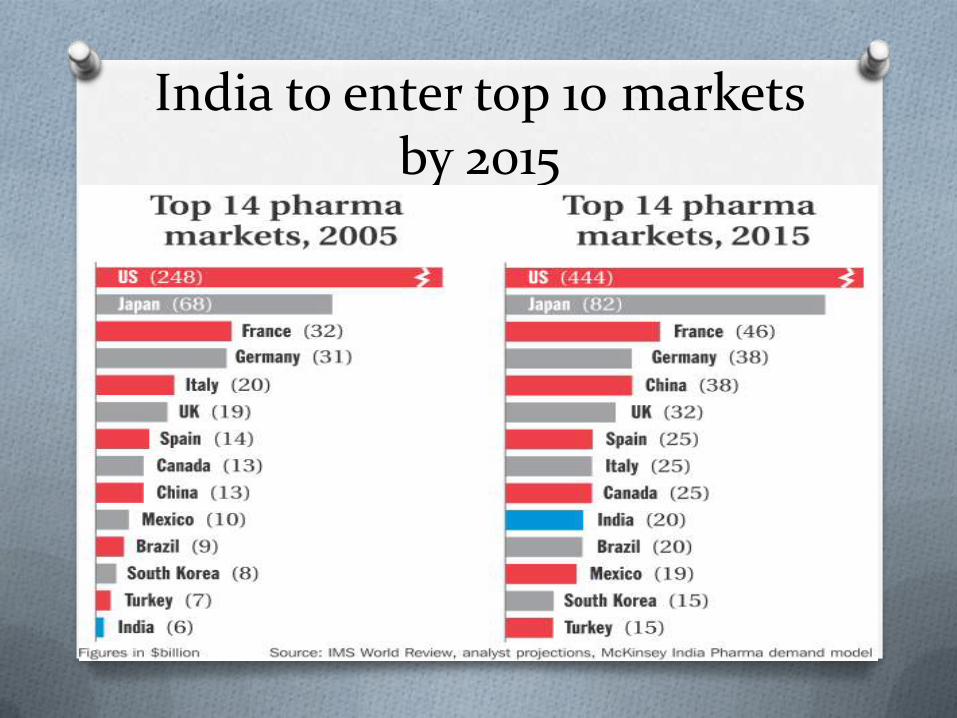

India to enter top 10 markets by 2015

Reasons for M&A(contd..)O Increase in market share

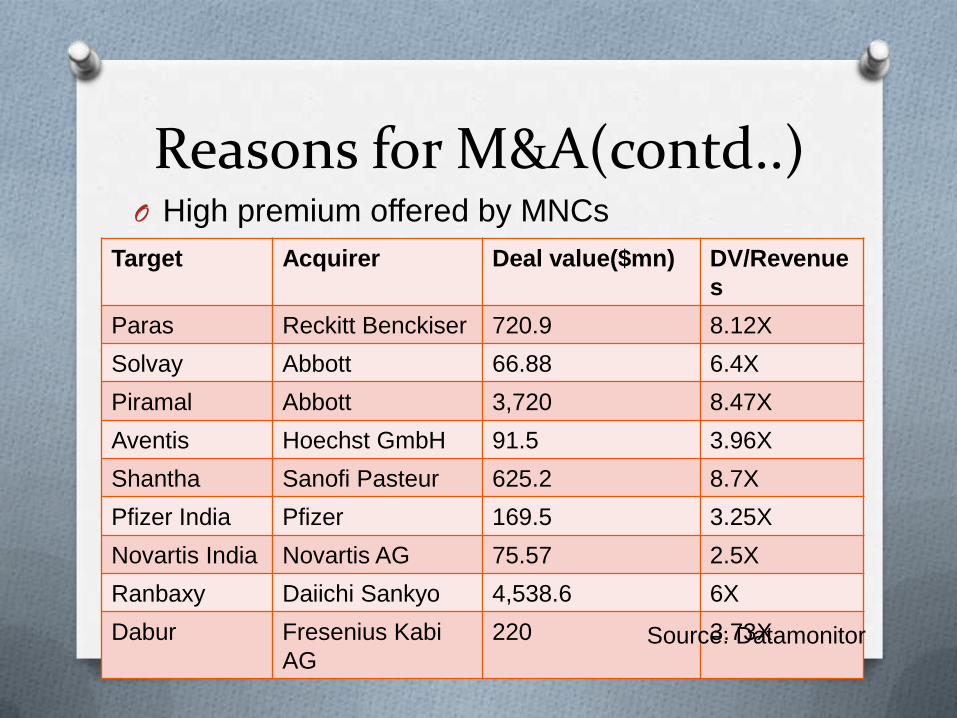

Reasons for M&A(contd..)O High premium offered by MNCs

Target Acquirer Deal value($mn) DV/Revenue

s

Paras Reckitt Benckiser 720.9 8.12X

Solvay Abbott 66.88 6.4X

