17

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016

METHODOLOGYGUIDEVALUINGMOTELSINONTARIO

ValuationDate:January1,2016

AUGUST2016

August22,2016

TheMunicipalPropertyAssessmentCorporation(MPAC)isresponsibleforaccuratelyassessingandclassifyingpropertyinOntarioforthepurposesofmunicipalandeducationtaxes.

InOntario’sassessmentsystem,MPACassessesyourpropertyvalueeveryfouryears.Thisyear,MPACisupdatingthevalueofeverypropertyintheprovincetoreflectthelegislatedvaluationdateofJanuary1,2016.

MPACiscommittedtoprovideOntariopropertyowners,municipalitiesandallitsstakeholderswiththebestpossibleservicethroughtransparency,predictabilityandaccuracyinvalues.Aspartofthiscommitment,MPAChasdefinedthreelevelsofdisclosureofinformationinsupportofitsdeliveryofthisyear’sassessmentupdate.ThisMethodologyGuideisthefirstlevelofinformationdisclosure.

ThisguideprovidesanoverviewofthevaluationmethodologyundertakenbyMPACwhenassessingmotelpropertiesforthisyear’supdateensuringthemethodologyforvaluingthesepropertiesiswelldocumentedandinalignmentwithindustrystandards.

Propertyownerscanaccessadditionalinformationabouttheirownpropertiesthroughaboutmyproperty.ca.Logininformationforaboutmyproperty.caisprovidedoneachPropertyAssessmentNoticemailedthisyear.AdditionalinformationaboutMPACcanbeaccessedatmpac.ca.

AntoniWisniowski

PresidentandChiefAdministrativeOfficer

RoseMcLean,M.I.M.A.

ChiefOperatingOfficer

TableofContents

1.0INTRODUCTION................................................................................................................4

1.1PROPERTIESCOVEREDBYTHISMETHODOLOGYGUIDE......................................................................4

1.2LEGISLATION.............................................................................................................................5

1.3CLASSIFICATION.........................................................................................................................5

1.4THEUSEOFTHISMETHODOLOGYGUIDE.......................................................................................6

1.5CONSULTATIONANDDISCLOSURE.................................................................................................6

2.0THEVALUATIONPROCESS.................................................................................................8

2.1OUTLINE..................................................................................................................................8

2.2APPROACH...............................................................................................................................9

2.3DATACOLLECTION.....................................................................................................................9

2.4DATAANALYSIS.......................................................................................................................11

2.5VALUATION............................................................................................................................12

2.6VALIDATINGTHERESULTS..........................................................................................................12

3.0THEVALUATION..............................................................................................................13

3.1DERIVINGTHEGIM.................................................................................................................13

3.2DATAQUALIFICATION...............................................................................................................13

3.3DATACLASSIFICATION..............................................................................................................14

3.4APPLYINGTHEGIMAPPROACH..................................................................................................14

3.5SAMPLEVALUATION.................................................................................................................16

3.6VERIFYINGTHERESULTS............................................................................................................17

3.7CONCLUSION..........................................................................................................................17

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 4

1.0Introduction

TheMunicipalPropertyAssessmentCorporation(MPAC)–mpac.ca–isresponsibleforaccuratelyassessingandclassifyingpropertyinOntarioforthepurposesofmunicipalandeducationtaxation.

InOntario,propertyassessmentsareupdatedonthebasisofafour-yearassessmentcycle.In2016,MPACwillupdatetheassessmentsofOntario’snearlyfivemillionpropertiestoreflectthelegislatedvaluationdateofJanuary1,2016.Assessmentsupdatedforthe2016baseyearareineffectforthe2017–2020propertytaxyears.

ThelastAssessmentUpdatewasbasedonaJanuary1,2012,valuationdate.Increasesbetweenthe2012assessedvalueandthe2016assessedvaluearephasedinoverafour-yearperiod.Anydecreasesinassessmentareappliedimmediately.

Itisimportanttoensurethatthevaluationmethodologyappliediscapableofprovidingarealisticestimateofcurrentvalueattherelevantvaluationdate,which,inturn,enablesallstakeholderstounderstandthevaluationprocessandhaveconfidenceinthefairnessandconsistencyofitsoutcome.

ThisMethodologyGuidehasbeenpreparedforthebenefitofMPACassessors,propertyownersandtheirrepresentatives,municipalitiesandtheirrepresentatives,AssessmentReviewBoardmembers,provincialofficials,andthegeneralpublic.

Thisguideoutlinesthevaluationprocesstobefollowedbyanassessor,includingstepsthatrequireappraisaljudgment.Itisincumbentupontheassessortomakeinformeddecisionsthroughoutthevaluationprocesswhenarrivingatestimatesincurrentvalue.

1.1PropertiesCoveredbyThisMethodologyGuide

Motelpropertiesvaryconsiderably.Theymayprovideshort-orlong-termlodging.Motelsareusuallylocatedwithgoodaccesstomajorroadnetworksandsituatednearhighwaysorontheoutskirtsofmajororsmallcities/towns.Theytypicallyhavefeweramenitiesthanhotels.

Motelstructuresaregenerallysingle-ortwo-storeybuildingswithconnectedrooms.Manyhaveopenwalkwaysandexteriorentrances.

ThefollowingMPACpropertycodesareusedtocategorizemotelsinOntario:

• 450Motel

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 5

1AssessmentAct,R.S.O1990,cA.31:https://www.ontario.ca/laws/statute/90a31.2OntarioRegulation282/98,GENERAL:https://www.ontario.ca/laws/regulation/980282.

• 451SeasonalMotel

Itshouldbenotedthatthesearegeneralguidelinesthatvarydependingonthespecificcircumstancesofaparticularproperty.

AnassessormayalsomakereferencetoadditionalMethodologyGuidesforpropertiesthatdonotfallpreciselywithinthedescriptionofoneofthepropertycodeslistedabove.

1.2Legislation

ThemainlegislationgoverningtheassessmentofpropertiesinOntarioforpropertytaxpurposesiscontainedintheAssessmentAct.1

TheActcontainsimportantdefinitionsandstatesthatallpropertyinOntarioisliabletoassessmentandtaxation,subjecttosomeexemptions.Section19(1)oftheActrequiresthatlandbeassessedatcurrentvalue,whichisdefinedtomean,inrelationtoland,“theamountofmoneythefeesimple,ifunencumbered,wouldrealizeifsoldatarm’slengthbyawillingsellertoawillingbuyer.”

TheMinisterofFinancefiledOntarioRegulation430/15onDecember18,2015,whichaddedadditionalrulesaffectingthevaluationandclassificationofpropertiesonwhichathird-partysign(billboard)islocated.Tocomplywiththeregulation,theincomeattributabletoathird-partysignwillnotbeincludedinthevaluationofanypropertyforassessmentpurposes.

1.3Classification

MPAC’sroleistoaccuratelyassessandclassifyallpropertiesinOntarioinaccordancewiththeAssessmentActanditsassociatedregulationsestablishedbytheGovernmentofOntario.Theclassificationofapropertywilldeterminewhichtaxratewillbeappliedbythemunicipalityortaxingauthority.Allpropertiesareclassifiedaccordingtotheiruse,andOntarioRegulation282/98oftheAssessmentActsetsouthowvariouspropertyusesareclassified.

MotelsareincludedinthecommercialpropertyclassinaccordancewithSection5(1)1ofOntarioRegulation282/98as“landandvacantlandthatisnotincludedinanyotherpropertyclass.”2

Mostmotelsalsocontainresidentiallivingquartersthataretypicallyoccupiedbytheowner/operator.TheseareasareclassifiedintheResidentialPropertyClassinaccordancewithSection3(1)1ofOntarioRegulation282/98.

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 6

Ifaportionofthepropertyisusedforotherpurposes,thetotalvalueofthepropertywillbeapportionedbetweenthevarioususestoensurethattheappropriatetaxrateisappliedtotherelevantpartsoftheproperty.

1.4TheUseofThisMethodologyGuide

ThisMethodologyGuideisintendedto:

• EnsureMPAC’sassessedvaluesforthesepropertiesarefair,accurate,predictable,andtransparent.

• Providedirectiontoassessorsandclearexplanationstomunicipalities,taxpayers,andAssessmentReviewBoardmembers.

• EnsurethatMPAC’smethodologyforvaluingthesepropertiesiswelldocumentedandalignswithindustrystandards.

• Explainthethoughtprocess/decision-makingprocessthatanassessorshouldundertaketoapplythevaluationmethodology.