Piramal Abbott 3,720 8.47X

Aventis Hoechst GmbH 91.5 3.96X

Shantha Sanofi Pasteur 625.2 8.7X

Pfizer India Pfizer 169.5 3.25X

Novartis India Novartis AG 75.57 2.5X

Ranbaxy Daiichi Sankyo 4,538.6 6X

Dabur Fresenius Kabi

AG

220 3.73XSource: Datamonitor

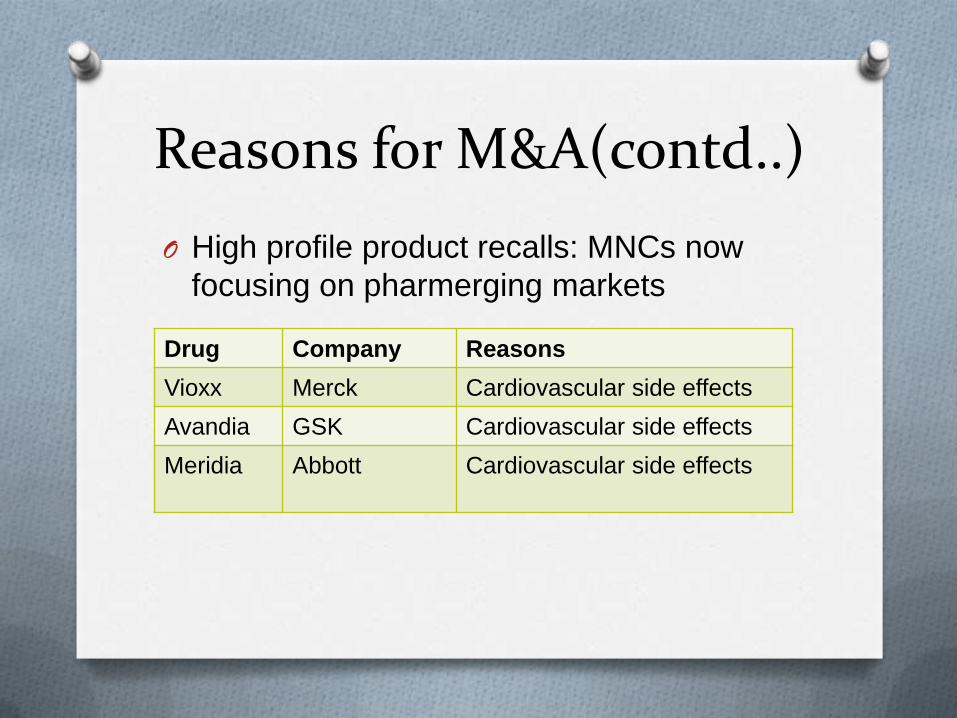

Reasons for M&A(contd..)

O High profile product recalls: MNCs now

focusing on pharmerging markets

Drug Company Reasons

Vioxx Merck Cardiovascular side effects

Avandia GSK Cardiovascular side effects

Meridia Abbott Cardiovascular side effects

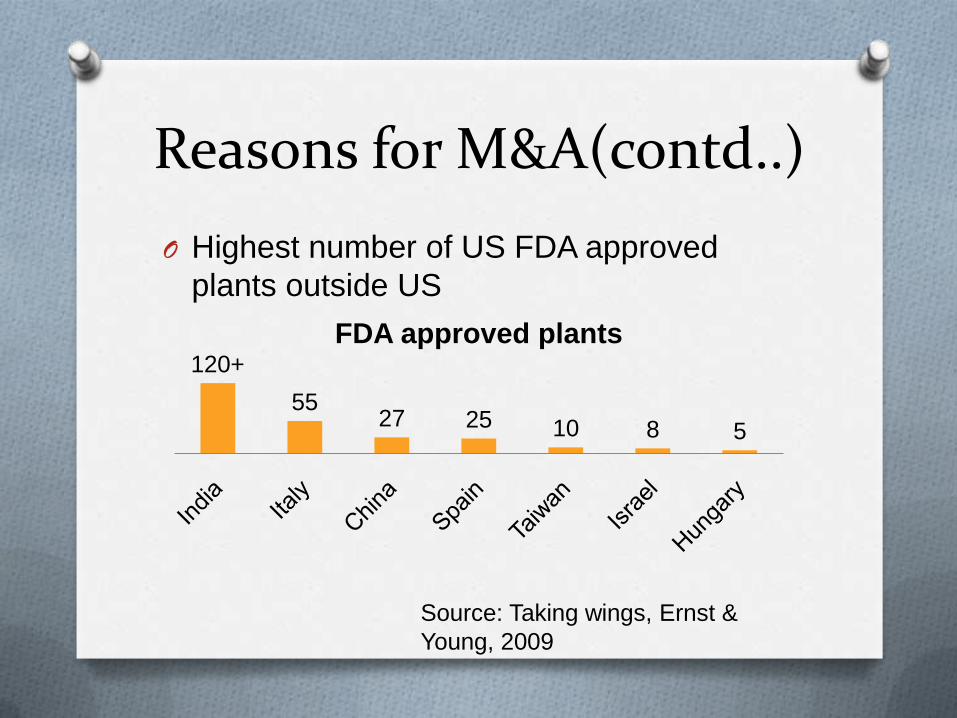

Reasons for M&A(contd..)

O Highest number of US FDA approved

plants outside US

120+

5527 25 10 8 5

FDA approved plants

Source: Taking wings, Ernst &

Young, 2009

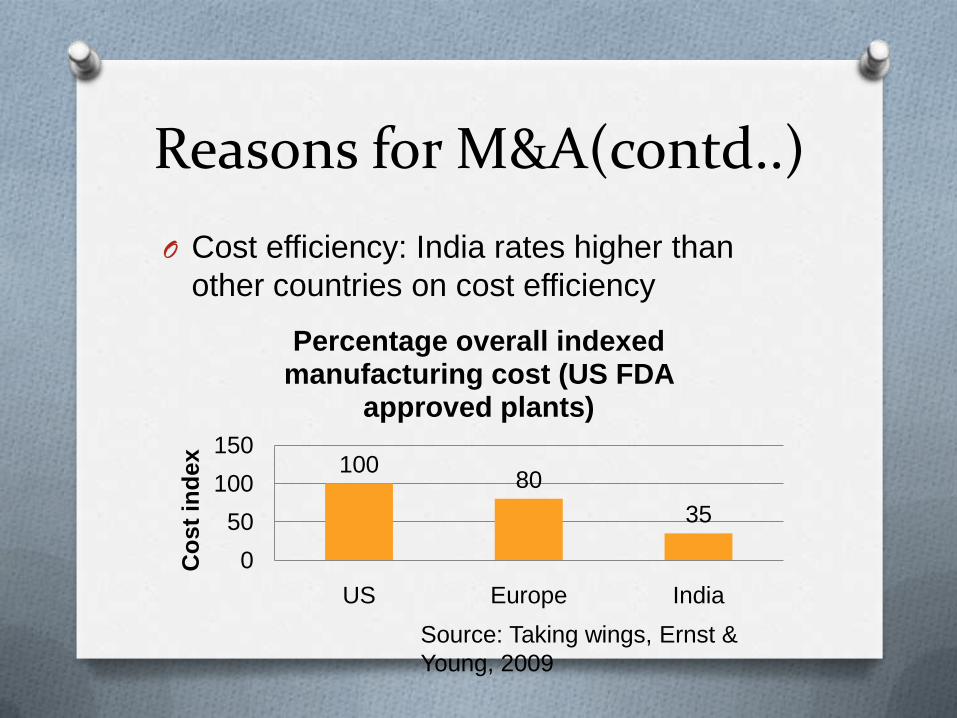

Reasons for M&A(contd..)