• Ensureaconsistentapproachtovaluingthesepropertytypes.

• SupportMPACassessorsinconductingtheirduediligencein:

Ø applyingOntario’slegislationandregulationsØ adheringtoindustrystandardsformarketvaluationinamassappraisal

environment

ItshouldbenotedthatthisMethodologyGuideisnotintendedtobeasubstituteforanassessor’sjudgmentinarrivingatamarketvalue–basedassessment(i.e.,currentvalue)foraparticularproperty.However,giventhattheMethodologyGuideexplainsindustrystandardsforpropertyassessment,conformstovaluationindustrynorms,andadherestoprovinciallegislationandregulation,MPACassessorsareexpectedtofollowtheproceduresintheMethodologyGuideandbeabletoclearlyandsatisfactorilyjustifyanydeviationsfromit.

1.5ConsultationandDisclosure

MPACiscommittedtoprovidingmunicipalities,taxpayersandallitsstakeholderswiththebestpossibleservicethroughtransparency,predictabilityandaccuracy.Insupportofthiscommitment,MPAChasdefinedthreelevelsofdisclosureaspartofitsdeliveryofthe2016province-wideAssessmentUpdate:

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 7

• Level1–MethodologyGuidesexplaininghowMPACapproachedthevaluationofparticulartypesofproperty

• Level2–MarketValuationReportsexplaininghowthemethodologyoutlinedinLevel1hasbeenappliedatthesectorlevelforthepurposesofeachassessment

• Level3–PropertySpecificValuationInformationavailabletopropertytaxpayers,theirrepresentativesandmunicipalities

Residentialpropertyownerscanaccessdetailedinformationabouttheirassessmentthroughaboutmyproperty.ca.Logininformationisprovidedonevery2016PropertyAssessmentNoticemailed.

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 8

2.0TheValuationProcess

Thevaluationprocessalwaysbeginswithadeterminationofthehighestandbestuseofthesubjectproperty.

Anyrelianceuponthisguideismadeonlyaftertheassessorhasdeterminedthatthehighestandbestuseofthesubjectpropertyisthatofamotel.

Assessorsdeterminethevalueofapropertyusingoneofthreedifferentapproachestovalue:

• thedirect(sales)comparisonapproach

• theincomeapproach

• thecostapproach

2.1Outline

Inthedirect(sales)comparisonapproach,valueisindicatedbyrecentsalesofcomparablepropertiesinthemarket.Inconsideringanysalesevidence,itiscriticaltoensurethatthepropertysoldhasasimilaroridenticalhighestandbestuseasthepropertytobevalued.

Intheincomeapproach(or,moreaccurately,theincomecapitalizationapproach),valueisindicatedbyaproperty’srevenue-earningpower,basedonthecapitalizationofincome.Thismethodrequiresadetailedanalysisofbothincomeandexpenditure,bothforthepropertybeingvaluedandothersimilarpropertiesthatmayhavebeensold,inordertoascertaintheanticipatedrevenueandexpenses,alongwiththerelevantcapitalizationrate.

MotelvaluationemploysasimplifiedversionoftheincomeapproachasaGIM(grossincomemultiplier)isusedtoestablishtherelationshipbetweengrossincomeandvalue.TheGIMisderivedfromadetailedanalysisforsimilarpropertiesthathavebeensold.

Inthecostapproach,valueisestimatedasthecurrentcostofreproducingorreplacingtheimprovementsoftheland(includingbuildings,structuresandothertaxablecomponents),lessanylossinvalueresultingfromdepreciation.Themarketvalueofthelandisthenadded.

MPACusestheincomeapproachtovaluemotels.Forthistypeofproperty,thegrossincomemultiplier(GIM)methodoftheincomeapproachisused.Thefollowingstepsarefollowed:

1) Collectincome,expenseandotherappropriateinformationfrommotelmanagementandothersources.

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 9

2) Analyzethedataandestablishindustrynorms–grossincome,occupancy,expenseratios,etc.,formotelsaccountingforsize,age,qualityandlocation.

3) Analyzeincomeandexpensedata,andstabilizedatatoreflecttypicalthree-yearperformance.

4) CompareactualincomeandexpenseswithsimilarmotelsineachlocalityinOntario.