O Cost efficiency: India rates higher than

other countries on cost efficiency

10080

35

0

50

100

150

US Europe India

Co

st

ind

ex

Percentage overall indexed manufacturing cost (US FDA

approved plants)

Source: Taking wings, Ernst &

Young, 2009

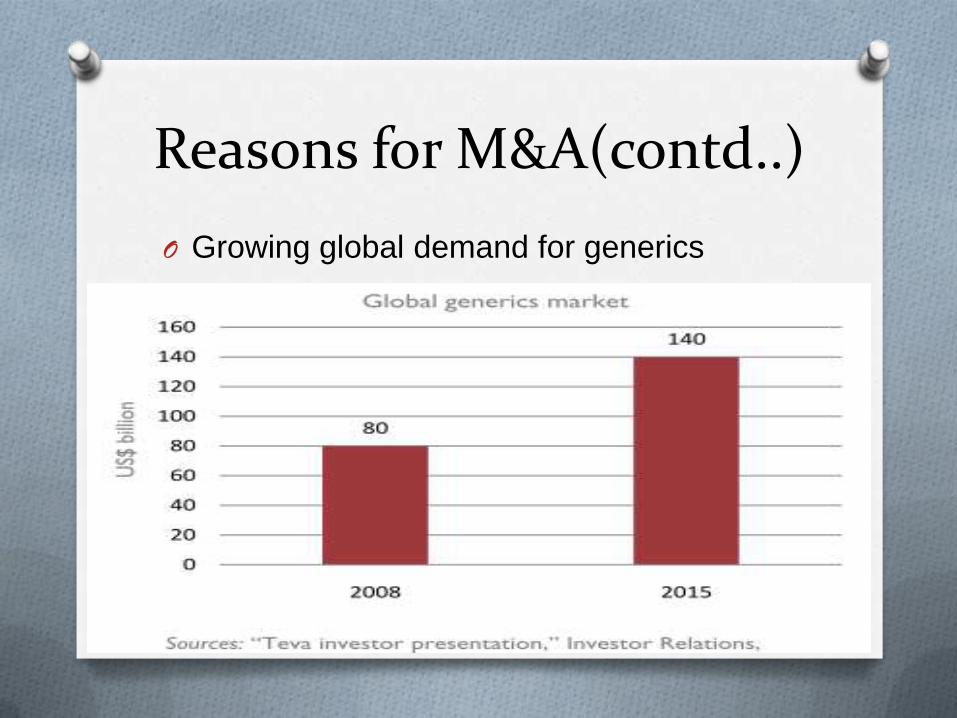

Reasons for M&A(contd..)

O Growing global demand for generics

M&A Deals

O M&A trend analysis:

2007 2008 2009 2010

Deal

volume

45 74 35 55

Deal

value($mn)

798.1 5,347.7 1,646.7 5,322.3

Source: Datamonitor

Recent M&A Deals(Inbound)

Date Target Acquirer Deal value($mn)

May 2010 Piramal Abbott 3,720

June 2008 Ranbaxy Daiichi Sankyo 4,538.6

Mar 2009 Matrix Mylan 736.0

Dec 2010 Paras Reckitt

Benckiser

720.9

July 2009 Shantha Sanofi Aventis 625.18

Dec 2009 Orchid Hospira 400.0

Apr 2008 Dabur Frenesius kabi 220.0

Source: Datamonitor

M&A by Indian companies

O Not a one way street

O Indian companies are not only looking to sell but they are also active buyers wherein they are looking to augment their capabilities by expanding their footprints, entering into new geographies or diversifying their business model or moving up the value chain

O Several cash rich domestic companies are looking at hitherto unexplored markets like Japan, Australia and East Asia

Drivers of acquisition by Indian companies

O Enhancing revenue through global presence

O Better market access

O Widening product portfolios

O Strengthening R&D capabilities

O Strengthening distribution network

O Increasing efficiencies through leveraging

economies of scale

O Gaining access to new technologies

O Establishing a new area in pharma value

chain

Some M&A Deals(Outbound)S. N. Company (Acquirer) Company (Target) For Amount

1 Biocon Axicorp (German) $ 30 million

2 Dr. Reddy's Labs Trigenesis Therapeutics (USA) $ 11 million

3 Wockhardt Esparma (German) $ 11million

4 Wockhardt C P Pharmaceuticals (UK) Rs 83 crore

5 Wockhardt Negma Laboratories (France) $ 265 million

6 Wockhardt Morton Grove Pharma (USA) $ 38 million

7 Zydus Cadilla Alpharma (France) EUR 5.5 million

8 Ranbaxy RPG Aventis (France) $ 70 million

9 Nicholas Piramal Biosyntech (Canada) $ 4.85mn

10 Sun Pharma Taro (Israel) $ 500mn

11 Cadilla Healthcare Quimica E Farmaceutica Nikkh -

The Big DealAbbott + Piramal

At $3.72 bn (Rs 17,500 crore), it’s the second largest

pharma deal in India, after the Rs 19,780 cr Daiichi-

Ranbaxy deal in 2008

What it means for Abbott?