5) Establishgrossincomemultipliers(GIM)fromthesalesdata.

6) CalculatethemotelvaluebymultiplyingthestabilizedgrossannualincomebytheGIM.

7) Deductpersonalpropertyallowance.

8) Calculatethecurrentvalueofrealestatebysubtractingthepersonalpropertyallowancefromthemotelvalue.

9) Addvalueofothercomponentslocatedontheproperty(residentiallivingquarters,excesslands)toproducethecurrentvalueoftheproperty.

10) Reviewtheoutcometoverifyaccuracy.

2.2Approach

TherearethreemainphasesintheprocessusedbyMPAC:

• datacollection

• analysisofthedatacollected

• valuation

2.3DataCollection

ApplicationoftheGIMrequiresthecollectionoffinancialandgeneraldata,including:

GeneralMotelData

• inspecting,measuringandquantifyingmotelimprovements

• identifyingimprovementagesandfunctions

• collectingdatafornumbersofroomsandamenities,carparking,etc.

• obtainingbuildingandsiteimprovementplansforthesubjectproperty

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 10

MotelFinancialData

• collectingincomeandexpensestatementsrelatingtothemotelforatleastthreeyears

• examiningincomeandexpensestatementstoconfirmthattheyaretypicalandreflectiveofthemarketplace

• tabulatingmotelrevenuesandotherincomevaluationparameters

InformationfromOwners

Theowneroroperatoristhemainsourceoffinancialdatarelatingtothemotel.AlthoughthedatarequestedbyMPACmayvarydependinguponthetypeofmotelconcernedandtheamenitiesprovided,itmayincludethefollowing:

• occupancylevels

• averageroomrate

• otherincome(mini-bar,catering,conferenceroomrentals,movies,etc.)

• operatingexpensesforthemotel

• otheroperatingexpensesbrokendownbytypeofexpense

• managementcontractdetails

• recordofexpendituresonFF&E

• recordofcapitalexpenditures

MPACalsorequestsdataonmotelsales.Thedatarequestedrelatestothesaleprice,grossincomeandotherrelevantinformationhelpfulinidentifyingwhichsalesareopenmarkettransactions,thecircumstancesofeachtransactionandthemotivationoftheparties.

Eachsaleisinvestigatedandwhereallrelevantinformationiscollected,aGIMiscalculated.SalesdataiscompiledandananalysisisconductedtodetermineGIMrangesforpropertiesbasedonsize,age,type,locationandquality.TheseGIMscanthenbeappliedtosimilarpropertiesthathavenotsold.

SaleswhereGIMscannotbecalculatedarenotincludedintheGIMstudybutarenotdiscardedastheymaystilloffersomevaluablemetricssuchassalepriceperroom.

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 11

Confidentiality

Asoutlinedabove,itisimportanttobeawarethat,inordertoenableMPACtoproduceanaccuratevaluationofthepropertyconcerned,informationneedstobeobtainedfromavarietyofsources.

ThiswillincludeinformationfromMPAC’srecords,fromtheowneroroperatoroftheproperty,fromthemunicipalityinwhichthepropertyislocated,fromtheassessor’svisittotheproperty,andfromothersources.

AllstakeholdersinthepropertytaxsystemhaveaninterestinensuringthatthecurrentvalueprovidedbyMPACiscorrect;inordertoachievethis,itisnecessaryforallpartiestocooperateintheprovisionofinformation.

Itisappreciatedthatsomeoftheinformationoutlinedabovemaybeofacommerciallysensitivenature.MPACrecognizestheneedtoensurethatanyinformationprovidedtoitisproperlysafeguardedandonlyusedforthepurposeforwhichitissupplied.Assessorsmustappreciatethenatureofthisundertakingandensuredataistreatedaccordingly.

If,afteranappealhasbeenfiled,MPACreceivesarequestforthereleaseofactualincomeandexpenseinformation,orothersensitivecommercialproprietaryinformation,theusualpracticeistorequirethepersonseekingtheinformationtobringamotionbeforetheAssessmentReviewBoard(ARB),withnoticetothethirdparties,requestingthattheARBorderproductionoftherequestedinformation.ThereleaseofsuchinformationisatthediscretionoftheARBandcommonlyaccompaniedbyarequirementforconfidentiality.

TheAssessmentActoutlinesinSection53(2)thatdisclosedinformationmaybereleasedinlimitedcircumstances“(a)totheassessmentcorporationoranyauthorizedemployeeofthecorporation;or(b)byanypersonbeingexaminedasawitnessinanassessmentappealorinaproceedingincourtinvolvinganassessmentmatter.”

2.4DataAnalysis

Theanalysisprocessinvolvesseveralsteps:

1) Thefirsttaskistoqualifythedatabeforeitisusedtoestablishtheratesandfactorsthatwillbeusedtovaluetheproperties.

2) Next,thedataisclassifiedsothatitcanbesortedintoappropriategroups,whichreflectconditionswheredatacomparisonscanbemadeandconclusionsdrawn.

3) Finally,thespecificindividualvaluationparametersaredeveloped.

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 12

2.5Valuation

Havingundertakenthenecessarystepsoutlinedabove,theassessorshouldnowbeinapositiontoapplytheappropriatevaluationmodel.

2.6ValidatingtheResults

Oncetheassessorhascompletedthevaluation,itisnecessarytocarryoutaseriesofcheckstoensurethatallrelevantpartsofthepropertyhavebeenincludedinthevaluation,therehasbeennodouble-countingofanyadjustmentsmadefordepreciation,theresultingvaluationhasbeencomparedwithanymarketevidencethatmaybeavailableinrelationtosimilarpropertiesandthefinalvaluationisinlinewiththevaluationofothersimilarpropertiesinOntario.

3.0 The Valuation

3.1 Deriving the GIM

This method calculates an estimated stable gross income that can be generated by the motel by reference to market rates, then applies the GIM to arrive at a current value for the property.

GIMs and market rates are derived from information obtained from sales of motels and from annual operating statements and rent rolls reported by motel owners.

In simple terms, the formula for deriving the GIM is as follows:

GIM = Sale Price / Gross Annual Income

For example, if a motel that has revenues of $150,000 sold for $600,000, the GIM calculation would be as follows:

GIM = $600,000 / $150,000

In this example, GIM = 4.

This GIM could then be used in the valuation of other similar motels where the gross annual income has been calculated.

However, the actual gross income may require some adjustments before it can be used in a GIM calculation. The income needs to be stabilized, which requires that the revenues used in the val-uation exclude any abnormal change in supply and demand, plus any temporary or infrequent conditions that may result in unusual levels of revenues or expenses to the property.