• Rights to 350 brands and trademarks of

generics, including Phensedyl cough syrup

• Market share close to 7%

• Strong presence in India(growth rate 13-17%)

• Complete product portfolio

The Big DealAbbott + Piramal

O The Piramal group has agreed that for

eight years after the deal's closing, it will

not enter the business of generic

pharmaceutical products in India, or make

or market them in emerging markets

O Abbott became market leader with the

acquisition of Piramal with appox. 7%

market share

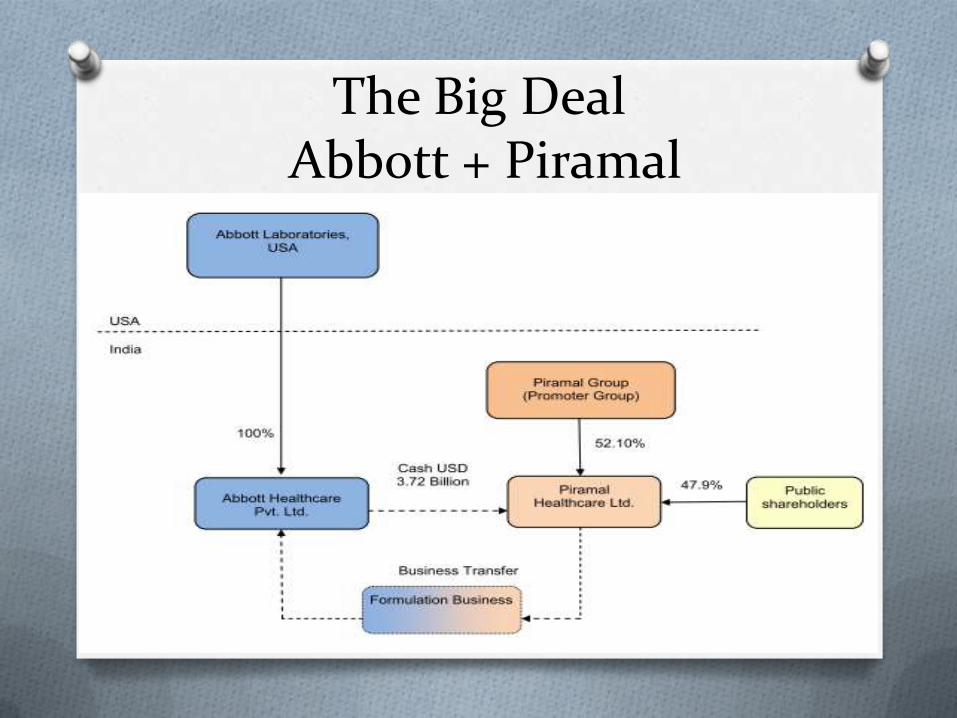

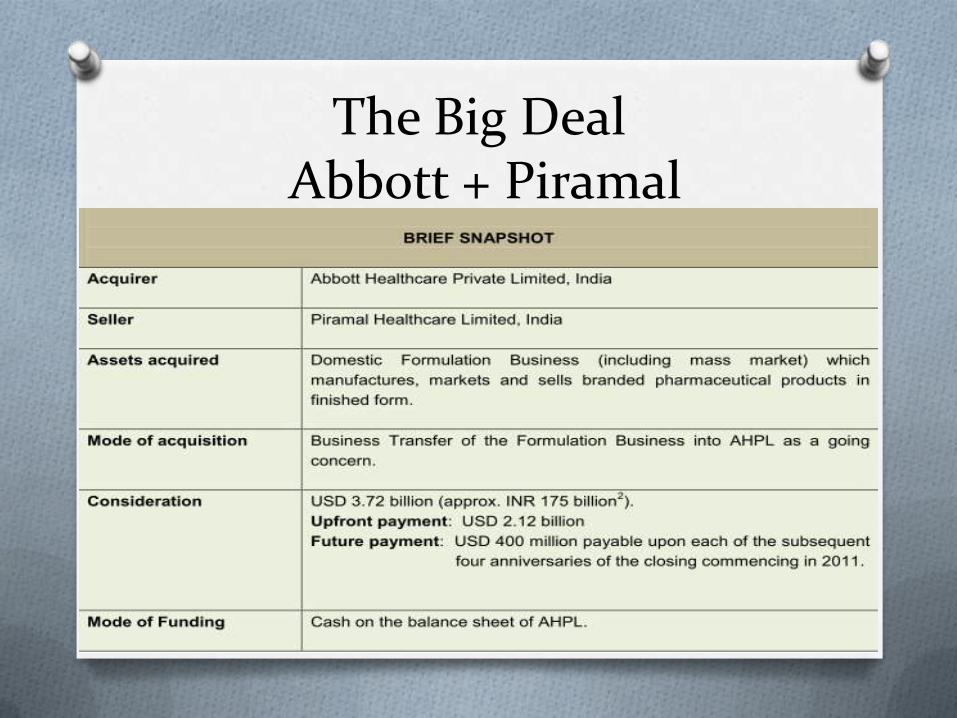

The Big DealAbbott + Piramal

The Big DealAbbott + Piramal

The Big DealAbbott + Piramal

O A leader in the Indian branded generics market

O Strong brand equity and presence in key areas: antibiotics, respiratory, cardiovascular, pain and neuroscience