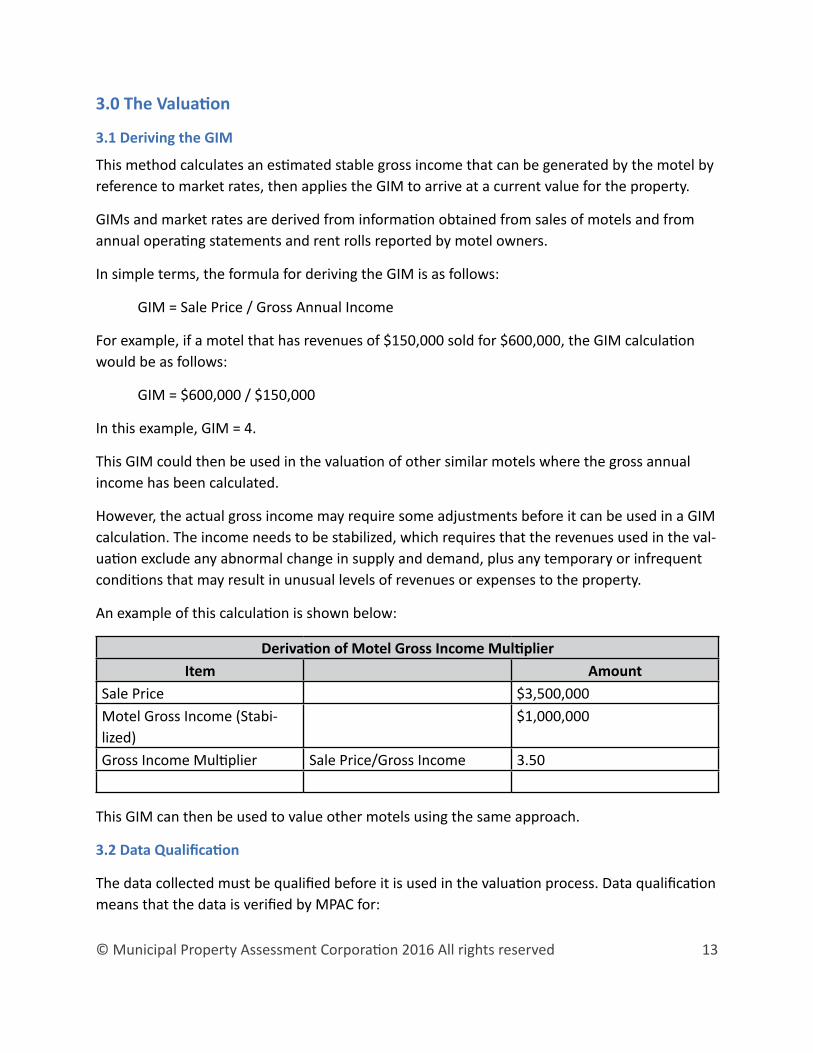

An example of this calculation is shown below:

Derivation of Motel Gross Income MultiplierItem Amount

Sale Price $3,500,000Motel Gross Income (Stabi-lized)

$1,000,000

Gross Income Multiplier Sale Price/Gross Income 3.50

This GIM can then be used to value other motels using the same approach.

3.2 Data Qualification

The data collected must be qualified before it is used in the valuation process. Data qualification means that the data is verified by MPAC for:

© Municipal Property Assessment Corporation 2016 All rights reserved 13

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 14

• Accuracy–Istheinformationcorrect,orhaveanyerrorsbeenmadeinreportingorrecordingit?

• Timeliness–Doesitreflectthetimeperiodbeinganalyzed?

• Appropriateness–Isthedatarepresentativeofthetypeofmotelbeinganalyzed?

Thedataforanindividualmotelwillbecomparedtothedataobtainedfromsimilarmotelstocheckthatitproperlyreflectsindustrynorms.Thisprocessisimportanttoensurethatthereisanequitableassessmentbaseestablishedforthevaluationofallmotels.

TheincomeandotherfinancialdatawillalsobestabilizedbyMPAC,meaningthatitshouldrepresentthetypicalperformancethatcanbeexpectedforanygivenyear.Stabilizingthedataalsomeansthatexceptionalincomeorexpensesinaparticularyearwillbesmoothedouttopreventdistortion.

3.3DataClassification

Motelsrangefromsmallmotelswithfewornoservicestolarge,full-serviceluxuryresortmotels.Therangeofservicesandfacilitiesprovidedinamotel,suchasmeetingrooms,swimmingpools,exercisefacilities,restaurants,conveniencestores,etc.,willaffectthepotentialrevenuesandthecostsofoperatingtheproperty.

Inadditiontothecostsofoperation,theexpertisedemandedofmanagementwillalsovarywiththesizeandcomplexityoftheproperty.Thedifferencesinrevenuesandexpensesassociatedwiththevarioustypesandsizesofmotels,alsoproducesadifferenceinthedegreeofriskassociatedwiththeseproperties.

Forthesereasons,itisimportanttoensurethatonlydataappropriatetotheparticulartypeofmotelconcernedisusedinthevaluationprocess.

BecauseMPACusesaGIMapproach,theincomeusedisnotadjustedforvacanciesorforoperatingexpenses.VariationsinthesefeaturesarereflectedintheuseofaGIM,whichreflectsatypicalsituationsinvacancyandexpenselevels.

3.4ApplyingtheGIMApproach

Havingundertakenadetailedanalysisofthefinancialperformanceofmotels,andtheavailablesalesdata,MPACcanproceedtovalueallmotelsusingtheGIMmethod.

MPAC’sanalysisofactualmarketsales,andthegrossincomeofthemotelsthathavesold,demonstratestheGIMforeachtransaction.Foreachsale,thegrossincome(andthereforethe

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 15

GIM)willvarydependinguponanumberoffactors,includingthesize,design,age,locationandqualityofthemotel.

Whenvaluinganactualmotel,MPACwilluseaGIMappropriatefortheparticularmotelbeingvalued.TheGIMappropriateforthepropertywillalsodependuponawiderangeoffactors(i.e.size,design,age,locationandquality).TheGIMusedwillbeconsideredinlightofacomparisonoftheactualmoteltotheaverageortypicalmotelinthelocality.