O ~350 branded generic products

O Significant local footprint – largest sales force in India

O One of the largest formulation plants in India

Piramal Overview

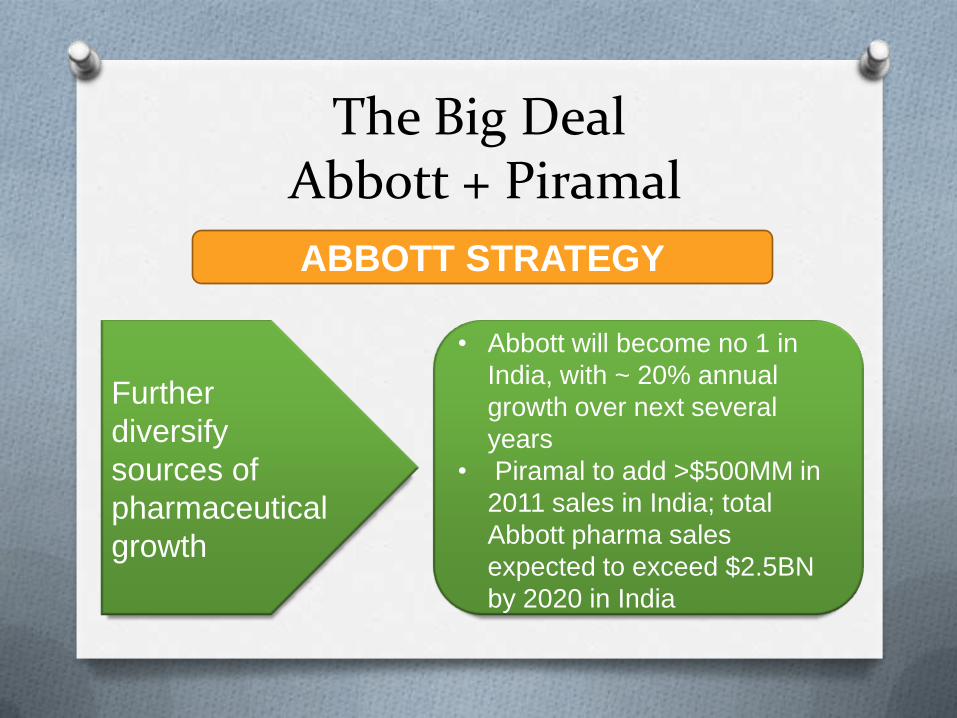

The Big DealAbbott + Piramal

ABBOTT STRATEGY

Further

diversify

sources of

pharmaceutical

growth

• Abbott will become no 1 in

India, with ~ 20% annual

growth over next several

years

• Piramal to add >$500MM in

2011 sales in India; total

Abbott pharma sales

expected to exceed $2.5BN

by 2020 in India

The Big DealAbbott + Piramal

ABBOTT STRATEGY

Expand

presence in

high-growth

emerging

markets

• India is one of the

world’s fastest-growing

markets; expected to

more than double by

2015

• Piramal has the largest

sales force in India;