Asalreadyindicated,thevalueofamotelrelatestoitsstabilizedactualandpotentialperformance.

Whiletherearemanymotelsofasimilarnature,theywillhavedifferentlocationsandoftenhavedifferentattributes,roommix,roomfinishes,restaurants,franchiseaffiliations,labourarrangements,marketfocus,etc.Therefore,inthevaluationprocess,actualincomeformsthestartingpointintheprocess.Thisdatawillthenbecomparedandtestedtotheperformanceofothermotelsandadjustedasappropriateinordertoestablishtheassessmentvalue.

Thesevaluationparameterscanthenbecomparedtopublishedindustrydataandfine-tunedtoestablishtheindustrynormsorexpectedperformancelevelsforaparticularmotel.

SourcesofRevenue

Motelshaveanumberofsourcesofrevenue(forexample,rooms,bars,restaurants,leisurefacilities,etc.),whichgenerateincomeandsupportthevalueoftheentiremotelenterprise.Thisincomearisesasaresultofbothtangibleassets,suchasland,buildingsandpersonalproperty,andintangibleassets,suchasthebrandandthequalityofmotelmanagement.

Thevaluationofamotelforpropertytaxpurposesrequiresthattherealestateportionbeseparatedfromthevalueoftheothercomponentparts,asonlytherealestateissubjecttopropertytax.

Furniture,FixturesandEquipment(FF&E)

PartoftherevenuegeneratedinamotelisattributabletoFF&E.AsFF&Earepersonalpropertyandnon-assessable,thevalueattributabletoFF&Emustbedeductedfromthefinalvaluegeneratedbythegrossincomeanalysis.Section45.3(2)ofOntarioRegulation282/98,statesthatunlesstheassessmentcorporationcandemonstratethattheuseofadifferentpercentageisappropriate,theamountdeductibleinrespectofpersonalpropertyshallnotexceed15percent.

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 16

AdditionsforSecondaryComponentsNotIncludedintheGIM

Inmostcases,motelpropertiestendtoalsocontainresidentiallivingquartersfortheowner/operatorortheremaybesurpluslandaspartoftheproperty,which,foravarietyofreasons(e.g.,marketconditions)maybeundeveloped.Thesesecondarycomponentsmustbevaluedseparatelyandaddedtothecurrentvalueoftheproperty.

Thedeterminationofexcesslandinvolvesareviewofcurrentzoningby-lawsaswellasthecurrentdensityandconfigurationoftheproperty.Excesslandvalueistypicallyderivedusingmarketsalesstudies.

CurrentValue

OncetheassessorhasdeductedtheestimatedvalueofthepersonalpropertyfromtheadjustedgrossincomemultipliedbytheGIM,theremainingvalueisthecurrentvalueofthemotel.

Therefore:

(AdjustedGrossIncomeXGIM)–PersonalProperty=ValueoftheMotel

And:

ValueoftheMotel+ValuesofAnyAdditionalComponentstotheProperty=

CurrentValueforPropertyTaxPurposes

Asamplevaluationisprovidedinthenextsection.

3.5SampleValuation

StabilizedAdjustedGrossIncome $500,000

AppropriateGrossIncomeMultiplier 5.5

IndicatedValue $2,750,000

PersonalProperty –$412,500

MotelCurrentValue $2,337,500

Valueofadditionalpropertycomponents $200,000

TotalPropertyValue $2,537,500

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 17

3.6VerifyingtheResults

HavingcompletedthevaluationusingtheGIMapproach,MPAC’sassessorwillreviewtheoutcometoensurethatitisanaccurateassessmentofthecurrentvalueofthepropertyandisinlinewiththeassessmentofothersimilarmotels.

3.7Conclusion

ThisguidesetsouthowMPACassessorsapproachthevaluationofmotelsforpropertyassessmentpurposes.

Althoughitoutlinesthegeneralapproachadopted,itdoesnotreplacetheassessor’sjudgmentandtheremaybesomecaseswheretheassessoradoptsadifferentapproachforjustifiablereasons.

ForfurtherinformationaboutMPAC’srole,pleasevisitmpac.ca.

![Hotels and Motels[1]](https://static.documents.pub/doc/80x56/548015615906b5f9288b46a5/hotels-and-motels1.jpg)