unique model with

dedicated people in high-

growth rural areas

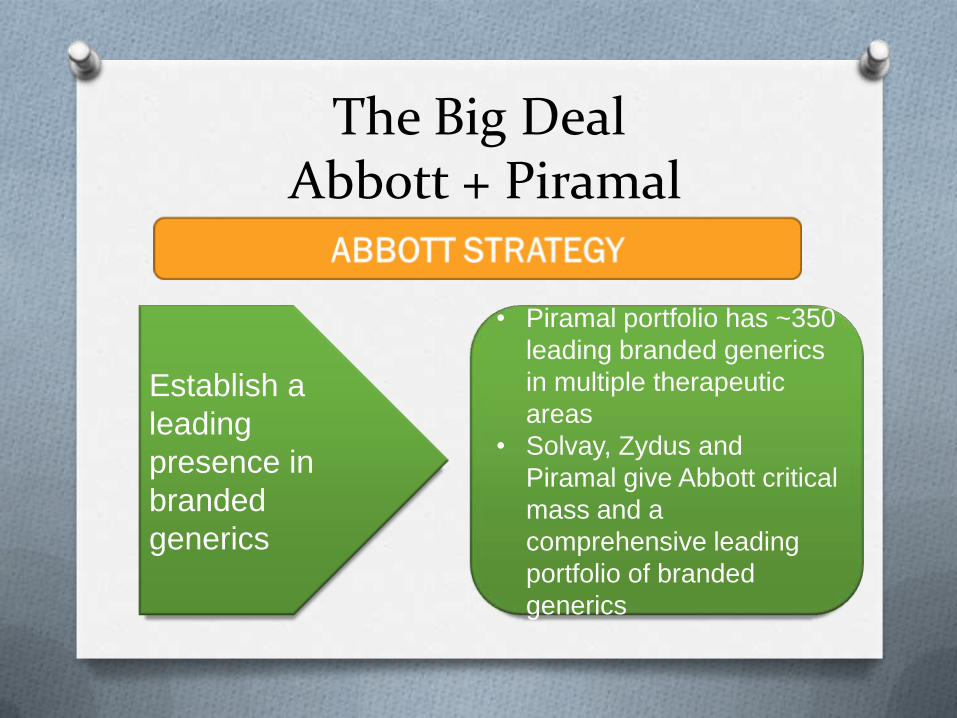

The Big DealAbbott + Piramal

Establish a

leading

presence in

branded

generics

• Piramal portfolio has ~350

leading branded generics

in multiple therapeutic

areas

• Solvay, Zydus and

Piramal give Abbott critical

mass and a

comprehensive leading

portfolio of branded

generics

The Big DealAbbott + Piramal

Deliver

sustained

double-digit

EPS growth

• Expect ~20% Piramal

sales growth over the

next five years

• Expect transaction to be

neutral to EPS over the

next several

years, accretive

thereafter

The Big DealAbbott + Piramal

“ Globally, there is a new way of selling

patented drugs, which we would not have

been able to do on our own. So as part of

future strategy, we took this decision.

Also, at almost 9.5 times the sales, its in the

best interest of our shareholders”

Ajay Piramal

Chairman, Piramal Group

Future

O India will break into top 5 pharma markets by 2020

O Increasing spending on healthcare will drive the MNCs to look for Indian presence

O Indian companies do not have the capital and expertise required for new drug development

O At the same time, from the standpoint of the MNCs, with the drying up of R&D productivity in the U.S. and developed markets and their search for other sources of innovation ,acquisitions are a cost-effective way to bring in a portfolio of branded generics

Future

O With the availability of 100 per cent FDI throughautomatic route, Indian companies may witnesstakeovers by foreign firms

O There has been a gradual shift in thinking of Indianpromoters who are now more open to exploringstrategic options for their companies which hasenabled increased M&A activity in this sector

O The new patent regime, challenges faced bygeneric companies in regulated markets and therobust valuation being offered by MNCs are someof the key factors which have resulted in thischanged mindset of both MNCs as well as Indianpromoters

Future

O These are interesting times for the Indian pharmaceuticals industry which offers diverse opportunities with substantial growth potential to both domestic as well as global pharma companies

O This will result in increased M&A activity in this sector as companies are prompted to evaluate their business models and re-align themselves to create value for their stakeholders